Industrial Sugar Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

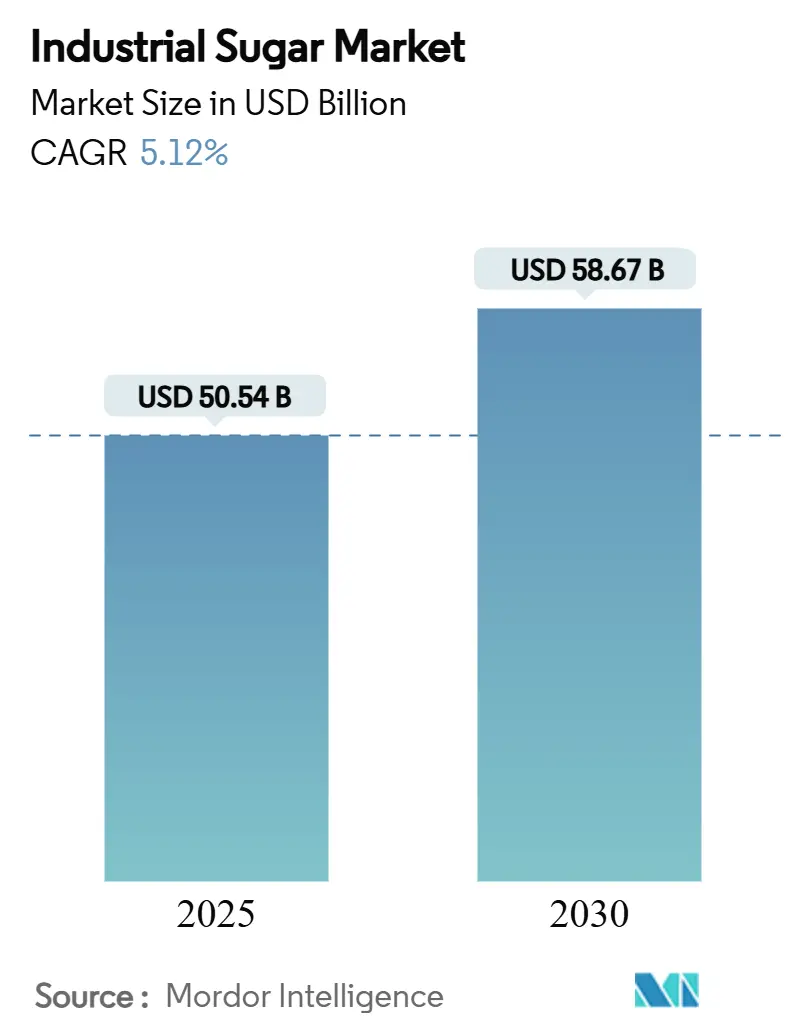

| Market Size (2025) | USD 50.54 Billion |

| Market Size (2030) | USD 58.67 Billion |

| Growth Rate (2025 - 2030) | 5.12% CAGR |

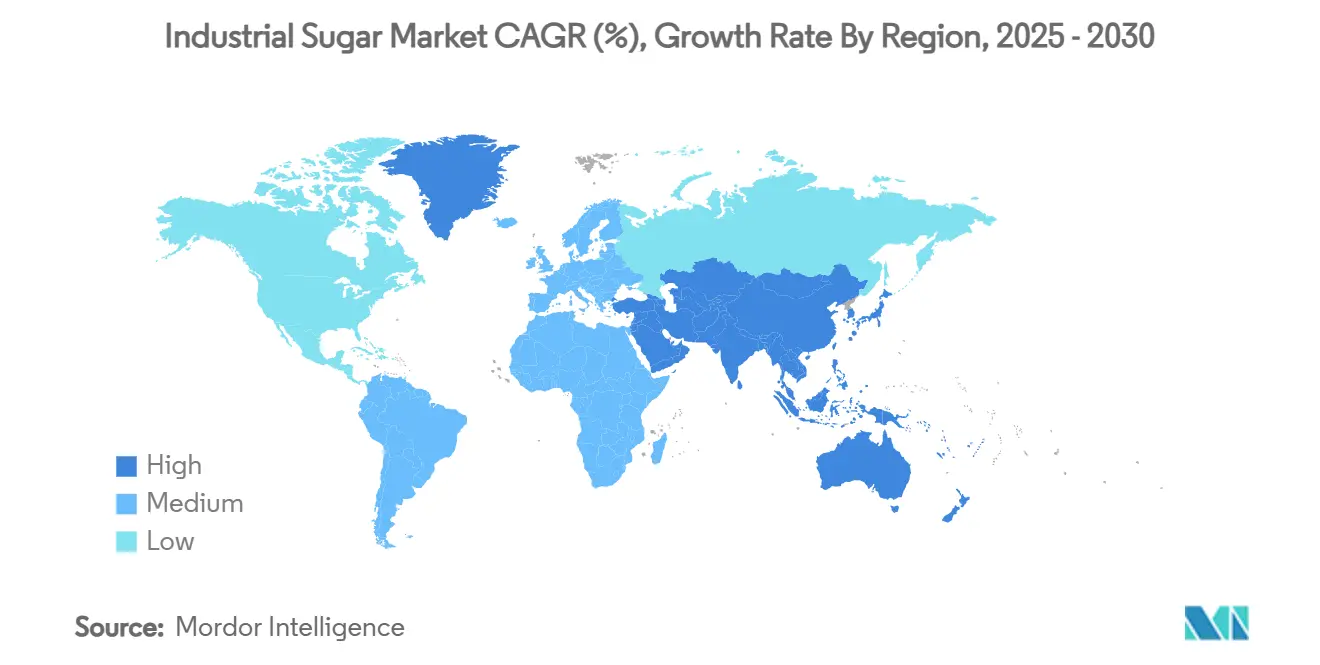

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

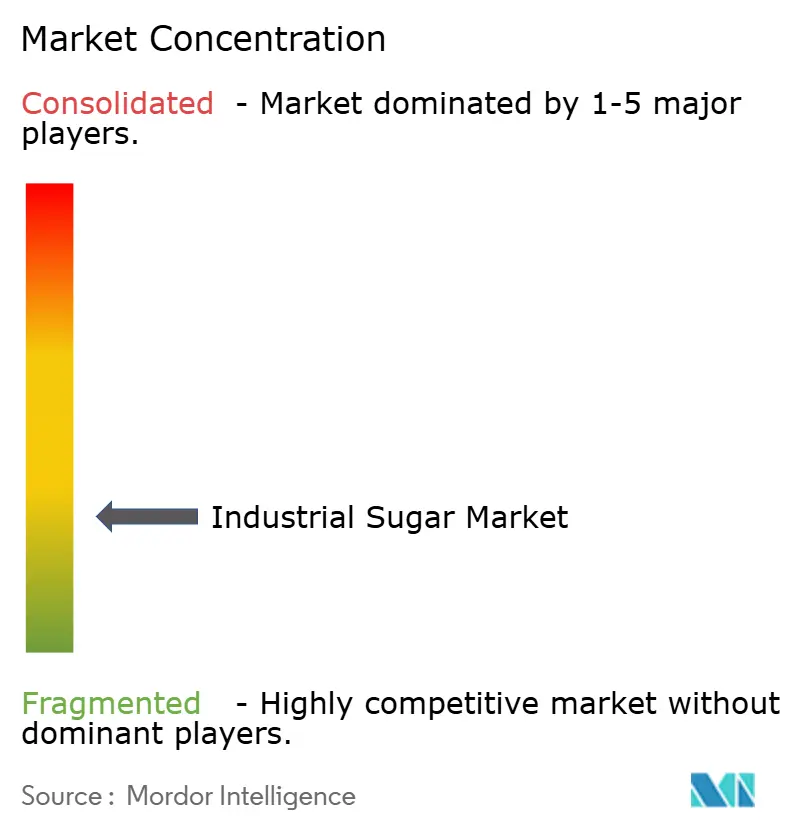

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Industrial Sugar Market Analysis by Mordor Intelligence

The global industrial sugar market size stands at USD 50.54 billion in 2025 and is forecast to reach USD 58.67 billion by 2030, advancing at a 5.12% CAGR. Sustained demand from processed-food manufacturers, strategic capacity shifts between sugar and ethanol in Brazil, and steady consumption in beverages underpin this expansion. Asia-Pacific’s leadership rests on robust household demand and large-scale refining capacity, while South America’s cost-competitive cane sector is accelerating exports. Technological upgrades from higher-yield cane varieties to automated extraction lines are improving margins and mitigating tightening environmental rules. Despite the rise of alternative sweeteners, the sugar market continues to benefit from sugar’s multifunctional role in texture, preservation, and fermentation, especially in baked goods and beverages.

Key Report Takeaways

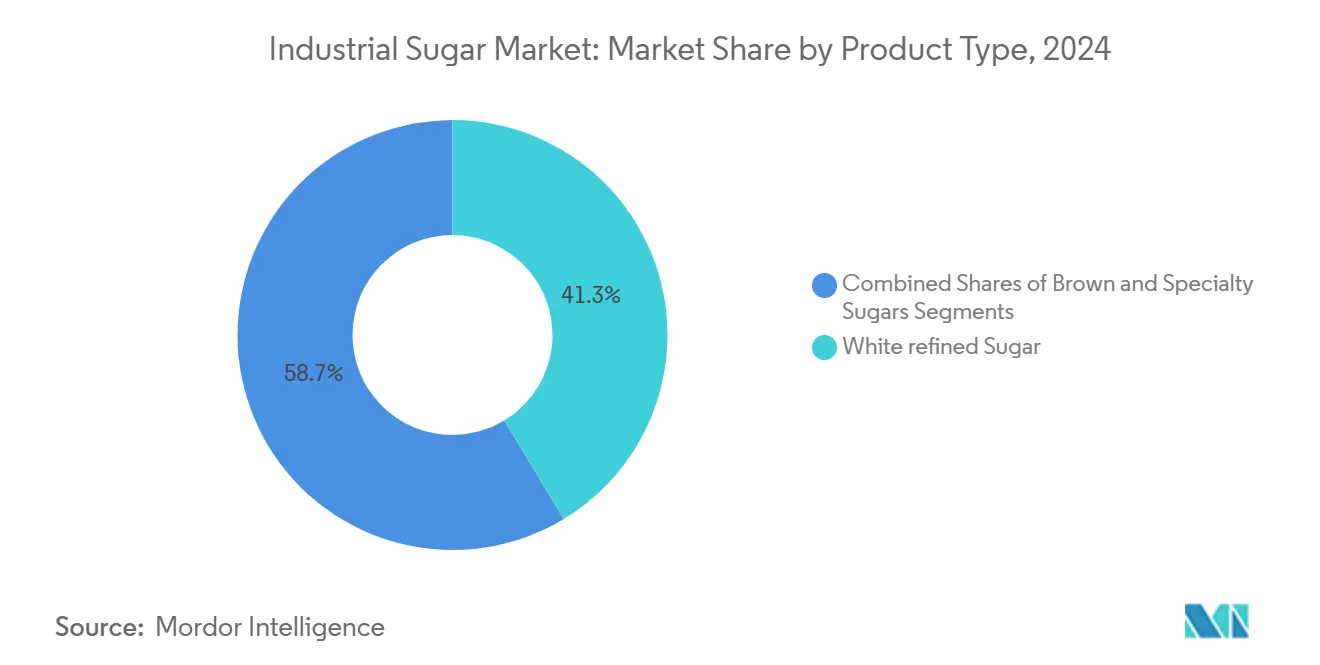

- By product type, white refined sugar led with 41.34% of the industrial sugar market share in 2024, whereas specialty sugars are projected to register a 6.12% CAGR between 2025-2030.

- By form, granulated sugar dominated with a 51.15% share in 2024; powdered sugar is expected to grow fastest at 5.79% CAGR through 2030.

- By source, cane sugar accounted for 65.78% of the 2024 share, while beet sugar is forecast to post a 6.11% CAGR to 2030.

- By application, beverages represented 37.67% of the 2024 share, yet bakery and confectionery products are poised to expand at a 6.78% CAGR.

- By geography, Asia-Pacific controlled 35.56% of the shares in 2024; South America is set to be the fastest-rising region with a 5.98% CAGR through 2030.

Global Industrial Sugar Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for processed foods and beverages | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Technological advancements in sugar processing | +0.8% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Expansion of cane-based ethanol programs redirecting capacity to sugar | +0.6% | South America, particularly Brazil | Short term (≤ 2 years) |

| Growth in International Trade | +0.4% | Global, with focus on Asia-Pacific imports | Medium term (2-4 years) |

| Government Incentives and Subsidies | +0.3% | North America, South America, and select Asian markets | Long term (≥ 4 years) |

| Supply Chain Resilience Investments | +0.2% | Global, with emphasis on major producing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Processed Foods and Beverages

As processed food consumption surges, it's reshaping sugar demand patterns. Industrial users are now prioritizing a consistent supply of sugar over price optimization. This shift underscores the food industry's heightened focus on supply security in the wake of the pandemic, alongside the increasingly intricate formulation needs spanning various product categories. With a commanding 37.67% market share, the beverage sector underscores sugar's pivotal role in crafting taste profiles. This is especially evident as manufacturers grapple with sugar reduction mandates while striving to keep consumers satisfied. Data from the U.S. Department of Agriculture reveals that, despite a trend towards health consciousness, industrial sugar consumption is on the rise, driven by population growth and urbanization in emerging markets. Beyond its sweetening capabilities, sugar offers functional benefits like preservation, texture modification, and fermentation support. These attributes, not fully replicated by alternative sweeteners, highlight the processed food segment's resilience.

Technological Advancements in Sugar Processing

Innovations in processing technology are not only boosting extraction efficiency but also minimizing environmental impacts. Automation systems now facilitate round-the-clock operations, ensuring optimal asset utilization. A prime example of this trend is Michigan Sugar Company's new facility, which, at a cost of USD 109 million, is dedicated to molasses desugarization. This facility not only extracts an additional 80 million pounds of sugar annually from byproducts but has also ramped up its processing capacity to an impressive 650 tons per day. Meanwhile, in China, the LC05-136 sugarcane variety, a product of breeding innovations, is being cultivated across more than 1.67 million hectares. Developed by the Chinese Academy of Sciences, this variety not only boosts yield and processing efficiency but also emphasizes climate resilience. Such technological strides are becoming increasingly vital as producers grapple with rising labor costs and stringent environmental regulations, pushing them to maximize output from every input. Furthermore, the adoption of digital monitoring systems and predictive maintenance is not only curtailing downtime but also fine-tuning energy consumption, bestowing sustainable competitive edges to those who embrace these changes early on.

Expansion of Cane-Based Ethanol Programs Redirecting Capacity to Sugar

Brazilian sugar mills are shifting their focus from ethanol to sugar production, responding to the rising economic viability of corn-based ethanol. This pivot underscores significant changes in Brazil's energy policy and agricultural economics. While corn processors are now taking on the mantle of ethanol production, sugar mills are honing in on their primary expertise, as reported by Reuters. This transition is especially noteworthy as Brazil stands as the world's leading sugar exporter. Projections indicate a record sugar production of 45.9 million tons in the 2025/26 cycle, even with a dip in sugarcane harvests, according to the National Supply Company. Such a reallocation not only stabilizes the global sugar market but also enables Brazilian producers to better align their asset utilization with fluctuating commodity prices. This trend hints at a fundamental transformation in the operations of integrated sugar-ethanol complexes, moving from a flexible production model to one of specialization.

Growth in International Trade

As regional production imbalances emerge, Asian importers are diversifying their supply sources to mitigate dependency risks, highlighting the intensifying dynamics of international trade. Demonstrating the reshaping of global flow patterns, the U.S. has enacted special agricultural safeguard measures on products with over 65% sugar content, a move set to last until September 2025, as reported by U.S. Customs and Border Protection[1]Source: U.S Customs and Border Protection, "QB 25-330 2025 Special Agricultural Safeguard Measures for Sugar-Containing Products", cbp.gov. Meanwhile, Canada's decision, as noted by the UK Government, to review its autonomous tariff quota for raw cane sugar — permitting 260,000 tonnes at a 0% duty — underscores the delicate balance between domestic protectionism and consumer pricing. Such policy shifts are not only crafting new trade corridors but also compelling exporters to refine their market entry strategies. Furthermore, the burgeoning trade in specialty sugars, managed through various quota tranches, signals a trend of heightened product differentiation in global markets.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Volatility of Raw Materials | -0.7% | Global, with particular impact on import-dependent regions | Short term (≤ 2 years) |

| Environmental and Sustainability Concerns | -0.5% | Global, with stricter enforcement in developed markets | Medium term (2-4 years) |

| Fermentation-based sweeteners eroding industrial volume | -0.4% | North America and Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Changing Consumer Preferences | -0.3% | Developed markets, with gradual adoption in emerging economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Raw Materials

Commodity price fluctuations are posing significant challenges for sugar processors, as raw material costs account for 60-70% of their total production expenses and have become increasingly linked to energy and transportation markets. The Egyptian sugar industry serves as a prime example of this vulnerability. Here, multiple devaluations of the Egyptian pound have not only hampered imports but also compelled local producers to shift crops towards molasses production. This shift has, in turn, diminished the feedstock availability for state-owned mills. Such volatility poses a particular challenge for smaller processors, who often lack the means for hedging and the security of long-term supply contracts. As a result, there's mounting pressure for consolidation within the industry. Furthermore, the tight interconnection between sugar prices and the broader agricultural commodity markets means that external factors—be it weather events, energy costs, or currency fluctuations—can swiftly disrupt profit margins throughout the entire value chain.

Environmental and Sustainability Concerns

As the U.S. Environmental Protection Agency tightens its grip on sugar processing, setting stringent limits on BOD5, TSS, and pH levels, companies are feeling the pinch. Suntory Holdings, in partnership with KTIS, is spearheading a pioneering low-carbon sugarcane farming initiative in Thailand, underscoring the shift of sustainability from a mere choice to a competitive edge[2]Source: U.S. Environmental Protection Agency, “Effluent Guidelines for Sugar Processing,” epa.gov. Yet, the hurdles aren't just about meeting regulations; they encompass shifting consumer perceptions and corporate policies that increasingly prioritize sustainably sourced ingredients. With crystalline cane sugar refineries now facing a stringent daily BOD5 cap of 2.38 pounds per ton of melt, the push for water usage optimization is paramount. This demand necessitates advanced treatment systems and process tweaks, as highlighted by the U.S. Government. Such stringent environmental mandates not only pose challenges for new entrants but also bolster the position of established players equipped with the necessary compliance infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialty Sugars Drive Premium Growth

In 2024, white refined sugar holds a 41.34% market share, underscoring its pivotal role in industrial applications. Meanwhile, specialty sugars, driven by health-conscious consumers and artisanal food production, are witnessing a robust 6.12% CAGR growth through 2030, commanding premium pricing. Notably, the coconut sugar segment is expanding, with the Philippines enhancing its global competitiveness through advanced sap collection techniques and hybrid coconut varieties for better yield efficiency, as reported by the Philippine News Agency. Brown sugar, enjoying steady demand in baking, is benefiting from clean-label trends and a natural product image. However, its production economics are closely linked to refining capacity utilization rates.

Product segmentation highlights varied supply chain dynamics. Specialty sugars, demanding advanced processing and stringent quality control, pose entry barriers for smaller producers. White refined sugar's widespread use in food and beverages cements its dominance, yet producers face margin pressures from commodity pricing, pushing them to enhance extraction efficiency and reduce processing losses. The rise of organic and fair-trade certifications in the specialty segment offers new revenue avenues for producers investing in certification and traceability, though these financial benefits are predominantly seen in developed markets.

By Form: Granulated Dominance Amid Powdered Growth

In 2024, granulated sugar commands a dominant 51.15% share of the market, underscoring its widespread use in both consumer and industrial applications. Meanwhile, powdered sugar, with a growth rate of 5.79%, is witnessing heightened demand, particularly in bakeries and confectioneries that prioritize specific particle size distributions. This differentiation in sugar forms not only carves out unique value propositions but also highlights their tailored applications: granulated sugar excels in dissolution, while powdered sugar is preferred for texture enhancement and decorative uses. Additionally, syrup forms cater to niche industrial needs, especially in beverage production, where their liquid nature streamlines operations, cutting down processing steps and ensuring consistency.

Producing various sugar forms necessitates specialized equipment and stringent quality controls, leading to a natural segmentation in production facilities. The rising demand for powdered sugar mirrors the bakery industry's shift towards premiumization, emphasizing the growing importance of texture and appearance in consumer choices. American Sugar Refining's strategic move to shutter its Yonkers facility, while simultaneously modernizing its Baltimore and Chalmette operations for continuous production, underscores the industry's focus on form-specific efficiency. Furthermore, syrup production's need for specialized storage and transport infrastructure creates significant competitive advantages for established producers with robust logistics networks.

By Source: Cane Leadership Faces Beet Acceleration

In 2024, cane sugar commands a dominant 65.78% share of the market, underscoring its production edge in tropical and subtropical locales. Meanwhile, the growth rate of beet sugar at 6.11% highlights the robustness of temperate climate production systems, bolstered by government backing and technological advancements. Beyond geographic distinctions, the differentiation in sources also hinges on processing economics. Cane sugar enjoys the advantage of a higher sucrose content, whereas beet sugar boasts more consistent yields and quicker production cycles. China's initiative to cultivate mechanized sugarcane varieties for mass production underscores the potential of source-specific innovations to redefine regional competitiveness.

Beet sugar's growth trajectory is driven by targeted investments in processing efficiencies and crop breeding, which enhance sugar content and disease resistance. This is especially evident in European and North American markets, where the climate is conducive to beet cultivation. Highlighting the influence of policy frameworks on source economics, the United States Department of Agriculture set fiscal year 2025 sugar loan rates at 19.75 cents per pound for raw cane sugar and 25.38 cents per pound for refined beet sugar[3]Source: United States Department of Agriculture, "USDA Announces Fiscal Year 2025 Sugar Loan Rates", fas.usda.gov. In response to mounting competition, cane sugar producers are adopting vertical integration strategies and diversifying revenue streams through flexible ethanol production. This segmentation of sources increasingly mirrors wider agricultural policy goals, emphasizing food security, rural development, and environmental sustainability.

By Application: Beverages Lead While Bakery Accelerates

In 2024, beverages hold a commanding 37.67% market share, underscoring sugar's pivotal role in shaping taste profiles and securing consumer approval. Meanwhile, the bakery and confectionery sectors witness a 6.78% growth, fueled by premiumization trends and a burgeoning food service industry. The beverage segment thrives not just on sugar's sweetness, but also on its unique properties, such as enhancing mouthfeel and preservation qualities that alternative sweeteners struggle to match. In pharmaceuticals, sugar plays a dual role as both an excipient and a coating agent. This specialized segment adheres to stringent quality and regulatory standards, creating formidable barriers for new entrants.

The bakery sector's growth isn't just about volume; it's also about value. Artisanal and premium products not only use more sugar but also opt for specialized types that enhance texture and appearance. In personal care and cosmetics, sugar, though used in smaller volumes, shines as a natural exfoliant and humectant, carving out niche markets for specialty producers. A case in point: the United Kingdom's sugar tax, which successfully halved the sugar intake from soft drinks for children, highlights how regulations can shift demand patterns. This shift, however, opens doors for reformulation and innovative product development, as noted by The Guardian. In dairy and frozen desserts, sugar's ability to modify texture and depress freezing points creates challenges for substitutes, ensuring a steady demand.

Geography Analysis

In 2024, Asia-Pacific commands a dominant 35.56% share of the market, underscoring the region's vast population and a burgeoning middle class. Meanwhile, South America, with a 5.98% growth rate, showcases the benefits of its integrated production systems and favorable agricultural conditions. China's sugar production is set to hit 10.4 million metric tons for the 2024/25 period, buoyed by expanded planting areas for both cane and beet, highlighting the region's robust demand and production capacity, as noted by the U.S. Department of Agriculture.

In India, a projected sugar output bounce-back to 35 million tons in the 2025-26 cycle, spurred by beneficial monsoon rains and an enlarged cane area, underscores the interplay of weather and government policies on regional supply dynamics, as reported by The Hindu Business Line. Brazil's strategic shifts in capacity and infrastructure investments are driving South America's growth, bolstering its export competitiveness. Concurrently, Argentina and Colombia are reaping benefits from regional trade agreements and favorable currency conditions.

After a 20% dip, Thailand's sugar production is on the mend for 2024/25, with export volumes climbing, showcasing how seasoned producers navigate market fluctuations, as highlighted by the U.S. Department of Agriculture. In North America and Europe, mature markets grapple with health-conscious consumption and regulatory hurdles, limiting growth. Yet, these regions retain significance through high-value specialty applications and cutting-edge processing. The Middle East and Africa are ripe with potential. However, Egypt grapples with production hurdles, stemming from currency devaluation and energy costs, leading to an import reliance that bolsters global trade dynamics.

Competitive Landscape

The sugar industry showcases fragmented competition, presenting substantial consolidation prospects for firms that can leverage operational scale and supply chain integration. This fragmentation is a result of the industry's geographic spread, regulatory hurdles to cross-border mergers, and the capital-heavy nature of processing, which curtails swift market share expansion. Major players, such as Südzucker AG and Tereos SCA, are increasingly focusing on vertical integration, overseeing the cultivation, processing, and distribution of their products. This strategy not only offers them cost benefits but also ensures supply security. Moreover, technology adoption is emerging as a pivotal differentiator, with firms channeling investments into automation, predictive maintenance, and digital monitoring, all aimed at curbing operational costs and enhancing quality consistency.

There are untapped opportunities in specialty sugar segments, refining supply chains, and adopting sustainable production methods that align with environmental standards and consumer demands. Precision fermentation firms are gaining attention with innovations like the protein-based sweetener brazzein. Brazzein, which has Food and Drug Administration Generally Recognized as Safe status, is reported to be 10,000 times sweeter than table sugar and contains zero calories.

The competitive arena is increasingly shaped by regulatory mandates, such as the EPA's effluent guidelines for sugar processing. These regulations not only pose entry challenges but also advantage established players with pre-existing environmental setups, as noted by the U.S. Environmental Protection Agency. In terms of market maneuvers, Beta San Miguel's strategic 15.93% stake acquisition in Sucro Limited stands out, bolstering its foothold in the North American market and enhancing its supply chain integration.

Industrial Sugar Industry Leaders

-

Südzucker AG

-

Tereos SCA

-

Associated British Foods plc (ABF Sugar)

-

Florida Crystals Corporation (ASR Group)

-

Wilmar International Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The Indian Government announced the permission to export 25,000 metric tons of high-quality pharma-grade sugar. The sugar is made from high-quality standards. It is used for various pharmaceutical applications.

- June 2025: Mysore Sugar Company in India, also known as Mysugar aimed to crush 4.5 lakh metric tonnes during the year 2025-26. The company invested USD 5.8 million on this expansion.

- March 2025: Saraswati Sugar Mills (SSM) commenced the production of invert liquid sugar. The new plant for invert liquid sugar was established by the Indian Sugar and General Engineering Corporation (ISGEC). The liquid sugar production meets national food safety regulations.

- February 2024: Sucro Ltd. announced plans to construct a cane sugar refinery in the greater Chicago area. The facility matches the scale of the Lackawanna plant and includes specialty sugar production capabilities. These capabilities encompass large grain crystals for specialty foods and confectionery, an integrated brown sugar line, specialty liquid sugar production, and organic sugar refining.

Global Industrial Sugar Market Report Scope

| White Refined Sugar |

| Brown Sugar |

| Specialty Sugars |

| Granulated |

| Powdered/Icing |

| Syrup |

| Cane Sugar |

| Beet Sugar |

| Bakery and Confectionery |

| Dairy and Frozen Desserts |

| Beverages |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Others (Chemicals, Textiles) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | White Refined Sugar | |

| Brown Sugar | ||

| Specialty Sugars | ||

| Form | Granulated | |

| Powdered/Icing | ||

| Syrup | ||

| Source | Cane Sugar | |

| Beet Sugar | ||

| Application | Bakery and Confectionery | |

| Dairy and Frozen Desserts | ||

| Beverages | ||

| Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Others (Chemicals, Textiles) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the global sugar market?

The sugar market size is USD 50.54 billion in 2025, and it is projected to reach USD 58.67 billion by 2030.

Which region holds the largest share of sugar demand?

Asia Pacific leads with 35.56% of global revenue in 2024 due to its vast consumer base and refining capacity.

What segment of the sugar market is growing fastest?

Specialty sugars are forecast to grow at a 6.12% CAGR between 2025-2030, driven by clean-label and premium bakery demand.

How are environmental regulations affecting sugar producers?

Stricter wastewater and carbon rules are increasing capital requirements, favoring companies with advanced treatment systems and sustainable farming programs.

Page last updated on: