Switzerland Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

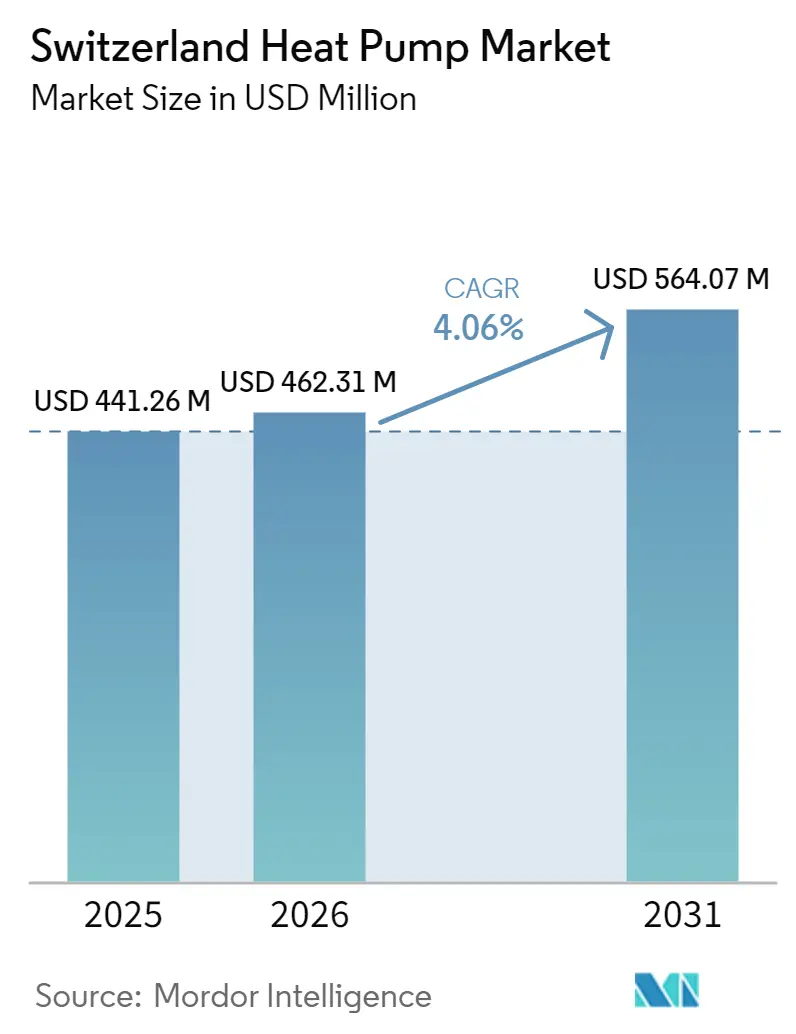

| Base Year Market Size (2025) | USD 441.26 Million |

| Market Size (2026) | USD 462.31 Million |

| Market Size (2031) | USD 564.07 Million |

| Growth Rate (2026 - 2031) | 4.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland Heat Pump Market Analysis by Mordor Intelligence

The Switzerland heat pump market size was valued at USD 441.26 million in 2025 and estimated to grow from USD 462.31 million in 2026 to reach USD 564.07 million by 2031, at a CAGR of 4.06% during the forecast period (2026-2031). The combination of generous federal and cantonal subsidies, escalating carbon-tax trajectories, and the country’s ambition to operate 1.5 million units by 2050 sustains a long-run expansion even though national sales dipped in 2024 as consumers digested earlier incentive waves. Roughly 450,000 systems were in service by mid-2025, and policy makers are doubling down on quality-assurance rules that favor certified installers, helping the Switzerland heat pump market stabilize profit margins. Competitive pressure is intensifying as Asian manufacturers deploy inverter-driven, natural-refrigerant models that address Swiss noise ordinances and high flow-temperature requirements, prompting European incumbents to speed R290 rollouts. Infrastructure constraints persist, yet pilot direct-load control programs and district-scale low-temperature networks demonstrate workable paths to integrate flexible demand into an aging grid.

Key Report Takeaways

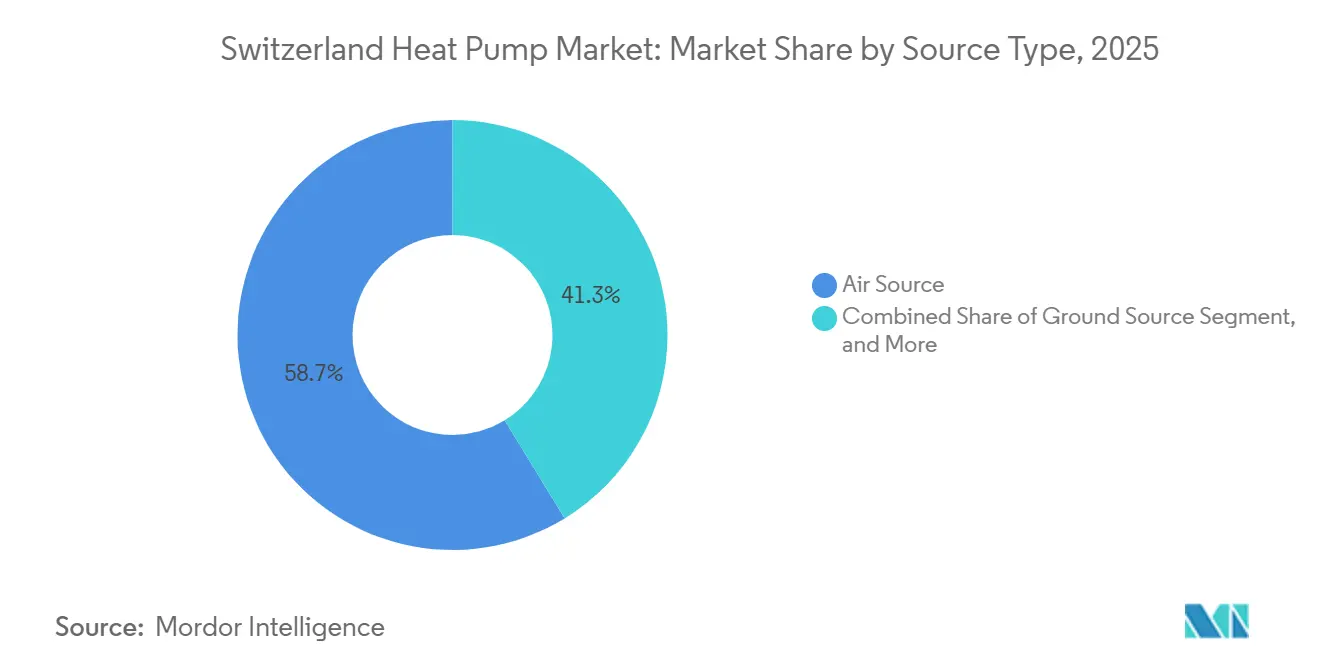

- By source type, air source captured 58.74% of the Switzerland heat pump market share in 2025, while hybrid systems are projected to expand at a 4.76% CAGR through 2031.

- By installation, retrofit projects held 57.43% share of the Switzerland heat pump market size in 2025, whereas new-build installations are forecast to grow at 4.87% CAGR over 2026-2031.

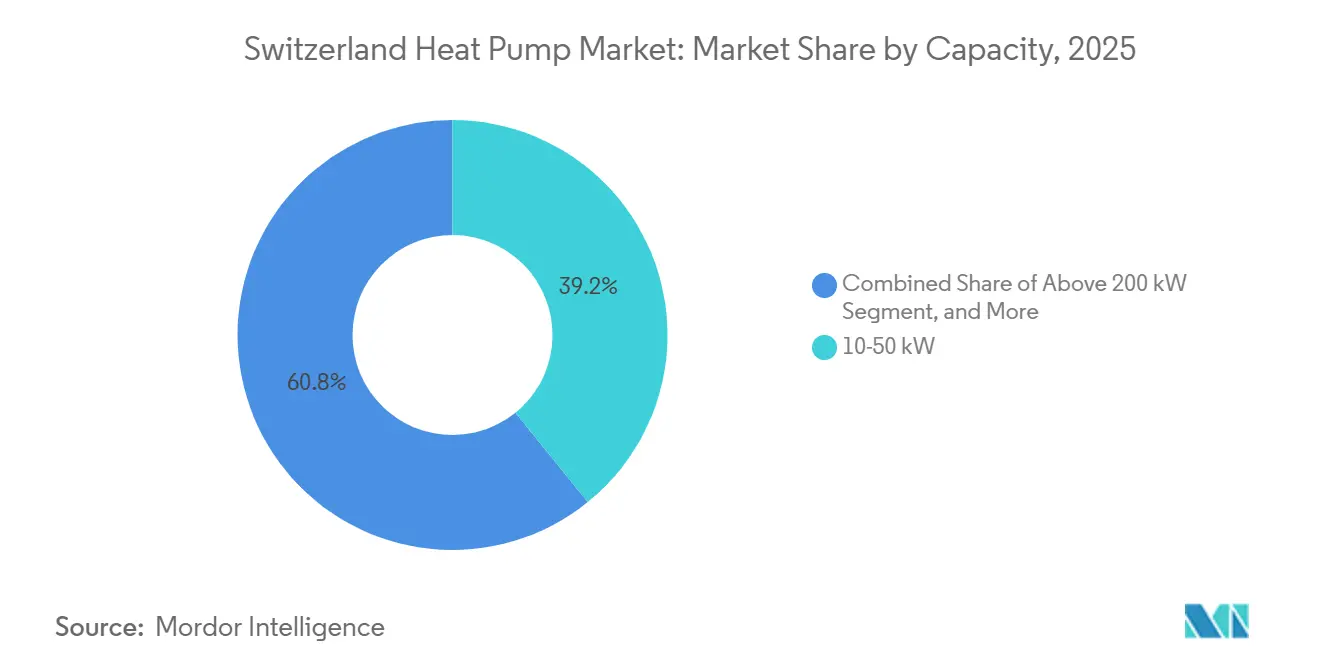

- By capacity, the 10-50 kW segment accounted for 39.16% share of the Switzerland heat pump market size in 2025, and systems below 10 kW lead growth at a 4.42% CAGR to 2031.

- By application, space heating led with 46.53% revenue share in 2025, while industrial and process heating is advancing at a 4.64% CAGR through 2031.

- By technology, air-to-water units commanded 53.31% share in 2025, yet ground-to-water solutions register the highest projected CAGR at 4.53% to 2031.

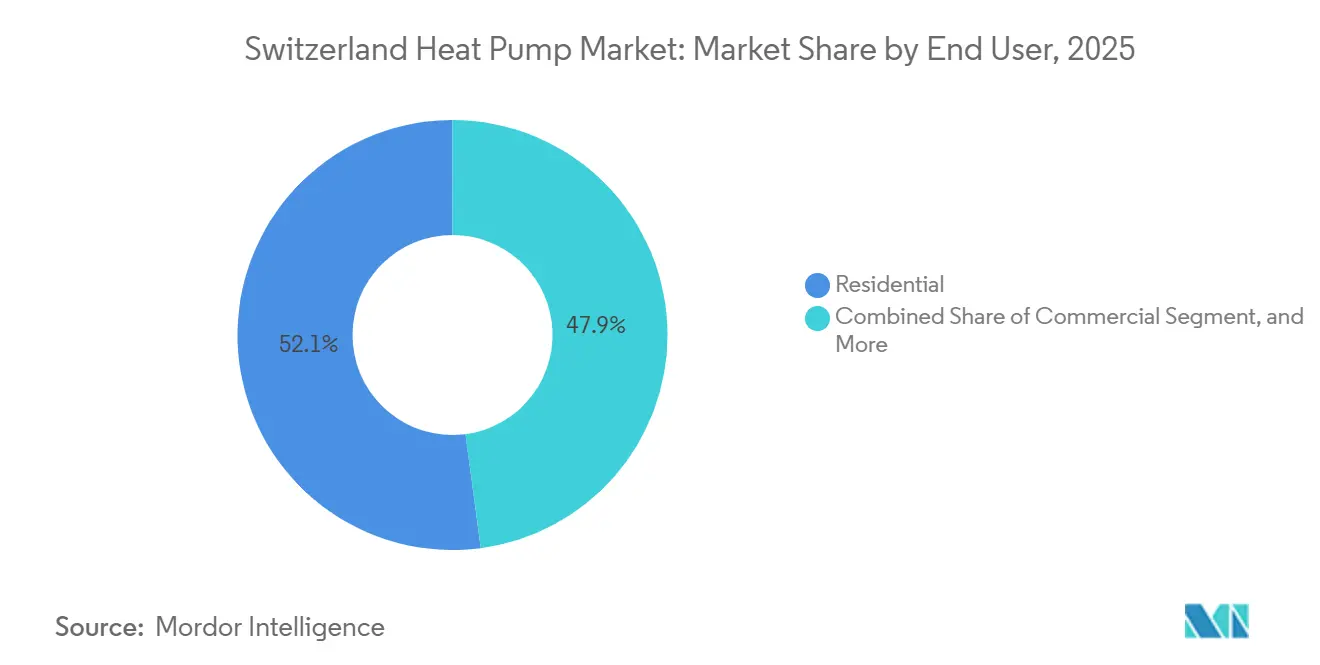

- By end user, residential buildings dominated with 52.09% market share in 2025, and the industrial segment records the fastest 4.21% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Switzerland Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Incentives and Subsidies for Decarbonized Building Stock | +1.2% | National, Higher Uptake in Vaud, Geneva, Zurich, Bern | Medium Term (2–4 Years) |

| Stricter Swiss Carbon-Tax Trajectories on Fossil Heating | +0.9% | National, Affects Oil and Gas Users in All Cantons | Long Term (≥ 4 Years) |

| Shift Toward Low-Temperature District Heating Retrofit Programs | +0.6% | Urban Centers, Notably Geneva, Zurich, Basel, Lausanne | Medium Term (2–4 Years) |

| Emergence of Building-Integrated PV-to-Heat-Pump Bundled Offers | +0.5% | National, Early Adoption in Aargau, Zurich, Vaud | Short Term (≤ 2 Years) |

| Growing Demand for Smart-Grid-Ready Heat Pumps Enabling Flexible Load Shifting | +0.4% | National, Pilots in Walenstadt, Neuchâtel, Baden | Medium Term (2–4 Years) |

| Accelerated Electrification of Alpine Tourism Infrastructure | +0.3% | Alpine Cantons, Notably Graubünden, Valais, Bern (Oberland) | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Government Incentives and Subsidies for Decarbonized Building Stock

Federal and cantonal programs channel CHF 2 billion (USD 2.3 billion) into building retrofits, and grants can reach CHF 15,000 (USD 17,000) for qualifying systems, compressing simple payback periods for homeowners.[1]Swiss Federal Office of Energy, “Buildings Programme,” bfe.admin.ch Zurich, Vaud, and Geneva layer additional subsidies that tilt the economics in favor of the Switzerland heat pump market even when upfront costs exceed gas-boiler alternatives.[2]Canton of Vaud, “Subventions Energie,” vd.ch The 2025 Klimaprämie adds CHF 360 (USD 410) per kW to multi-family projects, accelerating collective decision-making in apartment blocks. Quality-assurance rules now mandate professional monitoring for systems above 70 kW, steering demand toward established installers. These aligned incentives explain why retrofit activity captured 57.43% share in 2025 and keeps the Switzerland heat pump market on a steady adoption curve.

Stricter Swiss Carbon-Tax Trajectories on Fossil Heating

The CO₂ levy reached CHF 120 (USD 136) per tonne in 2025 and will climb further if targets are missed, cutting oil-boiler competitiveness and nudging consumers to electrify.[3]Swiss Federal Office for the Environment, “CO2 Levy,” bafu.admin.ch Cantons such as Geneva and Vaud overlay phase-out dates of 2030 and 2040, creating a regulatory ratchet that discourages new fossil systems. Hybrid heat pumps that retain a gas boiler for peak loads reduce annual carbon-tax exposure, a benefit validated by the Daru Geneva pilot, reinforcing their forecast 4.76% CAGR. The tax therefore shapes both consumer economics and product design, supporting the Switzerland heat pump market’s medium-term momentum.

Shift Toward Low-Temperature District Heating Retrofit Programs

Urban utilities are converting legacy networks into 5th-generation, low-temperature loops that integrate lake-, river-, and groundwater-source heat pumps, elevating seasonal performance while trimming losses.[4]SIG Geneva, “GeniLac,” sig-ge.ch Geneva’s GeniLac and Zurich’s 42 MW ammonia installation illustrate how municipal infrastructure, rather than individual boilers, drives incremental capacity.[5]ETH Zurich, “Heat pumps in district heating networks,” ethz.ch Vaud’s Grandvaux network cut borehole counts by 50% through thermal regeneration, proving that optimized shallow-geothermal design unlocks dense heritage areas. As more cities replicate these models, district conversions lift demand for medium-sized units and cement the Switzerland heat pump market as a grid asset rather than a standalone appliance.

Emergence of Building-Integrated PV-to-Heat-Pump Bundled Offers

Federal PV incentives now stack seamlessly with heat-pump grants, letting installers package rooftop solar, smart controllers, and thermal storage in turnkey deals that shorten payback to under 10 years in sunny regions. Genevan data centers and Aargau multi-generation houses show that oversized storage shifts compressor operation into midday solar peaks, cutting winter imports by 70%. This bundling particularly benefits the sub-10 kW class, forecast to outpace all capacity bands, and positions the Switzerland heat pump market as a cornerstone of behind-the-meter energy autonomy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CAPEX Versus Gas-Condensing Boilers | -0.8% | National, acute in rural cantons with lower subsidies | Short term (≤ 2 years) |

| Grid-Constrained Rural Communes Facing Transformer Upgrade Delays | -0.5% | Rural communes in Jura, Appenzell, Uri, Schwyz | Medium term (2-4 years) |

| Skilled-Labor Bottleneck for Certified Heat-Pump Installers | -0.4% | National, acute shortages in French-speaking cantons | Medium term (2-4 years) |

| Rising Ethical Concerns Over Rare-Earth Material Sourcing | -0.2% | National, driven by EU regulatory spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex Versus Gas-Condensing Boilers

Typical air-source systems cost CHF 30,000-CHF 40,000 (USD 34,000-USD 45,000) while equivalent gas boilers run CHF 15,000-CHF 20,000 (USD 17,000-USD 23,000), and drilling pushes ground-source investments to CHF 50,000 (USD 57,000).[6]Schmid AG energy solutions, “Air-to-water heat pump NIBE S2125,” schmid-energy.ch Electricity tariffs near CHF 0.22 (USD 0.25) per kWh mean a poorly insulated home achieving SCOP 3.5 can see higher operating costs than gas when the carbon tax is excluded. Subsidy disparities widen the gap, as rural cantons often offer half the urban grant level. Hybrid retrofits that retain a boiler cut capital outlay by 40% and therefore gain traction in cost-sensitive households. Until hardware prices fall or subsidy parity emerges, high first cost will temper the Switzerland heat pump market’s near-term acceleration.

Grid-Constrained Rural Communes Facing Transformer Upgrade Delays

Swissgrid’s CHF 5.5 billion (USD 6.2 billion) plan covers only 60% of expected load growth from electrified heating, leaving municipal utilities to finance low-voltage upgrades.[7]CIRED, “Grid Infrastructure and Heat Pump Integration,” cired2025.org A Walenstadt study showed voltage collapse beyond 40% penetration without hardware reinforcement, with each transformer upgrade priced at CHF 50,000-CHF 100,000 (USD 57,000-USD 113,000). Homeowners often delay installations until utilities commit to upgrades, while utilities wait for confirmed demand, creating a feedback loop that restrains the Switzerland heat pump market in sparsely populated areas. Direct-load control pilots in Neuchâtel and Baden aim to defer capital spend, yet only 15% of units installed by 2025 were smart-grid ready. Resolving this coordination problem is paramount for equitable rural adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Hybrid Systems Bridge Electrification Gap

Air source units delivered 58.74% of 2025 sales, supported by faster permitting and lower installation cost compared with ground-source alternatives. Models such as NIBE S2125 achieve SCOP 5.0 and operate at -25 °C, extending the Switzerland heat pump market reach into high-altitude regions. Water-source solutions are small in unit count but headline major municipal schemes, including Geneva’s GeniLac lake-water network, demonstrating their infrastructure value. Ground-source systems remain appealing for new builds with long ownership horizons because boreholes last more than 60 years and support seasonal COP above 5.0.

Hybrid configurations are forecast to expand at a 4.76% CAGR to 2031, the fastest among source types, by pairing R290 heat pumps such as Viessmann’s Vitocal 250-AH with existing gas boilers, cutting capital needs by roughly one-third while delivering 70% renewable coverage. The AirBiVal project shows that adaptive bivalent control strategies save CHF 2,000 (USD 2,300) in annual carbon-tax exposure compared with fixed-switchpoint operation. Cantonal drilling-permit delays and strict noise thresholds tilt urban retrofits toward air and hybrid systems, reinforcing their leadership in the Switzerland heat pump market.

By Technology: Ground-To-Water Gains In District Applications

Air-to-water designs represented 53.31% of 2025 shipments, owing to compact form factors that ease rooftop or façade placement in dense cities. Products like NIBE S2125 deliver 75 °C flow at -25 °C ambient, satisfying radiator retrofits that dominate the Switzerland heat pump market. Air-to-air units stay niche because domestic hot-water regulations require additional equipment. Water-to-water technology shines in data centers and district loops; Infomaniak’s Geneva facility upgrades 45 °C server heat to 85 °C for municipal distribution, replacing 3,600 tCO₂e of gas annually.

Ground-to-water systems are projected to post a 4.53% CAGR to 2031, powered by 5th-generation networks and institutional campuses. The Grandvaux UNESCO project used 64 boreholes in a single-tube loop to serve 67 heritage buildings without breaching geothermal extraction limits, underlining design innovation. Empa’s Dübendorf site pushes 65 °C into 100 m probes for seasonal storage, providing a live test bed for regulators wary of groundwater impacts. As district operators replicate these successes, ground-to-water adoption will rise from today’s low share within the Switzerland heat pump market.

By Capacity: Compact Units Target Urban Density

The 10-50 kW band held 39.16% of 2025 revenues by covering single-family homes and small multi-family blocks with modular units such as NIBE S1155, available in 6-25 kW outputs and SCOP 5.2. Above 50 kW, cascaded arrays like the six-unit Daru Geneva retrofit deliver redundancy and staged commissioning for 68 apartments, reflecting urban property constraints.

Systems below 10 kW should climb at a 4.42% CAGR through 2031 as compact, low-noise models such as Dimplex LA 1118CP meet stringent 40 dB(A) nighttime limits. Vaillant’s 5-7 kW aroTHERM pro range adds remote diagnostics and five-year warranties to offset installer shortages. Grid-friendly controls embedded in this class position it as the growth engine for the Switzerland heat pump market, particularly in apartment retrofits where outdoor space is scarce.

By Application: Industrial Process Heating Accelerates

Space heating accounted for 46.53% of 2025 revenues, reflecting its traditional dominance in Swiss residential and commercial buildings. Domestic hot water production rides alongside most residential units, while data centers now couple the cold side of water-to-water machines with server cooling duties, removing separate chiller loads. The Neuchâtel refurbishment showed that smart charging trimmed electricity bills by CHF 1,500 (USD 1,700) a year through off-peak scheduling. Space cooling is gaining ground in offices and hospitality as climate change lengthens summer demand, nudging multipurpose designs into retrofits that once focused only on heating.

Industrial and process heating is projected to grow at a 4.64% CAGR through 2031, the fastest of all uses, as high-temperature units reach 90 °C for dairy pasteurization, meat processing, and pharmaceutical sterilization. Roche’s 1.2 MW helium system and the Gais cheese-factory retrofit confirm that payback drops below five years when rising CO₂ levies are factored in. Waste-heat recovery schemes in data centers such as Infomaniak’s Geneva plant demonstrate how a steady 45 °C source can be boosted to 85 °C for district grids without fossil backup. As more sites copy this template, the Switzerland heat pump market will diversify beyond space heating, reinforcing long-term demand resilience.

By End User: Industrial Segment Gains Momentum

Residential buildings held 52.09% share in 2025, sustained by policy targets that call for 1.5 million installed systems by 2050. Subsidy stacking favors apartment blocks because the Klimaprämie rewards capacity above 70 kW, prompting condominium associations in Zurich and Lausanne to approve group retrofits despite complicated ownership structures. Compact 5-7 kW units with remote diagnostics lower service costs and offset the installer shortage, keeping the Switzerland heat pump market attractive to homeowners.

Industrial customers are forecast to expand at a 4.21% CAGR across 2026-2031, narrowing the gap with residential buyers. Early movers such as SFS Group and the Basel pharma cluster prove that uptime requirements can be met with redundant cascades and professional monitoring. Data centers create a hybrid category that blurs industrial and commercial boundaries by monetizing waste heat under long-term contracts with district-network operators. As these examples spread, the Switzerland heat pump market gains a second engine of growth that is less sensitive to consumer sentiment and subsidy revisions.

By Installation: New Builds Face Retrofit Competition

Retrofits captured 57.43% of 2025 installations because buildings erected between 1950 and 1985 are hitting boiler end-of-life just as cantons roll out fossil-phase-out mandates. Hybrid air-to-water arrays in Geneva’s Daru project showed that retaining a gas boiler for peaks can cut capital requirements by 40% and still displace 70% of annual fossil use. Continuous commissioning trimmed winter electricity consumption by 10%, highlighting the value of quality assurance now baked into federal rules.

New-build systems are set to rise at a 4.87% CAGR, the quickest among installation types, because cantonal energy codes effectively prohibit fossil heat in permits issued after 2024. Zurich and Bern require Minergie-class envelopes, steering developers to ground-source or district connections at the blueprint stage. Advanced geothermal layouts such as the Grandvaux 5th-generation network cut drilling meters by half, proving that front-loaded design delivers lower life-cycle cost. As land-use plans in suburban growth corridors press for higher density, pre-integrated heat-pump stations in utility rooms will anchor the next wave of the Switzerland heat pump market.

Geography Analysis

Vaud, Geneva, and Zurich dominate installations because their subsidy ceilings of CHF 10,000-CHF 15,000 (USD 11,300-USD 17,000) slice payback periods to under eight years. GeniLac’s lake-water network in Geneva and Zurich’s 42 MW ammonia plant show how city utilities embed large water-source machines into district loops, shifting demand from individual boilers to centralized assets. Bern positions itself as an innovation hub with Empa’s high-temperature borehole storage that pushes 65 °C into 100 m probes, answering groundwater regulators who worry about thermal plumes.

Rural cantons such as Jura, Appenzell, and Uri lag high-subsidy peers because transformer upgrades cost up to CHF 100,000 (USD 113,000) each and utilities hesitate without firm demand. ETH’s Walenstadt study warned that voltage drops become nonlinear once 40% of homes electrify heating, making direct-load control or hardware reinforcement unavoidable. Pilot curtailment contracts in Neuchâtel and Baden pay residents lower tariffs in exchange for remote switching, demonstrating one mitigation path. Alpine cantons Graubünden and Valais electrify ski-resort hotels with geothermal-ice-battery hybrids, proving that the Switzerland heat pump market can thrive even at 1,500 m altitude when design meets acoustic rules.

Language borders add labor friction: German-speaking installers command shorter wait times, while French-speaking regions depend on cross-border technicians who must pass Swiss certification exams. Italian-speaking Ticino trails in uptake because subsidies run lower and building stock skews oil heated; parity programs could unlock a leapfrog straight to R290 units that comply with F-gas phase-down. National modeling by ETH shows that balanced geographic roll-out could reduce net power imports 20% and raise renewable utilization by 4%, yet today’s urban concentration risks bottlenecks and stranded rural biomass potential. Together, these patterns illustrate how cantonal autonomy both stimulates local innovation and fragments the Switzerland heat pump market.

Competitive Landscape

Moderate fragmentation defines the field, with no brand above 15% share, yet rivalry stiffens as natural-refrigerant portfolios race to market. Daikin’s January 2026 joint venture with Copeland will ship R290 rotary compressors from Slovakia, enabling 75 °C flow while complying with F-gas quotas, a specification crucial for radiator retrofits that underpin the Switzerland heat pump market. Viessmann, Vaillant, and Stiebel Eltron answer with propane lines that embed activated-carbon boxes instead of exhaust pipes, cutting installation time in multi-family basements. NIBE partners with Schmid Mawera Group to cement distribution reach after their 2026 merger, indicating that local service scale is becoming a gating factor.

White-space opportunities lie in industrial high-temperature applications, where 80% of the 145-723 MW national potential remains untapped. Swiss maker CTA aims at hospitals and universities with domestically built ground-source systems that leverage a “buy Swiss” brand halo. Planeto supplies simulation software to utilities designing 5th-generation loops, taking a picks-and-shovels role that scales faster than hardware sales. Borobotics’ lightweight drilling robot could drop borehole cost below the prevailing CHF 150 (USD 170) per meter if its 2026 extrusion upgrade proves reliable, lowering the entry ticket for ground-source retrofits.

Regulatory compliance favors incumbents that pre-certify acoustics, seismic safety, and refrigerant mass limits across 26 cantons, yet the skilled-labor crunch opens doors for cloud-based remote-diagnostics platforms that cut on-site visits by 30%. Consolidation pressure rises among regional installers that lack capital to train bilingual technicians and manage canton-specific paperwork, spurring mergers or franchising deals. Overall, dynamic innovation and selective vertical integration keep the Switzerland heat pump market competitive but disciplined.

Switzerland Heat Pump Industry Leaders

Daikin Industries Ltd.

Viessmann Werke GmbH & Co. KG

Bosch Thermotechnology (Robert Bosch GmbH)

Stiebel Eltron GmbH & Co. KG

NIBE Industrier AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Daikin and Copeland formed a joint venture to manufacture R290 rotary compressors for European residential heat pumps, with Slovakian production slated for Q4 2026.

- January 2026: Schmid Energy debuted the ADAPT 2 air-to-water unit, merging with Mawera to create Schmid Mawera Group and expand national service coverage.

- December 2025: EGEC released “Geothermal Innovation Trends 2025,” highlighting Swiss seismic surveys that expand subsurface data for future shallow-geothermal rollouts.

- August 2025: Infomaniak activated two 1.6 MW Trane XStream water-to-water heat pumps at its Geneva data center, injecting 14.9 GWh of 85 °C heat annually into the cantonal network.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Switzerland heat pump market as the annual revenue generated from factory-built air-source, ground-source, water-source, and hybrid units that deliver space heating, space cooling, or sanitary hot water for residential, commercial, industrial, and institutional buildings. Systems shipped inside packaged HVAC rooftops are counted only when the heat-pump section exceeds 60% of seasonal operating hours.

Scope Exclusion: Portable room appliances, vehicle climate-control heat pumps, and tumble-dryer units are excluded.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed Swiss installers, wholesale distributors, utility efficiency advisors, and engineering consultants across German-, French-, and Italian-speaking cantons. These conversations clarified real-world retrofit costs, installer capacity, rated-capacity preferences, and forecast subsidy trajectories, allowing us to refine secondary assumptions and sense-check model outputs.

Desk Research

Analysts first gathered macro-building data from sources such as the Swiss Federal Office of Energy, Eurostat's energy balance tables, and the European Heat Pump Association to map installed stock, construction permits, and subsidy uptake. Trade flows and average selling prices were pulled from Swiss customs (TARIC code 8418) and the UN Comtrade mirror series, then checked against shipment intelligence from D&B Hoovers and price briefs in Dow Jones Factiva. Complementary insights on refrigerant regulations and grid-carbon factors came from the International Energy Agency, academic journals indexed on Questel, and policy notes issued by the Federal Council. Company 10-Ks, cantonal incentive portals, and industry press completed the picture. This list is illustrative; many additional open and paid sources fed our evidence base.

Market-Sizing & Forecasting

A top-down construct starts with dwelling stock by vintage and heated floor area, multiplies by heat-pump penetration rates and canton-level replacement cycles, and is converted to value using weighted average system ASPs. Bottom-up roll-ups of leading suppliers' Swiss revenues plus sampled installer invoices validate totals and adjust anomalies. Key variables tracked include: 1) new-build permits, 2) retrofit subsidy approvals, 3) annual heat-pump shipments, 4) electricity-to-gas price differential, and 5) average rated capacity mix. Forecasts to 2030 rely on multivariate regression, with shipment growth and energy-price spread as leading indicators and moderated by grid-capacity constraints flagged in interviews. Data gaps on large bespoke units are bridged through installer sample scaling.

Data Validation & Update Cycle

Outputs pass a three-level review in Mordor Intelligence: automated variance checks, peer analyst audit, and senior sign-off. We refresh the model each year and trigger interim updates when subsidy rules, currency swings, or unit shipments shift more than five percent.

Why Mordor's Switzerland Heat Pump Baseline Stays Dependable

Published figures differ because firms choose dissimilar scopes, cost bases, and refresh rhythms. By anchoring on installed-stock logic and verified ASPs, our totals track the economic reality decision-makers face.

Key Gap Drivers include rivals enlarging scope to include heat-pump water heaters, relying on customs values alone, or projecting aggressive subsidy continuance without installer-capacity limits.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 421.9 M | Mordor Intelligence | - |

| USD 567.6 M | Global Consultancy A | Bundles water-heaters and EV heat-pump modules; assumes uniform 15% annual subsidy rise |

| USD 165.0 M | Industry Database B | Uses import value for tariff 8418 only; omits domestic production and retrofit mark-ups |

The comparison shows why our 2024 baseline sits between inflated demand-pool views and narrow customs-only calculations, giving clients a balanced, transparent number they can trace back to real stock, real prices, and repeatable steps.

Key Questions Answered in the Report

What is the current size of the Switzerland heat pump market and how fast is it growing?

The Switzerland heat pump market size stood at USD 462.31 million in 2026 and is projected to reach USD 564.07 million by 2031, advancing at a 4.06% CAGR.

Which source type is expanding the quickest?

Hybrid systems that pair a heat pump with an existing gas boiler are forecast to grow at a 4.76% CAGR through 2031 because they lower capital cost while meeting carbon-reduction rules.

Why are ground-to-water systems gaining attention?

New low-temperature district networks and institutional campuses favor ground-to-water setups because borehole fields provide seasonal storage and help cut network heat loss by 65%.

How do subsidies differ by canton?

Urban cantons such as Geneva, Vaud, and Zurich offer grants up to CHF 15,000 (USD 17,000), while rural cantons often cap support at CHF 5,000 (USD 5,700), influencing adoption rates.

What limits faster rural uptake?

Distribution transformers in many rural communes require upgrades costing up to CHF 100,000 (USD 113,000), and utilities are cautious about spending before enough homeowners commit.

Which industrial sectors are adopting high-temperature heat pumps?

Dairy, pharmaceutical, and meat-processing plants are leading because modern machines now deliver 80-90 °C process heat with paybacks below five years when rising CO? levies are included.

Page last updated on: