Icing Sugar Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

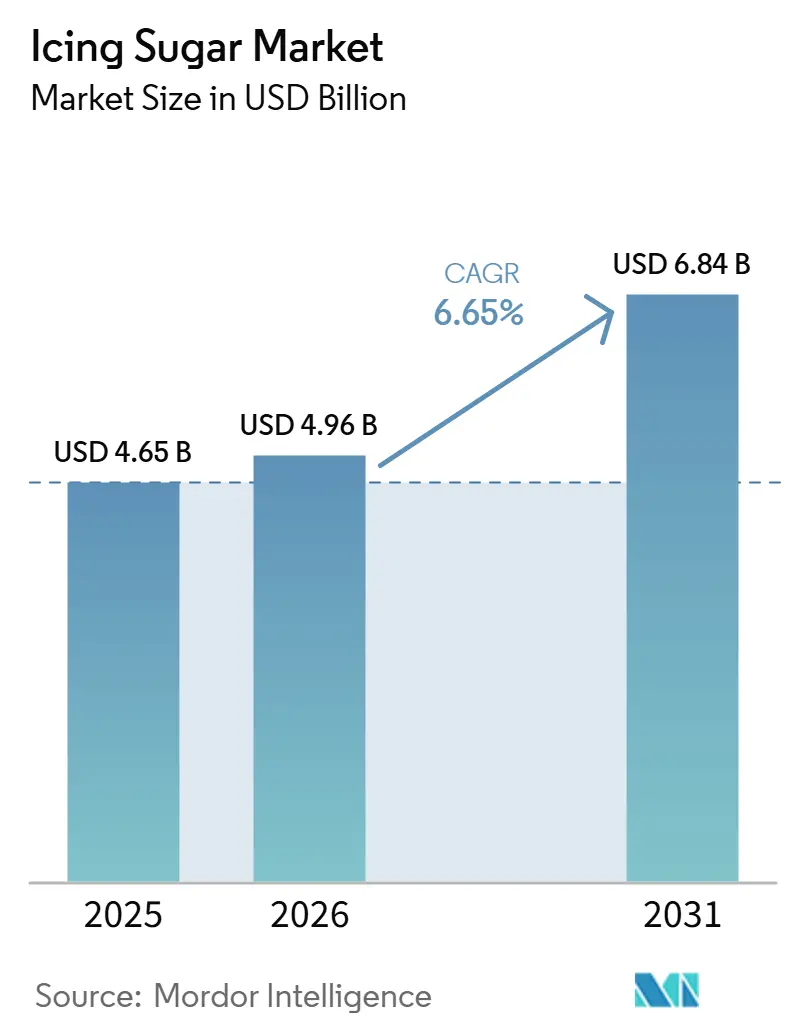

| Market Size (2026) | USD 4.96 Billion |

| Market Size (2031) | USD 6.84 Billion |

| Growth Rate (2026 - 2031) | 6.65% CAGR |

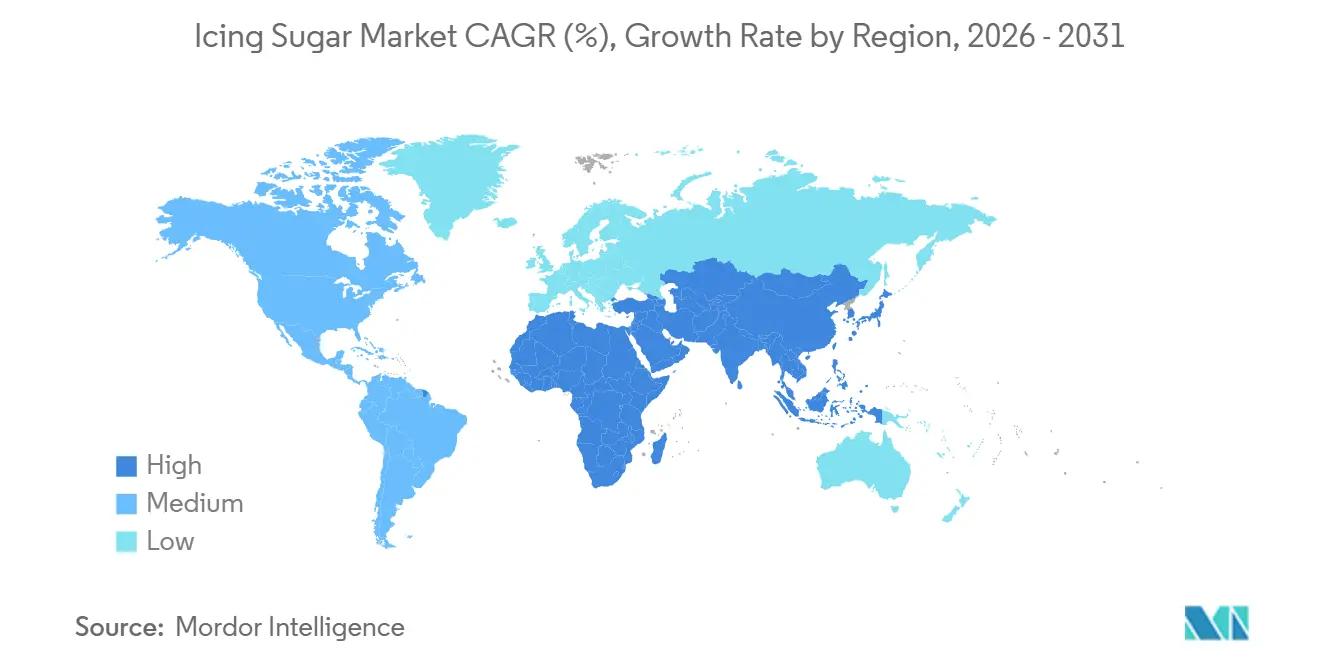

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Icing Sugar Market Analysis by Mordor Intelligence

The global icing sugar market is witnessing steady growth, increasing from USD 4.65 billion in 2025 to USD 4.96 billion in 2026, and is projected to reach USD 6.84 billion by 2031, with a CAGR of 6.65% during the forecast period of 2026–2031. This growth is largely attributed to the rising industrialization of food production systems, where manufacturers demand standardized, high-performance ingredients to ensure consistency, efficiency, and scalability. Icing sugar, characterized by its fine particle size and uniform composition, meets these requirements, facilitating its integration into automated and high-speed production processes. Furthermore, advancements in milling and refining technologies are improving product quality, enhancing flowability, and reducing processing variability, thereby driving its adoption in large-scale manufacturing operations.

Key Report Takeaways

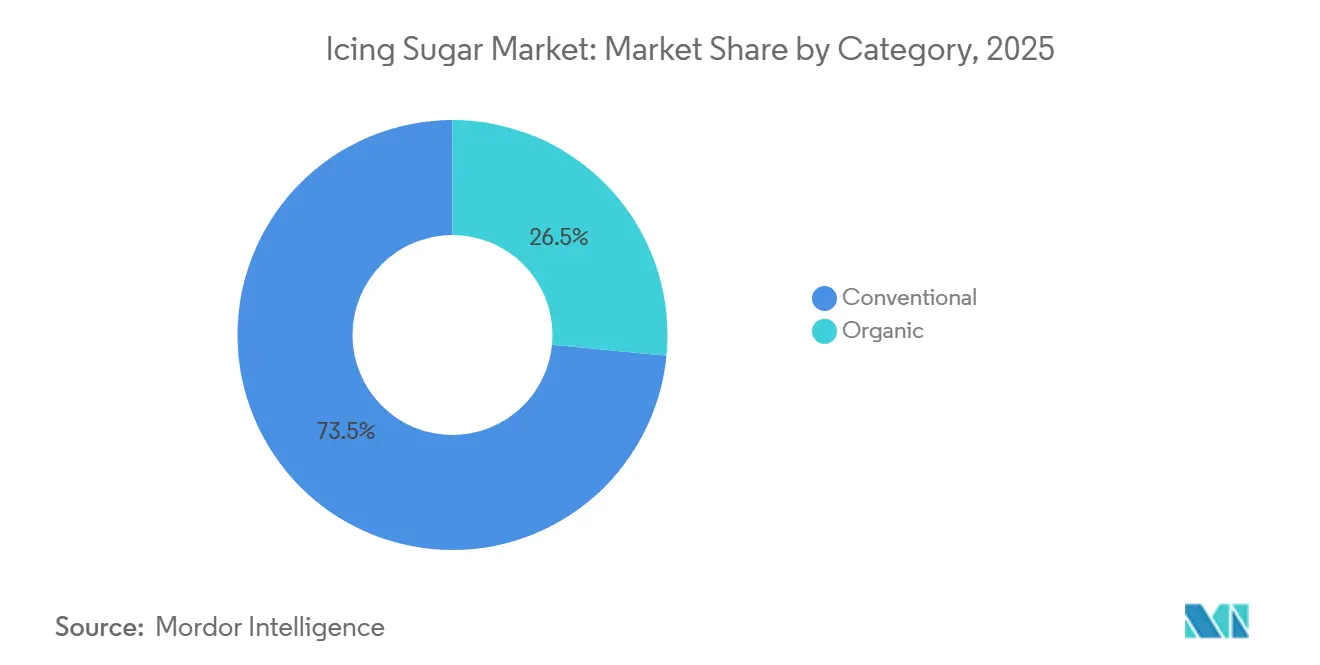

- By category, the conventional segment held 73.46% of 2025 sales, while organic products are expanding at an 8.11% CAGR through 2031 MORDORINTELLIGENCE.COM.

- By product type, 10X granulations commanded 48.49% of 2025 revenue, whereas 12X and other ultra-fine grades are projected to grow at a 6.87% CAGR to 2031.

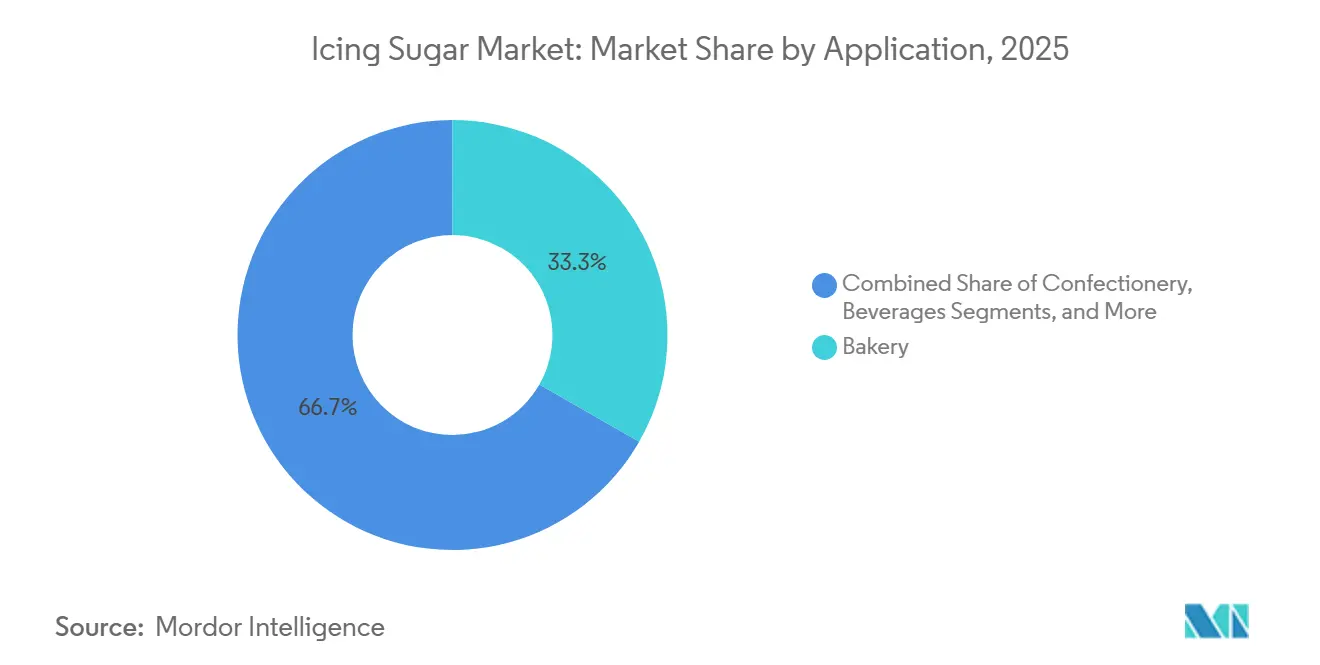

- By application, bakery captured 33.26% of 2025 demand, but dairy and frozen desserts are advancing at a 7.45% CAGR over 2026-2031.

- By distribution channel, B2B and industrial outlets accounted for 63.32% of the Icing Sugar market size in 2025, while retail is forecast to rise at an 8.56% CAGR through 2031.

- By geography, Europe led with a 38.09% market share in 2025, whereas Asia-Pacific is set to record the fastest 8.04% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Icing Sugar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumption of bakery and confectionery products | +1.8% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Growth of café culture and foodservice outlets | +1.2% | Urban centers in Asia-Pacific, Europe, and North America | Short term (≤ 2 years) |

| Development of organic, low-calorie, and flavored icing sugars | +1.5% | North America, Europe, and premium segments in Asia-Pacific | Long term (≥ 4 years) |

| Growth in celebration culture | +0.9% | Global, with emphasis on emerging markets in Asia and MEA | Medium term (2-4 years) |

| Growing influence of social media food trends | +0.7% | Global, led by digitally connected urban populations | Short term (≤ 2 years) |

| Increasing demand for ready-to-eat desserts | +1.1% | Asia-Pacific, North America, and urban Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising consumption of bakery and confectionery products

The increasing consumption of bakery and confectionery products is a significant driver of the global icing sugar market, as it boosts the demand for essential ingredients in large-scale food production. The ongoing growth of industrial bakery and confectionery manufacturing has resulted in greater procurement of standardized inputs like icing sugar, ensuring consistent processing and formulation efficiency. As manufacturers expand production to cater to changing consumer preferences for indulgent and premium sweet products, the demand for reliable, high-quality sugar ingredients has grown. Furthermore, the rise of organized food production systems and automated processing lines has strengthened the demand for icing sugar due to its uniform particle size and ease of integration into production workflows. This consistent growth in bakery and confectionery production across both developed and emerging markets remains a key factor driving the icing sugar market.

Growth of café culture and foodservice outlets

The growth of café culture and foodservice outlets, driven by the rapid expansion of organized dining and beverage service formats, is increasing the demand for standardized ingredient inputs in professional kitchens. The rise of cafés, quick-service restaurants, and mobile foodservice operators has created a need for consistent, high-quality ingredients to support efficient, high-volume preparation processes. This trend is particularly prominent in Europe, where the foodservice sector is well-developed and continues to grow. According to Eurostat, in 2024, France led Europe in the number of enterprises in restaurants and mobile food service activities, with 178,780 establishments, followed by Italy with 158,820 and Germany with 142,450 [1]Source: Eurostat, "Restaurants and mobile food service enterprises in the European Union", ec.europa.eu. This extensive and expanding network of foodservice outlets is driving large-scale procurement of essential ingredients, such as icing sugar, as operators focus on efficiency, consistency, and standardized preparation across their locations.

Development of organic, low-calorie, and flavored icing sugars

The development of organic, low-calorie, and flavored icing sugars is driving growth in the global icing sugar market, as manufacturers prioritize product diversification and value-added innovation to address changing industry demands. Companies are broadening their product portfolios to include organic-certified options, reduced-calorie formulations, and flavored variants, enabling differentiation in a competitive market. These advancements are facilitated by improvements in ingredient processing and formulation techniques, which allow producers to maintain functional performance while altering composition or flavor profiles. For example, Organic Times offers icing sugar made from certified organic golden cane sugar, reflecting the increasing focus on clean-label and certified ingredient sourcing. These trends are prompting manufacturers to invest in specialized production capabilities and certification processes, enhancing product positioning and creating opportunities for premium offerings.

Growth in celebration culture

The growing emphasis on celebration culture, marked by the increasing frequency and scale of social and cultural events, is driving demand for standardized ingredient inputs within organized production systems. Events such as birthdays, weddings, anniversaries, and festive gatherings are becoming more elaborate and frequent, leading to higher production volumes in the bakery and dessert manufacturing industry. This trend is further reinforced by the commercialization of celebrations, where event planning, customized offerings, and large-scale catering services require consistent, high-quality ingredients to ensure uniform results. Moreover, the influence of social media and evolving consumer expectations regarding presentation and personalization have prompted more structured and professionalized production processes, increasing the reliance on ingredients like icing sugar to achieve precision and consistency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing health concerns related to sugar consumption | -1.4% | Global, with regulatory intensity highest in Europe and North America | Long term (≥ 4 years) |

| Regulatory pressure on sugar reduction | -1.1% | Europe, North America, and select Asia-Pacific markets (e.g., Singapore) | Medium term (2-4 years) |

| Short shelf life and moisture sensitivity | -0.6% | Tropical and high-humidity regions in Asia-Pacific and MEA | Short term (≤ 2 years) |

| Fluctuations in raw material quality | -0.5% | Global, with acute impacts in beet-growing regions of Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing health concerns related to sugar consumption

Health concerns related to sugar consumption are a significant restraint on the global icing sugar market. Growing awareness of diet-related health issues, such as obesity and type 2 diabetes, is influencing ingredient choices within the food industry. Consumers and manufacturers are increasingly limiting the use of high-sugar ingredients, driving reformulation strategies aimed at reducing sugar content or replacing traditional sugars with alternative sweeteners. Furthermore, public health campaigns, nutritional labeling requirements, and industry-wide sugar reduction initiatives are pressuring manufacturers to adjust formulations, directly affecting the demand for icing sugar. Consequently, the emphasis on health-conscious consumption patterns continues to limit the growth potential of the icing sugar market.

Regulatory pressure on sugar reduction

Regulatory pressure to reduce sugar consumption is a significant restraint on the global icing sugar market. Governments and health authorities are increasingly introducing policies aimed at reducing sugar intake in processed foods. These policies include stricter nutritional labeling requirements, sugar taxes, reformulation targets, and front-of-pack warnings, which are driving manufacturers to lower added sugar levels in their products. Compliance with these regulations often necessitates substantial adjustments in formulation and processing, limiting the use of traditional icing sugar. Furthermore, industry-wide initiatives promoting sugar reduction are accelerating the adoption of alternative sweeteners and modified ingredient systems. As regulatory scrutiny intensifies globally, it continues to restrict the demand for icing sugar by encouraging manufacturers to develop lower-sugar or sugar-free formulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Conventional Dominance Masks Organic's Margin Contribution

The conventional icing sugar segment accounted for 73.46% of the global market share in 2025, primarily due to its strong supply-side advantages, standardized production processes, and widespread industry acceptance. This segment benefits from a well-established manufacturing infrastructure, where refined sugar is processed into fine powdered form using efficient, large-scale milling and anti-caking technologies. These processes ensure consistent quality and uniform particle size. Its dominance is further supported by robust global supply chains, which facilitate easy availability, reliable distribution, and uninterrupted procurement for both bulk and retail buyers. Additionally, conventional icing sugar complies with existing regulatory frameworks and does not require specialized certifications, unlike organic or specialty variants. This simplifies production, labeling, and market entry for manufacturers.

The organic icing sugar segment is emerging as a fast-growing category, with a projected CAGR of 8.11% through 2031. This growth is driven by increasing consumer demand for clean-label, sustainably sourced, and minimally processed ingredients. The segment's expansion is supported by the growing global organic ecosystem, where production capacity and raw material availability are steadily improving. For example, according to Organics International, the number of organic producers worldwide reached 4.8 million in 2024, reflecting significant growth in certified agricultural practices [2]Source: Eurostat, "Restaurants and mobile food service enterprises in the European Union", ec.europa.eu. This increase in organic farming enhances the supply of organically cultivated sugarcane, the primary input for organic icing sugar, thereby strengthening the segment’s production base.

By Product Type: Ultra-Fine Granulations Capture Premiumization

The 10X granulation segment, accounting for 48.49% of the global icing sugar market share in 2025, is a key driver of the market due to its balance of fineness, functionality, and processing efficiency. This segment benefits from a standardized particle size distribution, ensuring consistent performance in industrial-scale operations without requiring additional refinement or adjustments. The 10X grade is widely favored by manufacturers for its superior flowability and controlled dusting characteristics, which facilitate smoother handling in automated production systems. Its uniformity also minimizes variability during mixing and blending processes, enhancing batch consistency and reducing production losses.

The 12X and ultra-fine granulation segments are experiencing steady growth, with a projected CAGR of 6.87% through 2031. This growth is driven by their superior refinement, precision processing, and alignment with advanced manufacturing requirements. These finer grades are produced using advanced milling and sieving technologies, resulting in extremely small and uniform particle sizes that improve consistency in formulation processes. The demand for these grades is supported by the increasing need for high-performance ingredients that enable better dispersion, faster dissolution, and smoother integration within complex production systems.

By Application: Dairy and Frozen Desserts Outpace Traditional Bakery

The bakery segment, accounting for 33.26% of global icing sugar demand in 2025, is a significant contributor to market growth due to its integration within large-scale production systems and reliance on standardized, high-performance ingredients. This segment benefits from highly organized and industrialized manufacturing environments where consistency, precision, and process efficiency are essential. Icing sugar plays a crucial role in ensuring uniform mixing, stable formulations, and repeatable output across automated bakery production lines. The segment's dominance is further reinforced by the global expansion of industrial bakery operations, where manufacturers require ingredients that integrate seamlessly into high-speed processing equipment without causing variability or disruptions.

The dairy and frozen desserts segment is emerging as a high-growth area within the icing sugar market, projected to grow at a CAGR of 7.45% through 2031. This growth is driven by increasing demand for precision-based ingredient integration and advanced processing requirements. The segment relies on ingredients that ensure consistent solubility, smooth dispersion, and stable performance under varying temperature conditions, particularly in chilled and frozen processing environments. Icing sugar, with its fine particle structure, facilitates uniform incorporation into formulations, minimizes crystallization inconsistencies, and enhances processing efficiency. Additionally, advancements in dairy processing technologies are supporting this growth, as manufacturers focus on improving texture stability, batch uniformity, and production scalability.

By Distribution Channel: Retail Gains Share Despite B2B Dominance

The B2B and industrial distribution channel, which accounted for 63.32% of the global icing sugar market share in 2025, plays a significant role in driving the market. This channel aligns closely with large-scale procurement systems and structured supply networks. It is primarily driven by bulk purchasing practices, where manufacturers and institutional buyers depend on long-term supplier contracts to ensure consistent availability and price stability. The dominance of this channel is further reinforced by its well-organized logistics and distribution infrastructure, enabling efficient movement of large volumes with minimal supply disruptions. Moreover, B2B channels foster direct relationships between producers and end-users, reducing intermediaries and providing better control over quality specifications, customization requirements, and delivery schedules.

The retail distribution channel is experiencing robust growth, with a projected CAGR of 8.56% through 2031. This growth is fueled by increasing product accessibility, evolving consumer purchasing behavior, and the rapid expansion of organized retail formats. The segment benefits from the rising penetration of supermarkets, hypermarkets, and e-commerce platforms, which enhance the availability of icing sugar to a wider consumer base. Retail channels also allow manufacturers to offer diverse packaging sizes and formats, catering to varying consumer preferences and improving product visibility both on shelves and online. Additionally, advancements in packaging technology, such as moisture-resistant and resealable packs, support product stability and convenience, further driving retail purchases.

Geography Analysis

Europe is projected to hold 38.09% of the global icing sugar market share in 2025, maintaining its position as the leading regional contributor. This dominance is supported by a well-established sugar refining infrastructure, advanced processing technologies, and the strong presence of organized manufacturers. However, the region faces structural challenges that are moderating its growth. Persistently low sugar prices are compressing producer margins, while elevated sugar beet cultivation costs are creating input-side pressures for refiners. Additionally, evolving regulatory frameworks within the European Union, particularly concerning sugar production quotas, sustainability standards, and labeling requirements, are introducing uncertainty for market participants. These factors collectively constrain growth despite the region’s mature supply chain and high level of industry standardization.

Asia-Pacific is the fastest-growing region in the global icing sugar market, with a projected CAGR of 8.04% through 2031. This growth is driven by rapid structural transformation across food systems and supply chains. Factors such as increasing urbanization, rising income levels, and the accelerated development of modern retail and organized foodservice networks are enhancing distribution efficiency and product accessibility. The region’s strong reliance on sugar imports further supports the availability of refined sugar inputs necessary for icing sugar production. Countries like China and Indonesia rank among the world’s largest sugar importers. For example, according to the United States Department of Agriculture (USDA), China was projected to import 5.3 million metric tons of centrifugal sugar in the marketing year 2025/26, underscoring the scale of raw material inflows that facilitate downstream processing and market expansion in the region [3]Source: United States Department of Agriculture (USDA), "Principal sugar importing countries in 2025/2026", usda.gov.

North America, South America, and the Middle East and Africa collectively account for the remaining share of the global icing sugar market, exhibiting diverse and region-specific growth trends. In North America, a highly industrialized and efficient supply chain supports stable demand, although regulatory scrutiny regarding sugar consumption continues to influence market dynamics. South America benefits from robust sugar production capabilities, particularly in key exporting nations, which ensures raw material availability and supports regional processing activities. In the Middle East and Africa, a growing reliance on imports and the ongoing development of food processing infrastructure are gradually strengthening the region’s position in the market.

Competitive Landscape

The global icing sugar market is moderately fragmented, with numerous regional processors operating alongside a core group of large, vertically integrated sugar producers and refiners that dominate the upstream supply chain. While smaller players focus on localized markets with limited scale, global trade and refining activities are concentrated among a few established companies. These companies maintain strong control over raw material sourcing, processing infrastructure, and distribution networks. This structure allows leading firms to ensure consistent product quality, optimize costs through economies of scale, and provide reliable supply across multiple regions, thereby strengthening their competitive position despite the fragmented nature of downstream operations.

Prominent players in the market include Südzucker AG, Tereos S.A., Cargill, Incorporated, American Sugar Refining, Inc., and Nordzucker AG. These companies leverage vertically integrated operations encompassing sugar beet or cane sourcing, refining, and ingredient manufacturing. This integration enables them to exercise greater control over pricing, quality, and supply chain efficiencies. Their global presence, coupled with established relationships with industrial buyers and distributors, allows them to secure a significant share of bulk and contract-based demand. Furthermore, investments in process optimization, refining technologies, and logistics infrastructure support large-scale production while ensuring standardized product specifications.

Technological and strategic advancements are gradually shaping the market, with a growing focus on precision milling, particle size standardization, and improved moisture control to enhance product performance and shelf stability. Additionally, opportunities are emerging in niche segments such as organic and ultra-fine granulations. However, these segments face higher certification requirements, specialized processing needs, and capital-intensive infrastructure, which act as barriers to entry. These factors create a relatively protected competitive environment for early entrants, enabling them to achieve premium positioning and higher margins.

Icing Sugar Industry Leaders

-

Südzucker AG

-

Tereos S.A.

-

Cargill, Incorporated

-

American Sugar Refining, Inc. (Domino Foods)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: AB Mauri relaunched the Mauri Icing Sugar, the first and only SLS-certified icing sugar in Sri Lanka. It is produced using advanced German technology, adhering to the highest standards of quality and safety.

- January 2026: Truly (UK) Ltd, a Shropshire-based supplier of sprinkles and cake decorations, has acquired Sugar and Crumbs, a company specializing in flavored icing sugar. This acquisition represents a strategic effort to enhance product offerings and reinforce its position in the baking ingredients market.

- June 2024: French sugar brand Cristalco has replaced its previous plastic container with a Sonoco cardboard container featuring a polypropylene (PP) sprinkler, which the company claims makes the packaging fully recyclable. In an effort to reduce the carbon footprint of its packaging, Cristalco has redesigned its 500g Daddy Sugar icing sugar sprinkler container.

Global Icing Sugar Market Report Scope

Icing sugar is a very finely ground, powdery sugar mixed with a small amount of anti-caking agent to prevent clumping. The icing sugar market is segmented by category, product type, application, distribution channel, and geography. Based on category, the market is segmented into conventional, and organic. Based on product type, the market is segmented into 6X granulation, 10X granulation, and 12X / ultra-fine. Based on application, the market is segmented into bakery, confectionery, beverages, dairy and frozen desserts, and others. By distribution channel, the market is segmented into B2B / Industrial/HoReCa, and retail. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

| Conventional |

| Organic |

| 6X Granulation |

| 10X Granulation |

| 12X / Ultra-fine |

| Bakery |

| Confectionery |

| Beverages |

| Dairy and Frozen Desserts |

| Others |

| B2B / Industrial/HoReCa |

| Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Category | Conventional | |

| Organic | ||

| By Product Type | 6X Granulation | |

| 10X Granulation | ||

| 12X / Ultra-fine | ||

| By Application | Bakery | |

| Confectionery | ||

| Beverages | ||

| Dairy and Frozen Desserts | ||

| Others | ||

| By Distribution Channel | B2B / Industrial/HoReCa | |

| Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global Icing Sugar market in 2026?

It is valued at USD 4.96 billion and is projected to reach USD 6.84 billion by 2031 at a 6.65% CAGR.

Which region will grow fastest through 2031?

Asia-Pacific leads with an 8.04% CAGR, driven by urbanization, rising incomes, and café proliferation.

What product type is gaining share fastest?

12X ultra-fine granulations, growing at 6.87% annually due to superior solubility and visual finish.

How is retail performing versus B2B?

Retail is expanding at 8.56% a year, faster than B2B, supported by e-commerce and home-baking trends.

Page last updated on: