Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 55.40 Billion |

| Market Size (2026) | USD 57.62 Billion |

| Market Size (2031) | USD 70.13 Billion |

| Growth Rate (2026 - 2031) | 4.01% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Cane Sugar Market Analysis by Mordor Intelligence

The Indian cane sugar market size was valued at USD 55.40 billion in 2025 and estimated to grow from USD 57.62 billion in 2026 to reach USD 70.13 billion by 2031, at a CAGR of 4.01% during the forecast period (2026-2031). Consistent government mandates on ethanol blending, abundant domestic cane supplies, and steady demand from food processors underpin this growth path. Mills are diversifying into biofuel production, stabilizing cash flows, and reducing exposure to volatile wholesale prices. Investments in precision farming and micro-irrigation are increasing cane yields while reducing water use, thereby strengthening raw-material security for the Indian cane sugar market. Regulatory headwinds tied to rising health concerns are reshaping product portfolios toward low-sugar and organic variants, yet volume demand from beverages, bakery, and dairy continues to anchor overall consumption. Technology upgrades, including computer-integrated manufacturing and AI-enabled cane management, are giving early adopters a competitive cost edge and faster throughput.

Key Report Takeaways

- By form, crystallized sugar led with 61.78% of the Indian cane sugar market share in 2025, while liquid sugar is projected to grow at a 5.31% CAGR through 2031.

- By category, conventional sugar commanded 71.55% share of the Indian cane sugar market size in 2025; organic sugar is advancing at a 5.62% CAGR to 2031.

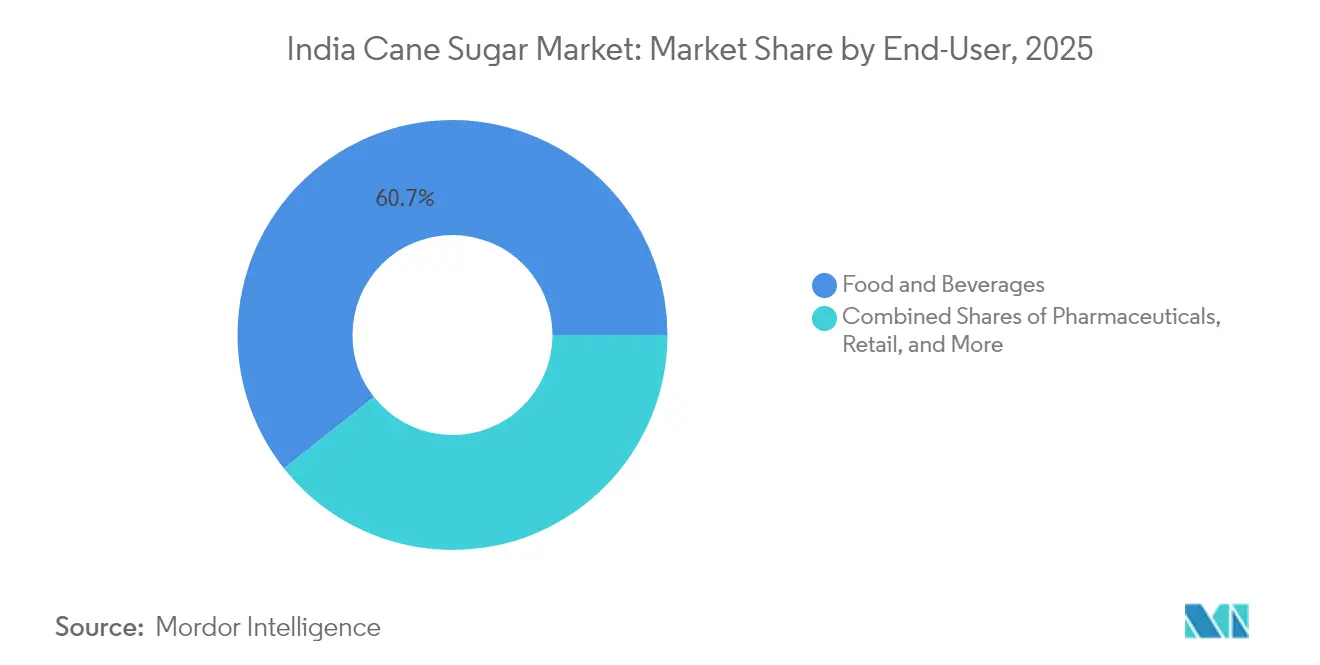

- By end-user, food and beverage applications held 60.66% in 2025, whereas pharmaceutical demand is climbing at a 5.92% CAGR through 2031.

- By geography, North India accounted for a 38.12% share of the Indian cane sugar market in 2025; West India offers the fastest growth at a 6.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Cane Sugar Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong government policies and abundant domestic raw materials bolster cane sugar production | +1.2% | National, with concentration in Uttar Pradesh, Maharashtra, Karnataka | Long term (≥ 4 years) |

| Expanding industrial sugar demand from beverages & processed foods | +0.9% | National, with early gains in North and West India | Medium term (2-4 years) |

| Expansion of Agro-Processing Units | +0.7% | National, spill-over to rural areas | Medium term (2-4 years) |

| Rising Interest in Ethanol Blending | +1.1% | National, with focus on major sugar-producing states | Long term (≥ 4 years) |

| Micro-irrigation & high-yield cane varieties adoption | +0.6% | National, with concentration in Maharashtra, Tamil Nadu | Long term (≥ 4 years) |

| Availability of Multiple Sugar Grades | +0.4% | National, with focus on industrial clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strong government policies and abundant domestic raw materials bolster cane sugar production

The Indian government has transformed the country's cane sugar market through strategic ethanol blending mandates and production incentives. By July 2024, the ethanol blending program achieved a 13.3% blending rate, with petroleum companies procuring 3.91 billion liters from the sugar industry for the 2024-25 period. Demonstrating policy flexibility, the government lifted the ban on using sugarcane juice for ethanol production in August 2024 to balance domestic sugar supply with biofuel objectives. This shift has enabled sugar mills to diversify their revenue streams. For example, major producers like Balrampur Chini Mills have generated additional income of up to INR 25 crore from ethanol production using C-heavy molasses. Additionally, the implementation of stored syrup technology (biosyrup) facilitates year-round ethanol production, addressing the seasonal limitations of traditional sugar operations.

Expanding industrial sugar demand from beverages and processed foods

The food processing industry is expected to reach USD 700 billion by 2030, driving significant demand for industrial sugar applications beyond traditional uses, according to the India Brand Equity Foundation[1]India Brand Equity Foundation, "Indian food processing industry to reach Rs. 60,65,500 crore (USD 700 billion) by 2030: PHD Chamber of Commerce and Industry (PHDCCI)", www.ibef.org. This growth is particularly notable in tier II and III cities, where increasing disposable incomes are fueling demand for processed foods, beverages, and confectionery products, as reported by the U.S. Department of Agriculture[2]United States Department of Agriculture, "India: Food Processing Ingredients Annual", www.fas.usda.gov. Additionally, the pharmaceutical sector's rising need for pharmaceutical-grade sugar is creating niche opportunities, with liquid sugar gaining popularity due to its superior dissolution properties and contamination control. The bakery and confectionery segments are expanding as consumer preferences shift toward premium products, while the dairy and frozen foods industries are increasing sugar usage for texture enhancement and preservation. Moreover, the development of specialty sugar grades, such as organic and raw variants, is enabling manufacturers to adopt premium positioning strategies aimed at health-conscious consumers.

Expansion of Agro-Processing Units

The Uttar Pradesh government has allocated USD 224.75 million to expand sugar mill capacities, marking a strategic investment aimed at improving the sector's operational efficiency. This initiative aligns with advancements in sugar processing technology, including the implementation of Computer Integrated Manufacturing systems, which enhance production efficiency and quality control, as noted by the Technology Information Forecasting and Assessment Council[3]Technology Information Forecasting and Assessment Council, "Automated machinery & production system for manufacturing capital equipment for the sugar industry", www.tifac.org. Additionally, artificial intelligence is revolutionizing sugarcane farming practices, enabling farmers to increase yields from 50-60 tons to 65-75 tons per acre while reducing water usage by 35-45%. On the sustainability front, zero-emission processing plants, such as the innovative facility in Assam, are establishing new benchmarks that may influence regulatory standards and consumer preferences. Furthermore, the sector's diversification efforts are evident in Triveni Engineering's expansion of its distillery capacity to 860 KLPD in 2024.

Rising Interest in Ethanol Blending

By 2025-26, the government's goal of achieving a 20% ethanol blending target has transformed sugar mills into integrated bio-refineries. Ethanol production has evolved from being a secondary by-product to a key profit driver. The allocation of 4 to 4.5 million tonnes of sugar for ethanol during the 2024-25 crushing season highlights this major shift. This transition necessitates efficient supply chain management to balance domestic sugar requirements with biofuel objectives. Additionally, the government has introduced premiums of INR 6.87 per liter for C-heavy molasses ethanol production. These measures enhance mill profitability and facilitate timely payments to farmers. However, policy inconsistencies regarding the use of sugarcane juice for ethanol have created uncertainty. Industry associations are advocating for stable, long-term policies to support sustained investments in distillery infrastructure.

Restraints Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising anti-sugar health regulations | -0.8% | National, with focus on urban centers | Medium term (2-4 years) |

| Increasing Health Awareness about sugar consumption | -0.6% | National, with concentration in metro cities | Long term (≥ 4 years) |

| Emergence of sugar alternatives | -0.5% | National, with early adoption in urban markets | Long term (≥ 4 years) |

| High Price Volatility | -0.7% | National, with regional variations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising anti-sugar health regulations

India's Food Safety and Standards Authority (FSSAI) is reshaping the food and beverage landscape with its stringent sugar content guidelines. Manufacturers must now limit sugar to under 5g per 100g to label their products as "low sugar." This move comes in response to India's pressing diabetes crisis, which affects over 101 million citizens, underscoring the nation's urgent push for sugar reduction. The FSSAI's recent draft on high fat, sugar, salt (HFSS) foods signals a significant shift towards preventive health measures, potentially reshaping age-old sugar consumption habits. Yet, amidst these regulations, there's a silver lining: a surge in demand for specialty sugar grades and natural sweeteners. Responding to this trend, the Council of Scientific and Industrial Research has rolled out low-calorie natural sweeteners, such as Monk fruit. Furthermore, these regulations aren't just influencing domestic markets; they're also bolstering India's export competitiveness, aligning with the global demand for health-compliant products.

High Price Volatility

Industry stakeholders are pushing for proportional adjustments to the Fair and Remunerative Price (FRP) increases, as these have not kept pace with stagnant sugar Minimum Support Prices, leading to financial strain across the value chain. The sector's vulnerability to climatic and biological factors is underscored by regional production variations, such as Uttar Pradesh's 15-25% production decline in 2023-24, attributed to flooding and red rot disease. Despite recommendations from the Commission for Agricultural Costs and Prices, the unimplemented dual pricing policy continues to foster financial instability, hampering long-term planning and investment decisions. Adding to the complexity, the 2024-25 export quota management allocates 1 million tonnes, a significant reduction from historical levels, impacting revenue planning for major producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Crystalline Sugar Dominates the Market

In 2025, crystallized sugar commands a dominant 61.78% share of the market, underscoring its entrenched role in India's food processing sector. This segment's stability is attributed to its wide-ranging applications, from household use to industrial food production, bolstered by established quality standards and cost-effective production methods. Meanwhile, liquid sugar is making waves as the fastest-growing segment, boasting a 5.31% CAGR through 2031. This surge is largely fueled by the pharmaceutical sector's need for sugar solutions that demand precise dissolution and stringent contamination controls.

The pharmaceutical industry's appetite for injectable-grade sugar solutions and niche medical uses is propelling the liquid sugar segment's ascent. Furthermore, food and beverage producers are turning to liquid sugar, valuing its enhanced mixing efficiency and quicker processing times. This is especially true in beverage production, where the speed of dissolution and clarity are paramount. Technological advancements, particularly in storage and transportation, are bolstering the segment's growth. Innovations like temperature-controlled logistics ensure product integrity throughout the supply chain. Additionally, the advent of stored syrup technology is transforming liquid sugar usage, allowing for consistent year-round availability and alleviating seasonal production challenges.

By Category: Organic Segment Gains Premium Positioning

In 2025, conventional sugar commands a dominant 71.55% share of the market, bolstered by established production systems and cost advantages that ensure its accessibility to all consumer segments. This stronghold underscores the sector's emphasis on volume production and the price sensitivity of Indian consumers. This is especially evident in rural markets, where conventional sugar is a staple. The segment reaps the benefits of economies of scale, thanks to large-scale processing facilities and an optimized supply chain network, ensuring consistent availability and competitive pricing.

Organic sugar is emerging as the fastest-growing segment, boasting a projected 5.62% CAGR through 2031. This surge is largely attributed to urban consumers becoming more health-conscious and their readiness to pay a premium for certified organic products. Supporting this growth, the Council of Scientific and Industrial Research is championing natural sweetener alternatives, while the Ministry of Science & Technology underscores the therapeutic benefits of certain natural sugar variants. Regulatory bodies are enforcing organic certification standards, paving the way for quality differentiation and enabling premium positioning strategies. Despite facing hurdles like elevated production costs and a nascent supply chain infrastructure, these challenges are being mitigated, thanks to government support programs and private sector investments in organic farming.

By End-User: Pharmaceutical Applications Emerge as Growth Driver

In 2025, the food and beverage industries command a dominant 60.66% market share, underscoring sugar's pivotal roles in enhancing taste, preserving freshness, and modifying texture across a myriad of products. Driven by India's burgeoning appetite for processed and premium baked goods, the bakery and confectionery subsegment leads in consumption. Meanwhile, the beverage sector witnesses rapid expansion, fueled by the soft drink industry's growth and a rising demand for ready-to-drink products. Urbanization and evolving lifestyle patterns, which increasingly favor convenience foods, bolster steady growth in the dairy and frozen foods segment.

Pharmaceutical applications are the fastest-growing end-user segment, boasting a 5.92% CAGR through 2031. This surge is propelled by India's burgeoning healthcare sector and a rising demand for pharmaceutical-grade sugar, especially in injectable solutions and tablet formulations. The stringent quality standards and specialized processing capabilities required in this segment not only create barriers to entry but also facilitate premium pricing strategies. Meanwhile, retail and foodservice channels enjoy moderate growth, buoyed by the expansion of organized retail and a thriving restaurant industry. Industrial applications, spanning chemical processing to fermentation, ensure a stable demand for specialized sugar grades. Notably, the biofuel/ethanol segment has carved out a significant niche, with government policies championing ethanol blending reshaping demand patterns and complementing traditional sugar applications.

Geography Analysis

In 2025, North India continues to lead with a 38.12% market share, primarily driven by Uttar Pradesh's extensive sugarcane cultivation, which exceeds 177 million tonnes annually. This dominance is supported by a widespread network of cooperative mills in districts such as Kanpur, Prayagraj, Lucknow, and Varanasi. The region benefits from a favorable subtropical climate and a well-developed irrigation system but faces challenges like disease outbreaks in traditional varieties, particularly Co 0238. These issues have caused production fluctuations and early closures of some mills. Demonstrating its commitment to maintaining leadership, the Uttar Pradesh government has allocated INR 1,967 crore for mill capacity expansion. While Bihar and Haryana contribute to the region's production, their outputs remain significantly lower than Uttar Pradesh's. Additionally, sugar mills in the region are increasingly focusing on ethanol production to enhance financial sustainability.

West India is the fastest-growing region, with a projected 6.21% CAGR through 2031. This growth is led by Maharashtra, where technological advancements and operational efficiencies consistently deliver higher recovery rates. The region's competitive edge lies in advanced processing technologies, efficient water management, and strategically located mills that reduce cane transportation costs and improve processing efficiency. Maharashtra's factories are adopting precision agriculture and stored syrup technology, enabling year-round ethanol production and addressing seasonal constraints. Gujarat also contributes to the region's output through targeted cultivation in suitable agro-climatic zones. Proximity to major industrial hubs further strengthens the region's position by providing ready markets for sugar and its by-products. Additionally, mills in the western region are leading the way in adopting zero-emission technologies and sustainable processing practices to comply with environmental regulations.

South India maintains stable production levels, with Karnataka contributing 624.6 lakh tons and Tamil Nadu adding 169.2 lakh tons to the national output in 2022-23. The region benefits from a tropical climate that supports higher per-hectare yields compared to northern regions. Advanced irrigation systems, particularly the widespread use of drip fertigation, enhance water efficiency and improve cane quality. Tamil Nadu achieves the highest productivity levels nationally. Karnataka's sugar mills are expanding capacity, as seen in Davangere Sugar Company's 45 KLPD capacity increase and 15,000-acre cultivation area expansion. Andhra Pradesh also supports regional production through focused development programs. The region's established export infrastructure facilitates access to international markets. East India, while the smallest regional segment, shows growth potential through government initiatives supporting sugar mill development and Assam's pioneering zero-emission processing plant, which sets a new benchmark for sustainability.

Regulatory Landscape

India's cane sugar market operates under food safety standards set by the Food Safety and Standards Authority of India (FSSAI) and supply-and-price oversight led by the Department of Food and Public Distribution (DFPD) under the Essential Commodities Act framework, including cane price administration through the Fair and Remunerative Price (FRP). FSSAI's Food Products Standards and Food Additives Regulations cover multiple sugar types (for example, plantation white sugar, refined sugar, and khandsari) and specify testing methods through its methods manuals, shaping quality compliance for both industrial and retail channels.

In 2026, compliance requirements tighten around digital approvals and trade controls. From June 1, 2026, FSSAI mandated the electronic Product and Claim Approval Application System (ePAAS) for risk assessment and approval of non-specified food ingredients, affecting companies introducing novel ingredients or claim-led formulations adjacent to sugar. On the trade side, India maintained restrictions on sugar exports through September 30, 2026 to manage domestic availability and prices, while import duties have historically been used as a lever to regulate inflows during volatility.

Value Chain Analysis

The value chain starts with sugarcane cultivation concentrated in major producing states such as Uttar Pradesh, Maharashtra, and Karnataka, where cane procurement economics are shaped by FRP (and State Advisory Prices in some states). Cane moves through aggregators and directly to cooperative and private mills, where crushing and recovery feed crystal sugar, liquid sugars, and by-products such as molasses and bagasse, increasingly linked to ethanol, power, and other bio-energy routes. The Sugar (Control) Order 2025 increased the role of digital reporting and compliance across the chain, reinforcing traceability and data availability for policy execution.

Downstream, millers supply wholesalers, institutional buyers, food and beverage processors, and pharmaceutical-grade customers, with logistics and working-capital discipline tied closely to regulated cane prices and periodic interventions on exports and domestic stock management. The ethanol-blending program has made by-product monetization a structural component of mill economics, influencing how much cane is diverted away from sugar and toward ethanol in specific seasons. In May 2026, the export ban through September 30, 2026 shifted the balance toward domestic absorption and by-product channels, raising the importance of integrated milling, distillation, and compliant reporting across sugar, molasses, and ethanol flows.

Competitive Landscape

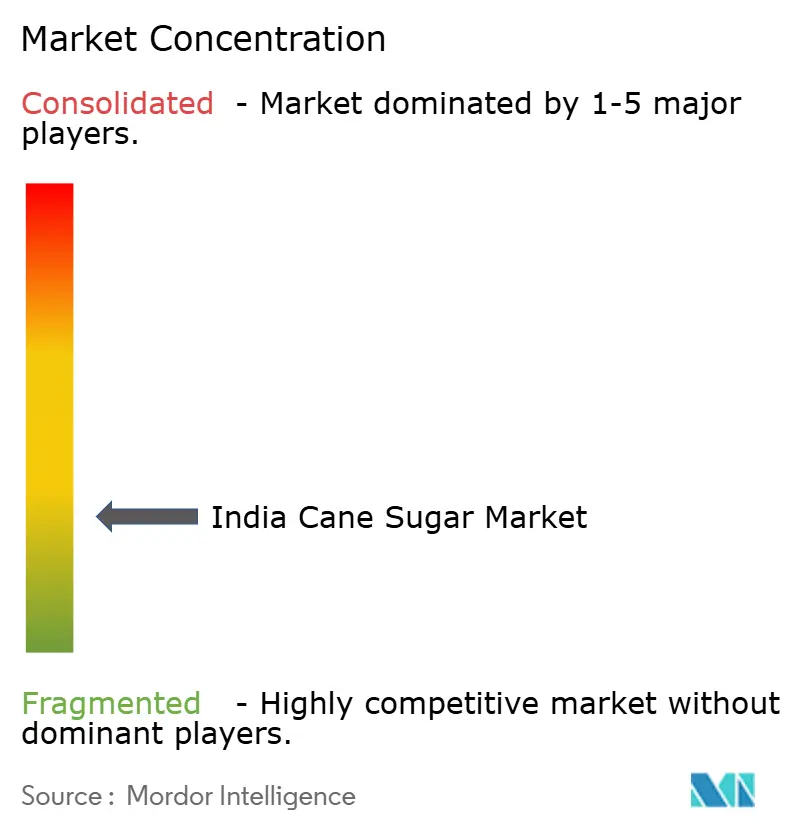

The India Cane Sugar Market has a fragmented competitive landscape, indicating the presence of numerous regional players and cooperative mills that serve diverse market segments across the country. This fragmentation presents opportunities for consolidation and strategic partnerships as mills strive to achieve economies of scale in ethanol production and technological advancements. Major players are adopting diversification strategies beyond traditional sugar production.

For example, Triveni Engineering plans to expand its distillery capacity to 860 KLPD in 2024, while Balrampur Chini Mills is generating additional revenue by optimizing C-heavy molasses pricing. Technology adoption has become a critical competitive advantage, with leading mills utilizing Computer Integrated Manufacturing systems and artificial intelligence applications to enhance operational efficiency and lower production costs, as noted by the Technology Information Forecasting and Assessment Council.

Regulatory compliance under the Sugar (Control) Order 2025 is reshaping the competitive landscape by requiring real-time data sharing and broader coverage of by-products. This creates benefits for technologically advanced mills while posing challenges for smaller operators. Additionally, white-space opportunities exist in specialty sugar segments, pharmaceutical-grade applications, and organic certification. Premium positioning in these areas can help offset commodity pricing pressures and establish sustainable competitive advantages.

India Cane Sugar Industry Leaders

-

DCM Shriram Consolidated Limited

-

Triveni Engineering & Industries Ltd (Ganga Sugar Corporation)

-

Murugappa Group (EID Parry India Limited)

-

Louis Dreyfus Holding B.V.

-

Shree Renuka Sugars Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Specialty and higher-assurance segments create whitespace within the existing market structure, especially where compliance and performance requirements are more stringent. Pharmaceutical-grade and liquid sugar applications benefit from demand for controlled dissolution, contamination control, and consistent specifications, while organic and differentiated grades gain relevance as manufacturers respond to sugar-reduction scrutiny and label-claim thresholds (for example, FSSAI's criteria for low-sugar claims). The mandatory move to ePAAS usage from June 2026 also creates a practical advantage for manufacturers with stronger regulatory and documentation capabilities when developing or scaling non-standard ingredient and claim-led formulations adjacent to sugar usage.

The sector's operating model is being shaped by the scale-up of integrated bio-refinery pathways and technology-driven efficiency programs within mills. National implementation of E20 from April 1, 2026, alongside the industry build-out of ethanol distillation capacity (cited at about 1,990 crore litres as of November 2025 versus demand of about 1,050 crore litres for ESY 2025-26), highlights both the opportunity and constraint: mills can diversify revenue via ethanol and other by-products, while surplus capacity and policy controls on sugar availability (including export restrictions through September 30, 2026) sharpen the need for cost reduction, recovery optimization, and disciplined allocation between sugar and ethanol. The draft Sugarcane (Control) Order 2026 consultation, including proposals such as increasing the minimum distance between mills to 25 km, also indicates that future capacity additions face a more formalized approval environment, which raises the value of modernization and debottlenecking within existing assets.

Recent Industry Developments

- May 2026: The Government of India implemented a ban on exports of raw, white, and refined sugar through September 30, 2026 to stabilize domestic availability and prices. The move tightened the domestic supply-demand focus for mills and increased the importance of alternative realizations from ethanol and other by-products when export channels are constrained.

- March 2025: DCM Shriram commissioned a 12 TPD compressed biogas (CBG) plant at its Ajbapur unit. The commissioning strengthened downstream by-product monetization from sugar operations and reinforced the broader industry shift toward integrated bio-energy platforms within existing mill complexes.

- November 2024: DCM Shriram commissioned a 2,100 TCD sugar capacity expansion at its Loni unit. The added crushing capability supported higher throughput potential and positioned the site to improve operational leverage across sugar and associated by-product streams.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the value of cane sugar sold in India that is produced from sugarcane processing and used across household and industrial consumption, including crystallized sugar and liquid syrup forms.

Scope exclusions: It excludes sugar made from non-cane feedstocks and it does not count non-sugarcane sweeteners.

Segmentation Overview

-

By Form

- Crystallized Sugar

- Liquid Sugar

-

By Category

- Conventional

- Organic

-

By End-User

-

Food & Beverage Industries

- Bakery and Confectionery

- Beverages

- Dairy and Frozen Foods

- Others

- Pharmaceuticals

- Retail

- Foodservice Channels

- Industrial

- Biofuel / Ethanol

-

Food & Beverage Industries

-

By State

- North India

- South India

- West India

- East India

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the model and to lock the most repeatable supply and demand signals for India. We relied on public datasets and official publications such as Indian government agriculture statistics, trade and customs releases, central bank and macro series for inflation and currency, food and standards notifications, and select peer reviewed articles on sugar recovery and cane yields.

To translate those signals into market value, we also reviewed company annual reports, investor decks, mill and association updates, and reputed press coverage for season drivers such as monsoon impact and policy changes around cane pricing and ethanol diversion. In addition, paid subscriptions for company financials, patent lookups, and shipment level import and export checks were used to cross-verify select assumptions where public series were not granular enough. This list is indicative only, and we also reviewed other sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews focused on validating how much cane sugar is actually available for food and industrial use after diversion, and how pricing moves through the season. We spoke with stakeholders across the value chain, including mill side functions, traders, bulk buyers, and downstream users, and then ran follow up calls when there were large gaps between desk indicators and on the ground reality.

Coverage was kept balanced across India so that regional production swings, procurement patterns, and channel differences could be reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 15% | |

| Mid tier: 59% | Functional/Unit leaders: 39% | |

| Smaller Players: 16% | Managers: 46% |

Market-Sizing & Forecasting

Sizing was built using a top-down model where India sugarcane and sugar production signals are reconstructed into a cane sugar availability pool, then converted into value using seasonally adjusted pricing. To keep totals realistic, we corroborated the output with selective bottom-up checks, such as sampled mill realizations, trader channel pricing, and a light roll up of reported revenues for a subset of visible suppliers.

Key inputs used (illustrative) included sugarcane crushing volumes, sugar recovery rates, government cane price and levy style policy shifts, ethanol diversion intensity, monthly wholesale price trends, and import or export movements. Where any bottom-up view had gaps, the missing portion was bridged using state level production shares and normalized realization bands, and then adjusted only after it matched the broader supply and price story.

Forecasts were produced using scenario analysis supported by short-cycle time series smoothing for prices, since policy and weather can move the market quickly. Assumptions on yields, diversion, and pricing were stress tested with expert feedback before finalizing the forward path.

Data Validation & Update Cycle

Validation was done by triangulating value outputs against independent signals, such as production volumes, stock movement patterns, and price direction across the season, and then checking that implied consumption did not break known festival or industrial demand periods. When outliers appeared, the driver was isolated first, and then the relevant assumption was revisited. If needed, we re-contacted respondents to confirm the change.

Before sign-off, the model goes through multiple analyst reviews so arithmetic, units, and conversions are consistent across regions and end uses. The report is refreshed annually, and interim updates are made when material events occur, such as major policy changes, sharp export controls, or abnormal monsoon outcomes. Right before delivery, a fresh check is run so clients receive the latest updated view.

Mordor Intelligence's India Cane Sugar Market Size Compared Against Other Published Estimates

It is common to see different market numbers for India cane sugar because the term can be interpreted in more than one way, and because some publishers lean more on price led assumptions while others lean more on production led assumptions. Differences also show up when studies use different years, different currency timing, or different treatments of diversion into ethanol.

Production and stock signals, along with wholesale price seasonality checks, are what keep Mordor Intelligence's estimate tied to the cane sugar availability and realization that the industry can actually sell in India. The main gap drivers in other figures usually come from narrower product coverage (for example, only refined white sugar), mixing in non-cane sweeteners, or applying a single average price across the year without correcting for policy events and seasonal spikes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 55.40 B (2025) | |

| Industry Portal A | USD 2.22 B (2024) | This number is scoped to refined cane sugar only and is presented as a smaller packaged and specialty product revenue pool, which leaves out a large share of bulk crystal sugar volumes and several downstream use cases. |

| Government Brief B | USD 34.00 B (2024) | This figure is commonly derived by converting production tonnage into value using a simplified price assumption and it often reflects raw value production logic, which can miss channel level realization differences and season specific pricing movements. |

Taken together, the spread is mainly explained by what is counted as cane sugar, whether the estimate is built from production tonnage or from value realization, and how the year and currency timing are handled. By keeping scope rules explicit and by grounding pricing and availability in repeatable signals, the model stays transparent and easy to reproduce for decision making.

Key Questions Answered in the Report

What is the current value and projected growth rate of the India cane sugar market through 2031?

It is valued at USD 57.62 billion in 2026 and is forecast to reach USD 70.13 billion by 2031, registering a 4.01% CAGR.

Which product form is expanding the quickest across Indian sugar applications?

Liquid sugar is the fastest-growing form, advancing at a 5.31% CAGR thanks to demand from beverages and pharmaceutical-grade solutions.

What health regulations are reshaping product formulation in the sweetener space?

FSSAI rules cap “low-sugar” claims at under 5 g per 100 g, driving reformulation toward reduced-sugar, organic, and natural-sweetener options.

Which Indian region shows the highest growth potential for cane-sugar production?

West India, led by technologically advanced mills in Maharashtra, is projected to grow at a 6.21% CAGR through 2031.

Page last updated on: