Netherlands Heat Pump Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

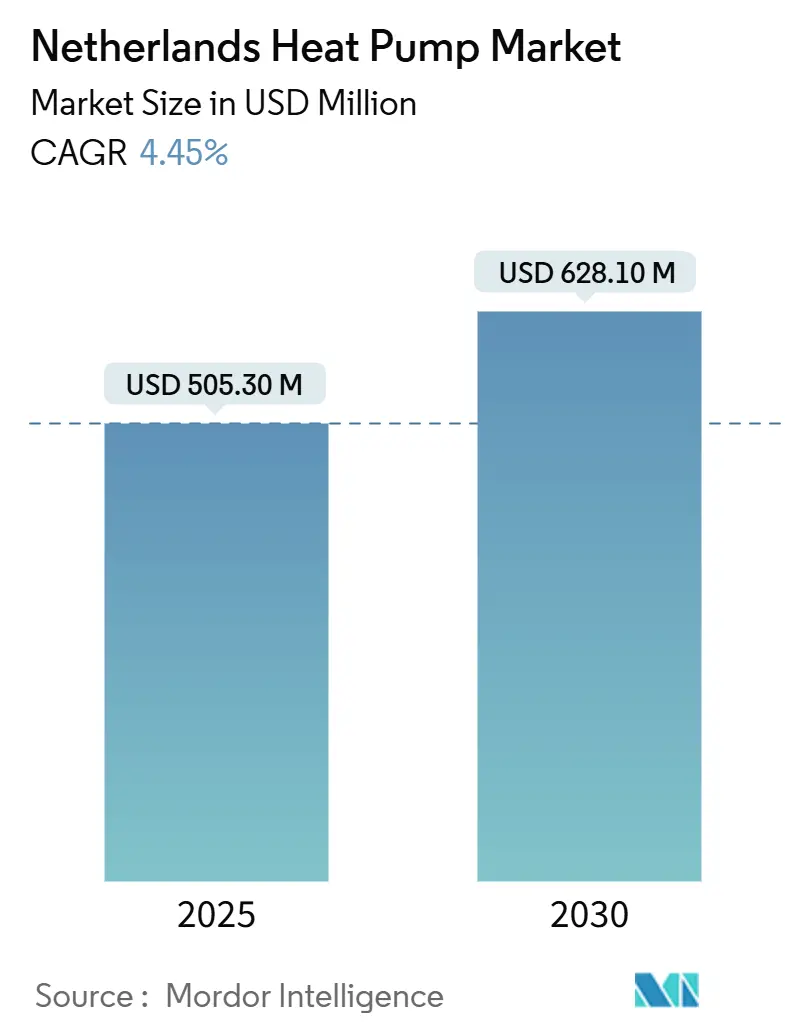

| Market Size (2025) | USD 505.30 Million |

| Market Size (2030) | USD 628.10 Million |

| Growth Rate (2025 - 2030) | 4.45% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Heat Pump Market Analysis by Mordor Intelligence

The Netherlands heat pump market size generated USD 505.3 million in 2025 and is forecast to expand to USD 628.1 million in 2030, reflecting a 4.45% CAGR over 2025-2030. Growth moderates in the near term as policy reversals, lower natural-gas prices, and subsidy adjustments temper demand, yet long-range prospects remain anchored in the country’s legally binding plan to phase out fossil-fuel space heating. Air-source units remain indispensable because they retrofit easily into the nation’s prevalent row houses, while aquathermal and ground-source solutions gain traction through district projects that deliver higher system efficiencies. Grid congestion continues to influence installation pacing and system design, spurring uptake of smart energy-management platforms and hybrid configurations that flatten peak-load profiles. Meanwhile, industrial decarbonization targets under EU ETS Phase 4 open a parallel growth track for large-capacity heat pumps, diversifying revenue streams and partially insulating suppliers from residential cyclicality. [1]Dutch Local Energy Transition Multi Level Instruments and Perspectives,” Netherlands Enterprise Agency, May 7, 2025, iea.blob.core.windows.net.

Key Report Takeaways

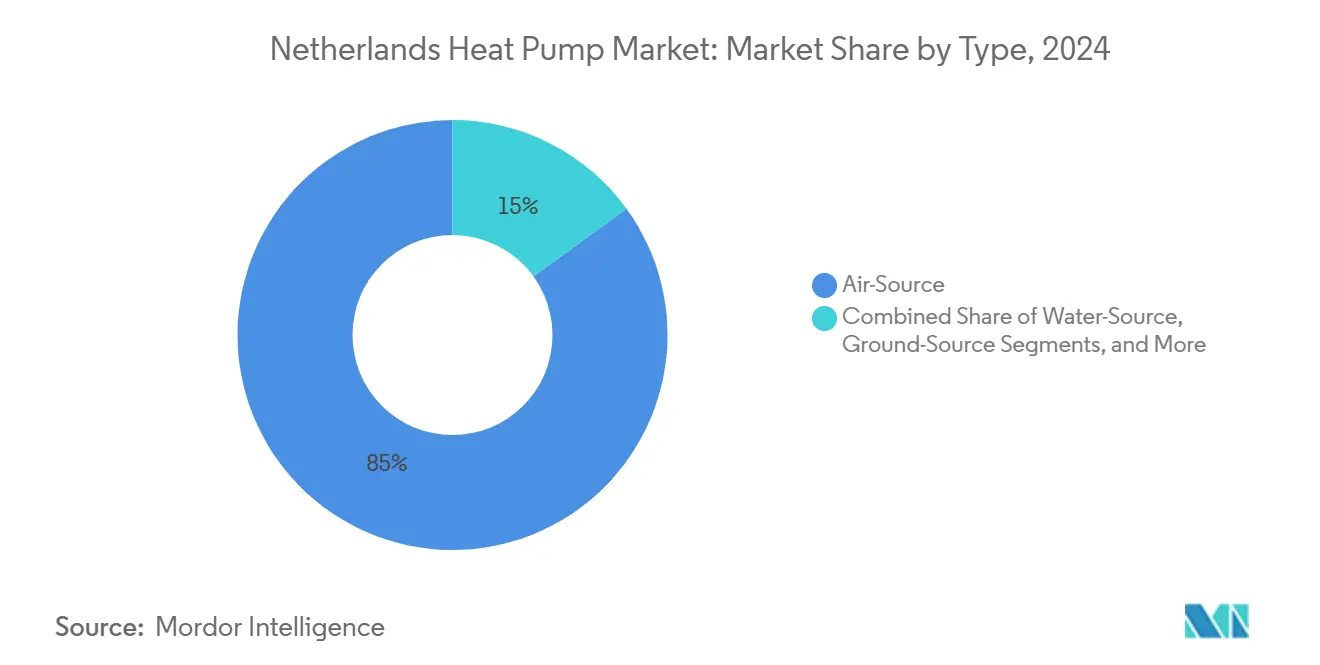

- By type, air-source units led with 85% revenue share in 2024; ground-source systems are projected to post the fastest 6.3% CAGR through 2030

- By rated capacity, the less than 10 kW segment held 56% of the Netherlands heat pump market share in 2024, while the above 100 kW band is poised for a 6.2% CAGR to 2030

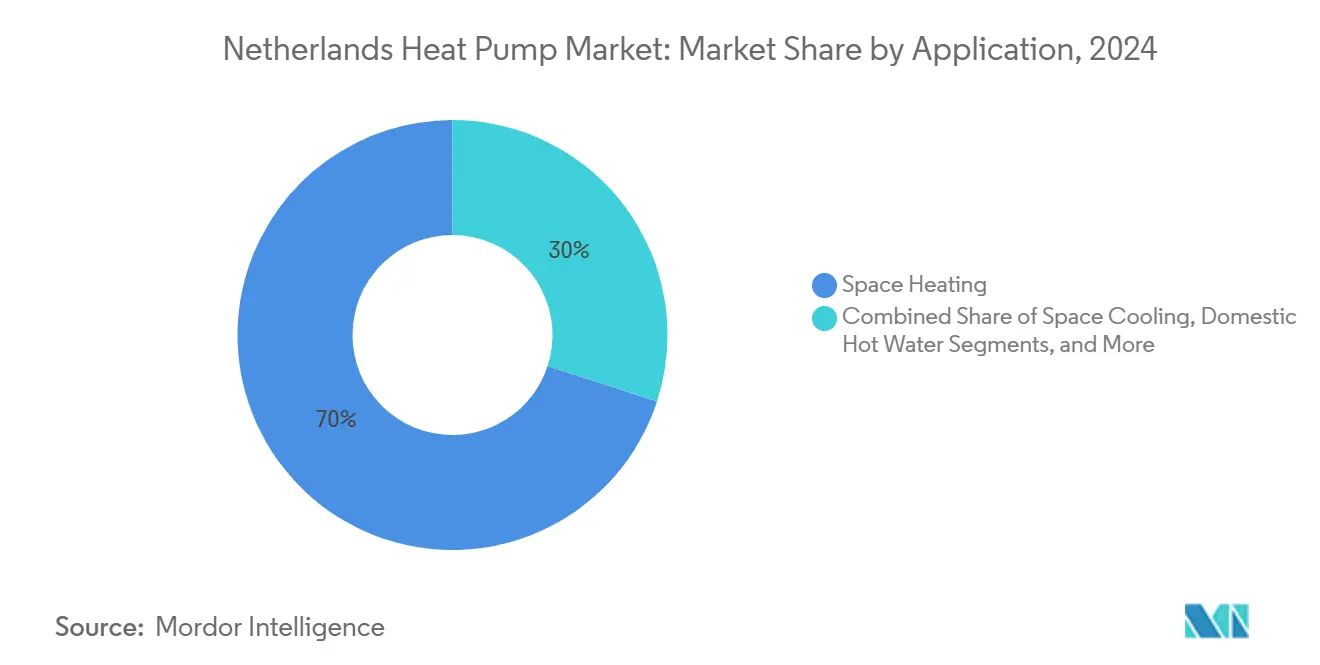

- By application, space heating accounted for 70% of the Netherlands heat pump market size in 2024 and is advancing at a 6.1% CAGR through 2030

- By end-user vertical, residential dominated with 60% revenue share in 2024; industrial installations are forecast to climb at a 6% CAGR

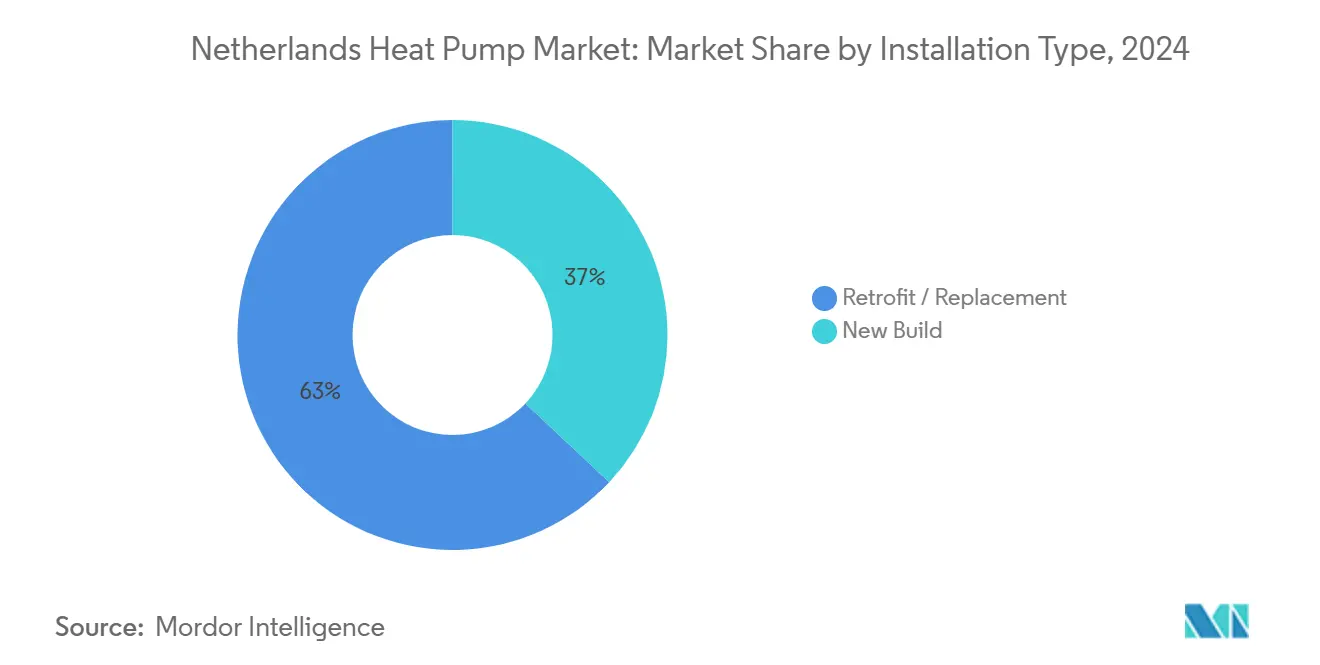

- By installation type, retrofits captured 63% of 2024 revenue; new-build deployments are projected to expand at a 5.9% CAGR

- By sales channel, installer networks controlled 70% of 2024 revenue, yet e-commerce is forecast for a 5.8% CAGR over 2025–2030

Netherlands Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supportive regulations and incentives | +1.5% | National – urban focus | Medium term (2–4 years) |

| Rising demand for energy-efficient heat pump systems | +1.2% | Commercial districts | Long term (≥ 4 years) |

| Phasing-out of natural gas | +2.1% | Major cities | Long term (≥ 4 years) |

| Integration with aquathermal networks | +0.8% | Coastal/waterway zones | Medium term (2–4 years) |

| Heat-as-a-Service models | +0.6% | Amsterdam, Utrecht | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supportive Government Regulations and Incentives

The ISDE programme allocated EUR 735 million (USD 794 million) in 2024, offsetting roughly 30% of residential installation costs. Yet July 2024 policy reversals on the hybrid mandate injected uncertainty that rippled through order pipelines, prompting developers in Utrecht to re-specify mixed systems that can flex with future rules. Subsidy timing now ranks alongside hardware efficiency in purchasing decisions, compelling manufacturers to refine product portfolios rapidly. Refrigerant regulations also drive re-engineering toward propane-charged units, absorbing margin to sustain sales momentum.

Rising Demand for Energy-Efficient Heat Pump Systems

The demand for energy-efficient heat pumps is surging, driven by heightened climate change awareness, government incentives, and cost-effectiveness. As a sustainable alternative to conventional cooling and heating systems, heat pumps are poised for significant adoption growth in the coming years. With rising consumer awareness and bolstered by government policies, the push for energy-efficient systems intensifies. In response, manufacturers are enhancing heat pump efficiency to align with rigorous energy standards. These optimizations not only conserve energy and lower utility bills but also diminish environmental repercussions.

Phasing-out of Natural Gas in Dutch Heating

Government targets call for 1.5 million homes converted by 2030 and universal fossil-free heating by 2050. A recent Amsterdam multi-family retrofit used distributed heat pumps to lower resident heating bills 40% and eliminate direct gas dependency. Material-price swings, copper in particular, have pressed engineers to substitute alternative piping, underscoring how supply-chain dynamics steer technological choices during the transition.

Integration with Aquathermal District Networks

In the Netherlands, aquathermal energy, harvesting heat from surface water, wastewater, and even drinking water, is carving out a niche in the nation's heat pump landscape, thanks to its vast water infrastructure. The Hague's 2023-adopted Heat Transition Vision spotlights aquathermal district heating networks as a pivotal solution for its urban centers, where space constraints hinder the installation of heat pumps. These networks harness large-scale heat pumps to draw low-temperature heat from water sources, channeling it through district systems. This approach reaps economies of scale that individual setups can't match. Backing this initiative, the Netherlands Enterprise Agency is championing pilot projects that meld heat pumps with aquathermal sources.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory compliance and safety standards | –0.8% | Dense urban zones | Medium term (2–4 years) |

| Skilled-labor shortage | –1.2% | Rural areas | Short term (≤ 2 years) |

| Grid congestion | –1.3% | Amsterdam, Rotterdam, Utrecht | Medium term (2–4 years) |

| Competition from hydrogen boilers | –0.5% | Pilot industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Compliance and Safety Standards

Noise limits of 40–45 dB(A) at property lines add EUR 2,500 (USD 2,700) per urban installation for acoustic mitigation. Parallel F-gas rules accelerate the pivot to natural refrigerants, extending R&D cycles and raising certification costs. Smaller vendors struggle to absorb these burdens, heightening entry barriers and nudging the Netherlands heat pump market toward higher consolidation.

Shortage of Skilled Labor

Nearly 2,000 consumer complaints surfaced in 2024 over installer availability. Wage inflation for certified technicians pushes up full-system costs and elongates payback periods, dampening uptake especially in price-sensitive segments. Fast-track training and modular plug-and-play designs are expanding, yet capacity constraints remain binding through 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Air-Source Dominates While Geothermal Accelerates

Air-source units accounted for 85% of the Netherlands heat pump market in 2024. Their price advantage and compact footprint align well with terraced homes, and subsidy structures historically favored these models. The Netherlands heat pump market size attributed to ground-source systems is smaller today, yet this segment is projected for 6.3% CAGR, powered by aquathermal-linked districts and EPC ‘A’ rules for new construction.

Seasonal performance factors above 5.0 for ground-source versus 3.0–4.0 for air-source. University pilots in Leiden, which achieved 80% CO₂ cuts, validate the efficiency story, although higher drilling costs and installer scarcity curtail the speed of adoption. Noise-free PVT panel integrations illustrate how innovation addresses urban space and regulatory constraints, supporting broader diffusion across the Netherlands' heat pump market.

By Rated Capacity: Small Units Lead, Industrial Scale Growing

Units below 10 kW captured 56% of Netherlands heat pump market revenue in 2024, reflecting the dominance of compact residences. Utility-bundled offers further streamline purchasing, sustaining high run-rates despite subsidy volatility. The 10–20 kW band follows for larger homes and small offices, while > 100 kW installations, though niche, are forecast to rise 6.2% annually.

Industrial electrification policies and greenhouse clusters underpin demand for high-capacity equipment, diversifying the Netherlands heat pump market. A Friesland dairy plant’s 250 kW system that slashed gas use 60% exemplifies payback potential, even after control-component shortages forced design revisions. Such proof points encourage capital-intensive sectors to reassess end-of-life boiler decisions.

By Application: Space Heating Expands Beyond Traditional Boundaries

Space heating represented 70% of Netherlands heat pump market revenue in 2024, following the 2026 ban on standalone gas boilers. Reversible systems now bundle cooling capability, elevating summer comfort appeal as heat waves become more common. Domestic hot-water heat pumps lag in share but advance steadily as part of integrated packages.

Process heating and cooling forms the fastest-growing niche at a 6.1% CAGR, catalyzed by VEKI (Accelerated Climate Investments Industry, a subsidy program) incentives tied to CO2 abatement. Pharmaceutical and food-processing pilots showcasing 40% energy savings and 70% emission cuts provide high-visibility evidence to boardrooms, reinforcing the Netherlands heat pump market trajectory in the industrial arena.

By End-User Vertical: Residential Base, Industrial Growth

Residential customers delivered 60% of 2024 revenue, buoyed by Heat-as-a-Service contracts that remove upfront cost barriers and boost EPC ratings. Commercial premises rank second but face split-incentive challenges between landlords and tenants. The industrial vertical is primed for a 6% CAGR on the back of EU ETS levies and maturing high-temperature technologies, expanding the Netherlands heat pump industry footprint.

Institutional buyers, municipalities, hospitals, schools, are fast-tracking bulk procurement within climate plans, bringing visibility to order books and encouraging local assembly investments. Cross-vertical synergies, such as shared service agreements for maintenance, enhance economics and smooth adoption curves.

By Installation Type: Retrofits Lead, New Builds Accelerating

Retrofit projects held 63% of share in 2024, given the urgency to decarbonize 2.4 million existing homes. Space limits, electrical upgrades, and acoustic compliance complicate these jobs, extending cycle-times relative to new builds. Nevertheless, retrofit-focused innovations such as hybrid all-in-one units that cut install labor 30% support continued volume.

New construction installations, though 37%, grow 5.9% annually on Nearly-Zero Energy Building codes that prescribe low-carbon systems from design stage. Developers integrate ground-source loops or central aquathermal plants to secure EPC ‘A’ ratings and comply with lending criteria that prefer green assets, cementing future share gains within the Netherlands heat pump market.

By Sales Channel: Installers Dominate, E-Commerce Rising

Traditional installer networks generated 70% of share in 2024 revenue, leveraging deep homeowner trust and turnkey service offerings. OEM direct sales serve bespoke commercial needs, but digital platforms now capture mindshare by coupling online configuration tools with certified-installer fulfillment.

E-commerce growth at 5.8% CAGR reshapes customer journeys, adding price transparency and buy-now-pay-later financing. A North Holland installer consortium’s digital portal cut acquisition costs 40%, signalling margin upside for early adopters. Regulatory mandates for certified commissioning ensure the channel evolves as click-to-install rather than pure DIY, preserving quality standards while expanding reach.

Geography Analysis

Amsterdam, Rotterdam, Utrecht, and The Hague concentrate early adoption of heat pumps, supported by municipal decarbonization agendas and dense housing that favors coordinated rollouts. The Hague’s aquathermal district for 500 apartments delivered a 50% emission reduction in 2024, illustrating urban viability even amid space constraints. [2]Decarbonising Homes in Cities in the Netherlands,” OECD, 2023, oecd.org Covenant of Mayors, “The Hague's Path to a Just Energy Transition,” Covenant of Mayors, 2025, eu-mayors.ec.europa.eu.

Grid congestion shapes regional feasibility, with some Amsterdam projects redesigning to hybrid systems that lower peak draw 40% after connection delays. National plans to double capacity within ten years confront shortages of skilled linemen and materials, implying a staggered expansion timeline that regionally differentiates the Netherlands heat pump market.

Rural provinces display lower penetration yet rising interest in shared ground-loop micro-districts. Friesland’s cooperative project reduced per-home installation costs 30% and improved seasonal efficiency, showing how community models can circumvent both capital and skills bottlenecks. Pilot funding under the National Programme for Local Heat Transition supports 66 such neighbourhood schemes, spreading uptake beyond the Randstad corridor.

Competitive Landscape

The Netherlands heat pump market is fragmented. International giants such as Daikin Industries Ltd., Mitsubishi Electric, and Viessmann are intensifying competition in the market. Their operations are not only raising performance benchmarks but also introducing advanced technologies, including high-temperature and natural refrigerants. Meanwhile, BDR Thermea's Remeha brand has bolstered domestic production with the inauguration of a new factory in 2023, boasting an annual output of 140,000 units. This move guarantees a resilient supply chain and enables tariff-free distribution across the EU. [3]BDR Thermea Group, “Remeha Opens the Largest Heat Pump Factory in the Netherlands,” BDR Thermea Group, August 28, 2023, bdrthermeagroup.com

Quatt BV, a venture-backed newcomer, focuses on AI-driven optimization and has installed over 7,500 smart heat pumps in the Netherlands over the past two years. The organization's swift payback period has made its heat pumps increasingly popular among the populace.

While established players experience some growth through installer loyalty and after-sales networks, emerging niches in both industrial and digital services are attracting new competitors. The surge in partnerships between original equipment manufacturers (OEMs) and energy service firms are creating integrated offerings.

Netherlands Heat Pump Industry Leaders

Viessmann Climate Solutions SE

Trane Technologies Plc

Daikin Industries Ltd.

Johnson Controls International Plc

Panasonic Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Viessmann Climate Solutions has introduced two new heat pump families: the Vitocal 250 and Vitocal 150. The premium Vitocal 250 series boasts top-tier efficiency, unparalleled comfort, and minimal noise emissions, while the more budget-friendly Vitocal 150 series offers a cost-effective alternative. Notably, the Vitocal 250-A heat pumps have achieved a noise emission reduction of up to 5 dB(A), now standing at 49 dB(A), Type A 10, which aligns with ErP regulations. This was achieved by enhancing the synergy between the compressor and fan.

- April 2025: Copeland, a provider of sustainable climate solutions, has strategically invested in BlueHeart Energy, a Netherlands-based startup pioneering an innovative heat pump technology. This move underscores Copeland's commitment to fostering innovations that combat climate change and strive for net-zero emissions.

- February 2025: A municipal wastewater treatment plant has been energized with a large-scale heat pump in Utrecht, the Netherlands, owing to the collaborative efforts of Innomotics, Eneco, and Johnson Controls. The newly installed system boasts four heat exchangers, each outfitted with dual compressors. By tapping into the residual heat from 65 million liters of treated wastewater daily, the system produces between 25 MW and 27 MW of heat. This output meets 15% of the district heating demand for both Utrecht and Nieuwegein, effectively serving around 20,000 households.

- November 2024: Trane has introduced the RTSF HT, a high-temperature water-to-water heat pump that can produce hot water at temperatures reaching 110°C. The RTSF HT joins Trane's CITY lineup, which features compact water-to-water heat pumps and chillers. Designed for reducing carbon emissions in high-temperature process heating, a sector still largely dependent on fossil fuel boilers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Netherlands heat pump market as the annual value generated from factory-built air-source, ground-source, and hybrid electric heat pump systems rated below 500 kW that are sold for space or process heating, hot water, and reversible cooling within Dutch residential, commercial, and light industrial buildings. We include both stand-alone and hybrid units so long as a heat pump compressor is present.

Scope Exclusions. We exclude room air conditioners without heating cycles, pure electric resistance heaters, large district energy heat pumps above 500 kW, and any gas-fired absorption heat pump units; these are tracked separately in our wider HVAC studies.

Segmentation Overview

- By Type

- Air-Source

- Water-Source

- Ground-Source (Geothermal)

- Others Types

- By Rated Capacity (kW)

- less than 10 kW

- 10-20 kW

- 20-50 kW

- 50-100 kW

- above 100 kW

- By Application

- Space Heating

- Space Cooling

- Domestic / Sanitary Hot Water

- Other Applications

- By End-User Vertical

- Residential

- Commercial

- Industrial

- Institutional

- By Installation Type

- New Build

- Retrofit / Replacement

- By Sales Channel

- Direct (OEM to End-User)

- Distributor / Installer Network

- E-Commerce

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts then interviewed Dutch installers, wholesaler buyers, energy cooperatives, and grid planning engineers across Randstad, Noord-Brabant, and Groningen. These conversations helped us validate retrofit-to-new-build ratios, installation lead times, subsidy uptake rates, and the likely shift toward natural refrigerant models, filling gaps left by desk work.

Desk Research

We began by assembling publicly available demand and supply indicators from sources such as Statistics Netherlands, Eurostat energy balance data, Dutch Customs import codes, European Heat Pump Association sales bulletins, and policy papers from the Ministry of Economic Affairs. Trade association white papers, municipal tender portals, and patent filings on R-290 compressors complemented the picture. Next, our team tapped paid databases, including D&B Hoovers for Dutch installer revenues and Dow Jones Factiva for investment news, to cross-check company footprints and average selling prices. This layered desktop review set the foundational volumes, typical capacities, and historic ASP trends. The sources cited above are illustrative only; many additional outlets were consulted for consistency checks.

Market-Sizing & Forecasting

We use a top-down demand pool build, starting with dwelling stock, floor area heat load norms, and announced boiler replacement milestones, corroborated with a bottom-up roll-up of sampled unit shipments from key distributors. Critical variables in the model include awarded ISDE incentive budgets, residential electricity-to-gas price spreads, grid connection queuing statistics, and yearly building permit issuances. A multivariate regression projects each driver through 2030, allowing scenario analysis around policy or fuel price shocks. Where shipment samples were partial, we gap filled using channel checks and average invoice values before reconciling totals against trade data.

Data Validation & Update Cycle

Every cycle, our analysts triangulate model outputs with EHPA unit tallies and CBS import values; anomalies trigger re-contacts with at least one market participant before sign-off. Reports refresh annually, and interim updates are issued when material events, such as incentive budget revisions, shift the baseline.

Why Mordor's Netherlands Heat Pump Baseline Commands Reliability

Published figures often diverge because firms apply contrasting equipment scopes, price assumptions, and refresh cadences. We openly anchor our 2025 baseline on installed capacity norms and subsidy linked ASPs, which our team re-verifies each quarter.

Key Gap Drivers include rival studies that fold the full HVAC equipment universe into a single line item or, conversely, isolate only geothermal loops; some also project in EUR and use static 2022 exchange rates, inflating gaps once restated in USD. Our yearly refresh and dual validation of volume and value temper such distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 505 M (2025) | Mordor Intelligence | - |

| USD 2.43 B (2025) | Regional Consultancy A | Includes all Dutch HVAC equipment, not just heat pumps |

| USD 302 M (2027) | Trade Journal B | Covers geothermal systems only; omits air source and hybrid units |

These contrasts show that Mordor's focused scope, live price updates, and bidirectional cross-checks yield a balanced, repeatable baseline that decision makers can trust.

Key Questions Answered in the Report

What is the current size of the Netherlands heat pump market?

The market generated USD 505.3 million in 2025 and is forecast to reach USD 628.1 million by 2030.

Which heat-pump type dominates Dutch installations?

Air-source models held 85% revenue share in 2024 because they retrofit easily into the nation’s existing housing stock.

How serious is grid congestion for future growth

Grid constraints subtract an estimated 1.3% points from forecast CAGR, prompting hybrid designs and smart energy management to spread peak loads.

Which customer segment will grow the fastest through 2030?

Industrial users are projected to adopt heat pumps at a 6% CAGR as EU ETS Phase 4 raises the cost of carbon-intensive process heat.

How are manufacturers addressing stricter refrigerant rules?

Leading brands now release propane-charged units and invest in local compressor production to meet F-gas limits while shortening supply chains.

What innovative financing models are boosting adoption?

Heat-as-a-Service subscriptions remove upfront costs and guarantee performance, making the technology attractive to renters and budget-conscious homeowners, especially in Amsterdam and Utrecht.

Page last updated on: