Denmark Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

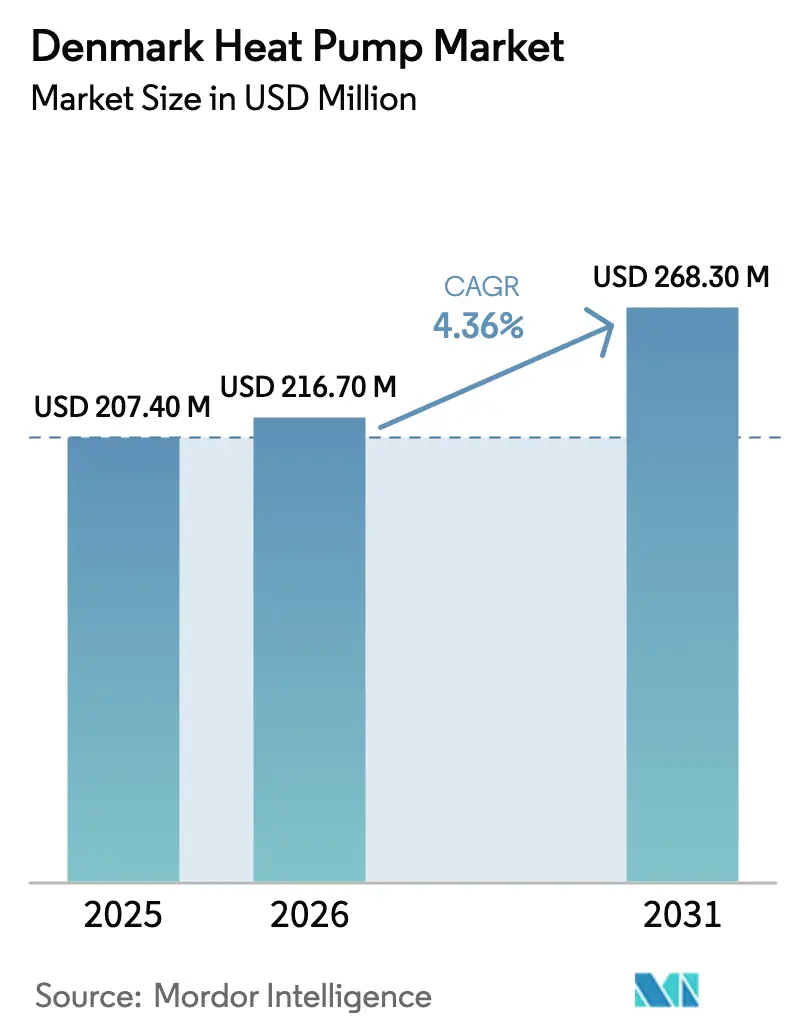

| Base Year Market Size (2025) | USD 207.40 Million |

| Market Size (2026) | USD 216.70 Million |

| Market Size (2031) | USD 268.30 Million |

| Growth Rate (2026 - 2031) | 4.36% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark Heat Pump Market Analysis by Mordor Intelligence

The Denmark heat pump market size is projected to expand from USD 207.4 million in 2025 and USD 216.7 million in 2026 to USD 268.3 million by 2031, registering a 4.36% CAGR between 2026 and 2031. Strong policy incentives, falling retail electricity prices, and district-heating electrification are compressing payback periods and converting latent interest into firm orders. Utilities are switching from fossil-fired boilers to multi-megawatt carbon-dioxide systems, while households embrace compact air-to-water units that qualify for fast-track permits. Vendors respond with factory-assembled modules that minimize on-site labor, a critical pivot amid a persistent shortage of certified technicians. Competitive intensity is therefore rising as traditional residential suppliers partner with industrial compressor specialists to win utility-scale tenders.

Key Report Takeaways

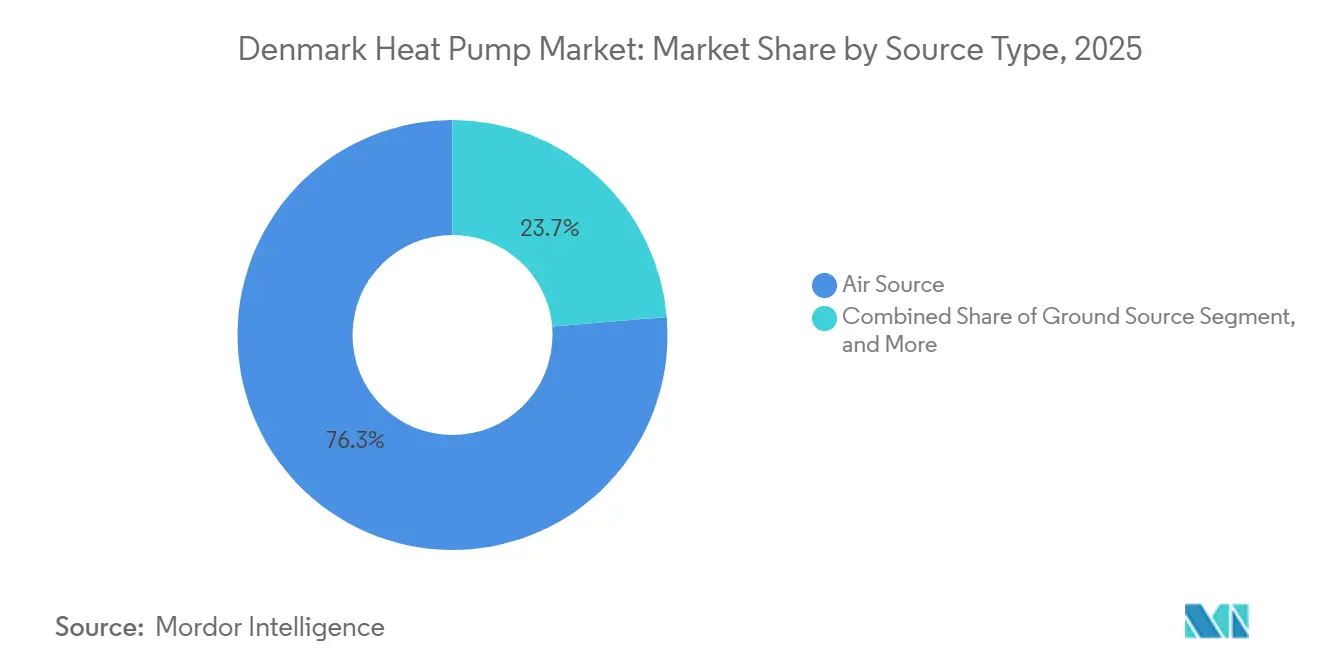

- By source type, air source systems held 76.34% of the Denmark heat pump market share in 2025, while hybrid configurations are on track to record a 6.31% CAGR through 2031.

- By technology, air-to-water technology accounted for 54.59% of the Denmark heat pump market size in 2025; ground-to-water installations are poised for a 5.02% CAGR to 2031.

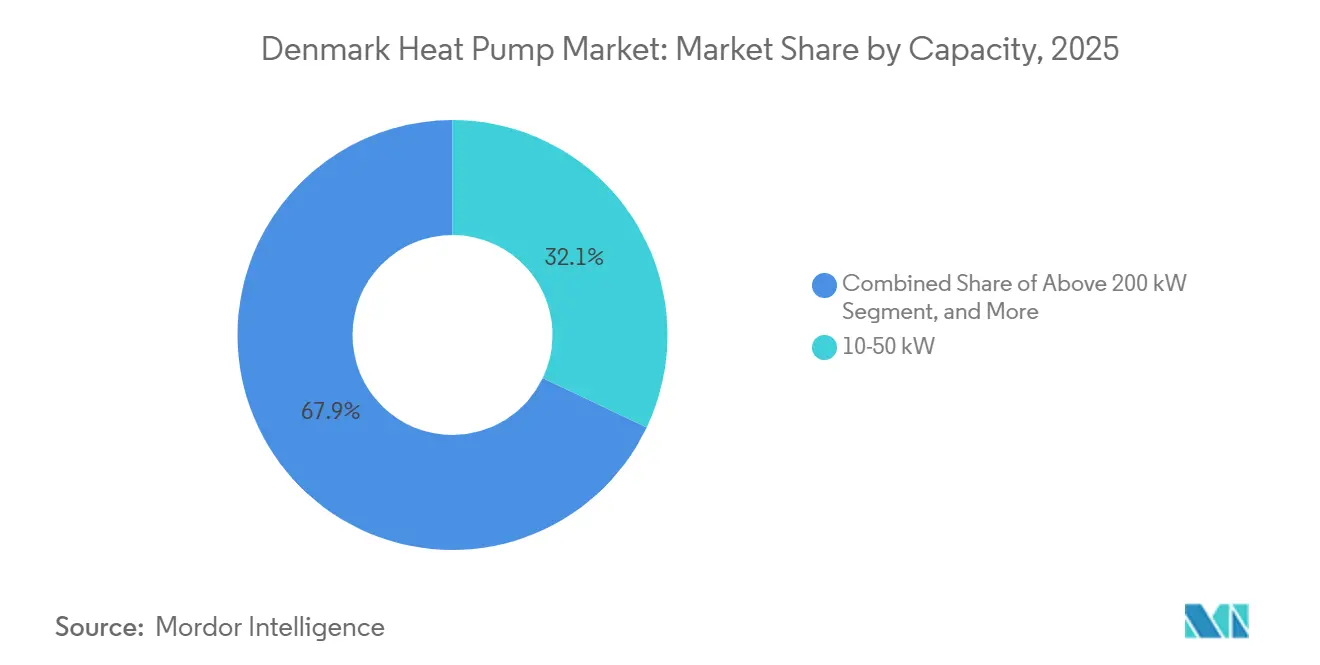

- By capacity, the 10-50 kW band captured 32.07% of 2025 capacity additions, whereas systems below 10 kW are forecast to advance at a 5.23% CAGR.

- By application, space heating represented 61.21% of 2025 demand, yet space cooling is projected to post a 4.74% CAGR as summers grow warmer.

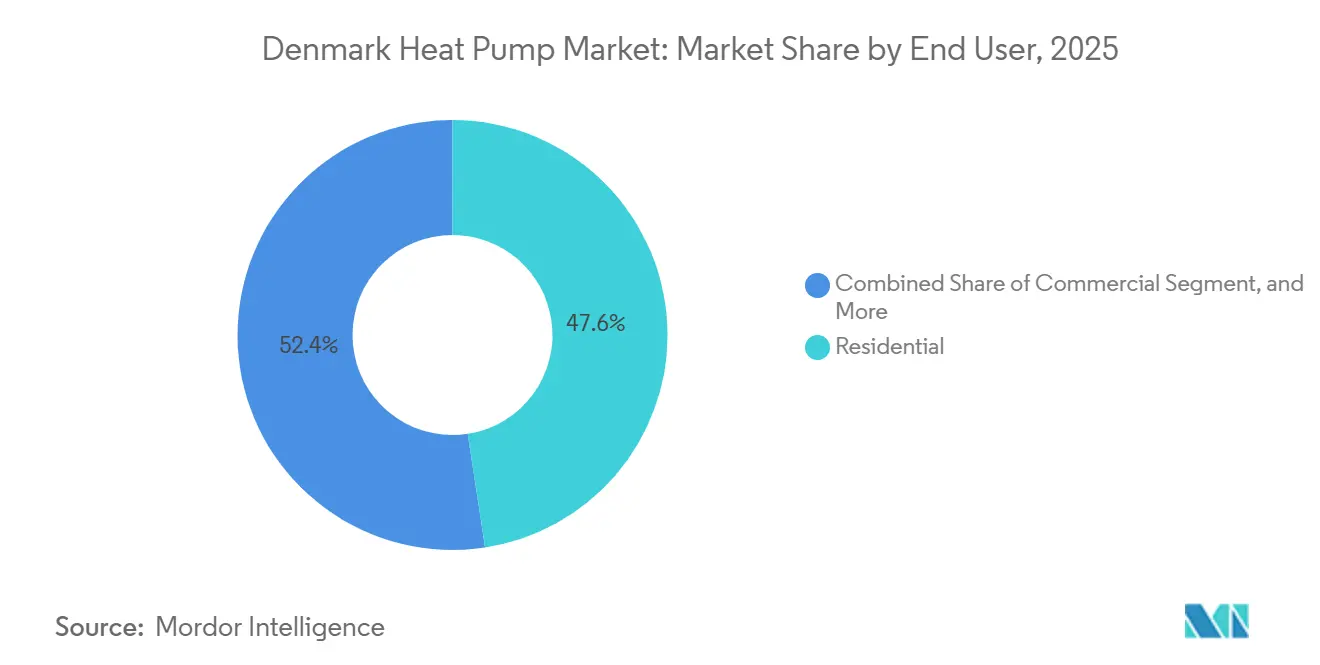

- By end user, residential users installed 47.58% of units in 2025, but commercial deployments are projected to grow at a 4.86% CAGR on the back of energy-label mandates.

- By installation, retrofit work dominated with 63.12% share in 2025; new-build projects are expected to expand at a 5.06% CAGR as all new structures must reach energy class A from 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Denmark Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supportive Government Incentives for Energy Savings | +0.8% | National, highest in Greater Copenhagen and Aarhus | Short term (≤ 2 years) |

| Rising Demand for Energy-Efficient Systems | +0.7% | Nationwide, stronger in municipalities enforcing energy labels | Medium term (2-4 years) |

| Mandatory 2030 Installation of Eco-Design Class A+++ Heat Pumps | +0.6% | Nationwide, phased from 2027 | Long term (≥ 4 years) |

| Electrification of District-Heating Networks in Copenhagen and Aarhus | +0.9% | Copenhagen, Aarhus, Aalborg, Esbjerg, Billund, Odense | Medium term (2-4 years) |

| High Carbon Tax Accelerating Residential Conversions | +1.0% | Nationwide, strongest in single-family homes outside district zones | Short term (≤ 2 years) |

| Rapid Decline in Retail Electricity Prices from Wind Overcapacity | +0.5% | Nationwide, most pronounced in DK1 (western Denmark) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supportive Government Incentives for Energy Savings

The 2026 Varmepumpepuljen budget of DKK 116.9 million (USD 18.1 million) raised the grant to DKK 27,000 (USD 4,190) per installation, representing a 59% jump over 2025. A digital portal now approves most claims in minutes, erasing paperwork delays and freeing installers to start jobs immediately.[1]CBRAIN, “New Federal Heat Pump Grant System Approves 67% of Applications in Minutes,” cbrain.dk Only 10% of buyers actually apply, however, because falling equipment prices and shorter payback periods already justify purchases without subsidies. Equal treatment of air-to-water and ground-source units removes the historic bias that distorted product choice and opens fresh runway for geothermal systems on large plots. Installers therefore schedule projects more predictably, reduce idle time, and improve overall capital utilization.

Rising Demand for Energy-Efficient Systems

All new Danish buildings must achieve energy class A from January 2030, while roughly 800,000 existing homes face staged upgrades to class E by 2033. Heat pumps deliver the lowest life-cycle cost among available solutions, especially when paired with envelope insulation and rooftop photovoltaics. Danfoss measured a 477-ton lifetime carbon saving for its VZN175 compressor, a datapoint lenders accept as collateral for discounted green mortgages.[2]Danfoss, “Solid Performance in a Volatile Year,” assets.danfoss.com Forthcoming QR-coded eco-labels will flag refrigerant climate impact, amplifying the reputational risk of sticking with fossil boilers. Building owners consequently accelerate investment decisions today to avoid costlier compliance hurdles when stricter refrigerant rules bite in 2027.

Electrification of District-Heating Networks

HOFOR plans up to 300 MW of heat-pump capacity by 2033, while Aarhus brought a 110 MW geothermal plant online in 2025, covering 20% of municipal heat.[3]HOFOR, “Heat Pump Roadmap 2033,” hofor.dk Billund reduced heat prices 25% after switching to an electrified network, providing a reference case that neighboring councils now quote in funding proposals. Fenagy’s CO₂ units already serve 130,000 Copenhagen apartments and reach a coefficient of performance of 2.7, proving large-scale viability. These mega-projects absorb scarce engineers and long-lead compressors, tightening residential supply and nudging vendors toward modular designs that ship fully wired and precharged.[4]Fenagy, “Large Heat Pumps and Cooling Systems Case Studies,” fenagy.dk District operators also prefer multi-vendor clusters to de-risk supply chains, broadening entry points for nimble specialists.

High Carbon Tax Accelerating Residential Conversions

The carbon tax on heating fuels climbed to DKK 350 (USD 54) per ton of CO₂ in 2025 and will rise to DKK 750 (USD 116) by 2030, while the electricity tax fell to a token DKK 0.8 (USd 0.06) øre per kWh for 2026-2027. A typical gas-heated household now pays an extra DKK 1,400 (USD 203) each year in carbon levies, rising to DKK 3,000 (USD 435) by 2030, whereas a heat-pump household saves DKK 1,440 (USD 209) annually in power tax. Metro Therm’s PVT-Booster shows annual savings around DKK 1,000 (USD 145), confirming a sub-five-year payback even without grants. The widening tax delta stimulates early replacement and even creates a gray market for second-hand oil boilers as owners exit fossil fuels ahead of the 2030 step-up. Installers therefore enjoy a steady pipeline of motivated customers, many of whom self-finance the retrofit from anticipated utility-bill savings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Compliance and Safety Standards | -0.3% | National, stricter in Copenhagen and Aarhus | Medium term (2-4 years) |

| Shortage of Certified Refrigeration Engineers | -0.6% | National, acute in rural Jutland and Zealand | Short term (≤ 2 years) |

| Imminent Ban on High-GWP Refrigerants Increasing Compliance Cost | -0.4% | Nationwide, aligned with EU F-gas schedule | Medium term (2-4 years) |

| Grid Congestion Costs in Rural Zealand and Jutland | -0.5% | Rural Zealand and Jutland | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Compliance and Safety Standards

EU Regulation 2024/573 caps the global-warming potential of small systems at 150 from 2027 and bans high-GWP refrigerants in monoblocks by 2032. Denmark also co-sponsors the PFAS REACH proposal, which could further narrow acceptable chemistries, while national law LBK 1036/2024 introduces third-party audits and higher seasonal performance thresholds. Compliance testing now requires accredited labs, specialized leak-detection rigs, and elaborate documentation, costs that small manufacturers struggle to absorb. The barrier to entry therefore rises, funneling share toward companies with deep regulatory benches and multi-market test facilities. Some niche brands respond by licensing compressor cores from larger peers, but this strategy compresses margins and reinforces dependence on upstream giants.

Shortage of Certified Refrigeration Engineers

Denmark registered just 5,944 F-gas technicians in 2024, and more than 60% of related EU vacancies are classified as hard to fill.[5]AREA, “European Refrigeration Technician Shortage Survey 2023-24,” area-eur.be With only 18% of workers under 30, retirements threaten to outpace new entrants, lengthening installation lead times from six to twelve weeks. Manufacturers counter with plug-and-play cartridges that reduce on-site work to four hours, enabling general contractors to finish projects under remote supervision.[6]Thermonova, “Nova Series Plug-and-Play Units,” thermonova.com Training programs, however, require multiple years to scale, so labor scarcity is likely to cap near-term growth at levels below underlying demand. Wage pressure also inflates total installed cost, partially offsetting the savings delivered by cheaper electricity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air Source Dominance, Hybrid Upside

Air source heat pumps captured 76.34% of the Denmark heat pump market share in 2025, thanks to modest upfront cost, short installation time, and proven reliability in Denmark’s temperate winters. Their extensive installer base insulates the channel from the current technician shortage, allowing vendors to sustain shipment volumes even during labor bottlenecks. However, hybrids combining a heat pump with a supplemental burner are projected to grow at a 6.31% CAGR through 2031 as households seek resilience against spot-price volatility on windy evenings. Utilities also favor hybrids in suburbs outside district-heating zones, because backup burners reduce peak-hour grid stress when wind capacity unexpectedly dips. As carbon taxes rise, the fuel-switch capability gives hybrids a transitional edge that may nibble at air source share, although absolute volumes should still favor pure electrification.

Growth within the Denmark heat pump market suggests hybrid models will cluster in single-family dwellings where existing gas networks remain functional and chimney stacks already meet safety codes. Air source manufacturers defend their lead by releasing R290-charged units that comply with 2027 GWP limits while keeping hardware costs low. Marketing campaigns now emphasize silence, compactness, and smartphone diagnostics, attributes that resonate with urban homeowners. Meanwhile, ground-source suppliers exploit the subsidy parity introduced in 2026 to pitch longer-life systems for properties with ample garden space. The resulting product mix should slowly diversify, but cost leadership and installer familiarity will ensure air source maintains numerical dominance.

By Technology: Air-to-Water Scale, Ground-to-Water Momentum

Air-to-water units delivered 54.59% of 2025 shipments, underpinned by compatibility with both radiator loops and underfloor coils commonly found in Danish housing stock. Manufacturers such as Bosch, Mitsubishi, and Panasonic supply A+++ rated models that operate reliably down to -35 °C, making them acceptable even in colder Jutland nights. Their hydraulic flexibility eases retrofit complexity, which is vital when labor shortages already stretch project timelines. Nevertheless, ground-to-water systems are projected to post a 5.02% CAGR through 2031, driven by district-heating utilities seeking superior seasonal performance and regulatory headroom for decades-long assets. Aarhus’s geothermal plant and Copenhagen’s planned aquifer projects validate the economics of deeper loops, encouraging municipalities to copy the blueprint.

Water-to-water designs also find traction where industrial wastewater or data-center effluent offers stable temperature sinks. Although these schemes remain niche, they command premium service contracts that pad vendor margins and create annuity-type revenue. Air-to-air systems hold a foothold in light commercial retrofits where ductwork already exists, but their share is capped by limited hot-water capability. Hybrid evaporation-assisted chillers round out the landscape, appealing to supermarkets that simultaneously need space cooling and freezer waste-heat recovery. Over the forecast horizon, technology choice will increasingly follow site-specific energy-price risk and refrigerant-compliance calculus rather than simple hardware cost.

By Capacity: Commercial Scale Leads, Compact Units Accelerate

Heat pumps rated 10-50 kW accounted for 32.07% of 2025 installations because schools, supermarkets, and multi-family blocks accelerated retrofits to safeguard property values ahead of the 2030 energy-class deadline. Municipalities bundle these medium-sized units into performance-contracting frameworks that lock in fixed service fees, creating predictable volume for OEMs and installers. Systems below 10 kW, however, are forecast to notch a 5.23% CAGR as factory-precharged cartridges from Nilan and Metro Therm enable quick DIY-style placements supervised remotely by certified engineers. Couples renovating 1970s oil-boiler homes particularly value this plug-and-play approach because it slashes onsite disturbance and avoids chimney decommissioning fees.

Large units in the 50-200 kW and >200 kW bands dominate district-heating and light-industrial conversions, segments led by MAN Energy Solutions and Johnson Controls. These megawatt-clusters benefit from favorable financing terms tied to proven carbon-reduction metrics, but their rollout pace is constrained by long grid-connection queues in rural zones. In response, Energinet earmarked DKK 96 billion for transmission upgrades, promising relief after 2028 and unlocking a backlog of pre-permitted projects. Until then, OEMs hedge volume risks by maintaining a diverse capacity portfolio, allowing production lines to pivot between residential cartridges and utility-scale modules as scheduling gaps appear.

By Application: Space Heating Prevails, Cooling Gathers Pace

Space heating commanded 61.21% of the Denmark heat pump market share in 2025, reflecting a climate that still demands prolonged heating seasons and a legacy building stock originally designed around hydronic radiators rather than active cooling. The segment’s sheer scale anchors the Denmark heat pump market size because almost every retrofit or new-build specification prioritizes reliable winter performance before any ancillary features are considered. Utilities and policymakers, however, now encourage reversible units as default, so each new installation quietly injects incremental cooling capability that can be monetized later if summers continue to warm. As a result, reversible products allow vendors to upsell demand-response software and time-of-use tariffs that flatten grid peaks while capturing new revenue streams from historically dormant summer months.

Space cooling is projected to expand at a 4.74% CAGR through 2031, a pace that will steadily erode heating’s percentage dominance even if absolute heating volumes keep climbing. Architects routinely specify variable-speed compressors and low-GWP refrigerants to satisfy both ecodesign noise rules and forthcoming F-gas limits, ensuring compliance is baked into each cooling-ready order. Domestic hot-water and sanitary applications remain a dependable baseline, particularly in multi-family complexes that must meet Legionella regulations with centralized storage cylinders sized for peak-hour demand. Meanwhile, industrial and process heating emerges as a showcase opportunity because breweries, data centers, and wastewater plants can harvest low-grade waste heat, creating high-profile case studies that accelerate acceptance of utility-scale equipment across broader commercial estates.

By End User: Residential Core, Commercial Catch-Up

Residential owners installed 47.58% of units in 2025, cementing households as the single largest demand driver and anchoring nearly one-half of the Denmark heat pump market size even before new construction accelerates toward the 2030 energy-class deadline. Rising carbon taxes, stricter mortgage underwriting linked to property energy grades, and a growing resale premium for A-rated homes keep household interest robust despite recent inflation in installation labor. Buyers increasingly choose plug-and-play cartridges that minimize renovation disruption, and realtors report faster closing cycles for listings that advertise smart-controlled heat pumps with verifiable efficiency certificates. These behavioral shifts suggest residential share will remain numerically dominant, though its exact percentage may taper as institutional procurement climbs.

Commercial users are projected to grow at a 4.86% CAGR to 2031, outpacing households as corporate decarbonization pledges move from aspirational press releases to audited key performance indicators. Offices, hotels, and grocery chains now benchmark scope-1 reductions against science-based targets, so heat-pump retrofits often unlock lower insurance premiums and cheaper sustainability-linked loans. Industrial participation, while episodic, involves multi-megawatt orders that swing quarterly shipment tallies and help vendors amortize R and D on high-capacity compressors. Over time, the Denmark heat pump market share will rebalance as energy-label mandates for public buildings reach enforcement, giving commercial procurement teams fresh budget justifications and pushing several thousand medium-sized sites into the bidding pipeline each year.

By Installation: Retrofit Dominance, New-Build Momentum

Retrofit projects represented 63.12% of the Denmark heat pump market share in 2025 because the country’s median dwelling age exceeds four decades and most legacy boilers now face punitive carbon levies. Streamlined digital permitting shortens approval cycles from weeks to mere hours, enabling installers to stack jobs efficiently and smooth cash flow. Property owners often bundle roof insulation, window upgrades, and photovoltaic arrays with a heat-pump swap, unlocking subsidized green loans that lower effective payback below five years even without government grants. This virtuous financing loop helps sustain retrofit leadership, yet also sows the seeds for longer-term moderation as the finite pool of eligible boilers gradually shrinks.

New-build installations are forecast to record a 5.06% CAGR through 2031 because every structure delivered after 2030 must meet energy class A, effectively making heat pumps the default HVAC option. Developers increasingly favor factory-assembled, R290-charged rooftop modules that crane directly onto plant decks, eliminating dangerous on-site refrigerant handling and compressing commissioning to a single afternoon. General contractors like the predictable sequencing such modules afford, while buyers welcome integrated monitoring dashboards that simplify warranty claims and maintenance scheduling. As residential construction rebounds from pandemic lows and mixed-use urban infill projects proliferate, the Denmark heat pump market size attributable to new builds will expand steadily, gradually closing the gap with the still-substantial retrofit base.

Geography Analysis

Copenhagen and Aarhus anchor national demand through ambitious district-heating electrification programs that allocate hundreds of megawatts in long-term tenders. Their dense housing stock, robust municipal budgets, and proximity to engineering talent ensure projects close on schedule, keeping the Denmark heat pump market size on an upward trajectory. HOFOR’s 300 MW roadmap alone could lift annual national shipments by high-single-digit percentages once procurement ramps, while Aarhus’s 110 MW geothermal plant already supplies roughly one-fifth of the city’s heat needs, validating large-scale baseload electrification.

Aalborg and Esbjerg follow closely, leveraging offshore-wind connections to power seawater and waste-heat extraction systems that deploy CO₂ refrigerants at unprecedented scale. The 70 MW Esbjerg unit commissioned in 2024 and a 177 MW build slated for 2027 position Denmark as a global reference site for mega-heat-pump engineering. Local authorities highlight these successes when pitching EU funding for port-side hydrogen hubs, thereby intertwining heating decarbonization with broader energy-transition narratives. Exporting design and operational know-how further cements Denmark’s reputation and attracts additional component suppliers to establish regional depots.

Rural Zealand and Jutland present the largest unrealized retrofit volume but grapple with grid congestion and limited installer density. Energinet’s connection queue touched 60 GW, nearly nine times peak demand, forcing a moratorium on new links in several zones and stretching project timelines. The state commits DKK 96 billion (USD 14 billion) to transmission upgrades, yet meaningful relief will materialize only after 2028, keeping near-term growth modest outside urban centers. Nonetheless, oil-to-heat-pump conversions in detached homes remain compelling once capacity frees up, promising a second adoption wave that could carry the market well into the next decade.

Competitive Landscape

The Denmark heat pump market features a layered field where global conglomerates, regional specialists, and disruptive start-ups compete across residential, commercial, and utility brackets. Danfoss integrates compressors, inverters, and controllers within one vertically consolidated platform, enabling rapid design-to-market cycles and reliable component supply. Its 2025 cash flow of EUR 734 million (USD 803 million) underwrites a EUR 503 million (USD 551 million) R&D budget aimed at natural-refrigerant innovations, reinforcing technological leadership.

Johnson Controls broke ground in July 2025 on a 2,300 m² production hall and 1,800 m² EN 14511 test center at its Holme campus, scheduled for completion in early 2026. The facility will qualify large-capacity, hydrocarbon-charged units destined for district-heating tenders and expands local employment opportunities, a politically attractive benefit. Nilan, meanwhile, acquired adjacent Hedensted plots totaling 5,000 m² in March 2026 to scale modular residential lines, signaling confidence in sustained sub-10 kW demand growth.

Fenagy, Metro Therm, and Thermonova differentiate through CO₂ or R290 architectures combined with remote-commissioning software, features that appeal when technician scarcity prolongs site visits. Industrial integrators such as MAN Energy Solutions and Alfa Laval dominate multi-megawatt deployments, bundling compressors with heat-recovery exchangers and turnkey service. Partnerships between residential OEMs and industrial heavyweights blur traditional segment borders, pushing the market toward ecosystem competition rather than single-product rivalry. As regulatory complexity and capital intensity increase, consolidation is likely, but agile niche suppliers can still thrive by owning specialized chemistries or digital workflows.

Denmark Heat Pump Industry Leaders

Trane Inc. (Trane Technologies Plc)

Danfoss A/S

LG Electronics

Daikin Industries Ltd.

Johnson Controls International Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Nilan acquired two adjoining properties in Hedensted, adding 5,000 m² of land and a 600 m² building to boost modular heat-pump output.

- March 2026: Danfoss reported record cash flow of EUR 734 million (USD 803 million) and invested EUR 503 million (USD 551 million) in R&D during 2025.

- February 2026: The Varmepumpepuljen opened with a DKK 116.9 million (USD 18.1 million) budget, offering DKK 27,000 (USD 4,190) per installation; only 10% of buyers claimed the grant.

- January 2026: Shipments of air-to-water and ground-source units reached 16,000 units in 2025, up 65% year on year, alongside 35,000 air-to-air units.

- November 2025: Aarhus activated a 110 MW geothermal plant supplying 20% of municipal heat under an Innargi and Kredsløb partnership.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Danish heat-pump market as the annual value of newly installed, electrically driven air, water, and ground-source units up to 500 kW that deliver space heating and/or sanitary hot water in residential, commercial, and light industrial premises.

District-scale plants, replacement spare parts, absorption or gas-fired hybrids, and portable air conditioner heat-pump modes are excluded.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

We interviewed installers, wholesalers, and utilities across Zealand, Jutland, and Bornholm, followed by calls with policy officers and compressor OEM engineers. Insights on average selling prices, subsidy pass-through, and likely 2026 retrofit intentions were captured and fed back to respondents for clarification, giving us confidence to fine-tune model assumptions.

Desk Research

Our analysts began by extracting baseline installation and sales counts from tier-1 public datasets such as Statistics Denmark, the European Heat Pump Association's sales barometer, Eurostat energy price files, and Danish Energy Agency subsidy bulletins. Energy performance studies from IEA-HPT journals, patent trends logged on Questel, and company financials accessed through D&B Hoovers added technology cost and revenue signals. Additional context came from investor presentations and parliament climate agreement papers. The sources listed illustrate, rather than exhaust, the secondary corpus used for cross-checks.

Market-Sizing & Forecasting

A top-down reconstruction converts EHPA unit sales and building stock heat demand profiles into value, using region-specific average selling prices validated through channel checks. Bottom-up vendor roll-ups of major suppliers' Danish revenues act as a reasonableness filter. Key drivers include: 1) yearly subsidy uptake rate under the "Skrotningsordningen" boiler scrap scheme, 2) electricity to gas retail price ratio, 3) average seasonal COP of installer best seller models, 4) share of dwellings outside district heating networks, and 5) new build floor area permits. A multivariate regression projects each driver through 2030, and scenario analysis tests COP or tariff shocks; gaps in supplier data are bridged with sampled ASPx volume proxies.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, variance checks against independent indicators, and automatic flags when quarterly subsidy disbursements diverge by +/-15%. Reports refresh annually; material policy moves trigger interim updates, ensuring clients receive the latest view.

Why Mordor's Denmark Heat Pump Baseline Commands Reliability

Published estimates differ widely because firms pick dissimilar scopes, price series, and refresh cadences.

By focusing strictly on newly installed electric units and reconciling policy-driven demand with on-ground ASP evidence, Mordor delivers a balanced, repeatable benchmark for decision makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 207.4 million (2025) | Mordor Intelligence | |

| USD 1.1 billion (2022) | Global Consultancy A | Bundles all HVAC appliances and retrofit services, inflating value and using pre-crisis price decks |

| USD 44 million (2024) | Trade Journal B | Relies solely on customs import data, omitting domestic production and installer margin layers |

These contrasts show that when scope inflation or partial data are removed, Mordor's disciplined approach yields the most transparent and dependable baseline for Denmark's heat-pump opportunity.

Key Questions Answered in the Report

How large will the Denmark heat pump market be in 2026?

The market is projected to reach USD 216.7 million in 2026 on its way to USD 268.3 million by 2031 at a 4.36% CAGR.

Which technology currently leads Danish installations?

Air-to-water systems held 54.59% of 2025 shipments and remain the mainstream retrofit choice in 2026.

What segment shows the fastest medium-term growth outlook?

Hybrid configurations are forecast to expand at a 6.31% CAGR from 2026 to 2031 as households seek resilience during spot-price swings.

Why are Danish utilities investing in mega-scale heat pumps?

Carbon taxes and electrification goals make multi-megawatt CO? systems the most cost-effective route for decarbonizing district heating.

What structural challenges could slow Danish heat-pump adoption?

A shortage of certified installers and rural grid congestion raise costs and delay projects, capping near-term growth despite strong underlying demand.

Page last updated on: