Poland Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

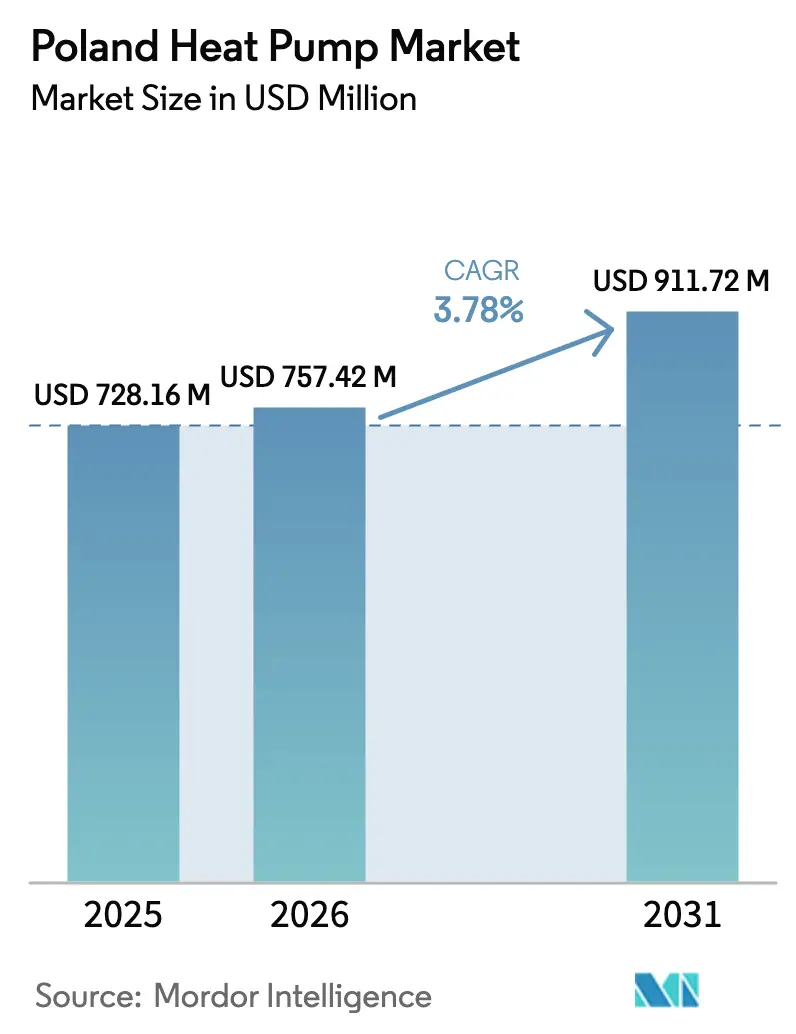

| Base Year Market Size (2025) | USD 728.16 Million |

| Market Size (2026) | USD 757.42 Million |

| Market Size (2031) | USD 911.72 Million |

| Growth Rate (2026 - 2031) | 3.78% CAGR |

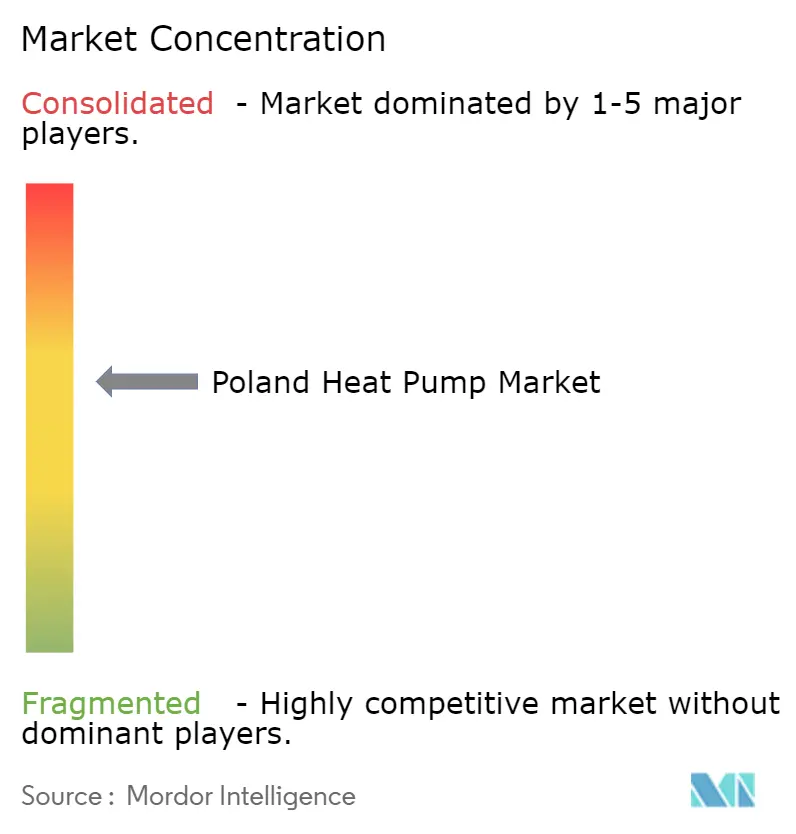

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Heat Pump Market Analysis by Mordor Intelligence

The Poland heat pump market size is projected to expand from USD 728.16 million in 2025 and USD 757.42 million in 2026 to USD 911.72 million by 2031, registering a CAGR of 3.78% between 2026 to 2031. During 2022-2025 the market swung from record double-digit growth to a steep contraction, revealing heavy reliance on subsidy continuity instead of purely economic pull factors. Subsidy reform in 2024, installer shortages, and grid bottlenecks created a short-term demand hole, yet structural decarbonization mandates, sustained tariff pressure on natural gas, and a strong rooftop solar roll-out have rebuilt a medium-term growth floor. Competition is intensifying as global majors scale local footprints while regional players leverage faster lead times and rural service reach. Market direction over the next five years will therefore hinge on simultaneous progress in grid reinforcement, workforce expansion, and refrigerant transition rather than on headline grant budgets alone.

Key Report Takeaways

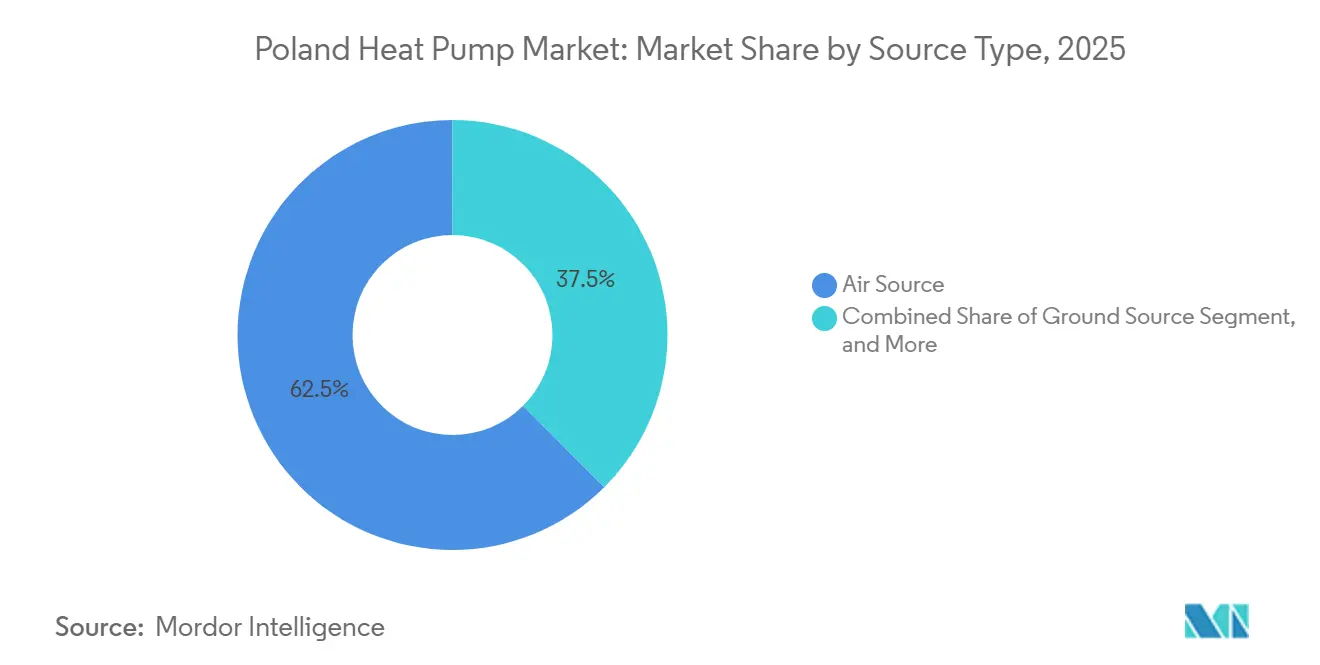

- By source type, air source systems led with 62.47% of the Poland heat pump market share in 2025, whereas hybrid configurations are forecast to grow the quickest at a 4.63% CAGR to 2031.

- By technology, air-to-water held 52.97% of the Poland heat pump market size in 2025, while ground-to-water is projected to expand at a 4.02% CAGR through 2031.

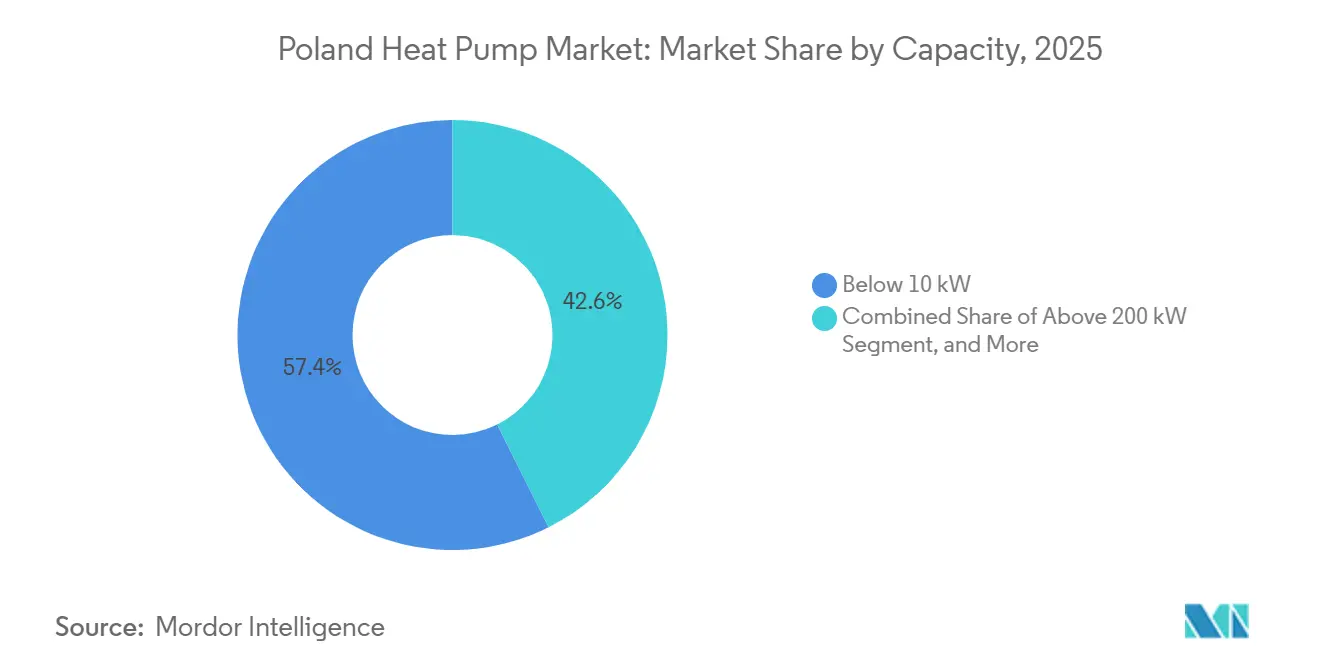

- By capacity, units below 10 kW captured 57.39% of 2025 revenue, yet 50-200 kW systems are on track for the fastest rise, advancing at a 3.97% CAGR to 2031.

- By application, space heating accounted for 68.72% of 2025 demand, whereas industrial and process heating will register the highest growth at a 4.07% CAGR over the forecast horizon.

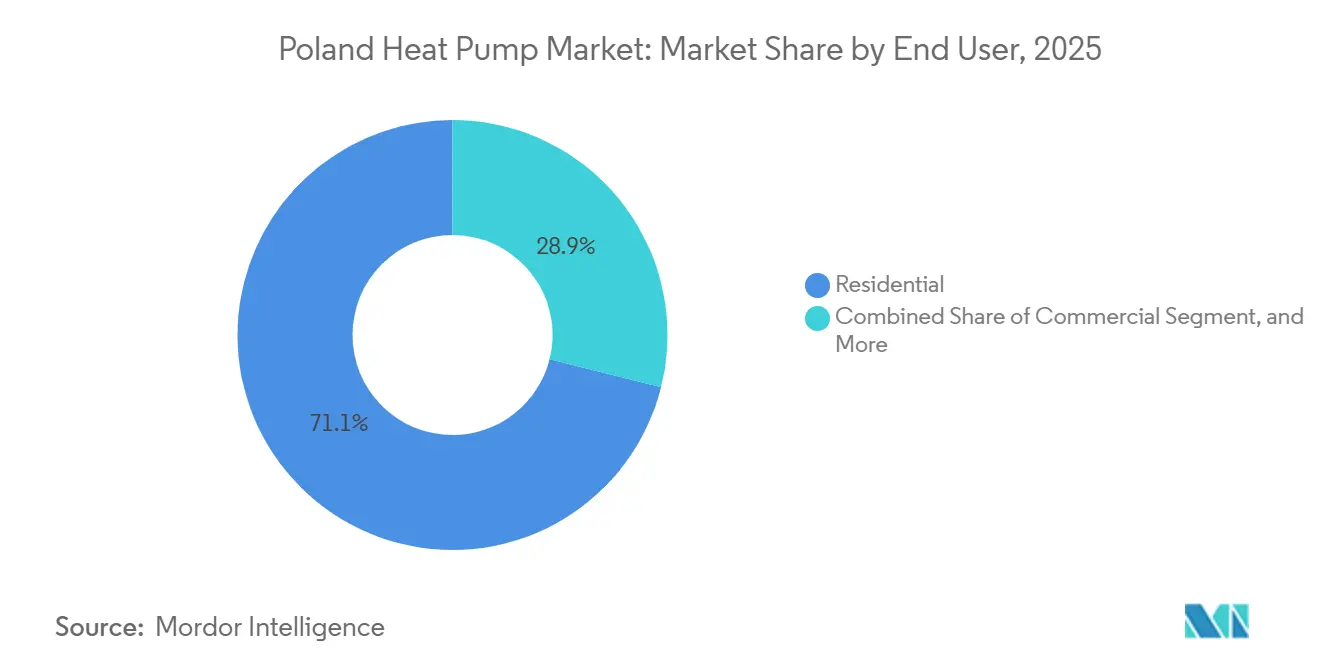

- By end user, residential installations dominated with 71.09% share in 2025, while commercial premises are anticipated to record a 3.91% CAGR to 2031.

- By installation type, new-build projects controlled 64.43% of 2025 volumes, but retrofit activity is expanding the quickest at a 3.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Poland Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained Government Subsidies Under the Clean Air and My Heat Programs | +0.9% | Nationwide, strongest in Mazowieckie, Małopolskie, Śląskie | Medium term (2-4 years) |

| EU Fit for 55 Decarbonization Mandates Accelerating Electrification | +0.8% | Nationwide within EU compliance framework | Long term (≥ 4 years) |

| Escalating Natural Gas and District Heating Tariffs | +0.7% | Urban centers with district heating dominance | Short term (≤ 2 years) |

| Surge in Rooftop PV Installations Enabling Self-Consumption Synergies | +0.5% | Southern and central voivodeships | Medium term (2-4 years) |

| Digital Twin-Enabled Remote Diagnostics Reducing Lifetime Costs | +0.3% | Commercial and industrial early adopters | Medium term (2-4 years) |

| Heat Pump Ready Municipalities Pilot Scheme | +0.2% | Selected pilot towns | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sustained Government Subsidies Under the Clean Air and My Heat Programs

Income-tiered grants introduced in 2025 now cover up to 90% of costs for low-income households replacing coal stoves, broadening affordability. Yet stricter energy certificate thresholds excluded poorly insulated dwellings, revealing that subsidies cannot substitute for envelope upgrades.[1]National Fund for Environmental Protection and Water Management, “Clean Air Program – Program Guidelines 2025,” nfosigw.gov.pl The My Heat scheme layered an extra PLN 56,000 (USD 14,000) for packages that couple heat pumps with rooftop PV, enticing the middle-income bracket. Approval backlogs averaging nine months shift working-capital risk onto installers, thereby favoring larger firms. Consequently, subsidy momentum is expected to peak during 2026-2027 before tapering as the pool of eligible homes shrinks.

EU Fit for 55 Decarbonization Mandates Accelerating Electrification

Poland must phase out 3.8 million coal boilers and 1.2 million gas units by 2030 to stay on its new climate pathway. The 2024 recast of the Energy Performance of Buildings Directive obliges all new homes from 2025 to meet near-zero targets, effectively locking in heat pumps at the design stage.[2]Official Journal of the European Union, “Directive (EU) 2024/1275 on the Energy Performance of Buildings (Recast),” eur-lex.europa.eu Minimum energy standards for the worst-performing 15% of existing stock will trigger mandatory retrofits, pushing demand even in reluctant regions. Enforcement risk persists because municipal compliance capacity lags EU timelines, but the legislative floor underpins long-run market volumes.

Escalating Natural Gas and District Heating Tariffs

Residential gas prices jumped 54% over 2024-2025 once temporary caps expired, while district heating fees climbed 31%, eroding their historic cost lead.[3]Polish Energy Regulatory Office, “Electricity and Gas Tariff Decisions 2024-2025,” ure.gov.pl The pivotal electricity-to-gas price ratio passed 3.5:1 in mid-2025, compressing heat-pump payback to seven-nine years. Although tariff relief could still swing sentiment, the probability of sustained fossil-fuel premium pricing rises as EU carbon charges deepen, reinforcing the Poland heat pump market pull. Household decision-making is now tied more to forward fuel-price expectations than to upfront equipment quotes.

Surge in Rooftop PV Installations Enabling Self-Consumption Synergies

Rooftop solar capacity reached 17 GW in 2024, with 11 GW on homes, providing daytime surplus electricity that can run compressors at very low marginal cost. Field data show combined PV-heat-pump systems cut grid purchases by up to 1,800 kWh a year, trimming integrated payback by almost two years. The My Heat grant design explicitly rewards this pairing, but looming net-metering revisions that lower the banking ratio from 1:0.8 to 1:0.6 after 2027 could dent the financial edge, creating policy uncertainty for installers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Equipment and Installation Costs amid Elevated Interest Rates | -0.6% | Lower-income households, rural areas | Short term (≤ 2 years) |

| Grid Congestion and Limited Low-Voltage Capacity in Rural Voivodeships | -0.4% | Podkarpackie, Lubelskie, Świętokrzyskie | Medium term (2-4 years) |

| Shortage of Certified Heat Pump Installers and HVAC Technicians | -0.3% | Nationwide, service deserts east and south | Medium term (2-4 years) |

| Refrigerant Supply Chain Volatility due to F-Gas Phase-Down | -0.2% | All regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Up-Front Equipment and Installation Costs Amid Elevated Interest Rates

Turn-key residential air-to-water systems cost USD 12,000-18,000, roughly two years of median disposable income. With consumer loan rates still near 10% in early 2026, financed purchases skew toward the top income quartile.[4]National Bank of Poland, “Monetary Policy Decisions 2024-2026,” nbp.pl Rural households lacking access to green-loan products remain locked into cheaper solid-fuel options despite generous grants. The 2023 sales crash underscored the sensitivity of the Poland heat pump market to monetary tightening rather than to hardware pricing alone.

Grid Congestion and Limited Low-Voltage Capacity in Rural Voivodeships

Legacy distribution lines sized for two-kilowatt evening loads cannot handle compressor spikes of 3-8 kW without voltage sag, forcing operators to impose costly transformer upgrades that add USD 3,000 or more per home.[5]Polish Distribution System Operators, “Grid Connection Requirements for Heat Pumps,” pse.pl Connection queues have stretched to 18 months in parts of Podkarpackie and Lubelskie, effectively freezing adoption despite available subsidies. EU funds worth EUR 225 million (USD 254.3 million) were earmarked for upgrades in 2024, yet work programs run to 2029, limiting near-term relief.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air Source Dominance With Hybrid Uptick

Air source products accounted for the largest slice of the Poland heat pump market size in 2025 and retained momentum thanks to installation simplicity and lower capital expenditure. Hybrid variants that couple compressors with legacy boilers are now the fastest risers, expanding in regions where consumers prize redundancy against grid brownouts. Manufacturers are embedding dynamic fuel-switching algorithms that respond to real-time tariff signals, shaving annual energy costs and nudging cautious homeowners toward partial electrification. Rural installers often recommend hybrids because the existing flue system stays in place and the fossil burner can cover sub-15 °C extremes, offsetting air-source derating.

Ground source systems hold a premium niche among suburban villas and commercial estates that own sufficient land or budget for boreholes. Their higher seasonal performance factors and exemption from outdoor noise limits appeal to quality-focused buyers, but four-to-six-month drilling permits and unit prices two-thirds higher than air systems temper wider adoption. Water source solutions remain marginal due to groundwater regulatory hurdles, whereas hybrid market share should keep inching up through 2031 as smart controls and R290 refrigerants boost low-temperature capacity.[6]International Journal of Refrigeration, “R290 Propane Refrigerant Performance in Heat Pump Applications,” sciencedirect.com

By Technology: Air-to-Water Lead and Ground-to-Water Commercial Momentum

Air-to-water units lead the Poland heat pump market share because they retrofit neatly onto existing radiator circuits. R290 refrigerant models, arriving in force since 2024, maintain full output down to -25 °C and close the performance gap with geothermal systems, helping sustain the segment’s edge. Ground-to-water technology, however, is pacing the commercial upswing in Mazowieckie and Wielkopolskie where large plots ease horizontal loop deployment. Hotel groups and logistics centers cite 20-year lifecycle economics and noise advantages as key triggers.

Air-to-air equipment remains a side-line, favored mostly in new low-energy homes where integrated cooling is specified at design stage. Water-to-water units serve small industrial heat-recovery roles but have little impact on retail volumes. Over the forecast horizon the technology battleground will revolve around variable-speed drives, natural refrigerants, and modular configurations that let installers stack 12-16 kW blocks up to mid-range commercial capacities without custom engineering.

By Capacity: Sub-10 kW Core With Mid-Range Upswing

Compact systems below 10 kW dominate detached-house retrofits and new builds alike, reflecting Poland’s average heated area of 120-150 m². Standardized workflows keep installation time under three days, an advantage in a market starved of technicians. Demand for 50-200 kW gear is climbing fastest as multi-family managers in Warsaw, Kraków, and Wrocław exit district heating grids and deploy roof-top cascades to feed central risers.

The 10-50 kW tier scales gradually with townhouse redevelopment and light commercial demand, while >200 kW units stay niche because grid connection charges soar and qualified designers are scarce. Modular inverter platforms launched by leading brands bridge part of the gap by allowing redundancy and phased capex, enticing cautious facility owners.

By Application: Heating Dominates, Process Loads Rise

Space heating still accounts for roughly two-thirds of units because Poland’s six-month heating season creates a clear anchor load. Yet process temperatures below 200 °C are emerging as a high-growth frontier inside food, textile, and chemical plants leveraging EU Just Transition cash. Field pilots show 40-60% fossil-fuel displacement alongside meaningful operating savings once carbon fees are factored in.

Cooling use cases lag due to modest cooling degree days, though climate change could spur uptake late in the decade. Domestic hot-water remains bundled with heating systems rather than a standalone driver. Over time, high-temperature 120-160 °C compressors will unlock new industrial pockets, but comfort heating will stay the primary revenue base through 2031.

By End User: Residential Holds Sway, Commercial Picks Up Speed

Owner-occupied houses produced 71% of 2025 installations, boosted by an 84% national homeownership rate and aggressive anti-smog policies. The commercial sector is now the fastest riser, helped by 10-12-hour operating profiles that sharpen payback and by corporate net-zero targets applied to offices, malls, and hotels.

Industrial penetration remains early stage, clustered in sub-200 °C applications compatible with current heat-pump technology. Residential momentum may moderate as population aging slows household formation, but retrofit waves in pre-1990 blocks still leave ample scope for volume.

By Installation Type: New-Build Lead, Retrofit Acceleration

Two-thirds of 2025 demand linked to new-build permits because near-zero energy codes effectively mandate heat pumps. Mortgage-rate headwinds have since cooled new starts, pivoting attention to retrofit business that benefits from thermomodernization tax relief. High-temperature monobloc models that run 70 °C water into legacy radiators are shrinking radiator-replacement cost, unlocking older stock.

Future subsidy tranches are expected to favor comprehensive fabric-plus-equipment packages, encouraging sequential projects where envelope work precedes compressor sizing. Regional patterns will diverge: peri-urban green-field zones stay new-build heavy, while inner-city boroughs and rural hamlets will rely on staged retrofits as grid upgrades and financing catch up.

Geography Analysis

Mazowieckie, anchored by Warsaw, delivered the highest absolute installations because incomes sit 18% above the national median and grid capacity supports simultaneous uptake of heat pumps and rooftop PV. Municipal air-quality bylaws that banned coal use inside the capital from 2024 added a regulatory nudge, reinforcing early-mover advantage. Kraków-centered Małopolskie follows, leveraging city-level co-financing that covers up to 95% of eligible project costs, a response to winter particulate peaks that frequently top EU limits.

Śląskie stands out for both opportunity and difficulty. EU Just Transition funding of EUR 1.5 billion (USD 1.695 billion) flows into coal-dependent towns, underwriting 85-90% grants and driving 3-4% annual penetration despite cultural ties to solid fuels. Still, grid reinforcement around mine-mouth plants lags, and workforce gaps persist. Coastal Pomorskie and Zachodniopomorskie add hotel-driven commercial orders but lag on residential front because of lower single-family prevalence.

The slowest roll-out is recorded in the rural east, Podkarpackie, Lubelskie, Świętokrzyskie, where per-capita income trails the mean by more than 12% and connection queues for 3-phase upgrades extend past a year. Without targeted grid financing and easier green loans the Poland heat pump market may see a widening urban-rural divide, with high-carbon heating entrenched where air quality concerns are paradoxically the most severe.

Competitive Landscape

The top five suppliers controlled roughly 48% of shipments in 2025, giving the Poland heat pump market a moderate concentration profile. Daikin has built company-run service hubs in the three largest metropolitan regions, capturing high-margin after-sales revenue and ensuring installer capacity. Carrier’s 2024 purchase of Viessmann’s climate division vaulted the combined entity to second place at around 11% share, and its integration roadmap prioritizes a USD 50 million digital platform that fuels predictive maintenance contracts.

NIBE’s acquisition of Enertech injected borehole drilling expertise that trims geothermal install costs by up to 18%, sharpening its pitch to commercial estates seeking lifecycle gains. LG, Panasonic, and Bosch lead the propane transition, fielding R290 lines that deliver eight-plus percent more heating capacity at sub-zero temperatures while satisfying F-gas quotas. Polish brand Galmet exploits four-week lead times and rural service density to defend a meaningful slice of price-sensitive customers, though its lack of advanced connectivity tools could cap future reach.

Installer scarcity is fast becoming the ultimate differentiator. Global brands have responded by launching proprietary certification programs that tie contractors into single-brand ecosystems, creating soft lock-in effects. Price-led Chinese entrants such as Midea and Gree have seized 18% share among budget buyers, yet higher complaint ratios and thinner service networks cloud their longer-term prospects. As digital diagnostics lower lifetime support costs the battle will pivot less on hardware discounts and more on ecosystem economics.

Poland Heat Pump Industry Leaders

Viessmann Werke GmbH & Co. KG

LG Electronics, Inc.

Fujitsu Limited

Daikin Industries Ltd

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Daikin committed EUR 150 million (USD 169.5 million) to expand European heat-pump output capacity by 30% through 2027, allocating lines for high-temperature units aimed at Polish industrial sites.

- February 2026: NIBE booked EUR 2.3 billion 2025 Climate Solutions revenue and unveiled a 45-technician service hub in Warsaw to buttress ground-source installations.

- January 2026: Panasonic launched its modular Aquarea L Generation using R290 refrigerant, scaled for 24-60 kW arrays that address Poland’s commercial retrofits.

- November 2025: Vaillant introduced aroTHERM plus 2.0 with tariff-responsive hybrid controls, posting 12-18% energy savings in Polish pilot homes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Polish heat-pump market as the annual revenue generated from first-sale, factory-built air, ground, or water-source (split or monoblock) units that provide space heating, cooling, or sanitary hot water across residential, commercial, industrial, and institutional buildings.

After-sales parts, contractor labor, hybrid HVAC chillers, and refurbished units fall outside this scope.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with installers, distributors, district-heating operators, and Clean Air program officers across Mazovia, Silesia, and Pomerania. Insights on average selling prices (ASP), preferred unit sizes, and grant uptake calibrated penetration curves and discount ladders.

Desk Research

Our team reviewed Poland's Central Statistical Office energy tables, Eurostat heat-pump series, EHPA and PORT PC unit reports, and subsidy guidelines from the Ministry of Climate & Environment. Company 10-Ks, press releases, and customs (HS 841861) data refined shipment scales. Paid utilities, D & B Hoovers for financials, and Dow Jones Factiva for deal flow validated revenue benchmarks. Questel patent analytics mapped R and D intensity. These sources are illustrative; numerous additional publications informed data cleaning and sense-checking.

Market-Sizing & Forecasting

We launched a top-down model that multiplies dwelling stock, new housing starts, and heated industrial floor space by heat-pump penetration rates tied to electricity-to-gas price spreads, insulation class, and grant intensity. Select bottom-up roll-ups of leading suppliers' domestic shipments verified totals before moderation. Key inputs include:

• retail electricity-to-gas ratio • Clean Air/My Heat outlay cadence • average seasonal COP • PV adoption that lowers running costs • building energy-efficiency codes

A multivariate regression supplemented by ARIMA smoothing projects revenue to 2030. Residual gaps in supplier roll-ups are balanced through moving-average ASP trendlines.

Data Validation & Update Cycle

Model outputs undergo variance checks versus EHPA unit tallies and import statistics. Senior analysts conduct peer reviews; figures refresh annually and adjust promptly after major tariff or subsidy shifts.

Why Mordor's Poland Heat Pump Baseline Earns Trust

Published estimates often diverge because firms vary in scope, year base, and data granularity.

Some track only import value or mix hybrid water-heaters, while others freeze currency at spot rates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 738 million (2025) | Mordor Intelligence | - |

| USD 500 million (2022) | Regional Consultancy A | Earlier base year; omits online and installer mark-ups |

| USD 325 million (2023) | Trade Statistics B | Imports only; excludes domestic output and retrofit channels |

Because our model aligns the latest unit volumes, ASPs, subsidy effects, and exchange rates, decision-makers gain a balanced, transparent baseline they can rely on for planning and investment.

Key Questions Answered in the Report

What is the projected revenue of the Poland heat pump market by 2031?

Revenue is forecast to reach USD 911.72 million by 2031, reflecting a 3.78% CAGR over 2026-2031.

Why did Polish heat pump sales fall sharply in 2023?

Subsidy reforms, macroeconomic uncertainty, and installer backlogs caused unit sales to drop 38.8% to 124,660.

Which technology leads installations today?

Air-to-water systems hold just over half of all units thanks to easy pairing with existing radiator circuits.

How are rising fuel tariffs influencing adoption?

Gas and district heating prices jumped 54% and 31% respectively through 2025, shortening heat-pump payback to below 10 years for many homes.

What limits rural uptake the most?

Weak low-voltage grids and long connection queues add thousands of dollars to project costs and delay installations up to 18 months.

Which capacity range is growing fastest in commercial retrofits?

Systems rated 50-200 kW are advancing at nearly 4% a year as multi-family blocks and light commercial sites exit district heating.

Page last updated on: