Collagen Drinks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

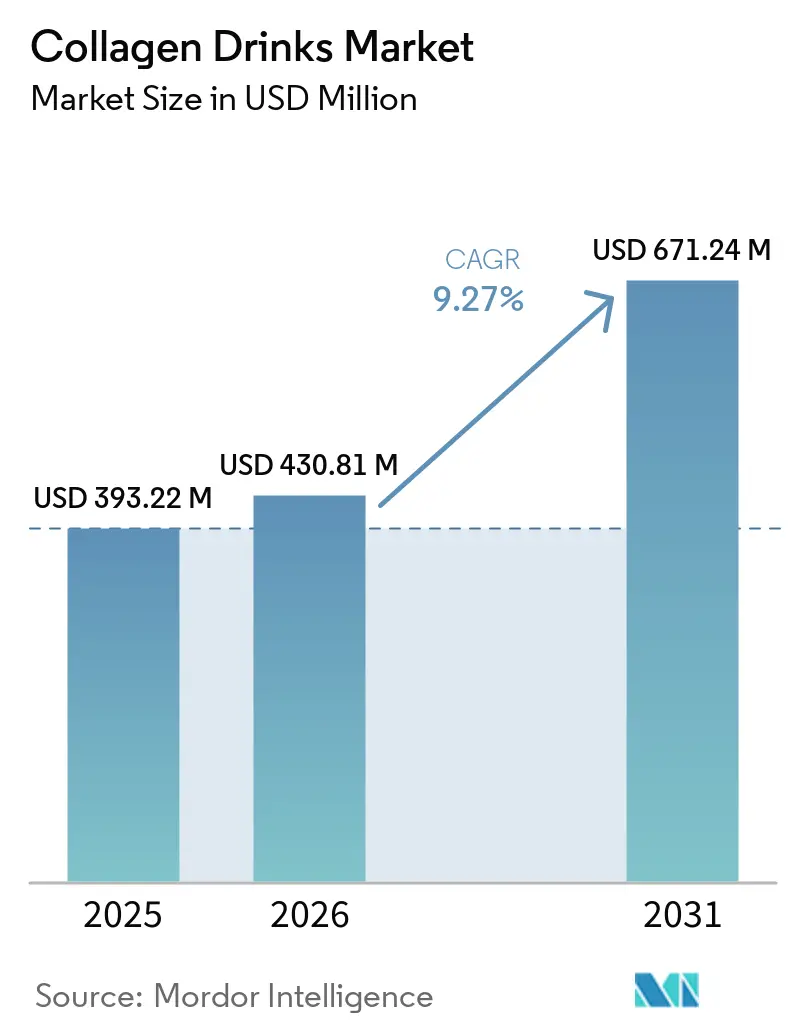

| Market Size (2026) | USD 430.81 Million |

| Market Size (2031) | USD 671.24 Million |

| Growth Rate (2026 - 2031) | 9.27% CAGR |

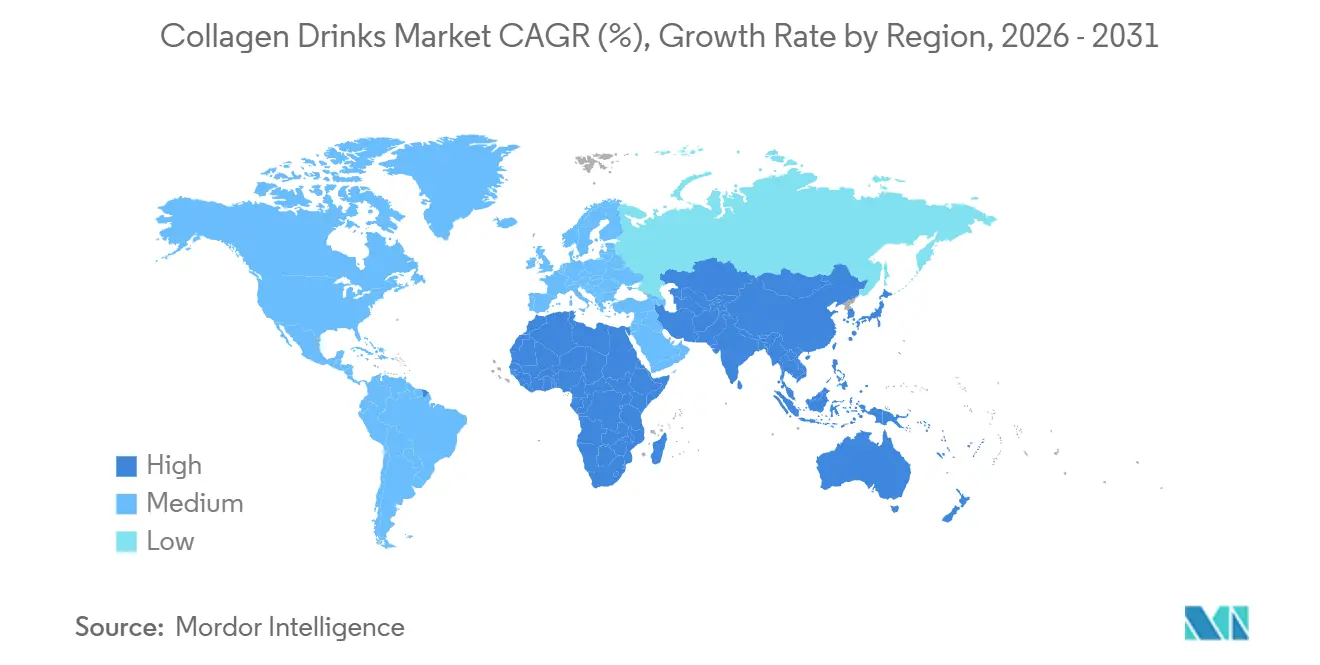

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Collagen Drinks Market Analysis by Mordor Intelligence

The Collagen Drinks Market size is expected to grow from USD 393.22 million in 2025 to USD 430.81 million in 2026 and is forecast to reach USD 671.24 million by 2031 at 9.27% CAGR over 2026-2031. Robust demand for beauty-from-within solutions, along with U.S. regulatory approval of hydrolyzed collagen as Generally Recognized as Safe for food and beverage use, and capacity expansions in the Asia-Pacific region, are driving this trend. After EFSA's March 2026 rejection of all oral-collagen health claims, manufacturers are reformulating products by incorporating vitamin C and other cofactors approved by the European Food Safety Authority. Growth prospects are further supported by marine-source premiumization, innovative formats like carbonated cans with a 12-month ambient shelf life, and vertical integration efforts by Thai Union and Nitta Gelatin. However, stricter quality-control measures, mandatory halal certification in Indonesia, and increasing competition from powders, gummies, and capsules are limiting near-term growth potential.

Key Report Takeaways

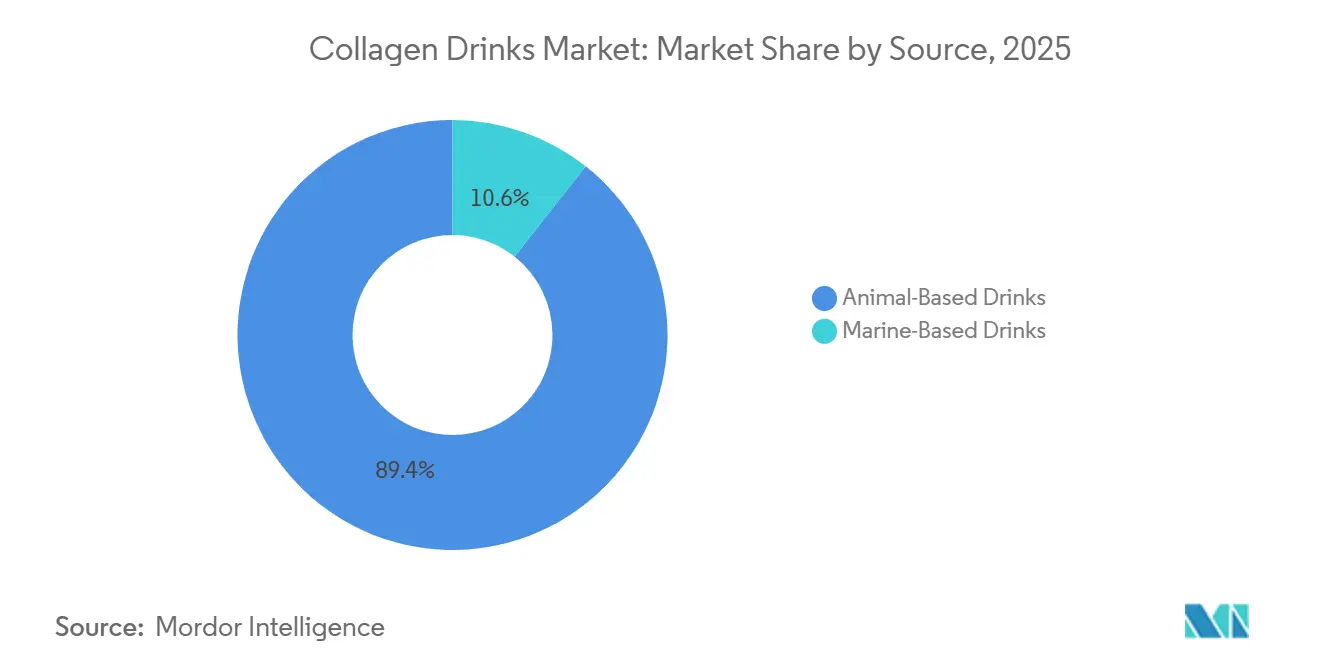

- By source, animal-based drinks led with 89.4% revenue share in 2025, while marine-based variants are projected to expand at a 10.4% CAGR through 2031.

- By packaging type, PET and glass bottles held 37.9% of Collagen Drink market share in 2025; pouches and sachets are forecast to grow at a 10.1% CAGR through 2031.

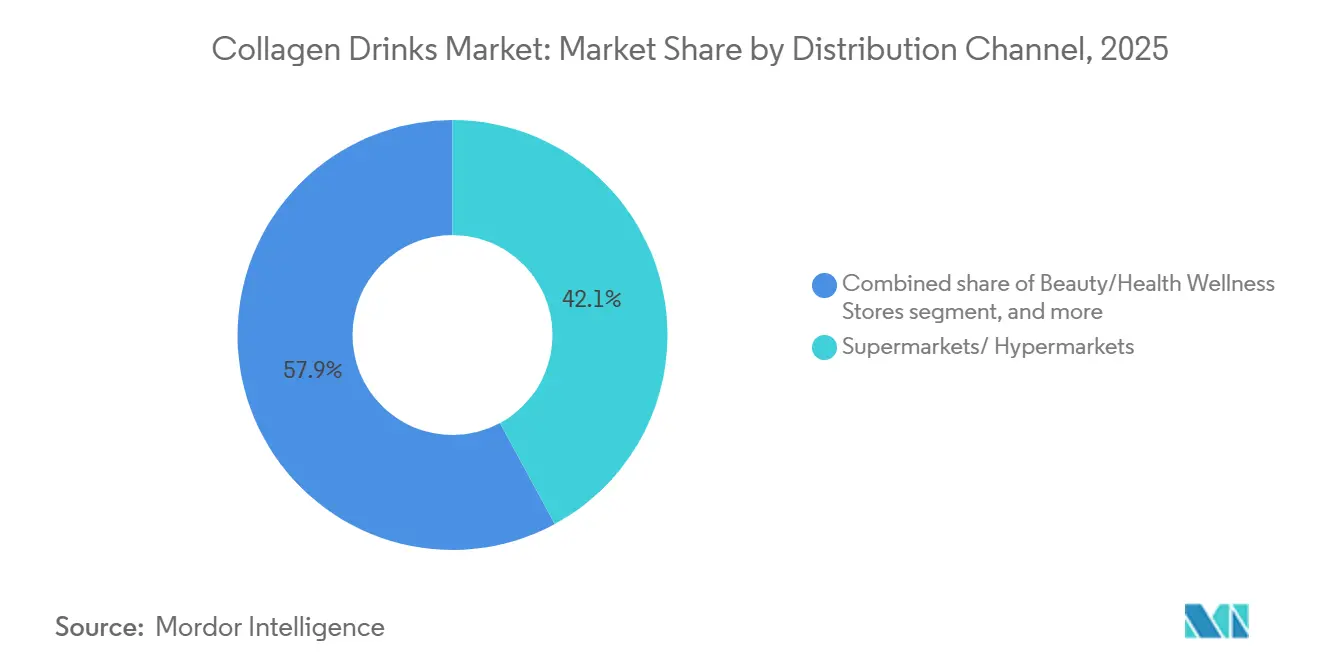

- By distribution channel, supermarkets and hypermarkets accounted for 42.1% of the Collagen Drink market size in 2025, whereas online retail stores are advancing at a 10.5% CAGR over 2026-2031.

- By geography, North America captured 37.0% revenue share in 2025, but Asia-Pacific is anticipated to register a 10.3% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Collagen Drinks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer focus on holistic well-being and preventive health fuels demand | +1.8% | Global, with concentration in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Influence of social media and celebrity endorsements | +1.2% | Global, particularly strong in Asia-Pacific (China, South Korea, Japan) and North America | Short term (≤ 2 years) |

| Product innovation and formulation advancements | +1.5% | Global, led by Japan, South Korea, and North America | Medium term (2-4 years) |

| Growth in the functional and fortified beverage category | +1.3% | Global, with rapid adoption in Asia-Pacific and North America | Medium term (2-4 years) |

| Increasing consumer demand for clean-label and natural ingredients | +1.1% | North America, Western Europe, Australia | Long term (≥ 4 years) |

| Growing demand for plant-based and vegan options | +0.9% | North America, Western Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer focus on holistic well-being and preventive health fuels demand

Preventive health spending has transitioned from occasional supplementation to daily routines, with collagen drinks becoming essential for beauty-conscious consumers. Regular intake of oral collagen peptides has been proven to improve skin hydration and elasticity within weeks, making them particularly appealing to aging populations. This shift is driven by the increasing number of older adults. For example, in 2024, individuals aged 65 and above accounted for 10% of the global population, according to the United Nations (UN)[1]Source: United Nations (UN), "Population ages 65 and above", worldbank.org. Additionally, the U.S. FDA's GRAS approvals for hydrolyzed pork cartilage collagen (GRN 713) and E. coli-derived collagen polypeptides (GRN 1171) have expanded formulation options. This enables brands to enhance ready-to-drink beverages without classifying them under dietary-supplement regulations. The primary consumers of premium collagen drinks prioritize ingredient transparency and clinical validation over cost. Significantly, this group is willing to pay a 30-50% premium for collagen derived from marine or fermentation sources, creating substantial opportunities for innovation and profit margins.

Influence of social media and celebrity endorsements

Digital discovery channels have accelerated the transition from awareness to purchase. Influencer partnerships effectively drive trials among Gen Z and millennials, who collectively contribute over 41% of wellness spending. In February 2025, HEYTEA partnered with Vida Glow to introduce collagen shots into bubble-tea menus at 3,000 outlets across China. This initiative demonstrates how cross-category collaborations can expand reach beyond traditional supplement aisles. In 2024, Thailand's FDA targeted e-commerce supplement listings, identifying over 80% for noncompliant advertising. This action highlights a significant enforcement gap between digital and physical retail, creating compliance challenges for brands heavily reliant on influencer marketing. The growing preference for short-form video content on platforms like TikTok and Instagram Reels emphasizes visually demonstrable benefits, such as skin glow and hair thickness, over claims related to joint or bone health, which require longer validation periods. This shift is driving product development toward marine collagen's Type I composition, valued for its visible skin benefits, rather than bovine collagen's Type I and Type III blend, which supports structural health. South Korea's stricter labeling requirements, effective January 1, 2026, for products containing guarana and sugar alcohols, aim to reduce misleading wellness claims. However, these regulations may inadvertently benefit established brands with regulatory teams over digitally native startups.

Product innovation and formulation advancements

Advancements in formulation prioritize improving bioavailability and refining sensory attributes. Marine collagen, characterized by its smaller peptide size of 2,000-5,000 daltons, achieves peak plasma concentration within 1-2 hours, approximately 1.5 times faster than bovine collagen. This rapid absorption positions marine collagen as a premium offering. In April 2024, Shiseido introduced its INRYU ampoule drinks, designed for the Japanese market. These drinks, containing low-molecular-weight collagen peptides and hyaluronic acid, align with the local demand for single-serve, refrigerated formats. Meiji's Amino Collagen NMN, launched in September 2025, combines collagen peptides with nicotinamide mononucleotide to target cellular aging, highlighting the convergence of nutricosmetics and longevity science. VeCollal's plant-based peptides, produced through fermentation, provide a vegan collagen alternative. While addressing ethical and religious concerns, their cost, 2-3 times higher than bovine or marine collagen, remains a limiting factor. Innovative methods like high-pressure processing and aseptic filling extend shelf life to 12 months without refrigeration, enabling distribution through supermarkets and convenience stores. Additionally, retort processing is suitable for packaging carbonated collagen drinks in aluminum cans.

Growth in functional and fortified beverage category

Functional beverages have shifted from niche wellness products to mainstream retail offerings. Collagen drinks have capitalized on this trend, joining the ranks of kombucha, cold-brew coffee, and protein shakes. The U.S. FDA's GRAS notices for collagen peptides allow brands to enhance juice, tea, and coffee beverages with collagen without being subject to dietary-supplement regulations. This regulatory clarity has facilitated wider distribution in grocery and convenience stores. Reflecting the industry's growth, Thai Union committed USD 30 million in June 2025 to establish a marine-collagen facility. This facility, which produces ThalaCol peptides from fish-processing byproducts, demonstrates a focus on vertical integration, enabling companies to capture greater margins across the value chain. Additionally, Darling Ingredients and Tessenderlo Group announced a joint venture, Nextida, in May 2025. With an anticipated annual revenue of USD 1.5 billion, Nextida aims to consolidate collagen peptide production for food, beverage, and pharmaceutical applications. Aluminum cans, offering complete protection against oxygen and light, are helping carbonated collagen drinks compete effectively with energy drinks and sparkling waters in terms of shelf presence and portability. As the functional beverage market grows, collagen drinks face increasing competition. They now contend with protein shakes, adaptogen lattes, and electrolyte waters, compelling brands to emphasize distinct benefits that go beyond generic wellness claims.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Source traceability and quality-control gaps | -0.8% | Global, particularly acute in Asia-Pacific and South America | Short term (≤ 2 years) |

| Competition from alternative nutricosmetic formats | -0.7% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Emerging EU scrutiny on peptide health-claims | -0.6% | Europe, with spillover to markets aligned with EFSA standards | Short term (≤ 2 years) |

| Sensory instability from chitosan clarifiers | -0.4% | Global, affecting premium and clean-label segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Source traceability and quality-control gaps

Brands are exposed to contamination risks and regulatory penalties due to supply-chain opacity. A 2024 study in the Journal of Food Science found that 30% of collagen supplements tested contained undeclared species or synthetic additives. Notably, some samples exceeded FDA and EFSA thresholds for heavy-metal concentrations. Although ISO 22000 food safety management and HACCP certification establish baseline controls, enforcement varies widely across regions. China's General Administration of Customs Decree No. 280, effective June 1, 2026, strengthens import protocols for collagen products by requiring full ingredient disclosure and third-party contaminant testing. This regulation delays market entry and increases compliance costs. Marine collagen, sourced from fish-processing byproducts, shows variability in peptide composition and bioavailability based on species, tissue type, and extraction method. Brands relying on suppliers from Southeast Asia and South America face increased scrutiny due to inconsistent quality-management practices and inadequate traceability infrastructure. In July 2025, Nitta Gelatin expanded its annual capacity by 550 metric tons in Kerala, India, integrating blockchain-based traceability systems. This initiative highlights the industry's recognition of these challenges.

Competition from alternative nutricosmetic formats

Gummies, powders, and capsules offer unmatched convenience and dosing precision compared to liquid formats. Gummies are particularly appealing to younger consumers who avoid traditional supplement routines. Powders allow for customization, enabling consumers to mix collagen into coffee, smoothies, or oatmeal, seamlessly incorporating supplementation into their daily habits. Capsules excel in portability and shelf stability, eliminating the need for refrigeration, an advantage that collagen drinks trade off for bioavailability claims. The U.S. FDA's GRAS determinations for collagen peptides have enabled powder and capsule manufacturers to fortify food products, blurring category lines and intensifying competition. Pricing trends also favor alternative formats: collagen powders, priced at USD 30-50 per container, provide 30-60 servings. In contrast, ready-to-drink formats, costing USD 3-5 per serving, may discourage repeat purchases among price-sensitive consumers. To justify the price difference, brands must highlight the bioavailability advantage of liquid formats, marine collagen's peptides, with a size range of 2,000-5,000 daltons, achieve peak plasma concentration within 1-2 hours, outperforming powder and capsule forms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Marine-Based Premiumization Versus Bovine Scale

Marine-based drinks are projected to grow at a CAGR of 10.36% from 2026 to 2031, surpassing the animal-based segment, which is expected to hold an 89.36% share in 2025. This growth is driven by superior bioavailability and sustainability narratives. Marine collagen, with its smaller peptide size of 2,000-5,000 daltons, reaches peak plasma concentration within 1-2 hours, approximately 1.5 times faster than bovine collagen. This enables brands to position marine variants as premium efficacy products. In June 2025, Thai Union announced a USD 30 million investment in a marine-collagen facility. This facility, which produces ThalaCol peptides from fish-processing byproducts, highlights the company's vertical integration strategy. This approach not only captures margins across the value chain but also reduces reliance on third-party suppliers. The sustainability strategy leverages fish-processing byproducts, such as skin, scales, and bones, that account for 25-70% of the total catch weight. This reduces waste and lowers the carbon footprint compared to bovine sources, which require dedicated livestock. However, marine collagen's premium pricing, 30-50% higher than bovine alternatives, limits its adoption among price-sensitive consumers, restricting growth to affluent urban markets in North America, Western Europe, and the Asia-Pacific region.

Animal-based drinks maintain their dominance due to cost efficiency and multi-benefit positioning. Bovine collagen, which combines Type I and Type III variants, supports skin, joint, and muscle health. This expands its appeal to include not only beauty-conscious consumers but also those in the active-aging and sports-nutrition segments. Established supply chains and regulatory approvals, such as the U.S. FDA's GRAS determination for hydrolyzed pork cartilage collagen (GRN 713), enable rapid formulation adjustments and market entry for bovine collagen. However, ethical and religious factors constrain its addressable market. Hindu consumers avoid bovine products, Muslim consumers require halal certification, and vegan consumers reject all animal-derived ingredients. While porcine collagen complies with halal standards, it faces acceptance challenges in regions with significant Muslim populations, leading to fragmentation within the animal-based segment.

By Packaging Type: Ambient Shelf Life Drives Can Adoption

Aluminum cans offer complete protection against oxygen and light, ensuring a 12-month shelf life at ambient temperatures. This capability enables wider distribution in supermarkets, convenience stores, and vending machines without requiring a cold chain. Pouches and sachets are projected to grow at a 10.06% CAGR from 2026 to 2031, driven by their single-serve convenience, lower material costs, and reduced carbon footprint compared to glass bottles. In 2025, PET and glass bottles accounted for 37.94% of the packaging market. Premium brands prefer these formats for their transparency and perceived quality. However, the weight and fragility of glass increase logistics costs by 20-30% compared to aluminum or PET. PET bottles, compatible with high-pressure processing, are ideal for premium wellness shots. These products are distributed through direct-to-consumer and specialty channels, supported by refrigeration infrastructure that maintains their fresh positioning and short shelf life. Retort processing allows aluminum cans to hold carbonated collagen drinks, aligning them with energy drinks and sparkling waters in terms of shelf presence and portability.

Pouches and sachets attract travel-focused consumers and those in emerging markets where refrigeration infrastructure is limited. Single-serve formats eliminate dosing ambiguity and encourage trials without requiring consumers to commit to multi-serving bottles, lowering the entry barrier for new users. However, the multi-layer laminate construction of pouches complicates recycling, challenging their sustainability claims among clean-label and eco-conscious consumers. Aluminum cans, with their infinite recyclability, over 70% of all aluminum ever produced remains in use today, are positioned as the most sustainable packaging option. However, their opacity conceals the product's appearance, requiring brands to rely on packaging graphics instead of visual cues to convey quality. Glass bottles, while positioned as a premium option, limit distribution to specialty retailers and direct-to-consumer channels where consumers are more accepting of refrigeration requirements and higher per-serving costs. Ultimately, the choice of packaging format reflects the brand's distribution strategy: mass-market brands prefer aluminum cans for their ambient shelf life and cost efficiency, while premium brands choose glass or PET to emphasize quality and justify higher price points.

By Distribution Channel: Digital Discovery Reshapes Retail Mix

Online retail stores are projected to grow at a 10.51% CAGR from 2026 to 2031, exceeding the 42.11% market share held by supermarkets and hypermarkets in 2025. This growth is driven by direct-to-consumer models that effectively capture consumer data and enhance subscription revenues. Moreover, increasing internet access is bolstering online retail platforms. For instance, the International Telecommunication Union (ITU) reported that global internet access rose to 74% in 2025, up from 71% in 2024[2]Source: International Telecommunication Union (ITU), "Individuals Using Internet", itu.int. Beauty and health wellness stores, while providing experiential environments where staff educate consumers on collagen benefits and recommend complementary products, face challenges in geographic reach compared to supermarkets and e-commerce platforms. Other channels, such as pharmacies, convenience stores, and vending machines, cater to impulse purchases and on-the-go consumption but lack the product variety needed for strong brand building.

Supermarkets and hypermarkets maintain their dominance through widespread availability and the ability to encourage larger purchases. However, their heavy reliance on promotions compresses profit margins, leading to the commoditization of collagen drinks, grouping them with protein shakes and other functional beverages. In 2024, Thailand's FDA crackdown on e-commerce supplement listings flagged over 80% of products for noncompliant advertising, highlighting a significant enforcement gap between digital and physical retail. This gap creates compliance risks for brands that depend heavily on influencer marketing and direct-to-consumer sales. Beauty and health wellness stores, such as Sephora's expansion into ingestible beauty, gain credibility through curated offerings and staff expertise. However, their premium positioning limits their target audience to affluent urban consumers. The shifting distribution landscape reflects consumer segmentation: mass-market brands focus on supermarkets and online platforms for broader reach, while premium brands prioritize direct-to-consumer channels and specialty retail to control their brand narrative and maximize margins.

Geography Analysis

In 2025, North America accounted for 37.03% of the revenue, driven by the United States' advanced wellness infrastructure and consumers' willingness to pay a premium for clinically validated products. The U.S. FDA's GRAS approvals for hydrolyzed pork cartilage collagen (GRN 713) and E. coli-derived collagen polypeptides (GRN 1171) expanded formulation options, allowing brands to enhance ready-to-drink beverages without falling under dietary-supplement regulations. In Canada, the Natural and Non-prescription Health Products Directorate requires product licensing for collagen drinks with health claims, creating a regulatory advantage for established brands with regulatory teams over newer, digitally native startups. Mexico's expanding middle class and growing health awareness offer growth opportunities, but challenges such as distribution infrastructure and cold-chain limitations hinder expansion beyond urban areas.

Asia-Pacific, led by China's strong market, is expected to grow at a CAGR of 10.27% from 2026 to 2031. This growth is fueled by increasing disposable incomes, a beauty-conscious population, and innovative developments by regional leaders. According to China's National Bureau of Statistics, the average annual per capita disposable income for households rose from 39,218 yuan in 2023 to approximately 41,300 yuan in 2024, indicating rising demand[3]National Bureau of Statistics of China, "Average annual per capita disposable income of households in China from 1990 to 2024", www.stats.gov.cn.. China's General Administration of Customs, through Decree No. 280, has tightened import requirements for collagen products, mandating full ingredient disclosure and third-party contaminant testing. While these regulations, effective June 1, 2026, may delay market entry and increase compliance costs, they enhance product safety. Starting September 1, 2026, Japan's Consumer Affairs Agency will require mandatory Foods with Function Claims labeling, which obligates brands to provide clinical evidence and safety data. This regulation creates a clear pathway for brands to differentiate functional foods from generic supplements. In Australia, the expiration of Therapeutic Goods Order 92 on October 1, 2026, reclassifies oral collagen drinks with cosmetic claims as therapeutic goods. This change requires listing on the Australian Register of Therapeutic Goods, increasing compliance costs but reinforcing the product's safety appeal to consumers. Indonesia's mandatory halal certification, effective October 17, 2026, adds compliance requirements, favoring marine or fermentation-derived collagen sources over bovine options.

Europe is experiencing regulatory shifts. The European Food Safety Authority's rejection of all oral-collagen health claims on March 30, 2026, has removed the option for efficacy messaging across the EU's 27 member states. This forces brands to reformulate or pivot to structure-function messaging. While the United Kingdom's post-Brexit alignment with EFSA standards ensures consistency for brands operating across Europe, potential divergence may arise as the UK Food Standards Agency develops its independent framework. Germany, France, and Italy lead Europe's market, with consumers favoring clean-label and natural ingredients. However, as disposable incomes grow and wellness awareness increases, Spain and Eastern European markets present new growth opportunities. South America and the Middle East and Africa remain emerging markets. Brazil's beauty-conscious consumers and the affluent expatriate population in the United Arab Emirates offer early-mover opportunities, but challenges such as distribution infrastructure, regulatory frameworks, and consumer education needs limit immediate market penetration.

Competitive Landscape

The global collagen drinks market is characterized by fragmentation, with numerous global, regional, and niche players competing across various formulations and price ranges. Leading companies in the market include Shiseido Company, Limited, Meiji Holdings Co., Ltd., Nestlé S.A. (operating through its Vital Proteins brand), Kino Biotech Co., Ltd. (recognized for Kinohimitsu), and Kirin Holdings Company, Limited (associated with Fancl Corporation). The absence of a dominant market leader compels manufacturers to emphasize product innovation. These innovations range from collagen blends designed for beauty enhancement to formulations aimed at improving physical performance. This fragmentation fosters competitive pricing, a broad product portfolio, and frequent launches targeting specific consumer groups or emerging wellness trends.

Competition in the market focuses on three critical areas: building scientific credibility through clinical research, maintaining quality through strong supply chain management, and expanding distribution networks to reach diverse consumer segments. Companies are increasingly adopting advanced technologies to differentiate themselves, introducing innovations such as improved peptide processing techniques and delivery systems that enhance bioavailability and improve the overall consumer experience.

Significant growth opportunities lie in plant-based collagen alternatives, personalized nutrition solutions, and therapeutic applications addressing specific health conditions beyond general wellness. Emerging disruptors in the market include biotechnology companies developing fermentation-based collagen substitutes and startups leveraging digital platforms to offer subscription-based models. These models not only enhance customer retention but also provide continuous health monitoring, adding value to the consumer experience.

Collagen Drinks Industry Leaders

-

Shiseido Company, Limited

-

Meiji Holdings Co., Ltd.

-

Nestlé S.A. (Vital Proteins)

-

Kino Biotech Co., Ltd (Kinohimitsu)

-

Kirin Holdings Company, Limited (Fancl Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Naturecan, a wellness brand based in the UK, has launched its high-quality collagen drink at Natural Lawson stores across Japan. Celebrating its 5th anniversary in the Japanese market, this popular product, previously available mainly through online channels, is now easily accessible at health-conscious "Konbini" (convenience stores) in Japan's urban areas.

- April 2026: Kylie Jenner's Sprinter has introduced k2o, a product designed to support hydration, recovery, and skin health. Offered in three appealing flavors – Strawberry Lychee, Peach, and Watermelon Lime – k2o focuses on improving skin moisture and hydration from within.

- February 2025: Revive Collagen, the British liquid collagen brand, has launched its award-winning product range across more than 100 Supercare stores and online channels in the United Arab Emirates, marking a significant milestone in its international expansion.

- January 2025: GNC has launched its Premier Collagen line, offering marine and bovine collagen supplements enhanced with vitamin C and other beauty-boosting ingredients, designed to support skin hydration, firmness, and radiance. According to the brand, the new products are available as both quick-absorbing powders and ready-to-drink shots.

Global Collagen Drinks Market Report Scope

A collagen drink is an oral, hydrolyzed collagen supplement often derived from fish, bovine, or chicken sources, designed to be ingested for improved skin elasticity, hydration, and joint health. The collagen drink market report is segmented by source, packaging type, distribution channels, and geography. By source, the market is segmented into animal-based drinks and marine-based drinks. By packaging type, the market is segmented into PET/glass bottles, cans, and pouches/sachets. By distribution channel, the market is segmented into supermarkets/hypermarkets, online retail stores, beauty/health wellness stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, the market forecasts are provided in terms of value (USD) and volume (liters).

| Animal-Based Drinks |

| Marine-Based Drinks |

| PET/ Glass Bottle |

| Cans |

| Pouches/Sachets |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Beauty/Health Wellness Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Source | Animal-Based Drinks | |

| Marine-Based Drinks | ||

| By Packaging Type | PET/ Glass Bottle | |

| Cans | ||

| Pouches/Sachets | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Online Retail Stores | ||

| Beauty/Health Wellness Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the collagen drink category today and what is the projected value by 2031?

Global sales were roughly USD 430.81 million in 2026 and are forecast to reach about USD 671.24 billion by 2031, reflecting a 9.3% CAGR over 2026-2031.

Why are marine-sourced formulations gaining share over bovine options?

Marine peptides are smaller (≈2,000-5,000 Da) and reach peak plasma levels within two hours, about 1.5 times faster than bovine forms, supporting visible skin-benefit positioning.

What is the main regulatory hurdle in Europe after 2026?

The European Food Safety Authority rejected all oral-collagen health claims in March 2026, forcing brands to rely on structure-function language or vitamin C co-formulation.

How are brands addressing traceability concerns?

Leading suppliers now embed blockchain systems and third-party heavy-metal testing (Clean Label Project standards) to assure species authenticity and contaminant safety.

Page last updated on: