Finland Heat Pump Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

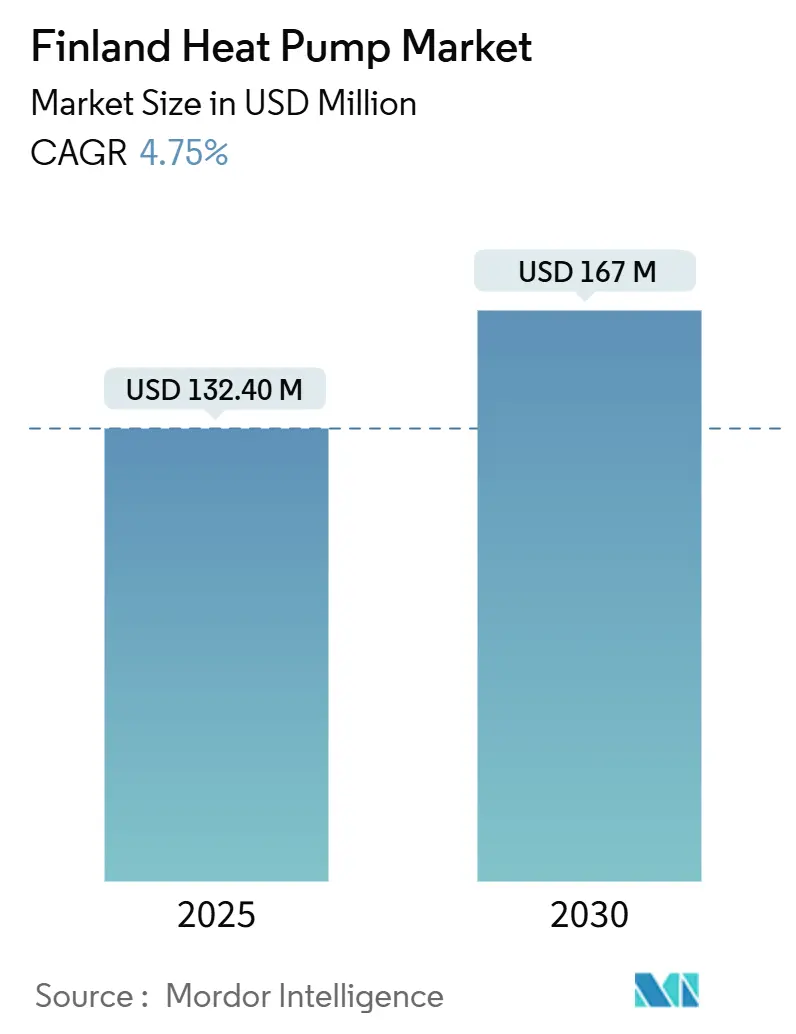

| Market Size (2025) | USD 132.40 Million |

| Market Size (2030) | USD 167 Million |

| Growth Rate (2025 - 2030) | 4.75% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Finland Heat Pump Market Analysis by Mordor Intelligence

The Finland heat pump market stands at USD 132.40 million in 2025 and is forecast to expand at a 4.75% CAGR to reach USD 167 million by 2030. Rapid electrification, generous subsidies and stringent carbon-neutrality milestones have made heat pumps the preferred replacement for oil and direct-electric heating. Air-source units still account for most installations because of their lower upfront costs and easier siting, yet ground-source systems are scaling quickly as drilling costs fall and grid operators reward flexible demand. Digital sales channels, once peripheral, now capture a double-digit growth rate as homeowners exploit online eligibility tools for subsidies. On the supply side, international majors are buying Nordic service outfits to secure installation capacity, while local specialists differentiate through cold-climate engineering and natural-refrigerant designs.

Key Report Takeaways

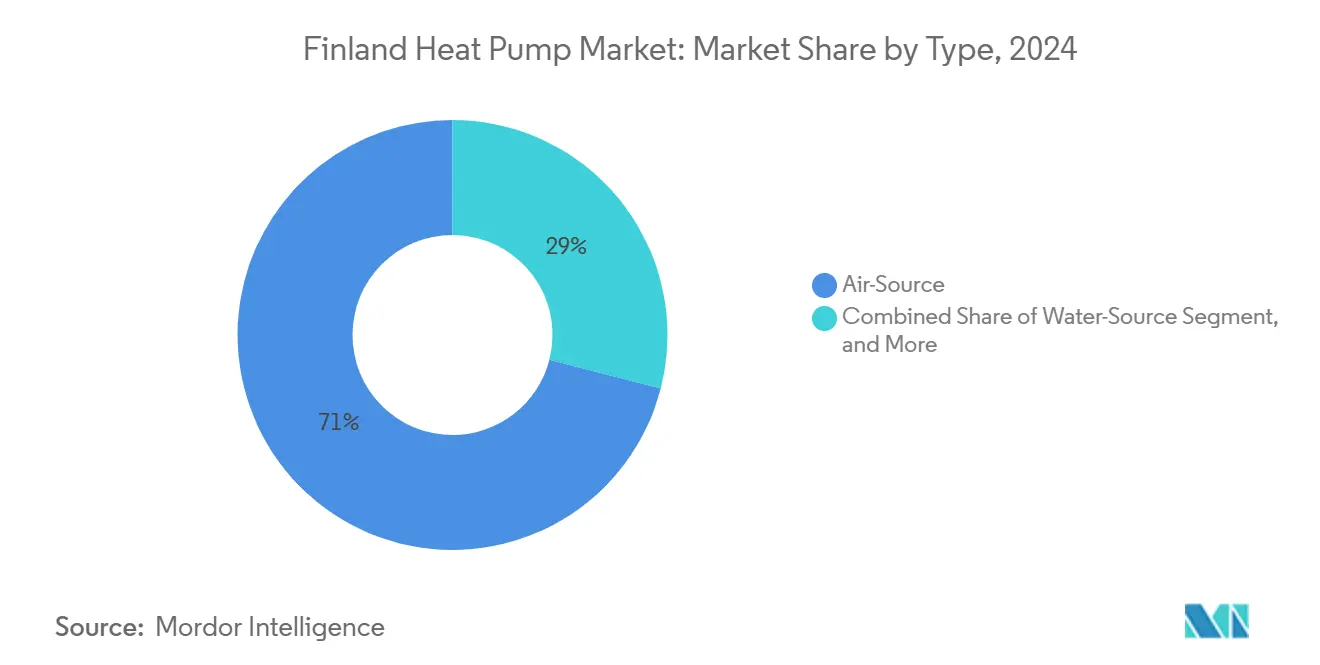

- By type, air-source systems held 71% of the Finland heat pump market share in 2024; ground-source units posted the fastest growth rate of 4.8% through 2030.

- By rated capacity, the less than 10 kW class accounted for a 56% share of the Finland heat pump market size in 2024, whereas the 50–100 kW band is projected to grow at 5.2% from 2024 to 2030.

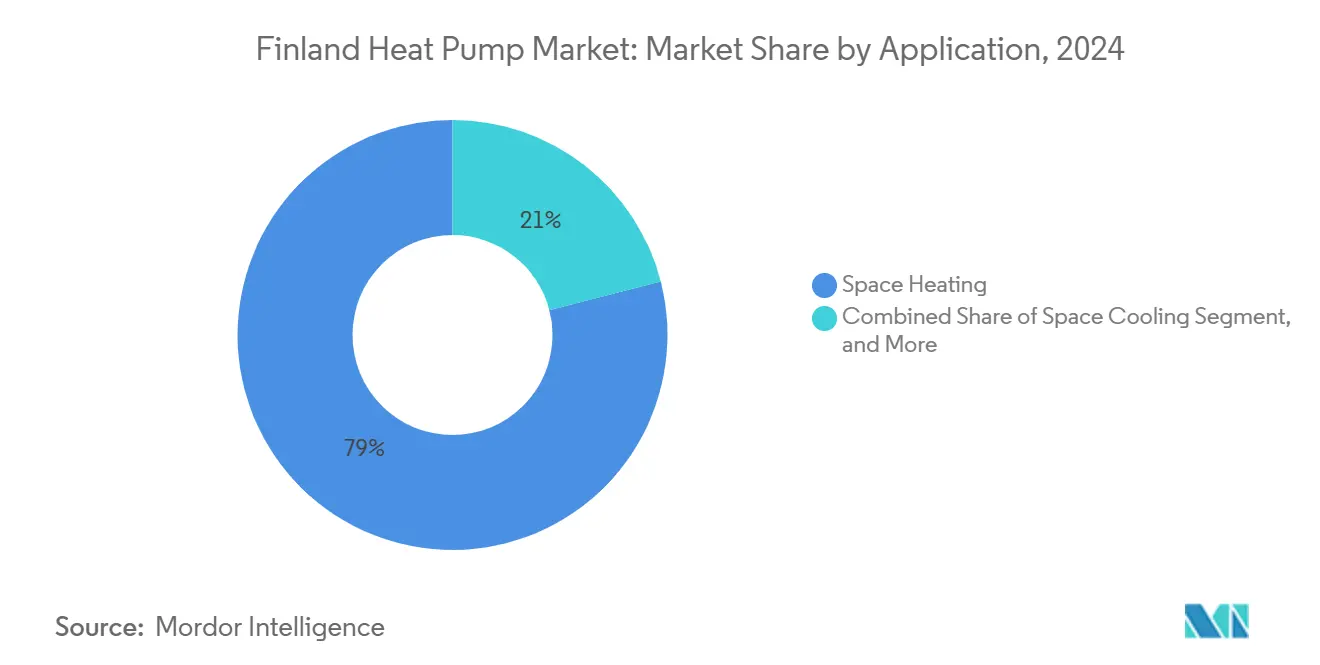

- By application, space heating captured 79% revenue in 2024; domestic hot-water demand advances at a 4.95% CAGR through 2030.

- By end-user vertical, the residential segment led with 68% of the Finland heat pump market size in 2024; commercial installations are expected to record the highest 5% CAGR through 2030.

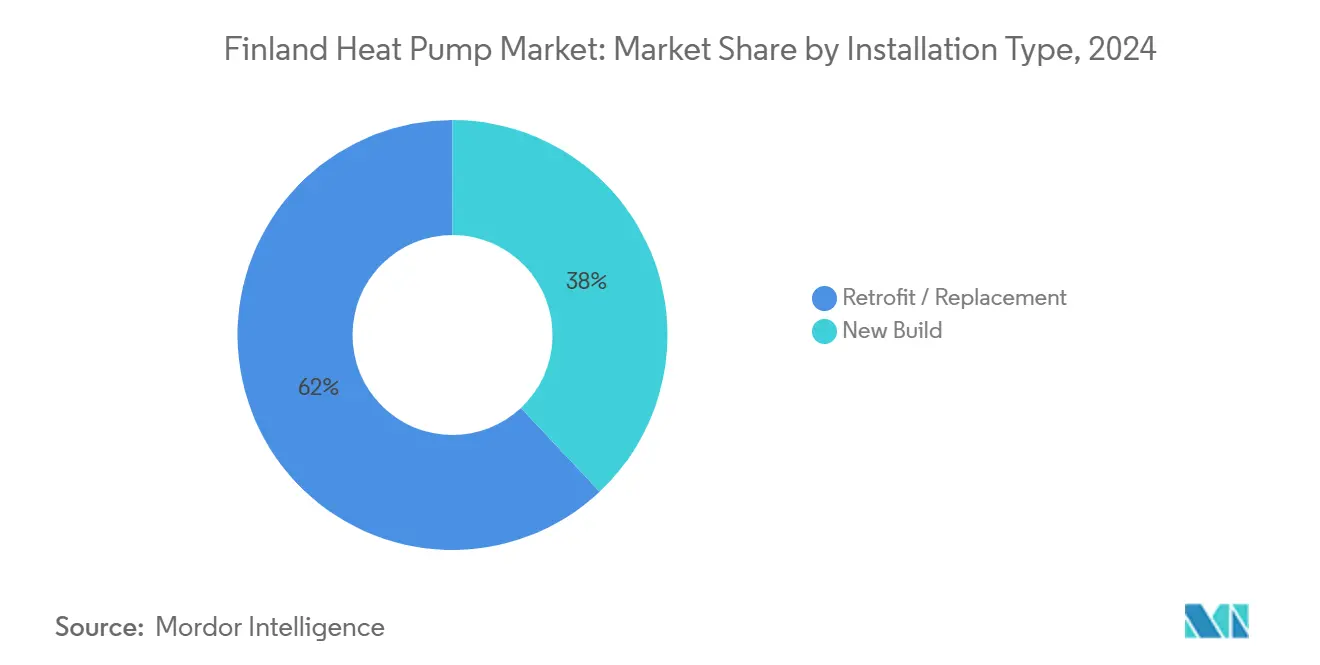

- By installation type, retrofits contributed 62% of the 2024 value, while new-build activity is expected to accelerate at a 4.82% CAGR through 2030.

- By sales channel, distributors/installers commanded a 59% share of the Finland heat pump market in 2024; e-commerce is expected to expand at a 5.2% annual CAGR through 2030.

Finland Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supportive energy–tax incentives | +2.9% | Rural oil-heating areas | Medium term (2–4 years) |

| Rising demand for energy-efficient systems | +2.1% | Urban centers | Long term (≥4 years) |

| National subsidy schemes (Energy Efficiency and ARRA) | +1.7% | Lower-income regions | Short term (≤2 years) |

| Carbon-neutral 2035 target | +2.6% | Helsinki, Tampere, Espoo pilots | Long term (≥4 years) |

| Expansion of district heating network integration | +1.8% | Southern and Western Finland | Medium term (2–4 years) |

| Advancements in heat pump technology for cold climates | +2.4% | Northern Finland and Lapland | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Supportive energy–tax incentives

Finland has ramped up its push for heat pump adoption, rolling out direct subsidies and tax incentives. In 2024, homeowners saw renovation subsidies soar to EUR 9,000 (USD 10,402.65) for air-to-water heat pumps and EUR 15,000 (USD 17,337.75) for ground source variants. On top of this, the Finnish government bolstered its support with a 20% corporate income tax credit for industrial-scale heat pump investments, capping at EUR 150 million (USD 173.38 million) per corporate group. These moves sync seamlessly with Finland's National Climate and Energy Strategy, which champions non-combustion heat production and offers tax breaks for larger industrial heat pumps, all aimed at fast-tracking market changes.

Rising Demand for Energy-Efficient Systems

The Finnish Energy Authority, in 2023, reported that 80% of consumers in Finland are now actively comparing or switching their energy contracts, marking a significant shift in consumer awareness regarding energy efficiency benefits. This growing awareness is fueling the adoption of heat pumps, especially as the price gap between electricity and oil widens. Research shows that heat pumps can cut heating energy costs by 45% in Finland and notably reduce CO2 emissions, a fact underscored by renovation projects in Jyvaskyla. In response to this trend, the market is rolling out advanced products, including air-to-water heat pumps. These innovative models are designed to thrive in Finland's harsh climate, with some proving efficient even at frigid temperatures of -20°C.

National subsidy schemes (Energy Efficiency and ARRA)

Subsidies aimed at boosting renewable energy production and improving energy efficiency have been instrumental in reducing technology risks associated with new heat pump investments, particularly for projects utilizing surplus heat. For 2025, the energy aid budget of EUR 14.1 million (USD 16.29 million) earmarks at least 60% for energy efficiency initiatives. Notably, heat pumps exceeding 1 MW capacity can receive subsidies if linked to low-temperature heating networks. This strategic focus has spurred market growth, particularly in lower-income regions where residents historically allocate a larger share of their income to energy, underscoring the subsidies' impact.

Carbon-neutral 2035 target

Finland is on track to meet its ambitious carbon neutrality goal by 2035, and at the core of this electrification strategy are heat pumps. This commitment has not only fueled investments in renewable energy but has also led Finland to achieve a remarkable milestone: nearly 95% of its electricity generation is now carbon-neutral, a feat accomplished by 2025. The energy sector has set its sights on ambitious CO2 emission reductions: 60% by 2030 and 80% by 2040, both benchmarks set against 1990 levels. This aggressive timeline underscores the urgent need for the rapid electrification of heating. The impact of these policies is evident in the market dynamics: in 2024, a striking 75% of new single-family homes in Finland opted for heat pumps, a stark contrast to the mere 14% adoption rate in similar markets, such as the United States.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightened F-gas quotas | –1.4% | Air-source segment nationwide | Short term (≤2 years) |

| High upfront CAPEX vs biomass | –1.2% | Rural central and northern Finland | Medium term (2–4 years) |

| Slow permitting and regulatory approval processes | –1.6% | Urban and suburban regions | Medium term (2–4 years) |

| Limited availability of skilled installation workforce | –1.3% | Nationwide, especially rural areas | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Tightened F-gas quotas

EU F-gas rules effective March 2024 limit HFC availability and have inflated the price of popular blends by over 40%, squeezing installers’ margins and nudging buyers toward propane or CO₂ designs. [1]Daikin, “Thinking About Buying a Heat Pump?,” daikin.ie In sparsely populated regions, the EUR 8,000 (USD 9,040) cost of a modern pellet boiler still undercuts a EUR 15,000 (USD 16,950) ground-source package, delaying fuel-switch projects despite lifetime savings.

High upfront CAPEX vs biomass

In rural Finland, heat pumps, despite their long-term economic benefits, struggle to gain traction. The primary hurdle is their initial investment costs are steeper than those of traditional biomass heating solutions. In regions where housing prices are modest, residents are less inclined and financially equipped to adopt heat pumps. This economic dilemma hits harder in rural locales, where biomass is abundant and traditional heating methods hold cultural significance. In response, the market is rolling out innovative financing solutions. One notable model is "Heat as a Service" (HaaS), which waives upfront costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Ground-Source Gains on Air-Source Dominance

Air-source units generated 71% of share the Finland heat pump market. Subsidised pricing and easy rooftop or façade mounting sustain their lead. Yet refrigerant compliance costs and rising demand for year-round efficiency have lifted the profile of closed-loop bore-hole systems in new districts. Propane-charged air-to-water models capable of –20 °C operation now ship with predictive frost algorithms, trimming defrost losses during prolonged cold spells.[2]Finnish Environment Institute, “F-Gases and Ozone-Depleting Substances,” ymparisto.fi

Ground-source systems are on track for a 4.8% CAGR, bolstered by municipal zoning that reserves drill plots under parking lots. When loop fields connect to district heating, operators access Fingrid’s balancing market and earn flexibility fees. The Finland heat pump market size for this segment is forecast to reach USD 55 million by 2030, underscoring its role in long-duration storage and summer cooling. A Helsinki office block that switched from district heating to a 600 kW bore-hole array now sells excess heat in summer, cutting net energy costs 35%.

By Rated Capacity: Small Units Dominate While Medium Capacity Accelerates

Systems below 10 kW served fragmented detached-house demand worth USD 70.9 million in 2024 and remain the volume driver of the Finland heat pump market. Online showrooms bundled with remote-support apps have shrunk acquisition friction.

Nevertheless, installers active in the 50–100 kW range report order books up 30% year-on-year as schools, supermarkets and logistics centres retrofit fossil boilers. This mid-capacity band, projected to grow 5.2% annually, benefits from the 20% corporate tax credit and robust ESG disclosure rules on property portfolios.

By Application: Space Heating Leads While Hot Water Accelerates

Space-heating duty absorbed 79% of share in 2024 revenue in the Finland heat pump market. Metered district loops still dominate high-density cores, yet apartment cooperatives are peeling off to autonomous geothermal fields, citing lifecycle savings and control over tariff escalation.

Hot-water-only systems, once rare, now post an 4.95% CAGR as building codes demand higher sanitary-water efficiency. Developers increasingly specify split-circuit layouts that separate DHW and space-heating loads, optimising COP across seasons and earning A-rated EPCs.

By End-User Vertical: Residential Dominance with Commercial Acceleration

Households represented 68% share, of the Finland heat pump market size in 2024. Sales are buoyed by automatic e-grant portals and utility-run leasing offers. Commercial premises, offices, retail and hospitality, will outpace other segments at a 5% CAGR, helped by corporate net-zero pledges and payback windows shortened to under five years where waste-heat recovery is feasible.

Industrial campuses are currently testing high-temperature units designed to deliver process heat of up to 120 °C. This development represents a significant step forward in industrial heating technologies. By enabling higher temperature outputs, these units create new opportunities for further electrification in industrial processes, aligning with the broader goals of energy efficiency and sustainability.

By Installation Type: Retrofit Market Leads While New Build Accelerates

Retrofits accounted for a share of 62% of the Finland heat pump market in 2024. Oil-to-air replacements dominate, but geothermal conversions in 1960s apartment blocks are climbing once preliminary bore-field studies confirm viability.

Despite rising interest rates, the new-build penetration rate is expected to grow at an annual rate of 4.82%. This growth is attributed to lenders incentivizing EPC-A projects by offering margin discounts. Currently, new-build penetration accounts for 70-80% of annual dwellings, and this trend is anticipated to continue during the forecast period.

By Sales Channel: Distributors Dominate While E-Commerce Surges

Traditional distributor/installer chains delivered 59% of 2024 revenue, in the Finland heat pump market share. They have responded to F-gas turbulence by stocking dual-refrigerant-ready inventories. E-commerce, running at 5.2% CAGR, wins mostly sub-10 kW orders.

Digital DIY guidance and plug-and-play packages have significantly reduced the frequency of service callbacks. These solutions empower customers to handle installations independently, minimizing the need for professional assistance. However, larger capacity projects still require the expertise of certified technicians. This dependency is further exacerbated by the persistent shortage of installers in regions outside the primary growth corridors.

Geography Analysis

Urban Finland anchors the Finland heat pump market through early integration of wastewater, seawater and data-centre waste heat. Helsinki’s Katri Vala plant exemplifies the model: two 17 MW ammonia compressors lift wastewater thermal energy into district loops that serve 20% of the capital’s heating load.

Similar projects in Tampere and Espoo adapt the concept to mine geothermal wells beneath industrial brownfields. The south-western archipelago leverages mild coastal winters to maximise air-source COP, while Lapland resorts prefer geothermal to shield against –30 °C extremes.

Regional policy activism shapes adoption speed. Helsinki mandates carbon-neutral new buildings by 2026, driving near-universal ground-source specification in greenfield housing. Conversely, municipalities in central Finland still subsidise biomass micro-CHP, slowing the Finland heat pump market in those districts. Grid flexibility incentives up to EUR 7/MWh (USD 7.9/MWh) for demand response favour installations clustered near wind-power hubs along the west coast.

Competitive Landscape

The Finland heat pump market features moderate concentration. NIBE and Daikin keep scale advantages in R&D and service while Finnish players Oilon and Gebwell retain loyalty through Nordic-tuned designs and responsive after-sales.

Global OEMs deepen service networks by acquiring local maintenance firms; Daikin’s 2025 purchase of Kylslaget AB secures 7,000 annual service calls across Sweden and Finland.[3]Cooling Post, “Daikin Buys Swedish Heat Pump Service Business,” coolingpost.com Institutional investors show rising appetite: CBRE IM’s 80% stake in Geonova funds larger bore-field drilling rigs, and CapMan Infra channels Heat-as-a-Service models that remove CAPEX obstacles for housing co-ops.

NIBE released R290 units with self-learning defrost cycles, while Trane and Johnson Controls move mainstream portfolios to R454B below the 700-GWP limit. Finnish startup Nido raised USD 5.6 million to develop plug-in modules that connect to smart-meter APIs, promising 15% extra savings through dynamic electricity tariffs, potentially disrupting legacy controls.

Finland Heat Pump Industry Leaders

Viessmann Climate Solutions SE

Oilon GmbH

Daikin Industries Ltd.

Trane Technologies Plc

Panasonic Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: CapMan Infra’s portfolio company, ProPellet, has obtained the majority stake in Geo Geo Oy, a Finnish firm that specializes in the comprehensive delivery of ground source heat pump ("GSHP") solutions. ProPellet primarily provides pellet-based heating, and the acquisition of Geo Geo broadens the group’s heating technology portfolio and facilitates expansion into new customer segments through the heating-as-a-service ("HaaS") business model.

- December 2024: Daikin Industries Ltd introduced the Daikin Altherma 4 H, marking its debut in residential air-to-water heat pumps, now utilizing R-290 (propane) refrigerant. Designed for single-family homes, this innovative system boasts impressive heating capabilities, functioning in frigid conditions as low as -28°C and supplying hot water at temperatures reaching 75°C.

- November 2024: Panasonic Holdings Corporation introduced two new heat pump lines tailored for the Canadian market. The ductless EXTERIOS Z and ClimaPure XZ product lines utilize R32 (difluoromethane) as their refrigerant. R32 stands out as a climate-friendly cooling agent, ensuring efficient heat transfer. With these innovations, Panasonic is not only elevating standards for air quality and energy efficiency but also championing a sustainable future.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Finland heat pump market as annual gross revenue from the sale and installation of air, ground, and water-source heat pump units rated below 100 kW that provide space or domestic hot-water heating in dwellings and small commercial premises across Finland.

Scope exclusion: systems larger than 100 kW used in district or industrial heating are outside this scope.

Segmentation Overview

- By Type

- Air-Source

- Water-Source

- Ground-Source (Geothermal)

- Others Type

- By Rated Capacity (kW)

- less than 10 kW

- 10-20 kW

- 20-50 kW

- 50-100 kW

- more than 100 kW

- By Application

- Space Heating

- Space Cooling

- Domestic / Sanitary Hot Water

- Other Application

- By End-User Vertical

- Residential

- Commercial

- Industrial

- Institutional

- By Installation Type

- New Build

- Retrofit / Replacement

- By Sales Channel

- Direct (OEM to End-User)

- Distributor / Installer Network

- E-Commerce

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed installers, utility rebate officers, component suppliers, and e-commerce retailers in Southern, Central, and Lapland regions. Conversations confirmed retrofit share, average selling prices, and seasonality that raw statistics alone could not reveal.

Desk Research

We pulled Statistics Finland building-permit counts, Finnish Customs CN 841861 trade records, Eurostat energy balances, and unit-sales dashboards from EHPA and SULPU. Policy circulars from the Ministry of the Environment, company filings mined via D&B Hoovers, patent clusters flagged in Questel, and tender notices on Tenders Info helped us capture subsidy cadence, pricing, and technology shifts. These references are illustrative; many other public and proprietary sources enriched our desk work.

Market-Sizing & Forecasting

We start top-down. EHPA and SULPU unit shipments are multiplied by region-specific average selling prices validated through interviews. Installer revenue roll-ups and customs import values act as bottom-up guardrails; gaps over three percent trigger assumption resets. Key variables feeding the multivariate regression forecast include new-housing completions, heating-degree-days, subsidy budget execution, the electricity-to-oil price ratio, and typical replacement cycles. Scenario analysis stress-tests policy or fuel-price shocks before totals are finalized.

Data Validation & Update Cycle

Outputs clear a two-layer analyst review; automated variance flags prompt re-contact with sources. Reports refresh every twelve months, with interim updates whenever subsidy rules or energy prices shift materially, so clients receive the latest view.

Why Mordor's Finland Heat Pump Baseline Commands Reliability

Published estimates often diverge because providers vary scope, pricing assumptions, and refresh cadence.

Some fold in industrial mega-plants, while others track consumption rather than revenue. We limit scope to sub-100 kW equipment, validate prices on the ground, and update annually, which keeps Mordor's 2025 baseline closely aligned with observable cash flows.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 132.4 M (2025) | Mordor Intelligence | - |

| USD 749.2 M (2024) | Global Consultancy A | Includes industrial and service revenue; no local interviews |

| USD 83 M (2024) | Trade Journal B | Excludes air-to-air units; values consumption not revenue |

| USD 250 M (2024) | Horizon Data Firm C | Air-source only; uses list prices instead of transaction prices |

These contrasts show how our disciplined scope, Finnish fieldwork, and timely refresh supply decision-makers with a balanced, transparent baseline they can trust.

Key Questions Answered in the Report

What is the current size of the Finland heat pump market and how fast is it growing?

The market totals USD 132.40 million in 2025 and is projected to reach USD 167 million by 2030, advancing at a 4.75% CAGR.

Which heat-pump type leads Finnish sales today?

Air-source units dominate with 71% market share, thanks to lower installation costs and fast retrofits.

How do Finnish subsidies lower the upfront cost of a heat pump?

Homeowners can receive up to USD 10,170 for an air-to-water retrofit and up to USD 16,950 for a ground-source installation, while companies can claim a 20% tax credit on eligible CAPEX.

What impact will the EU F-gas rules have on Finnish heat-pump buyers?

Tightened quotas are raising the price of traditional HFC refrigerants, nudging the market toward natural alternatives such as propane and CO₂.

Page last updated on: