Market Overview

| Study Period | 2021 - 2031 |

|---|---|

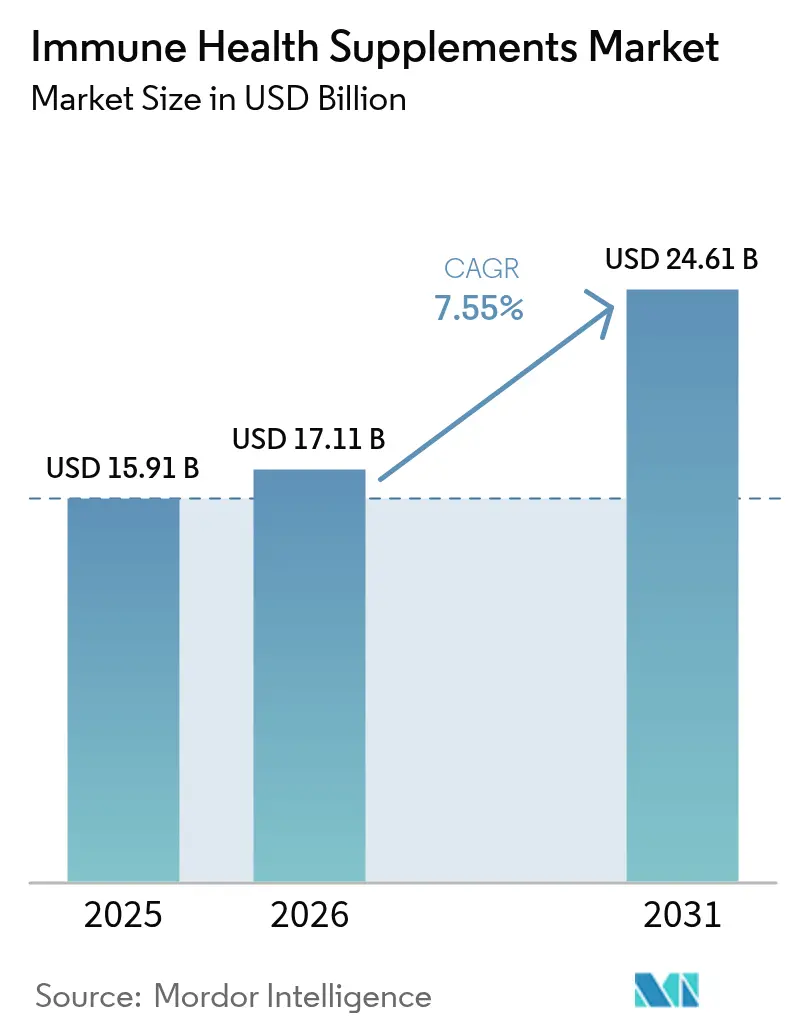

| Market Size (2026) | USD 17.11 Billion |

| Market Size (2031) | USD 24.61 Billion |

| Growth Rate (2026 - 2031) | 7.55% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Immune Health Supplements Market Analysis by Mordor Intelligence

The immune health supplements market size was valued at USD 15.91 billion in 2025 and estimated to grow from USD 17.11 billion in 2026 to reach USD 24.61 billion by 2031, at a CAGR of 7.55% during the forecast period (2026-2031). Preventive nutrition is increasingly seen as essential to healthcare, driving market growth. The focus on immune resilience, highlighted during the COVID-19 pandemic, continues to influence purchases. Vitamins and minerals lead the market, addressing diverse nutritional deficiencies, while probiotics gain traction due to their proven link to gut and immune health. Gummies and chewables are growing in demand for their convenience and appeal. Mature economies dominate revenue, but the Middle East and Africa and parts of Asia are experiencing rapid growth. The fragmented market offers opportunities for smaller players adept at managing supply chains, innovating delivery formats, or leveraging personalized nutrition trends.

Key Report Takeaways

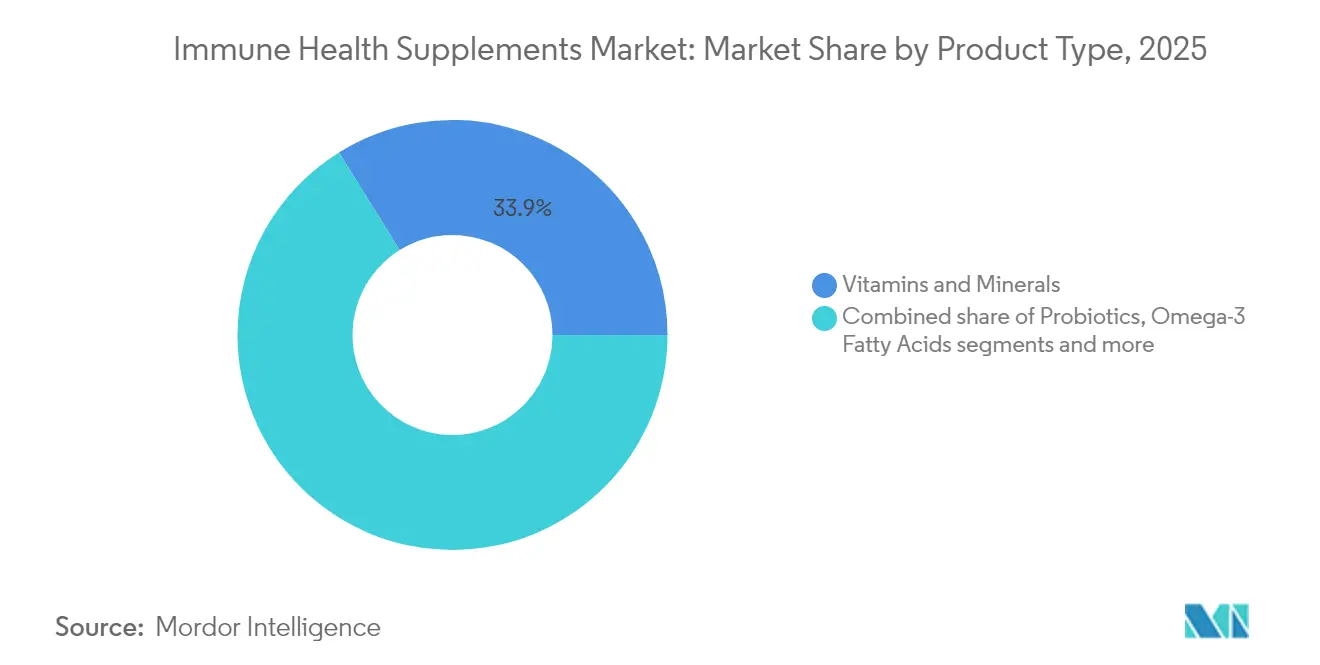

- By product type, vitamins and minerals held 33.85% of the immune health supplements market share in 2025, while probiotics are projected to expand at a 9.52% CAGR through 2031.

- By form, tablets commanded 31.20% share of the immune health supplements market size in 2025; gummies are the fastest-growing form at 8.55% CAGR to 2031.

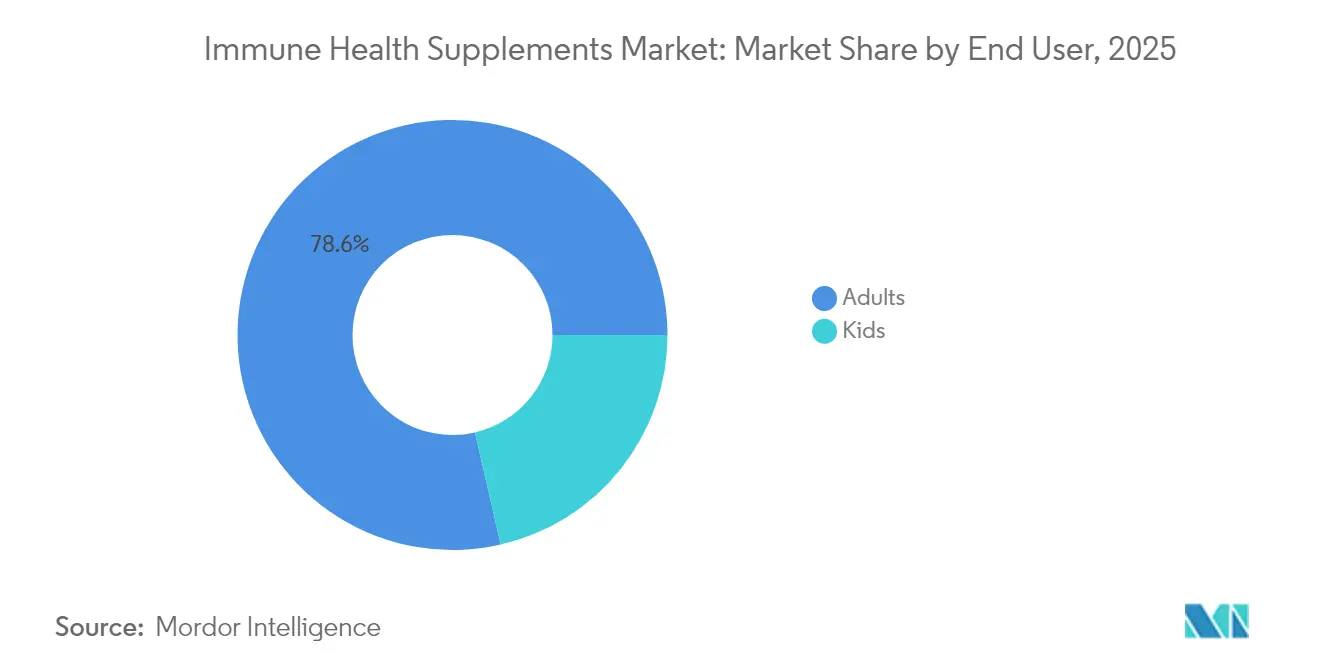

- By end user, adults captured 78.60% of the market share in 2025, with the kids segment projected to grow at a 9.04% CAGR through 2031.

- By distribution channel, specialty and health stores led with 40.75% revenue share in 2025, whereas online retail is set to grow at 7.78% CAGR during the forecast period.

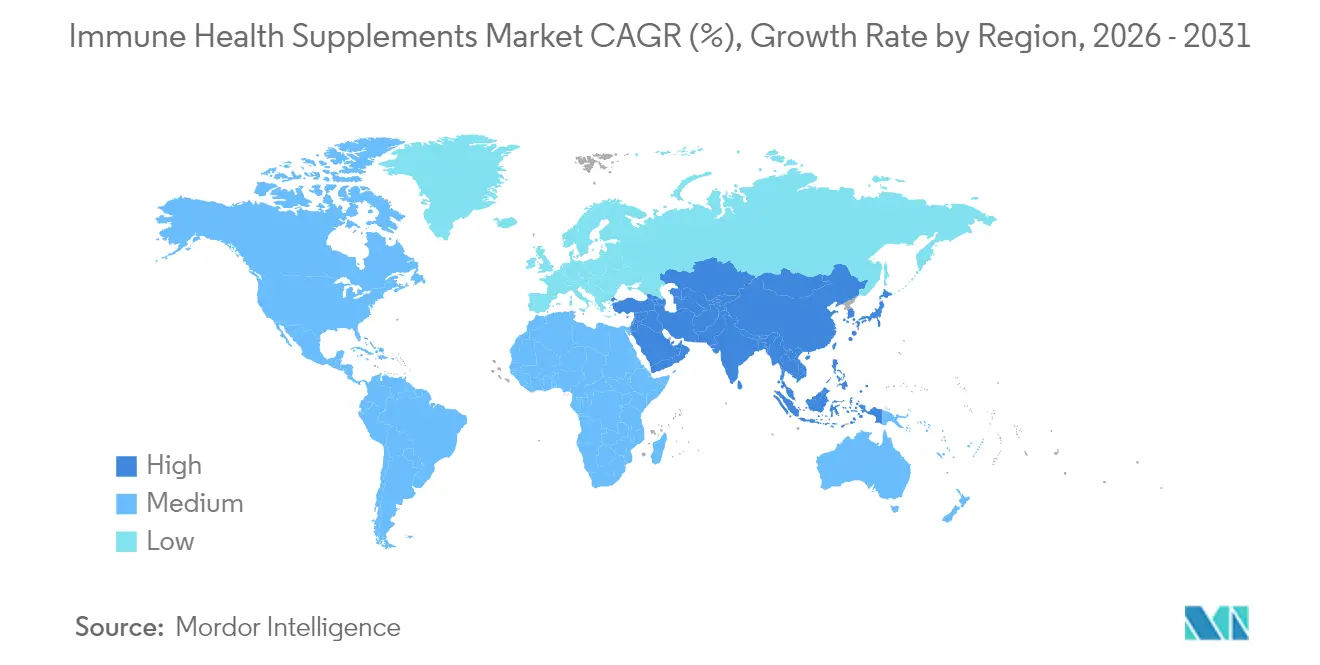

- By geography, North America accounted for 26.85% share of the immune health supplements market size in 2025, but the Middle East and Africa are advancing at 9.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Immune Health Supplements Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Enhanced focus on immunity post-covid-19 fueling market expansion | +1.8% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Aging populations globally seek immunity-boosting support | +2.1% | Global, particularly developed markets in North America, Europe, and the Asia-Pacific | Long term (≥ 4 years) |

| Chronic disease prevalence drives preventive supplement use | +1.5% | Global, with higher impact in developed markets | Long term (≥ 4 years) |

| Demand for personalized nutrition stimulates innovation | +0.9% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Social media influence increases consumer engagement | +0.7% | Global, strongest in digitally connected markets | Short term (≤ 2 years) |

| Scientific advancements and innovation | +1.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging populations globally seek immunity-boosting support

As individuals age, their immune systems weaken, a process called immunosenescence. To counter this, many seniors use supplements like zinc, vitamin D, probiotics, and antioxidants. The World Health Organization estimates the global population aged 60+ will grow from 1 billion in 2020 to 1.4 billion by 2030 and double to 2.1 billion by 2050, with those aged 80+ tripling to 426 million [1]Source: World Health Organization, "Ageing and health," who.int. This shift has increased supplement use among older adults. The NIH Office of Dietary Supplements has included research on aging-related supplements in its 2025-2029 strategic plan [2]Source: National Institutes of Health (NIH) Office of Dietary Supplements (ODS), ": ODS Publishes 2025–2029 Strategic Plan," ods.od.nih.gov. Manufacturers are addressing aging concerns like inflammation and metabolism with specialized products. For example, Abbott’s Ensure line, focused on adult nutrition, achieved USD 4.4 billion in sales in 2024, with 9% organic growth, as reported by the company.

Enhanced focus on immunity post-covid-19 fueling market expansion

Awareness of immune health has surged since the COVID-19 pandemic, with individuals, especially those with pre-existing conditions, taking proactive steps to improve their health. In 2024, the FDA expanded its Dietary Supplement Ingredient Directory, enhancing consumer trust and simplifying supplement selection [3]Source: Food and Drug Administration, "FDA Launches New Directory of Ingredients Used in Products Marketed as Dietary Supplements," fda.gov. As of June 2025, the World Health Organization reported 359,000 active COVID-19 cases globally, emphasizing the ongoing need for immune support [4]Source: World Health Organization, "COVID-19 Cases, World," who.int. Social media trends reveal strong commercial ties to immunity discussions, highlighting brand innovation and investment. These factors are driving demand for immune health supplements and fueling market growth.

Chronic disease prevalence drives preventive supplement use

As chronic conditions like diabetes and heart disease rise globally, there is a growing focus on preventive health through nutrient-rich supplements. In the Gulf states, addressing vitamin D deficiency is critical, as maintaining optimal levels (30 ng/mL) may reduce heart attack risks by 25%. Advances in gene-nutrition research highlight the superior benefits of personalized supplements over standard multivitamins. For instance, Herbalife's "Immunity Essentials," combining vitamin D3, zinc, and echinacea, targets adults with immune vulnerabilities due to lifestyle-related health issues. This shift toward prevention improves health outcomes and drives growth in the immune health supplements market by transitioning healthcare spending from treatments to proactive supplementation.

Demand for personalized nutrition stimulates innovation

The growing demand for tailored health solutions is driving innovation in the immune health supplements market. Advances in nutrigenomics enable brands to create products aligned with individual genetic differences. The American Nutrition Association highlights personalization as a key market trend. In 2024, Nestlé Health Science launched a GLP-1 nutrition support platform combining immune-boosting nutrients with weight-loss drug regimens to meet specific metabolic needs. Technologies like micro-encapsulation and precision-release systems enhance probiotic efficacy by ensuring survival through digestion. Personalized products are commanding premium prices, fueling growth and ensuring long-term market expansion.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Lack of standardized regulations across regions | -0.8% | Global, particularly affecting cross-border trade | Medium term (2-4 years) |

| High price sensitivity in developing markets | -1.2% | Asia-Pacific, Latin America, Africa | Long term (≥ 4 years) |

| Growing scrutiny of unverified health claims | -0.6% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Supply chain disruptions affecting raw material availability | -1.4% | Global, with highest impact in import-dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lack of standardized regulations across regions

Immune supplement manufacturers face challenges due to inconsistent regulatory standards across regions, which increase costs and delay product launches. For instance, the EU’s Food Supplements Directive 2002/46/EC aimed to unify regulations but allows member states to set their own rules, complicating launches. In the U.S., the FDA's 75-day premarket notification for New Dietary Ingredients adds complexity, especially for e-commerce-focused brands. Varying probiotic labeling rules globally further hinder standardized claims. These issues particularly burden smaller businesses, slowing innovation, hindering international expansion, and impacting the immune health supplements market's growth.

Supply chain disruptions affecting raw material availability

The immune health supplements market faces challenges in sourcing raw materials due to geopolitical tensions, environmental factors, and trade disruptions. China, a key supplier of ascorbic acid and botanical extracts, makes the market vulnerable to diplomatic conflicts and tariff changes expected by 2025. These issues have increased costs and delivery times. Climate events like the 2023 El Niño disrupted supply chains, with reduced anchovy catches temporarily spiking omega-3 prices due to limited fish oil. Companies are mitigating risks by diversifying sourcing, integrating vertically, and maintaining larger inventories. While these strategies stabilize supply chains, they raise operational costs, straining smaller businesses and impacting profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Scientific Progress Elevates Probiotics and Postbiotics

In 2025, vitamins and minerals led the immune health supplements market, contributing 33.85% of the revenue. Their popularity stems from their ability to address common nutrient deficiencies and their widespread acceptance by healthcare professionals. Meanwhile, probiotics are experiencing the fastest growth, with a projected CAGR of 9.52% through 2031. This rapid expansion is supported by clinical studies that highlight the benefits of specific probiotic strains in boosting upper respiratory immunity. Regulatory approvals, such as EFSA’s clearance of paramylon in 2024 and the FDA’s GRAS status for Bacillus subtilis NRRL 68053, have further enhanced consumer trust in probiotics. As a result, probiotics are expected to gain significant market share, gradually overtaking traditional multivitamins.

The market is also seeing a wave of innovation with the introduction of new ingredients like postbiotic metabolites, yeast-fermentate concentrates, and algae-derived beta-glucans. For instance, clinical studies on EpiCor have shown its effectiveness in reducing cold symptoms in children, making it a promising option for pediatric health. These advancements are supported by intellectual property protections, which help companies maintain a competitive edge and secure higher profit margins. As research expands to include broader health benefits, such as microbiome modulation in addition to traditional immune markers, the market continues to reward companies that invest in research and development.

By Form: Gummies and Chewables Bring Experience to Compliance

In 2025, tablets dominated the market with a 31.20% share. Their affordability, precise dosing, and convenience in combining multiple vitamins make them a top choice for consumers. Yet, gummies are on the rise, boasting a robust CAGR of 8.55%. Adults are increasingly opting for gummies due to their pleasant taste and seamless integration into daily routines. While leading brands like Church & Dwight have set the bar high, competition has surged with over 60 branded players entering the fray. In response to concerns about sugar content, brands have introduced reduced-calorie options, and pectin-based formulations are now catering to vegan consumers. Historically, gummies struggled with bioavailability, particularly for sensitive nutrients like probiotics and omega oils.

Capsules and softgels attract consumers who prioritize a pharmaceutical-grade experience and efficient delivery of fat-soluble nutrients. Powders, on the other hand, are the go-to choice in sports nutrition and elderly care, owing to their adjustable dosing and ease of use for those with swallowing challenges. This ongoing innovation in delivery formats empowers brands to address the diverse preferences of consumers spanning various age groups and lifestyles. Such diversification not only meets specific consumer needs but also cultivates strong loyalty within the expansive immune health supplements market.

By End User: Adult Demographics Anchor Demand While Pediatric Formulas Accelerate

In 2025, adults held 78.60% of the immune health supplements market share, driven by established supplement habits, financial capacity, and awareness of aging's impact on immunity. Studies show that combining vitamin D with N-acetylcysteine reduces cellular aging markers in vitamin D-deficient older adults. Additionally, 75% of individuals aged 65-80 fail to meet the recommended zinc intake, highlighting the demand for targeted products. Companies like Vitafusion cater to adult preferences with tailored formats and doses. However, rising competition in gummy supplements pushes brands to innovate in delivery methods and marketing.

The children’s segment is the fastest-growing in the immune health supplements market, with a projected CAGR of 9.04% through 2031. Growth is driven by parents adopting preventive health measures early. Improved formulations and scientific validation have increased pediatric supplement acceptance. For example, brands like SmartyPants and Zarbee’s are expanding their children’s lines with gummy-based multivitamins that include vitamins C, D, and zinc to support immunity. Innovations in delivery formats, such as dissolvable strips and chewables, are also gaining popularity among young users. This shift to pediatric products drives life-stage-specific offerings, fostering customer loyalty while addressing unique health and regulatory needs.

By Distribution Channel: Omnichannel Blurs Physical and Digital Borders

In 2025, specialty and health stores led the way in distributing immune health supplements, capturing 40.75% of the market's revenue. These stores are favored for their expert guidance and curated product selections. Yet, online retail is on the rise, boasting a 7.78% CAGR, as consumers increasingly gravitate towards the ease of home shopping. E-commerce's allure is heightened by features like same-day delivery and the ability to easily compare products. Direct-to-consumer websites harness customer data for tailored offerings, while online marketplaces thrive on customer feedback and rapidly changing inventories. Subscription services are also on the rise, striking a balance between consumer convenience and steady revenue for businesses. Supermarkets and hypermarkets play a pivotal role by offering budget-friendly choices and spurring impulse buys. However, their limited shelf space curtails product variety. Meanwhile, pharmacies, long trusted for their dependability, grapple with tightening profit margins. To navigate these challenges, innovative hybrid models are surfacing. These include click-and-collect services, in-store kiosks, and QR codes that deliver in-depth product insights and educational content. Such strategies meld the advantages of traditional shopping with the perks of online convenience. As the lines between distribution channels blur, companies are urged to hone their inventory management and bolster their digital footprint to stay ahead in the dynamic immune health supplements arena.

Geography Analysis

North America accounted for 26.85% of global revenue in 2025, driven by a strong culture of supplement use, high disposable incomes, and clear regulatory oversight from the FDA. Surveys from the National Institutes of Health (NIH) reveal that over 10% of U.S. adults specifically choose supplements for immune health. Canada and Mexico are also seeing steady growth, supported by integrated supply chains across North America, although potential tariff challenges remain. In Europe, spending on immune health supplements is comparable to North America, but the region faces varying regulations across member states. The European Food Safety Authority (EFSA) promotes trust with its evidence-based approach, allowing brands to position themselves as premium, though compliance costs remain a challenge. Countries like Germany, France, and the U.K. are seeing consistent demand for probiotic blends backed by clinical research, while Eastern Europe is gradually contributing to growth as disposable incomes rise and awareness about healthcare improves.

The Middle East and Africa is experiencing the fastest growth rate, with a CAGR of 9.07%, largely due to widespread vitamin D deficiencies and government-led initiatives promoting supplementation. Research in countries like Saudi Arabia and the UAE indicates that addressing vitamin D deficiencies could significantly reduce cardiovascular risks. Retailers in the region are aligning with local consumption habits by bundling immune health supplements with fortified dairy products and beverages. In the Asia-Pacific region, the combination of a large population and increasing urban stress is driving demand for immune health supplements. Countries like China and India are adopting products that blend traditional botanicals with modern nutrients, although affordability remains a key factor, leading to the popularity of sachets and stick-pack formats. Japan’s Food for Specified Health Use (FOSHU) system ensures scientific credibility, attracting a loyal customer base, particularly among older adults.

South America present long-term growth opportunities but face challenges such as currency fluctuations and weak regulatory enforcement, which can lead to counterfeit products entering the market. To address these issues, multinational companies are partnering with local distributors to navigate fragmented retail environments and educate consumers about the benefits of evidence-backed supplements. E-commerce is playing a significant role in breaking down geographic barriers, enabling even smaller, specialized brands to reach international customers. This trend is intensifying competition globally, as brands across regions strive to capture a share of the growing immune health supplements market.

Competitive Landscape

The immune health supplements market is highly fragmented, indicating significant opportunities for both established players and new entrants. Major global companies like Amway Corp., Bayer AG, Glanbia plc, NOW Foods, and Herbalife Nutrition Ltd dominate the market by leveraging their strong research and development capabilities and clinical research budgets. These companies focus on securing regulatory approvals and health claims to expand their product portfolios. For example, Abbott’s Ensure brand has successfully transitioned from medical-grade nutrition to mainstream consumer adoption, maintaining premium pricing.

Mid-sized companies are carving out their niche by innovating with new delivery formats like gummies, shots, and dissolvable strips, which appeal to younger demographics, including millennials and Gen Z. Church & Dwight, for instance, has expanded its range of immune-support gummies but faces growing competition from emerging brands that quickly replicate successful products. Meanwhile, digital-first brands are leveraging social media and subscription-based models to build direct relationships with consumers. These companies often rely on contract manufacturers to maintain flexibility and reduce operational costs.

Companies are also expanding their product offerings into related areas like gut-brain health, metabolic support, and healthy aging, creating opportunities to cross-sell alongside their core immunity products. The competitive landscape remains dynamic, with mergers, acquisitions, and licensing deals expected to increase as companies seek to scale operations and differentiate themselves through advanced scientific research in the immune health supplements market.

Immune Health Supplements Industry Leaders

-

Amway Corp.

-

Bayer AG

-

Glanbia plc

-

NOW Foods

-

Herbalife Nutrition Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Amway India expanded its nutrition portfolio with Nutrilite Triple Protect, a plant-based supplement featuring Acerola Cherry, Turmeric, and Licorice. The formulation supports immunity, reduces inflammation, and offers antioxidant protection for gut, skin, and immune health.

- March 2025: Kirin Holdings, in collaboration with its subsidiary Blackmores, launched an immune health supplement in Taiwan. The product, developed jointly by Kirin Holdings and its Australian subsidiary Blackmores, contains Kirin's proprietary LC-Plasma ingredient.

- March 2025: Nature Made has expanded its digestive health portfolio with new probiotic formulations and clinically studied products. The company introduced a comprehensive range of probiotic, prebiotic, and fiber supplements designed for daily gut health maintenance and immune system health support.

- September 2024: Airborne, a Reckitt brand, has introduced its most advanced immune support formula to date. The newly reformulated Effervescent and Chewable supplements feature increased levels of Zinc, added Vitamin D, and a high dose of Vitamin C, offering comprehensive immunity support ahead of the back-to-school season.

Global Immune Health Supplements Market Report Scope

Immune health supplements are dietary supplements containing vitamins, minerals, and other nutrients that support the body's immune system in fighting infections and diseases. Teh global immune health supplements market is segmented into product type, form, distribution channel and geography.

Based on product type, the market is segmented into vitamins & minerals, herbal/botanical extracts, probiotics, omega-3 fatty acids and others; by form, into capsules & softgels, tablets, gummies & chewables, powders and others; by distribution channel into supermarkets/ hypermarkets, specialty & health stores, online retailers, and other distribution channels. By geography, the market is segmented into North America (United States, Canada, Mexico, and Rest of North America), Europe (United Kingdom, Germany, France, Italy, Spaine, Russia, Netherlands, and Rest of Europe), Asia-Pacific (China, India, Japan, South Korea, Australia and Rest of Asia-Pacific), South America (Brazil, Argentina and Rest of South America), and Middle-East and Africa (Saudi Arbaia, United Arab Emirates, South Africa and Rest of Middle East & Africa).

By Product Type

| Vitamins and Minerals |

| Herbal/Botanical Extracts |

| Probiotics |

| Omega-3 Fatty Acids |

| Other Product Types |

By Form

| Capsules and Softgels |

| Tablets |

| Gummies and Chewables |

| Powders |

| Other Forms |

By End User

| Adults |

| Kids |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty and Health Stores |

| Online Retailers |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Vitamins and Minerals | |

| Herbal/Botanical Extracts | ||

| Probiotics | ||

| Omega-3 Fatty Acids | ||

| Other Product Types | ||

| By Form | Capsules and Softgels | |

| Tablets | ||

| Gummies and Chewables | ||

| Powders | ||

| Other Forms | ||

| By End User | Adults | |

| Kids | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty and Health Stores | ||

| Online Retailers | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the immune health supplements market?

The market is valued at USD 17.11 billion in 2026 and is projected to reach USD 24.61 billion by 2031 at a 7.55% CAGR.

Which product segment is growing fastest?

Probiotics lead growth with a 9.52% CAGR thanks to expanding clinical evidence linking gut flora and immunity.

Which region offers the highest growth rate?

The Middle East and Africa shows the fastest expansion at 9.07% CAGR, mainly due to widespread vitamin D deficiency and supportive public-health measures.

How fragmented is the industry?

The market is highly fragmented, with no single company holding a dominant share, leaving ample room for both multinationals and agile start-ups.

Page last updated on: