Middle East Sports Drinks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

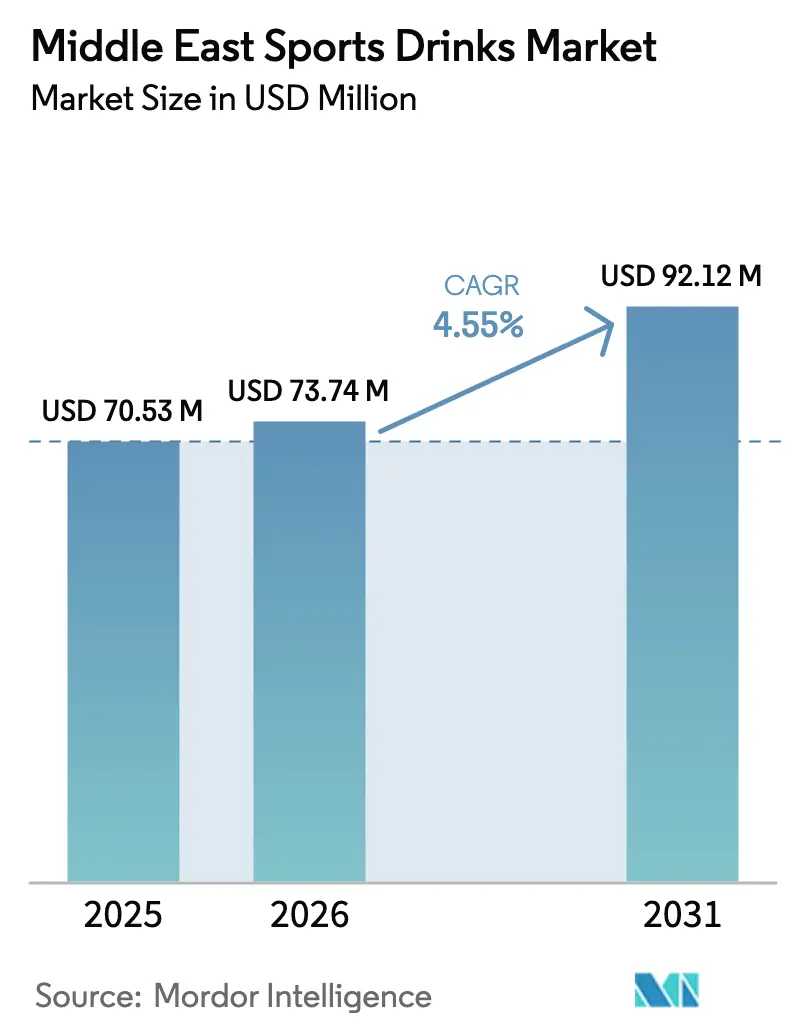

| Base Year Market Size (2025) | USD 70.53 Million |

| Market Size (2026) | USD 73.74 Million |

| Market Size (2031) | USD 92.12 Million |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

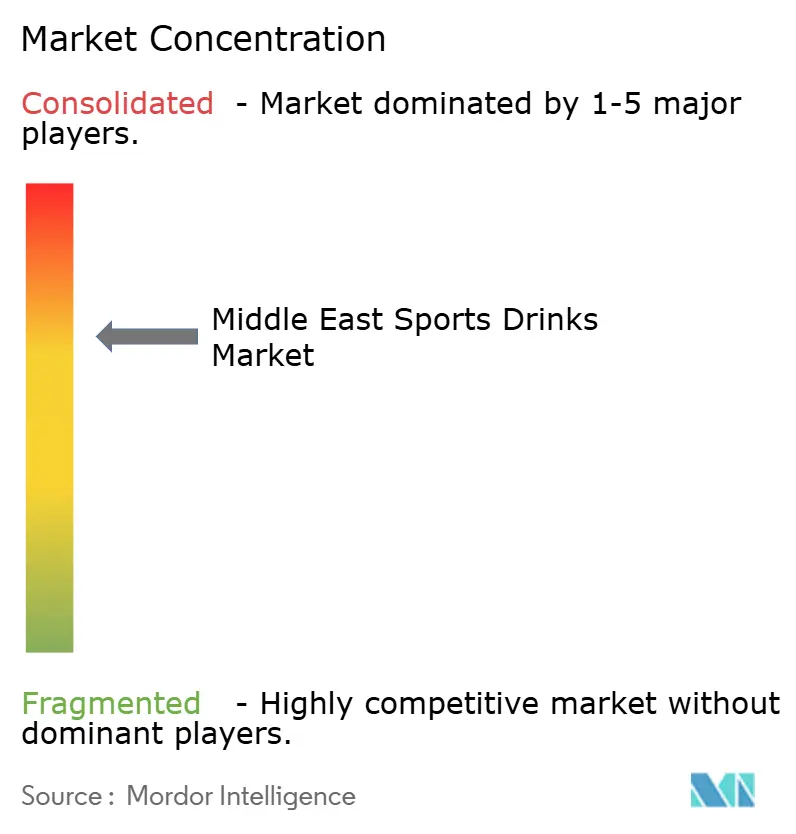

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East Sports Drinks Market Analysis by Mordor Intelligence

The Middle East Sports Drinks Market size is expected to grow from USD 70.53 million in 2025 to USD 73.74 million in 2026 and is forecast to reach USD 92.12 million by 2031 at 4.55% CAGR over 2026-2031. Extreme summer temperatures, government-backed fitness programs, and an ambitious roster of international competitions all reinforce stable demand for functional hydration. Saudi Arabia’s Vision 2030 plan to push sports participation to 40% by 2030, the United Arab Emirates's Walk 30 initiative, and Dubai’s annual 30 × 30 Fitness Challenge collectively move sports drinks from niche athletic use to everyday consumption. Besides, event-led infrastructure, such as the 15 new or upgraded stadiums pledged for FIFA World Cup 2034, broadens consumer exposure while creating high-traffic on-trade points. Meanwhile, tiered sugar taxes to be enforced from January 2026 in both the United Arab Emirates and Saudi Arabia accelerate reformulation toward lower-sugar, clean-label variants. Supply-chain innovation in aseptic packaging is further reshaping format choices and helping brands reach second-tier cities without refrigeration.

Key Report Takeaways

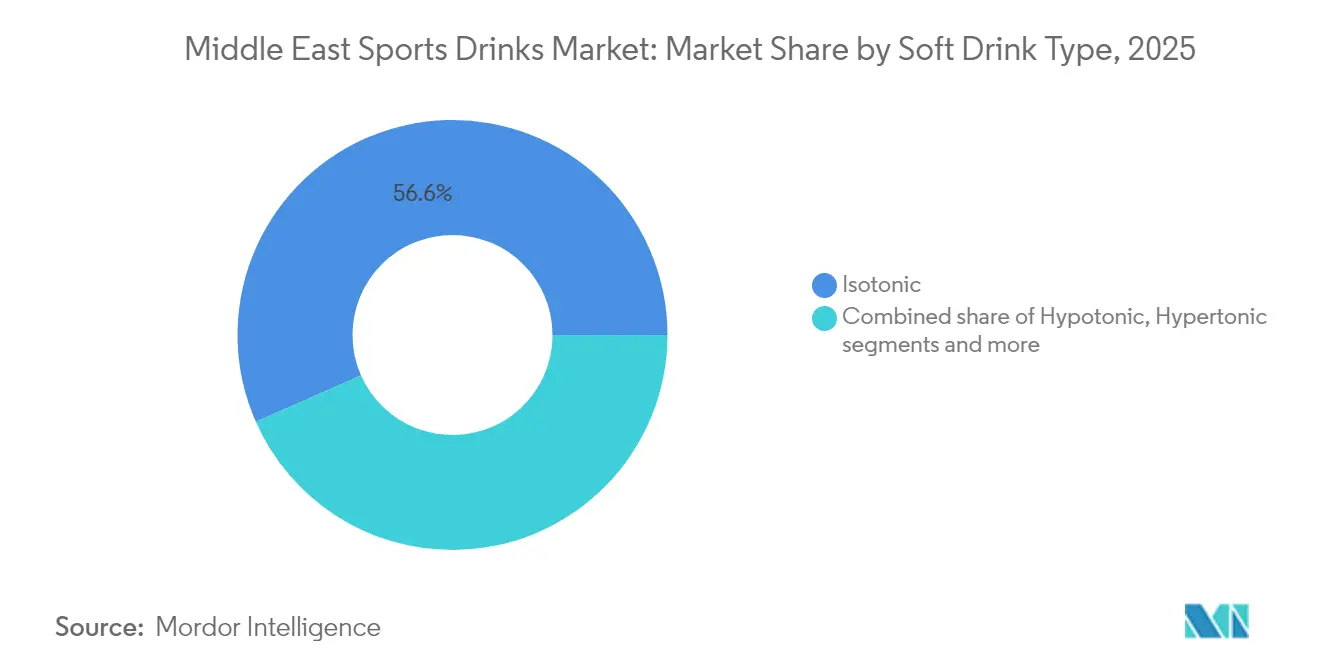

- By soft-drink type, isotonic drinks led with 56.62% of the Middle East sports drinks market share in 2025; hypertonic drinks are forecast to expand at a 5.72% CAGR through 2031.

- By packaging, PET bottles captured 84.78% share of the Middle East sports drinks market size in 2025, while aseptic formats are projected to record 6.21% CAGR by 2031.

- By distribution channel, off-trade commanded 76.12% revenue in 2025; on-trade outlets are expected to grow at a 6.03% CAGR to 2031.

- By functionality, intra-workout beverages represented 58.04% of 2025 demand, whereas post-workout drinks are advancing at a 5.84% CAGR through 2031.

- By country, the United Arab Emirates accounted for 35.92% of 2025 sales, whereas Saudi Arabia is poised for the fastest 5.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Sports Drinks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Geographic Relevance |

|---|---|---|---|

| Intensifying health and fitness focus | +0.9% | Saudi Arabia, United Arab Emirates; spillover to Qatar, Bahrain | Medium term (2-4 years) |

| Hot climate and heat stress management driving hydration demand | +1.2% | GCC-wide, peak impact in the United Arab Emirates, Saudi Arabia, Qatar | Long term (≥ 4 years) |

| Rising sports culture and events | +1.0% | Saudi Arabia, United Arab Emirates, Qatar; event-driven spikes in host cities | Medium term (2-4 years) |

| Clean-label and "better-for-you" reformulation | +0.8% | United Arab Emirates, Saudi Arabia; spillover to Qatar, Bahrain | Short term (≤ 2 years) |

| Partnerships with gyms, clubs, and federations unlocking new demand pockets | +0.5% | United Arab Emirates, Saudi Arabia; urban fitness hubs in Riyadh, Dubai, Doha | Medium term (2-4 years) |

| Growing interest in protein-infused and recovery enhancing sports drinks | +0.7% | United Arab Emirates, Saudi Arabia; urban fitness hubs and premium retail channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying health and fitness focus

Rising gym memberships, running clubs, football academies, and mass-participation events are driving a shift toward making physical activity a regular routine, significantly increasing demand for sports drinks tailored to pre-, during-, and post-workout hydration. National wellness strategies, such as the Dubai Sports Council’s long-term agenda, are embedding structured training calendars that normalize sports drink consumption at marathons, grassroots tournaments, and other events. In Saudi Arabia, as per the General Authority for Statistics (GASTAT), in 2024, where 58.5% of adults meet weekly physical activity targets, and 18.7% of children achieve daily activity thresholds, the need for convenient hydration solutions is growing [1]Source: Ministry of Sport of Saudi Arabia, "General Authority for Statistics Announces Physical Activity Statistics for Saudi Arabia in 2024", mos.gov.sa. Formal settings like gyms, fitness chains, and football clubs further reinforce the association of sports drinks with training, while partnerships between brands and institutions drive predictable demand spikes during tournament seasons. Brands such as Gatorade and Pocari Sweat are becoming default choices in these environments, while others like iPRO Hydrate secure exclusivity through direct collaborations with clubs and federations. Over time, this interplay between rising participation rates, structured programs, and branded partnerships shapes consumer behavior, with regular exercisers differentiating between plain water for low-intensity activities and electrolyte- or protein-enhanced sports drinks for intensive sessions. Parents of active children are also increasingly exposed to sports drinks through school leagues and academies, where hydration routines often include isotonic drinks in small PET formats. As event calendars expand with marathons, city runs, and regional tournaments, brands visible on-course, in athlete packs, and in fan zones convert trial into habitual purchases. This convergence of top-down policies, behavioral changes, and brand activations positions the growing focus on health and fitness as a critical structural driver for the sports drinks market, ensuring sustained growth rather than a short-term promotional effect.

Hot climate and heat stress management driving hydration demand

High Gulf summer temperatures exceeding 40°C accelerate fluid and electrolyte loss, making rapid rehydration essential for workers in sectors such as construction, logistics, municipal services, and outdoor hospitality. Recognizing the link between heat stress, dehydration, and productivity losses, authorities have implemented regulations like the United Arab Emirates's midday work ban, which mandates cold drinking water, hydration aids, and shaded rest areas. Similar measures in Saudi Arabia and Qatar have positioned hydration as a core occupational safety requirement. For example, Dubai Municipality’s 2024 heat stress guidelines mandate hydration breaks between 12:30 and 15:00 from June to September, requiring employers to plan drink volumes and formats for large teams [2]Source: Ministry of Human Resources and Emiratisation, "Occupational Heat Stress Prevention Policy", mohre.gov.ae. Saudi Arabia’s National Center for Occupational Safety and Health has also reinforced protocols for heat-exposed industries, linking dehydration and heat-related illnesses to economic costs, thereby strengthening the case for electrolyte-based solutions in high-sweat environments. These developments have elevated isotonic and hypotonic beverages from discretionary purchases to essential provisions in workplaces where sweating is continuous, and air-conditioned rest is limited. This shift has created a dedicated B2B channel for sports drinks in industries such as construction, oil and gas support services, logistics yards, and outdoor operations at theme parks or resorts, where bulk procurement is integrated into safety compliance budgets. Brands are responding with tailored formats, such as Pocari Sweat’s multi-pack and powder options for on-site mixing, and functional hydration brands offering large-volume bag-in-box or multi-case deals marketed as “workforce hydration solutions.” These programs operate on contracts, bypassing retail margins and stabilizing demand during peak summer months. The combination of extreme climate conditions, codified work bans, and evolving safety frameworks is embedding sports drinks into Gulf employers’ risk-management strategies, making heat-stress management a durable non-athletic demand driver in the region.

Rising sports culture and events

Saudi Arabia’s successful bid to host the FIFA World Cup 2034, backed by a USD 10 billion investment in 15 stadiums, training facilities, and sports complexes across Riyadh, Jeddah, NEOM, and Qiddiya, is establishing elite football as a long-term structural driver of the region’s sports drinks market. This infrastructure expansion is complemented by projects like Riyadh’s 135-kilometer Sports Boulevard, designed to attract 3 million visitors annually and aligned with Vision 2030’s goal of increasing sports participation from 13% in 2016 to 40% by 2030. These developments provide year-round access to cycling tracks, running paths, and outdoor gyms, fostering regular fitness activities. As these facilities become operational, they generate thousands of training sessions, academy programs, and community events weekly, creating consistent demand for performance-oriented hydration. Similarly, initiatives like the United Arab Emirates's Dubai Fitness Challenge, which encourages residents to engage in 30 minutes of activity for 30 consecutive days, act as annual behavioral resets, offering sports drink brands predictable opportunities for product sampling in gyms, community runs, and corporate wellness events. Brands securing official sponsorship rights for national teams, stadiums, or city-wide challenges gain advantages such as pouring rights, logo visibility, and on-site sales exclusivity, fostering high trial-to-repeat conversion rates. For example, Lucozade Sport leverages sponsorships to provide on-pitch coolers, finisher-bottle giveaways, and team-branded packaging, reinforcing its association with performance. These sponsorships, often spanning multiple seasons, sustain market share growth beyond single events. The interplay of mega-events, Vision 2030-aligned infrastructure, and recurring fitness initiatives is steadily expanding the scale and resilience of sports-related demand, positioning sports culture and events as a key driver of growth in the sports drinks market.

Clean-label and “better-for-you” reformulation

Consumer demand for clean-label and "better-for-you" reformulations is reshaping the sports drinks market in the Middle East. With increasing awareness of obesity, diabetes, and wellness, there is a growing preference for products that are low in sugar and free from artificial additives. In response, beverage companies are introducing zero-sugar product lines and replacing artificial sweeteners, flavors, and colors with natural ingredients that can be clearly communicated on packaging. Brands like Bodyarmor highlight "no artificial flavors, dyes, or sweeteners" as a core message, while United Arab Emirates-focused entrants incorporate vitamins and functional botanicals with no added sugar to position themselves as both health-conscious and premium. Natural sweeteners such as stevia and monk fruit are being leveraged to provide sweetness without raising glycemic levels or breaching sugar tax regulations, which are now enforced across much of the Gulf Cooperation Council. This trend is further driven by younger consumers’ interest in wellness and the overlap with beauty-focused positioning, as clear labeling and vitamin-enriched formulations appeal to those seeking holistic hydration that supports an active lifestyle. Regulatory policies also play a significant role, with Saudi Arabia’s Saudi Food and Drug Authority (SFDA) emphasizing healthy ingredient transparency as part of its Vision 2030 public health agenda. Additionally, the increasing preference for environmentally responsible and recyclable packaging among Emirati consumers is accelerating the adoption of aseptic and eco-friendly formats by sports drink brands. Clean-label preferences are now influencing research and development as well as branding strategies, steering the market away from traditional soft drink approaches toward modern, science-based hydration solutions that align with regional demands for purity and trust.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from other hydration formats | -0.6% | United Arab Emirates, Saudi Arabia, Qatar; premium retail channels and health-conscious segments | Medium term (2-4 years) |

| Regulatory pressure on sugar and HFSS products | -0.9% | United Arab Emirates, Saudi Arabia; GCC-wide harmonization underway | Short term (≤ 2 years) |

| Price sensitivity vs. perceived value in basic use-cases | -0.4% | Saudi Arabia, Rest of Middle East; price-conscious consumer segments | Short term (≤ 2 years) |

| Cold-chain gaps for protein-based formulations | -0.3% | Rest of Middle East, second-tier cities in Saudi Arabia; rural and semi-urban areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from other hydration formats

The growing popularity of coconut water, alkaline water, and low-fat milk beverages is reshaping the hydration market by targeting similar consumption occasions as sports drinks while emphasizing natural and minimally processed attributes. These alternatives appeal to health-conscious consumers by promoting clean hydration, free from artificial colors, flavors, and high sugar content, which has also driven reformulation efforts among sports drink brands. Coconut water highlights naturally occurring electrolytes like potassium, magnesium, and sodium, reinforcing its "from the coconut" narrative over synthetic fortification. Alkaline water, often positioned as a premium product, aligns with wellness trends such as detoxification and pH balance, despite limited performance science compared to isotonic sports drinks. Flavored low-fat or skim milk beverages attract parents and active adults seeking protein and hydration in one product, diverting consumption from traditional sports drinks. In GCC markets, taxes on sugar-sweetened beverages further shift consumer preferences toward untaxed or lower-taxed options like bottled or flavored waters, amplifying the appeal of these alternatives. This dynamic pressures sports drink brands to justify their price premium by demonstrating superior functional benefits, such as faster rehydration, optimized electrolyte ratios, or added performance ingredients, supported by clear messaging and innovations like low-sugar isotonic lines. Meanwhile, direct-to-consumer and quick-commerce platforms, including Talabat, Noon Minutes, and Careem, enable niche brands to reach urban consumers without traditional retail channels. These platforms often feature "recommended for you" or "healthier hydration" sections, placing water-based alternatives alongside sports drinks, encouraging substitution when price discounts or clean-label messaging resonate more than performance claims. For established sports drink brands, this competition compresses profit margins, fragments demand, and necessitates continuous evidence-based differentiation to maintain market share in key hydration occasions.

Regulatory pressure on sugar and HFSS products

Regulatory measures targeting sugar and HFSS (high-fat, sugar, salt) products are intensifying across the Middle East, with the United Arab Emirates and Saudi Arabia set to implement a tiered volumetric excise tax system in January 2026. This system, approved by the GCC’s Financial and Economic Cooperation Committee in 2025, replaces the current flat 50% tax on sweetened beverages and ties tax rates to sugar content per 100ml [3]Source: Saudi Press Agency (SPA), "GCC Financial Committee Adopts Sugar-Based Methodology for Sweetened Beverages Tax", spa.gov.sa . Beverages with less than 5g of sugar per 100ml or those using only artificial sweeteners will be exempt, while drinks with 5g–7.99g of sugar will face a medium tax rate, and those with 8g or more will incur the highest tax. This policy applies to sports drinks, carbonated soft drinks, flavored milks, and energy drinks, encouraging manufacturers to reduce sugar content or risk significant price-driven demand losses. Coordinated enforcement by Saudi Arabia’s Zakat, Tax and Customs Authority and the UAE’s Federal Tax Authority aims to ensure seamless implementation across the GCC. For major brands like Gatorade, this creates a strong incentive to develop reduced-sugar or zero-sugar products to qualify for lower tax brackets. However, reformulation involves substantial research and development and ingredient costs, production line adjustments, and compliance with updated labeling requirements from the SFDA (Saudi Food and Drug Authority) and ESMA (Emirates Authority for Standardization and Metrology). While multinational corporations with robust regulatory teams and innovation pipelines are better positioned to adapt, smaller regional players and local brands face significant financial and operational challenges, making it harder to compete in the newly segmented market. Brands unable to reformulate may absorb higher taxes, compressing margins, or pass costs to consumers, risking volume declines as price-sensitive buyers shift to alternatives. This regulatory shift also accelerates the trend toward cleaner-label formulations, but compliance burdens increasingly favor established multinationals, positioning regulatory changes as a long-term constraint for the Middle East sports drinks market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Soft Drink Type: Isotonic Dominance Meets Hypertonic Momentum

In 2025, isotonic drinks captured 56.62% of the market, driven by their osmolality profile. This profile aligns with the human body's fluid concentration, enabling rapid absorption during and after physical exertion. The region's climate-driven hydration needs have strengthened the position of brands like Gatorade and Powerade, which have long educated consumers on electrolyte replacement. Hypertonic formulations, containing higher concentrations of carbohydrates and electrolytes, are projected to grow at an annual rate of 5.72% through 2031. This growth is primarily attributed to endurance athletes and gym-goers seeking effective post-workout glycogen replenishment.

Moreover, hypotonic drinks, designed for faster fluid absorption, appeal to casual exercisers and individuals exposed to extreme heat, prioritizing hydration speed over energy delivery. Electrolyte-enhanced water, offering mineral fortification without the caloric content of traditional sports drinks, is gaining popularity among office workers and non-athletes seeking functional hydration. Protein-based sports drinks, though still an emerging segment, are expanding as brands like WOW Hydrate introduce formulations combining 20 grams of protein with electrolytes, targeting the post-workout recovery market. Besides, reformulation trends are reshaping the isotonic segment. Gatorade's introduction of a lower-sugar variant with 75% less sugar than the original formula, alongside Gatorade Zero and Gatorade Water, highlights PepsiCo's strategy to maintain market share amid the impending tiered sugar tax regulations.

By Packaging Type: Aseptic Innovation Challenges PET Hegemony

In 2025, PET bottles accounted for 84.78% of the packaging market share, driven by their cost efficiency, widespread consumer acceptance, and compatibility with existing bottling infrastructure. However, aseptic packages, including cartons, pouches, and Tetra Paks, are projected to grow at an annual rate of 6.21% through 2031, marking the fastest growth among packaging formats. This growth is attributed to sustainability mandates, increasing demand for shelf-stable protein formulations, and brand differentiation initiatives. Tetra Pak's Tetra Prisma Aseptic 1000 Edge, equipped with the Bio-based LightCap 30 and manufactured at its Dubai Industrial City facility, incorporates renewable materials sourced from responsibly managed forests. The company aims to achieve 90% renewable content by 2030.

Glass bottles, metal cans, and disposable cups occupy niche segments within the packaging landscape. Glass bottles are associated with premium positioning and are commonly used in upscale gyms and hotels, but their weight and fragility limit their scalability in mass markets. Metal cans dominate the energy drink category but are less prevalent in sports drinks due to consumer perceptions linking cans with carbonation and stimulants rather than hydration. Disposable cups are primarily used in event venues and sports complexes, where single-serve, on-the-go consumption is prevalent. The increasing adoption of aseptic packaging also addresses cold-chain limitations in second-tier cities and rural areas, where refrigerated retail space is scarce and high ambient temperatures compromise product stability. Companies targeting national distribution must navigate the trade-off between the premium appeal of chilled PET bottles and the logistical efficiency of shelf-stable cartons.

By Distribution Channel: On-Trade Gains Ground as Fitness Culture Expands

Off-trade channels, which include supermarkets, hypermarkets, convenience stores, specialty stores, and online retail, accounted for 76.12% of distribution in 2025. This dominance is particularly evident in the United Arab Emirates, where hypermarket penetration ranks among the world's highest. The region's retail density, combined with the convenience of purchasing multi-packs for home use, underscores this trend. However, on-trade outlets, spanning gyms, sports clubs, stadiums, and event venues, are projected to grow at an annual rate of 6.03% through 2031, outpacing the expansion of off-trade channels. This momentum is fueled by exclusive partnerships that position brands directly in front of consumers during peak purchase intent moments. For instance, iPRO's distribution deal with Al Rabie in Saudi Arabia ensures visibility in fitness centers and sports venues, capitalizing on consumers' heightened receptiveness to hydration messaging. Similarly, WOW Hydrate's collaborations with fitness influencers and gym chains in the United Arab Emirates bolster brand visibility, creating trial opportunities that lead to consistent off-trade purchases.

Among off-trade channels, online retail is emerging as the fastest-growing segment. Quick-commerce platforms like Talabat, Noon Minutes, Careem, Amazon Prime Now, and InstaShop, which guarantee delivery within 30 to 60 minutes, are driving this surge. These platforms democratize access for niche brands, allowing them to connect with urban consumers without the need for traditional retail shelf space. This shift not only fragments the competitive landscape but also fosters direct engagement with consumers. Supermarkets and hypermarkets continue to serve as the volume backbone, leveraging promotional depth and multi-pack formats to attract price-sensitive households. Meanwhile, convenience stores and petrol stations excel in capturing impulse purchases, especially for single-serve formats. Specialty stores, such as health food retailers and sports nutrition shops, cater to enthusiasts in search of premium or niche offerings, including protein-infused drinks and organic formulations.

By Functionality: Post-Workout Recovery Gains Momentum

Intra-workout consumption accounted for 58.04% of functional use cases in 2025, highlighting the established role of sports drinks in providing hydration and energy during physical activity. This segment's prominence stems from decades of marketing that links isotonic drinks to athletic performance and emphasizes their role in replenishing fluids and electrolytes lost through sweating. Forecasted to grow at an annual rate of 5.84% through 2031, post-workout drinks are set to outpace other functional segments. This growth is driven by the increasing popularity of protein-infused formulations and a focus on recovery-oriented messaging. Brands like iPRO, WOW Hydrate, and the Hype line, showcased at Gulfood 2025, are leveraging the critical 30-minute post-exercise window for muscle protein synthesis by combining protein, electrolytes, and amino acids. This shift aligns with a broader recognition in sports nutrition: recovery is essential for enhancing performance and preventing injuries.

Pre-workout drinks, while occupying a smaller niche, play a strategically significant role. They often overlap with energy drinks and supplements, delivering key ingredients like caffeine, beta-alanine, and nitric oxide precursors. The "others" category includes all-day hydration scenarios, from workplace consumption to non-exercise contexts, where consumers seek benefits like mental clarity or immune support. The growth of the post-workout segment is closely tied to the rising popularity of gym memberships and structured training programs in Saudi Arabia and the United Arab Emirates. Initiatives like Vision 2030 and the Dubai Fitness Challenge are normalizing regular exercise among previously sedentary populations. Brands that effectively educate consumers on recovery science, covering aspects like glycogen replenishment, muscle repair, and inflammation reduction, can command premium prices and foster loyalty that extends beyond the gym.

Geography Analysis

In 2025, the United Arab Emirates (UAE) secured 35.92% of the regional revenue, driven by its extensive retail network, high per-capita income, and a significant expatriate population with a preference for premium functional beverages. Dubai's strategic position as a logistics hub ensures efficient distribution across the GCC. Additionally, the UAE's dense network of gyms, sports clubs, and wellness centers supports a well-established on-trade channel. Initiatives such as the UAE's Walk 30 and the Dubai Fitness Challenge not only sustain demand for sports drinks but also provide opportunities for brand activations. With a tiered sugar tax set to be implemented in January 2026, brands like Gatorade, Reward Hydration, and AZRO are proactively introducing zero-sugar and reduced-sugar variants to avoid the highest tax tier.

Saudi Arabia is projected to achieve the fastest growth among major markets, with an annual growth rate of 5.96% through 2031. This growth aligns with the kingdom's Vision 2030 objective to increase sports participation from 13% in 2016 to 40% by 2030. This target is supported by a USD 10 billion investment in sports infrastructure, including 15 stadiums for the FIFA World Cup 2034, the Riyadh Sports Boulevard project, and the Qiddiya entertainment and sports complex. The February 2025 launch of iPRO through Al Rabie highlights the potential for premium, protein-focused products in the market. Saudi Arabia's tiered sugar tax, modeled after the UAE's framework, is driving reformulation efforts toward lower-sugar profiles, creating opportunities for brands capable of navigating regulatory complexities.

Qatar, while holding a smaller market share in 2024, benefits from event-driven demand spikes tied to the AFC Asian Cup 2027 and the Asian Winter Games 2029. Legacy infrastructure from the 2022 FIFA World Cup, including eight climate-controlled stadiums, provides year-round venues for tournaments and training camps, ensuring sustained on-trade opportunities. The "Rest of Middle East" segment, comprising Bahrain, Oman, and Kuwait, relies on cross-border distribution from Dubai and benefits from the GCC-wide harmonization of excise tax policies, which simplifies regulatory compliance for regional brands. Investments in cold-chain logistics in Saudi Arabia and the UAE are facilitating the rollout of protein-based formulations, although second-tier cities face challenges due to limited refrigerated retail capacity.

Competitive Landscape

The Middle East sports drinks market shows moderate consolidation, where multinational incumbents such as PepsiCo, Coca-Cola, Suntory, and Otsuka dominate the sports drinks market through their established brand equity, which fosters consumer trust during critical moments like workouts or events. These companies combine their global scale with strong retailer relationships, ensuring their products are widely available in supermarkets, convenience stores, and on-trade venues across the region, from Dubai malls to Riyadh stadiums. Exclusive bottling partnerships with regional players further enhance their distribution capabilities, creating a level of availability that smaller brands find difficult to match without significant long-term investment.

These market leaders capitalize on centralized research and development pipelines to introduce reformulated products such as Gatorade Zero for sugar-conscious consumers and Powerade Ultra for low-calorie hydration. This approach keeps their legacy isotonic lines relevant amid increasing demand for clean-label products. Their agility allows them to quickly adapt to regional trends, including preferences for zero-sugar options and protein-enriched beverages. Additionally, their bottling networks efficiently manage localization, such as flavor adjustments or Halal compliance, without disrupting supply chains. This strategic positioning strengthens their market dominance, as consumers continue to choose trusted brands despite rising prices driven by sugar taxes.

Regional challengers like WOW Hydrate and iPRO are targeting underserved niches by leveraging United Arab Emirates-based manufacturing to cater to Gulf-specific preferences, such as fruit-forward flavors and smaller PET sizes for gym-goers. WOW Hydrate’s local production enables faster product iterations, while iPRO’s planned February 2025 entry into Saudi Arabia, in partnership with Al Rabie, combines premium protein positioning with reliable local distribution to penetrate a market historically led by isotonic giants. These regional players differentiate themselves further through Halal certification and influencer-driven campaigns, appealing to digitally-savvy youth who prioritize authenticity over global branding. As the market evolves from volume-driven competition to functional segmentation, brands that align with specific consumer needs, such as protein recovery or zero-sugar hydration, are better positioned to succeed, creating opportunities for both established players and agile newcomers.

Middle East Sports Drinks Industry Leaders

-

PepsiCo, Inc.

-

The Coca-Cola Company

-

Suntory Holdings Limited

-

Otsuka Holdings Co., Ltd

-

Oshee Polska Sp. z.o.o.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: PepsiCo inaugurated its expanded Regional Headquarters (RHQ) for the Middle East in Riyadh’s King Abdullah Financial District (KAFD). At the event, it announced a SAR 30 million (USD 8 million) investment in a regional research and development center in Saudi Arabia. The center was planned to serve as a hub for product and packaging innovations in the GCC, featuring a culinary facility for prototype creation and product testing, along with an immersive sensory studio to gather consumer insights and adapt its product portfolio, including sports drinks, to regional preferences.

- February 2025: United Kingdom-based challenger sports hydration brand iPRO expanded into Saudi Arabia through a partnership with juice manufacturer Al Rabie. This collaboration, which included Al Rabie's co-branding on the packaging, enabled iPRO to access 21,000 outlets across Saudi Arabia. The product was made available in four flavors: berry mix, citrus blend, mango, and orange and pineapple.

- February 2024: The Roshn Saudi League (RSL) announced PepsiCo as its newest gold partner for the remainder of the current season and the full 2024-2025 season. Under this partnership, PepsiCo's key products were designated as the Official Water Partner (Aquafina), Official Soft Drinks Partner (Pepsi), Official Sports Drink Partner (Gatorade), and Official Potato Chips Partner (Lays). The collaboration aimed to enhance the match-day experience for fans.

Middle East Sports Drinks Market Report Scope

The Middle East Sports Drinks Market Report is Segmented by Soft Drink Type into Isotonic, Hypertonic, Hypotonic, Electrolyte-Enhanced Water, Protein-based Sport Drinks), Packaging Type (PET Bottles, Glass Bottles, Metal Can, Aseptic Packages, Disposable Cups), Distribution Channel (On-Trade, Off-Trade), Functionality (Pre-Workout, Intra-Workout, Post-Workout, Others), and Geography (UAE, Saudi Arabia, Qatar, Rest of Middle East). Market Forecasts are Provided in Terms of Value (USD).

| Isotonic |

| Hypertonic |

| Hypotonic |

| Electrolyte-Enhanced Water |

| Protein-based Sport Drinks |

| PET Bottles |

| Glass Bottles |

| Metal Can |

| Aseptic Packages (tetra pak, cartons, pouches) |

| Disposable Cups |

| On-Trade | |

| Off-Trade | Supermarket/Hypermarket |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail | |

| Other Distribution Channels |

| Pre-Workout |

| Intra-Workout |

| Post-Workout |

| Others |

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Rest of Middle East |

| By Soft Drink Type | Isotonic | |

| Hypertonic | ||

| Hypotonic | ||

| Electrolyte-Enhanced Water | ||

| Protein-based Sport Drinks | ||

| By Packaging Type | PET Bottles | |

| Glass Bottles | ||

| Metal Can | ||

| Aseptic Packages (tetra pak, cartons, pouches) | ||

| Disposable Cups | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarket/Hypermarket | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Functionality | Pre-Workout | |

| Intra-Workout | ||

| Post-Workout | ||

| Others | ||

| By Country | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Rest of Middle East | ||

Market Definition

- Carbonated Soft Drinks (CSDs) - Carbonated soft drinks (CSDs) refer to non-alcoholic beverages that are carbonated and typically flavored, containing dissolved carbon dioxide to create effervescence. These beverages commonly include cola, lemon-lime, orange, and various fruit-flavored sodas. Marketed in cans, bottles, or fountain dispense.

- Juices - We have considered packaged juices which encompass non-alcoholic beverages derived from fruits, vegetables, or a combination thereof, processed and sealed in various packaging formats such as bottles, cartons, or pouches. Excluding fresh juices, this market segment involves commercially prepared and preserved juices, often with added preservatives and flavors.

- Ready-to-Drink (RTD) Tea and RTD Coffee - Ready-to-Drink (RTD) tea and RTD coffee are pre-packaged, non-alcoholic beverages that are brewed and prepared for consumption without further dilution. RTD tea typically includes various tea varieties, infused with flavors and sweeteners, and comes in bottles, cans, or cartons. Similarly, RTD coffee involves pre-brewed coffee formulations, often mixed with milk, sugar, or flavorings, and is conveniently packaged for on-the-go consumption.

- Energy Drinks - Energy drinks are non-alcoholic beverages formulated to provide a quick boost of energy and alertness. Whereas, sports drinks are beverages designed to hydrate and replenish electrolytes, particularly after physical exertion, exercise, or intense activity

| Keyword | Definition |

|---|---|

| Carbonated Soft Drinks | Carbonated soft drinks (CSDs) are a combination of carbonated water and flavouring, sweetened by sugar or a non-sugar sweeteners. |

| Standard Cola | Standard Cola is defined as the original flavor of cola soda. |

| Diet Cola | A cola-based soft drink containing no or low amounts of sugar |

| Fruit Flavored Carbonates | A carbonated beverage prepared from fruit juice/fruit flavor with carbonated water and containing sugar, dextrose, invert sugar or liquid glucose either singly or in combination. It may contain peel oil and fruit essences. |

| Juice | Juice is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| 100% Juice | Fruit/vegetable juice made from fruit in the form of its juice with no water added to make up the volume. It is not permitted to add sugars, sweeteners, preservatives, flavourings or colourings to fruit juice. |

| Juice Drinks (up to 24% Juice) | Fruit/vegetable juice drinks with up to 24% fruits/vegetable extract. |

| Nectars (25-99% Juice) | Juices that can have between 25 and 99% of fruit, with the minimum legal limits defined depending on the type of fruit |

| Juice concentrates | Juice Concentrates are those form of juices when most of this liquid is removed resulting in a thick, syrupy product known as juice concentrate. |

| RTD Coffee | Packaged coffee beverages that are sold in a prepared form and are ready for consumption at the time of purchase. |

| Iced Coffee | An iced coffee is a cold version of coffee, usually a combination of hot espresso and milk with ice added to it. |

| Cold Brew Coffee | Cold brew also called cold water extraction or cold pressing is made by steeping ground coffee in room-temperature water for several hours. |

| RTD Tea | Ready-to-drink (RTD) tea is a packaged tea product ready for immediate consumption without brewing or preparation |

| Iced Tea | Ice tea or iced tea is a drink made from tea without milk but with sugar and sometimes fruit flavourings, drunk cold. |

| Green Tea | Green tea is a tea beverage which promotes mental alertness, relieving digestive symptoms and promoting weight loss. |

| Herbal Tea | Herbal tea beverages are made from the infusion or decoction of herbs, spices, or other plant material in hot water. |

| Energy Drink | A type of drink containing stimulant compounds, usually caffeine, which is marketed as providing mental and physical stimulation. They may or may not be carbonated and may also contain sugar, other sweeteners, or herbal extracts, among numerous possible ingredients. |

| Sugar-free or Low-calories Energy Drinks | Sugar-free or Low-calories Energy Drinks are sugar-free, artificially sweetened energy drinks with few or no calories. |

| Traditional Energy Drink | Traditional Energy Drinks are functional soft drinks containing ingredients designed to boost the consumer's energy. |

| Natural/Oraganic Energy Drinks | Natural/Organic energy drinks are energy drinks free of artificial sweeteners and synthetic colorings. Instead, they contain naturally derived ingredients such as green tea, yerba mate, and botanical extracts. |

| Energy Shots | A small but highly concentrated energy drink that contains large amounts of caffeine and/or other stimulants. The quantity is comparatively smaller compared to energy drinks. |

| Sports Drink | Sports drinks are beverages designed specifically for the rapid supply of fluid, carbohydrates, and electrolytes before, during or after exercise. |

| Isotonic | Isotonic drinks contain similar concentrations of salt and sugar as in the human body, and are designed to quickly replace fluids lost during exercise but with an increase of carbohydrate. |

| Hypertonic | Hypertonic drinks have a higher concentration of salt and sugar than the human body. They are best drunk after exercise as it is important to replace glycogen levels quickly after exercise. |

| Hypotonic | Hypotonic drinks are designed to quickly replace fluids lost during exercise. They have very low carbohydrate content and a lower concentration of salt and sugar than the human body. |

| Electrolyte-Enhanced Water | Electrolyte water is water infused with electrically-charged minerals, such as sodium, potassium, calcium, and magnesium. |

| Protein-based Sport Drinks | Protein-based sports drinks are those sports drinks which has added protein in it that will improve performance and reduce muscle protein breakdown. |

| On-Trade | The on-trade refers to places that sell beverages for immediate consumption on the premises like bars, restaurants, and pubs |

| Off-Trade | Off-trade usually means places like liquor stores, supermarkets and other places where you don't consume the beverage right away. |

| Convenience Store | A retail business that provides the public with a convenient location to quickly purchase a wide variety of consumable products and services, generally food and gasoline. |

| Specialty store | A specialty store is a shop/store that carries a deep assortment of brands, styles, or models within a relatively narrow category of goods |

| Online Retail | Online retail is a type of eCommerce whereby a business sells goods or services directly to consumers from a website. |

| Aseptic Packaging | Aseptic packaging refers to the filling of a cold, commercially sterile product under sterile conditions into a presterilized container and closure under sterile conditions to form a seal that effectively excludes microorganisms. These includes tetra packs, cartons, pouches etc. |

| PET Bottle | PET bottle means a bottle made of polyethylene terephthalate. |

| Metal Cans | Metal containers made of aluminum or tin- plated or zinc-plated steel, which are commonly used for packaging food, beverages or other products. |

| Disposable Cups | Disposable Cup means a cup or other container designed for single use to serve beverages, such as water, cold drinks, hot drinks and alcoholic beverages. |

| Gen Z | A way of referring to the group of people who were born in the late 1990s and early 2000s. |

| Millenial | Anyone born between 1981 and 1996 (ages 23 to 38 in 2019) is considered a Millennial |

| Taurine | Taurine is an amino acid that supports immune health and nervous system function. |

| Bars & Pubs | It is a drinking establishment licensed to serve alcoholic drinks for consumption on the premises. |

| Café | It is a foodservice establishment serving refreshments (mainly coffee) and light meals. |

| On the go | It means doing / dealing with while busily engaged with something and not diverting plans in order to accommodate. |

| Internet Penetration | The Internet Penetration Rate corresponds to the percentage of the total population of a given country or region that uses the Internet. |

| Vending Machine | A machine that dispenses small articles such as food, drinks, or cigarettes when a coin or token is inserted |

| Discount store | A discount store or discounter offers a retail format in which products are sold at prices that are in principle lower than an actual or supposed "full retail price". Discounters rely on bulk purchasing and efficient distribution to keep down costs. |

| Clean Label | Clean label on the beverage market are drinks that are made from few ingredients of natural origin and are not or only slightly processed. |

| Caffeine | An alkaloid compound which is a stimulant of the central nervous system. It is mainly used recreationally, as a mild cognitive enhancer to increase alertness and attentional performance. |

| Extreme sport | Action sports, adventure sports or extreme sports are activities perceived as involving a high degree of risk. |

| High-intensity interval training | It incorporates several rounds that alternate between several minutes of high intensity movements to significantly increase the heart rate to at least 80% of one's maximum heart rate, followed by short periods of lower intensity movements. |

| Shelf life | The length of time for which an item remains usable, fit for consumption, or saleable. |

| Cream Soda | Cream soda is a sweet soft drink. Generally flavored with vanilla and based on the taste of an ice cream float |

| Root Beer | Root beer is a sweet North American soft drink traditionally made using the root bark of the sassafras tree Sassafras albidum or the vine of Smilax ornata as the primary flavor. Root beer is typically, but not exclusively, non-alcoholic, caffeine-free, sweet, and carbonated. |

| Vanilla Soda | A carbonated soft drink flavoured with vanilla. |

| Dairy-Free | A product that does not contain any milk or milk products from cows, sheep or goats. |

| Caffeine-Free Energy Drinks | Caffeine-free energy drinks rely on other ingredients to boost the energy. Popular choices include amino acids, B vitamins, and electrolytes. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated reports, custom consulting assignments, databases & subscription platforms