Energy Supplements Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

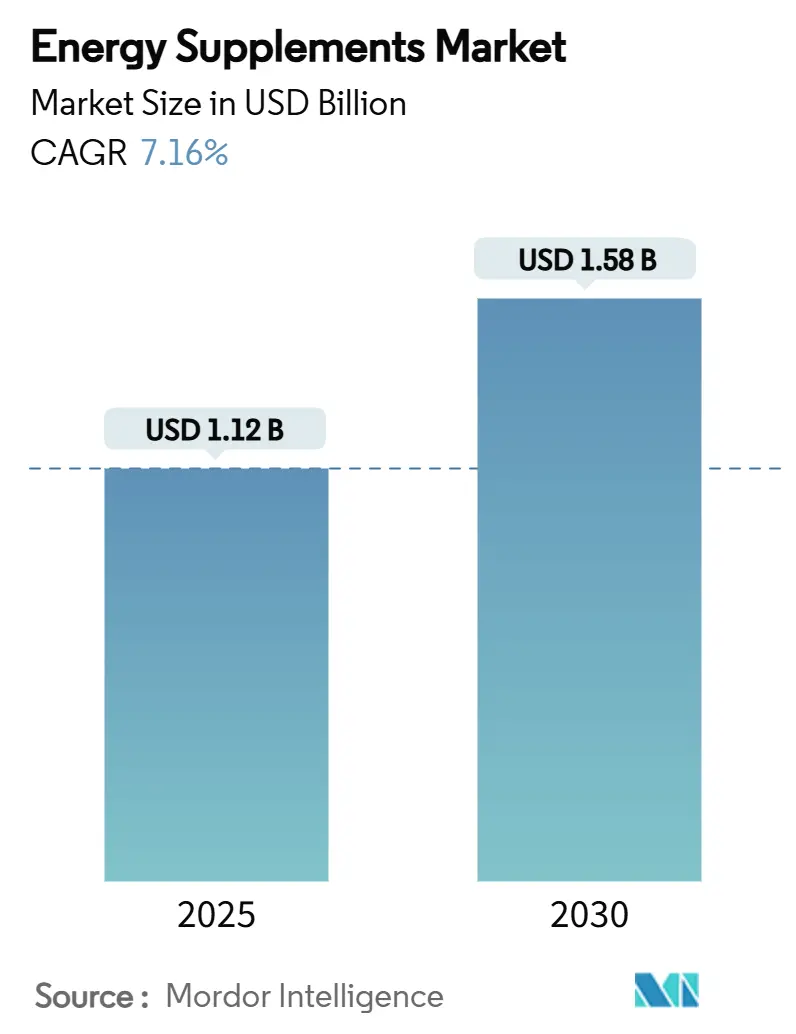

| Market Size (2025) | USD 1.12 Billion |

| Market Size (2030) | USD 1.58 Billion |

| Growth Rate (2025 - 2030) | 7.16% CAGR |

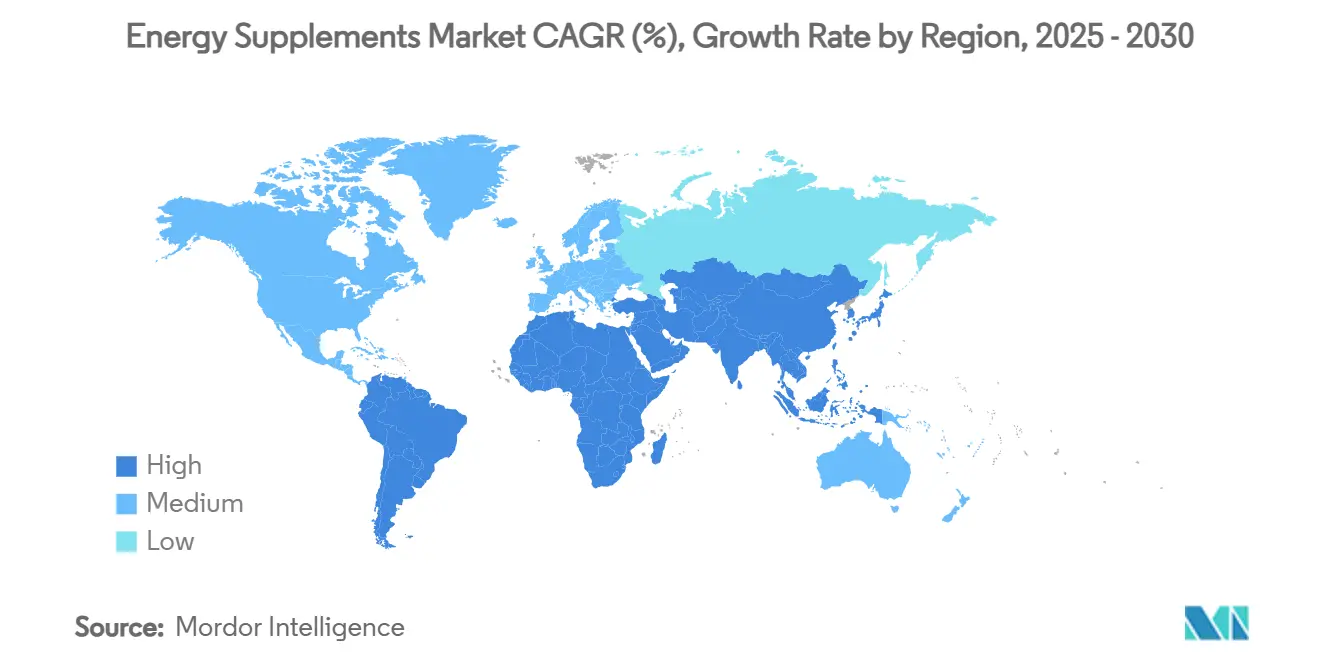

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

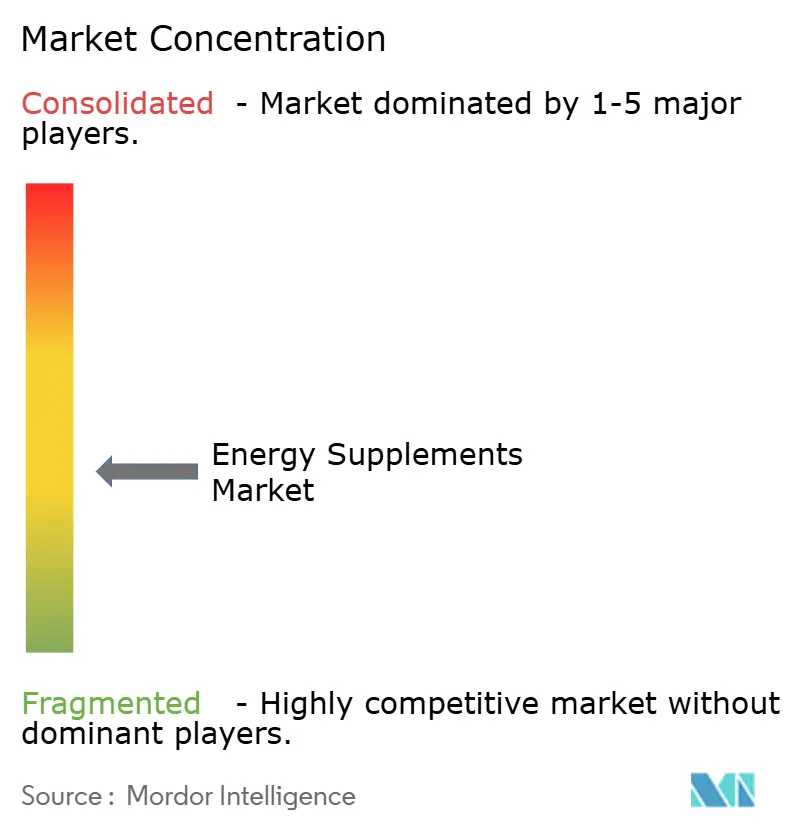

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Energy Supplements Market Analysis by Mordor Intelligence

The energy supplements market size, valued at USD 1.12 billion in 2025, is projected to grow to USD 1.58 billion by 2030, reflecting a CAGR of 7.16% during the forecast period. This growth is primarily driven by increasing consumer awareness of health and wellness, regulatory support for dietary supplements, and innovations in delivery technologies that improve product convenience and efficacy. North America remains the largest revenue contributor, but the Asia-Pacific region is emerging as the fastest-growing market, supported by rising disposable incomes, urbanization, and a growing fitness-oriented lifestyle. Consumer preferences are evolving, with stimulant-free botanical ingredients gaining traction alongside the sustained demand for caffeine-based products. Additionally, market consolidation is intensifying, as demonstrated by Keurig Dr Pepper’s acquisition of Ghost, emphasizing the growing importance of brand scalability, vertical integration, and a robust omnichannel presence as critical factors for competitive success.

Key Report Takeaways

- By nature, stimulant-based products held 71.34% of the energy supplements market share in 2024, while the stimulant-free segment is projected to advance at a 7.95% CAGR to 2030.

- By form, powders accounted for 34.87% of the energy supplements market size in 2024; gummies represent the fastest-growing format with 8.45% CAGR through 2030.

- By ingredient, caffeine captured 47.87% share of the energy supplements market size in 2024, whereas herbal/plant extracts are set to grow at 9.21% CAGR to 2030.

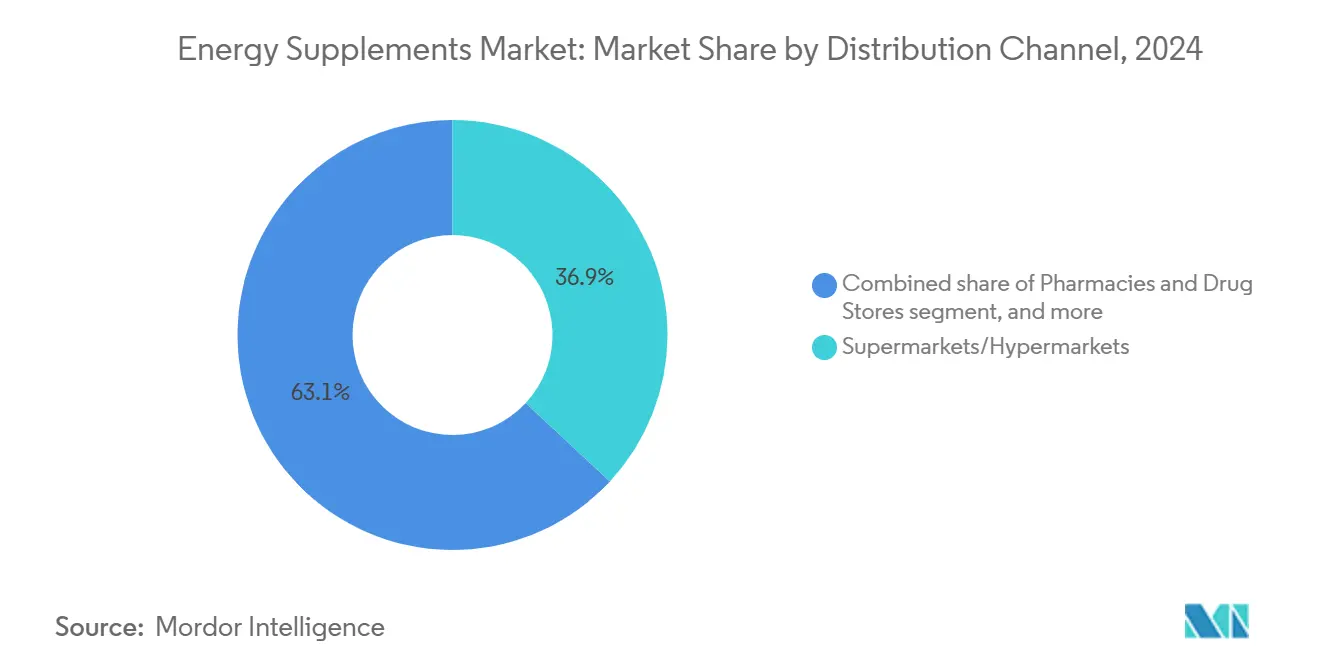

- By distribution channel, supermarkets/hypermarkets controlled 36.92% revenue in 2024, yet online retail is rising at 8.59% CAGR to 2030.

- By region, North America led with 39.21% of the energy supplements market share in 2024, while Asia-Pacific is forecast to expand at a 9.33% CAGR over the forecast period.

Global Energy Supplements Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding health and fitness culture among all age groups | +1.8% | Global, with strongest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Growth of e-commerce and digital platforms | +1.5% | Global, with accelerated adoption in emerging markets | Short term (≤ 2 years) |

| Increasing demand for multi-functional and fortified energy supplements | +1.2% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Product innovation and personalization | +0.9% | North America and EU core markets | Long term (≥ 4 years) |

| Influencer marketing and social media awareness | +0.7% | Global, with highest penetration in developed markets | Short term (≤ 2 years) |

| Growing niche for non-GMO, gluten-free, and allergen-free formulations | +0.6% | North America and EU, with spillover to urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding health and fitness culture among all age groups

The widespread adoption of fitness culture across various demographic groups is reshaping energy supplement consumption, broadening its appeal beyond traditional athletic users. The American College of Sports Medicine's 2025 Worldwide Fitness Trends report identifies wearable technology and mobile exercise apps as major drivers of this transformation. These innovations are fostering data-driven fitness ecosystems, making supplements more accessible and appealing to previously untapped consumer segments. This trend spans across generations, including older adults pursuing active lifestyles and Generation Z, who are seamlessly incorporating wellness into their daily routines. Additionally, the CDC's Healthy People 2030 initiative emphasizes increasing physical activity across all age groups, further supporting the use of supplements as tools to enhance performance and overall health[1]Centers for Disease Control and Prevention, "Healthy People 2030 Related to Physical Activity, Nutrition, and Obesity", www.cdc.gov. The integration of fitness tracking technology with personalized nutrition is creating new opportunities for developing tailored supplement formulations that align with individual metabolic needs and activity levels, driving growth in the market.

Growth of e-commerce and digital platforms

Digital commerce is reshaping the accessibility of energy supplements while intensifying regulatory oversight on online marketing practices. The FTC's Consumer Reviews and Testimonials Rule, which will take effect in October 2024, introduces civil penalties of up to USD 51,744 per violation for fake reviews. This regulation is compelling brands to prioritize genuine customer engagement strategies to maintain compliance and consumer trust[2]Federal Trade Commission, "The Consumer Reviews and Testimonials Rule: Questions and Answers", www.ftc.gov. Online retail stores are leading growth among distribution channels, with a CAGR of 8.59%, driven by the increasing adoption of direct-to-consumer models that bypass traditional retail markups, offering cost advantages to both brands and consumers. However, the FDA's recent warning letters to Amazon regarding adulterated supplements underscore the growing accountability of e-commerce platforms, signaling potential increases in compliance costs for operators in this space. In 2024, the United States emerged as the largest importer of health foods from China, supported by the rapid expansion of e-commerce platforms and stockpiling activities in anticipation of tariff changes. Meanwhile, the adoption of artificial intelligence in personalized nutrition platforms is creating new opportunities for competitive differentiation by offering tailored health solutions to consumers. However, the lack of well-defined regulatory frameworks for AI-driven health recommendations presents challenges, requiring the industry to navigate these uncertainties carefully while leveraging the technology's potential.

Increasing demand for multi-functional and fortified energy supplements

Consumer preferences are shifting toward advanced formulations that address multiple physiological needs in a single product, challenging the traditional single-ingredient supplement model. The NIH's All of Us Research Program, with over 834,000 participants as of August 2024, is generating critical insights into precision medicine. These insights, based on genetic and biomarker profiles, are driving the development of personalized, multi-functional supplements. Herbal and plant extracts are leading the market with the highest growth rate, recording a CAGR of 9.21%. This growth is fueled by scientific validation of adaptogenic compounds such as Ecdysterone and Turkesterone, which have shown promising benefits in enhancing sports performance and supporting metabolic health. The FDA's updated definition of "healthy" nutrient content claims, effective February 2025, will open new regulatory pathways for fortified supplements that meet specific food group requirements and nutrient limits. Furthermore, research on Indonesian plants has identified 25 species, particularly from the Zingiberaceae and Lamiaceae families, known for their energy-boosting properties. This discovery broadens the ingredient options for developing innovative multi-functional formulations.

Product innovation and personalization

Technological advancements are revolutionizing energy supplements, shifting them from standardized products to personalized health solutions. The University of Illinois, through its Personalized Nutrition Initiative, supported by over USD 170 million in funding from the NIH, is leading the development of genome-based nutrition technology. This innovation enables the creation of customized supplement recommendations tailored to individual genetic profiles and metabolic biomarkers, paving the way for precision nutrition. Gummy formulations are gaining traction as a promising delivery method, with research demonstrating their ability to effectively deliver bioactive compounds, such as ginger extract and B-vitamins, through stable gelatin matrices. These formulations not only enhance the stability of active ingredients but also improve consumer adherence due to their convenience and palatability. The personalized nutrition market is projected to experience robust growth by 2030, driven by increasing consumer demand for tailored health solutions. However, regulatory uncertainties pose significant challenges. These challenges, in turn, create opportunities for early adopters who can establish compliant and transparent frameworks for personalized recommendations. Biomarker-guided supplementation is emerging as a key differentiator in this market. To capitalize on this trend, companies must invest in advanced data analytics to interpret complex biomarker data and develop expertise in navigating evolving regulatory landscapes. By addressing these challenges, businesses can position themselves as leaders in the growing personalized nutrition market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Risk of adulteration and quality issues | -1.4% | Global, with highest impact in emerging manufacturing regions | Short term (≤ 2 years) |

| Inconsistent regulatory standards | -0.8% | Global, with particular challenges in cross-border trade | Medium term (2-4 years) |

| Supply chain vulnerabilities | -0.6% | Global, with concentration risks in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Allergen and ingredient sensitivities | -0.4% | North America and EU, expanding awareness globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Risk of adulteration and quality issues

Quality control failures in the global supply chain continue to weaken consumer trust and prompt regulatory actions, which hinder market growth. In 2024, the FDA issued several warning letters for violations of Current Good Manufacturing Practices. For example, Top Health Manufacturing LLC was cited for not adhering to quality control procedures and failing to establish necessary specifications for finished products[3]U.S Food and Drug Administration, "Top Health Manufacturing, LLC", www.fda.gov. A significant concern arose when certain tejocote root supplements were found contaminated with toxic yellow oleander, leading the FDA to warn about severe health risks, including neurologic, gastrointestinal, and cardiovascular effects. Additionally, the discovery of undeclared pharmaceutical ingredients, such as diclofenac and omeprazole, in products marketed as dietary supplements revealed sophisticated adulteration methods that exploit gaps in regulations. International manufacturing facilities are also under increased scrutiny. For instance, Kilitch Healthcare India Limited received warning letters for unsanitary conditions and inadequate aseptic practices. However, the FDA's decision to reduce its workforce in 2025, including cutting 170 positions from the Office of Inspections and Investigations, could inadvertently increase compliance risks. With fewer resources for surveillance, the agency may face challenges in maintaining oversight, even as it continues to enforce regulatory standards.

Inconsistent regulatory standards

Fragmented regulatory frameworks across jurisdictions create significant compliance challenges, driving up operational costs and restricting market access, particularly for smaller manufacturers. The European Food Safety Authority's updated Novel Foods guidance, effective February 2025, introduces stringent requirements for safety assessments and consumption data. These demands could overwhelm the resources of emerging supplement companies, potentially delaying or preventing their market entry. In Australia, the Therapeutic Goods Administration plans to reclassify vitamin B6 supplements exceeding 50mg as "pharmacist-only" medicines by February 2027. This proposed change illustrates how evolving safety standards can lead to product reclassification, disrupt distribution channels, and alter market dynamics. Similarly, the Netherlands Food and Consumer Product Safety Authority has recommended the adoption of supplement notification systems, citing that over 60% of certain supplements contain regulated pharmacological substances. This recommendation reflects the growing focus on regulatory oversight to ensure consumer safety. In the United States, the FDA's proposed mandatory dietary supplement product listing marks a significant regulatory shift. While this initiative aims to enhance transparency and oversight, it also introduces additional administrative burdens, which could disproportionately impact smaller manufacturers struggling to meet compliance requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Efficiency Versus Gummy Convenience Revolution

In 2024, powders hold the largest market share at 34.87%, driven by their cost efficiency, dosing flexibility, and formulation versatility. These advantages make powders popular among fitness enthusiasts and cost-conscious consumers. Their dominance is supported by manufacturing economies of scale, long shelf life, and the ability to include high-potency ingredients without technical limitations. Powders allow users to customize doses based on weight, tolerance, and performance goals, appealing to experienced users who value transparency, cost-effectiveness, and the ability to mix products. However, challenges like inconvenience and taste limit their appeal among casual users and younger demographics, who prefer ease of use. Industry organizations, such as the American Herbal Products Association, emphasize the need for strict manufacturing practices to ensure quality and prevent contamination in powder supplements.

Gummies are the fastest-growing format, with an 8.45% CAGR projected through 2030, reflecting a shift toward convenience, taste, and user-friendly experiences. This growth is fueled by younger and casual users who prioritize palatability and ease of consumption over cost. Research confirms gummies as effective delivery systems, successfully incorporating bioactive compounds like ginger extract and B-vitamins to improve compliance. Innovations, such as Specnova's NovaQSpheres encapsulation technology used in The Vitamin Shoppe's BodyTech Elite Creatine Beadlets, address stability and taste challenges while maintaining convenience. Consumers' willingness to pay a premium for gummies creates growth opportunities, though manufacturers must balance ingredient potency with taste and stability. Studies show that sensory experience significantly influences purchase decisions, offering brands a chance to combine functionality with enjoyable consumption.

By Ingredient Type: Caffeine Dominance Challenged by Botanical Innovation

In 2024, caffeine holds a significant 47.87% market share due to its proven effectiveness, regulatory clarity, and widespread use in energy supplements across various formats. Its well-researched pharmacokinetics, predictable effects, and strong safety profile provide manufacturers with confidence in formulation and compliance. Caffeine's flexibility allows its inclusion in diverse products, from powders to gummies, ensuring consistent performance and consumer satisfaction. However, market saturation has pushed manufacturers to innovate with proprietary blends, sustained-release systems, and combinations that enhance benefits while reducing side effects. Growing concerns about sleep disruption and tolerance have further driven the need for advanced formulations, such as time-release technologies and combinations that maintain effectiveness while minimizing peak concentrations.

Herbal and plant extracts are projected to grow at the fastest rate, with a 9.21% CAGR through 2030, driven by increasing consumer demand for natural, multifunctional ingredients supported by traditional and scientific validation. This trend reflects a shift toward holistic wellness, favoring botanicals with adaptogenic, nootropic, and metabolic benefits. Research in Indonesia has identified 25 energy-boosting plant species, particularly from the Zingiberaceae and Lamiaceae families, expanding options for natural energy formulations with cultural and scientific credibility. The U.S. Pharmacopeia highlights the historical importance and growing validation of Pan American botanicals in dietary supplements, providing clear regulatory pathways for innovation. Advances in extraction and standardization technologies ensure consistent potency and bioavailability, addressing past concerns about variability. Additionally, the premium pricing potential of scientifically validated botanicals offers attractive margins for manufacturers investing in research and compliance.

By Distribution Channel: Traditional Retail Leadership Meets Digital Disruption

In 2024, supermarkets and hypermarkets hold the largest market share at 36.92%, driven by their widespread presence, convenience, and integration of supplements into routine grocery shopping. These retailers offer one-stop shopping, competitive pricing through bulk purchasing, and trusted brands, ensuring consistent product availability. Major players like Walmart and Target cater to mainstream consumers who value familiar environments and the ability to physically inspect products. However, limited shelf space restricts variety, and standardized pricing limits premium product positioning. Retail partnerships, as highlighted by the National Association of Chain Drug Stores, play a key role in improving accessibility and consumer education, especially for health-focused products like energy supplements. Additionally, private label programs are gaining traction, leveraging retailer brand equity for better margins, which pressures branded manufacturers to differentiate through value and consumer preference.

Online retail stores are the fastest-growing channel, with an 8.59% CAGR through 2030, driven by direct-to-consumer models, personalized shopping, and data-driven engagement. This channel now includes subscription services, tailored recommendations, and educational content, fostering loyalty and increasing customer lifetime value. The FTC's Consumer Reviews and Testimonials Rule, effective October 2024, benefits brands with authentic testimonials but adds compliance costs, favoring established companies. Meanwhile, FDA warnings to Amazon about adulterated supplements highlight stricter platform accountability, benefiting brands with strong quality controls. AI integration in online platforms enables personalized recommendations based on health profiles and purchase history, though regulatory frameworks for AI-driven health advice remain underdeveloped. Subscription models are particularly effective for energy supplements due to regular consumption, offering predictable revenue and stronger customer retention for brands with effective engagement strategies.

By Nature: Stimulant Dominance Meets Clean Energy Innovation

In 2024, stimulant-based energy supplements hold a dominant 71.34% market share, driven by widespread consumer reliance on caffeine for quick and effective energy boosts. Caffeine's proven mechanisms, such as blocking adenosine receptors and stimulating the central nervous system, ensure rapid energy enhancement. Regulatory support from the European Food Safety Authority, which deems up to 400mg of daily caffeine intake safe for healthy adults, further strengthens this segment. However, concerns about tolerance, sleep disruption, and cardiovascular risks are pushing manufacturers to innovate. Companies are introducing sustained-release caffeine systems and combining caffeine with L-theanine to reduce side effects like jitters while maintaining energy benefits. As the segment matures, differentiation through advanced delivery systems, ingredient combinations, and targeted marketing becomes essential to stay competitive.

Stimulant-free energy supplements are experiencing the fastest growth, with a 7.95% CAGR projected through 2030. This growth is fueled by health-conscious consumers seeking energy solutions without the drawbacks of caffeine, such as sleep interference or nervous system stimulation. These products leverage alternative energy pathways, including mitochondrial support, blood glucose regulation, and stress response modulation. Research highlights the efficacy of ingredients like Panax Ginseng extract, which lowers fasting blood triacylglycerides and reduces oxygen consumption during exercise without caffeine's side effects. Additionally, the FDA's approval of D-ribose as safe for daily intake up to 36mg/kg body weight expands formulation opportunities for cellular energy support. Educating consumers is critical for this segment, as stimulant-free products deliver energy differently, with slower onset times compared to caffeine. The potential for premium pricing on scientifically validated ingredients offers manufacturers strong profit margins, provided they invest in research and consumer awareness initiatives.

Geography Analysis

In 2024, North America holds a 39.21% market share, driven by a strong fitness culture, clear regulations, and high disposable incomes supporting premium product adoption. The region benefits from mature market characteristics, including advanced consumer segmentation, robust distribution networks, and balanced regulatory frameworks that encourage innovation while ensuring safety. The FDA's 2025-2029 strategic plan focuses on advancing dietary supplement science through coordinated research, fostering market growth, and building consumer trust. However, market saturation among core demographics highlights the need to target underserved groups, such as aging populations and ethnic communities with specific nutritional needs. The Biden-Harris Administration's goal to end hunger and reduce diet-related diseases by 2030 supports functional nutrition products like energy supplements. In trade, the U.S. emerged as the top importer of China's health foods in 2024, with tariff-related stockpiling causing temporary demand spikes.

Asia-Pacific is the fastest-growing region, with a 9.33% CAGR through 2030, fueled by urbanization, rising incomes, and a shift toward Western wellness trends. Growth is driven by an expanding middle class, increasing health awareness, and government initiatives promoting fitness and preventive healthcare. Germany became the second-largest exporter of health foods to China in 2024, with exports rising 57.84% to USD 1.165 billion, reflecting the importance of regulatory reputation and quality. China's health food imports reached USD 7.75 billion in 2024, growing 15.1% due to rising domestic demand and a preference for international brands. However, regulatory complexity varies across the region. For example, Australia's stricter controls on vitamin B6 supplements contrast with more lenient policies elsewhere. While manufacturing concentration in Asia-Pacific improves supply chain efficiency, it also increases vulnerability, as seen in FDA warnings to several facilities for quality issues.

Europe is a mature market with strict regulations and a preference for natural, scientifically validated ingredients. The European Food Safety Authority's updated Novel Foods guidance, effective February 2025, requires detailed safety assessments, favoring established companies with regulatory expertise. The Netherlands Food and Consumer Product Safety Authority's push for supplement notification systems highlights growing scrutiny, with over 60% of certain supplements containing regulated substances. South America and the Middle East & Africa are emerging markets with low penetration but increasing awareness of energy supplements for active lifestyles. Despite challenges like infrastructure gaps and regulatory development, urbanization and fitness trends create opportunities for companies investing in local partnerships and market growth.

Competitive Landscape

The energy supplements market is moderately fragmented, with numerous regional and global players competing across various product formats, including powders, capsules, and ready-to-drink shots. Prominent players in the market include Glanbia plc, Herbalife Nutrition Ltd., PepsiCo Inc., Amway Corporation, and GNC Holdings LLC. The absence of a dominant market leader provides opportunities for niche brands and startups to establish themselves through innovative products and targeted marketing strategies.

This fragmentation is primarily influenced by diverse consumer preferences, which vary based on age, activity levels, and dietary requirements. Additionally, brands differentiate their offerings by focusing on factors such as natural ingredients, caffeine content, and specific functionalities. As a result, competition remains intense, with companies emphasizing advancements in product formulations and expanding their distribution networks to capture a larger market share.

Significant growth opportunities exist in areas such as personalized nutrition services, clean-label formulations, and catering to underserved demographic segments. However, capitalizing on these opportunities requires substantial investments in regulatory compliance, clinical validation, and consumer education. Emerging disruptors are reshaping the market by adopting direct-to-consumer models, subscription-based services, and data-driven personalization. These approaches allow them to bypass traditional distribution channels, deliver enhanced customer experiences, and achieve better profit margins.

Energy Supplements Industry Leaders

-

Glanbia plc

-

Herbalife Nutrition Ltd.

-

PepsiCo Inc

-

Amway Corporation

-

GNC Holdings LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Sneak has launched its new Energy Gummies, aiming to redefine the caffeine category by offering a convenient and tasty alternative to traditional energy products. According to the brand, these gummies provide a precise caffeine dose combined with added vitamins for sustained energy and focus, appealing to consumers seeking healthier and portable caffeine options.

- June 2025: ProZenith has expanded its product line by launching a new wellness supplement designed to help individuals maintain energy, focus, and mindful appetite awareness as part of a balanced and active lifestyle. The brand states that the supplement is manufactured in the United States in an FDA-registered and GMP-certified facility and is available through official online channels.

- September 2024: Factor has launched a new supplements brand called Factor Form. According to the brand, its all-in-one greens powder features 40 vitamins and superfoods that help fill nutrient gaps and support gut health, immunity, and boost energy and mood.

Global Energy Supplements Market Report Scope

| Stimulant-Based |

| Stimulant-Free |

| Powders |

| Capsules |

| Tablets |

| Gummies |

| Others (Strips, chews) |

| Caffeine |

| Amino Acids |

| Vitamin and Minerals |

| Herbal/Plant Extracts |

| Others |

| Pharmacies and Drug Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Nature | Stimulant-Based | |

| Stimulant-Free | ||

| By Form | Powders | |

| Capsules | ||

| Tablets | ||

| Gummies | ||

| Others (Strips, chews) | ||

| By Ingredient Type | Caffeine | |

| Amino Acids | ||

| Vitamin and Minerals | ||

| Herbal/Plant Extracts | ||

| Others | ||

| By Distribution Channel | Pharmacies and Drug Stores | |

| Supermarkets/Hypermarkets | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How large is the energy supplements market in 2025?

The energy supplements market size is USD 1.12 billion in 2025.

Which region is growing fastest for energy supplements?

Asia-Pacific is projected to grow at 9.33% CAGR through 2030, the highest of any region.

What ingredient type is expanding quickest?

Herbal and plant extracts are set to rise at 9.21% CAGR, topping the growth league.

Why are gummies gaining popularity in energy supplements?

Gummies deliver taste, portability, and dose flexibility, driving an 8.45% CAGR that outpaces all other formats.

Page last updated on: