Germany Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.19 Billion |

| Market Size (2026) | USD 3.33 Billion |

| Market Size (2031) | USD 4.02 Billion |

| Growth Rate (2026 - 2031) | 3.84% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Heat Pump Market Analysis by Mordor Intelligence

The Germany heat pump market size is expected to increase from USD 3.19 billion in 2025 to USD 3.33 billion in 2026 and reach USD 4.02 billion by 2031, growing at a CAGR of 3.84% over 2026-2031. Adoption accelerated in 2024-2025 when installations jumped 55% year on year, enabling heat pumps to supply 47% of residential space-heating demand and overtaking gas boilers as the default option for new construction and deep retrofits. Federal law now requires that at least 65% of heating energy in new and substantially renovated buildings comes from renewables, effectively hard-coding heat pump leadership through 2045. The European Union’s emissions-reduction timetable and the looming 2027 ban on high-GWP refrigerants are steering capital toward propane-based models even as only a few manufacturers can currently produce them at scale. Grid constraints and propane supply volatility will temper percentage growth in the short run, yet they also motivate hybrid configurations, demand-response programs, and installer-training investments that reinforce the long-term trajectory of the Germany heat pump market.

Key Report Takeaways

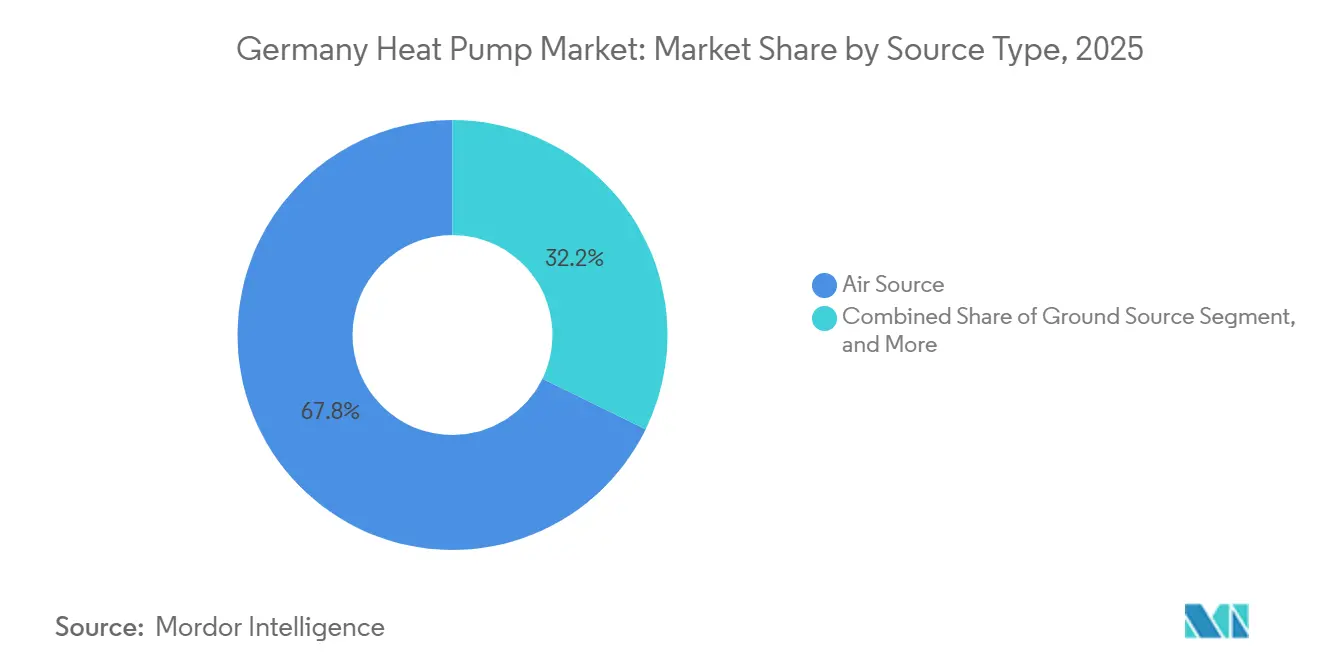

- By source type, air-source systems accounted for 67.78% of the Germany heat pump market share in 2025, while hybrid air-source plus gas boilers are projected to expand at a 5.61% CAGR through 2031.

- By technology, air-to-water units led with 59.31% revenue share in 2025, yet ground-to-water solutions are forecast to register the fastest 5.02% CAGR between 2026-2031.

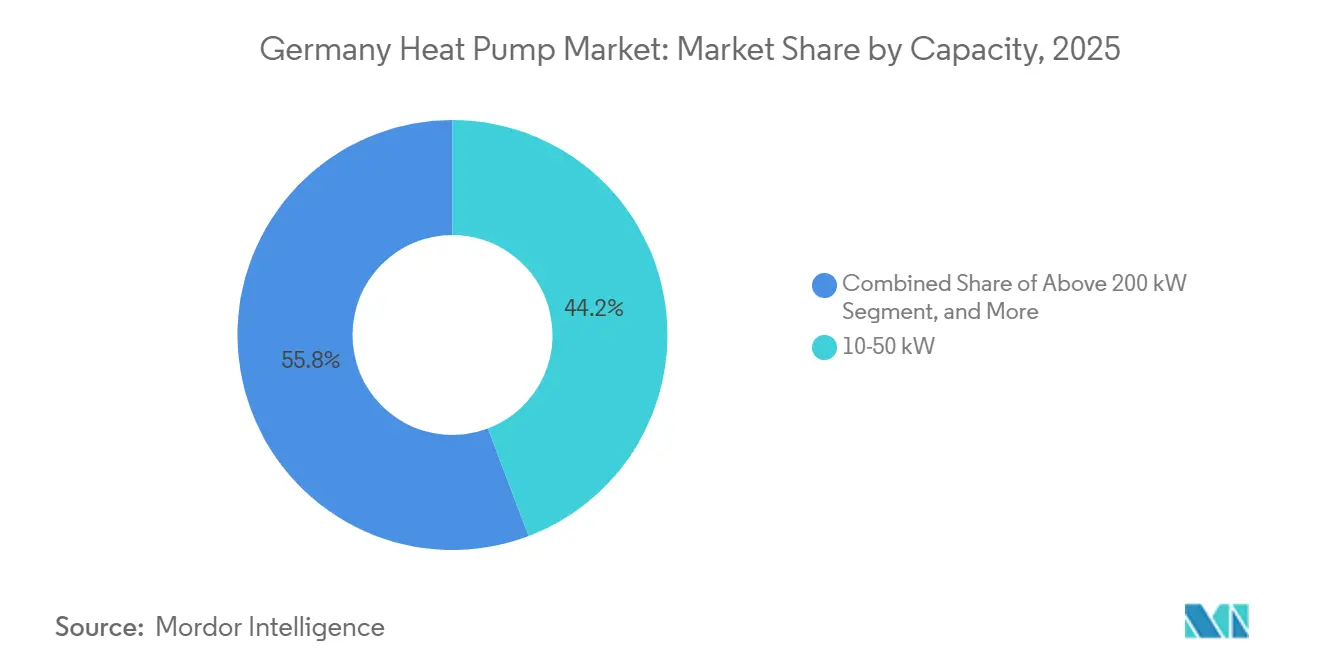

- By capacity, the 10-50 kW band held 44.23% of the Germany heat pump market size in 2025, whereas systems above 200 kW are the quickest-growing tier at a 4.72% CAGR to 2031.

- By application, space heating represented 52.72% of revenue in 2025, and industrial process heating is advancing at a 4.16% CAGR over 2026-2031.

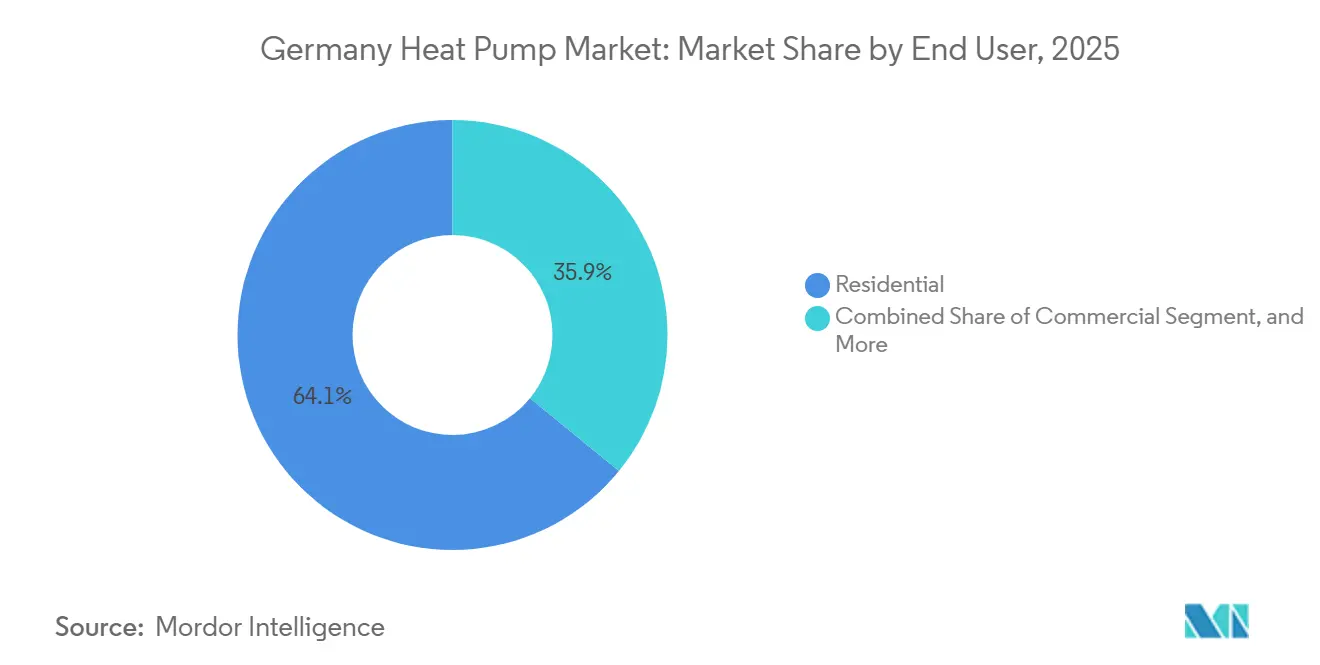

- By end user, residential installations captured 64.09% share in 2025, while industrial users mark the highest 3.97% CAGR outlook.

- By installation type, retrofits led with 54.43% of 2025 volume, yet new-build projects are on track for a 4.37% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Heat Pump Market Trends and Insights

Drivers Impact Analysi*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust Federal and State Subsidies, Tax-Credit Schemes | +1.2% | Nationwide, strongest in Baden-Württemberg, Bavaria, North Rhine-Westphalia | Short term (≤ 2 years) |

| Rising Demand for High-Efficiency Heating and Cooling | +0.9% | Urban centers with dual-use needs | Medium term (2-4 years) |

| EU Fit-for-55 Decarbonization Targets and Electrification Push | +0.8% | National, aligned with EU milestones | Long term (≥ 4 years) |

| Surge in Low-Noise Air-to-Air Heat Pumps for Multi-Family Retrofits | +0.6% | Berlin, Hamburg, Munich, Cologne, Frankfurt | Medium term (2-4 years) |

| Smart-Grid Demand-Response Incentives From German TSOs | +0.4% | Grid-constrained regions, notably Bavaria and Lower Saxony | Medium term (2-4 years) |

| EU Component Near-Shoring Driven by Supply-Chain Resilience Policies | +0.3% | Domestic plants with spillovers across the EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Federal and State Subsidies, Tax-Credit Schemes

Germany’s BEG program disbursed EUR 3.8 billion (USD 4.3 billion) in heat-pump grants during 2025, underwriting up to 70% of eligible costs for qualifying households.[1]Bundesamt für Wirtschaft und Ausfuhrkontrolle, “BEG Subsidy Guidelines 2025,” BAFA.DE Payback periods compressed to four-to-six years, tipping the cost equation decisively away from gas boilers.[2]Fraunhofer ISE, “Heat Pump Efficiency Study 2025,” ISE.FRAUNHOFER.DE State top-ups in Baden-Württemberg and Bavaria further sweeten the economics for ground-source and district-connected systems. Bundling incentives with building-envelope upgrades and rooftop photovoltaics can push combined subsidies past EUR 50,000 (USD 56,500) per project, a level that has spawned a consultancy niche to navigate the complex approval pipeline Although administrative friction remains, the magnitude and duration of the grant architecture underpin demand through the decade.

Rising Demand for High-Efficiency Heating and Cooling

Climate adaptation is now a mainstream buying trigger: dual-use units capable of cooling captured 38% of residential installs in 2026, up from 22% two years earlier.[3]Bundesverband Wärmepumpe, “Heat Pump Market Data Germany 2025,” BWP.DE Southern states enduring heatwaves above 35 °C favor air-to-air models with seasonal performance factors over 4.5. Commercial buyers specify variable-speed compressors that slice peak load by nearly 30% while sharpening zone control. Propane-charged systems add another 8-12% efficiency lift versus R410A predecessors, satisfying ESG scorecards. Impending 2027 Ecodesign thresholds will lock these performance gains into regulatory minimums.

EU Fit-for-55 Decarbonization Targets and Electrification Push

Germany must swap roughly six million fossil boilers for heat pumps by 2030 to stay within its sectoral carbon budget . Municipal heat-planning laws compel cities to map heat-pump zones by 2026-2028, catalyzing district-scale projects and private retrofits alike. Gas-grid expansion no longer earns regulated cost recovery, steering all new housing toward all-electric designs. Capital is following policy: Bosch alone has earmarked more than EUR 1 billion (USD 1.13 billion) for heat-pump R&D and manufacturing through 2026. The synchrony of EU and national mandates therefore continues to accelerate the Germany heat pump market.

Surge in Low-Noise Air-to-Air Heat Pumps for Multi-Family Retrofits

Façade-integrated units operating below 35 dB now unlock densely populated districts previously off-limits due to acoustic limits. Compact outdoor modules under 60 kg simplify balcony and rooftop installs, trimming labor hours by 40%. Updated tax rules allow landlords to depreciate retrofit costs more rapidly, aligning owner-tenant incentives. Coupled with the GEG’s 65% renewable-heat stipulation, municipalities are fast-tracking permits that effectively mandate heat pumps in multi-family renovations. This combination of technical breakthroughs and policy nudges is set to deepen penetration across Germany’s 19 million apartment units.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent F-Gas and Safety Compliance Requirements | -0.7% | Nationwide, stricter in Baden-Württemberg and Hesse | Short term (≤ 2 years) |

| Shortage of Certified Installers and HVAC Technicians | -0.9% | Rural areas and eastern federal states | Medium term (2-4 years) |

| Rural Distribution-Grid Congestion | -0.5% | Bavaria, Lower Saxony, Mecklenburg-Vorpommern, Brandenburg | Medium term (2-4 years) |

| Propane (R290) Refrigerant Supply Bottlenecks | -0.4% | Dependent on EU petrochemical hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent F-Gas and Safety Compliance Requirements

The 2027 ban on refrigerants with GWP above 150 forces a pivot to propane, classified as highly flammable, adding EUR 300-500 (USD 339-565) per unit in compliance outlays for safety features and installer certifications. Smaller OEMs lack the engineering depth to redesign quickly and are instead merging or exiting, narrowing consumer choice. Germany’s occupational-safety authority mandates extra training and leak-detection gear, stretching installer capacity still further. Legacy R410A and R32 systems risk becoming orphaned as production quotas ratchet down, a prospect that dampens near-term retrofit demand. Until supply chains normalize around R290, compliance drag will shave momentum from the Germany heat pump market.

Shortage of Certified Installers and HVAC Technicians

Only 12,000 VDI-certified technicians graduated in 2025, versus the 25,000 needed annually to hit installation targets.[4]Verein Deutscher Ingenieure, “VDI 4645 Certification Standards,” VDI.DE Wait times exceed 18 months in Brandenburg and Mecklenburg-Vorpommern, eroding the value of subsidies that expire if work is not completed within two years. Labor now consumes up to 65% of project budgets in complex retrofits. Manufacturers are investing heavily in academies, yet most new capacity will not arrive before 2028.[5]Stiebel Eltron, “Höxter Plant Expansion Press Release,” STIEBEL-ELTRON.COM The installer bottleneck therefore remains the single most immediate cap on growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Hybrid Configurations Extend Air-Source Leadership

Air-source units produced 67.78% of 2025 revenue in the Germany heat pump market, retaining pole position through a mix of moderate upfront cost and straightforward installation that suits most retrofit projects . Hybrids pairing an air-source module with a condensing gas boiler are forecast to deliver the fastest 5.61% annual growth, because they meet the 65% renewable-heat rule while insulating owners from potential electricity-price spikes. Water-source and ground-source solutions remain niche, yet the federal subsidy bonus for geothermal systems narrows the cost gap and is drawing interest from municipalities that need baseload heat for dense districts.

Hybrid momentum also reflects technological refinements: Vaillant’s aroTHERM plus calibrates fuel switching in real time, while Daikin’s flow-temperature boost to 70 °C removes the need for radiator changes in older homes. Policymakers amplify the trend by allowing dual-fuel systems to qualify for full BEG grants once the heat pump supplies two-thirds of annual load, effectively pushing legacy boilers into backup status. As a result, hybrids are expected to lift their Germany heat pump market share each year through 2031, even while pure air-source units keep dominating overall shipments.

By Technology: Ground-to-Water Climbs on District-Heating Demand

Air-to-water systems controlled 59.31% of 2025 sales, underpinned by mature supply chains and installer familiarity. Yet ground-to-water units are projected to grow 5.02% per year, faster than the 3.84% aggregate, because drilling costs fall sharply when district-heating operators connect hundreds of buildings to a shared bore-field. Water-to-water designs occupy an industrial niche tied to process heat and swimming pools, whereas air-to-air splits are winning multi-family retrofits that need low-noise facade units.

Federal subsidies add five extra percentage points for geothermal systems that achieve seasonal performance factors above 4.0, bringing total support to as high as 70% of project cost. Hamburg’s 4 MW air-source plant and Cologne’s 150 MW geothermal contract exemplify how city utilities are scaling diverse technologies to decarbonize legacy steam networks. Incremental upgrades, such as Viessmann’s R290 revision of its Vitocal line, help air-to-water incumbents defend share, but the longer-term upswing in district networks tilts incremental Germany heat pump market size toward ground-centric architectures.

By Capacity: Megawatt-Scale Units Register the Quickest Upside

The 10-50 kW bracket represented 44.23% of sales in 2025, reflecting its suitability for single-family and small multi-family dwellings. Systems above 200 kW, though smaller in absolute volume, are forecast to advance 4.72% annually as industrial users and city utilities deploy high-temperature units capable of 130 °C steam.[6]SPH Sustainable Process Heat, “ThermBooster Technical Specifications,” SPH.DE Below-10 kW machines cover compact apartments and serve as modular building blocks that installers cascade for redundancy, while the 50-200 kW class fits supermarkets and offices hunting combined heating-and-cooling savings.

Large-capacity growth is catalyzed by federal grants that refund up to 40% of capital outlays and by demand-response income that operators earn for grid services. MVV Mannheim’s 165 MW Rhine project underscores the shift, showing how a single installation can expand the Germany heat pump market size materially in one step. Meanwhile, intense competition in the 10-50 kW range is compressing average selling prices by almost 8% a year as Asian brands enter with cut-rate models, adding price pressure but also widening access.

By Application: Process Heat Outpaces Space-Heating Maturity

Space heating commanded 52.72% of 2025 turnover, yet its growth moderates as early-adopter retrofits saturate. Industrial process heating is tracking a 4.16% CAGR, bolstered by natural-gas prices that lingered near EUR 0.08 (USD 0.09) per kWh in 2025 and by EU carbon-border rules that reward low-emission production. Domestic hot-water and pool-heating niches remain small but attractive, aided by solar-plus-heat-pump bundles that maximize self-consumption.

High-temperature innovations, such as SPH’s 139 °C ThermBooster, extend heat-pump utility into breweries and chemical plants formerly locked into gas boilers. Hybrid space-heating packages with thermal storage flatten demand curves, letting owners tap off-peak tariffs. Collectively, these use-case shifts diversify revenue and will lift Germany heat pump market share in energy-intensive industries more quickly than in the maturing residential space-heating segment.

By End User: Residential Dominates, Industrial Momentum Builds

Residential buyers captured 64.09% of 2025 revenue thanks to a retrofit pool of roughly six million obsolete boilers. Commercial premises account for most of the remainder, leveraging variable-refrigerant-flow systems for simultaneous heating and cooling in mixed-use structures. Industrial clients, though still smaller in absolute euros, show the highest 3.97% CAGR as they pursue energy-cost arbitrage and compliance with EU climate quotas.

Landlord-tenant incentive alignment has improved after tax rules started allowing accelerated depreciation of retrofit costs, while municipal bans on new gas-grid links lock green-field housing into all-electric designs. On the industrial side, firms see heat pumps as a hedge against volatile gas pricing and as a route to monetizing surplus heat through district networks, giving this customer class growing relevance in overall Germany heat pump market share calculations.

By Installation: New-Build Expansion Outstrips Retrofit Volume

Retrofits owned 54.43% of volume in 2025 but now grow slower than green-field installs because easy single-family conversions are largely harvested. New-build deployments are projected to rise at 4.37% annually, driven by the Building Energy Act’s 65% renewable-heat rule and by local heat-planning zones that prohibit new gas mains.

Purpose-built designs integrate low-temperature hydronics and thicker insulation, pushing seasonal performance factors beyond 4.5 and easing load on the power grid. Retrofit work remains sizable yet faces friction from hydraulic complexity, older radiators, and the installer shortage. Manufacturers answer with plug-and-play packages like Stiebel Eltron’s modular wpnext line, but until technician capacity improves, retrofit timelines will stay protracted relative to streamlined new-build rollouts.

Geography Analysis

Southern Germany dominates installations, with Bavaria alone providing around 37% of national volume in 2024 thanks to a high share of detached homes, generous state add-on grants, and sub-zero winter temperatures that justify larger compressors. Baden-Württemberg sits close behind, leveraging its own renewable-heat mandate, in force since 2008, to normalize heat pumps as the default for new housing. North Rhine-Westphalia focuses on industrial and district solutions around the Ruhr, repurposing former coal assets into low-carbon heat networks anchored by megawatt-scale pumps.

Eastern federal states trail because lower household incomes, aging building stock, and sparse installer coverage stretch wait times past 18 months, diluting the value of subsidies that expire after two years. Nevertheless, Brandenburg and Saxony have begun funding cooperative purchasing groups that aggregate orders, trimming equipment cost by roughly 15%. Hamburg and Berlin pursue 100% renewable-heat targets by 2030, driving multi-family retrofits that favor low-noise air-to-air units and sewage-heat recovery.

Lower Saxony and Schleswig-Holstein battle rural grid congestion where winter voltage sags already prompt temporary curtailments. Utilities there pilot demand-response tariffs and accelerate feeder-line upgrades to unlock further adoption. Saarland and Thuringia, Germany’s two smallest states, experiment with community-owned bore-fields that split drilling expense across dozens of households, a template watched closely by other rural regions. Overall, geography dictates installer availability, climate benefit, and subsidy stacking, so state-level policy nuance will keep reshaping the spatial profile of the Germany heat pump market in the years ahead.

Competitive Landscape

Market concentration is moderate: Viessmann, Vaillant, Bosch, Daikin, and Stiebel Eltron together shipped about 60% of 2025 units, while dozens of smaller brands fill regional or technical niches. Incumbents deepen moats by verticalizing, from refrigerant supply to installer training, to shield themselves from regulatory and labor bottlenecks. Viessmann’s ViCare platform, now connected to 1.2 million pumps, delivers predictive maintenance and demand-response aggregation, embedding data-driven lock-in that rivals struggle to match.

Daikin is tripling R290 capacity at Güglingen to 200,000 units per year by 2027, ensuring compliance with the 2027 high-GWP ban just as smaller peers still engineer propane redesigns. Stiebel Eltron’s EUR 600 million (USD 678 million) Höxter upgrade adds 50,000 square meters of floor space and trains 2,000 installers annually, a strategic bid to ease the industry’s technician shortfall. Bosch filed 47 heat-pump patents in 2025 around variable-speed compressors and smart-grid interfaces, signposting where differentiation may unfold next.

Challengers include Chinese OEMs supplying competitively priced air-to-water units that meet efficiency codes yet lack nationwide service coverage, and niche German firms like Alpha Innotec and Waterkotte that specialize in ground-source designs. Regulatory pressure on installer certification under VDI 4645 favors brands that finance training academies, handicapping low-support importers. With industrial process heating emerging as a fresh revenue pool, specialists such as SPH and MAN Energy Solutions are carving out high-temperature strongholds, widening the technology spectrum and ensuring that rivalry across the Germany heat pump market remains dynamic even as top-tier shares consolidate.

Germany Heat Pump Industry Leaders

-

Daikin Industries Ltd.

-

Viessmann Climate Solutions SE

-

Panasonic Holdings Corporation

-

Trane Technologies Plc

-

BDR Thermea Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Daikin allocated EUR 150 million (USD 169.5 million) to add a third R290 line in Güglingen, lifting annual capacity to 200,000 units by 2027.

- February 2026: MVV Energie won final approval for its EUR 200 million (USD 226 million) 165 MW Rhine river heat pump slated for winter 2028 start-up.

- January 2026: Viessmann unveiled the Vitocal 250-AW Pro with built-in demand-response capability for the ViFlex program.

- November 2025: Stiebel Eltron completed phase one of its EUR 600 million (USD 678 million) Höxter expansion, adding production space and a training academy.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Germany heat pump market as the value of newly installed, factory-built units that extract ambient, aquatic, or geothermal heat and deliver it for space conditioning or sanitary hot water across residential, commercial, industrial, and district-heating settings. We cover air-source, water-source, ground-source, hybrid, and large-scale natural-refrigerant systems rated below 1 MW, as well as multi-MWth plants feeding municipal networks.

Scope exclusion: portable air conditioners or VRF units used solely for cooling are not counted.

Segmentation Overview

-

By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

-

By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

-

By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

-

By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

-

By End User

- Residential

- Commercial

- Industrial

-

By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed installers in Bavaria, equipment wholesalers in North-Rhine Westphalia, and energy-service companies serving district networks. They then spoke with policy officers in Berlin to gauge subsidy disbursement velocity. These discussions validated shipment tallies, sales-channel margins, and likely retrofit rates, filling gaps left by published statistics.

Desk Research

We began with Destatis building-permit files, BAFA subsidy ledgers, Eurostat import codes 8418 69 10/20 for heat pumps, and EHPA shipment registers, which collectively frame installed volumes and technology splits. Policy texts such as the Building Energy Act and EU F-Gas Regulation clarified compliance triggers, while peer-reviewed journals on R290 charge limits informed efficiency assumptions. Company filings, press releases, and Questel patent families helped benchmark price moves and product pipelines. The sources above are illustrative; many additional public and paid references guided data gathering and sense-checking.

Market-Sizing & Forecasting

A top-down model starts with Germany's dwelling stock, commercial floor area, and industrial process-heat demand. It applies heat-pump penetration by end use and multiplies by average selling price tiers (<10 kW, 10-50 kW, >50 kW). Results are cross-checked through selective bottom-up roll-ups of manufacturer sales and installer order books. Key variables like new-build completions, BAFA grant uptake, electricity-to-gas price ratio, refrigerant transition costs, and certified-installer capacity feed a multivariate regression that projects demand through 2030. Where supplier roll-ups undershoot the top-down total, volumes are re-apportioned using installer backlog data before freezing the baseline.

Data Validation & Update Cycle

Outputs pass a two-level analyst review. Anomaly rules flag deviations against EHPA and BDH benchmarks, and material events trigger mid-cycle revisions. Mordor refreshes every twelve months and performs a final data sweep just before delivery.

Why Mordor's Germany Heat Pump Baseline Stands Firm

Published values often diverge because firms choose differing product mixes, subsidy-pass-through assumptions, and currency bases. By aligning scope with legal definitions in the Building Energy Act and anchoring prices to actual invoice medians, Mordor avoids inflation or understatement that can arise when hybrid boilers are bundled in or industrial mega-plants are left out.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.19 B (2024) | Mordor Intelligence | - |

| USD 1.50 B (2024) | Regional Consultancy A | Counts air-source units only and excludes district-heating projects |

| USD 1.22 B (2024) | Global Consultancy B | Uses residential demand model, overlooks commercial retrofits above 20 kW |

| USD 2.02 B (2024) | Industry Association C | Applies aggressive subsidy-driven ASP discounts and omits hybrid systems |

The comparison shows that when scope, pricing, and end-user breadth are fully harmonized, Mordor's balanced approach provides decision-makers with the most dependable, transparent baseline for sizing opportunities and stress-testing strategies.

Key Questions Answered in the Report

How large is the Germany heat pump market in 2026?

It stands at USD 3.33 billion, on track to reach USD 4.02 billion by 2031.

What is the forecast CAGR for heat pumps in Germany from 2026-2031?

The market is projected to grow at a 3.84% CAGR during the forecast window.

Which source type leads in market share?

Air-source heat pumps led with 67.78% revenue share in 2025.

Why are hybrid heat pumps growing so quickly?

They hedge against electricity price swings and qualify for subsidies when they cover at least 65% of annual load.

What is the main bottleneck holding back faster growth?

A shortage of certified installers has extended project wait times beyond 18 months in some regions.

Which German states are adopting heat pumps fastest?

Bavaria and Baden-Württemberg lead adoption, supported by state subsidies and stricter renewable-heat mandates.

Page last updated on: