Molasses Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 9.40 Billion |

| Market Size (2031) | USD 11.80 Billion |

| Growth Rate (2026 - 2031) | 4.66% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Europe |

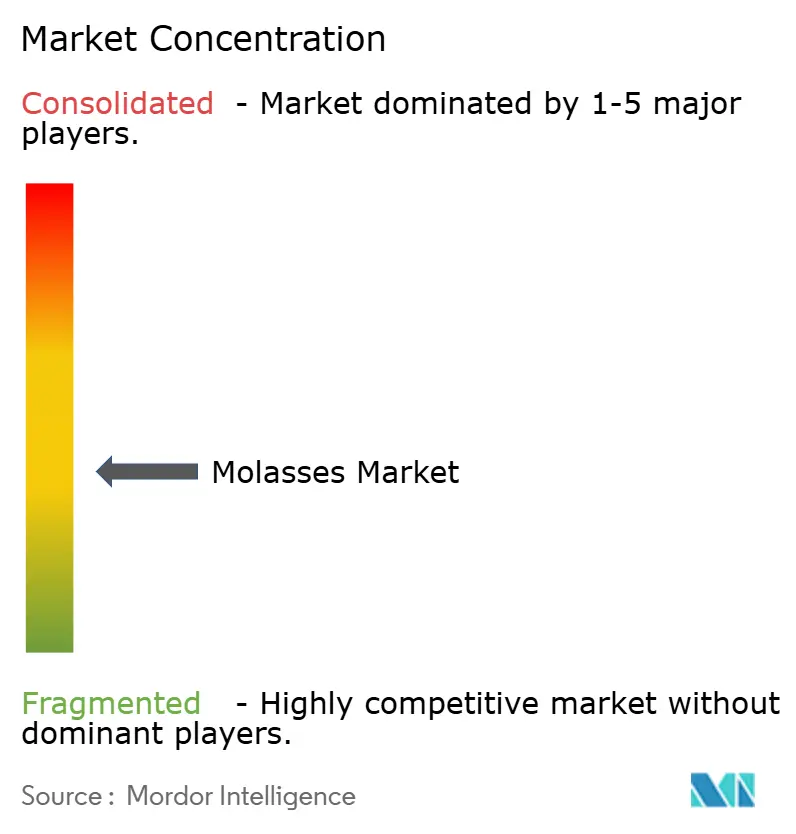

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Molasses Market Analysis by Mordor Intelligence

The molasses market size is projected to expand from USD 8.98 billion in 2025 and USD 9.40 billion in 2026 to USD 11.80 billion by 2031, registering a CAGR of 4.66% between 2026 and 2031. This growth is driven by increasing demand across feed, biofuel, and clean-label food applications, leveraging molasses' Generally Recognized as Safe (GRAS) status. The rising adoption of molasses in animal feed, particularly in the dairy and poultry sectors, is driven by its nutritional benefits and its ability to enhance feed palatability. Additionally, the supply of sugar-beet-derived molasses is increasing as the European Union shifts toward beet-based bioethanol production to meet Renewable Energy Directive targets. Blackstrap molasses is gaining traction due to its role in livestock nutrition protocols aimed at reducing enteric methane emissions in dairy herds, aligning with global sustainability goals. The market is also witnessing growing interest from the food and beverage industry, where molasses is increasingly used as a natural sweetener and flavoring agent in clean-label products, further driving its demand.

Key Report Takeaways

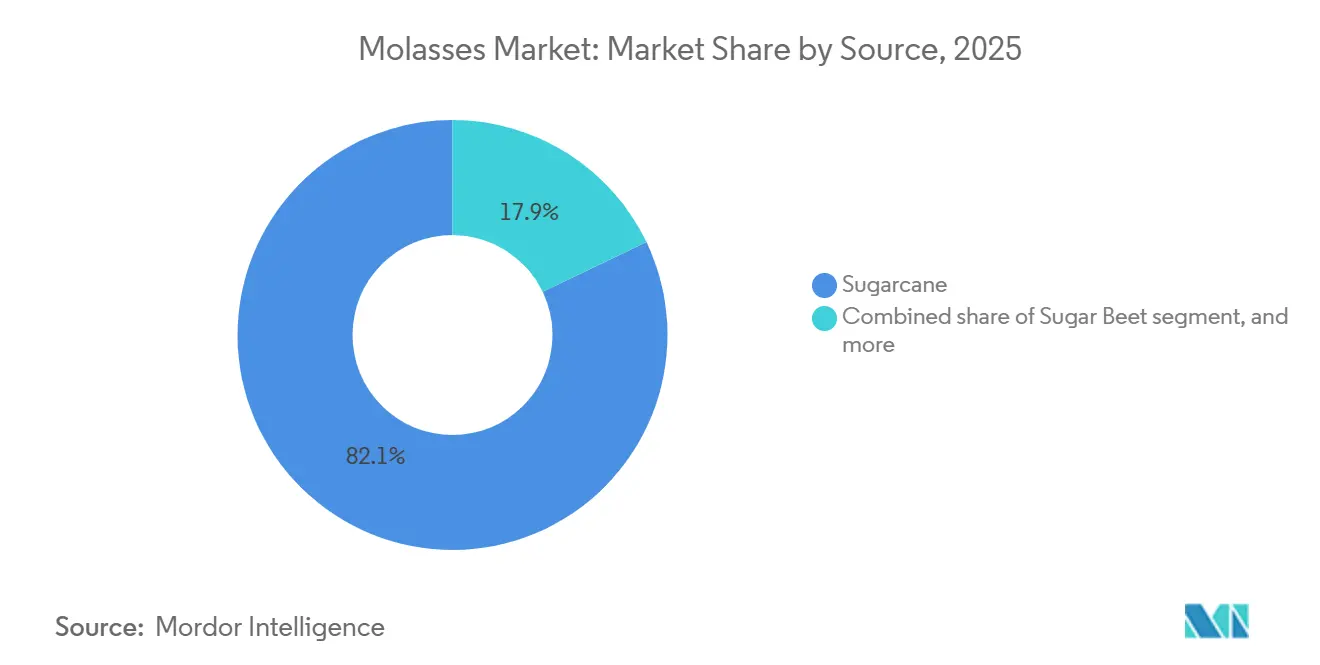

- By source, sugarcane captured 82.11% of the 2025 market, while sugar beet is advancing at a 6.19% CAGR through 2031.

- By grade, blackstrap retained a 53.39% share of the molasses market size in 2025, and is forecast to grow at a 5.80% CAGR through 2031.

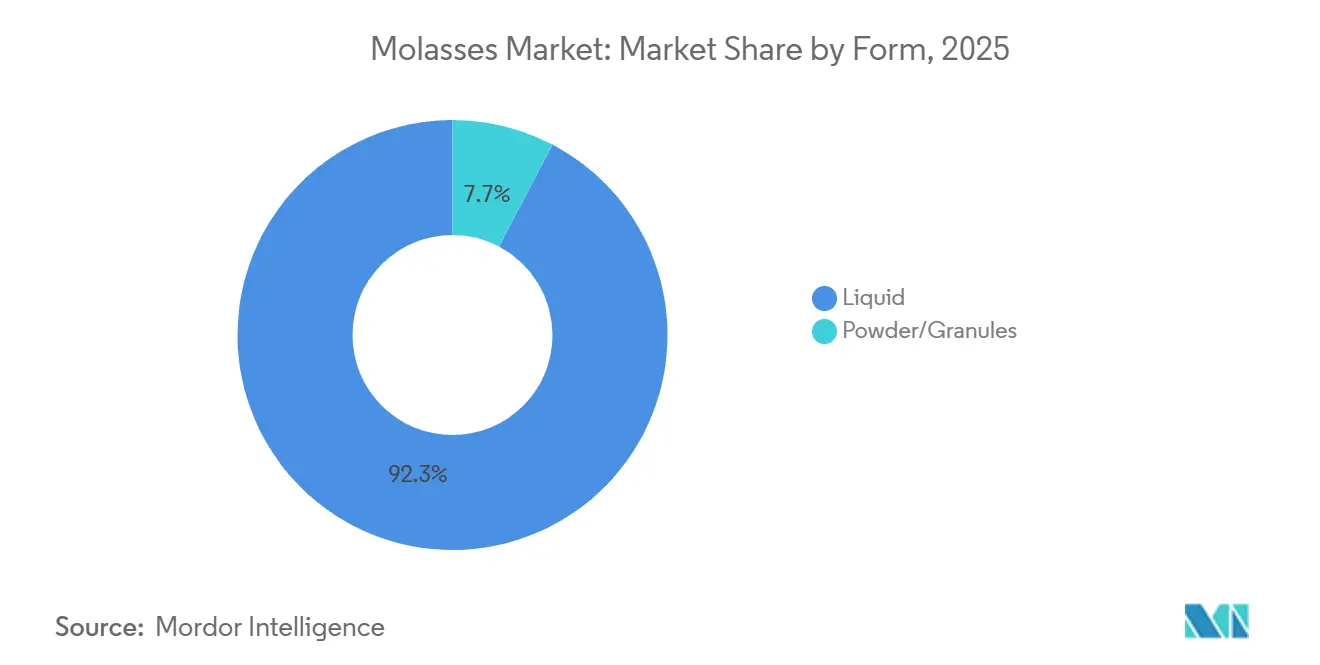

- By form, liquid products accounted for 92.31% of market share in 2025, yet powder and granules are pacing the field with a 7.07% CAGR during 2026-2031.

- By application, food and beverage commanded 61.16% of demand in 2025, whereas animal feed and pet food are expanding fastest at 6.85% CAGR between 2026-2031.

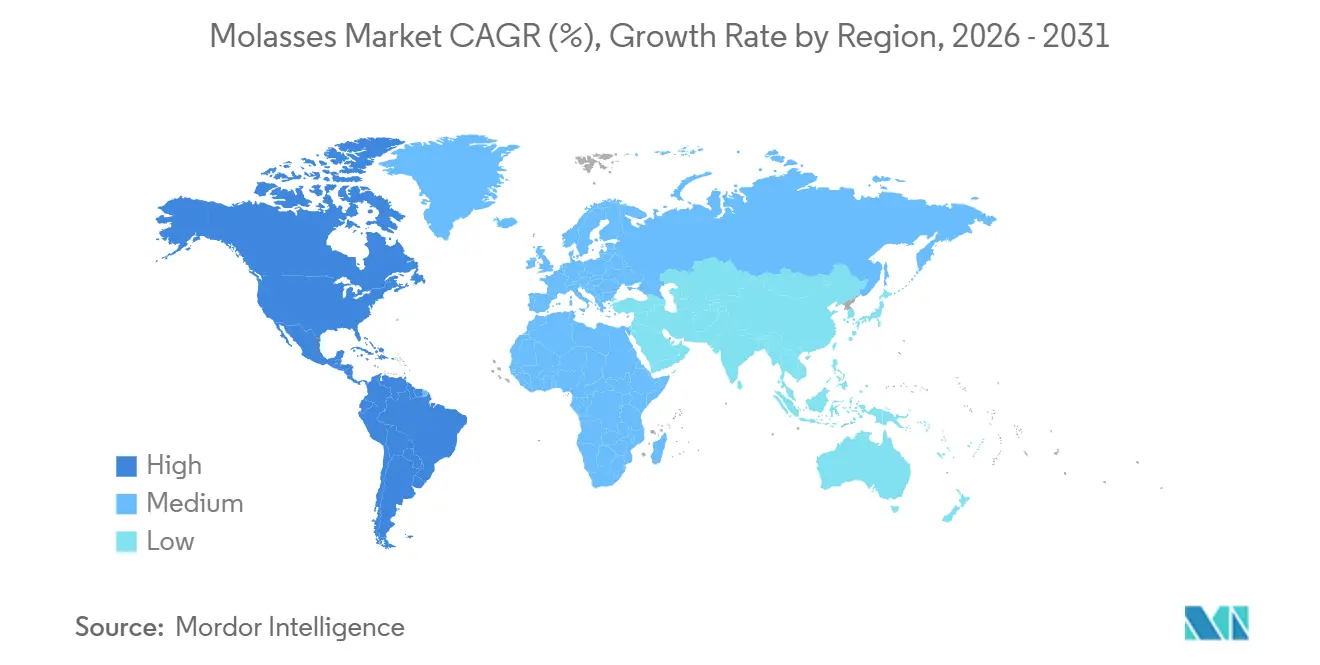

- By geography, Europe accounted for 40.58% of 2025 revenue, but South America is the fastest-growing region, with a 5.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Molasses Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising use of molasses in animal feed and livestock nutrition | +0.9% | Global, with concentration in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Growing demand for bioethanol production | +1.2% | Global, led by United States, Brazil, Philippines, and India | Short term (≤ 2 years) |

| Growing preference for natural, organic and clean-label sweeteners | +0.6% | North America and Europe, spillover to urban Asia-Pacific | Medium term (2-4 years) |

| Soil-biostimulant adoption in regenerative agriculture | +0.4% | North America and Europe organic-certified acreage, early adoption in Australia | Long term (≥ 4 years) |

| Advancements in biotechnology and precision fermentation | +0.7% | Global, with pilot-scale deployments in Europe, North America, and China | Long term (≥ 4 years) |

| Growth in craft alcohol and distillery industries | +0.3% | United States, Caribbean, and emerging South American craft corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising use of molasses in animal feed and livestock nutrition

Dairy and beef producers are increasingly incorporating molasses into total mixed rations to provide readily fermentable carbohydrates that stabilize rumen pH and enhance microbial protein synthesis. This shift aligns with the Association of American Feed Control Officials' Official Publication 2025 and is reflected in Canadian feed-ingredient definitions[1]Source: Association of American Feed Control Officials, “Official Publication 2025,” aafco.org. Additionally, pet food manufacturers are utilizing liquid molasses in extruded kibble formulations to mask the bitterness of alternative protein sources such as insect proteins and algae meals. This trend is further supported by European Union regulations on novel foods, which now permit the inclusion of black soldier fly larvae in companion-animal diets. In North America, feed mills are adopting advanced inline molasses-injection systems that enable precise, real-time metering of inclusion rates. These systems not only reduce batch-mixing variability but also lower labor requirements compared to manual drum additions, enhancing operational efficiency.

Growing demand for bioethanol production

Government-driven biofuel policies in major sugar-producing nations are increasing the utilization of sugarcane by-products, such as molasses, for ethanol production. The U.S. Environmental Protection Agency's Renewable Fuel Standard Set 2 rule has fixed conventional ethanol volumes at 15 billion gallons for 2025, promoting the diversification of ethanol feedstocks beyond corn[2]Source: U.S. Environmental Protection Agency, "Renewable Fuel Standard Program: Standards for 2025 and Beyond (Set 2 Rule)," epa.gov. In emerging markets such as the Philippines and India, governments are allocating a larger share of sugarcane output to ethanol production to meet national blending targets. For instance, India diverted 3.4 million metric tons of sugar to ethanol production in 2024/25 under its E20 program, while the Philippines mandated diverting 20% of sugarcane juice for ethanol production. These policies are altering global molasses trade flows, intensifying competition for molasses across fuel, feed, and beverage industries, and enhancing its commercial value and strategic role in industrial processing.

Advancements in biotechnology and precision fermentation

Industrial biotechnology platforms are increasingly utilizing molasses as a cost-effective feedstock for precision fermentation. For instance, Trichoderma reesei strains are being engineered to convert blackstrap sugars into cellulase enzymes at high titers, significantly reducing enzyme production costs for cellulosic ethanol plants. Additionally, lactic acid fermentation using molasses has reached commercial scale in countries such as Thailand and Brazil, achieving titers of 120-140 g/L. The downstream purification process produces food-grade lactate, which is essential for the manufacture of biodegradable polylactic acid (PLA) resins. Furthermore, yeast-protein fermentation is gaining traction, with Saccharomyces cerevisiae and Candida utilis metabolizing molasses into single-cell protein containing crude protein. This innovation is scaling rapidly in Europe and Asia, providing the aquaculture and pet food industries with non-soy alternatives that offer amino acid profiles comparable to those of fishmeal.

Growth in craft alcohol and distillery industries

Craft rum distilleries in the United States are sourcing single-estate molasses to differentiate terroir-driven expressions, with Tennessee producers such as Old Dominick and Louisiana's Oxbow Rum highlighting cane provenance on labels. American craft white-rum producers are bypassing Caribbean suppliers to procure molasses directly from Florida and Louisiana mills, cutting lead times and ensuring traceability that appeals to consumers prioritizing domestic agriculture. Whiskey and bourbon producers are experimenting with molasses-based neutral spirits as blending components to extend barrel-aged inventory, a strategy that preserves oak-matured character while reducing per-bottle costs. Regulatory frameworks such as the Alcohol and Tobacco Tax and Trade Bureau's Standards of Identity permit "rum" labeling only when fermentable sugars derive from sugarcane products, constraining molasses substitution in other spirit categories but cementing its role.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in sugarcane and sugar beet production | -0.8% | Global, acute in India, Thailand, European Union, and Australia | Short term (≤ 2 years) |

| Regulatory and food safety compliance burdens | -0.5% | Global, with heightened enforcement in European Union, India, and North America | Medium term (2-4 years) |

| Competition from alternative sweeteners and feed ingredients | -0.4% | North America and Europe for sweeteners; global for feed ingredients | Medium term (2-4 years) |

| Freight disruptions along major export routes | -0.3% | Middle East, South Asia, and East Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in sugarcane and sugar beet production

The Food and Agriculture Organization's Food Outlook revised global sugar production downward by 2.1 million metric tons to 178.3 million metric tons for 2025/26, citing El Niño-induced drought in Thailand that cut cane yields by 18% and European Union beet acreage contraction of 5.7% driven by low sugar prices and escalating input costs[3]Source: Food and Agriculture Organization, "Food Outlook: Biannual Report on Global Food Markets - November 2025," fao.org. Volatility in sugarcane and sugar beet production has become a significant concern, with unpredictable weather patterns, such as droughts and floods, increasingly impacting yields. Additionally, rising input costs, including fertilizers and labor, have further strained production. India's 2024/25 sugar output fell to 29.7 million metric tons as lower ratoon yields in Uttar Pradesh and Karnataka reduced per-hectare cane tonnage by 12-15%, tightening molasses availability and prompting the government to cap exports at 500,000 metric tons. These fluctuations in production are expected to influence global sugar prices and disrupt supply chains, creating challenges for both producers and end users.

Competition from alternative sweeteners and feed ingredients

High-fructose corn syrup retains cost advantages in North American beverage and bakery applications, and on a dry-solids basis, offers neutral flavor profiles that simplify formulation in light-colored products. Stevia extracts and monk-fruit concentrates are capturing share in zero-calorie beverage segments, with global stevia volumes growing annually as brands reformulate to meet consumer demand for "natural" non-nutritive sweeteners that carry no glycemic load. Additionally, erythritol and allulose, polyol and rare-sugar alternatives, are gaining traction in confectionery and dairy applications where molasses' dark color and robust flavor limit utility, particularly in premium ice creams and white-chocolate coatings. Alternative feed ingredients, such as corn and soy-based products, are increasingly competing with sugarcane by-products like molasses in animal feed formulations, driven by their consistent availability and lower prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Sugarcane Anchors Volume, Beet Gains on Policy Tailwinds

Sugarcane accounted for 82.11% of the global molasses market in 2025, driven by its widespread cultivation in tropical and subtropical regions, including Brazil, India, Thailand, and Pakistan. Brazil remains the largest producer, leveraging its extensive sugarcane plantations and integrated processing facilities to dominate global exports. India, the second-largest producer, primarily uses sugarcane molasses for domestic ethanol blending programs and animal feed production. Thailand and Pakistan continue to contribute significantly, with Thailand focusing on export markets and Pakistan catering to domestic demand for feed and ethanol production. Additionally, advancements in sugarcane processing technologies have improved molasses extraction efficiency.

Sugar beet is experiencing the fastest growth among source categories, with a 6.19% CAGR projected through 2031. This growth is fueled by European Union and Chinese policies favoring beet-derived bioethanol to reduce fossil fuel dependency and support local agriculture. Germany, France, and Poland have optimized extraction efficiencies, boosting regional molasses production. In addition, the EU's focus on sustainability and carbon reduction has incentivized the use of beet molasses in bioethanol production, further driving demand. China has expanded beet cultivation in Inner Mongolia and Xinjiang to reduce sugar imports, creating a surplus of beet molasses that has pressured domestic prices. This surplus has opened opportunities for feed exporters targeting Southeast Asia. The cost competitiveness of beet molasses is expected to improve as EU carbon pricing narrows the cost gap between beet ethanol and imported fossil fuels.

By Grade: Blackstrap Dominates on Mineral Density and Fermentation Utility

Blackstrap molasses accounted for 53.39% of the global molasses volume in 2025 and is projected to grow at a CAGR of 5.80% during the forecast period. This growth is driven by its increasing use in mineral-dense feed rations, particularly in North America and Oceania. The high concentrations of iron, calcium, and potassium in blackstrap molasses enable dairy producers to partially replace mineral premixes, thereby reducing feed costs. Additionally, its technical specifications, including a pH range of 5-6.5, Brix levels of 79-80%, and ash content of 10-15%, make it an optimal choice for fermentation processes critical to ethanol and organic acid production.

First molasses, which retains 60-70% sucrose content, is primarily utilized in the confectionery sector and commands a price premium. However, refiners are increasingly focusing on maximizing sugar extraction, leading to a decline in the share of first molasses in the market. Despite this, blackstrap molasses continues to dominate the fermentation-grade molasses segment due to its complete monosaccharide profile and enzyme-free processing. Its nutrient density and versatility across sectors ensure its sustained demand, even though its color and flavor characteristics limit its application in certain food products.

By Form: Liquid Retains Bulk Handling Edge, Powder Scales for Remote Markets

Liquid molasses dominated the market in 2025, accounting for 92.31% of the market share. This dominance is attributed to its lower processing costs and compatibility with bulk tanker logistics, making it a preferred choice for large-scale ethanol distilleries and industrial fermentation processes. The ability to directly inject liquid molasses from storage tanks to fermenters via pipelines eliminates the need for reconstitution steps, preserving microbial-available sugars that might otherwise degrade during thermal drying. Additionally, liquid molasses is widely used in animal feed formulations due to its ease of handling and nutrient-rich composition.

Powdered and granulated molasses are projected to grow at a robust CAGR of 7.07% through 2031. This growth is fueled by increasing adoption in remote feed mills across sub-Saharan Africa and Central Asia, where heated storage infrastructure is limited, and spoilage losses are a concern when handling liquid molasses in high-temperature environments. The advancement in spray-drying technology has significantly reduced the moisture content, extending the shelf life of powdered molasses to 18-24 months. This extended shelf life, coupled with the ability to transport and store at ambient temperatures, has simplified last-mile distribution to smallholder farms.

By Application: Food and Beverage Leads, Animal Feed Outpaces on Methane Mandates

Food and beverage applications accounted for 61.16% of the 2025 market share, led by bakery and confectionery, beverages, and dairy products that leverage molasses' caramel notes and humectant properties to extend shelf life. Sauces, soups, and marinades are embedding molasses to balance acidity and deliver umami depth in barbecue glazes and Asian-inspired condiments. Beverages, including craft sodas, cold-brew coffee, and ready-to-drink teas, are substituting molasses for cane sugar to achieve "clean-label" positioning. Dairy products such as yogurt and ice cream incorporate molasses to mask off-flavors from probiotic cultures and deliver caramel notes that resonate with consumers seeking indulgent yet natural formulations.

Animal feed and pet food are growing at a 6.85% CAGR through 2031, driven by precision-nutrition protocols that blend molasses with urea to deliver rumen-available nitrogen. Animal feed applications are bifurcating into ruminant (dairy, beef) and monogastric (poultry, swine) channels, with ruminant demand outpacing that of monogastrics due to molasses' role in stabilizing rumen pH and enhancing microbial protein synthesis. Molasses is being used as a palatability enhancer in feed formulations, improving feed intake and nutrient absorption in livestock. Its high energy content and cost-effectiveness make it a preferred ingredient in compound feed production, particularly in regions with large-scale livestock farming. Pet food formulators are layering liquid molasses into extruded kibble to mask bitterness from novel insect proteins and algae meals.

Geography Analysis

Europe accounted for 40.58% of the 2025 market share, driven by the region's strong focus on sustainability and renewable energy initiatives. Germany, France, and Poland are increasingly diverting beet juice to ethanol production, aligning with the European Union's carbon-reduction targets. Key European countries such as France, Germany, and Ukraine lead in beet molasses production due to their extensive sugar beet cultivation, providing a stable supply for both animal feed and industrial fermentation applications. The growing demand for bioethanol, coupled with advancements in extraction technologies, is expected to further strengthen Europe's position in the global molasses market.

South America is the fastest-growing region, with a projected CAGR of 5.18% through 2031. Brazil’s 603.67 million-ton Center-South crush and Argentina’s record 26.5 million-ton 2026/27 crop are driving regional growth. High hydrous-ethanol parity in São Paulo has led mills to allocate up to 95% of cane to fuel production, reducing exportable molasses and pushing FOB Santos prices to USD 185-195 per ton. While Chile, Colombia, and Peru remain smaller players, Chile's 2025 sugar production of 180,000 metric tons and Peru's 1.2 million metric tons generate molasses streams that primarily support local distilleries and livestock operations.

Asia-Pacific is witnessing steady growth, driven by evolving market dynamics and government initiatives. In India, the E20 program has redirected 3.4 million tons of sugar toward ethanol production, creating strong demand for molasses as a primary feedstock for distilleries. Thailand and China also contribute significantly, with Thailand producing around 10 million tons of cane molasses annually for domestic ethanol and export, while China’s sugar industry supports growing industrial and feed applications. North America remains relatively stable, with the United States producing approximately 8.5 million tons of sugar during the 2024/25 period, primarily cane-based molasses from Louisiana and Florida, presenting opportunities for further investment and innovation in the biofuel sector.

Competitive Landscape

The molasses market is moderately fragmented, with leading multinationals such as Wilmar, Cargill, ADM, and Louis Dreyfus leveraging vertical integration owning cane plantations, sugar mills, ethanol distilleries, and bulk-liquid terminals, to capture margin across crushing, refining, and downstream fermentation. This integration enables cost efficiencies and risk mitigation across sugar, fuel, and feed markets. For instance, Raizen’s integrated São Paulo complex exemplifies this approach by co-locating ethanol production, yeast protein manufacturing, and molasses dewatering facilities to maximize revenue streams.

Regional cooperatives are increasingly focusing on securing price premiums through certifications such as Bonsucro, Organic, and Fair Trade. However, adoption of these certifications remains limited, accounting for less than 15% of global trade, as audit costs range from USD 10,000 to USD 25,000 per site. Process innovations are also gaining traction, with advancements such as vacuum evaporators that reduce moisture content to 20-22%, in-line viscosity sensors that enhance blending precision, and blockchain pilots like ABF’s 50,000-ton traceability test in the United Kingdom. Additionally, biotechnology firms are entering the market, aiming to convert molasses into value-added products such as lactic acid, PHA biopolymers, and single-cell proteins.

Regulatory compliance is emerging as a critical competitive advantage in the molasses market. ISO 22000 re-audits, EU 2017/625 controls, and expanding HACCP mandates favor mills with established quality management systems. Smaller processors often redirect their output to domestic or regional markets to avoid the annual compliance costs, which range from USD 15,000 to USD 30,000. Freight volatility further underscores the importance of strategic investments in export infrastructure. For example, Louis Dreyfus’ 2025 acquisition of a 300,000-ton Santos facility secures direct access to Asian markets while mitigating risks associated with port congestion.

Molasses Industry Leaders

-

Wilmar International Limited

-

Cargill, Incorporated

-

The Archer-Daniels-Midland Company

-

Louis Dreyfus Company

-

Hartree Partners (ED&F Man Holdings)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Hartree Partners, a global energy and commodities trading firm, acquired ED&F Man Commodities' four major business units: Volcafe (coffee), ED&F Man Liquid Products (molasses, animal feed, and fish oil), ED&F Man Sugar, and ED&F Man Cotton. The acquisition followed Hartree's takeover of ED&F Man's senior secured debt and received all regulatory approvals. The transaction expanded Hartree's soft commodities portfolio, incorporating molasses trading operations and distribution networks that serve over 20 million animals daily and provide feedstock to the fermentation industry.

- May 2024: Michigan Sugar Company inaugurated a molasses desugarization facility at its Bay City sugar-beet processing plant. The 22,000 sq ft facility, completed after four years of development at a cost of USD 109 million, processes 100% of byproduct molasses, up from 60% previously. The facility doubled daily processing capacity from 325 to 650 tons and enables recovery of up to 80 million additional pounds of sugar annually.

- April 2023: The Nira Bhima Sahakari Sakhar Karkhana Ltd. in Shahajinagar, Pune (Maharashtra), announced plans to upgrade its molasses-based distillery. The expansion will increase ethanol production capacity from 30 KLPD to 300 KLPD. The project includes increasing sugarcane crushing capacity from 3,500 to 7,500 TCD and expanding cogeneration power output from 18 MW to 24 MW, utilizing both heavy molasses and cane syrup (C/B grades).

Global Molasses Market Report Scope

Molasses is a thick, dark brown, or light syrup produced during the refining of sugarcane or sugar beets into sugar, or by boiling down sugary fruit/vegetable juices.

The molasses market is segmented by source, grade, form, application, and geography. Based on source, the market is segmented into sugarcane, sugar beet, and others. By form, the market is segmented into first/light, second/dark, and blackstrap. By form, the market has been segmented into liquid and powder/granules. By application, the market has been segmented into food and beverage, animal feed and pet food, biofuel/ethanol, and others. By geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD).

| Sugarcane |

| Sugar Beet |

| Others |

| First/Light |

| Second/Dark |

| Blackstrap |

| Liquid |

| Powder/Granules |

| Food and Beverage | Bakery and Confectionery |

| Sauces, Soups, and Marinades | |

| Beverages | |

| Dairy Products | |

| Others | |

| Animal Feed and Pet Food | |

| Biofuel/Ethanol | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | Sugarcane | |

| Sugar Beet | ||

| Others | ||

| By Grade | First/Light | |

| Second/Dark | ||

| Blackstrap | ||

| By Form | Liquid | |

| Powder/Granules | ||

| By Application | Food and Beverage | Bakery and Confectionery |

| Sauces, Soups, and Marinades | ||

| Beverages | ||

| Dairy Products | ||

| Others | ||

| Animal Feed and Pet Food | ||

| Biofuel/Ethanol | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the molasses market in 2026 and what is the forecast growth?

The molasses market size stands at USD 9.40 billion in 2026 and is expected to reach USD 11.80 billion by 2031, advancing at a 4.66% CAGR.

Which source segment dominates the molasses market, and which is growing the fastest?

Sugarcane dominates with 82.11% of 2025 volume, while sugar beet is the fastest-growing source, expanding at 6.19% CAGR through 2031.

What grade of molasses holds the largest market share and shows the highest growth potential?

Blackstrap accounted for 53.39% of 2025 volume and projects the quickest grade-level CAGR of 5.80% to 2031.

Which application segment is expanding fastest?

Animal feed and pet food are rising at 6.85% CAGR as regulators target enteric methane cuts and nutritionists deploy molasses-urea blends.

Which region will grow most rapidly?

South America leads with a 5.18% CAGR, fueled by Brazil’s ethanol pivot and Argentina’s E12-E15 mandates.

Page last updated on: