Stevia Sugar Blends Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

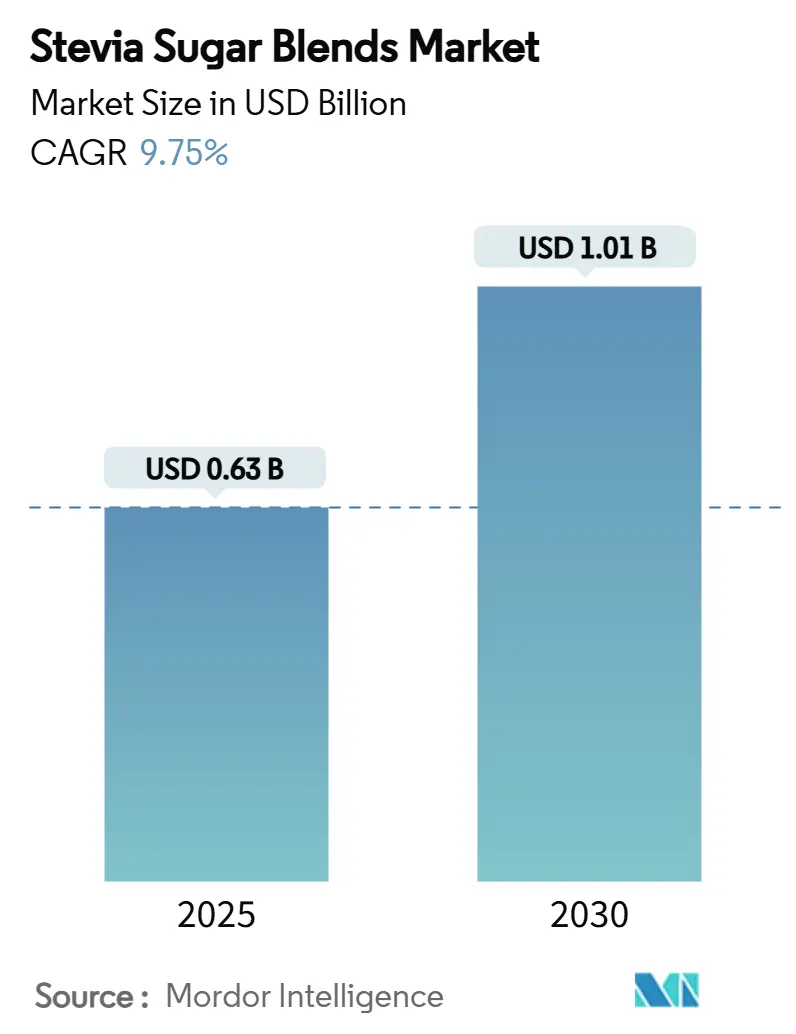

| Market Size (2025) | USD 0.63 Billion |

| Market Size (2030) | USD 1.01 Billion |

| Growth Rate (2025 - 2030) | 9.75% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stevia Sugar Blends Market Analysis by Mordor Intelligence

The stevia sugar blends market size is anticipated to be valued at USD 0.63 billion in 2025 and is forecast to climb to USD 1.01 billion by 2030, progressing at a 9.75% CAGR. Global pressures to reduce added sugars, the FDA's updated definition of "healthy" excluding stevia, and the swift commercial uptake of cost-effective bioconversion for premium rebaudioside M drive this expansion. Thanks to China's new GB 2760-2024 food additive standard and an expanding domestic leaf cultivation ensuring raw material availability, the Asia-Pacific region boasts a dominant 39.34% market share. Meanwhile, the Middle East and Africa, spurred by the UAE's growing GDP and a USDA-backed policy push for healthier imports, chart the swiftest growth at a 12.56% CAGR. While conventional blends lead in sales, certified organic products, like those from Pyure, capitalizing on USDA organic seals, are outpacing the overall growth, securing premium shelf space.

Key Report Takeaways

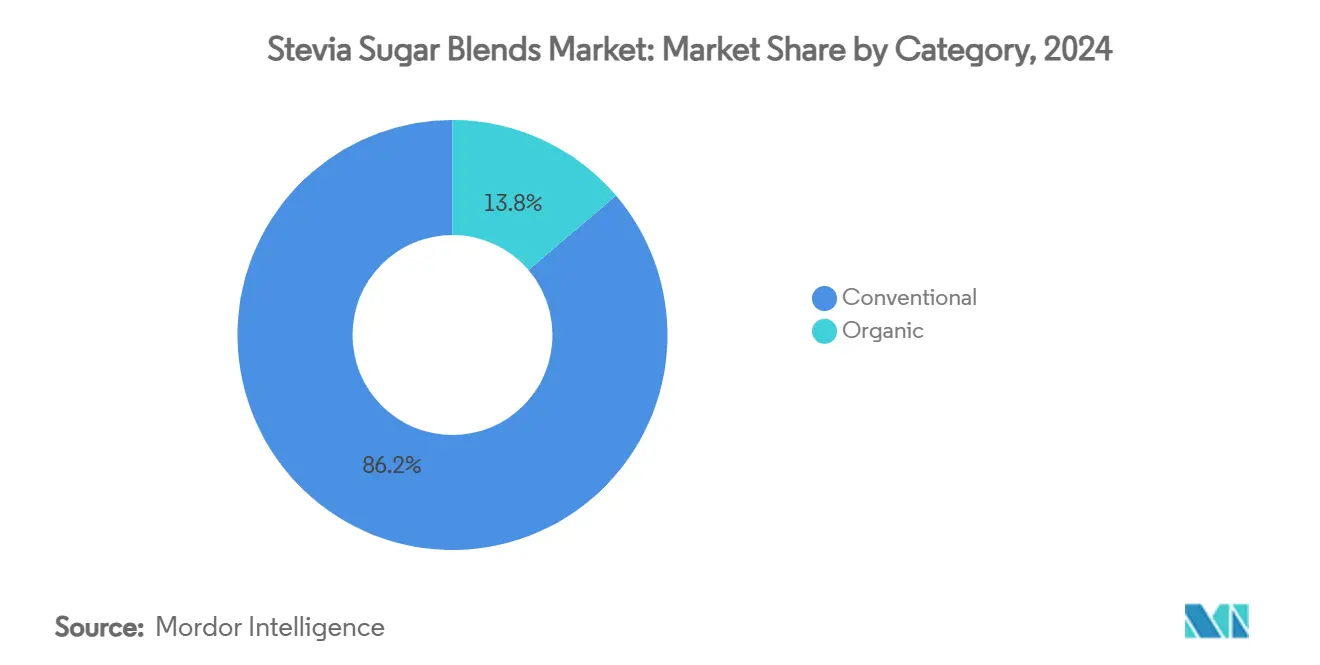

- By category, conventional products captured 86.24% revenue share in 2024 while organic blends are advancing at a 12.44% CAGR through 2030.

- By product form, powder blends accounted for 54.65% of the stevia sugar blends market share in 2024, whereas liquid formats are projected to post a 13.76% CAGR to 2030.

- By sweetener combination, stevia-plus-sugar dominated with 38.27% of the stevia sugar blends market size in 2024; stevia-plus-monk-fruit is forecast to grow at 11.53% CAGR to 2030.

- By application, beverages led with 42.86% share in 2024, and the nutraceuticals and pharmaceuticals segment is expanding at an 11.82% CAGR through 2030.

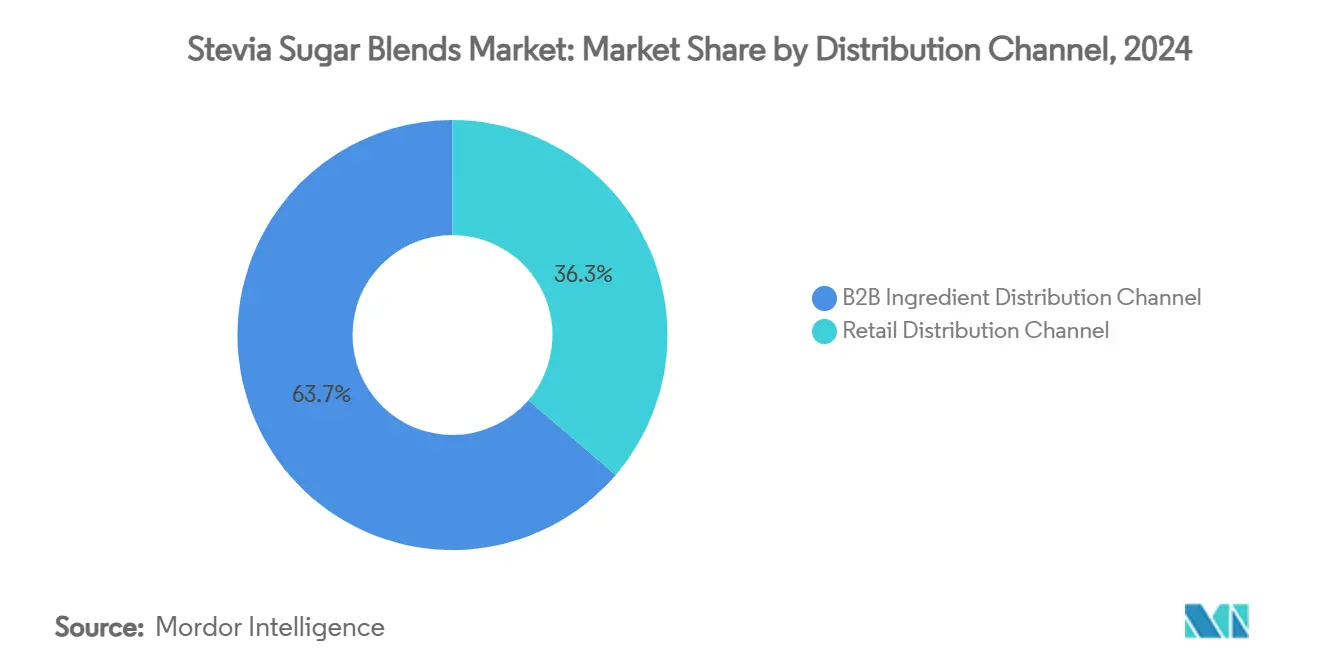

- By distribution channel, the B2B ingredient distribution channel held 63.71% of the stevia sugar blends market size in 2024, while the retail distribution channel is projected to grow 10.38% annually to 2030.

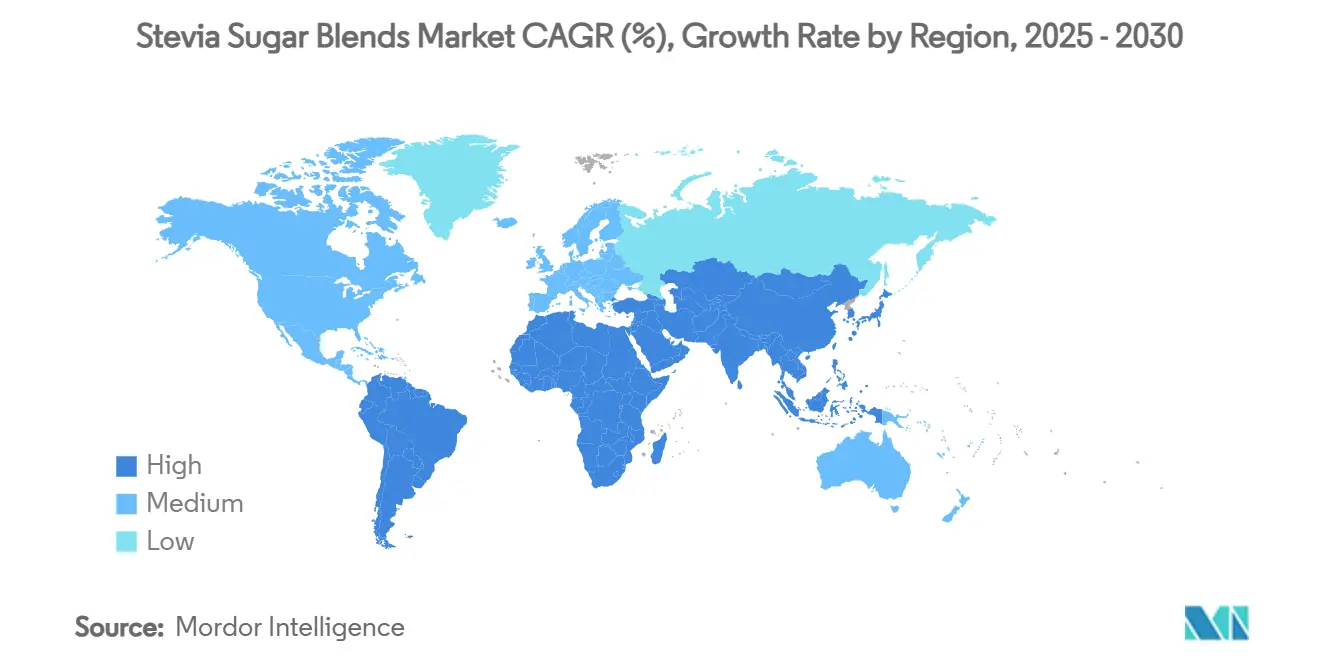

- By geography, Asia-Pacific accounted for 39.34% of the stevia sugar blends market share in 2024. The Middle East and Africa is forecast to register the quickest expansion with a 12.56% CAGR through 2030.

Global Stevia Sugar Blends Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sugar-reduction policies and soda-tax expansion | +1.8% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Product reformulations by global beverage majors | +1.5% | Global, concentrated in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Cost-efficient bioconversion of Rebaudioside M | +1.2% | North America and Asia-Pacific production hubs | Medium term (2-4 years) |

| Product personalization and functional food trends | +0.9% | North America and Europe premium segments | Long term (≥ 4 years) |

| Patented micro-encapsulation improving mouthfeel | +0.7% | Global, with R and D centers in North America and Europe | Medium term (2-4 years) |

| Emergence of organic and Non-GMO stevia blends | +0.6% | North America and Europe organic markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sugar-reduction policies and soda-tax expansion

Government mandates aimed at reducing sugar consumption are significantly altering the food industry's dynamics. Highlighted by DLA Piper, the FDA's 2025-2030 Dietary Guidelines advocate for a complete halt on added sugars. Concurrently, the USDA is imposing stricter limits on added sugars in school meals, leading to a surge in demand for stevia blends in educational institutions. The FDA is also intensifying its efforts, pushing for front-of-package nutrition labels that classify added sugars as "Low," "Med," or "High," underscoring the urgency for food reformulation[1]Source: United States Food and Drug Administration, “Front-of-Package Nutrition Labeling Proposed Rule,” regulations.gov. This synchronized regulatory approach favors stevia blends, which, thanks to the FDA's updated definitions, can proudly flaunt "healthy" claims— a privilege denied to traditional added sugars. The Institute of Food Technologists highlights the growing influence of GLP-1 medication users in the sugar reduction initiative, projecting this group's expansion at a robust 20% annual rate through 2030. Additionally, as sugar taxes gain traction in emerging markets globally, the potential for growth becomes evident, albeit with varying implementation speeds.

Product reformulations by global beverage majors

Major beverage corporations, including Coca-Cola, are rapidly adopting stevia to align with consumer health demands and regulatory standards. Coca-Cola's SEC filings spotlight steviol glycosides as pivotal in their product reformulations. According to Ingredion, sports drinks are witnessing a notable surge, with brands capitalizing on stevia's heat stability and zero-calorie nature, leading to a significant CAGR in no-added-sugar claims[2]Source: Ingredion Incorporated, “News Releases and Investor Updates,” ingredionincorporated.com. Energy drink producers are turning to Cargill's EverSweet stevia, blending it with ClearFlo natural flavor to counterbalance the bitterness of functional ingredients while preserving a sugar-like sweetness. This trend isn't confined to beverages; food manufacturers are tapping into stevia's adaptability across bakery, dairy, and confectionery sectors. Yet, as blend ratios become more intricate, there's a heightened need for advanced flavor masking technologies to meet consumer acceptance.

Cost-efficient bioconversion of Rebaudioside M

UK authorities have greenlit PureCircle's bioconversion methods for producing Reb D and Reb M, processes that closely resemble natural synthesis, as reported by Food Ingredients First. Ingredion, as highlighted in its 2023 Annual Report, is expanding its stevia bioconversion facilities in Malaysia, positioning itself to leverage cost benefits while catering to the surging Asian appetite for high-purity sweeteners. Rebaudioside M, boasting a taste profile 300 times sweeter than sugar and devoid of a bitter aftertaste, commands a premium price. While its production is intricate, bioconversion techniques have managed to slash manufacturing costs by roughly 30% in comparison to traditional extraction methods. Joint patent applications by The Coca-Cola Company and PureCircle for enhanced Reb M solubility compositions underscore a sustained commitment to innovation and commercial viability. However, significant scaling challenges persist, especially in fermentation capacity and downstream purification processes.

Product personalization and functional food trends

Driven by a desire for personalized nutrition, consumers are increasingly turning to stevia blends that cater to their unique dietary needs and health goals. Many are cutting back on sugar and shunning artificial sweeteners. Research highlights stevia's promise, especially in nutraceuticals, with studies indicating its potential in managing diabetes. Notably, clinical studies published by MDPI show that sweeteners combined with chromium picolinate can enhance insulin sensitivity and lower fasting blood glucose. In the realm of functional beverages, there's a growing trend to blend stevia with prebiotics, probiotics, and botanical extracts, crafting wellness products aimed at distinct consumer groups. As consumers push for ingredient transparency, the demand for clean-label stevia solutions surges. However, the challenge lies in the complexity of formulations with diverse functional components. While personalization technologies are paving the way for tailored sweetness profiles, scaling these solutions for the broader market presents hurdles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Distinct aftertaste and flavor challenges | -1.4% | Global, particularly pronounced in Asia-Pacific taste preferences | Short term (≤ 2 years) |

| Supply chain and crop yield volatility | -1.1% | South America production regions, global supply networks | Medium term (2-4 years) |

| Pending EU harmonised labelling for blends | -0.8% | European Union markets | Short term (≤ 2 years) |

| Regulatory hurdles and market entry barriers | -0.6% | Emerging markets in MEA and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Distinct aftertaste and flavor challenges

Despite technological strides, taste profile limitations hinder stevia's broader market adoption. Rebaudioside A, a dominant player in commercial formulations, has been met with consumer backlash over its lingering bitter aftertaste, as highlighted by SupplySide Food Business Journal. While stevia commands a notable share in the global sugar-reduction product arena, inconsistencies in taste have stymied its deeper integration across various food categories. While advanced micro-encapsulation and flavor masking technologies offer some respite, they come at a cost, elevating final product prices by 15-25% over traditional sweeteners. Although newer steviol glycosides like Reb M promise enhanced taste profiles, their limited natural availability and elevated production costs curtail widespread adoption. Geographic preferences play a pivotal role in consumer acceptance: Asian markets exhibit a greater tolerance for stevia's unique flavor nuances, whereas Western consumers lean towards a taste experience akin to traditional sugar.

Supply chain and crop yield volatility

Pricing volatility, driven by agricultural production constraints and supply chain disruptions, undermines market predictability. U.S. tariffs on stevia imports from China and India compel brands to absorb costs and rethink sourcing strategies. While domestic cultivation initiatives in North Carolina and California show promise, their scale is limited. Despite USDA research funding for best management practices, fewer than 400 acres are planted across 10 counties, as reported by Farm Progress[3]Source: Farm Progress Editors, “First U.S. Commercial Stevia Planting in San Joaquin Valley,” farmprogress.com. Stevia's yield variability, influenced by environmental conditions, is further complicated by the absence of registered herbicides and fungicides. Research indicates potential in gibberellic acid treatments for salt stress tolerance and iron oxide nanoparticles for enhanced growth, but commercial implementation is still years away, according to MDPI. Efforts to diversify supply face hurdles due to limited global production regions and concentration risks in South America's growing areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Organic Premiumization Accelerates Despite Conventional Dominance

In 2024, conventional stevia blends dominate the market with an 86.24% share, thanks to established supply chains and cost advantages that facilitate widespread adoption in food and beverage applications. Meanwhile, organic stevia variants are on a rapid ascent, boasting a 12.44% CAGR through 2030, fueled by their premium positioning and the rising demand for clean-label products. Stevia First Corporation's pilot project in California, producing USDA and California Certified Organic stevia leaf, underscores the push for domestic organic production. Simultaneously, Pyure's achievement as the inaugural USDA Organic Certified stevia brand underscores the market's readiness to invest in certified organic products.

Quality Assurance International's organic certification underscores the intricate journey of stevia, ensuring its organic integrity from farm to final blend[4]Source: Quality Assurance International, “Organic Certification,” qai-inc.com. Cultivating organic stevia mandates specialized farming, eschewing synthetic pesticides and fertilizers. This commitment elevates production costs by 40-60%, yet the resultant premium pricing validates the investment. While the segment thrives on heightened consumer awareness of sustainable agricultural practices, supply constraints pose challenges to its swift expansion.

By Product Form: Powder Dominance Challenged by Liquid Innovation

In 2024, powder blends dominate the market with a 54.65% share, thanks to their established manufacturing processes, extended shelf life, and versatility across food categories, from baked goods to tabletop sweeteners. Their stability and cost-effective packaging make them a go-to for food manufacturers. Meanwhile, liquid blends are on the rise, boasting a 13.76% CAGR through 2030, driven by the beverage industry's push for ready-to-use formulations that sidestep dissolution issues.

Liquid stevia stands out for its superior dispersibility and instant sweetness, a boon for cold beverages where powder dissolution can be problematic. While granular and crystal blends cater to niche applications with specific particle size and flow needs, their market share is constrained by higher processing costs. Innovations in spray-drying are enhancing powder solubility without sacrificing cost benefits, yet liquid formats are carving a niche in premium beverages, where the convenience of instant use justifies the steeper price tag.

By Sweetener Combination: Sugar Blends Lead While Monk Fruit Partnerships Surge

In 2024, the combination of stevia and sugar (sucrose) commands a dominant 38.27% market share. This trend underscores consumers' preference for familiar sugar taste profiles and manufacturers' efforts to cut sweetener costs without compromising flavor. This blend allows for a notable sugar reduction—usually between 30-50%—while maintaining the mouthfeel and sweetness that pure stevia often struggles to deliver. Meanwhile, blends of stevia and erythritol are gaining traction, merging the advantages of zero calories with enhanced bulk and texture.

Stevia combined with monk fruit is the fastest-growing duo, boasting an impressive 11.53% CAGR through 2030. Its rise is attributed to its premium market positioning and a taste profile that effectively addresses the aftertaste concerns of single-sweetener blends. Yet, monk fruit's expansion faces hurdles in EU markets due to regulatory challenges. The EU's Novel Foods Regulation mandates extra safety assessments, posing significant entry barriers, as highlighted by MDPI. Other pairings, like stevia with allulose and prebiotic fibers, are making headway in functional food sectors. However, their market growth is tempered by challenges like ingredient costs and the intricacies of formulation.

By Application: Beverages Dominate While Nutraceuticals Accelerate

In 2024, beverages command a dominant 42.86% market share, buoyed by the rising popularity of carbonated soft drinks, sports nutrition, and energy drinks. Stevia's unique heat stability and zero-calorie nature offer these beverages a competitive edge. In response to sugar reduction mandates and a growing health-conscious consumer base, major beverage brands are rapidly reformulating their products, leading to an accelerated adoption of stevia. While the bakery and confectionery sectors grapple with stevia's effects on texture and browning, advancements in micro-encapsulation technology are enhancing stevia's performance in these applications.

Stevia is making significant inroads into nutraceuticals and pharmaceuticals, the industry's fastest-growing segment, projected to expand at an impressive 11.82% CAGR through 2030. This surge is largely attributed to research underscoring stevia's health benefits, which extend beyond mere sweetness to include potential antidiabetic and antihypertensive properties. Dairy products, especially yogurt and flavored milk, are increasingly turning to stevia blends, allowing them to cut down on sugar without compromising on taste. Meanwhile, tabletop sweeteners are riding the wave of consumer preference for natural over artificial. However, their market growth is tempered by challenges in taste acceptance and heightened price sensitivity when stacked against traditional sugar substitutes.

By Distribution Channel: B2B Ingredient Distribution Channel Drive Volume While Retail Accelerates

In 2024, the B2B Ingredient Distribution Channel commands a dominant 63.71% market share, underscoring the industrial focus of stevia processing. Food manufacturers lean towards bulk purchasing, seeking cost efficiencies. This channel reaps benefits from long-term supply contracts and the technical support services that ingredient suppliers extend to food and beverage manufacturers. Established ties between stevia producers and leading food corporations not only fortify these relationships but also pose entry challenges for newcomers, all while ensuring consistent volume stability.

Retail Distribution Channels are on a robust growth trajectory, boasting a 10.38% CAGR through 2030. This surge is fueled by a rising consumer appetite for natural sweetening alternatives and their growing presence in mainstream grocery outlets. While premium positioning allows retail products to command higher margins, their market penetration faces hurdles from consumer price sensitivity and distinct taste preferences. As retailers aim to capitalize on the burgeoning demand for natural sweeteners, private label opportunities broaden. Meanwhile, e-commerce platforms are carving out a niche, offering direct access to specialty and organic stevia products for the discerning consumer.

Geography Analysis

Asia-Pacific commands a dominant 39.34% share of the global market, bolstered by China's updated GB 2760-2024 additive standard, which delineates maximum-use levels for various food categories, as highlighted by Knoell Group. In Guangxi and Yunnan, contract farming, coupled with yield-improvement initiatives and automated drying lines, has optimized domestic leaf output and reduced unit costs. In a significant regulatory shift, India's authorities in 2024 relaxed restrictions on cross-category stevia applications, paving the way for its use in previously off-limits bakery and dairy sectors. Japan, a longstanding innovator, maintains its per-capita consumption levels by introducing mini-confectionery innovations. Meanwhile, in a proactive move, brands in Australia and New Zealand are adopting stevia ahead of impending reforms on "added-sugar" labels.

The Middle East and Africa emerge as the fastest-growing region, boasting an annual growth rate of 12.56%. As awareness of lifestyle diseases rises, the UAE, with its USD 536.83 billion economy, turns to imports of high-value clean-label ingredients, according to USDA insights. In a bid to attract suppliers from the U.S. and Europe, Saudi Arabia's Food and Drug Authority has expedited approvals for novel sweetener blends. South African beverage producers, drawing from their experience with sugar-tax compliance, are experimenting with stevia-infused sodas, eyeing neighboring markets. Despite challenges like cold chain and lab service gaps, sustained government health targets promise enduring demand.

North America maintains its influential stance, driven by regulatory clarity. The GRAS designation, alongside USDA-backed pilot cultivation initiatives in North Carolina and California, bolsters efforts for import substitution. Recognizing the importance of cross-border consistency, Canada’s bilingual labeling already incorporates steviol glycosides. In Europe, progress is more measured; the European Food Safety Authority is in the midst of reevaluating acceptable daily intake levels, and the lack of unified labeling for blends introduces an element of unpredictability. While South America continues to be a crucial supplier of leaves, fluctuations in currency values are moderating investments in downstream activities.

Competitive Landscape

The stevia sugar blends market exhibits moderate fragmentation, with the top five players collectively holding a significant share. Ingredion solidifies its market leadership with an 88% stake in PureCircle and a USD 100 million bioconversion facility in Indianapolis. Tate & Lyle's strategic USD 1.8 billion acquisition of CP Kelco integrates hydrocolloids into its sweetener portfolio, paving the way for enhanced cross-selling opportunities in dairy and beverage sectors.

Cargill sets itself apart with EverSweet, a fermentation-based rebaudioside M and D solution, now a staple in soft drinks and flavored waters. Their innovative closed-loop corn-sugar feedstock not only curtails carbon emissions but also bolsters ESG commitments in collaboration with global beverage giants. Meanwhile, smaller biotech players like SweeGen are making waves with patented enzyme platforms that boost conversion yields and minimize purification waste. Organic-focused Stevia First Corporation, capitalizing on California's unique terroir and fermentation techniques, secures contracts in the premium retail market.

Supply agreements are evolving, now often featuring joint R&D clauses tailored for custom sweetness profiles, effectively binding buyers in long-term partnerships. The licensing of encapsulation technology emerges as a pivotal competitive edge, enabling suppliers to earn royalties even on products they don't directly produce. While regional players in South America and Southeast Asia carve out niches through local leaf sourcing and government ties, they still lag in scale compared to their multinational counterparts.

Stevia Sugar Blends Industry Leaders

Cargill, Incorporated

Tate and Lyle PLC

Archer Daniels Midland Company

GLG Life Tech

Ingredion Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Ingredion announced an advancement in stevia sustainability initiatives while the EU approved fermented rapeseed cake ingredient, demonstrating continued regulatory progress for natural food ingredients. The company continues expanding its PureCircle stevia solutions portfolio with proprietary varietals.

- April 2025: Farm Progress reported on stevia cultivation expansion in Georgia as part of the state's non-traditional crop exploration program, with research universities and the Center of Innovation for Agribusiness collaborating to develop sustainable production methods for international markets.

- February 2025: S&W Seed Company initiated the first U.S. commercial stevia planting in California's San Joaquin Valley, partnering with PureCircle Limited for a 100-acre site with expansion plans to 1,000 acres. The project addresses mechanization challenges and profit model development for farmers.

- November 2024: Tate & Lyle completed the USD 1.8 billion acquisition of CP Kelco, creating a leading global specialty food and beverage solutions business with enhanced capabilities in sweetening, mouthfeel, and fortification technologies.

Global Stevia Sugar Blends Market Report Scope

| Organic |

| Conventional |

| Powder Blends |

| Liquid Blends |

| Granular/Crystal Blends |

| Stevia + Erythritol |

| Stevia + Monk-Fruit |

| Stevia + Sugar (Sucrose) |

| Others |

| Beverages |

| Bakery and Confectionery |

| Dairy Products |

| Table-top Sweeteners |

| Nutraceuticals and Pharmaceuticals |

| Other Applications |

| B2B Ingredient Distribution Channel |

| Retail Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Category | Organic | |

| Conventional | ||

| By Product Form | Powder Blends | |

| Liquid Blends | ||

| Granular/Crystal Blends | ||

| By Sweetener Combination | Stevia + Erythritol | |

| Stevia + Monk-Fruit | ||

| Stevia + Sugar (Sucrose) | ||

| Others | ||

| By Application | Beverages | |

| Bakery and Confectionery | ||

| Dairy Products | ||

| Table-top Sweeteners | ||

| Nutraceuticals and Pharmaceuticals | ||

| Other Applications | ||

| By Distribution Channel | B2B Ingredient Distribution Channel | |

| Retail Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How large is the stevia sugar blends market in 2025?

The stevia sugar blends market size is valued at USD 0.63 million in 2025 and is on track for steady expansion.

What is the forecast CAGR for stevia sugar blends to 2030?

Global revenue is projected to rise at a 9.75% CAGR between 2025 and 2030 on the back of sugar-reduction policies and bioconversion breakthroughs.

Which region leads consumption of stevia sugar blends?

Asia-Pacific holds the top spot with 39.34% share, supported by China’s updated additive rules and expanding leaf supply.

Which application is growing fastest?

Nutraceuticals and pharmaceuticals exhibit the fastest growth, with an 11.82% CAGR driven by interest in metabolic-health benefits.

Page last updated on: