Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 9.18 Billion |

| Market Size (2031) | USD 11.42 Billion |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

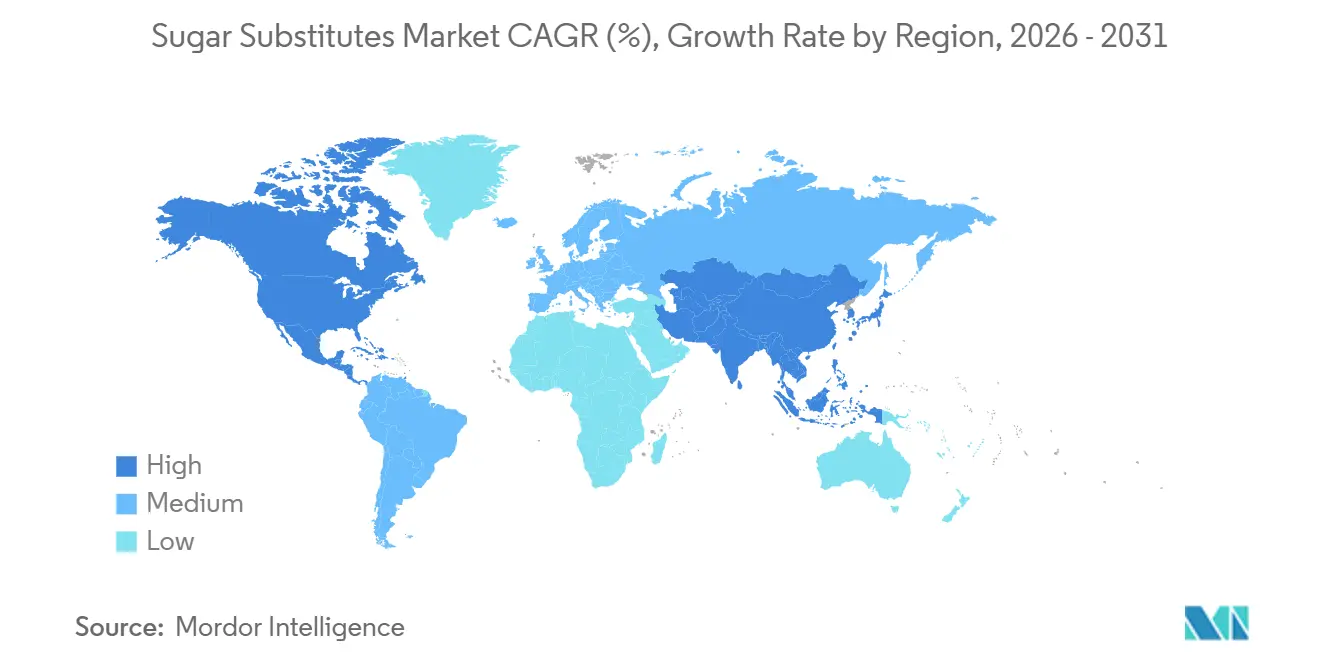

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sugar Substitutes Market Analysis by Mordor Intelligence

The sugar substitutes market size was valued at USD 8.55 billion in 2025 and is estimated to grow from USD 9.18 billion in 2026 to reach USD 11.42 billion by 2031, at a CAGR of 4.68% during the forecast period (2026-2031). Rapid growth in diabetes and obesity prevalence, the proliferation of front-of-package warning labels, and expanding zero-sugar product lines are reshaping purchasing patterns. Multinational beverage companies are pushing reformulation agendas to avoid sugar taxes, while food manufacturers adopt blend strategies that combine high-intensity sweeteners with polyols to solve texture gaps. Precision-fermentation platforms are lowering production costs and carbon footprints across the sugar substitutes market, creating a pathway for next-generation sweeteners that satisfy clean-label and sustainability demands. Competitive pressure in the sugar substitutes market is intensifying as Chinese polyol exporters leverage cost advantages and biotech start-ups commercialize novel molecules that bypass agricultural volatility.

Key Report Takeaways

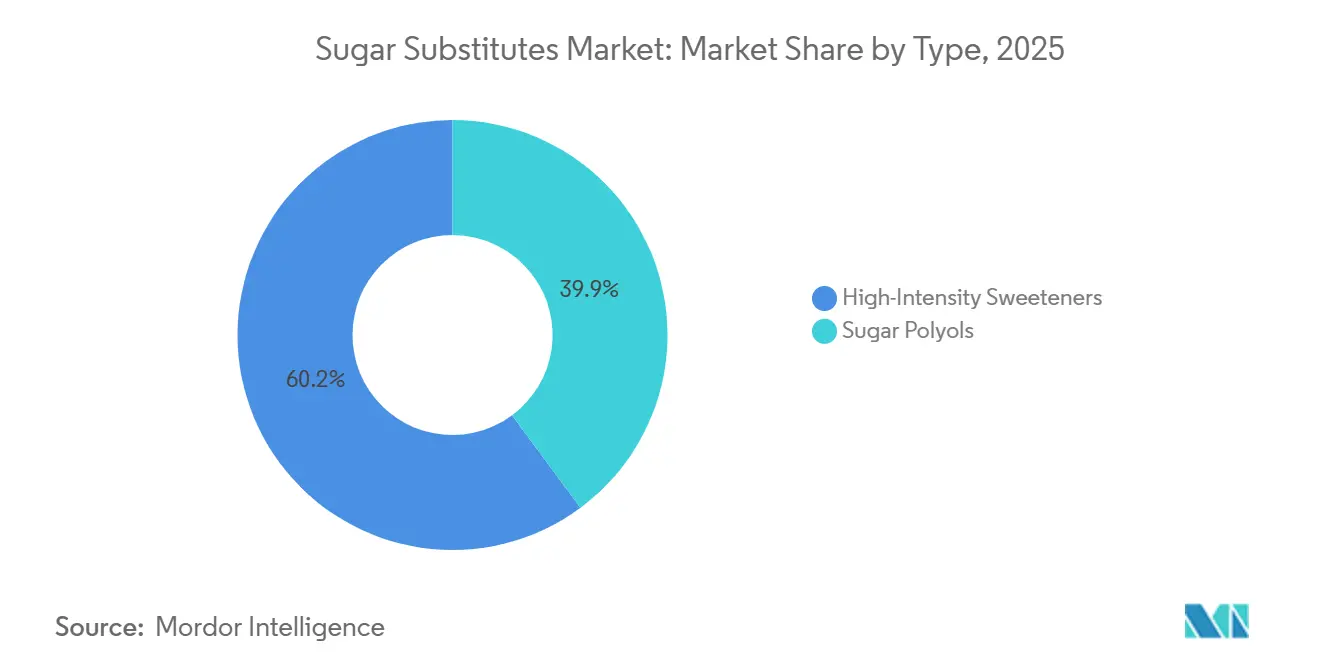

- By type, high-intensity sweeteners led with 60.15% of the sugar substitutes market share in 2025, while sugar polyols recorded the fastest projected CAGR at 5.89% through 2031.

- By origin, plant-based sweeteners captured 55.32% revenue in 2025; biotechnology-fermented variants are forecast to expand at a 6.14% CAGR to 2031.

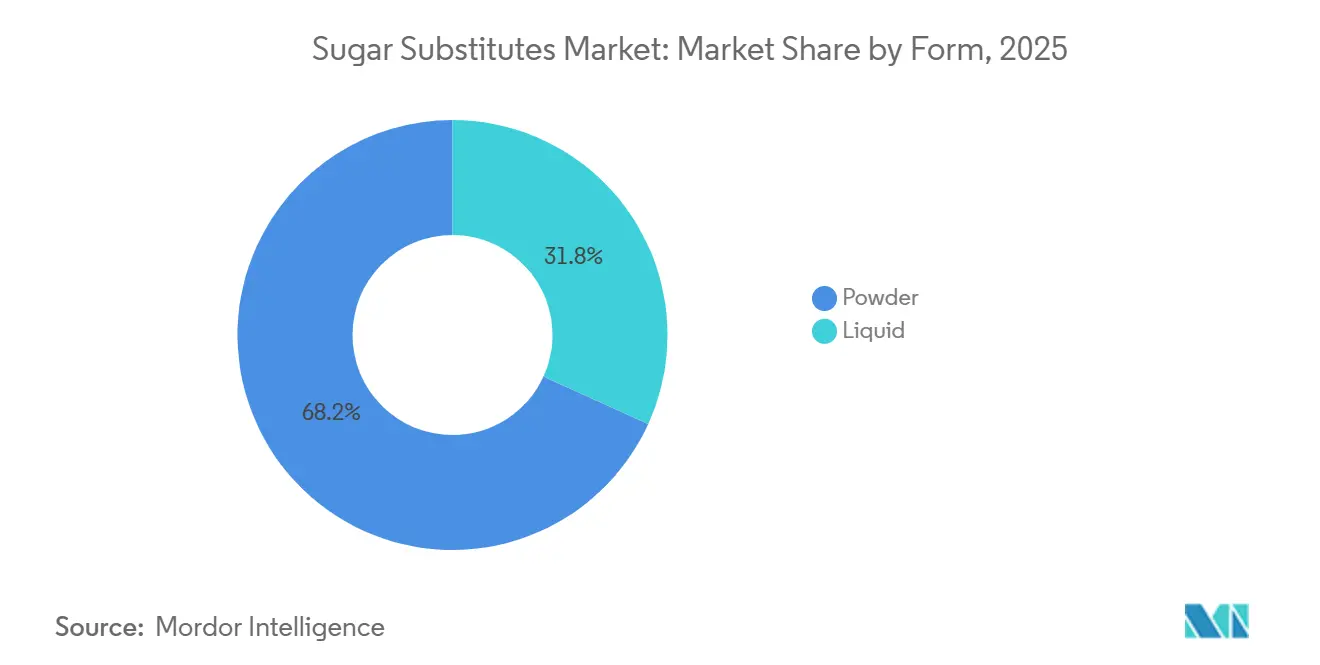

- By form, powders accounted for 68.21% of the sugar substitutes market size in 2025, whereas liquids posted the highest growth at 5.42% CAGR.

- By application, beverages commanded 42.12% of 2025 revenue, yet food applications are advancing at a 5.58% CAGR through 2031.

- By geography, Asia-Pacific dominated with 45.21% share in 2025 and is set to grow at 6.21% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sugar Substitutes Market Trends and Insights

Drivers Impact Table*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring Diabetes and Obesity Rates Fuel Demand for Low-Calorie Sweeteners | +1.2% | Global, with highest impact in Asia-Pacific (China, India) and North America | Long term (≥ 4 years) |

| Surge in Demand for Clean-Label Sweeteners | +0.9% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Advances in Extraction and Processing Technologies Reduce Production Costs | +0.7% | Global, with production concentrated in China and fermentation hubs in North America, Europe | Medium term (2-4 years) |

| Sugar Substitutes Offer Customizable Sweetness and Texture Profiles | +0.5% | Global, particularly food and beverage manufacturers in developed markets | Short term (≤ 2 years) |

| Expansion of Low/No-Sugar Products Fuels Market Growth | +1.0% | Global, led by North America and Europe, expanding in Asia-Pacific | Short term (≤ 2 years) |

| Rising Shift to Lower-Carbon Footprint Ingredients | +0.4% | Europe, North America, with spillover to Asia-Pacific sustainability-focused brands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring Diabetes and Obesity Rates Fuel Demand for Low-Calorie Sweeteners

The prevalence of obesity is projected to rise from 2.11 billion adults in 2021 to 3.80 billion by 2050, driving significant demand for zero-calorie and low-calorie sweeteners. The Asia-Pacific region faces the greatest impact, with China reporting 140 million diabetes cases and India 101 million. However, per-capita sweetener consumption in these countries remains far below Western levels. Beverage multinationals are capitalizing on this disparity by introducing localized zero-sugar products. Additionally, the emergence of GLP-1 receptor agonists, such as semaglutide and tirzepatide, is transforming consumer behavior. While users of these weight-loss drugs reduce overall caloric intake, they continue to prefer sweetened products. This has led manufacturers to reformulate using high-intensity sweeteners that offer flavor without metabolic effects. This shift represents a long-term trend rather than a temporary change in the sugar substitutes market rather than a temporary trend. Despite margin pressures caused by Chinese polyol export pricing, the sugar substitutes industry expects sustained volume growth.

Surge in Demand for Clean-Label Sweeteners

Consumer preference has solidified around plant-derived sweeteners, with 75% of respondents in a Kerry Group survey highlighting the importance of natural ingredients. Furthermore, 56% of participants in an International Food Information Council (IFIC) survey recognized the health benefits of low- and no-calorie sweeteners when used as substitutes for added sugars[1]Source: International Food Information Council. "2024 Food and Health Survey." foodinsight.org. This growing trend is driving the adoption of stevia and monk fruit in North America and Europe. In these markets, products with "natural" claims on their front packaging command a price premium of 15-20% over synthetic alternatives. The demand for clean labels is transforming supply chains across the sugar substitutes market. Brands are increasingly sourcing certified organic stevia from Paraguay and monk fruit from Guangxi province in China to comply with Non-GMO Project and USDA Organic standards, creating a traceability challenge. Vertically integrated suppliers like Ingredion, which increased its ownership of the PureCircle stevia subsidiary to 98% in 2024, are well-positioned to address these complexities. While synthetic sweeteners remain in pharmaceutical excipients and industrial applications, where cost considerations dominate, the sugar substitutes market is clearly segmenting. Consumer-facing products are dividing into two distinct categories: premium natural and cost-effective synthetic.

Advances in Extraction and Processing Technologies Reduce Production Costs

Precision fermentation and metabolic engineering are collapsing the cost gap between plant-extracted and biotech-derived sweeteners, with engineered yeast strains now achieving erythritol titers of 245 grams per liter and xylitol titers of 200 grams per liter in fed-batch reactors. CRISPR/Cas9 gene editing has enabled researchers to overexpress xylose reductase and xylitol dehydrogenase pathways in Yarrowia lipolytica, boosting polyol yields by 40% compared to first-generation strains. DSM-Firmenich and Cargill's Avansya joint venture received EFSA and UK Food Standards Agency approval in January 2024 for EverSweet, a fermented stevia glycoside that uses 81% less carbon, 96% less land, and 97% less water than cane sugar. This sustainability profile aligns with Scope 3 emissions targets for multinational food companies. Enzymatic conversion routes are also maturing within the sugar substitutes market, with D-allulose 3-epimerase and L-arabinose isomerase enabling cost-effective rare-sugar production from fructose feedstocks. These bioprocessing advances are geographically concentrated in North America and Europe, strengthening technological leadership in the sugar substitutes market, where regulatory frameworks for genetically modified microorganisms are established, creating a technology moat that Chinese contract manufacturers are racing to replicate through licensing deals and reverse engineering.

Expansion of Low/No-Sugar Products Fuels Market Growth

By 2024, Coca-Cola introduced over 800 reduced- or no-sugar products in its global portfolio. This includes the February 2024 launch of Coca-Cola Spiced Zero Sugar and the Coca-Cola Creations series, which combines zero-sugar formulations with limited-edition flavors. In 2023, PepsiCo reformulated Pepsi Zero Sugar and expanded the distribution of Mountain Dew Zero Sugar to appeal to younger consumers seeking energy without metabolic concerns. Mexico's Phase 3 front-of-package warning labels, effective in 2025, will mandate "excess sugar" warnings on beverages containing more than 5 grams of sugar per 100 milliliters. This regulation has prompted Coca-Cola FEMSA and Arca Continental to increase their zero-sugar product offerings across Latin America. Kerry Group's Tastesense™ Sweetness platform, launched in February 2026, enables up to 100% sugar reduction in dairy, bakery, and beverage applications by masking metallic and bitter off-notes from high-intensity sweeteners. This innovation represents a significant breakthrough in the sugar substitutes market. The expansion of zero-sugar offerings extends opportunities in the sugar substitutes market beyond beverages; Nestlé's KitKat Plant-Based and Milo's 25% reduced sugar variant demonstrate that, as taste-masking technologies advance, confectioneries and malt beverages are also viable for reformulation.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer Safety Perception Issues Around Artificial Sweeteners | -0.6% | Global, with heightened concerns in North America and Europe | Short term (≤ 2 years) |

| Regulatory Ambiguity Around Novel Sweeteners | -0.5% | Europe (EFSA jurisdiction), with spillover to emerging markets adopting EU standards | Medium term (2-4 years) |

| Taste Profile Challenges in Mass-Produced Products | -0.3% | Global, particularly in cost-sensitive segments and developing markets | Short term (≤ 2 years) |

| Competition from Natural Sugars | -0.2% | North America, Europe, where premium positioning supports higher prices | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer Safety Perception Issues Around Artificial Sweeteners

In March 2023, the FDA responded by stating it "does not question the safety" of erythritol, reaffirming its Generally Recognized As Safe (GRAS) status, while committing to monitor new scientific developments[2]Source: FDA, “Statement on Erythritol Safety,” fda.gov. At the same time, the European Food Safety Authority (EFSA) maintained its 2023 determination of an acceptable daily intake of 0.5 grams per kilogram of body weight and chose not to implement additional restrictions. Despite the absence of regulatory action, the study raised consumer concerns within the sugar substitutes market. Consequently, some brands quietly reformulated their products, replacing erythritol with stevia-allulose blends to protect their reputations. The Calorie Control Council, an industry group, criticized the study's methodology and emphasized that erythritol naturally occurs in fruits and fermented foods in small amounts. However, the negative perception persists, particularly among health-conscious consumers. Similarly, aspartame faced scrutiny when the International Agency for Research on Cancer classified it as "possibly carcinogenic to humans" (Group 2B) in July 2023. Nevertheless, the Joint FAO/WHO Expert Committee on Food Additives reaffirmed its acceptable daily intake of 40 milligrams per kilogram of body weight. These periodic safety controversies create uncertainty across the sugar substitutes industry, leading cautious brands to diversify their sweetener portfolios to reduce reliance on single ingredients.

Regulatory Ambiguity Around Novel Sweeteners

In 2025, EFSA denied allulose's novel food application due to an incomplete safety dossier[3]Source: EFSA, “Novel Foods Database Entry – Allulose,” efsa.europa.eu. This decision sharply contrasts with the FDA's 2019 determination of Generally Recognized As Safe (GRAS) status for allulose, which also excluded it from total and added sugars labeling. This regulatory divergence complicates product development across the Atlantic. Monk fruit extract faces similar geographic challenges. While the FDA permits broad use under GRAS status, the EU restricts approval to aqueous extracts, excluding alcohol-extracted mogrosides that provide superior sweetness intensity. This fragmented regulatory environment forces multinational manufacturers to develop region-specific formulations, increasing R&D costs and delaying global product launches. Emerging markets often adopt EU standards when establishing novel food frameworks, extending EFSA's influence beyond its jurisdiction. Consequently, US-approved sweeteners like allulose face disadvantages in regions such as Africa and Southeast Asia. The lack of regulatory harmonization also creates opportunities for smaller brands to navigate fragmented approvals. Companies that secure EFSA's novel food authorization gain a competitive advantage in the 27-member EU market, while US-focused brands benefit from faster commercialization under the FDA's GRAS notification pathway.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Polyols Gain as Pharma Demand Rises

In 2025, high-intensity sweeteners accounted for 60.15% of the market share, highlighting their dominance in zero-calorie beverages and tabletop formats. Meanwhile, sugar polyols are projected to grow at a 5.89% CAGR through 2031, driven by increased use of sorbitol, xylitol, and mannitol by pharmaceutical manufacturers as excipients in chewable tablets, syrups, and lozenges. Among high-intensity sweeteners, stevia leads the sugar substitutes market due to its broad regulatory acceptance and clean-label appeal. Sucralose follows, benefiting from cost advantages in industrial applications despite its taste-profile limitations. Monk fruit is establishing a niche in premium beverages, particularly in Asia, where China's production capacity exceeds 8,000 tonnes of steviol glycosides annually, according to the China National Food Industry Association. Aspartame and acesulfame potassium are losing market share in consumer-facing categories due to concerns over their synthetic perception but remain widely used in pharmaceutical and industrial applications, where cost per sweetness unit outweighs label claims. Neotame and advantame, next-generation aspartame derivatives approved by the FDA, have struggled to gain market traction due to limited supplier diversity and low familiarity among formulators.

Sugar polyols are dividing into commodity and specialty segments within the sugar substitutes market. Sorbitol and maltitol serve cost-sensitive confectionery applications, while erythritol and xylitol command premium pricing in functional foods and oral care products due to their dental health benefits and lower glycemic impact. Erythritol, with its 90% absorption rate and minimal caloric contribution, is the preferred polyol for ketogenic and diabetic-friendly products. However, a cardiovascular study by the Cleveland Clinic has prompted some brands to adopt erythritol-stevia blends as a precautionary measure. Xylitol's proven ability to reduce Streptococcus mutans colonization supports its continued use in sugar-free gum and dental products. Roquette and Danisco (DuPont) dominate the pharmaceutical-grade supply of xylitol. Maltitol's bulking properties and its role in the Maillard reaction make it essential in sugar-free chocolate, despite its potential laxative effects at high doses. The faster growth of the polyol segment reflects its dual functionality—providing both sweetness and texture in applications where high-intensity sweeteners alone cannot replicate the physical properties of sugar.

By Origin: Fermentation Routes Disrupt Plant Extraction

In 2025, plant-derived sweeteners accounted for 55.32% of the market share, supported by stevia cultivated in Paraguay and China, as well as monk fruit from Guangxi province. Meanwhile, biotechnologically fermented variants are expanding at a 6.14% CAGR, driven by precision fermentation's ability to mitigate agricultural risks and deliver improved sustainability metrics. Synthetic sweeteners, such as aspartame, sucralose, and acesulfame potassium, are losing prominence in consumer-facing markets but remain competitive in pharmaceutical excipients and industrial food production due to established regulatory acceptance and high price sensitivity. The shift toward fermentation is accelerating across the sugar substitutes market, with metabolic engineering reducing production costs below those of plant extraction. For instance, EverSweet® fermented stevia received EFSA approval in January 2024, achieving an 81% carbon reduction compared to cane sugar. This sustainability profile aligns with corporate commitments to Scope 3 emissions.

In May 2025, Ingredion announced its decision to phase out its RealSweet joint venture with Amyris while retaining exclusive rights to fermented Reb M. This move highlights a strategic focus on enhancing in-house fermentation capabilities, reducing reliance on external biotech partners, and capturing greater value across the supply chain. However, plant-derived sweeteners in the sugar substitutes market face challenges from climate variability. In Paraguay, stevia yields fluctuate due to inconsistent rainfall, while in China, monk fruit harvests are limited by the scarcity of arable land suitable for cultivating Siraitia grosvenorii. Synthetic sweeteners are regaining traction in specific applications as manufacturers recognize that consumer backlash is primarily directed at retail-facing brands. Conversely, B2B and pharmaceutical buyers prioritize cost efficiency and regulatory reliability over label claims.

By Form: Liquids Gain in Beverage Reformulation

In 2025, powder formats accounted for 68.21% of the market share, showcasing their dominance in tabletop sweeteners, bakery mixes, and dry beverage concentrates. However, liquid sweeteners are growing at a 5.42% CAGR as beverage manufacturers increasingly prefer them for their ease of blending and precise dosing in high-speed production lines. Tate & Lyle's TASTEVA SOL stevia, with solubility 200 times greater than conventional steviol glycosides, addresses a key challenge in clear beverages by preventing haze and sedimentation caused by undissolved particles. Liquid formats also support co-processing with flavors and acids, reducing ingredient additions and shortening cycle times in carbonated soft drink production. On the other hand, powder sweeteners remain advantageous in applications like protein powders, instant coffee, and bakery mixes, where moisture could lead to clumping or microbial growth.

The rapid growth of the liquid segment is driving expansion in the sugar substitutes market as ready-to-drink beverages gain popularity, such as cold brew coffee, functional waters, and energy drinks. Manufacturers in these categories favor liquid sweetener systems that disperse instantly without requiring heating or extended mixing, as outlined in Coca-Cola Company Technical Specifications. While spray-dried and agglomerated powders are improving solubility through particle engineering, liquid formats retain a 20-30% cost advantage in high-volume beverage production due to reduced handling and blending time. In the pharmaceutical sector, powders are still preferred for solid-dose formulations like tablets and capsules, but there is a growing adoption of liquid polyols, such as USP-grade sorbitol solution, for syrups and suspensions where viscosity and sweetness need precise control. The distinction between formats is narrowing as suppliers, such as Ingredion's PureCircle stevia line, now offer both powder and liquid variants to meet diverse production requirements.

By Application: Food Segment Accelerates on Bakery Innovation

In 2025, beverages led the market, representing 42.12% of applications. This growth was primarily driven by the rising demand for zero-sugar carbonated soft drinks, energy drinks, and functional waters. At the same time, the food sector, including bakery, confectionery, and dairy manufacturers, is experiencing significant growth at a 5.58% CAGR. These manufacturers are increasingly adopting advanced sweetener blends to address challenges related to taste and texture. A key innovation in this space is Kerry Group's Tastesense Sweetness platform, launched in February 2026. This platform enables up to a 100% sugar reduction in dairy and bakery products by effectively masking the metallic and bitter off-notes commonly associated with high-intensity sweeteners. This breakthrough has removed previous limitations on zero-sugar baked goods. Allulose is gaining popularity in bakery applications due to its ability to participate in Maillard browning reactions, which produce the desirable golden crust and caramelized flavor notes that stevia and sucralose cannot replicate. In Latin America, dairy reformulation is accelerating, driven by Brazil's front-of-package labeling regulations, which took effect in 2022. These regulations have compelled manufacturers to reduce sugar content by 30% to avoid "excess sugar" warning labels.

Pharmaceutical applications, including chewable tablets, syrups, and lozenges, primarily rely on polyols such as sorbitol, xylitol, and mannitol. These polyols are selected for their compliance with USP and European Pharmacopoeia monograph standards, ensuring both purity and appropriate particle size distribution. Confectionery manufacturers continue to face challenges with taste profiles. While polyols like maltitol and erythritol provide cooling sensations that are acceptable in gum, they are less appealing in chocolate. This limitation has slowed the adoption of sugar-free chocolate, restricting its appeal to diabetic and ketogenic markets. Beyond confectionery, xylitol is gaining traction in other applications. Its proven effectiveness in reducing dental caries has led to its inclusion in products such as toothpaste, mouthwash, and chewing gum. This trend highlights the expanding use of xylitol, particularly in oral care and nutritional supplements. The food segment's 5.58% CAGR growth is supporting expansion of the sugar substitutes market driven by advancements in taste-masking technologies and the increasing prevalence of front-of-package labeling regulations that penalize high-sugar formulations. These regulatory measures complement the growing consumer preference for healthier alternatives.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 45.21% of the sugar substitutes market and is expected to grow at a 6.21% CAGR through 2031, driven by the presence of 241 million diabetes patients in China and India. Chinese companies, which supply over 80% of the global erythritol, hold significant pricing power in the sugar substitutes market over Western buyers. While India's FSSAI has approved stevia and sucralose, it has not yet cleared allulose, forcing multinationals to use split formulations in the region. Japan's cautious approach to new sweeteners is delaying product launches, and Indonesia's upcoming 2025 sugar tax is pushing beverage manufacturers toward zero-sugar products.

North America, a mature yet profitable region within the sugar substitutes market, benefits from faster commercialization through the FDA's GRAS pathways. The FDA's decision to exclude allulose from added-sugar counts gives formulators a nutritional advantage, driving continued category innovation. Canada's front-of-package warning labels, set to take effect in 2026 and modeled after Mexico's system, are expected to trigger significant reformulations in dairy and bakery products. In Europe, EFSA's regulatory stance creates challenges: while it has rejected allulose and only partially approved monk fruit, its approval of EverSweet® signals growing acceptance of fermentation-based solutions.

South America, along with the Middle East and Africa, holds a smaller market share of the sugar substitutes market but is experiencing above-average growth rates. Brazil's 2022 labeling regulations are driving reformulations in dairy and beverage products, and Chile's long-standing sugar tax has resulted in a sustained decline in caloric soda sales. In the Gulf Cooperation Council states, where diabetes prevalence exceeds 15%, the underdeveloped regulatory framework creates opportunities for companies with expertise in global compliance. Many emerging regulators are adopting EU standards, which favor suppliers already meeting EFSA requirements, influencing sourcing strategies across the broader sugar substitutes market.

Competitive Landscape

The sugar substitutes market exhibits low concentration, as multinational ingredient suppliers (Cargill, Tate & Lyle, ADM, Ingredion, DSM-Firmenich) compete against Chinese polyol exporters and biotech disruptors commercializing fermentation-derived sweeteners. Cargill and DSM-Firmenich's Avansya joint venture, which secured EFSA approval for EverSweet fermented stevia in January 2024, exemplifies the shift toward vertical integration and sustainability-driven differentiation, with the product delivering 81% lower carbon emissions than cane sugar. Ingredion's expansion of PureCircle ownership to 98% in 2024 and its retention of exclusive rights to fermented Reb M after winding down the RealSweet joint venture in May 2025 signal a strategic pivot toward in-house fermentation capabilities, reducing reliance on external biotech partners and capturing margin across the value chain.

White-space opportunities are emerging across the sugar substitutes market in pharmaceutical excipients, where polyols meeting USP monograph specifications command 30-40% premiums over food-grade variants, and in precision fermentation, where CRISPR-optimized yeast strains are achieving erythritol titers of 245 grams per liter, economics that threaten traditional plant-extraction supply chains. Smaller biotech firms are unsettling incumbents by commercializing novel sweeteners through fermentation routes that bypass agricultural supply volatility; companies like Bonumose are developing allulose production platforms that could undercut plant-derived pricing if scaled to commercial volumes. Chinese erythritol producers, controlling 80% of global production, are leveraging cost advantages from vertically integrated corn-to-polyol supply chains to pressure European and North American suppliers, forcing consolidation and capacity rationalization in mature markets.

Technology leadership in the sugar substitutes market is shifting from extraction efficiency to metabolic engineering, with patent filings for CRISPR-edited microbial strains and enzymatic conversion routes accelerating in the US and Europe, a dynamic that favors R&D-intensive suppliers over commodity producers. Regulatory arbitrage is creating competitive moats in the sugar substitutes industry, as suppliers with both FDA GRAS and EFSA novel food approvals can serve global markets with unified formulations, while single-jurisdiction approvals fragment product portfolios and inflate compliance costs.

Sugar Substitutes Industry Leaders

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

International Flavors & Fragrances Inc.

-

Ingredion Incorporated

-

Tate & Lyle Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Tate & Lyle partnered with BioHarvest to develop botanical-synthesis sweeteners that match sugar’s taste without residual off-notes. This partnership will focus on creating new plant-derived molecules, initially within the sweetener platform, with the potential to expand into other areas.

- October 2024: Tate & Lyle and Manus Bio formed a strategic partnership and introduced stevia Reb M, marking the first large-scale commercialization of an Americas-sourced and manufactured bioconverted stevia Reb M ingredient. This partnership aims to provide customers with a reliable, high-quality source of Reb M while also expanding access to natural sugar reduction solutions.

- July 2024: Sweegen introduced its Tastecode taste optimization tools at the IFT FIRST event in Chicago. The company showcased its reduced-sugar natural flavor technologies to address taste challenges in healthier food products.

- May 2024: Ingredion's PureCircle introduced a stevia sweetener that directly replaces sugar in formulations. The natural sweetener functions similarly to sugar without requiring additional ingredients and is suitable for beverages, syrups, and sauces.

Global Sugar Substitutes Market Report Scope

Sugar substitutes are chemical or plant-based substances used to sweeten or enhance the flavor of food products and beverages.

The sugar substitute market is segmented by type, origin, form, application, and geography. By type, the market is segmented into high-intensity sweeteners (acesulfame potassium, advantame, aspartame, neotame, saccharin, sucralose, stevia, monk fruit and others) and sugar polyols (sorbitol, xylitol, maltitol, erythritol and others). By origin, the market is segmented into plant-derived, synthetic and biotechnologically fermented. By form, into powder and liquid. By application, the market is segmented into food, beverage, pharmaceuticals and others. The food segment is further segmented into bakery and cereals, confectionery, dairy and dairy alternatives, sauces, condiments, and dressings, and other food applications. The beverage segment is further segmented into carbonated soft drinks, RTD tea and coffee, sports and energy drinks and other beverages. The report further analyses the market's global scenario, including a detailed analysis of North America, Europe, Asia-Pacific, South America, and the Middle East and Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Type

| High-Intensity Sweeteners | Acesulfame Potassium |

| Advantame | |

| Aspartame | |

| Neotame | |

| Saccharin | |

| Sucralose | |

| Stevia | |

| Monk Fruit | |

| Other High-Intensity Sweeteners | |

| Sugar Polyols | Sorbitol |

| Xylitol | |

| Maltitol | |

| Erythritol | |

| Other Sugar Polyols |

By Origin

| Plant-Derived |

| Synthetic |

| Biotechnologically Fermented |

By Form

| Powder |

| Liquid |

By Application

| Food | Bakery and Cereals |

| Confectionery | |

| Dairy and Dairy Alternatives | |

| Sauces, Condiments, and Dressings | |

| Other Food Applications | |

| Beverage | Carbonated Soft Drinks |

| RTD Tea and Coffee | |

| Sports and Energy Drinks | |

| Other Beverages | |

| Pharmaceuticals | |

| Other Applications |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Type | High-Intensity Sweeteners | Acesulfame Potassium |

| Advantame | ||

| Aspartame | ||

| Neotame | ||

| Saccharin | ||

| Sucralose | ||

| Stevia | ||

| Monk Fruit | ||

| Other High-Intensity Sweeteners | ||

| Sugar Polyols | Sorbitol | |

| Xylitol | ||

| Maltitol | ||

| Erythritol | ||

| Other Sugar Polyols | ||

| By Origin | Plant-Derived | |

| Synthetic | ||

| Biotechnologically Fermented | ||

| By Form | Powder | |

| Liquid | ||

| By Application | Food | Bakery and Cereals |

| Confectionery | ||

| Dairy and Dairy Alternatives | ||

| Sauces, Condiments, and Dressings | ||

| Other Food Applications | ||

| Beverage | Carbonated Soft Drinks | |

| RTD Tea and Coffee | ||

| Sports and Energy Drinks | ||

| Other Beverages | ||

| Pharmaceuticals | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the sugar substitutes market today and how fast is it growing?

The sugar substitutes market size reached USD 9.18 billion in 2026 and is projected to hit USD 11.42 billion by 2031, advancing at a 4.68% CAGR.

Which product type is expanding fastest?

Sugar polyols are forecast to grow at 5.89% CAGR through 2031, driven by their dual role as sweeteners and bulking agents in pharma and confectionery.

Why is Asia-Pacific the leading demand center?

The region’s 241 million diabetes patients and tightening sugar-tax regimes are spurring rapid adoption of low-calorie alternatives, giving Asia-Pacific 45.21% market share in 2025.

How are precision-fermented sweeteners changing the landscape?

Fermentation delivers 81% lower carbon footprints and sidesteps crop volatility, enabling biotech-derived stevia and allulose to grow at 6.14% CAGR.

Page last updated on: