Sulfite-Based Paperboard Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

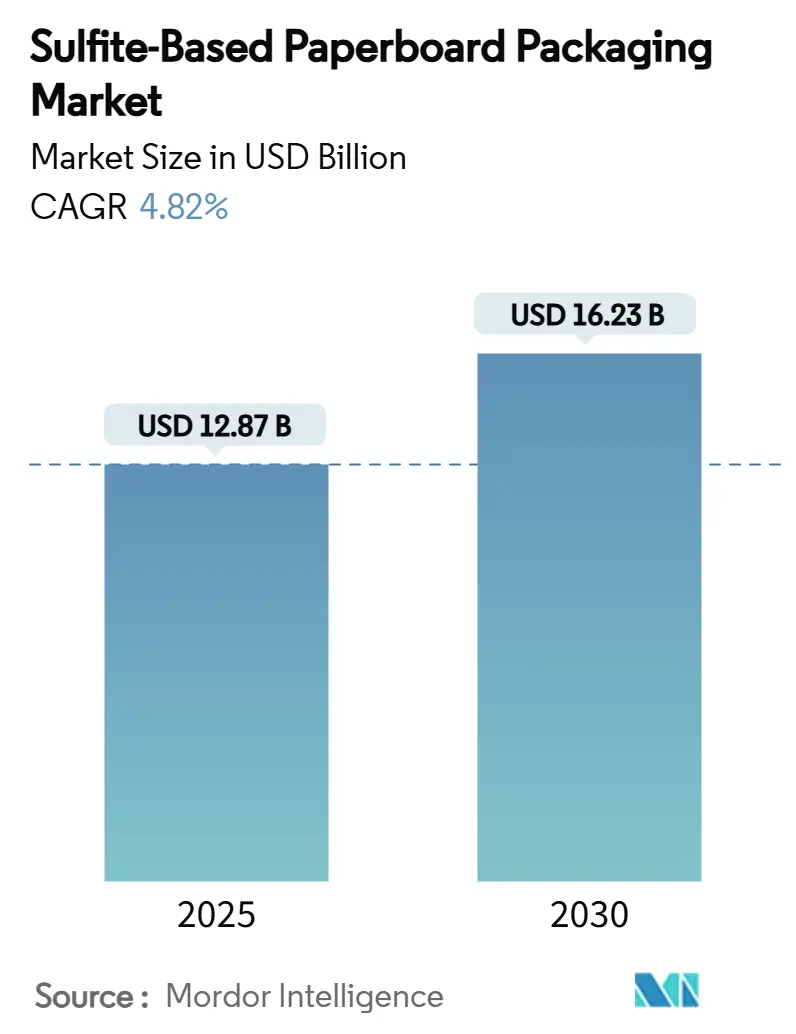

| Market Size (2025) | USD 12.87 Billion |

| Market Size (2030) | USD 16.23 Billion |

| Growth Rate (2025 - 2030) | 4.82% CAGR |

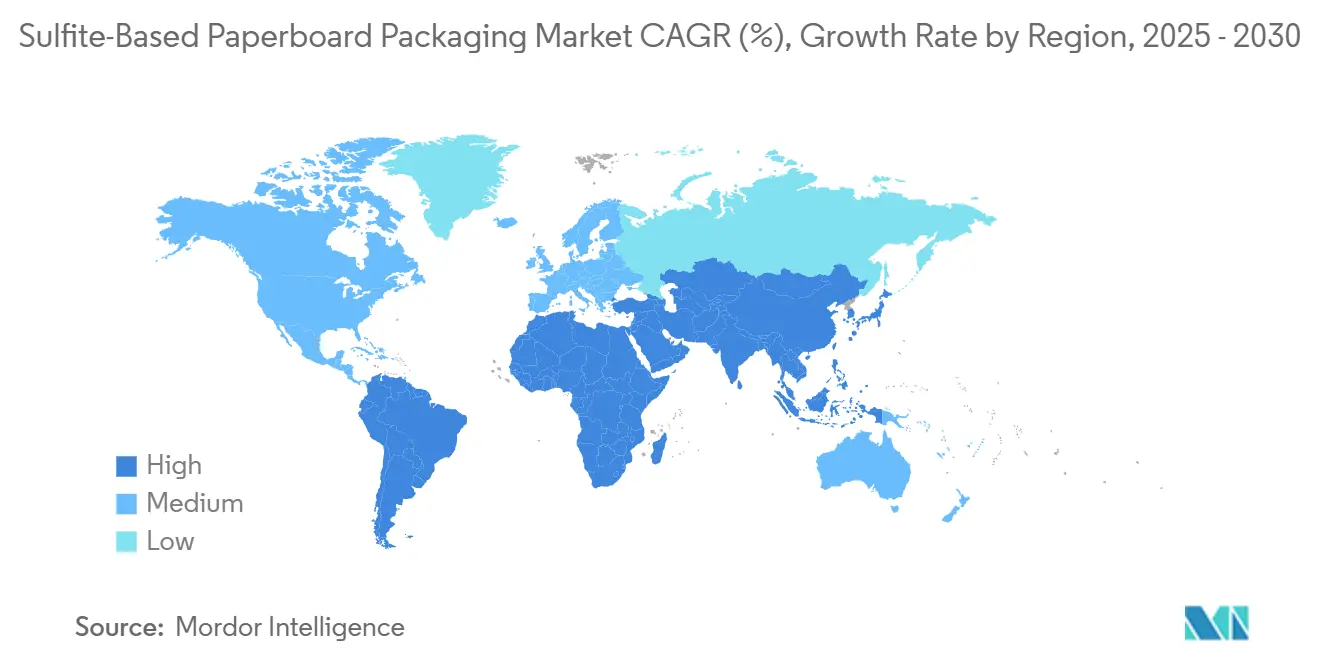

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

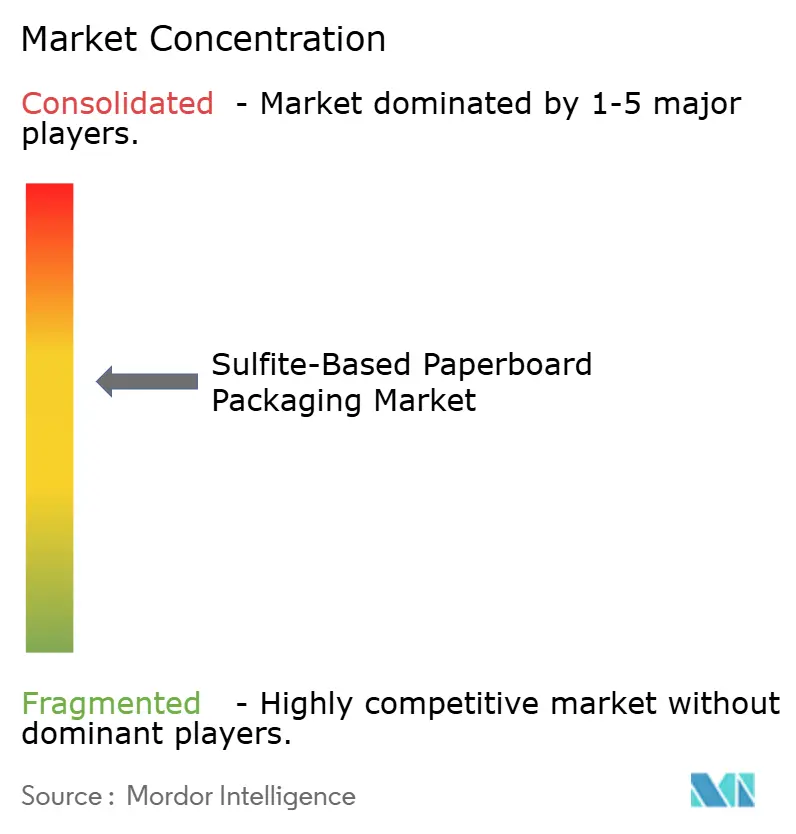

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sulfite-Based Paperboard Packaging Market Analysis by Mordor Intelligence

The sulfite-based paperboard packaging market size reached USD 12.87 billion in 2025 and is forecast to grow at a 4.82% CAGR to USD 16.23 billion by 2030, underscoring resilient demand for low-SO₂, high-printability substrates. Rising carbon-credit revenues for mills that cut sulfur dioxide emissions, the rapid uptake of enzymatic sulfite pulping, and brand-owner sustainability mandates collectively reinforce the competitive appeal of sulfite boards over kraft alternatives. Premium cosmetics, pharmaceutical barrier packs, and beverage liquid cartons continue to pivot toward sulfite substrates because of superior surface smoothness that reduces ink use and improves color fidelity. Beverage makers in North America and Europe are accelerating plastic-to-fiber transitions to comply with polystyrene bans, while Asian mills leverage integrated operations to underwrite cost leadership. Technology investments aimed at circular economy compliance, ranging from enzymatic fiber modification to closed-loop water systems, further differentiate producers that can monetize both environmental and performance benefits in the Sulfite-based paperboard packaging market.

Key Report Takeaways

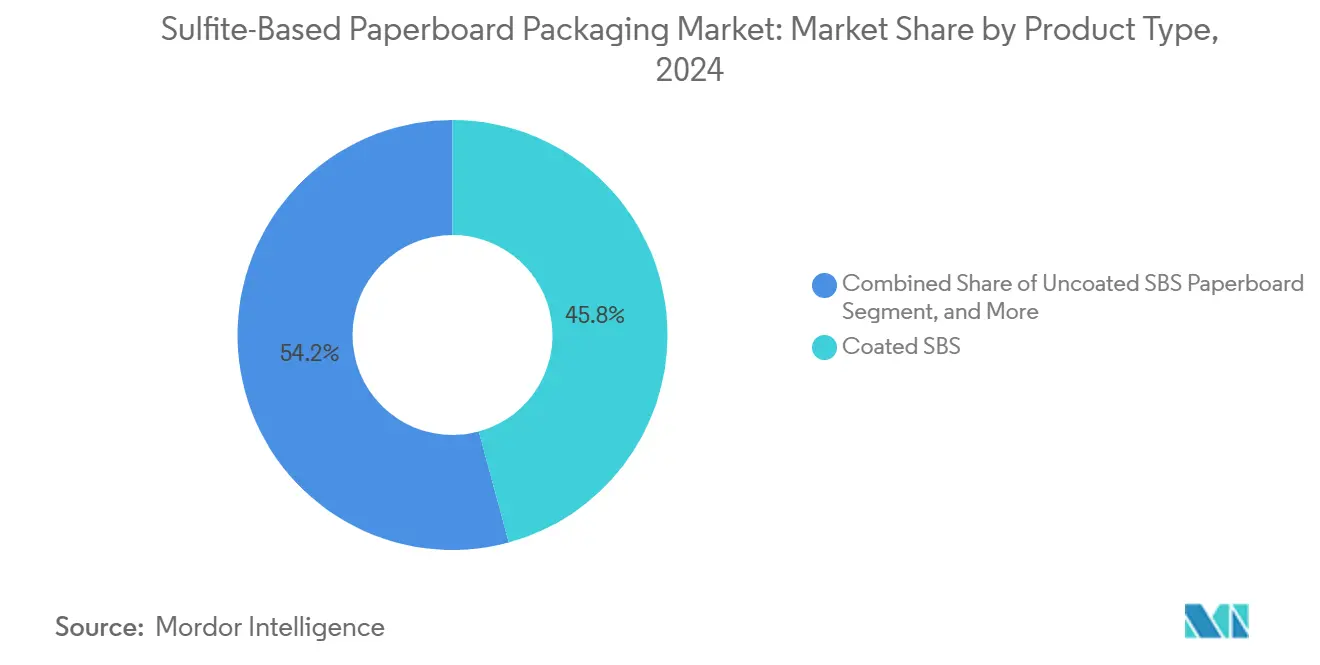

- By product type, coated SBS captured 45.78% of the sulfite-based paperboard packaging market share in 2024.

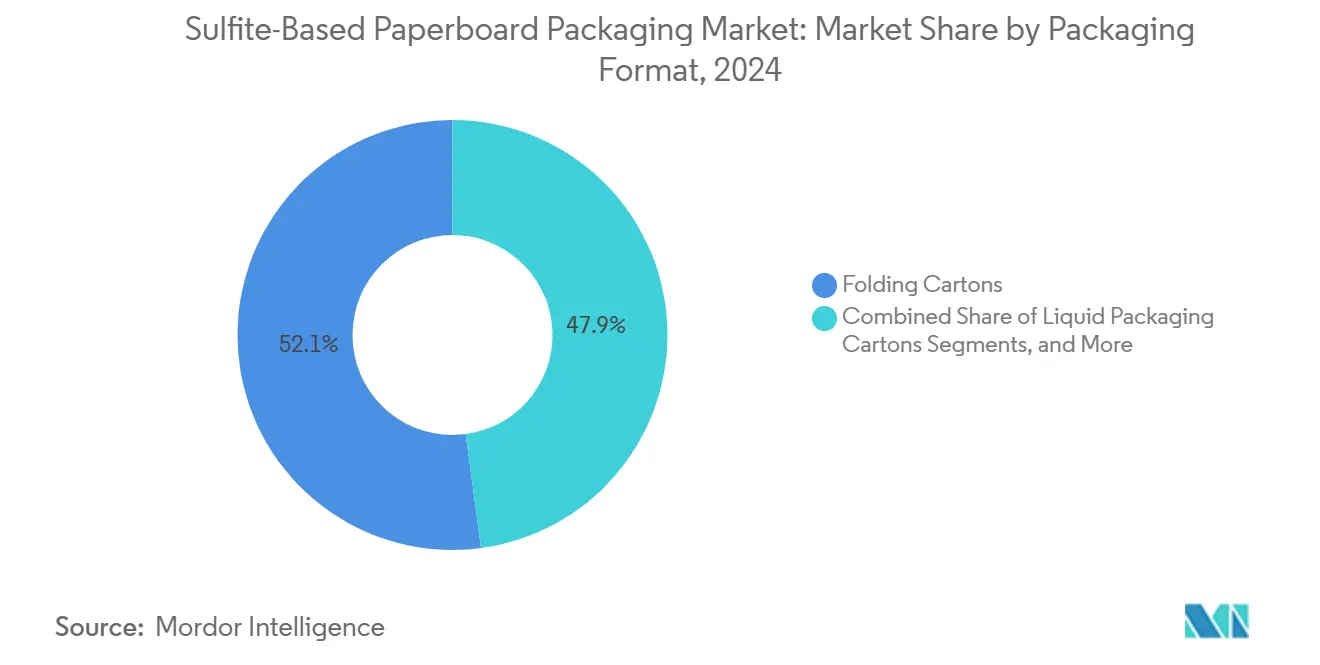

- By packaging format, the sulfite-based paperboard packaging market size for the liquid packaging cartons segment is projected to grow at a 7.82% CAGR between 2025-2030.

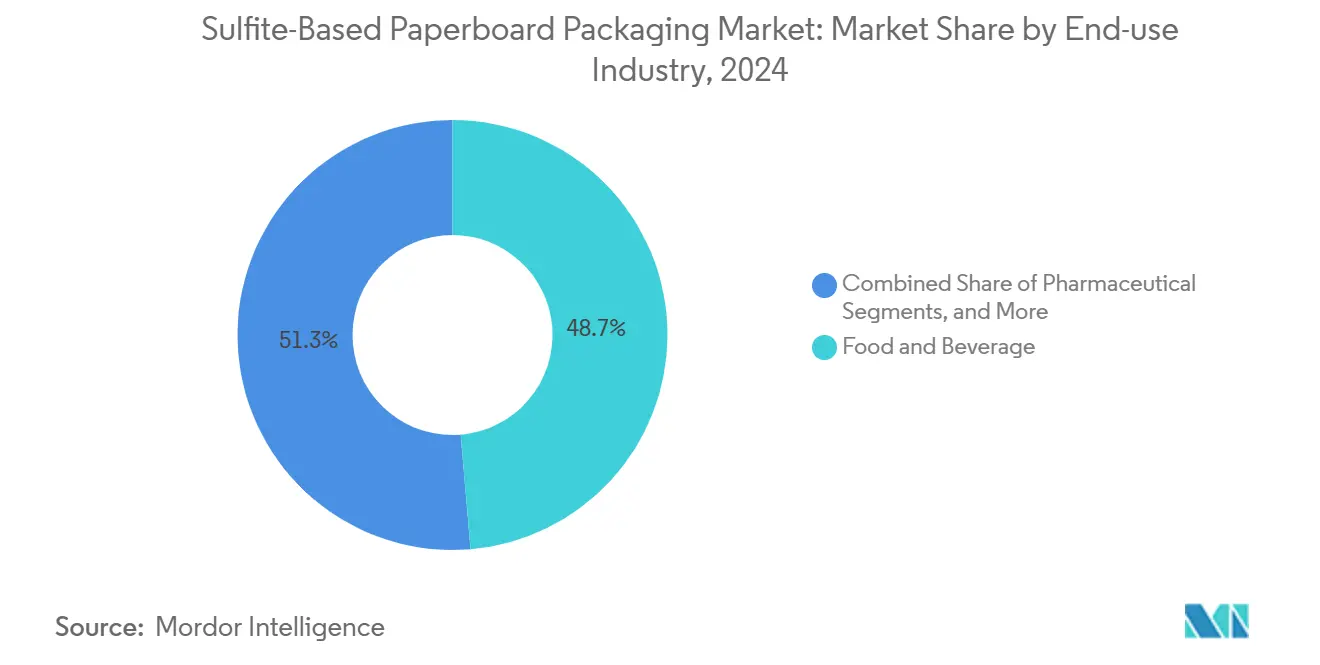

- By end-use, food and beverage captured a 48.67% of the sulfite-based paperboard packaging market share in 2024.

- By geography, the sulfite-based paperboard packaging market size for the Africa region is projected to grow at a 6.12% CAGR between 2025-2030.

Global Sulfite-Based Paperboard Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainable shift from plastic to paperboard | +1.2% | Global; early uptake in North America and EU | Medium term (2-4 years) |

| E-commerce packaging volume boom | +0.9% | Global; concentrated in APAC and North America | Short term (≤ 2 years) |

| Premium printability driving cosmetics | +0.7% | North America and EU luxury hubs; expanding to APAC | Medium term (2-4 years) |

| Food-service bans on expanded polystyrene | +0.8% | North America municipal markets; spreading globally | Short term (≤ 2 years) |

| Enzymatic sulfite pulping cost breakthrough | +0.6% | Global; early roll-out in Scandinavia | Long term (≥ 4 years) |

| Carbon-credit revenue streams | +0.4% | EU and North America compliance markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainable Shift from Plastic to Paperboard

Consumer packaged-goods brands continue to substitute plastic trays and clamshells with recyclable fiber solutions to meet 2030 circularity pledges. Sulfite boards gain preference in premium SKUs because smoother fibers enable brighter graphics without extra coating layers. The EU’s Circular Economy Action Plan and similar U.S. state mandates elevate demand certainty for recyclable substrates. Mill trials in Germany show sulfite liners can achieve 12-color process printing on a single pass, removing the need for lamination and further lowering material weight. Brands also value lower SO₂ footprints that unlock additional carbon credits under voluntary reporting schemes. Together these factors accelerate volume migration into the Sulfite-based paperboard packaging market.

E-commerce Packaging Volume Boom

Global online retail parcel counts rose 15% year-on-year in 2024, boosting folding-carton orders for branded fulfillment. E-tailers prize sulfite board because its uniform surface reduces ink bleed during high-speed digital printing, allowing crisp logos for unboxing experiences. WestRock’s USD 140 million Wisconsin box plant features energy-efficient ink-jet lines calibrated for sulfite substrates, underlining capital re-allocation toward premium e-commerce grades. Short-run, versioned graphics also benefit from the board’s dimensional stability, reducing re-order waste. These dynamics keep e-commerce a demand catalyst within the Sulfite-based paperboard packaging market.

Premium Printability Driving Cosmetics Adoption

Luxury cosmetics and personal-care brands specify sulfite grades for high-gloss cartons that match glass and metallic primary packs. Laboratory tests show sulfite surfaces yield 25% higher gloss readings and sharper edge definition than comparable kraft liners. In 2024, three of the top five global prestige beauty houses shifted holiday gift sets to coated SBS to achieve metallic foil finishes without micro-fluting. Enhanced adhesion also supports oxygen-barrier coatings that prolong product shelf life while permitting clear recycling streams. As color fidelity and tactile effects remain critical to brand equity, cosmetics demand strengthens the Sulfite-based paperboard packaging market.

Food-Service Bans on Expanded Polystyrene

City-level polystyrene prohibitions in Los Angeles and San Francisco have already shifted millions of meal-tray units to compostable paperboard alternatives. Municipal inspectorates often cite sulfite board for compliance due to its rapid biodegradation and superior grease resistance when paired with aqueous coatings. Chain restaurants now pilot sulfite take-out boxes that withstand 95 °C filling temperatures, meeting thermal requirements without plastic lining. As more U.S. and EU jurisdictions replicate bans, the Sulfite-based paperboard packaging market benefits from immediate volume substitution.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher price versus recycled grades | -1.1% | Global; most acute in price-sensitive mass segments | Short term (≤ 2 years) |

| Sulfite pulping chemical effluent compliance | -0.8% | North America and EU regulatory jurisdictions | Medium term (2-4 years) |

| Bleached hardwood pulp supply volatility | -0.6% | North America and Scandinavia commodity pulp corridors | Medium term (2-4 years) |

| SO₂ emission caps near major ports | -0.4% | Coastal regions in North America, EU, and APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Price Versus Recycled Grades

Uncoated recycled boards typically sell at a 12% discount to sulfite equivalents, creating budget constraints for private-label food and household products. The price spread widened in early 2025 when bleached hardwood pulp climbed 8% on tightened Nordic supply. Brands that can tolerate muted graphics increasingly revert to recycled sheets, especially for inner cartons unseen by consumers. To bridge the gap, sulfite mills tout lower total applied ink and shorter press-setup times, but these savings are not always persuasive in commodity lines. Consequently, price sensitivity acts as a near-term drag on the Sulfite-based paperboard packaging market.

Sulfite Pulping Chemical Effluent Compliance

Although enzymatic processes cut sulfite chemical loads by 25%, legacy mills still shoulder high capital costs to meet effluent discharge and SO₂ stack limits under EPA cluster rules. Required scrubbers and continuous monitoring add USD 25-35 per tonne to operating costs, constraining competitiveness against kraft mills located in jurisdictions with lighter oversight. Scandinavian producers, benefiting from government grants, have begun retro-fitting closed-loop liquor recovery, but widespread adoption remains capital-intensive. Until retrofits proliferate, compliance costs temper the expansion pace of the Sulfite-based paperboard packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Coated SBS Leads Premium Applications

Coated SBS captured the largest share of the Sulfite-based paperboard packaging market at 45.78% in 2024 due to its glossy finish and superior ink holdout. Brands in cosmetics and premium confectionery rely on the grade for photo-quality imagery that elevates shelf presence. Laminated sulfite board, while smaller, is set to post a 6.91% CAGR to 2030 as pharmaceutical and nutraceutical fillers demand barrier layers that defend against moisture and oxygen ingress.

Cost-sensitive goods still employ uncoated SBS, which pairs sulfite’s native smoothness with moderate savings by eliminating clay coatings. The enzymatic pulping advance holds particular promise for this tier, lowering fiber costs and enabling mills to price more aggressively without sacrificing stiffness. If pulp price volatility eases, uncoated SBS could increase its Sulfite-based paperboard packaging market share by tapping mid-range personal-care SKUs.

By Packaging Format: Folding Cartons Dominate While Liquid Packaging Accelerates

Folding cartons accounted for 52.12% of the Sulfite-based paperboard packaging market size in 2024 as consumer-goods makers favor high-graphics secondary packs for retail differentiation. The format’s versatility suits everything from OTC drugs to premium chocolates, ensuring a broad demand base.

Liquid packaging, while niche, is forecast to outpace all formats at 7.82% CAGR as dairies and juice brands convert Tetra-style packs to full-fiber structures that skirt polystyrene liners. Nippon Paper’s dedicated carton board line intends to capture this opportunity, signalling rising capital flows toward barrier-enhanced sulfite boards. Labels, tags, and industrial tubes meanwhile benefit from sulfite’s dimensional stability, though they collectively remain secondary in revenue contribution.

By End-use Industry: Food and Beverage Leadership with Pharmaceutical Acceleration

Food and beverage applications held 48.67% of the Sulfite-based paperboard packaging market in 2024 thanks to FDA clearances for sulfite compounds in direct food contact. Shelf-ready convenience foods increasingly utilize sulfite trays that withstand microwaving while showcasing vivid graphics.

Pharmaceutical demand is rising fastest at 8.51% CAGR, propelled by stricter moisture-barrier standards for biologics and regulatory clarity on sulfite substrates. Laminated grades with aluminum-oxide or PVOH coatings now rival plastic blisters in barrier metrics while offering recyclability. The trend anchors long-term volume visibility for mills targeting medical packaging niches within the Sulfite-based paperboard packaging market.

Geography Analysis

Asia-Pacific retained 35.67% share of the Sulfite-based paperboard packaging market in 2024, leveraging integrated pulp-and-paper complexes and lower labor costs across China, Indonesia, and Japan. Expanded e-commerce penetration, combined with escalating regional cosmetics exports, keeps carton demand buoyant. Nippon Paper’s multi-year plan emphasizes cellulose-based barrier laminates, underscoring technology leadership that shields margins amid commodity competition.

North America remains a significant contributor as brand owners seek USDA-certified biobased content and exploit proximity to consumer markets. Recent capacity adds in Wisconsin and Georgia showcase ongoing investment even as consolidation via the impending Smurfit-WestRock merger tightens supply discipline. Carbon markets in California and the Northeast provide extra revenue to mills that achieve low-SO₂ processing, sustaining competitiveness versus imports.

Africa is forecast to log a 6.12% CAGR through 2030, the fastest regional clip in the Sulfite-based paperboard packaging market, as urbanizing populations demand packaged staples and governments promote import substitution. Initial greenfield projects in Kenya and Nigeria target folding carton backlogs that today rely heavily on imports. Technical assistance partnerships with Scandinavian technology suppliers aim to shorten learning curves, ensuring local output meets multinational brand specifications.

Competitive Landscape

The Sulfite-based paperboard packaging industry exhibits moderate concentration; the top five producers collectively account for roughly 45% of installed capacity worldwide. International Paper, and Stora Enso exploit vertical integration and longstanding brand relationships to secure premium contracts. Stora Enso’s 2025 sawmill acquisition adds 1.7 million cubic metres of wood supply, insulating its Finnish board line from fiber shocks.

Asian entrants, led by Nippon Paper and several Chinese state-backed groups, expand aggressively in Europe and Latin America, leveraging cost advantages and growing reputations for high-definition print capabilities. Metsä Group’s EUR 210 million (USD 227.2 million) Husum expansion boosts folding boxboard output 50%, aiming squarely at luxury cosmetics and pharma converters in Western Europe. Meanwhile, enzymatic pulping adoption differentiates innovators by trimming chemical spend and generating tradable carbon credits, factors increasingly weighted in procurement scorecards.

Strategic moves center on capacity rationalization in older bleached mills paired with greenfield investments in multi-grade lines optimized for lightweight, high-barrier cartons. Joint ventures with coating-chemistry specialists proliferate to unlock water-based barriers compatible with mainstream recycling streams. As sustainability audits intensify, mills that document chain-of-custody certifications and low end-to-end emissions stand to gain share within the Sulfite-based paperboard packaging market.

Sulfite-Based Paperboard Packaging Industry Leaders

International Paper Company

Smurfit Westrock plc

Stora Enso Oyj

Mondi plc

Metsä Board Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Stora Enso completed the acquisition of Finnish sawmill company Junnikkala Oy for up to EUR 137 million (USD 148 million), widening raw-material integration for its Oulu board line.

- April 2025: International Paper posted Q1 2025 net sales of USD 5.9 billion following the DS Smith acquisition, bolstering its North American packaging footprint.

- March 2025: Stora Enso began production ramp-up on its new consumer packaging board line at Oulu, slated for full capacity by 2027.

- February 2024: Graphic Packaging agreed to sell its Augusta bleached board plant to Clearwater Paper for USD 700 million to sharpen its strategic focus.

Global Sulfite-Based Paperboard Packaging Market Report Scope

| Coated SBS Paperboard |

| Uncoated SBS Paperboard |

| Laminated Sulfite Board |

| Folding Cartons |

| Liquid Packaging Cartons |

| Labels and Tags |

| Tubes and Cores |

| Other Packaging Format |

| Food and Beverage |

| Personal Care and Cosmetics |

| Pharmaceutical |

| Tobacco |

| Household and Industrial |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Coated SBS Paperboard | ||

| Uncoated SBS Paperboard | |||

| Laminated Sulfite Board | |||

| By Packaging Format | Folding Cartons | ||

| Liquid Packaging Cartons | |||

| Labels and Tags | |||

| Tubes and Cores | |||

| Other Packaging Format | |||

| By End-use Industry | Food and Beverage | ||

| Personal Care and Cosmetics | |||

| Pharmaceutical | |||

| Tobacco | |||

| Household and Industrial | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving the shift toward sulfite-based paperboard in premium consumer packaging?

Brand owners prize the board’s smoother fiber surface, which delivers high-definition graphics while complying with corporate sustainability goals and new plastic-reduction rules.

How fast is the sulfite-based paperboard packaging market expected to grow?

Current forecasts show a 4.82% CAGR from 2025 to 2030, taking global value to about USD 16.23 billion by the end of the period.

Which end-use segment will post the highest growth over the next five years?

Pharmaceutical packaging is projected to expand at an 8.51% CAGR as regulators clarify material approvals and demand for moisture-barrier drug packs rises.

Why are mills investing in enzymatic sulfite pulping technology?

The enzymatic route cuts chemical consumption roughly 25%, lowers sulfur-dioxide emissions, and unlocks carbon-credit revenues, improving mill economics versus traditional kraft lines.

What regions present the strongest growth opportunities?

Africa leads in percentage growth, at a 6.12% CAGR through 2030, while Asia-Pacific retains the largest volume share thanks to integrated pulp-and-paper complexes and expanding e-commerce demand.

Page last updated on: