Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year Market Size (2025) | USD 14.38 Billion |

| Market Size (2026) | USD 14.96 Billion |

| Market Size (2031) | USD 18.25 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

| Largest Market | United States |

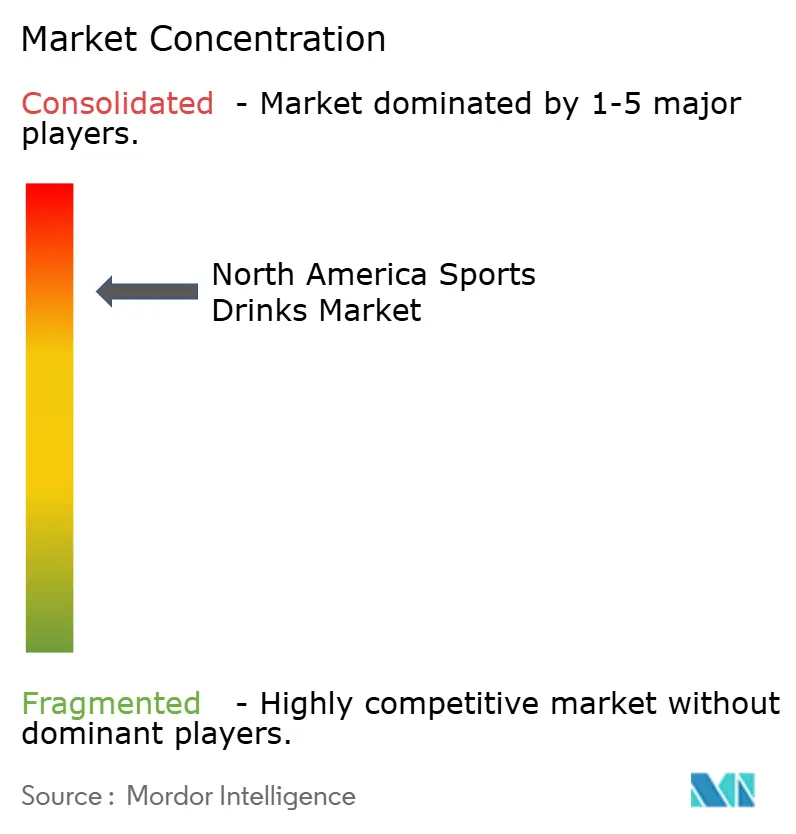

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Sports Drinks Market Analysis by Mordor Intelligence

The North America sports drinks market size in 2026 is estimated at USD 14.96 billion, growing from 2025 value of USD 14.38 billion with 2031 projections showing USD 18.25 billion, growing at 4.05% CAGR over 2026-2031. In North America, the surge in sports participation from athletics and bodybuilding to weightlifting and cycling fuels the demand for sports drinks. As the athleisure trend gains traction, athletes are increasingly seeking tailored sports drinks to meet their hydration, nutrition, and electrolyte needs. These beverages help athletes stay hydrated and replenish essential nutrients, such as carbohydrates and electrolytes, which are crucial for maintaining optimal performance and promoting recovery. With the rise in athletic participation, the demand for these replenishing beverages has correspondingly intensified. Manufacturers, keenly aware of this growing interest, are adopting strategies like partnerships, product innovations, and expansions to capture a larger market share. For instance, companies are collaborating with sports teams and fitness influencers to enhance brand visibility and credibility. Furthermore, as consumers shift towards low-calorie, low-sugar, and functional beverages, market players are responding with innovative, alternative low-sugar products, thereby further propelling the growth of the sports drink market.

Key Report Takeaways

- By soft drink type, isotonic products led with 52.40% revenue share in 2025; hypertonic variants are projected to climb at a 6.65% CAGR through 2031.

- By packaging type, PET bottles held a 95.40% share of the North American sports drinks market size in 2025, while aseptic formats are expected to advance at a 5.70% CAGR through 2031.

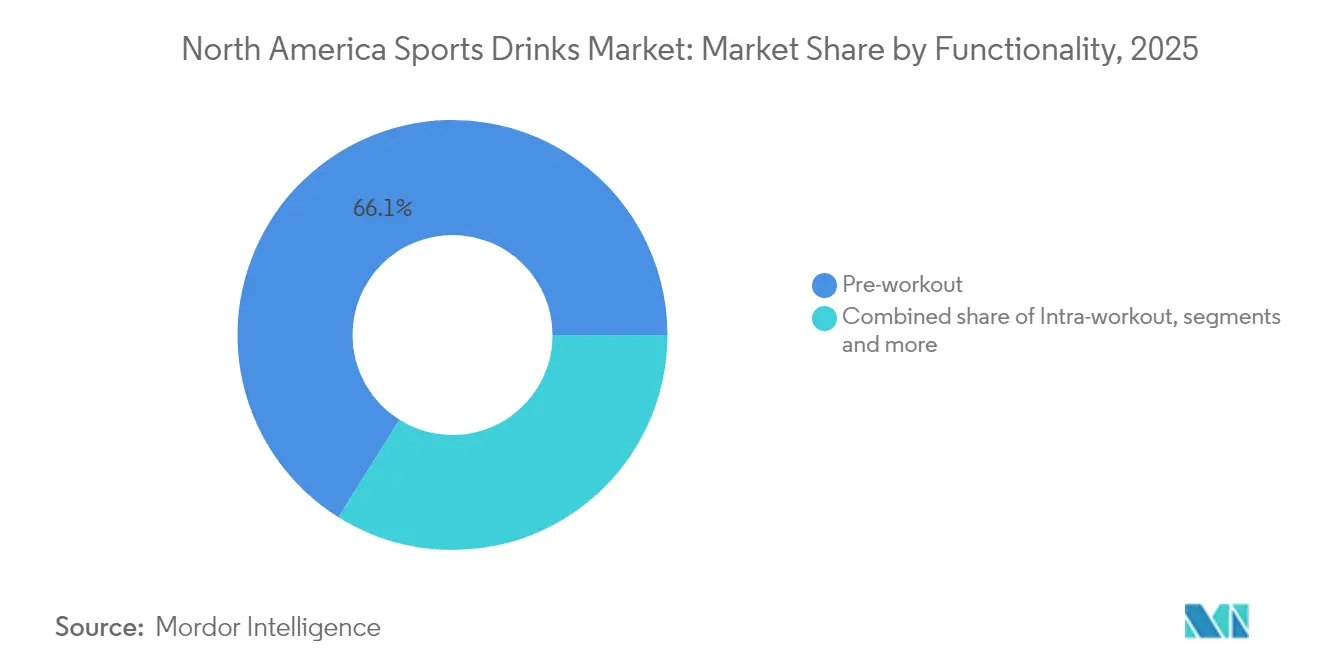

- By functionality, pre-workout drinks accounted for a 66.10% revenue share in 2025; post-workout products are expected to expand at an 7.55% CAGR through 2031.

- By distribution channel, supermarkets maintained a 55.30% share in 2025, while online retail is set to grow at a 8.35% CAGR, reflecting shifts in direct-to-consumer preferences.

- By geography, the United States commanded 87.60% of North America's sports drinks market share in 2025; Canada is forecast to rise at a 5.70% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Sports Drinks Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid fitness and gym-membership growth | +1.0% | United States and Canada core, spillover to Mexico | Medium term (2-4 years) |

| Intensifying heat-wave frequency elevating hydration demand | +0.8% | Global North America, concentrated in southwestern United States | Short term (≤ 2 years) |

| Retailer pivot toward high-margin functional beverages | +0.6% | United States and Canada, emerging Mexico | Medium term (2-4 years) |

| Advertisement and marketing campaigns undertaken by players | +0.4% | Global North America | Short term (≤ 2 years) |

| Surge in Gen-Z social-media challenges boosting daily hydration rituals | +0.9% | United States core, Canada secondary | Medium term (2-4 years) |

| Electrolyte-mix adoption cutting logistics costs for DTC brands | +0.5% | United States and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid fitness and gym-membership growth

As gym memberships hit record levels in North America, the expanding fitness industry fuels a growing demand for performance hydration solutions[1]Source: International Health, Racquet & Sportsclub Association, “IHRSA Global Report 2024”, ihrsa.org. Younger demographics, in particular, are rapidly adopting fitness routines as part of their post-pandemic recovery, often in pursuit of holistic wellness. Boutique fitness studios and specialized training centers are now prominently featuring premium sports drinks, establishing direct-to-consumer channels that sidestep conventional retail markups. Brands that provide tailored hydration solutions, whether pre-, during, or post-workout, are reaping the rewards, as consumers increasingly align their hydration choices with specific exercise regimens. Moreover, the rise of wearable tech and fitness tracking has heightened awareness around hydration, leading to consistent consumption patterns that extend beyond typical seasonal surges.

Intensifying heat-wave frequency elevating hydration demand

North Americans, increasingly aware of hydration needs due to climate change-induced temperature extremes, are extending their consumption of electrolyte solutions beyond the traditional summer peak. The National Weather Service highlights a rising trend in heat advisories and extreme temperature events, with the southwestern United States and central Canada bearing the brunt. As a result, outdoor workers, recreational athletes, and everyday consumers are turning to electrolyte replacements to combat heat stress. Retailers, attuned to this consistent demand, are broadening their sports drink displays beyond just seasonal peaks, leading to optimized inventory and improved margins. This shift is especially advantageous for isotonic and hypotonic drinks, as consumers now prioritize their functional benefits over conventional taste preferences.

Retailer pivot toward high-margin functional beverages

Retailers are shifting their strategies, focusing on functional beverages that promise better margins than traditional soft drinks. Sports drinks, in particular, are being given prime shelf space. Recognizing that consumers are willing to pay more for perceived health benefits, major retailers are dedicating more shelf space to sports nutrition categories. This evolving landscape is paving the way for emerging brands to forge distribution partnerships, a space once dominated by industry giants. Retailers, in their quest for unique product offerings that can spur category growth, are increasingly turning to private labels. For instance, Costco is broadening its Kirkland Signature hydration line, aiming to boost margins while staying competitively priced. As retailers push for greater sports drink consumption, they're employing strategies like strategic placement, promotions, and cross-merchandising with wellness products, further fueling the category's expansion.

Surge in Gen-Z social-media challenges boosting daily hydration rituals

Social media platforms, through viral challenges and influencer content, are reshaping the narrative around sports drinks. Instead of being seen merely as a functional necessity, these drinks are increasingly viewed as lifestyle symbols. Campaigns on TikTok and Instagram, spotlighting hydration tracking, flavor reviews, and workout recovery, have successfully engaged the 18-25 demographic, leading to tangible purchase behaviors. This trend isn't confined to traditional sports settings; Gen Z is now seamlessly weaving sports drinks into their daily lives, treating them as wellness accessories and props for social media. Brands are seizing this opportunity, launching targeted digital marketing campaigns, introducing limited edition flavors, and designing packaging for maximum social media impact. This strategy not only creates viral marketing loops but also slashes customer acquisition costs. Brands boasting a strong visual identity and innovative flavors stand to gain the most, as social media buzz fuels both trial and repeat purchases.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High sugar content and health concerns | -0.7% | Concentrated in health-conscious urban markets | Medium term (2-4 years) |

| Recyclate-grade PET shortages inflating packaging costs | -0.5% | United States and Canada manufacturing hubs | Short term (≤ 2 years) |

| Shelf-space cannibalization by enhanced waters and energy drinks | -0.4% | North America retail chains | Medium term (2-4 years) |

| Competition from healthier substitutes | -0.6% | United States and Canada urban and premium segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High sugar content and health concerns

As consumers become more aware of the health risks associated with sugar, traditional sports drink formulations are facing challenges, especially from health-conscious individuals who are now more diligent in scrutinizing nutritional labels. Manufacturers are feeling the heat from the FDA's updated nutrition labeling requirements and its proposed guidelines on "healthy" claims[2]Source: U.S. Food and Drug Administration, “Use of the Term ‘Healthy’ in Food Labeling”, fda.gov. These pressures are pushing manufacturers to either reformulate their products or risk losing market share to alternatives with lower sugar content. Medical studies have established a link between excessive sugar consumption and metabolic disorders, further fueling consumer skepticism. This has led to a surge in demand for zero-sugar and naturally sweetened variants. While these alternatives often come with a premium price tag, they do grapple with challenges related to taste acceptance. Established brands, traditionally centered around high-sugar formulations, are feeling the brunt of this shift. They're now compelled to make costly reformulation investments, risking fragmentation of their consumer base in the process. Moreover, healthcare providers are increasingly endorsing electrolyte-only solutions for hydration, even outside athletic contexts. This endorsement intensifies competition from enhanced water categories, which are marketing themselves as healthier substitutes to conventional sports drinks.

Recyclate-grade PET shortages inflating packaging costs

Sports drink manufacturers, striving to meet sustainability targets, face cost pressures due to supply chain constraints in recycled PET materials. These constraints arise as recyclate-grade plastics fetch a premium over their virgin counterparts. The Environmental Protection Agency's (EPA) National Recycling Strategy, combined with state-level mandates for recycled content, has increased the demand for post-consumer recycled PET[3]Source: U.S. Environmental Protection Agency, “National Recycling Strategy 2024”, epa.gov. This surge in demand, juxtaposed with supply limitations, has led to inflated packaging costs throughout the beverage industry. High-volume producers, reliant on consistent supplies of recyclates for their large-scale operations, find themselves at a crossroads, balancing their sustainability commitments against the need to preserve profit margins. While alternative packaging solutions, such as aseptic cartons and aluminum cans, present sustainability advantages, they come with the caveat of hefty capital investments in new production lines and the necessity for consumer acceptance campaigns. The ongoing shortage has spurred consolidation among packaging suppliers and prompted long-term contract negotiations, potentially curbing flexibility in adapting to market demand shifts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Soft Drink Type: Isotonic Dominance Faces Hypertonic Disruption

In 2025, isotonic formulations dominate the market with a 52.40% share, thanks to their balanced electrolyte concentration and palatability, making them a favorite among mainstream consumers. This segment's stronghold is bolstered by decades of consumer education, highlighting the physiological benefits of isotonic solutions for moderate exercise and daily hydration, as noted by the Journal of Sports Medicine. Meanwhile, hypertonic variants are making waves, emerging as the fastest-growing segment with a 6.65% CAGR projected through 2031. Their rise is fueled by niche applications in athletics and a focus on recovery, appealing to dedicated fitness enthusiasts. Endurance athletes and workers in hot climates continue to favor hypotonic formulations. At the same time, electrolyte-enhanced water is winning over health-conscious consumers, offering functional benefits without the typical associations of sports drinks.

While protein-based sports drinks hold the title of being the most innovative. Manufacturers are venturing into plant-based proteins and unique amino acid profiles, setting themselves apart from the conventional carbohydrate-electrolyte mixes. The focus is on blending proteins with electrolytes, targeting the post-workout recovery market, especially among strength trainers. However, for this segment to truly flourish, there's a pressing need for taste enhancements and cost reductions. Despite boasting superior nutritional profiles over traditional options, many current formulations grapple with consumer acceptance hurdles.

By Packaging Type: Sustainable Innovation Challenges PET Dominance

In 2025, PET bottles command a dominant 95.40% market share, thanks to their cost efficiency, durability, and widespread consumer familiarity. Meanwhile, aseptic packages are the rising star, boasting a robust 5.70% CAGR, fueled by sustainability mandates and their ability to extend shelf life, thus slashing inventory costs for both retailers and manufacturers. Glass bottles are the go-to for premium craft and organic brands, while metal cans are making waves in convenience stores, especially where refrigerated display space comes at a premium. Disposable cups, although niche, find their primary use in foodservice and events, driven by the need for portion control and branding visibility.

The packaging industry is grappling with disruptions, spurred by regulatory pressures and a shift towards sustainability. California's recycled content mandates and Canada's crackdown on single-use plastics are reshaping industry strategies. Manufacturers are investing in lightweight PET technologies and exploring alternatives, such as aluminum bottles. Yet, hurdles remain in terms of consumer acceptance and cost dynamics. The focus of innovation is on enhancing barrier properties to uphold product quality while minimizing material use. Notably, several leading brands are piloting refillable packaging systems in select markets, aiming to tackle environmental concerns without compromising on operational efficiency.

By Functionality: Pre-Workout Leadership Yields to Post-Workout Growth

In 2025, pre-workout products command a dominant 66.10% share of the market, thanks to ingrained consumer habits and strategic merchandising by retailers. These retailers adeptly position sports drinks alongside fitness supplements and energy products. This segment's prominence underscores a clear consumer preference for caffeine-infused formulations and energy-boosting ingredients, integral to their exercise routines. Meanwhile, post-workout variants are witnessing the fastest growth, surging at an 7.55% CAGR. This uptick is fueled by a heightened awareness of recovery nutrition, with protein-rich formulations catering to the muscle repair and glycogen replenishment needs of dedicated athletes.

Intra-workout products cater to niche endurance needs, especially within cycling and running circles. Here, the demand for sustained energy during prolonged sessions necessitates unique formulations. The "Others" category encompasses budding trends like daily wellness hydration and meal replacements. This expansion sees sports drink brands venturing into the wider realm of functional beverages. As brands emphasize the importance of timing in nutrition, they're crafting diverse product lines that cater to the entire workout journey, rather than isolated moments.

By Distribution Channel: E-commerce Disrupts Traditional Retail Patterns

In 2025, supermarkets and hypermarkets command a 55.30% share of the distribution landscape, harnessing their vast reach and promotional prowess to boost sales across diverse consumer segments. Yet, online retail is the rising star, boasting a robust 8.35% CAGR, underscoring a shift in consumer behavior towards subscription models, bulk buying, and direct engagements with brands. While convenience stores thrive on impulse buys and immediate needs, specialty outlets cater to discerning customers in search of premium and organic products often absent from mainstream shelves.

The retail landscape is evolving, with brands adopting omnichannel approaches that seamlessly blend physical and digital experiences. These strategies see major players pouring investments into direct-to-consumer platforms, sidestepping traditional retail margins yet preserving ties with retailers. Amazon's foray into expanding its beverage category and its push for subscription services are reshaping competitive dynamics, compelling traditional retailers to bolster their digital strategies and enhance their offerings. Across the board, there's a notable surge in private label development, as retailers aim to boost profit margins while providing viable alternatives to established national brands.

Geography Analysis

In 2025, the United States commands a dominant 87.60% market share, a testament to its well-established sports culture, robust retail framework, and elevated per capita consumption rates. These factors collectively underpin a projected growth rate of 4.05% CAGR through 2031. Within the United States, regional nuances present unique opportunities: southwestern states, influenced by their climate and a culture of outdoor recreation, showcase heightened consumption. In contrast, northeastern markets gravitate towards premium and organic offerings, resonating with their health-conscious populace, as highlighted by the United States Census Bureau's Economic Indicators. The United States market's maturity paves the way for intricate segmentation strategies. Brands are now crafting region-specific flavors and formulations, attuned to local palates and climatic nuances. Furthermore, major retailers are harnessing heat-mapping technologies, fine-tuning sports drink placements and inventory management across diverse climate zones, all in a bid to amplify sales velocity and optimize margins.

Canada stands out as the region's fastest-growing market, boasting a robust 5.70% CAGR. This surge is fueled by a rise in fitness participation and a modernization of retail channels, broadening category access in both urban and rural locales. Canadians show a marked preference for natural and organic products, presenting a golden opportunity for premium brands to carve out a niche before the market becomes saturated. Major cities like Toronto and Vancouver are witnessing a surge in convenience store expansions, creating fresh distribution avenues. Additionally, cross-border shopping habits are shaping pricing strategies and brand placements. Recent shifts in regulations, particularly concerning recycled packaging, resonate with the growing consumer emphasis on sustainability, giving an edge to brands championing environmental responsibility.

Mexico, often viewed as the underdog in North America's market landscape, holds vast untapped potential. Local stalwarts like Electrolit have successfully tailored their offerings to align with regional tastes and budgetary considerations. Thanks to the USMCA trade agreements, there's a noticeable uptick in cross-border investments and distribution collaborations. This has empowered United States and Canadian brands to set up local production in Mexico, slashing logistics costs and enhancing market agility. The trajectory of Mexico's market growth is closely intertwined with its economic evolution and urbanization, both of which are bolstering disposable incomes and fitness engagement among the burgeoning middle class. Cultural nuances play a pivotal role in shaping consumption trends; for instance, traditional fruit flavors and family-sized packaging are more warmly embraced than the specialized athletic formulations that find favor in northern territories.

Competitive Landscape

In North America, the sports drinks market is fiercely competitive, dominated by industry titans PepsiCo and Coca-Cola. Through their Gatorade/Propel and Powerade/BodyArmor brands, these giants command a significant share of the market. Notably, both companies are diversifying their brand portfolios, often acquiring emerging brands to tap into niche markets and evolving demographics. A case in point is Coca-Cola's USD acquisition of BodyArmor and Keurig Dr Pepper's strategic purchase of Ghost, both aimed at appealing to the gaming and lifestyle audiences. These acquisitions highlight a broader trend where established players seek to align with shifting consumer preferences, particularly among younger demographics, by integrating brands that resonate with specific lifestyles and interests.

Technology plays a pivotal role in setting companies apart. Innovations like personalized nutrition platforms, AI-driven flavor creation, and direct-to-consumer subscription services are reshaping the landscape. These models not only sidestep traditional retail margins but also amass valuable consumer data for targeted marketing. For instance, personalized nutrition platforms allow brands to cater to individual health goals, while AI-powered flavor development enables rapid adaptation to emerging taste trends. Meanwhile, newcomers like Prime Hydration are making waves, harnessing social media and celebrity endorsements to capture the attention of Gen Z. In response, established brands are ramping up their innovation efforts and forging alliances with fitness influencers and professional sports entities to maintain relevance and expand their consumer base.

Today's competitive arena rewards those with robust digital marketing strategies, eco-friendly packaging, and nimble product development. Companies that swiftly adapt to trending flavors and ingredient innovations, often spotlighted by social media and the growing wellness culture, are finding greater success. For example, the increasing demand for functional ingredients, such as electrolytes and adaptogens, is driving product innovation, while sustainable packaging solutions are becoming a key differentiator as consumers prioritize environmental responsibility.

North America Sports Drinks Industry Leaders

PepsiCo, Inc.

The Coca-Cola Company

Monster Beverage Corporation

Red Bull GmbH

Celsius Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Stephen Curry, a four-time NBA champion, joined forces with former First Lady Michelle Obama to unveil Plezi Hydration, a healthier sports drink alternative. Crafted with intelligent ingredients, Plezi is available at Walmart, Albertsons, and Safeway in California, and can also be purchased nationwide on Amazon.

- October 2024: Keurig Dr Pepper finalized its USD 990 million acquisition of Ghost. This move not only broadens KDP's footprint in the energy and sports nutrition sectors but also taps into Ghost's robust gaming and lifestyle audience. With this acquisition, KDP is better positioned to challenge established players in the functional beverage arena, capitalizing on Ghost's innovative marketing and dedicated consumer following.

- January 2024: Coca-Cola rolled out BodyArmor Zero Sugar, making its debut across North American retail and online platforms.

North America Sports Drinks Market Report Scope

Electrolyte-Enhanced Water, Hypertonic, Hypotonic, Isotonic, Protein-based Sport Drinks are covered as segments by Soft Drink Type. Aseptic packages, Metal Can, PET Bottles are covered as segments by Packaging Type. Convenience Stores, Online Retail, Specialty Stores, Supermarket/Hypermarket, Others are covered as segments by Sub Distribution Channel. Canada, Mexico, United States are covered as segments by Country.

By Soft Drink Type

| Isotonic |

| Hypertonic |

| Hypotonic |

| Electrolyte-Enhanced Water |

| Protein-based Sport Drinks |

By Packaging Type

| PET Bottles |

| Glass Bottles |

| Metal Can |

| Aseptic Packages (tetra pak, cartons, pouches) |

| Disposable Cups |

By Functionality

| Pre-Workout |

| Intra-Workout |

| Post-Workout |

| Others |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail | |

| Other Distribution Channels |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Soft Drink Type | Isotonic | |

| Hypertonic | ||

| Hypotonic | ||

| Electrolyte-Enhanced Water | ||

| Protein-based Sport Drinks | ||

| By Packaging Type | PET Bottles | |

| Glass Bottles | ||

| Metal Can | ||

| Aseptic Packages (tetra pak, cartons, pouches) | ||

| Disposable Cups | ||

| By Functionality | Pre-Workout | |

| Intra-Workout | ||

| Post-Workout | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Market Definition

- Carbonated Soft Drinks (CSDs) - Carbonated soft drinks (CSDs) refer to non-alcoholic beverages that are carbonated and typically flavored, containing dissolved carbon dioxide to create effervescence. These beverages commonly include cola, lemon-lime, orange, and various fruit-flavored sodas. Marketed in cans, bottles, or fountain dispense.

- Juices - We have considered packaged juices which encompass non-alcoholic beverages derived from fruits, vegetables, or a combination thereof, processed and sealed in various packaging formats such as bottles, cartons, or pouches. Excluding fresh juices, this market segment involves commercially prepared and preserved juices, often with added preservatives and flavors.

- Ready-to-Drink (RTD) Tea and RTD Coffee - Ready-to-Drink (RTD) tea and RTD coffee are pre-packaged, non-alcoholic beverages that are brewed and prepared for consumption without further dilution. RTD tea typically includes various tea varieties, infused with flavors and sweeteners, and comes in bottles, cans, or cartons. Similarly, RTD coffee involves pre-brewed coffee formulations, often mixed with milk, sugar, or flavorings, and is conveniently packaged for on-the-go consumption.

- Energy Drinks - Energy drinks are non-alcoholic beverages formulated to provide a quick boost of energy and alertness. Whereas, sports drinks are beverages designed to hydrate and replenish electrolytes, particularly after physical exertion, exercise, or intense activity

| Keyword | Definition |

|---|---|

| Carbonated Soft Drinks | Carbonated soft drinks (CSDs) are a combination of carbonated water and flavouring, sweetened by sugar or a non-sugar sweeteners. |

| Standard Cola | Standard Cola is defined as the original flavor of cola soda. |

| Diet Cola | A cola-based soft drink containing no or low amounts of sugar |

| Fruit Flavored Carbonates | A carbonated beverage prepared from fruit juice/fruit flavor with carbonated water and containing sugar, dextrose, invert sugar or liquid glucose either singly or in combination. It may contain peel oil and fruit essences. |

| Juice | Juice is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| 100% Juice | Fruit/vegetable juice made from fruit in the form of its juice with no water added to make up the volume. It is not permitted to add sugars, sweeteners, preservatives, flavourings or colourings to fruit juice. |

| Juice Drinks (up to 24% Juice) | Fruit/vegetable juice drinks with up to 24% fruits/vegetable extract. |

| Nectars (25-99% Juice) | Juices that can have between 25 and 99% of fruit, with the minimum legal limits defined depending on the type of fruit |

| Juice concentrates | Juice Concentrates are those form of juices when most of this liquid is removed resulting in a thick, syrupy product known as juice concentrate. |

| RTD Coffee | Packaged coffee beverages that are sold in a prepared form and are ready for consumption at the time of purchase. |

| Iced Coffee | An iced coffee is a cold version of coffee, usually a combination of hot espresso and milk with ice added to it. |

| Cold Brew Coffee | Cold brew also called cold water extraction or cold pressing is made by steeping ground coffee in room-temperature water for several hours. |

| RTD Tea | Ready-to-drink (RTD) tea is a packaged tea product ready for immediate consumption without brewing or preparation |

| Iced Tea | Ice tea or iced tea is a drink made from tea without milk but with sugar and sometimes fruit flavourings, drunk cold. |

| Green Tea | Green tea is a tea beverage which promotes mental alertness, relieving digestive symptoms and promoting weight loss. |

| Herbal Tea | Herbal tea beverages are made from the infusion or decoction of herbs, spices, or other plant material in hot water. |

| Energy Drink | A type of drink containing stimulant compounds, usually caffeine, which is marketed as providing mental and physical stimulation. They may or may not be carbonated and may also contain sugar, other sweeteners, or herbal extracts, among numerous possible ingredients. |

| Sugar-free or Low-calories Energy Drinks | Sugar-free or Low-calories Energy Drinks are sugar-free, artificially sweetened energy drinks with few or no calories. |

| Traditional Energy Drink | Traditional Energy Drinks are functional soft drinks containing ingredients designed to boost the consumer's energy. |

| Natural/Oraganic Energy Drinks | Natural/Organic energy drinks are energy drinks free of artificial sweeteners and synthetic colorings. Instead, they contain naturally derived ingredients such as green tea, yerba mate, and botanical extracts. |

| Energy Shots | A small but highly concentrated energy drink that contains large amounts of caffeine and/or other stimulants. The quantity is comparatively smaller compared to energy drinks. |

| Sports Drink | Sports drinks are beverages designed specifically for the rapid supply of fluid, carbohydrates, and electrolytes before, during or after exercise. |

| Isotonic | Isotonic drinks contain similar concentrations of salt and sugar as in the human body, and are designed to quickly replace fluids lost during exercise but with an increase of carbohydrate. |

| Hypertonic | Hypertonic drinks have a higher concentration of salt and sugar than the human body. They are best drunk after exercise as it is important to replace glycogen levels quickly after exercise. |

| Hypotonic | Hypotonic drinks are designed to quickly replace fluids lost during exercise. They have very low carbohydrate content and a lower concentration of salt and sugar than the human body. |

| Electrolyte-Enhanced Water | Electrolyte water is water infused with electrically-charged minerals, such as sodium, potassium, calcium, and magnesium. |

| Protein-based Sport Drinks | Protein-based sports drinks are those sports drinks which has added protein in it that will improve performance and reduce muscle protein breakdown. |

| On-Trade | The on-trade refers to places that sell beverages for immediate consumption on the premises like bars, restaurants, and pubs |

| Off-Trade | Off-trade usually means places like liquor stores, supermarkets and other places where you don't consume the beverage right away. |

| Convenience Store | A retail business that provides the public with a convenient location to quickly purchase a wide variety of consumable products and services, generally food and gasoline. |

| Specialty store | A specialty store is a shop/store that carries a deep assortment of brands, styles, or models within a relatively narrow category of goods |

| Online Retail | Online retail is a type of eCommerce whereby a business sells goods or services directly to consumers from a website. |

| Aseptic Packaging | Aseptic packaging refers to the filling of a cold, commercially sterile product under sterile conditions into a presterilized container and closure under sterile conditions to form a seal that effectively excludes microorganisms. These includes tetra packs, cartons, pouches etc. |

| PET Bottle | PET bottle means a bottle made of polyethylene terephthalate. |

| Metal Cans | Metal containers made of aluminum or tin- plated or zinc-plated steel, which are commonly used for packaging food, beverages or other products. |

| Disposable Cups | Disposable Cup means a cup or other container designed for single use to serve beverages, such as water, cold drinks, hot drinks and alcoholic beverages. |

| Gen Z | A way of referring to the group of people who were born in the late 1990s and early 2000s. |

| Millenial | Anyone born between 1981 and 1996 (ages 23 to 38 in 2019) is considered a Millennial |

| Taurine | Taurine is an amino acid that supports immune health and nervous system function. |

| Bars & Pubs | It is a drinking establishment licensed to serve alcoholic drinks for consumption on the premises. |

| Café | It is a foodservice establishment serving refreshments (mainly coffee) and light meals. |

| On the go | It means doing / dealing with while busily engaged with something and not diverting plans in order to accommodate. |

| Internet Penetration | The Internet Penetration Rate corresponds to the percentage of the total population of a given country or region that uses the Internet. |

| Vending Machine | A machine that dispenses small articles such as food, drinks, or cigarettes when a coin or token is inserted |

| Discount store | A discount store or discounter offers a retail format in which products are sold at prices that are in principle lower than an actual or supposed "full retail price". Discounters rely on bulk purchasing and efficient distribution to keep down costs. |

| Clean Label | Clean label on the beverage market are drinks that are made from few ingredients of natural origin and are not or only slightly processed. |

| Caffeine | An alkaloid compound which is a stimulant of the central nervous system. It is mainly used recreationally, as a mild cognitive enhancer to increase alertness and attentional performance. |

| Extreme sport | Action sports, adventure sports or extreme sports are activities perceived as involving a high degree of risk. |

| High-intensity interval training | It incorporates several rounds that alternate between several minutes of high intensity movements to significantly increase the heart rate to at least 80% of one's maximum heart rate, followed by short periods of lower intensity movements. |

| Shelf life | The length of time for which an item remains usable, fit for consumption, or saleable. |

| Cream Soda | Cream soda is a sweet soft drink. Generally flavored with vanilla and based on the taste of an ice cream float |

| Root Beer | Root beer is a sweet North American soft drink traditionally made using the root bark of the sassafras tree Sassafras albidum or the vine of Smilax ornata as the primary flavor. Root beer is typically, but not exclusively, non-alcoholic, caffeine-free, sweet, and carbonated. |

| Vanilla Soda | A carbonated soft drink flavoured with vanilla. |

| Dairy-Free | A product that does not contain any milk or milk products from cows, sheep or goats. |

| Caffeine-Free Energy Drinks | Caffeine-free energy drinks rely on other ingredients to boost the energy. Popular choices include amino acids, B vitamins, and electrolytes. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated reports, custom consulting assignments, databases & subscription platforms