White Sugar Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

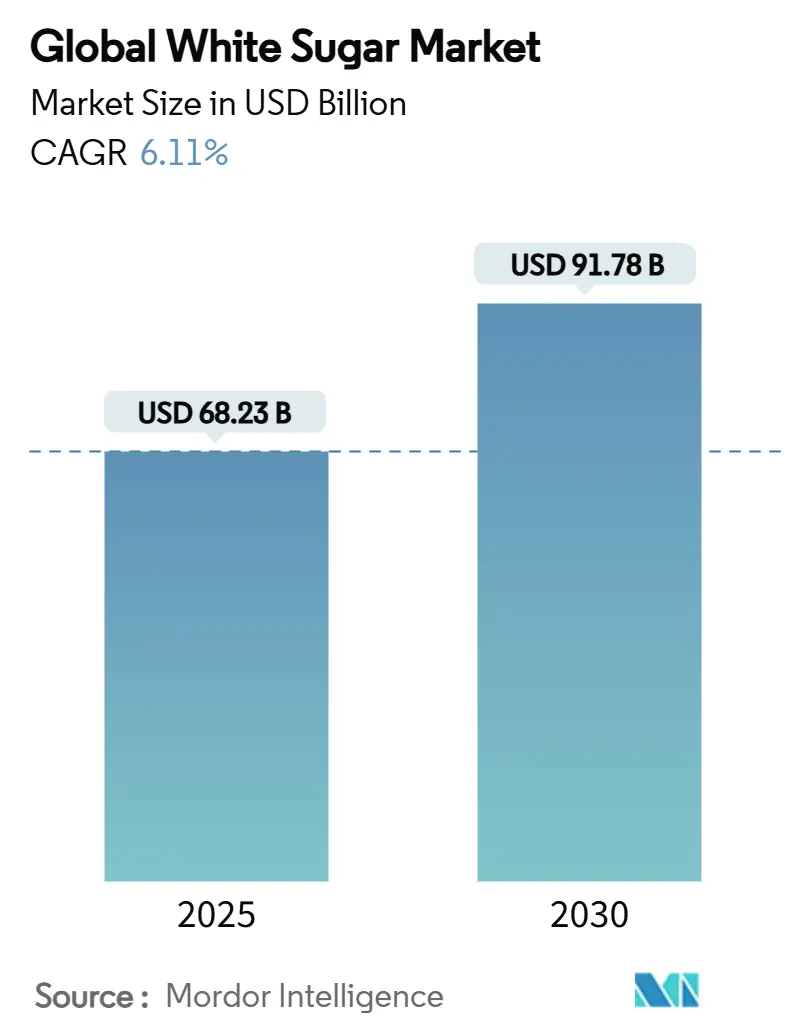

| Market Size (2025) | USD 68.23 Billion |

| Market Size (2030) | USD 91.78 Billion |

| Growth Rate (2025 - 2030) | 6.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

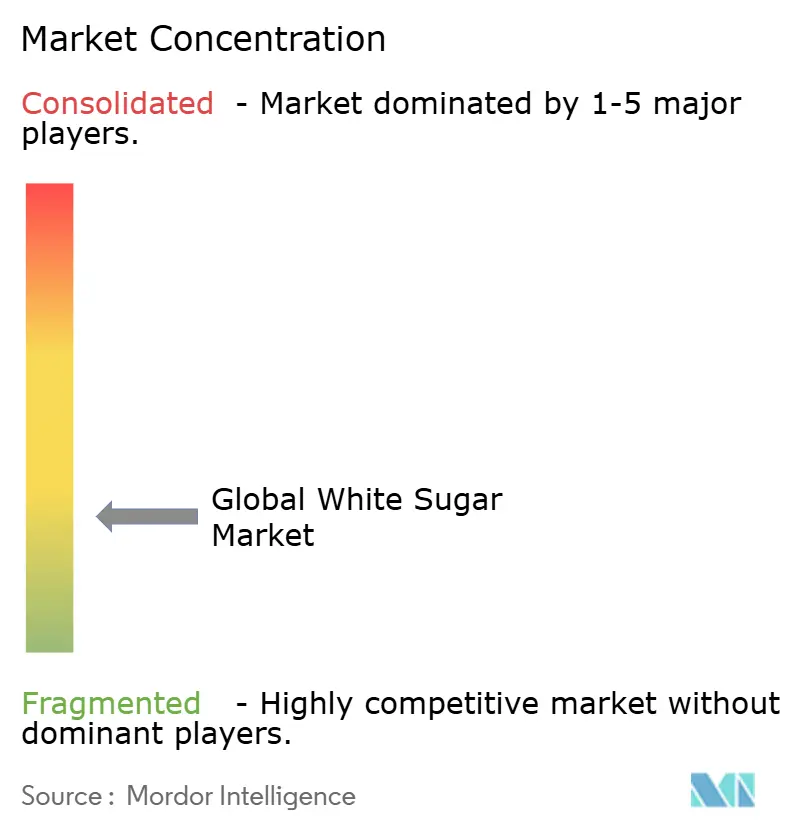

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

White Sugar Market Analysis by Mordor Intelligence

The white sugar market size is USD 68.23 billion in 2025 and is forecast to touch USD 91.78 billion by 2030, advancing at a 6.11% CAGR. Demand stability arises from sugar’s dual identity as a household staple and an indispensable industrial input. Industrial users value its functional traits—moisture retention, texture enhancement, and preservative ability—which anchor consumption even when retail preferences shift. According to the USDA Foreign Agricultural Service, in 2023/2024, India had a total sugar consumption amounting to approximately 31 million metric tons[1]Source: USDA Foreign Agricultural Service, "Sugar: World Markets and Trade", apps.fas.usda.gov. The global sugar consumption exceeded 176 million metric tons during that period. Fast-growing pharmaceutical and personal-care formulations widen the customer base, while innovations such as liquid formats streamline processing for beverage majors. Asia-Pacific leads both volume and velocity, benefiting from supportive farm policies in India, Thailand, and China that safeguard supply and feed rising urban appetites.

Key Report Takeaways

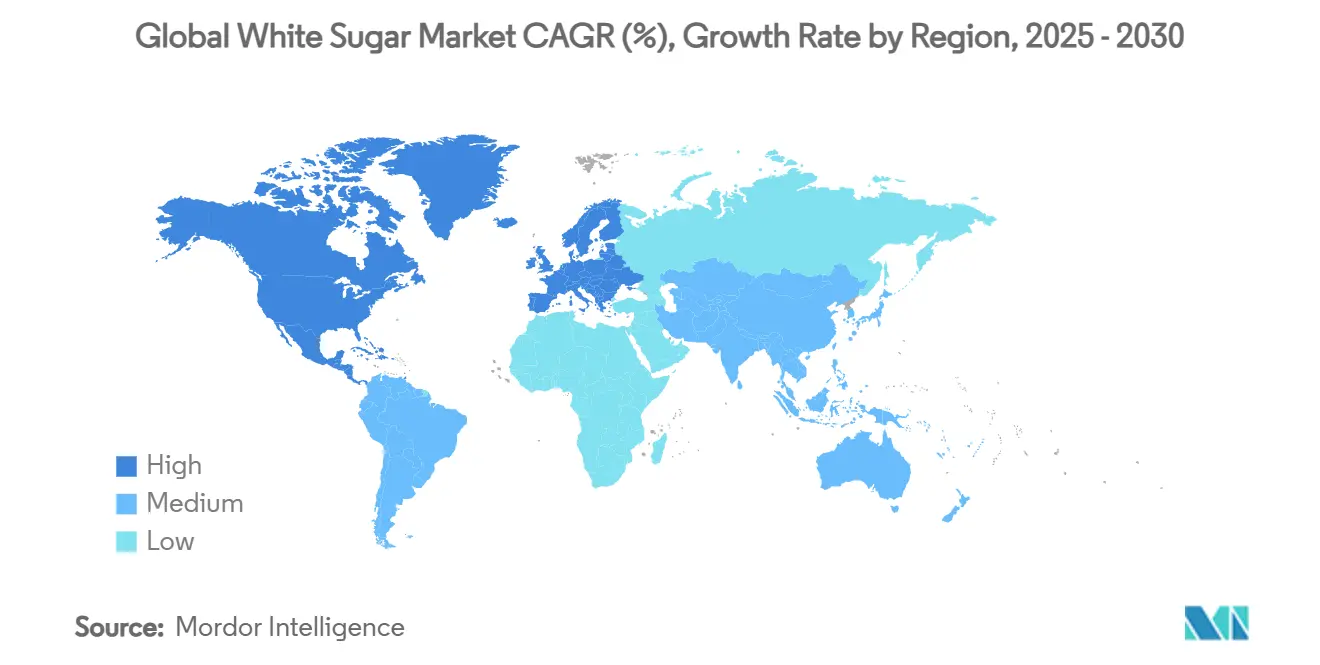

- By geography, Asia-Pacific held 38.4% of the white sugar market share in 2024 and is expanding at a 7.9% CAGR through 2030.

- By end-user industry, processed food and beverage captured 63.2% of the white sugar market size in 2024; industrial applications are set to grow 7.1% CAGR to 2030.

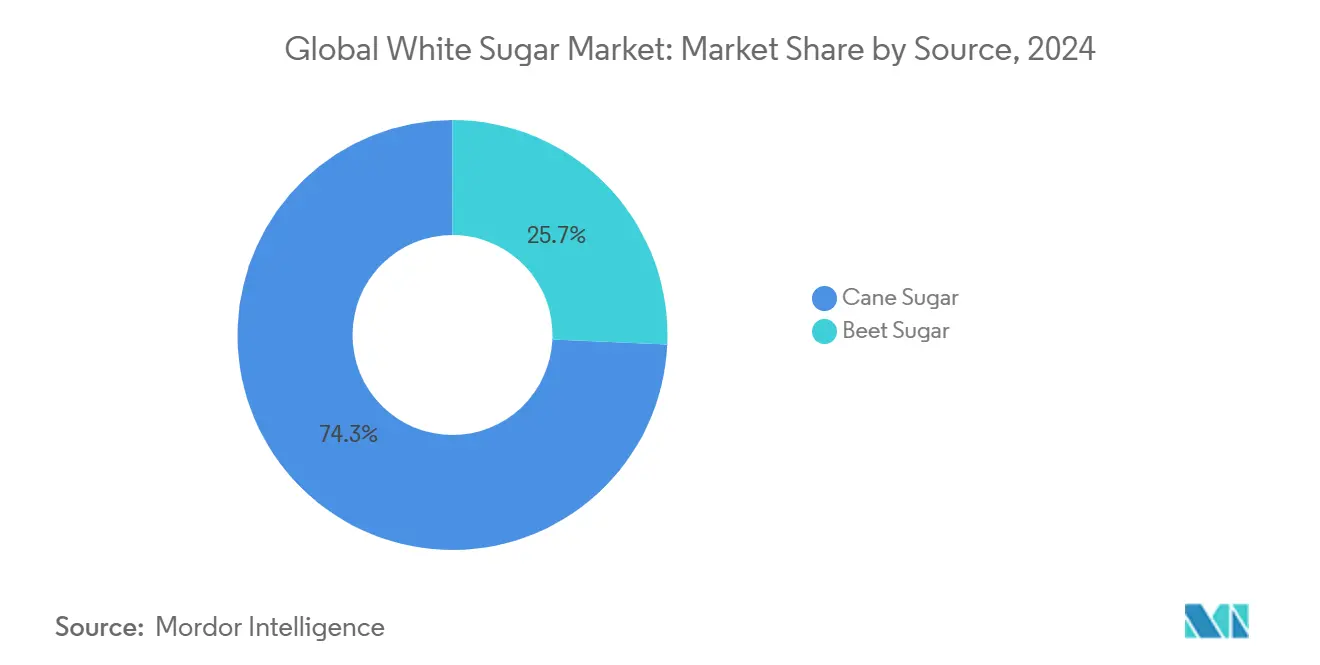

- By source, cane sugar accounted for 74.3% of the white sugar market share in 2024 and is projected to progress at a 6.8% CAGR during the period.

- By form, granulated sugar commanded 71.5% share of the white sugar market size in 2024, while liquid sugar is advancing at a 7.3% CAGR through 2030.

Global White Sugar Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Processed Food Industry | +1.8% | Global, with a concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Sugar's Role in Pharmaceuticals and Personal Care Products | +1.2% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Rising Popularity of Sweetened Beverages | +0.9% | Asia-Pacific core, spill-over to the Middle East and Africa, and Latin America | Short term (≤ 2 years) |

| Technological Advancements in Sugar Processing | +0.7% | Global, led by developed markets | Medium term (2-4 years) |

| Government Policies Promoting Domestic Sugar Production | +0.6% | India, Brazil, Thailand, Europe | Long term (≥ 4 years) |

| Sugar's Functional Properties in Food Manufacturing | +0.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Processed Food Industry

The processed food sector's expansion serves as the primary catalyst for white sugar demand growth, contributing an estimated 1.8% points to the market's CAGR. Food manufacturers increasingly rely on sugar's multifunctional properties beyond sweetening, including moisture retention, texture enhancement, and preservation capabilities. The sector's evolution toward convenience foods and ready-to-eat products amplifies sugar consumption per unit, as manufacturers optimize formulations for shelf stability and consumer palatability. For instance, according to the International Food Information Council, in 2024, a total of 60% of respondents in the United States stated that they snack once or twice a day[2]Source: International Food Information Council, "2024 IFIC Food & Health SURVEY", www.ific.org. Coca-Cola's strategic pricing models now explicitly factor sugar cost volatility into concentrate operations, reflecting the ingredient's critical role in beverage economics. This industrial dependence creates demand resilience that transcends consumer health trends, as functional requirements often necessitate sugar inclusion regardless of sweetness preferences.

Sugar's Role in Pharmaceuticals and Personal Care Products

Pharmaceutical and personal care applications represent the highest-growth driver segment, adding 1.2% points to market expansion through specialized excipient and formulation requirements. Sugar's role extends beyond traditional sweetening to include tablet binding, coating applications, and stability enhancement in liquid formulations. The FDA's recent approval of calcium phosphate as a color additive for doughnut sugar and coated candies demonstrates regulatory support for sugar-based innovations in specialized applications. Personal care manufacturers increasingly leverage sugar's natural origin and gentle properties for exfoliation and moisturizing products, creating premium market segments with higher margins. This diversification reduces the industry's exposure to food-focused health regulations while opening pathways to value-added product development.

Rising Popularity of Sweetened Beverages

Beverage industry expansion, particularly in emerging markets, contributes to sugar market growth through volume increases and premiumization trends. Asia-Pacific markets drive this expansion, with urbanization and rising disposable incomes fueling demand for carbonated soft drinks, energy beverages, and traditional sweetened teas. The segment's growth accelerates during economic recovery periods and cultural celebrations, as evidenced by Indonesia's increased sugar import allocations following recent elections and religious festivities. For instance, according to the U.S. Department of Agriculture, in 2024/2024, Indonesia imported 5 million metric tons of sugar and was the biggest importer of sugar in that period[3]Source: US Department of Agriculture, "Sugar: World Markets and Trade", apps.fas.usda.gov. Beverage manufacturers' preference for liquid sugar formats enhances processing efficiency and quality consistency, supporting the 7.3% CAGR growth in the liquid white sugar segments. This trend creates supply chain optimization opportunities for refiners capable of delivering just-in-time liquid sugar solutions.

Technological Advancements in Sugar Processing

Processing technology innovations contribute to market growth through efficiency gains and quality improvements that expand application possibilities. Advanced enzymatic treatments now enable sugar production from poor-quality beets, with α-galactosidase applications reducing raffinose content and improving sucrose yield. China's development of the LC05-136 sugarcane variety demonstrates how agricultural technology enhances production efficiency, with the variety now cultivated across 1.67 million hectares and offering superior drought resistance. Moreover, digital solutions in sugarcane production, including precision agriculture and data analytics, enable yield optimization and cost reduction across major producing regions. These technological advances create competitive advantages for early adopters while expanding the economic viability of sugar production in marginal growing conditions.

Restrains Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health Concerns and Regulatory Pressure | -1.4% | Global, most pronounced in North America and Europe | Short term (≤ 2 years) |

| Competition from Alternative Sweeteners | -0.8% | Developed markets, expanding globally | Medium term (2-4 years) |

| Quality Control and Production Variability | -0.6% | Global, acute in developing regions | Medium term (2-4 years) |

| Government Policy and Trade Restrictions | -0.4% | Regional, affecting trade flows | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health Concerns and Regulatory Pressure

Escalating health concerns and regulatory interventions represent the most significant growth constraint, reducing market CAGR through consumption reduction mandates and reformulation pressures. According to the survey conducted by the International Food Information Council, 66% of respondents were reportedly trying to limit sugars in their diet in 2024. The FDA's proposed front-of-package nutrition labeling requirements will mandate clear identification of added sugar content, potentially influencing consumer purchasing decisions and forcing manufacturers to reformulate products. Additionally, WHO guidelines linking excessive sugar intake to noncommunicable diseases create policy frameworks that national governments increasingly adopt for public health interventions. The regulatory environment's evolution toward mandatory sugar reduction targets, similar to sodium reduction initiatives, threatens traditional consumption patterns across developed markets. However, this pressure simultaneously creates opportunities for specialty sugar products that offer functional benefits beyond sweetening, potentially offsetting volume declines through value premiums.

Competition from Alternative Sweeteners

Alternative sweetener adoption constrains sugar market growth as manufacturers seek cost-effective substitution strategies amid health-conscious consumer trends. Ingredion's sweetener portfolio, representing 34% of the company's net sales in 2024, demonstrates the scale of competitive pressure from high fructose corn syrup and glucose-based alternatives. Tate & Lyle's strategic focus on bio-converted stevia and specialty sweetening solutions reflects industry efforts to capture health-conscious market segments while maintaining functional performance. The competitive threat intensifies in developed markets where regulatory frameworks support alternative sweetener approval and consumer education promotes substitution. Nevertheless, sugar's unique functional properties in baking, preservation, and texture development create defensive moats that limit substitution potential in specific applications, particularly in industrial food manufacturing where performance requirements exceed simple sweetening needs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Cane Sugar Dominance Drives Global Production

Cane sugar commands 74.3% market share in 2024, with its segment projected to grow at 6.8% CAGR through 2030, reflecting both production advantages and established supply chain infrastructure. Tropical and subtropical regions provide optimal growing conditions for sugarcane cultivation, enabling year-round production cycles that beet sugar cannot match. Brazil's record sugarcane production of 705 million metric tons in the 2023-2024 marketing year exemplifies this segment's scale advantages, though production is expected to decline by 8.5% in 2024-2025 due to adverse weather conditions, according to the U.S. Department of Agriculture. Beet sugar production faces increasing pressure from climate variability and cost inflation, as evidenced by the closure of California's Spreckels facility after cumulative losses over the past decade.

The cane sugar segment benefits from technological innovations that enhance processing efficiency and expand cultivation possibilities. Digital solutions in sugarcane production, including precision agriculture and data analytics, enable yield optimization while reducing environmental impact. Beet sugar processors increasingly focus on niche markets and specialty applications, with enzymatic treatments improving sugar quality from poor-quality beets and creating differentiation opportunities in premium segments.

By Form: Liquid Sugar Innovation Transforms Processing

Granulated sugar maintains 71.5% market share in 2024, serving traditional retail and basic industrial applications, while liquid white sugar emerges as the fastest-growing segment at 7.3% CAGR through 2030. This growth differential reflects food manufacturers' preference for liquid formats that enhance processing efficiency, reduce handling costs, and improve quality consistency in automated production lines. Liquid sugar eliminates dissolution steps in beverage production, reduces contamination risks, and enables precise dosing in continuous manufacturing processes. The segment's expansion aligns with the broader industrial trend toward just-in-time delivery and lean manufacturing principles that minimize inventory carrying costs.

Powdered sugar occupies specialized applications in confectionery and baking, where particle size and flow characteristics determine product quality and processing performance. The form segmentation increasingly reflects end-user sophistication, with industrial customers demanding customized specifications that optimize their specific production requirements. Südzucker's focus on sugar specialties and customized products demonstrates how refiners capture value through form differentiation rather than commodity competition. Technological advances in spray drying and crystallization control enable refiners to produce specialized forms that command premium pricing while serving niche market requirements.

By End-User Industry: Industrial Applications Drive Future Growth

The processed food and beverage industry represents 63.2% of market demand in 2024, leveraging sugar's multifunctional properties beyond sweetening to include preservation, texture enhancement, and moisture control. This segment's maturity creates stability but limits growth potential as health-conscious reformulation reduces sugar content per unit of production. Industrial uses for non-food applications emerge as the fastest-growing segment at 7.1% CAGR, driven by pharmaceutical excipient requirements, personal care formulations, and chemical processing applications. The FDA's approval of calcium phosphate as a color additive for sugar-based products demonstrates regulatory support for specialized industrial applications.

Household and retail consumption patterns reflect regional economic development and urbanization trends, with emerging markets driving volume growth while developed markets focus on premium and organic segments. Foodservice demand correlates with tourism recovery and dining industry expansion, creating cyclical growth patterns that amplify during economic recovery periods. The segmentation increasingly reflects value chain sophistication, with industrial customers demanding technical support, quality guarantees, and supply chain reliability that extend beyond commodity pricing considerations. This evolution favors integrated refiners capable of providing comprehensive solutions rather than spot market suppliers competing solely on price.

Geography Analysis

Asia-Pacific controls 38.4% of global volume and posts a brisk 7.9% CAGR, underpinned by population density, rising disposable incomes, and supportive farm policies. India forecasts 35.5 million tons of sugar output in 2024-2025 after favorable monsoons, ensuring ample raw material for domestic refiners, according to the U.S. Department of Agriculture. Thailand anticipates a 10.2 million-ton crop, aided by replanting programs and irrigation upgrades. China’s mix of cane and beet production provides supply flexibility, shielding processors from climatic shocks.

North America represents a mature consumption basin where quota regimes stabilize prices. The 2025 tariff-rate quota reassignment adjusts import ceilings to balance supply, maintaining predictability for confectioners while guarding farm incomes, according to the Office of the United States Trade Representative. Beverage taxes in select US municipalities dampen volume growth, yet bakery and dairy sectors sustain baseline offtake. Liquid sugar logistics hubs along the Gulf Coast enhance just-in-time delivery for soda and dairy plants, illustrating infrastructural entrenchment.

Europe confronts climatic volatility and acreage contraction. French cooperative Tereos predicts a 9% decline in beet planting for the 2025 season, squeezing continental output. Processors offset tighter supply through refinery efficiency gains and by importing raw cane for toll refining. Stringent labeling norms push formulators toward lower-sugar recipes, but premium organic and Fairtrade lines preserve margin headroom, maintaining Europe’s relevance within the white sugar market.

Competitive Landscape

The global white sugar market exhibits moderate consolidation with established players leveraging vertical integration strategies to capture value across the supply chain from agricultural production through refining and distribution. Market leaders including Sudzucker, Tereos, and Wilmar International maintain competitive advantages through scale economies, geographic diversification, and technological capabilities that enable cost leadership and quality consistency. Südzucker's preliminary 2024-2025 financial results, showing revenues around EUR 9.7 billion despite challenging market conditions, demonstrate the resilience of integrated operations during price volatility periods.

The competitive intensity reflects the commodity nature of basic sugar products, with differentiation opportunities emerging through specialty grades, liquid formats, and value-added services that address specific customer requirements. Strategic patterns emphasize operational efficiency improvements, sustainability initiatives, and geographic expansion into high-growth markets as primary competitive vectors. Nordzucker's biomethane project in Denmark, powering sugar production from beet residues, exemplifies how sustainability investments create both cost advantages and market differentiation.

Technology adoption in precision agriculture and digital processing solutions enables yield optimization and quality enhancement that translates into competitive advantages for early adopters. White-space opportunities exist in specialty applications, pharmaceutical-grade products, and emerging markets where local production capabilities remain underdeveloped, creating entry points for focused competitors willing to invest in market development and customer education.

White Sugar Industry Leaders

-

American Sugar Refining, Inc.

-

Südzucker AG

-

Tereos S.A.

-

Wilmar International Ltd.

-

Associated British Foods plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Domino Sugar revamped its packaging with the "Easy Baking Tub," a rectangular, recyclable, and easy-to-store container for granulated sugar. The new design uses 28% less plastic than previous canisters, features tamper-evident and user-friendly lids, and allows consumers to buy refills and reuse the tub for sustainability.

- March 2025: C&H Sugar introduced a new ultrafine granulated baker’s sugar in a convenient “Easy Baking Tub” packaging. Designed for superior baking performance, it dissolves quickly and is Non-GMO and Kosher certified. The new packaging focused on enhanced user convenience and recycling friendliness, expanding availability across the Western U.S. and online channels.

- January 2025: ADM launched new minimally processed liquid sugar solutions tailored for industrial food processing, offering uniform color and texture, and designed for improved food production efficiency in the bakery and beverage sectors.

- November 2024: Florida Crystals introduced new packaging across its retail sugar lines, prominently displaying the "Regenerative Organic Certified" insignia. The rebranding included bolder graphics, product renaming, and packaging made from compostable, multi-wall paper-based materials. The certification and refreshed branding emphasize soil health, sustainable agriculture, and transparency for environmentally conscious consumers.

Global White Sugar Market Report Scope

| Cane Sugar |

| Beet Sugar |

| Granulated |

| Powdered |

| Liquid White Sugar |

| Processed Food and Beverage Industry |

| Industrial Uses (Non-food applications) |

| Household/Retail |

| Foodservice |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | Cane Sugar | |

| Beet Sugar | ||

| By Form | Granulated | |

| Powdered | ||

| Liquid White Sugar | ||

| By End-User Industry | Processed Food and Beverage Industry | |

| Industrial Uses (Non-food applications) | ||

| Household/Retail | ||

| Foodservice | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the current global demand for refined white sugar?

The white sugar market size is USD 68.23 billion in 2025 and is projected to climb to USD 91.78 billion by 2030.

Which region is expanding fastest in refined sugar consumption?

Asia-Pacific records the quickest growth at a 7.9% CAGR, supported by urbanization, rising incomes, and pro-farm policies.

What segment offers the highest growth opportunity?

Industrial applications—pharmaceuticals, personal care, and chemicals—are forecast to grow 7.1% CAGR, outpacing food and beverage demand.

Why are liquid sugar formats gaining traction?

Beverage and dairy processors adopt liquid sugar to avoid on-site dissolution, cut contamination risk, and enable precise automated dosing.

How do health regulations affect sugar producers?

Front-of-package labeling and sugar-reduction targets impose volume pressure, yet they also encourage premium specialty sugars with functional advantages.

Who are the major global players and what is their strategy?

Südzucker, Tereos, and Wilmar International dominate through vertically integrated models, efficiency initiatives, and expansion into high-growth APAC markets.

Page last updated on: