Market Overview

| Study Period | 2021 - 2031 |

|---|---|

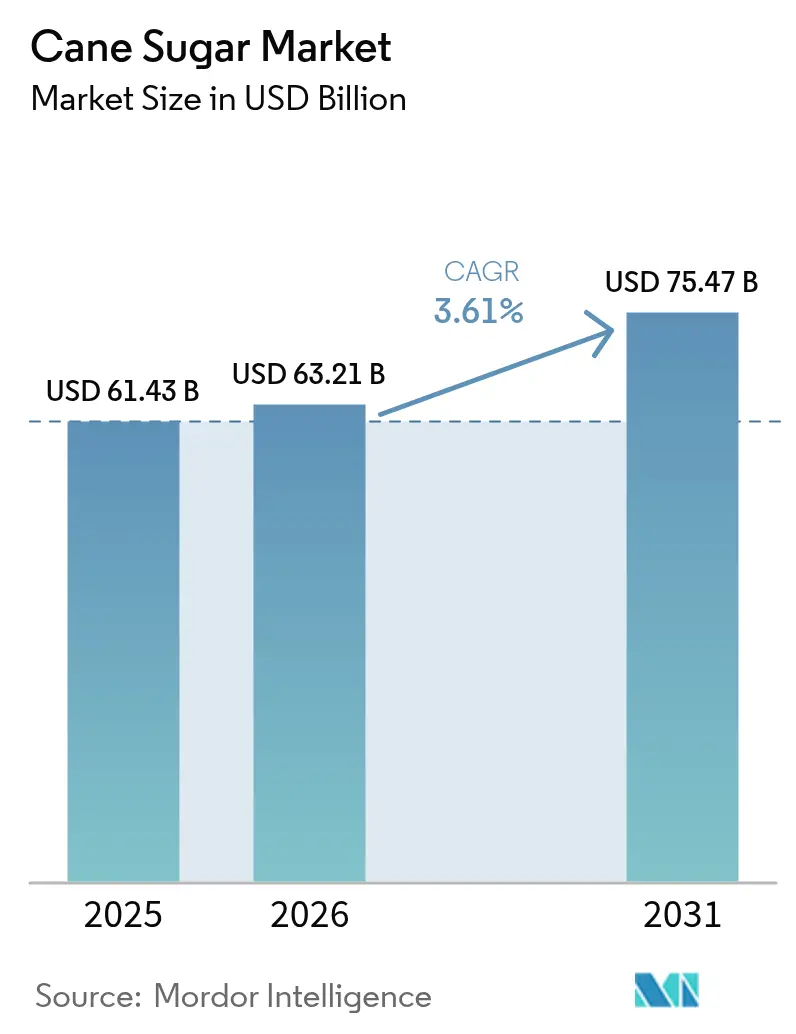

| Market Size (2026) | USD 63.21 Billion |

| Market Size (2031) | USD 75.47 Billion |

| Growth Rate (2026 - 2031) | 3.61% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

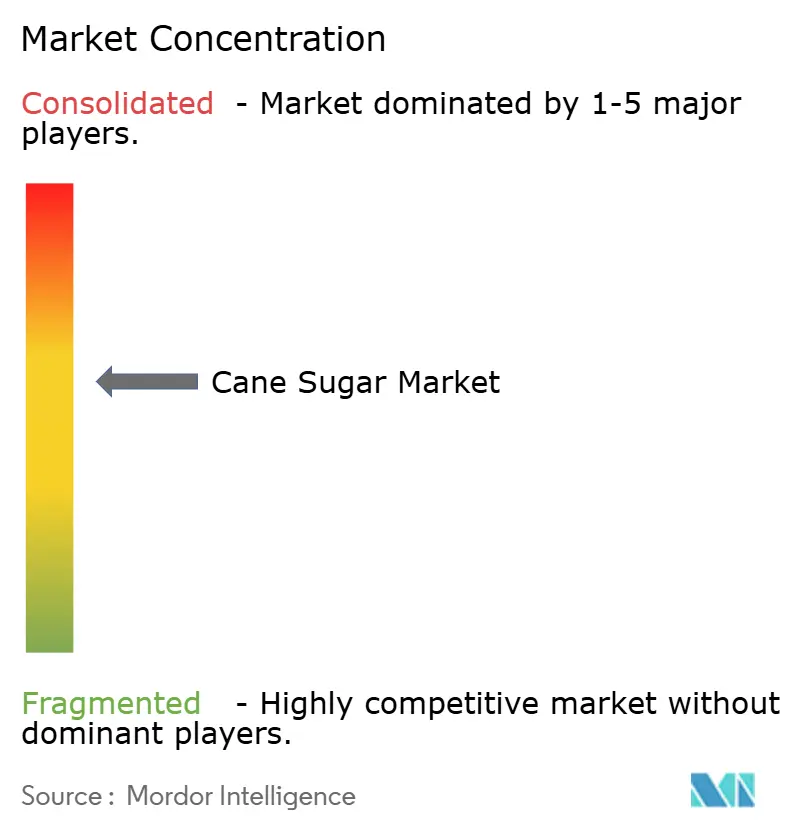

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cane Sugar Market Analysis by Mordor Intelligence

The cane sugar market size was USD 61.43 billion in 2025, projected to reach USD 63.21 billion in 2026, and USD 75.47 billion by 2031, growing at a CAGR of 3.61% from 2026 to 2031. Robust demand from packaged food and beverage manufacturers, expanding middle-income populations in Asia, and government initiatives that favor cane cultivation collectively strengthen near-term sales prospects for the cane sugar market. Investments in high-efficiency milling technologies lower extraction losses and enhance overall returns, prompting estates in Brazil, India, and Thailand to modernize their facilities. Retailers continue to witness a seasonal lift during religious and cultural festivals, when households purchase larger packs for home cooking and gifting, further amplifying volume throughput. At the same time, multinationals pushing premium brown and organic variants encourage value growth even where per-capita consumption has plateaued.

Key Report Takeaways

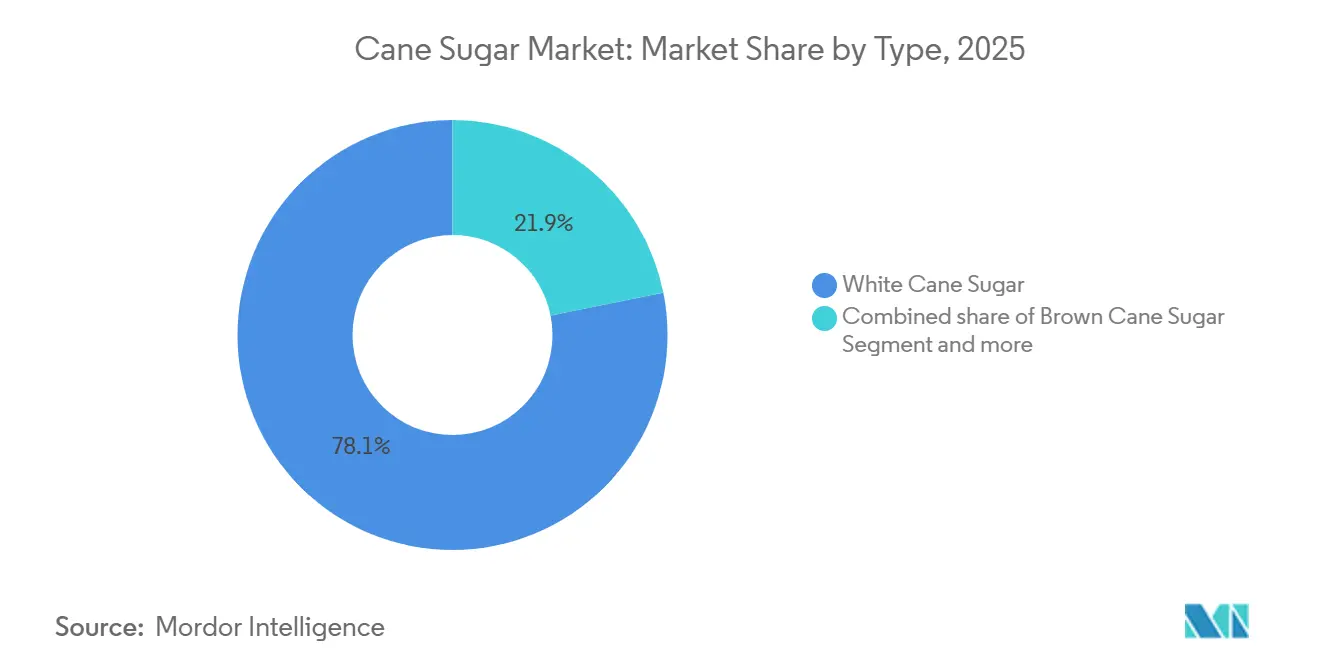

- By ingredient type, white cane sugar led with 78.14% of the cane sugar market share in 2025; brown cane sugar is forecast to expand at a 4.26% CAGR between 2026 and 2031.

- By category, conventional products accounted for 91.26% of the 2025 cane sugar market size, and organic offerings are projected to grow at a 5.21% CAGR from 2026 to 2031.

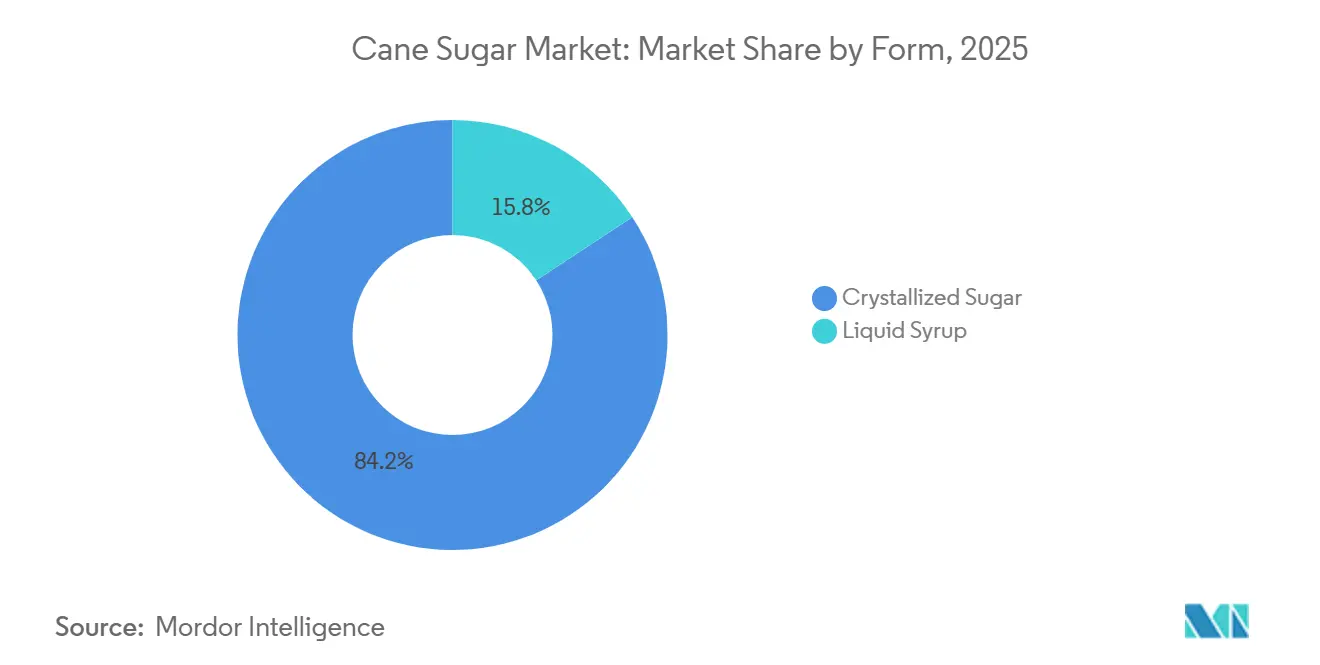

- By form, crystallized sugar commanded 84.23% of global revenue in 2025, while liquid syrup is set to register a 5.55% CAGR through 2031.

- By end-user, the food processing industry captured 45.03% of sales in 2025, whereas retail channels are poised for the fastest 5.28% CAGR during 2026-2031.

- By geography, Asia-Pacific represented 41.09% of worldwide demand in 2025, and the Middle East and Africa are projected to post the strongest 5.26% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Cane Sugar Market*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Processed foods industry expansion boosts market demand | +0.8% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Festive seasons spark surge in bulk sugar purchases | +0.6% | APAC core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Tech innovations enhance cane extraction and processing | +0.7% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Government backing for sugarcane farming fuels industry growth | +0.3% | Global, with regional variations in timing | Short term (≤ 2 years) |

| Affordable and accessible: developing markets drive demand | +0.5% | Brazil, India, Thailand, Australia | Long term (≥ 4 years) |

| Beverage consumption surge drives market demand | +0.4% | India, Brazil, Thailand, select African nations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Beverage consumption surge drives market demand

The beverage industry's growth, driven by both traditional carbonated drinks and the rising popularity of functional beverages, is significantly boosting the demand for cane sugar. In 2023, Brazil achieved a record sugar production of 45.8 million tons, a milestone influenced by elevated international prices fueled by the beverage industry's demand. Additionally, Brazil's ethanol production reached 35.3 billion liters, highlighting the sector's adaptability in balancing sugar and ethanol outputs based on market dynamic [1]Source: Energy Research Office, "Analysis of Current Biofuels Outlook –Year 2023", epe.gov.br. Looking ahead, the International Sugar Organization forecasts a global sugar deficit of 500,000 tons in 2024. This shortfall is expected to have a pronounced impact on beverage-heavy regions such as the Middle East, where supply chain disruptions, exacerbated by the ongoing Red Sea crisis, are intensifying demand pressures. This imbalance between supply and demand presents strategic opportunities for beverage companies to mitigate risks by securing long-term supply contracts. Such measures could accelerate vertical integration trends, enabling companies to gain greater control over their supply chains and reduce dependency on external suppliers.

Affordable and accessible: developing markets drive demand

Developing markets are leveraging the cost advantages of cane sugar over alternative sweeteners, driven by local production scaling, reduced import dependency, and supportive government policies. For example, India's decision to increase the Fair and Remunerative Price to INR 355 per quintal for the 2025-26 period reflects a dual focus on maintaining competitive pricing and enhancing farmer incomes. This variety is notable for its high yield and resilience, which are critical for sustaining production levels. In contrast, Canada exemplifies a developed market approach with its open sugar policy, characterized by one of the lowest global sugar tariffs and the absence of government subsidies. This policy framework ensures competitive pricing and broad market acces [2]Source: Canadian Sugar Institute, "Canada's Open Market Sugar Policy", sugar.ca. However, the cost advantage of cane sugar is increasingly challenged by climate-induced yield variability. Weather-related production disruptions in major producing regions highlight the growing need for technological advancements and climate-resilient agricultural practices to safeguard competitive positioning in the global market.

Processed foods industry expansion boosts market demand

Industrial applications increasingly require sugar with consistent quality and functional properties that go beyond basic sweetening, such as preservation, texture improvement, and flavor enhancement. For the period from October 2024 to September 2025, the U.S. Customs and Border Protection has established refined sugar quotas totaling 7,090,000 kg, with specific allocations of 10,300,000 kg for Canada and 2,954,000 kg for Mexico [3]Source: U.S. Customs and Border Protection, "QB 24-301 2025 Refined Sugar", cbp.gov. These allocations reflect structured trade relationships that support the processed food manufacturing sector. Rising urbanization and busier lifestyles push consumers toward packaged snacks, sauces, and ready-to-drink beverages that rely on crystalline sugar for consistent taste and texture. Global brands have scaled up localized manufacturing in Indonesia, Mexico, and Nigeria, anchoring steady offtake agreements with nearby mills. The effect is particularly visible in baked goods, where sugar acts as both a sweetener and a structural ingredient that controls browning.

Festive seasons spark surge in bulk sugar purchases

In India, the Middle East, and Latin America, religious and cultural calendars set the stage for predictable surges in wholesale orders, notably during festive periods like Ramadan, Diwali, and Christmas. These peaks aren't just about tradition; they're pivotal moments that shape the financial landscape for many businesses. Confectioners, keenly aware of these rhythms, front-load their procurement, often securing inventory four to six weeks ahead of these festivities. This strategy not only locks in favorable spot prices but also acts as a buffer against potential transport disruptions. Retail promotions, especially on multi-kilogram packs, play a crucial role in encouraging home cooking of desserts and traditional beverages. This push not only celebrates cultural practices but also nudges up per-capita consumption rates. Producers, astute in their approach, schedule maintenance during quieter months. They then ramp up crushing capacity as the festive window approaches, a move that effectively stabilizes factory utilization rates. As a result, this strategic dance with seasonal demand not only amplifies top-line revenue but also ensures smoother cash flows for both cane growers and refiners.

Restraints Impact Analysis of Cane Sugar Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health warnings on sugar consumption dampen its usage | -0.9% | North America and EU primarily, expanding globally | Medium term (2-4 years) |

| Surge in natural and artificial sugar substitutes stifles growth | -0.6% | Developed markets, gradually spreading to emerging economies | Long term (≥ 4 years) |

| Government-imposed sugar taxes hamper market expansion | -0.5% | EU, select North American jurisdictions, expanding to APAC | Short term (≤ 2 years) |

| Unpredictable weather patterns disrupt cane farming and supply | -0.7% | Brazil, India, Thailand, Australia, Caribbean | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health warnings on sugar consumption dampen its usage

Public-health agencies continue to link high-added-sugar diets with obesity, diabetes, and dental cavities, prompting stricter labeling mandates. In response to these health concerns, several countries are considering even more stringent measures. These measures aim not only to inform consumers but also to curb the rising tide of sugar-related health issues. Foodservice chains in the United States have lowered fountain beverage cup sizes, while European schools limit sugary snack availability. These initiatives reflect a growing global consensus on the need to address sugar consumption. As awareness grows, more institutions are likely to adopt similar measures. Some consumers switch to reduced-calorie products or reach for fresh fruits rather than confectionery. This shift highlights a broader trend towards health-conscious choices in daily diets. As alternatives gain popularity, traditional sugary treats face declining demand. Although reformulations often replace a portion of sucrose with non-nutritive sweeteners, total sweetener weight still declines, shaving incremental demand over the medium term. This trend suggests a fundamental shift in consumer preferences, with potential long-term implications for the sugar industry.

Surge in natural and artificial sugar substitutes stifles growth

Plant-based options such as stevia and monk-fruit extracts have moved from niche to mainstream, gaining shelf space in carbonated drinks and tabletop sachets. These natural sweeteners are not only being embraced by health-conscious consumers but are also finding their way into gourmet and artisanal products. Sucralose and aspartame remain popular among weight-management and diabetic demographics. Their continued use underscores a persistent demand for sugar Substitutes, especially in the face of rising health awareness. Major beverage multinationals advertise “zero sugar” variants heavily, carving share from traditional full-sugar lines. This shift not only reflects changing consumer preferences but also highlights the industry's pivot towards healthier offerings. Ingredient suppliers also tout sugar-reduction solutions that blend fibers with high-intensity sweeteners, preserving mouthfeel while halving sucrose content. Such innovations are reshaping the landscape of sweetener solutions, catering to both taste and health. This evolution in sweetener technology signals a transformative phase for the sugar industry, with implications for producers and consumers alike.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Cane Sugar Market Segment Analysis

By Ingredient Type:

White Sugar Industrial DominanceThe white cane sugar segment accounted for 78.14% of 2025 revenue, reflecting its ubiquitous role across packaged foods, beverages, and household cooking. This overwhelming share underscores how refiners have optimized large-scale crystallization processes that deliver cost advantages, uniform grain size, and high purity. Brown cane sugar, conversely, retains trace molasses, imparting a caramel note coveted in premium bakery goods. Gourmet brands highlight their “less processed” positioning, which appeals to millennials seeking authenticity. The cane sugar market size for brown variants is projected to expand at a 4.26% CAGR between 2026 and 2031, outpacing overall category growth as cafés, breweries, and craft dessert parlors experiment with distinctive flavor layers. Specialty grocers in Europe and North America are devoting additional shelf facings to turbinado and demerara formats, nurturing trial and repeat purchases.

White cane sugar’s supremacy translates into economies of scale that limit price differentials against beet-derived substitutes, preserving high penetration in mass-market applications. The segment’s considerable cane sugar market share also supports stable refinery asset utilization rates, enabling operators to amortize capital upgrades swiftly. In fast-growing Asian economies, household shifts from loose jaggery to packaged white sugar further cement the product’s leading status. Brown sugar’s opportunity lies in value rather than sheer tonnage, evidenced by average unit prices that track 15-20% above refined grades. With café chains incorporating brown syrup toppings and craft cola makers trumpeting natural color, the segment enjoys brand-building potential that can insulate margins during commodity price swings.

By Category:

Conventional Production Scale AdvantagesConventional cane sugar captured 91.26% of 2025 sales, reflecting extensive cultivation under standard agronomic practices and the wide availability of chemical inputs that maximize yields. Large-scale plantation owners favor fertilizers and pesticides to mitigate pests and disease pressure, keeping farm-gate costs low. Bulk buyers, particularly bottlers and bakery groups, prize this predictable quality and volume. Organic cane sugar remains a small niche in current tonnage terms, yet its 5.21% projected CAGR implies meaningful headroom. Certification prohibits synthetic agro-chemicals, aligning with consumer demand for clean-label products. The premium averages USD 0.14 per kilogram, cushioning grower profitability even at reduced yields.

Retail brands highlight traceability and environmental stewardship to justify higher shelf prices, while craft chocolate makers specify single-origin organic sugar on ingredient panels. Multinationals have pledged to source a percentage of inputs under regenerative standards, raising long-term procurement of certified organic cane. Development agencies in Paraguay and the Philippines fund smallholder transition programs, easing certification costs and linking producers to export markets. As supply chains mature, the size of the cane sugar market for organic variants could accelerate further, especially if governments roll out incentives analogous to those in cocoa and coffee sustainability initiatives.

By Form:

Crystallized Sugar Versatility LeadershipCrystallized sugar accounted for 84.23% of worldwide revenue in 2025, driven by its broad utility in both solid and liquid formulations after dissolution. Refineries rely on centrifugation and drying lines capable of producing multiple grain sizes that fit applications ranging from powdered drink mixes to decorations on donuts. The form’s large cane sugar market size cements its bargaining leverage with food processors, who negotiate annual contracts pegged to commodity indices. Liquid syrup, comprising invert and glucose-fructose blends derived from cane. Despite modest tonnage, syrup is expected to enjoy a 5.55% CAGR through 2031 as beverage concentrate plants embrace its pumpable format, which lowers handling losses.

Syrup also simplifies cold-fill operations and reduces dissolution time in instant coffee mixes, offering throughput gains that outweigh its marginally higher price per sucrose unit. Start-ups producing cocktail mixers and flavored milk are shifting to cane-sourced liquid sweeteners to market “natural” credentials versus corn syrups. Meanwhile, crystallized sugar producers adopt moisture-controlled packaging that extends shelf life in humid climates, protecting their market leadership. Investments in refinery side-stream capabilities, such as on-site inversion units, enable firms to capture demand in both crystallized and liquid segments, optimizing asset ROI within the broader cane sugar market.

By End-User:

Food Processing Industry Dominates While Retail SurgesFood processing accounted for 45.03% of global revenue in 2025, underscoring the centrality of sucrose in formulations that rely on its bulking, texturizing, and preservative properties. Large-volume users negotiate multi-year supply agreements, anchoring a predictable offtake for refiners. Within this channel, bakery and confectionery claim the lion’s share, followed by dairy and beverage producers that require consistent sweetness profiles. Retail channels, including supermarkets, convenience stores, and e-commerce, hold a significant share yet are slated for the fastest 5.28% CAGR through 2031. Rising home-baking trends, fueled by social-media cooking tutorials, spur households to trade up to specialty sugars such as raw and muscovado formats.

Foodservice represents a significant share of current demand, with cafés and quick-service restaurants integrating portion-control sachets to manage cost and hygiene. As tourism rebounds in Southeast Asia and the Middle East, beverage outlets anticipate higher footfall, indirectly benefiting the cane sugar market size captured by foodservice. Processors diversify their supply bases geographically to mitigate weather-related disruptions, while retailers deploy dynamic pricing algorithms that align pack sizes with household budget constraints. Across all channels, value-added packaging, such as resealable pouches and recyclable paper bags, differentiates brands and supports premium positioning.

Geography Analysis

APAC Cane Sugar Market

Asia-Pacific generated 41.09% of global revenue in 2025, anchored by India’s vast consumer base and China’s industrial demand for beverages and confectionery. Governments in the region subsidize drip-irrigation equipment, boosting field productivity and ensuring raw-material availability for domestic refiners. Rapid urban migration elevates disposable incomes, spurring demand for packaged snacks and sweetened teas that intensively utilize sucrose. As a result, the Asia-Pacific cane sugar market size is forecast to climb steadily despite public-health awareness campaigns, thanks to population momentum and lifestyle shifts toward convenience foods.

LATAM Cane Sugar Market

Latin America, led by Brazil and Mexico, remains both a supply powerhouse and a growing consumption hub. Mills in Brazil benefit from integrated operations that switch between sugar and ethanol depending on global price spreads, stabilizing revenue streams. Mexico’s proximity to the United States secures tariff-rate quotas that guarantee export outlets while its domestic bakery sector expands. Together, these dynamics foster investment in mechanical harvesting and cogeneration facilities, which lower per-unit costs and cement competitive advantage for Latin American producers. Regional beverage giants also market fruit-flavored sodas sweetened with cane, sustaining internal demand and underpinning the cane sugar market share captured by local refineries.

MEA Cane Sugar Market

In the Middle East and Africa, the cane sugar market is projected to post the highest 5.26% CAGR through 2031, albeit from a smaller base. Gulf Cooperation Council states import refined sugar for re-export as value-added blends, leveraging port infrastructure and free-zone incentives. Meanwhile, Egypt and Sudan invest in irrigation projects along the Nile corridor to curtail reliance on imports. Rising young populations and fast-food proliferation in Nigeria, Kenya, and South Africa elevate consumption of carbonated drinks and confectionery. Nonetheless, sub-Saharan supply chains contend with logistic bottlenecks, prompting policymakers to prioritize rail upgrades that could unlock latent demand over the long term.

Competitive Landscape

The cane sugar market features integrated agro-industrial conglomerates and regionally entrenched cooperatives. Florida Crystals (ASR Group) leverages vertically aligned estates in Florida and the Dominican Republic to supply North American customers under the Domino brand. In 2025, the company completed a biomass-powered turbine upgrade that reduced steam consumption, signaling efficiency priority. Wilmar International and Louis Dreyfus broadened their refining footprints across Indonesia and the UAE, respectively, to reach burgeoning Asian and Middle-Eastern confectionery clients. Such capacity expansions reinforce logistical agility while tapping duty-free trade corridors.

Strategic alliances remain pivotal. Cosan and Shell continue to co-manage Raízen, enabling flexible output sharing between crystal sugar and ethanol depending on market signals. Tereos renewed multiyear contracts with European beverage bottlers, securing base-load volumes that justify refinery debottlenecking investments. Mitr Phol intensified R&D into high-fiber bagasse pellets, adding circular-economy revenue alongside its core sweetener business. Meanwhile, Associated British Foods (AB Sugar) piloted carbon-capture systems at its British refineries, positioning itself for anticipated EU emissions regulations.

Despite ongoing consolidation, regional niches persist. Dalmia Bharat and Balrampur Chini command scale in India’s Uttar Pradesh belt through proximity to cane growers and sustained state price supports. Tongaat Hulett restructures asset holdings in Southern Africa to streamline debt, while Sudzucker focuses on specialty sugar derivatives for Europe’s premium chocolate segment. Competitive intensity is shaped by access to low-cost raw cane, energy-efficient processing technologies, and diversified downstream portfolios that hedge commodity cyclicality.

Cane Sugar Industry Leaders

-

Louis Dreyfus Company B.V.

-

Wilmar International Limited

-

Cosan S.A.

-

Florida Crystals Corporation (ASR Group)

-

Biosev SA

- *Disclaimer: Major Players sorted in no particular order

Cane Sugar Market Companies Covered in this Report

- Florida Crystals Corporation (ASR Group)

- Wilmar International Limited

- Louis Dreyfus Company B.V.

- Biosev SA

- Dalmia Bharat Group

- Global Organics Ltd.

- DO-IT Food Ingredients B.V.

- Cosan S.A.

- Tereos S.A.

- Balrampur Commercial Enterprises Limited

- Murugappa Group (EID Parry )

- Mitr Phol Sugar Corporation Ltd.

- Tongaat Hulett Limited

- Sudzucker AG

- Thai Roong Ruang Sugar Group Co., Ltd.

- Associated British Foods plc (AB Sugar)

- DCM Shriram Ltd.

- Bunge Limited

- Dhampur Sugar Mills Ltd

- Bajaj Group (BHSL)

Recent Industry Developments in Cane Sugar Market

- April 2025: Sucro Limited has announced the successful completion of its purchase of an adjoining property in Chicago from a related party. This strategic acquisition supports Sucro’s ongoing expansion in the United States' cane sugar supply chain, enabling increased operational capacity and improved logistics at its Chicago facility.

- March 2025: C&H Sugar introduced C&H Baker’s Sugar™ in its new Easy Baking Tub. According to the company, this ultrafine grain pure cane sugar helps achieve superior baking performance, while the easy-to-use packaging enhances convenience and efficiency.

- August 2024: KSL (Khon Kaen Sugar Industry Public Company Limited) is significantly expanding its production capacity with the construction of a new sugar factory in Sa Kaeo Province, Thailand. This strategic move is part of KSL’s broader effort to boost operational efficiency and support its growth targets. According to the brand, the new plant is projected to help raise cane extraction to 6.75 million tons, a 23% increase over the previous year, and drive expected 2025 revenue to over 19 billion baht.

Global Cane Sugar Market Report Scope

The cane sugar market is primarily developing owing to sugarcane accessibility and other properties, such as a superior flavor prevalent enough to beat beet sugar. The Cane Sugar Market is Segmented by Ingredient Type (White Cane Sugar, and More), Category (Organic and Conventional), Form (Crystallized Sugar and Liquid Syrup), End-User (Retail, Foodservice, and Food Processing Industry), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Segmentation Overview

By Ingredient Type

| White Cane Sugar |

| Brown Cane Sugar |

| Others |

By Category

| Organic |

| Conventional |

By Form

| Crystallized Sugar |

| Liquid Syrup |

By End-User

| Retail | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| Foodservice | ||

| Food Processing industry | Bakery and Confectionery | Cakes and Pastries |

| Cookies | ||

| Candies | ||

| Chocolates | ||

| Others | ||

| Dairy | Ice Cream | |

| Yogurt | ||

| Milkshakes | ||

| Others | ||

| Beverages | Carbonated Drinks | |

| Fruit Juices | ||

| Coffee and Tea Sweeteners | ||

| Alcoholic Beverages | ||

| Others | ||

| Sauces and Condiments | ||

| Savory Snacks | ||

| Other Applications | ||

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Ingredient Type | White Cane Sugar | ||

| Brown Cane Sugar | |||

| Others | |||

| By Category | Organic | ||

| Conventional | |||

| By Form | Crystallized Sugar | ||

| Liquid Syrup | |||

| By End-User | Retail | Supermarkets and Hypermarkets | |

| Convenience Stores | |||

| Online Retail Stores | |||

| Other Distribution Channel | |||

| Foodservice | |||

| Food Processing industry | Bakery and Confectionery | Cakes and Pastries | |

| Cookies | |||

| Candies | |||

| Chocolates | |||

| Others | |||

| Dairy | Ice Cream | ||

| Yogurt | |||

| Milkshakes | |||

| Others | |||

| Beverages | Carbonated Drinks | ||

| Fruit Juices | |||

| Coffee and Tea Sweeteners | |||

| Alcoholic Beverages | |||

| Others | |||

| Sauces and Condiments | |||

| Savory Snacks | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What is the projected value of cane sugar market by 2031?

The cane sugar market is forecast to reach USD 75.47 billion by 2031.

How fast is cane sugar consumption expected to grow between 2026 and 2031?

Global demand is projected to expand at a 3.61% CAGR over 2026-2031.

Which ingredient type currently leads worldwide cane sugar sales?

White cane sugar led with a 78.14% share of 2025 revenue.

Which region will post the fastest growth through 2031?

The Middle East and Africa are expected to record the highest 5.26% CAGR to 2031.

Page last updated on: