Market Overview

| Study Period | 2021 - 2031 |

|---|---|

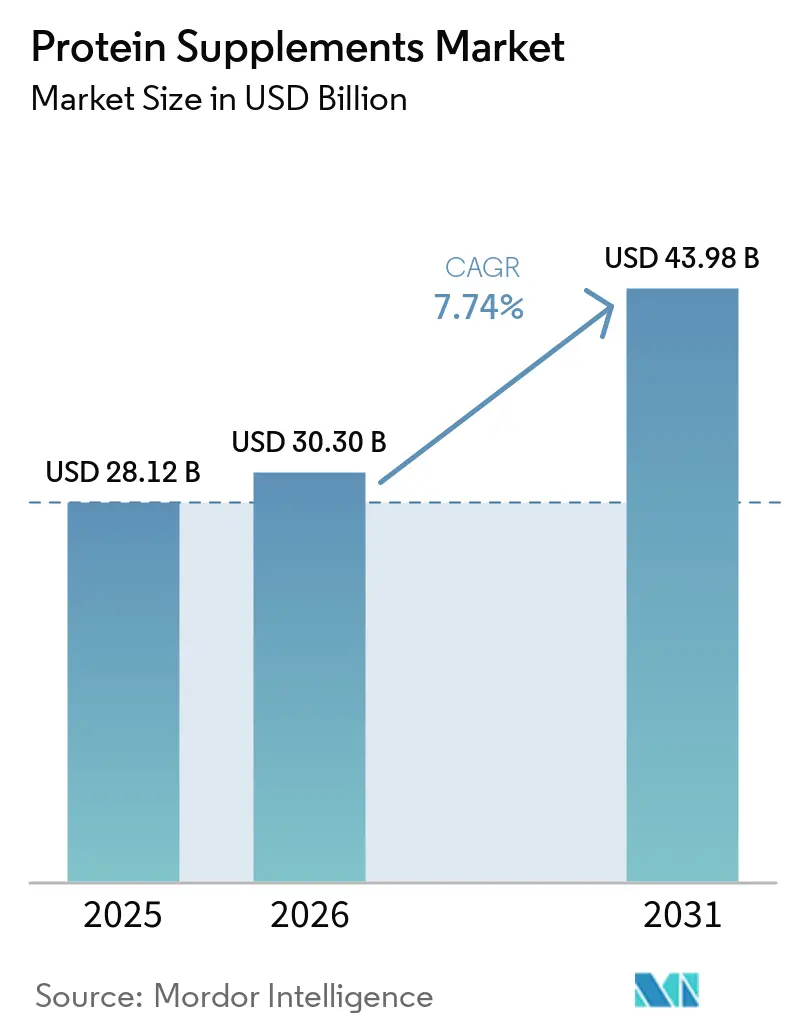

| Market Size (2026) | USD 30.30 Billion |

| Market Size (2031) | USD 43.98 Billion |

| Growth Rate (2026 - 2031) | 7.74% CAGR |

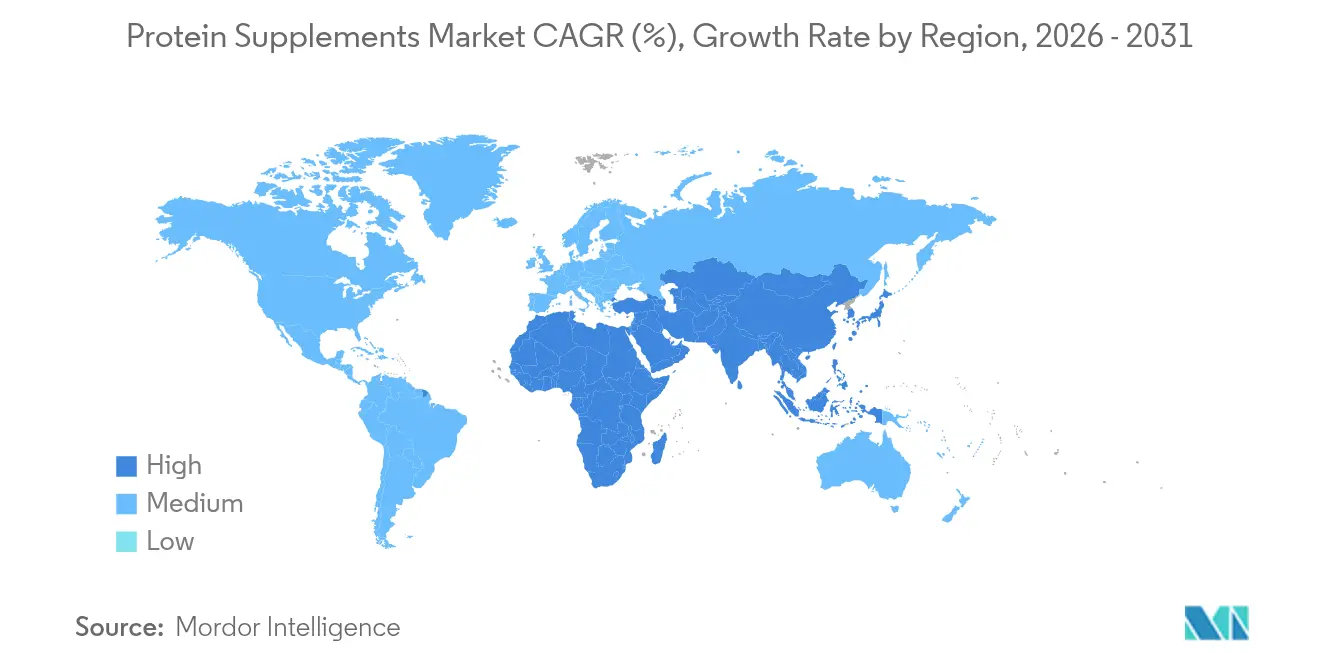

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Protein Supplements Market Analysis by Mordor Intelligence

The protein supplements market size was valued at USD 28.12 billion in 2025 and estimated to grow from USD 30.3 billion in 2026 to reach USD 43.98 billion by 2031, at a CAGR of 7.74% during the forecast period (2026-2031). Rising demand for convenient nutrition, expanding consumer bases beyond core athletes, and sustained product innovation in plant-based and ready-to-drink (RTD) formats anchor growth. Manufacturers in the protein supplements market are broadening ingredient portfolios, investing in cleaner labels, and re-engineering supply chains to secure high-grade raw materials. The global protein supplements market is witnessing a notable shift towards plant protein supplements and sustainable protein alternatives, reflecting broader environmental and ethical considerations. Plant-derived inputs benefit from improved taste and texture, animal-free production methods such as precision fermentation, and lower allergen risk. Meanwhile, channel evolution toward direct-to-consumer models is reshaping the competitive calculus, rewarding firms that excel at data-driven personalization and agile fulfillment.

Key Report Takeaways

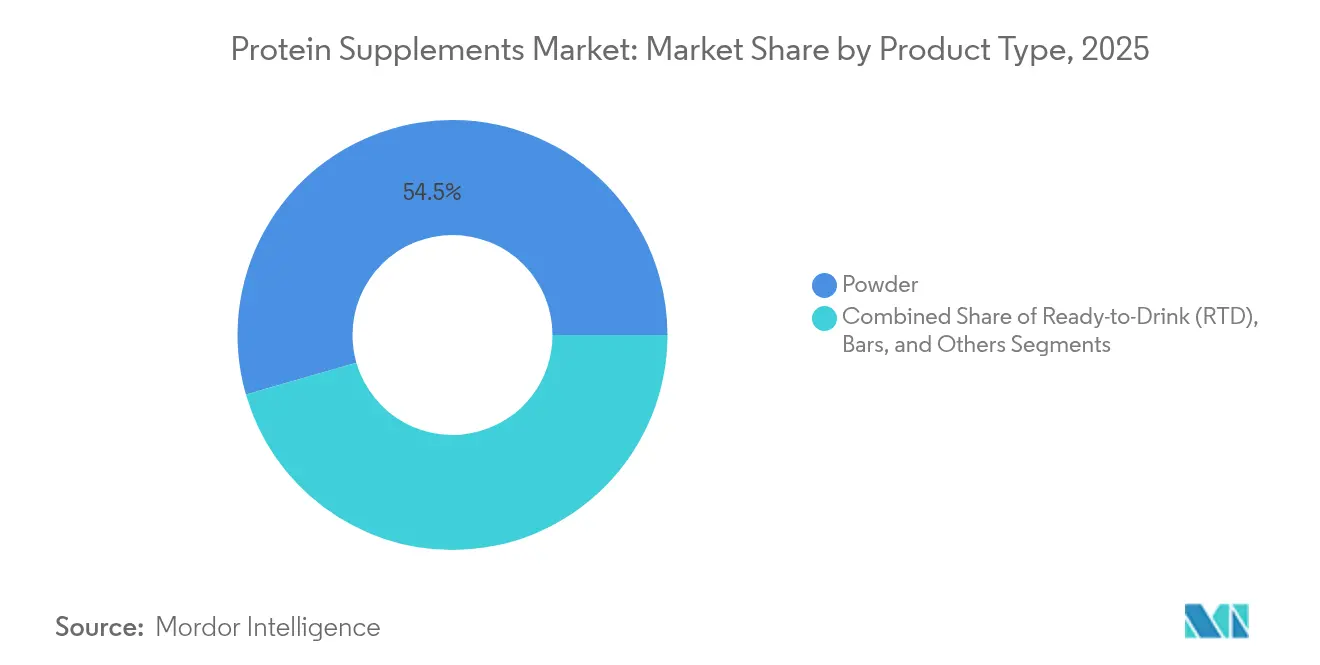

- By form, powder products retained 54.46% of the protein supplements market share in 2025, yet the RTD segment is set to expand at a 9.18% CAGR by 2031.

- By type, animal-based offerings accounted for 72.63% of the protein supplements market size in 2025, while plant-based alternatives are projected to grow at 8.53% CAGR through 2031.

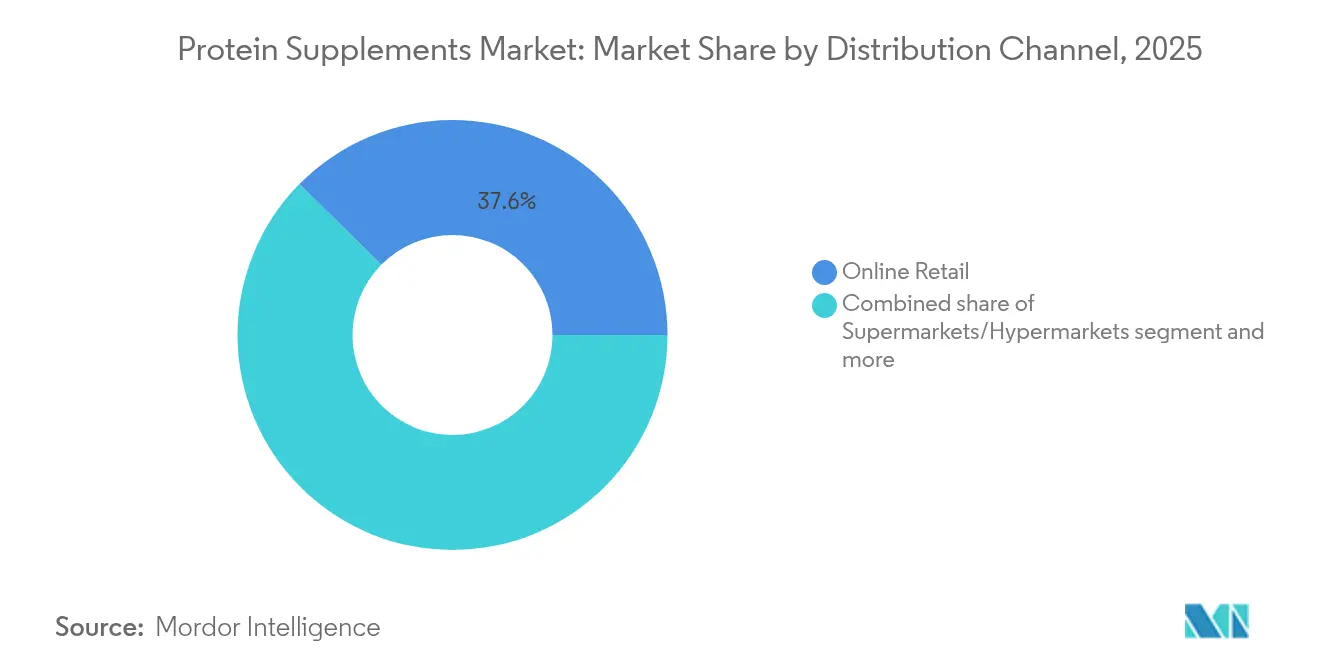

- By distribution channel, online retail commanded 37.62% of the protein supplements market share in 2025 and remains the fastest-growing route at 8.1% CAGR.

- By geography, North America led geographically with 62.25% protein supplements market share in 2025; Asia-Pacific is anticipated to post the highest 9.72% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Protein Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in fitness engagements and active living trends | +1.9% | Global, with higher impact in North America and Europe | Medium term (2-4 years) |

| Social media buzz and celebrity backing fuel market growth | +1.4% | Global, with significant impact in North America and Asia Pacific | Short term (≤ 2 years) |

| Sports sponsorships boost market presence | +0.9% | North America, Europe, and emerging markets in Asia Pacific | Medium term (2-4 years) |

| Consumers show increasing appetite for tailored nutrition | +1.6% | Global, with higher adoption in developed markets | Long term (≥ 4 years) |

| Tech innovations propel growth in plant-based and allergen-free proteins | +2.1% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) |

| Rising demand for convenient and on-the-go protein solutions | +0.9% | Global, with higher impact in urban markets and developed economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Fitness Engagements and Active Living Trends

The fitness industry's growth has expanded protein consumption beyond athletes to the general population, driven by increased health awareness and widespread accessibility of fitness resources through digital platforms, mobile apps, and traditional gyms. Gyms, boutique fitness studios, and digital fitness platforms have integrated comprehensive protein education programs that focus on daily intake requirements for muscle maintenance, metabolic health, and wellness goals, including personalized nutrition plans and expert consultations. According to the Health & Fitness Association (formerly IHRSA), the number of fitness facilities in the United States reached 55,000 in 2024, up from 31,028 in 2022, indicating substantial industry expansion[1]Source: Health & Fitness Association, "2024 Health and Fitness Association Economic Impact Study", ihrsa.org. Retailers in the protein supplements market have significantly increased dedicated shelf space for protein powders, ready-to-drink shakes, and protein bars while introducing specialized nutrition sections with diverse product offerings and nutritional guidance. Subscription-based protein delivery services have provided brands with predictable demand patterns and improved inventory management capabilities, offering consumers convenience, personalized nutrition options, and flexible delivery schedules tailored to individual needs. These market developments have established consistent year-round category growth, reducing seasonal fluctuations and creating a sustainable market for protein supplements across diverse consumer segments, from fitness enthusiasts to health-conscious individuals seeking balanced nutrition.

Social Media Buzz and Celebrity Backing Fuel Market Growth

Social media platforms, particularly TikTok and Instagram, are transforming the global protein supplements market by serving as comprehensive marketing channels where consumers engage with product content, participate in fitness challenges, and share supplement experiences. Cargill's 2025 Protein Profile indicates that 52% of consumers have tried new foods after seeing them on social media, highlighting these platforms' influence on purchasing decisions.[2]Source: Cargill, “2025 Protein Profile,” cargill.com Generation Z consumers are driving this trend through their adoption of diverse protein meals. The combination of celebrity endorsements and fitness influencer partnerships has strengthened product credibility and streamlined the discovery of new protein supplements. The protein supplements market has expanded beyond traditional fitness enthusiasts, with increased female consumer participation reshaping the previously male-dominated segment. This demographic expansion creates opportunities for brands that leverage social proof, user-generated content, and influencer collaborations to build consumer trust. Companies achieving success in the protein supplements market focus on developing sustainable purchasing patterns through authentic digital engagement, community building, and educational content, rather than pursuing temporary viral trends that generate short-term interest without establishing lasting consumer relationships.

Sports Sponsorships Boost Market Presence

Sports sponsorships drive growth in the protein supplements market by establishing direct connections with target audiences and building brand credibility through authentic athlete endorsements and performance demonstrations. These strategic partnerships effectively showcase product benefits in real athletic settings, emphasizing the fundamental connection between supplementation and enhanced sports performance. Athletes' regular usage and endorsements provide tangible validation of product effectiveness across various competitive environments. In March 2025, Optimum Nutrition partnered with the Royal Challengers Bengaluru (RCB) cricket team in India, launching a comprehensive campaign to promote fitness and nutrition awareness through multiple marketing channels and community engagement initiatives. The partnership includes a specially designed "Protein Choice of RCB" Gold Standard Whey product, supported by integrated digital marketing campaigns, strategic retail promotions, and targeted influencer partnerships across social media platforms. These sponsorships build long-term brand value and market development by creating sustained consumer engagement, fostering trust, and driving category growth through increased product visibility and credibility. Companies are actively exploring partnerships with emerging sports and athletes to establish distinctive market positions and expand into new consumer segments, particularly in regions where protein supplements are gaining mainstream acceptance and becoming culturally relevant for health-conscious consumers.

Tech Innovations Propel Growth in Plant-based and Allergen-free Proteins

Technological advancements in protein extraction, processing, and formulation are transforming the plant-based protein market by addressing key challenges in taste, texture, and nutrition. High-pressure processing (HPP) and pulse electric field (PEF) technologies improve protein solubility and functionality while preserving sensory qualities, enabling the development of competitive plant-based alternatives to animal products. Precision fermentation technology produces functional ingredients that replicate traditional proteins while reducing off-flavors and enhancing product quality. The implementation of AI in formulation optimization and consumer preference prediction reduces product development time and enables targeted innovation. These technological developments are crucial for creating allergen-free products, increasing accessibility for consumers with dietary restrictions. The combination of these technologies enables the production of plant-based proteins that match or exceed the nutritional value, taste, and functionality of animal-based products, influencing market dynamics during the forecast period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in counterfeit product growth | -1.2% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Price volatility of raw materials amid supply chain instabilities | -1.0% | Global, with significant impact on plant-based segment | Short term (≤ 2 years) |

| Adhering to regulatory frameworks and quality control norms | -0.8% | Global, with varying impact based on regional regulations | Medium term (2-4 years) |

| Health risks linked to overconsumption | -0.5% | Global, with higher impact in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Counterfeit Product Growth

The global protein supplements market faces significant challenges from counterfeit products, which contain inaccurate protein information and harmful contaminants. Laboratory tests on leading protein powders have identified critical issues, including incorrect protein content declarations, undisclosed fillers, artificial sweeteners, and dangerous microbial contamination. These tests also revealed the presence of heavy metals, banned substances, and substandard raw materials. In India, the rapidly expanding market has attracted unauthorized operators who distribute through third-party online platforms, particularly e-commerce marketplaces and social media channels, leading the Food Safety and Standards Authority of India to implement mandatory QR-based authentication. In response, manufacturers are implementing comprehensive security measures, including tamper-evident holographic seals, blockchain-based supply chain traceability systems, and unique product identification codes. Companies are also conducting extensive consumer awareness campaigns to educate buyers about identifying authentic products and purchasing through authorized distribution channels to ensure product safety and efficacy. Additionally, manufacturers are strengthening partnerships with authorized distributors and implementing rigorous quality control measures throughout their supply chains to combat the proliferation of counterfeit products.

Price Volatility of Raw Materials amid Supply Chain Instabilities

The protein supplements industry faces significant margin pressure due to raw material price volatility, particularly in whey protein prices, which affects pricing strategies and production planning. The fluctuating costs of whey protein concentrate, whey protein isolate, and other key ingredients have created challenges for manufacturers in maintaining consistent profit margins. This volatility extends to the plant-based segment, where variations in soy, pea, and rice protein prices impact manufacturers' pricing competitiveness. Supply chain disruptions, caused by geopolitical tensions and climate-related agricultural challenges such as droughts and floods, have created uncertainty in ingredient sourcing. The 2025 tariff implementation in the United States on imported products has increased production costs, leading manufacturers to explore nearshoring and alternative ingredient sources for risk mitigation. Companies with vertical integration or long-term supplier agreements have gained competitive advantages, as demonstrated by Nutrabolt's strategy of securing agreements for 70% of its purchasing volume to maintain cost stability. The persistent price pressures may lead to industry consolidation as smaller companies struggle with cost absorption, potentially transforming the competitive landscape during the forecast period, with larger companies likely acquiring regional players to expand market presence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: RTD Formats Reshape Consumption Patterns

In 2025, powder formulations commanded a dominant 54.46% share of the protein supplements market. Their popularity stems from cost-effective production, versatility in recipes from smoothies to baked goods, and longer shelf stability compared to liquids. Meanwhile, the ready-to-drink (RTD) segment is on track to expand at a robust 9.18% CAGR, driven by a growing consumer appetite for convenient nutrition. RTD products are especially favored by busy professionals and recreational athletes, offering them instant post-workout nutrition without the hassle of mixing or measuring. Protein bars, the third-largest segment, strike a balance between nutrition and indulgence, boasting precise portion control and innovative flavors.

Innovations in manufacturing, such as aseptic filling and mineral-based oxygen scavengers, have extended the shelf life of RTD products. These advancements eliminate the need for chemical preservatives, ensuring product integrity over time. Companies adeptly cater to varied consumer needs by offering both home-consumed powders and on-the-go RTD multipacks. This strategy not only boosts brand loyalty but also encourages repeat purchases. Sustainability plays a pivotal role in the RTD segment's ascent. Aluminum bottles, being lighter and infinitely recyclable, cut down transportation emissions. Simultaneously, fiber-based packaging aligns with retail plastic reduction goals and resonates with eco-conscious consumers. Moreover, advanced data analytics in flavor development has streamlined product creation, accurately predicting consumer preferences and minimizing unsuccessful launches. The protein supplements market thrives, adapting to evolving consumer tastes and lifestyle shifts.

By Type: Plant-Based Proteins Disrupt Traditional Dominance

Animal-based proteins maintain a commanding 72.63% market share in 2025, with whey protein continuing as the preferred choice due to its comprehensive amino acid profile and extensively documented effectiveness in muscle recovery and growth. The plant-based protein segment in the protein supplements market demonstrates substantial growth at 8.53% CAGR (2026-2031), propelled by increasing environmental consciousness, ethical considerations regarding animal welfare, and the widespread adoption of flexitarian dietary patterns. Within the plant-based category, soy protein maintains its leadership position, while pea protein experiences significant market penetration due to its hypoallergenic characteristics, balanced amino acid composition, and particular appeal among consumers with specific dietary sensitivities and restrictions.

Technological innovations are systematically addressing the traditional limitations in plant-based proteins, encompassing improvements in taste profiles, texture optimization, and enhanced bioavailability. Precision fermentation technology represents a significant advancement, enabling the production of proteins molecularly identical to animal-derived variants without conventional agricultural requirements. The market continues to expand through the strategic incorporation of diverse protein sources, including specialized varieties of lentils, chickpeas, and fava beans, each offering unique nutritional profiles and functional properties. This wave of technological advancement has generated substantial investment interest from both established food manufacturers and innovative startups, indicating robust long-term growth potential in the protein alternatives market.

By Distribution Channel: Online Retail Drives Market Accessibility

Digital storefronts hold 37.62% share of the protein supplements market in 2025 and are growing at an 8.1% CAGR. These platforms implement sophisticated product filters, third-party authenticity certifications, and detailed user reviews to build consumer trust and encourage first-time purchases. Direct-to-consumer websites increase sales through personalized product bundles and flexible subscription programs that generate predictable monthly revenue. Health and wellness specialty stores continue to drive sales through comprehensive educational approaches, with nutrition-certified staff providing in-depth guidance on ingredient sourcing, quality standards, and optimal dosage protocols. Independent natural product retailers show growth rates 4-6 times higher than mass-market retailers, indicating premium consumers prefer carefully curated product selections with verified quality standards.

Supermarkets strategically position ready-to-drink protein supplements near functional beverages in high-traffic areas to capture impulse purchases. Retailers combine interactive in-store product sampling experiences with integrated digital elements like QR codes linking to personalized online nutrition calculators to strengthen brand connections and consumer engagement. Success in the protein supplements market depends on real-time inventory management systems, strict temperature-controlled supply chains for ready-to-drink products, and streamlined return processes that maintain product integrity.

Geography Analysis

North America held 62.25% of global revenue in 2025, driven by an established fitness culture, high household spending, and integrated omnichannel retail. Ready-to-drink (RTD) beverages show double-digit growth as consumers prioritize convenience. Clear regulatory guidelines for protein claims enable product innovation, while the demand for personalized protein sachets benefits from advanced digital commerce systems. Companies use loyalty app data to optimize promotional strategies, resulting in higher customer retention.

The Asia-Pacific protein supplements market projects a 9.72% CAGR through 2031. Rising urbanization and growing middle-class populations increase nutrition spending, especially in China, India, Vietnam, and Indonesia. Arla Foods Ingredients expanded its presence across Vietnam, Indonesia, and Thailand in May 2025 to meet increasing whey demand from RTD and bar manufacturers. Companies develop region-specific flavors like matcha, black sesame, and mango lassi while maintaining halal and vegetarian certifications to build consumer trust.

Europe demonstrates stable growth with an emphasis on sustainability. Environmental concerns drive plant-based protein demand, with consumers focusing on carbon labeling and biodegradable packaging. EU regulations on health claims create market entry challenges but ensure product quality and consumer trust. Nordic markets lead in innovative ingredients, including barley-based protein concentrates. The UK shows high e-commerce adoption, while German drugstore chains offer comprehensive sports nutrition and wellness products. South America and the Middle East & Africa represent smaller but growing market segments. Brazil dominates South America through established gym culture and social media marketing, while Saudi Arabia benefits from young demographics and government fitness programs. Regional contract manufacturers collaborate with global brands to address local taste preferences and regulations, improving market entry speed and supply chain efficiency.

Competitive Landscape

The market demonstrates moderate competitive concentration with dynamic characteristics. Large global companies leverage economies of scale in dairy sourcing and diverse brand portfolios, while smaller competitors establish market presence through plant-based products, natural ingredients, and direct consumer relationships. Major companies expand their product lines into related categories, including hydration, cognitive enhancement, and recovery drinks, to increase market share. Some of the leading companies in the market include Glanbia plc, Abbott Laboratories, Nestlé S.A., PepsiCo Inc., and Post Holdings Inc.

Market opportunities exist in personalization services. New companies implement artificial intelligence systems to recommend protein formulations based on genetic data and lifestyle factors. Some businesses incorporate home blood testing to modify amino acid formulations quarterly, establishing subscription-based revenue streams and increasing customer retention. Supply chain verification systems, including blockchain technology and unique QR codes, help legitimate manufacturers differentiate themselves from counterfeit products while meeting consumer demands for ingredient transparency.

Precision fermentation technology emerges as a significant market development. Companies have introduced dairy-free whey proteins that match the amino acid composition of traditional dairy products without lactose or antibiotics. Major food companies have established investment funds to acquire rights to innovative protein startups, maintaining market relevance amid stricter environmental regulations.

Protein Supplements Industry Leaders

-

Glanbia plc

-

Abbott Laboratories

-

Nestle S.A

-

PesiCo Inc

-

Post Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Eat Just, Inc., a company developing sustainable food alternatives through scientific research, announced the launch of its Just One protein at the United States Whole Foods Market locations. Just One is produced from mung bean protein, which offers high nutritional value and environmental sustainability.

- March 2025: French precision fermentation company Bon Vivant has rebranded to Verley and launched its animal-free functional whey protein line, FermWhey. The rebranding reflects the company's international expansion plans and focuses on developing dairy alternatives for nutritional and performance applications.

- October 2024: REBBL has launched its 26g Protein Shakes at Target Stores in the United States. The ready-to-drink (RTD) protein shake contains a plant protein blend that is Upcycled Certified and Non-GMO Project Verified. The product aims to combine sustainability with high protein content in the beverage market.

- March 2024: Perfect Snacks launched a Perfect Bar line-up of refrigerated protein bars in Chocolate Brownie flavor. The new variant is a blend of freshly ground peanut butter, cashew butter, and cocoa, topped with dark chocolate chips. The new bar is claimed to be an organic and gluten-free brownie-flavored protein bar containing more than 20 superfoods as ingredients.

Global Protein Supplements Market Report Scope

Protein supplements are processed, refined protein products available in various forms, ranging from powders to bars to drinks. Athletes and individuals use these products extensively as dietary supplements to increase muscle mass, enhance recovery, and boost overall performance.

The global protein supplements market is segmented by form, source, distribution channel, and geography. By form, the market is segmented into powder, bars, ready-to-drink, and other forms. By source, the market is segmented into animal-based and plant-based. By distribution channel, the market is segmented into supermarkets & hypermarkets, online retail stores, health and wellness stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Form

| Powder |

| Ready-to-Drink (RTD) |

| Bars |

| Other Forms |

By Type

| Animal-Based | Whey |

| Casein | |

| Others | |

| Plant-Based | Soy |

| Pea | |

| Hemp | |

| Others |

By Distribution Channel

| Supermarkets and Hypermarkets |

| Health and Wellness stores |

| Online Retail |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Form | Powder | |

| Ready-to-Drink (RTD) | ||

| Bars | ||

| Other Forms | ||

| By Type | Animal-Based | Whey |

| Casein | ||

| Others | ||

| Plant-Based | Soy | |

| Pea | ||

| Hemp | ||

| Others | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Health and Wellness stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the protein supplements market?

The protein supplements market is valued at USD 30.3 billion in 2026 and is projected to reach USD 43.98 billion by 2031.

Which region leads global sales of protein supplements?

North America holds the largest share at 62.25% of 2025 revenue, supported by mature fitness culture and extensive retail coverage.

Which product form is growing fastest?

Ready-to-drink (RTD) beverages are expanding at a 9.18% CAGR for 2026-2031, outpacing powders and bars.

How quickly is the plant-based protein segment expanding?

Plant-based protein supplements are advancing at an 8.53% CAGR, the fastest rate among protein types through 2031.

Which sales channel delivers the highest growth?

Online retail is both the largest (37.62% share in 2025) and fastest-growing channel, rising at 8.1% CAGR on the strength of direct-to-consumer models.

Page last updated on: