Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 61.39 Billion |

| Market Size (2031) | USD 86.58 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

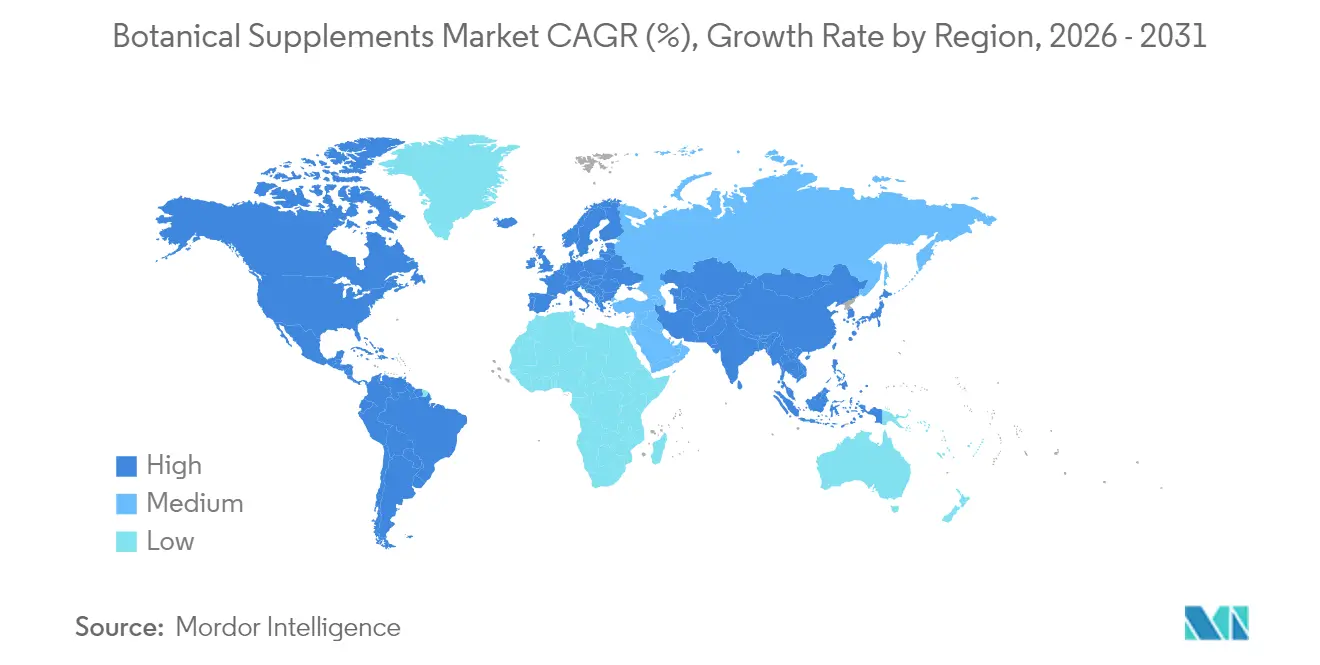

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

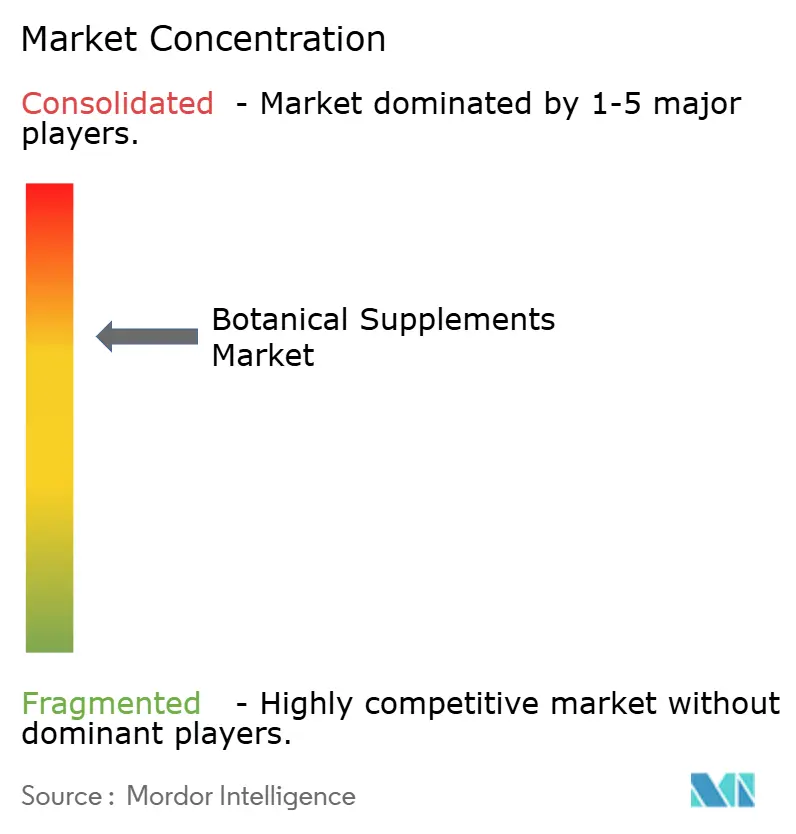

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Botanical Supplements Market Analysis by Mordor Intelligence

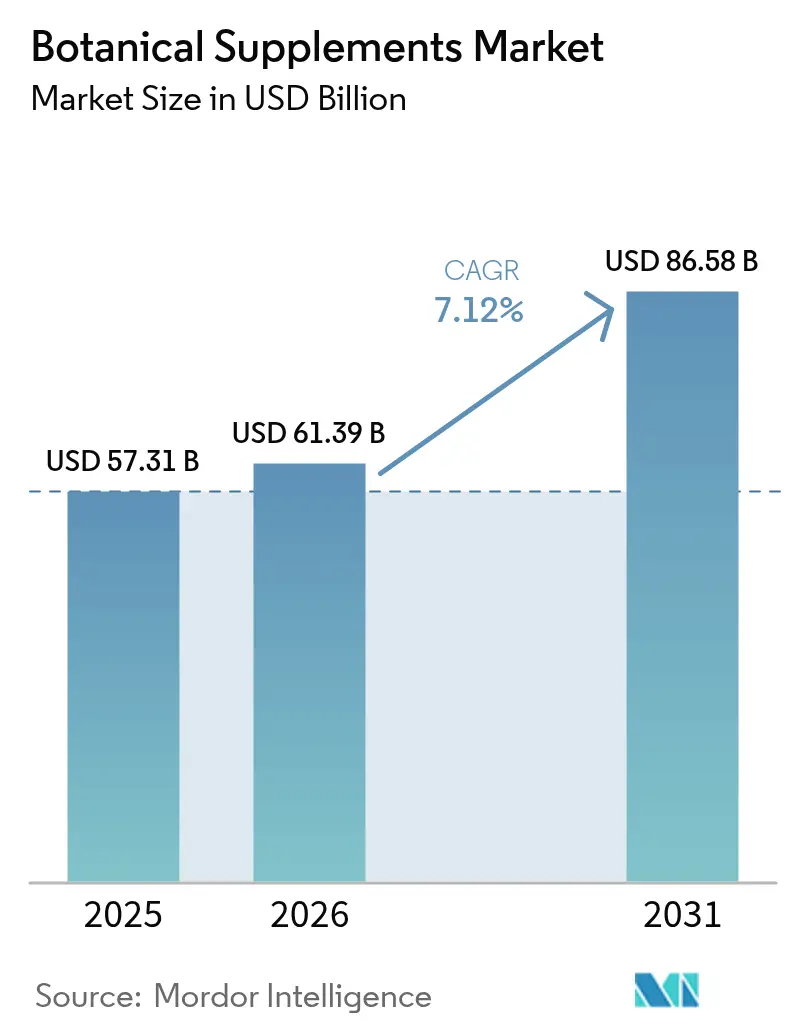

The Botanical Supplements market size is expected to grow from USD 57.31 billion in 2025 to USD 61.39 billion in 2026 and is forecast to reach USD 86.58 billion by 2031 at 7.12% CAGR over 2026-2031.

This growth is driven by the increasing integration of traditional medicine with modern scientific advancements, along with clear regulatory oversight from the United States Food and Drug Administration (FDA). The adoption of advanced technologies, such as artificial intelligence in extraction processes, vertical farming, and plant-cell culture, is helping to reduce variability in raw materials, improve consistency in production batches, and shorten lead times. These advancements are making high-quality, premium formulations more widely available to consumers. In regions like Latin America and Asia-Pacific, regulatory harmonization is facilitating cross-border e-commerce, enabling companies to expand their reach. Updated European Union regulations on hydroxyanthracene derivatives are encouraging faster reformulation of products to meet compliance standards. Companies are also investing in clinical studies to substantiate their product claims, while retailers are focusing on offering curated selections of clean-label and non-synthetic products. The competitive landscape is moderately concentrated, with the top five companies collectively holding a significant share of the global market value.

Key Report Takeaways

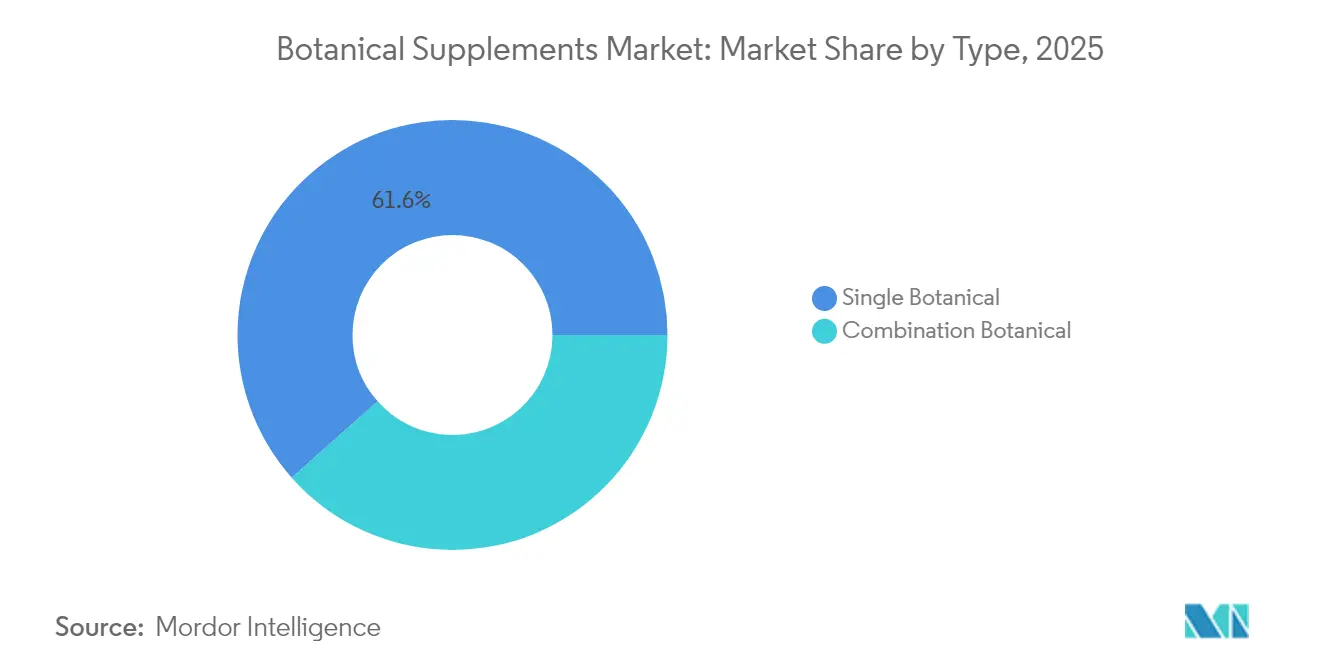

- By type, single botanical supplements held 61.55% of the botanical supplements market share in 2025, whereas combination formulations are projected to expand at a 9.12% CAGR through 2031.

- By form, tablets led with 32.92% revenue share in 2025, while gummies are set to register the fastest 8.88% CAGR to 2031.

- By functionality/health benefit, digestive and gut health products accounted for a 35.12% share of the botanical supplements market size in 2025; immune support is advancing at an 7.78% CAGR through 2031.

- By distribution channel, specialty and health stores commanded 71.35% of revenue in 2025, yet online retail is growing at a 7.54% CAGR.

- By geography, North America controlled 31.86% of global revenue in 2025, whereas Asia-Pacific is forecast to climb at an 8.09% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Botanical Supplements Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing consumer demand for natural and organic health products | +1.8% | Global, with the strongest impact in North America and Europe | Medium term (2-4 years) |

| Strategic marketing through celebrity and influencer endorsements | +0.9% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Consumer preference shift toward plant-based ingredients over synthetic alternatives | +1.5% | Global, led by developed markets | Long term (≥ 4 years) |

| Integration of traditional medicine practices driving botanical supplement adoption | +1.2% | Asia-Pacific core, spill-over to global markets | Long term (≥ 4 years) |

| Expanding elderly population seeking natural health solutions | +1.0% | Global, concentrated in developed economies | Long term (≥ 4 years) |

| Scientific backing and product innovation | +1.3% | Global, with research and Development centers in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer preference shift toward plant-based ingredients over synthetic alternatives

Consumers are increasingly aware of environmental concerns and are becoming more cautious about synthetic or petrochemical-based additives, leading to a growing preference for plant-based ingredients. Innovations in extraction technologies, such as supercritical CO₂ and ultrasonic methods, have enabled the production of highly concentrated botanical actives while minimizing environmental impact. Regulatory bodies, like the European Medicines Agency, have introduced clearer and more streamlined guidelines for registering plant-based actives, simplifying compliance for manufacturers[1]Source: Food and Drug Administration, "Dietary Supplements," fda.gov. For instance, these guidelines have reduced the time and complexity involved in bringing new botanical products to market. Brands are actively responding to this trend with new product launches. For example, Holland & Barrett introduced a range of plant-based supplements targeting immunity and stress support in 2024, featuring ingredients like ashwagandha, elderberry, and turmeric. Advancements in traceability systems are enhancing consumer confidence by ensuring that botanical ingredients are safer and more sustainable.

Increasing consumer demand for natural and organic health products

Consumers are increasingly choosing botanical and organic supplements as part of a growing trend toward natural and healthier lifestyles. This shift is strongly supported by clean-label regulations, particularly in regions like Europe, which focus on ensuring transparency and traceability in how these products are sourced and manufactured. Regulatory agencies, such as the United States FDA, are also playing a critical role by enforcing accurate and truthful labeling standards. For example, these regulatory agencies require companies to verify the identity of botanical ingredients and provide evidence to support health claims under the Dietary Supplement Health and Education Act (DSHEA)[2]Source: European Medicine Agency, "Good manufacturing practice," ema.europa.eu. These regulations push brands to maintain detailed documentation, which helps build trust and credibility with consumers. Despite being priced 15–20% higher than conventional products, botanical supplements continue to see strong demand. Even price-sensitive consumers are willing to pay the premium, as they perceive the health benefits to outweigh the cost.

Expanding elderly population seeking natural health solutions

The aging global population is driving consistent demand for botanical supplements, particularly those addressing age-related health concerns. The supplement consumption data shows that 81% of Americans aged 55 and above use supplements, and in Germany, over 60% of supplement consumers are 55 years or older, as reported by the Glanbia Nutritionals 2022 report. Elderly consumers demonstrate a preference for botanical supplements with established traditional uses, such as turmeric, ginger, and ginseng, which target common age-related issues. Due to their complex health requirements, older consumers tend to take supplements daily, creating opportunities for personalized products combining immune health with additional benefits. The World Health Organization (WHO) projects that the population aged 60 years and over will increase from 1 billion in 2020 to 1.4 billion by 2030, and reach 2.1 billion by 2050[3]Source: World Health Organization, "Ageing," who.int. This combination of aging demographics and growing acceptance of botanical supplements continues to influence product development and marketing strategies in the market.

Strategic marketing through celebrity and influencer endorsements

The botanical supplements market is gaining significant traction among younger consumers, fueled by marketing strategies that effectively use celebrities and social media influencers to promote natural wellness as a lifestyle choice. These influencers play a key role in simplifying complex scientific information, making botanical products more relatable and appealing to a broader audience. Social media platforms like Instagram and TikTok have become essential for boosting brand visibility. For instance, as of 2025, Grüns Supplements successfully built a community of 250,000 followers and secured USD 500 million in funding by leveraging user-generated content and influencer collaborations. To strengthen credibility, brands are increasingly incorporating results from clinical studies, such as randomized controlled trials, into their marketing efforts. This approach accelerates the adoption of botanical supplements among tech-savvy, younger demographics, helping these products evolve from niche offerings to mainstream lifestyle essentials.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Risk of contamination or adulteration in raw botanical materials | -1.2% | Global, particularly affecting developing country suppliers | Short term (≤ 2 years) |

| Limited availability of sustainable and high-quality raw material sources | -0.8% | Global, concentrated in source regions | Medium term (2-4 years) |

| Presence of counterfeit products | -0.6% | Global, with higher impact in unregulated markets | Short term (≤ 2 years) |

| Growing competition from alternative dietary supplements | -0.9% | Developed markets, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Risk of contamination or adulteration in raw botanical materials

The botanical supplements market faces significant challenges related to raw material quality and safety. According to a study published in August 2024 by JAMA Network under Complementary and Alternative Medicine, approximately 4.7% of US adults used at least one of six potentially hepatotoxic botanical products[4]Source: JAMA Network, "Estimated Exposure to 6 Potentially Hepatotoxic Botanicals in US Adults," jamanetwork.com. The risk is particularly pronounced in markets with less stringent regulatory oversight, where adulteration with pharmaceutical compounds or contamination with heavy metals can occur. These safety concerns create market hesitation among consumers and healthcare providers, limiting the broader adoption of botanical supplements. In response, the industry has established initiatives such as the Botanical Safety Consortium, a collaborative forum by the FDA, NIH, and the Health and Environmental Sciences Institute, to develop improved evaluation methods for botanical safety. These ongoing safety challenges and regulatory complexities continue to restrain the market's growth potential despite increasing consumer interest in natural health solutions.

Limited availability of sustainable and high-quality raw material sources

Sourcing consistent, high-quality botanical raw materials continues to be a major challenge, especially as climate change and environmental issues disrupt the production of key adaptogens like ashwagandha, rhodiola, and maca. Factors such as unpredictable weather patterns, rising global temperatures, and soil degradation in key growing regions have significantly impacted crop yields. Export restrictions imposed by governments in countries like Peru and India have further strained the supply chain, creating volatility in the availability of these ingredients. To address these issues, some producers are adopting vertical integration strategies. For instance, farms in India are using advanced techniques like drip irrigation and controlled drying processes to ensure the preservation of active compounds, such as withanolides in ashwagandha, before milling. At the same time, innovations like plant-cell culture systems and aeroponic farming are gaining traction as sustainable solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Combination Formulations Drive Innovation

Single-ingredient products accounted for 61.55% of the revenue in 2025, as consumers continued to rely on well-researched ingredients like curcumin, echinacea, and milk thistle. These products have maintained their dominance due to their long-standing safety profiles and widespread acceptance among healthcare professionals. Their established reputation ensures consistent demand, making them a staple in the botanical supplements market. However, the growing interest in more comprehensive health solutions is driving a shift toward combination formulations, which are projected to grow at a 9.12% CAGR through 2031. These blends appeal to consumers seeking products that address multiple health concerns in a single dose, offering convenience and perceived added value.

The rising popularity of combination formulations aligns with the broader trend of personalized nutrition, where digital tools help consumers identify tailored solutions for their specific health needs. Brands are increasingly incorporating adaptogens, nootropics, and probiotics into multi-functional products, such as once-daily softgels, marketed as comprehensive solutions for various life stages. Retailers are also responding to this demand by dedicating more shelf space to these innovative products, signaling confidence in their market potential. As a result, combination formulations are expected to gain significant traction, gradually closing the gap with single-ingredient products.

By Form: Gummies Revolutionize Delivery Mechanisms

Tablets accounted for 32.92% of global sales in 2025, driven by their affordability, long shelf life, and precise dosing capabilities that align with pharmaceutical standards. These attributes make tablets a preferred choice for cost-conscious consumers and ensure their continued presence in pharmacies and drugstores. However, gummies and chews are rapidly gaining traction, with an expected annual growth rate of 8.88%. Gummies and chews are reshaping the botanical supplements market by appealing to consumers who dislike traditional pill formats. Their pleasant taste and ease of consumption make them particularly popular among families and individuals seeking a more enjoyable supplement experience.

Advancements in gummy production technology have addressed previous challenges, such as high sugar content and moisture issues. Innovations like starch-free molds, pectin-based gelling agents, and low-glycemic sweeteners have enabled the creation of gummies that cater to diverse dietary preferences, including vegan, keto, and diabetic-friendly options. Leading brands are now offering zero-added-sugar gummies sweetened with plant-based stevia, which maintains a desirable texture and flavor. These improvements have expanded the appeal of gummies beyond children to adult consumers, with products targeting specific health needs such as sleep support, cognitive enhancement, and immune health.

By Functionality: Immune Support Accelerates Growth

In 2025, digestive and gut health products accounted for 35.12% of the market's revenue, reflecting the increasing recognition of the link between gut health and overall wellness. Products that combine digestive enzymes with herbal extracts provide quick relief for gastric discomfort, while synbiotic blends help improve gut microbial diversity. Growing consumer awareness of the gut-brain connection has driven repeat purchases and high adherence to these products. At the same time, immune support products are emerging as a fast-growing segment, with an 7.78% CAGR. This growth is fueled by heightened health awareness following the pandemic and scientific validation of botanicals like Andrographis paniculata and Rhodiola rosea, which are known for their ability to regulate immune responses and promote overall health.

Manufacturers are innovating by combining beta-glucan-rich mushrooms with antioxidant-packed berries to create versatile immune-support products, such as soft chews and effervescent powders. Immune health claims now account for 33% of all new product launches in the botanical supplements market, highlighting the segment's growing importance. Related categories such as stress relief, sleep support, and cognitive health are also gaining momentum. These segments often utilize adaptogenic ingredients, enabling companies to optimize raw material usage while addressing multiple consumer needs within the botanical supplements market.

By Distribution Channel: Digital Transformation Accelerates

Specialty and health retailers account for 71.35% of 2025 revenue, driven by their curated product selections and knowledgeable staff who help customers understand botanical supplement benefits. This retail format enables premium pricing as consumers demonstrate a willingness to pay more for professional guidance. E-commerce channels are projected to grow at a 7.54% CAGR, exceeding other distribution channels, as consumers embrace subscription services and home delivery options. Digital platforms utilize AI technology to analyze consumer behavior and recommend product combinations that increase purchase value.

International e-commerce platforms enable Asian manufacturers to sell certified products directly to United States and European consumers, reducing intermediary costs and expanding market reach. Online retailers differentiate themselves through subscription services, incorporating home testing kits for personalized supplement recommendations, and building valuable consumer data assets. While supermarkets and pharmacies adopt digital solutions like QR codes and pickup lockers, they continue to lose market share as younger consumers prefer mobile shopping platforms.

Geography Analysis

North America remained the leading region in the botanical supplements market in 2025, capturing a 31.86% revenue share. A well-established regulatory framework, advanced research infrastructure, and a growing focus on preventive health among consumers drive this dominance. The FDA’s updated New Dietary Ingredient notification guidance has streamlined the process for introducing new products while ensuring high safety standards. Research hubs in states like California and Massachusetts continue to validate the efficacy of innovative plant-based extracts, which have strengthened consumer trust and scientific credibility. These factors collectively contribute to the region's strong market position.

The Asia-Pacific region is emerging as a key growth driver for the botanical supplements market, with a projected CAGR of 8.09%. Government initiatives integrating traditional medicine systems like Ayurveda, Traditional Chinese Medicine, and Kampo into public health programs are fueling this growth. For example, China’s Healthy China 2030 initiative highlights the government’s commitment to promoting health and wellness, while Japan’s Foods with Function Claims framework has simplified the approval process for functional food labels. Multinational companies are investing in local cultivation and extraction facilities to overcome export restrictions and benefit from favorable tariffs under Regional Comprehensive Economic Partnership agreements. Domestic start-ups are leveraging their cultural heritage to create niche products for e-commerce platforms, often targeting diasporic communities.

Europe presents a mixed outlook. Demand remains robust in Germany, France and Italy, yet the 2025 ban on hydroxyanthracene derivatives forces reformulation of certain laxative herbs like senna and aloe. Manufacturers allocate capital toward high-performance thin-layer chromatography to confirm compliance and sustain market access. The European Food Safety Authority continues to harmonize monographs, reducing national fragmentation. Eastern European economies, notably Poland and Romania, enjoy double-digit volume growth as incomes rise and pharmacy chains expand shelf space.

Regulatory Landscape

Regulation of botanical supplements continues to tighten around ingredient identity, safety substantiation, and traceability, with the United States Food and Drug Administration (FDA) overseeing products under DSHEA and current good manufacturing practices. In March 2026, the FDA Office of Dietary Supplement Programs held a public meeting to collect stakeholder input on the scope of dietary supplement ingredients under DSHEA, indicating closer scrutiny of how novel botanicals are classified and supported with evidence.

In Europe, botanical oversight remains split between EU-level safety assessment and member-state decisions on use and claims, while EFSA maintains botanical resources such as its compendium. In June 2026, EFSA opened a public consultation to modernize and consolidate botanical safety assessment approaches into a single cross-sectoral guidance spanning food and feed applications. In July 2026, the Codex Alimentarius Commission adopted updated standards for certain botanical spices (including vanilla and black cardamom), reinforcing globally referenced quality and contaminant benchmarks used in cross-border trade.

Competitive Landscape

The botanical supplements market is moderately concentrated, with the top five companies holding a significant share of the overall market. This level of concentration reflects a competitive landscape where established multinationals are expanding their presence in the botanical space through strategic acquisitions. For example, Dr. Willmar Schwabe recently acquired Enzymatic Therapy, leveraging its Nature’s Way brand to strengthen its foothold in the United States market.

Technological advancements are becoming a key differentiator in the market. Companies like Brightseed are utilizing artificial intelligence to explore botanical metabolomes and discover new bioactive compounds, partnering with vertical farming pioneers like Botalys to commercialize rare ingredients.

Marketing strategies are also playing a crucial role in shaping the botanical supplements market. Companies are allocating significant portions of their revenue to influencer partnerships, short-form video campaigns, and wellness app integrations to engage consumers effectively. Loyalty programs are being designed to reward repeat customers with personalized dosage recommendations based on symptom-tracking tools. Collaborations between functional beverage and supplement brands are blurring category lines, with powdered botanical blends now appearing in ready-to-drink formats co-branded with major energy drink companies.

Botanical Supplements Industry Leaders

-

Nestle SA

-

Dr. Willmar Schwabe GmbH & Co. KG

-

NOW Foods

-

Himalaya Global Holdings Ltd.

-

Dabur India Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The market is creating whitespace for suppliers and brand owners seeking to reduce botanical variability and the documentation burden through controlled production and upgraded analytical verification. Activity in 2026 points to more plant-cell and fermentation-based biomass as an alternative to climate- and export-restriction-sensitive agricultural supply, including Herbalife and IIT Madras launching India’s first Centre of Excellence focused on plant cell fermentation technology to develop sustainable herbal biomass and enriched extracts. At the same time, investment in higher-resolution identity testing is increasingly becoming a practical differentiator for quality-led brands, including NOW implementing a next-generation DNA sequencing program at its Sparks, Nevada facility in partnership with LeafWorks to improve botanical identity verification.

Regulatory and standards updates are also shaping opportunity around compliant, export-ready supply chains and clearer ingredient status classification. The European Commission’s January 2026 Novel Food Catalogue update provided immediate assessment-status signals for selected botanicals, supporting faster internal go/no-go decisions for cross-border portfolios, while EFSA’s June 2026 consultation on modernizing botanical safety guidance points to a more uniform evidence pathway in the EU once finalized. Traceability initiatives are also accelerating between major sourcing and consumption markets, including the Organic and Natural Health Association partnering with India’s SHEFEXIL to standardize documentation protocols for botanical ingredient supply chains between the US and India, which can support digital batch documentation, auditing services, and compliant ingredient platforms serving both D2C and specialty retail channels.

Recent Industry Developments

- April 2026: NOW Foods launched Vitamin C (250 mg) and Vitamin D3 (1,000 IU) gummies, marking the company’s entry into gummy-format supplements. The launch broadens NOW’s delivery formats beyond traditional tablets and capsules, which tracks consumer movement toward more palatable botanical and wellness products sold through both retail and online channels.

- June 2025: Dabur India Ltd. launched Siens by Dabur as a digital-first nutraceutical brand spanning beauty, gut health, and daily wellness. This launch strengthens Dabur’s direct-to-consumer playbook in supplements, supporting faster portfolio iteration and customer data capture versus legacy pharmacy-led routes to market.

- August 2024: Dabur India Limited received board approval to invest INR 135 crore in a new manufacturing facility in the SIPCOT industrial zone near Tindivanam, Tamil Nadu. The plant expands Dabur’s domestic manufacturing footprint and adds capacity relevant to Ayurvedic and herbal product lines that support broader botanical wellness positioning.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers finished botanical supplement products meant for oral consumption, where the active ingredients are plant based (whole herb, parts, or standardized extracts) and sold for wellness or health support.

Scope exclusions: We exclude topical botanicals, prescription only herbal drugs, and botanical ingredients sold mainly as food flavors, cosmetics inputs, or bulk raw materials.

Segmentation Overview

-

By Type

- Single Botanical

- Combination Botanical

-

By Form

- Tablets

- Capsules/Softgels

- Gummies and Chews

- Powders

- Others

-

By Functionality/Health Benefits

- Digestive and Gut Health

- Stress, Sleep and Cognitive Health

- Immune Support

- Others

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty and Health Stores

- Online Retailers

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Nigeria

- Saudi Arabia

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helps set the market boundaries and build a demand story before any numbers are modeled. We reviewed public sources such as the US NIH Office of Dietary Supplements, the US FDA dietary supplement guidance pages, the European Food Safety Authority (EFSA) scientific opinions, and the WHO monographs related to selected medicinal plants. For cross checks on consumption and purchasing signals, we also used statistical series and reference pages such as OECD health statistics and UN Comtrade, focusing on herbal and plant material trade direction (used carefully because raw botanicals are not the same as finished supplements).

We then aligned these findings with company filings, investor decks, annual reports, and reputable press coverage to understand product mix shifts across capsules, gummies, powders, and liquids, as well as channel momentum across pharmacies, specialty stores, and online. Where public filings were thin, we used paid subscriptions for company financials and intelligence, and also patent databases to track ingredient and claims activity without relying on private sales ledgers. The source list above is illustrative, and we used additional public and paid references for data capture, checks, and clarification.

Primary Interviews and Surveys

Primary work was used to test what desk findings suggested, especially around pricing ladders, product form preferences, and how claims are positioned across regions. We spoke with a mix of brand owners, contract manufacturers, ingredient specialists, distributors, and retail channel contacts, and then checked consistency of these inputs across APAC, EMEA, and the Americas so the same assumptions were not applied everywhere.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | APAC: 47% |

| Mid tier: 45% | Functional/Unit leaders: 35% | EMEA: 29% |

| Smaller Players: 16% | Managers: 51% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where population and income pools are filtered through supplement usage rates and region level spending patterns, and only then the botanical share is applied based on product mix evidence from desk work and interviews. We also corroborated results with selective bottom-up approximations, mainly by rolling up a sample of supplier and brand revenues where available, followed by channel checks and an ASP times volume sense check for key forms such as capsules, gummies, and powders.

Key model inputs include the penetration of dietary supplements by region, the share of botanicals within supplement baskets, average retail price bands by form and claim intensity, online channel contribution, and the pace of new product launches tied to specific botanicals. When a country lacks clean public readouts, we proxy using nearby markets with similar regulation and retail structure, then adjust using interview feedback so the gap does not distort the regional total. For forecasting, we run scenario analysis to reflect different adoption and pricing paths, and then align the selected path to expert consensus on demand drivers such as immunity and stress support, along with expected channel mix shifts.

Data Validation & Update Cycle

Outputs are checked against independent signals such as supplement consumption indicators, reported category growth in public filings, and trade direction for relevant botanicals, which helps spot totals that drift from reality. If a region shows an unusual jump in value without a matching change in volumes, prices, or distribution, it is flagged, reviewed, and assumptions are revisited, followed by re-contacting selected respondents to confirm what changed.

Before sign-off, numbers go through multi-step internal reviews focused on math integrity, scope alignment, and consistency across years and regions. Reports are refreshed annually, and interim updates are triggered when there are material events such as regulatory shifts, major pricing moves, or clear demand shocks. Right before delivery, a final analyst pass is done so the client receives the latest view available at that time.

Mordor Intelligence's Botanical Supplements Market Size Compared With Other Published Estimates

Published estimates for botanical supplements can vary widely because each publisher draws the line around products differently and also uses different pricing and channel assumptions. Differences can also come from the reference year, how currency conversion timing is handled, and whether growth is built from observed adoption signals or from a high-growth storyline.

The table points to a clear spread. In Mordor Intelligence's model, we count only finished botanical supplements intended for oral consumption, and we keep adjacent areas like bulk botanical ingredients and topical botanicals outside the total. This changes the denominator before any forecasting is applied.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 61.39 B (2026) | |

| Trade Journal A | USD 42.04 B (2025) | Uses a different base year and appears to anchor value closer to a conservative retail revenue pool, where botanical product mixes and price ladders are not consistently separated by form and channel. |

| Industry Portal B | USD 51.95 B (2025) | Applies a higher growth arc across a longer horizon, and the scope likely blends a wider set of botanical wellness products, which can shift the starting value and the implied ASP progression. |

Taken together, the comparison shows that scope boundaries and base-year alignment drive most of the gap, and growth math only comes after that. Our approach stays traceable because each step ties back to practical inputs such as usage rates, channel mix, and form level pricing, which can be rechecked when conditions change.

Key Questions Answered in the Report

What is the current value of the botanical supplements market?

The botanical supplements market size is USD 61.39 billion in 2026.

How fast is the botanical supplements market expected to grow?

The market is forecast to expand at a 7.12% CAGR, reaching USD 86.58 billion by 2031.

Which region will post the highest growth through 2031?

Asia-Pacific leads in growth with an expected 8.09% CAGR, driven by integration of traditional medicine and rising incomes.

What delivery format is growing fastest?

Gummies and chews exhibit the highest growth rate at 8.88% CAGR due to superior taste and convenience.

Page last updated on: