Norway Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 226.78 Million |

| Market Size (2026) | USD 230.67 Million |

| Market Size (2031) | USD 248.91 Million |

| Growth Rate (2026 - 2031) | 1.53% CAGR |

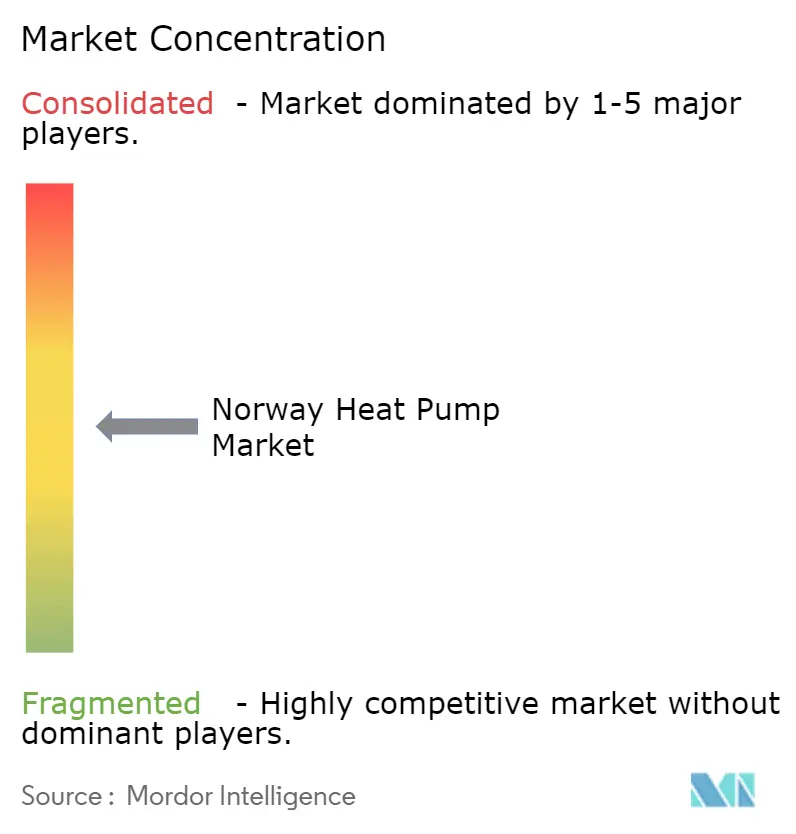

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Norway Heat Pump Market Analysis by Mordor Intelligence

The Norway heat pump market size is expected to increase from USD 226.78 million in 2025 to USD 230.67 million in 2026 and reach USD 248.91 million by 2031, growing at a CAGR of 1.53% over 2026-2031. Although the headline expansion appears modest, the market already enjoys more than 96% penetration in new heating-system sales and serves over one-half of Norwegian households, limiting pure volume upside. Carbon taxation of NOK 2,000 (USD 188) per tonne of CO₂, coupled with a nationwide ban on new oil-fired boilers effective January 2027, sustains technology preference, yet incremental demand now comes mainly from industrial high-temperature projects and mandated renewable heating in new construction. Asian manufacturers are expanding Nordic footprints, while local innovators commercialize helium-based Stirling-cycle units that reach 250 °C output, carving out process-heating niches. Installer shortages north of the Arctic Circle and single-phase grid constraints in rural municipalities temper adoption speed, channeling policy instruments toward demand-response capability and hybrid system design.

Key Report Takeaways

- By installation, retrofit projects commanded 62.43% revenue in 2025, while new-build activity is projected to advance at a 1.72% CAGR through 2031.

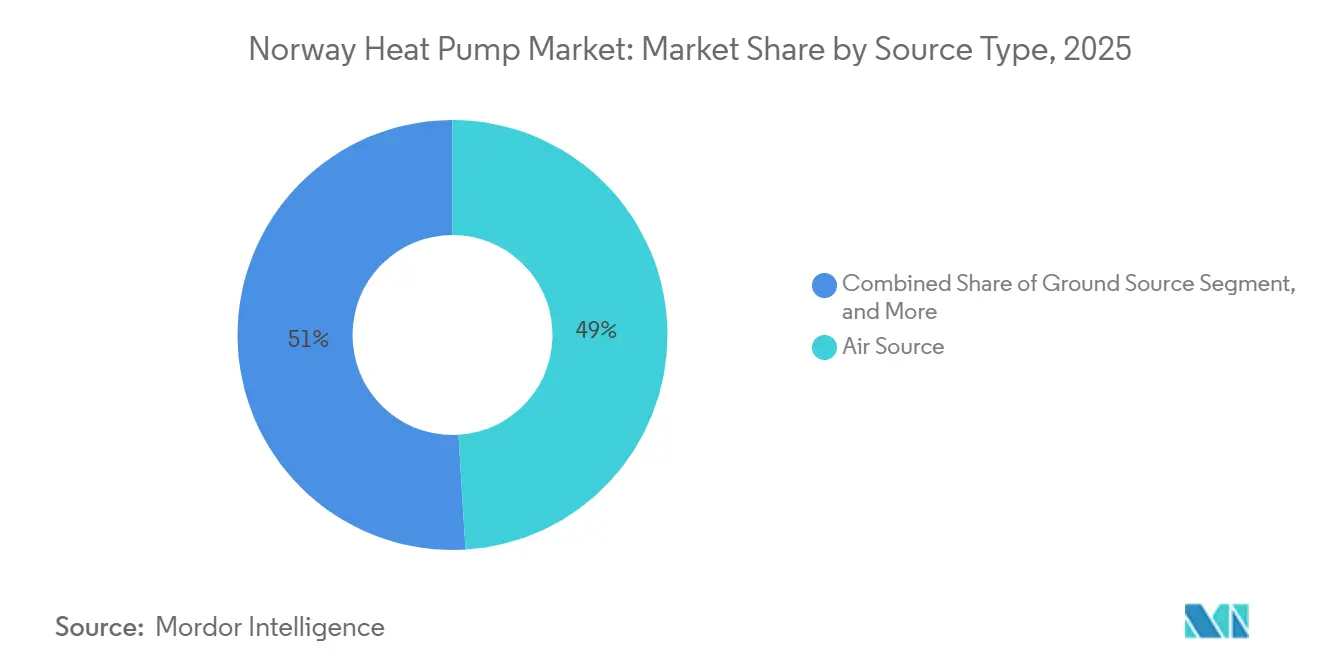

- By source type, air-source units captured 49.03% of 2025 revenue, whereas hybrid configurations are forecast to expand at a 2.47% CAGR to 2031.

- By application, space heating accounted for 50.16% share of the Norway heat pump market size in 2025 and is advancing at a 1.53% CAGR through 2031; industrial process heating is the fastest-growing segment at 2.13% over the same horizon.

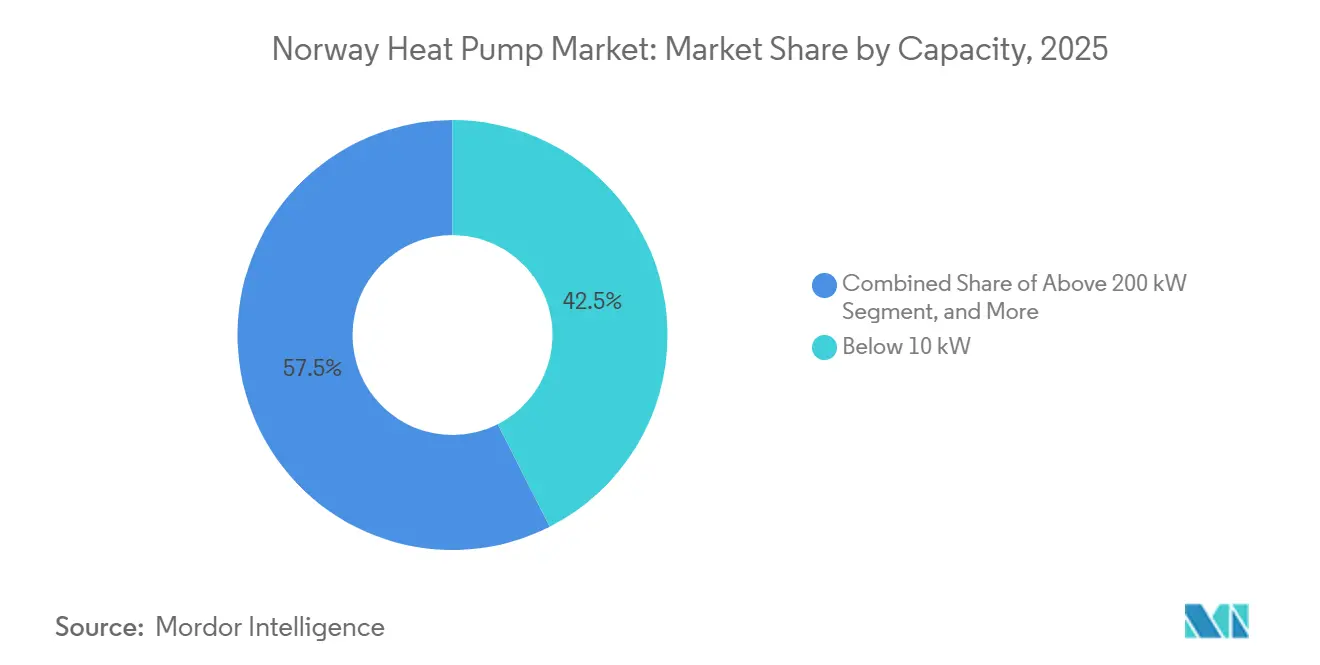

- By capacity, units above 200 kW represented the quickest growth trajectory with a 1.96% CAGR, yet systems below 10 kW retained 42.53% share of the Norway heat pump market size in 2025.

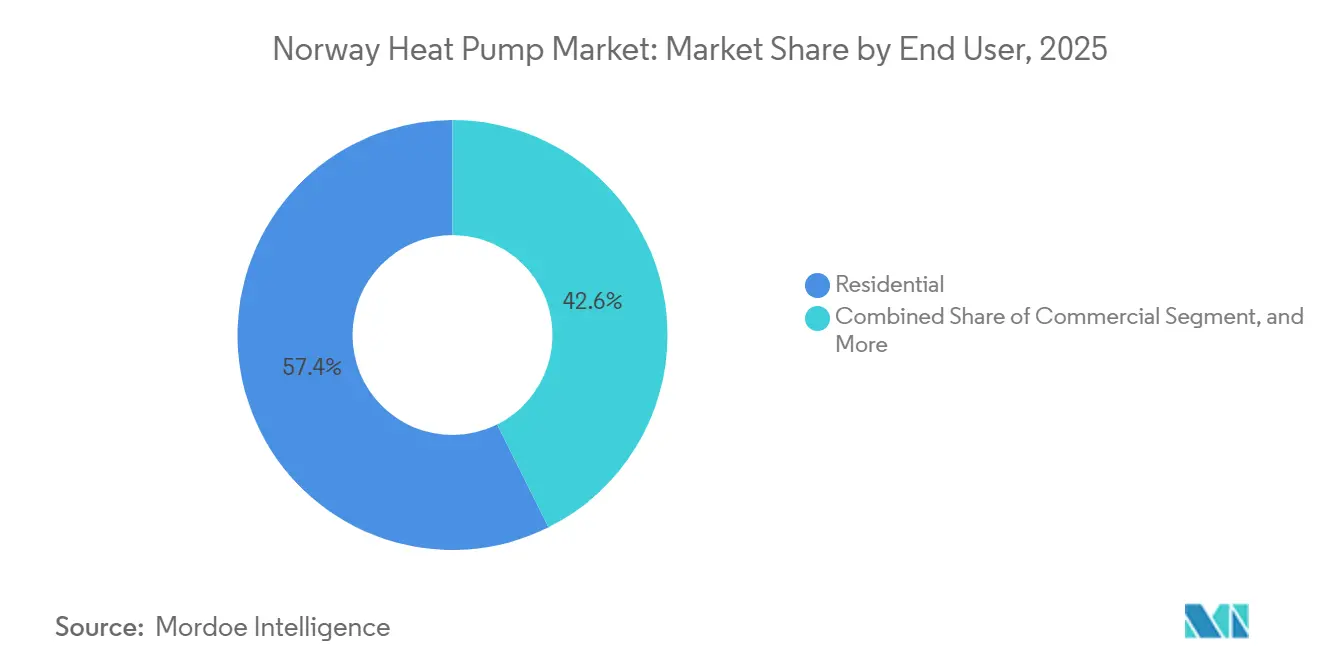

- By end user, residential deployments held 57.37% revenue share in 2025, while industrial users recorded a 1.89% CAGR outlook to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Norway Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Hour-Ahead Spot Prices Enhancing Heat-Pump Payback | +0.4% | National, acute in southern grid zones NO1 and NO2 | Short term (≤ 2 years) |

| Decarbonization Targets Embedded in Norway's 2027 Climate Action Plan | +0.3% | National, strongest in Oslo, Bergen, Trondheim | Medium term (2-4 years) |

| Mandatory Ban on New Oil-Fired Boilers Effective 1 Jan 2027 | +0.2% | National, legacy impact in rural municipalities | Short term (≤ 2 years) |

| Grid-Operator Rebates for Demand-Response Ready Units | +0.2% | Oslo, Trondheim, Stavanger pilots | Medium term (2-4 years) |

| Pilots for Heat-Pump Integration with District-Heating Return Loops | +0.2% | Oslo, Bergen, Drammen | Long term (≥ 4 years) |

| Lowered Borehole Drilling Fees Stimulating Ground-Source Adoption | +0.1% | Suburban and rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge In Hour-Ahead Spot Prices Enhancing Heat-Pump Payback

Nord Pool day-ahead electricity prices spiked above NOK 1.50 (USD 0.14) per kWh during the 2024-2025 winter. By contrast, heat pumps with coefficients of performance between 3.0 and 5.0 deliver heat at NOK 0.30-0.50 (USD 0.03-0.05) per kWh, undercutting direct electric resistance by 60-70%.[1]Nord Pool, “Nord Pool Spot Prices,” nordpoolgroup.com Capacity-based distribution tariffs introduced in 2025 further reward households that shift compressor operation to off-peak hours, trimming monthly grid charges of NOK 400-600 (USD 38-56). Smart thermostats linked to the NorFlex demand-response platform automate load shifting, compressing simple payback for an air-source retrofit in Southern Norway to under four years.

Decarbonization Targets Embedded In Norway's 2027 Climate Action Plan

The 55% greenhouse-gas reduction goal versus 1990 levels has reframed heat pumps as compliance instruments for municipal building portfolios. A carbon tax that reached NOK 2,000 (USD 188) per tonne in 2026 levies an extra NOK 5-6 per liter on heating oil, shrinking payback periods for air-source systems in coastal zones.[2]Enova, “Support for Heat Pumps,” enova.no District-heating operators must lift renewable input to 60% by 2028, catalyzing pilots that reclaim low-grade heat from sewage, data centers, and cooling loops through 1-3 MW heat pumps delivering 40-60 °C supply temperatures. Procurement tenders increasingly cite ISO 14001 credentials, edging the market toward vendors that verify embedded carbon savings.

Mandatory Ban on New Oil-Fired Boilers Effective 1 Jan 2027

Fewer than 5% of households still rely on oil heating, yet the prohibition now bites in commercial warehouses and fish-processing plants. Operators choose hybrid systems pairing a downsized heat pump with gas or biomass backup to meet peak loads without breaching the ban. Enova subsidies of up to NOK 55,000 (USD 5,156) for combined ground-source and air-to-water packages accelerate uptake, while shuttered rural fuel depots remove a logistical lifeline for legacy boilers, nudging even reluctant owners toward electrification.[3]Norwegian Ministry of Climate and Environment, “Climate and Environment,” regjeringen.no

Grid-Operator Rebates for Demand-Response Ready Units

Statnett earmarked NOK 150-200 billion (USD 14.1-18.8 billion) for grid reinforcement through 2034. To delay substation upgrades, distribution companies pay households NOK 1,000-3,000 (USD 94-281) annually for installing OpenADR-enabled controllers that curtail load at peak times. Although only 10% of smart meters have active HAN ports, the stipend offsets 20-30% of annual maintenance costs, making demand-response capability a tangible selling point. Misaligned incentive structures, monthly peak calculations versus hourly price optimization, still limit aggregate grid relief, highlighting the need for unified tariff design.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Upfront Costs Still > NOK 160,000 for Deep Retrofit Cases | -0.4% | Pre-1980 housing stock nationwide | Short term (≤ 2 years) |

| Limited Three-Phase Supply in Rural Municipalities | -0.3% | Inland and northern rural areas | Medium term (2-4 years) |

| Shortage of Certified F-Gas Installers in Northern Counties | -0.2% | Troms, Finnmark, Nordland | Long term (≥ 4 years) |

| Consumer Concerns over Frost-Related Noise Levels Below -15 °C | -0.1% | High-latitude inland zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Upfront Costs Still above NOK 160,000 for Deep Retrofit Cases

Ground-source retrofits in uninsulated pre-1980 homes regularly surpass NOK 200,000 (USD 18,800) owing to borehole drilling and radiator swaps, while Enova’s NOK 40,000 (USD 3,750) grant covers only one-fifth of that outlay. The financing gap deters households earning below NOK 600,000 (USD 56,400), a group disproportionately concentrated in rural municipalities where heating loads are highest. Rising policy rates of 4.5% in 2025 curbed home-equity borrowing, leaving energy-poor consumers locked into direct resistance heating despite escalating electricity tariffs.[4]Norges Bank, “Central Bank Policy Rates,” norges-bank.no

Limited Three-Phase Supply In Rural Municipalities

Roughly 300,000 km of distribution lines leave many rural dwellings on single-phase 230 V service, capping continuous loads at 10-12 kW. Whole-house air-to-water units need 15-20 kW at peak, forcing installers to integrate fossil or biomass backups. Upgrading a property to three-phase costs NOK 50,000-150,000 (USD 4,700-14,100), undermining the economics of deep retrofits. Distribution companies prioritize industrial loads for transformer capacity, placing residential upgrades into multiyear queues that stall adoption in the coldest inland municipalities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Hybrid Adoption Outpaces Stand-Alone Models

Hybrid systems integrating heat pumps with fossil or biomass backups are forecast to expand at a 2.47% CAGR, the fastest rate among source types, as rural grid constraints favor flexible peak-load coverage. Air-source units secured 49.03% of revenue in 2025 on the strength of average installed costs near NOK 155,000 (USD 14,570) and straightforward permitting, sustaining the Norway heat pump market leadership despite efficiency losses below -10 °C. Ground-source packages, although dearer at NOK 200,000-250,000 (USD 18,800-23,500), deliver seasonal COP values of 3.5-5.0 and pair well with new-build basements where drilling can coincide with foundation work.

Hybrid system deployment is most pronounced in commercial grain-drying, aquaculture, and food-processing plants that balance a 100-300 kW heat pump against a biomass or gas boiler. Case in point, Felleskjøpet’s Trondheim grain terminal installed a 1.5 MW Aneo unit in 2024 that cuts gas use by 70%, while the boiler provides redundancy during arctic cold snaps. Such configurations position hybrids to capture incremental Norway heat pump market share in industrial conversions through 2031.

By Technology: Ground-To-Water Drives Innovation Momentum

Ground-to-water configurations are projected to grow at a 2.02% CAGR, buoyed by stabilized drilling fees and promising seasonal storage pilots that charge bedrock during summer. Air-to-air heat pumps retained 47.18% revenue in 2025, their ductless simplicity suiting coastal apartments with modest loads, yet performance fades inland where design temperatures reach -25 °C. Air-to-water units remain the retrofit workhorse, feeding existing radiator circuits with 50-60 °C water, albeit at lower COP below -10 °C.

Tromsø’s 2024 UTES project achieved a seasonal COP above 4.0 by storing 120 °C waste heat underground for winter retrieval, a template now under feasibility study in Bergen and Drammen. Manufacturers respond to the evolving regulatory climate: Mitsubishi Heavy Industries unveiled R290 systems in December 2025, aligning with F-gas phase-out rules, while Midea’s dual-compressor Raynor series holds rated output down to -25 °C, targeting inland homeowners.[5]Mitsubishi Heavy Industries, “R290 Heat Pump Models,” mhi.com These advances reinforce the Norway heat pump market position of ground-coupled and propane-charged technologies as F-gas restrictions tighten.

By Capacity: Industrial-Scale Units Gain Ground

Units exceeding 200 kW are set to climb at a 1.96% CAGR as the carbon tax penalizes steam boilers. Nevertheless, sub-10 kW equipment still generated 42.53% of revenue in 2025, mirroring Norway’s 2.7 million homes with average 8,000-15,000 kWh heat demand. The 10-50 kW band services larger residences and small commercial properties, whereas 50-200 kW machines populate schools, offices, and light factories.

Enerin installed 400 kW helium-based prototypes at GE Healthcare’s Lindesnes plant and Pelagia’s fish facility in 2024-2025, validating high-temperature performance with COP values up to 2.16. The AdO Arena in Bergen adopted a 170 kW CO₂ heat pump that recovers rink refrigeration waste heat, underscoring crossover potential between cooling and heating applications. Such projects elevate large-capacity solutions in the Norway heat pump market hierarchy for industrial decarbonization.

By Application: Process Heating Outpaces Space Heating

Space heating contributed 50.16% of 2025 revenue yet advances merely in line with the overall 1.53% CAGR because of nearly saturated residential coverage. Industrial process heating, by contrast, is forecast at 2.13% as plants seek alternatives to fossil-fired steam. Domestic hot water continues to hitchhike on combined systems, while space cooling stays marginal given Norway’s temperate climate.

Felleskjøpet’s 1.5 MW installation generates 10-bar steam for feed processing, reflecting a broader migration toward 150-250 °C heat pumps that comply with looming F-gas and ammonia safety codes. The Norway heat pump market size attached to process heating should therefore register the highest incremental contribution across applications through 2031.

By End User: Industrial Growth Outstrips Residential Base

Residential customers held 57.37% revenue in 2025, but replacements dominate as first-generation units installed between 2005 and 2010 reach end-of-life. Industrial users are forecast at a 1.89% CAGR, buoyed by carbon-tax pass-through costs and the emergence of COP-favorable helium and transcritical CO₂ systems. Commercial buildings occupy the midpoint, their outlook tied to 500 m² new-build code thresholds mandating renewable heating.

LG’s USD 93.3 million purchase of OSO in June 2025 exemplifies vertical integration that links storage tanks with demand-response software to stretch grid capacity. Panasonic’s EUR 320 million (USD 349 million) Czech plant expansion will deliver R290 inventory tailored for the Norway heat pump market, and Daikin’s 2025 takeover of Swedish service network Kylslaget reinforces post-installation support where F-gas certification is non-negotiable.

By Installation: Retrofits Dominate Yet New-Builds Accelerate

Retrofit activity supplied 62.43% of 2025 turnover, reflecting the replacement of direct electric resistors in existing dwellings. New-build growth at 1.72% CAGR benefits from ability to coordinate drilling, foundation work, and hydronic design upfront, compressing lead times to six weeks in suburban communities. Billingstad Energy Center’s 2 MW CO₂ system feeding 4,000 residents illustrates scale economies when thermal infrastructure is baked into master planning.

Conversely, deep retrofits in pre-1980 stock demand radiator swaps, insulation improvement, and sometimes service-panel upgrades, driving costs above NOK 200,000 (USD 18,800). The lack of low-interest green loans, unlike Sweden and Finland, slows conversion rates among rural and lower-income households, thereby capping retrofit expansion in the Norway heat pump market.

Geography Analysis

Urban southern municipalities such as Oslo, Bergen, Stavanger, and Trondheim anchor the Norway heat pump market owing to milder -10 °C to -15 °C winter design temperatures, widespread three-phase supply, and proximity to the country’s 12 refrigeration-training schools that replenish the certified technician pool. District-heating networks clustered in these cities are piloting 1-3 MW heat pumps that recover data-center and sewage-plant waste heat, while seasonal storage demonstrations like USES4HEAT in Furuset promise to smooth summer-winter load imbalances.

Inland regions across Hedmark, Oppland, and Trøndelag face -20 °C to -25 °C design temperatures that erode air-source COP, steering adopters toward ground-source or hybrid systems. Single-phase supply caps, coupled with NOK 50,000-150,000 (USD 4,700-14,100) upgrade costs, dampen economics, and local building authorities unfamiliar with bedrock thermal-response testing often add six-week permitting delays. The Norway heat pump market share for hybrid systems is therefore set to climb fastest in these colder inland municipalities.

Northern counties Troms, Finnmark, and Nordland present compounded obstacles: installer scarcity, 10-20 week project backlogs, and 30-40% higher labor costs due to travel premiums. Tromsø’s UTES project validates sub-Arctic ground-source viability, but scaling hinges on expanding local F-gas training beyond the single 15-seat Ishavsbyen videregående program. Coastal Nordland enjoys maritime moderation, yet the same workforce bottleneck produces a two-tier adoption pattern in which commercially funded retrofits proceed, while lower-income households defer upgrades, limiting the Norway heat pump market penetration in high-latitude zones.

Competitive Landscape

No manufacturer exceeds 15% share, rendering the Norway heat pump market moderately concentrated yet fiercely competitive. Nordic incumbents NIBE and Viessmann defend market presence via established installer networks and warranty structures tied to F-gas certification. Mitsubishi Electric and Daikin differentiate through OpenADR-enabled controllers that qualify for grid-operator rebates. LG leverages its June 2025 OSO acquisition to bundle heat pumps with storage tanks, smoothing peak load and fortifying demand-response compatibility. Panasonic’s Czech plant expansion to 1.4 million units annually by 2030 introduces scale economics on propane-charged units that comply with upcoming R32 phase-outs.

Emergent players focus on high-temperature process heating. Enerin secured NOK 180 million (USD 16.9 million) in December 2025 to scale 250 °C helium-Stirling technology, recording COP values up to 2.16 in GE Healthcare and Pelagia pilots. HEATEN, backed by Advent International, readies the 50 MWth HeatBooster for aquaculture and chemical applications, banking on the NOK 2,000 (USD 188) per-tonne carbon tax to deliver sub-three-year paybacks. Compliance with ISO 5149 ammonia and CO₂ safety codes plus R290-friendly product lines becomes a strategic moat as F-gas quotas tighten. Installer fragmentation, only 4,037 certified technicians nationwide, continues to favor manufacturers offering in-house service capability or strong third-party alliances, preserving brand loyalty in a replacement-driven Norway heat pump market.

Norway Heat Pump Industry Leaders

Fujitsu Limited

Daikin Industries Ltd

NIBE Industrier AB (NIBE Group)

Mitsubishi Electric Corporation

LG Electronics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Enerin raised NOK 180 million (USD 16.9 million) to scale helium-based Stirling-cycle production targeting 250 °C industrial steam.

- December 2025: Mitsubishi Heavy Industries introduced Nordic-oriented R290 models that maintain rating at -25 °C.

- December 2025: Midea launched the Raynor series with dual-compressor architecture and built-in grid-response interfaces.

- August 2024: Panasonic committed EUR 320 million (USD 349 million) to expand Czech heat-pump manufacturing to 1.4 million units annually by 2030.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Norwegian heat pump market as all revenue from factory-built air-source, ground-source, water-source, and exhaust-air units that provide space heating, cooling, or domestic hot water to residential, commercial, institutional, and light-industrial buildings. According to Mordor Intelligence, standalone heat-pump water heaters and district or utility-scale (>100 kW) plants sit outside this boundary.

Scope Exclusions: Revenues from maintenance contracts, spare parts, and large industrial process heat pumps are excluded.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed installers, component makers, municipal energy advisers, and rebate administrators across Oslo, Bergen, Tromso, and Trondheim. The dialogues clarified replacement cycles, typical installed costs, and near-term regulatory shifts, letting us adjust desk-based price and volume assumptions before finalizing the model.

Desk Research

We anchored volumes with publicly available data sets from Statistics Norway, Eurostat energy balances, the Norwegian Water Resources and Energy Directorate's electricity-price bulletins, and Norwegian Customs import codes for compressors and refrigerants. Trade bodies such as the European Heat Pump Association and the Norwegian Heat Pump Association contributed yearly installation and stock counts, while peer-reviewed papers on cold-climate COP performance supplied efficiency norms. Company 10-Ks, investor decks, and reputable press gave price corridors and channel trends; to deepen coverage, our team tapped D&B Hoovers for manufacturer financials and Dow Jones Factiva for archived distributor announcements. These sources illustrate, not exhaust, the desk research pool consulted.

Market-Sizing & Forecasting

A top-down build started with Norway's heated floor space and dwelling stock, applied penetration and replacement ratios, and multiplied by verified average selling prices. Bottom-up roll-ups from sampled suppliers and distributor checks then tested totals and corrected bias. Key drivers fed into the model include heating-degree days, electricity-to-oil price spreads, new-build completions, rebate uptake, and compressor cost trends. Forecasts rely on multivariate regression with scenario analysis, and every coefficient is benchmarked with primary-research consensus prior to lock-in.

Data Validation & Update Cycle

Outputs pass analyst self-checks, peer audits, and senior sign-off. Any variance exceeding +/-5% versus independent indicators triggers a re-engagement of sources. Reports refresh annually, with interim revisions when material policy or energy price shocks occur, ensuring clients receive the latest view.

Why Mordor's Norway Heat Pump Baseline Earns Confidence

Published figures often diverge because firms define scope, price baskets, and refresh cadences differently, and we acknowledge that at the outset.

Key gap drivers show that other publishers bundle heat-pump water heaters, include aftermarket services, or extrapolate regional averages into Norway, whereas Mordor limits scope to packaged space-conditioning units, applies locally surveyed ASPs, and updates models every twelve months with fresh exchange rates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 223.4 million (2024) | Mordor Intelligence | - |

| USD 770.1 million (2024) | Global Consultancy A | Bundles water-heater units and service revenues; uses Nordic-wide ASPs |

| USD 1.1 billion (2022) | Specialist Analyst B | Covers thermally driven and large industrial systems; older base year rolled forward without 2024 policy revision |

The comparison underscores that our Norway-specific pricing, tighter scope, and frequent updates provide a balanced, transparent baseline that decision-makers can trace and replicate with confidence.

Key Questions Answered in the Report

How large is the Norway heat pump market in value terms today?

The Norway heat pump market size reached USD 226.78 million in 2025 and is projected at USD 230.67 million for 2026.

What annual growth rate is expected for Norwegian heat pump sales through 2031?

Aggregate revenue is forecast to climb at a 1.53% CAGR over 2026-2031.

Which source type is expanding fastest in Norway?

Hybrid configurations that pair heat pumps with backup boilers are advancing at a 2.47% CAGR on the back of rural grid constraints and industrial flexibility needs.

Why are industrial users adopting heat pumps more aggressively now?

A NOK 2,000 (USD 188) per-tonne carbon tax and the arrival of 150-250 °C high-temperature units deliver sub-three-year paybacks when replacing steam boilers.

Are installer shortages impacting adoption in northern Norway?

Yes, Troms, Finnmark, and Nordland face technician backlogs of up to 20 weeks and 30-40% higher labor costs, delaying projects despite favorable economics.

How will F-gas regulation shape product offerings after 2027?

The phase-out of R32 propels manufacturers toward natural refrigerants such as propane, CO?, and ammonia, resulting in multiple R290 and transcritical systems already launched for the Norwegian climate.

Page last updated on: