Market Overview

| Study Period | 2021 - 2031 |

|---|---|

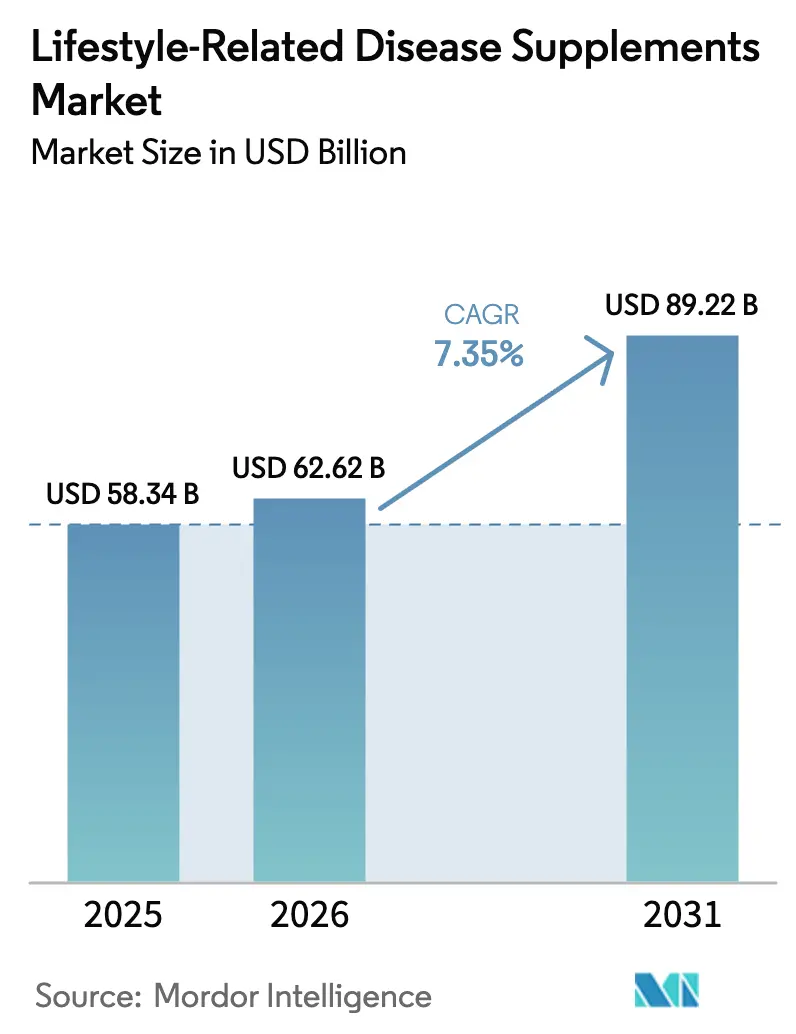

| Market Size (2026) | USD 62.62 Billion |

| Market Size (2031) | USD 89.22 Billion |

| Growth Rate (2026 - 2031) | 7.35% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Lifestyle-Related Disease Supplements Market Analysis by Mordor Intelligence

The lifestyle-related disease supplements market size is expected to grow from USD 58.34 billion in 2025 to USD 62.62 billion in 2026 and is forecast to reach USD 89.22 billion by 2031 at 7.35% CAGR over 2026-2031. Projections indicate it will climb to USD 84.73 billion by 2030, marking a steady CAGR of 7.75%. This growth trajectory underscores a pivotal shift: preventive wellness is evolving from a mere self-care choice to a central component of overall health strategy. A 2023 survey by the Council for Responsible Nutrition (CRN) revealed that a record 74% of U.S. adults turned to dietary supplements[1]Source: Council for Responsible Nutrition (CRN), "2023 CRN Consumer Survey on Dietary Supplements", crnusa.org. Factors such as an aging population, rising prevalence of non-communicable diseases, and advancements in formulation science are driving consumers toward targeted nutritional products. While North America continues to be the primary revenue source, the Asia-Pacific region, buoyed by a growing middle class, urban lifestyles, and government-backed prevention campaigns, is poised as the engine of future growth. The category's expansion is further fueled by retail digitization, ingredient innovation, and enhanced clinical validation, fostering trust among both healthcare providers and consumers. Concurrently, efforts towards regulatory harmonization and transparent supply chains bolster investor confidence, paving the way for cross-border brand growth.

Key Report Takeaways

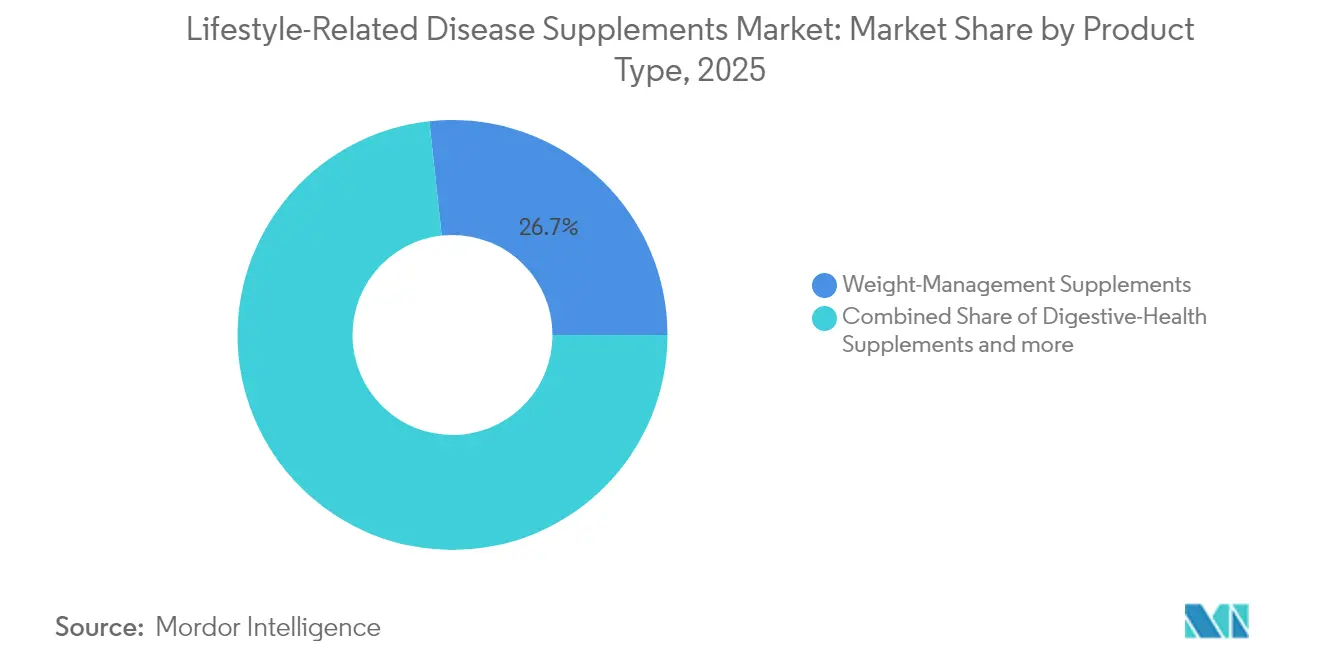

- By product type, weight-management solutions captured 26.72% of the lifestyle-related disease supplements market share in 2025, whereas digestive-health formulas are projected to post the fastest growth rate of 8.45% through 2031.

- By form, softgels commanded a 35.10% share of the lifestyle-related disease supplements market size in 2025, while gummies are projected to advance at a 9.35% CAGR between 2026 and 2031.

- By distribution channel, specialty and drug stores led with 37.10% revenue share in 2025, and online retail is forecast to expand at a 10.15% CAGR to 2031.

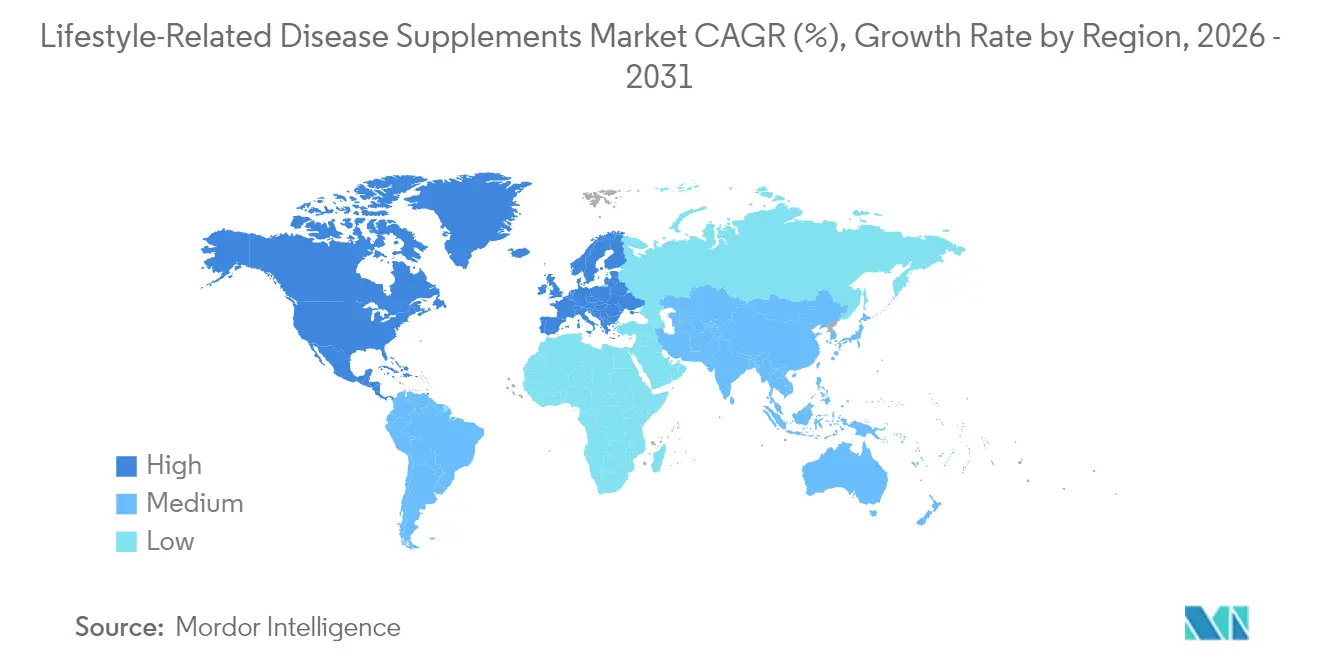

- By geography, North America retained 31.85% revenue share in 2025, whereas the Asia-Pacific recorded the highest 8.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lifestyle-Related Disease Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift towards preventive healthcare | +1.2% | Global, with the strongest adoption in North America and Europe | Medium term (2-4 years) |

| Rising incidence of lifestyle-related diseases | +1.8% | Global, particularly acute in the Asia-Pacific urban centers | Long term (≥ 4 years) |

| An aging global population | +1.5% | North America and Europe primary, expanding to the Asia-Pacific | Long term (≥ 4 years) |

| Innovation in product formulation | +1.0% | Global, led by North America and Europe's research and development centers | Short term (≤ 2 years) |

| Increased focus on mental wellness | +0.8% | North America and Europe, emerging in the Asia-Pacific | Medium term (2-4 years) |

| Shift towards natural and plant-based supplements | +1.3% | Global, with premium segments in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift towards preventive healthcare

Globally, government healthcare policies are shifting focus from reactive treatments to preventive care, reshaping how consumers approach and adopt supplements. The World Health Organization's push for the prevention of non-communicable diseases has spurred national health strategies, highlighting nutritional supplements as a cost-effective means to alleviate healthcare burdens. This shift is particularly evident in developed nations, where aging populations are challenging traditional healthcare systems. In response, policymakers are increasingly promoting preventive measures, including dietary supplements. Surveys reveal that 75% of Americans now turn to dietary supplements, with a striking 91% deeming them essential for health maintenance, as reported by the Council for Responsible Nutrition. This underscores a cultural shift: supplements are evolving from optional wellness aids to essential components of healthcare. Moreover, this trend isn't limited to individual choices; employers are now weaving supplement benefits into their workplace wellness initiatives, bolstering institutional demand and fueling market growth. Recognizing the preventive role of supplements, regulatory bodies in various regions, including the FDA, are offering clearer guidelines on health claims, further solidifying this perspective.

Rising incidence of lifestyle-related diseases

Health authorities project a significant rise in diabetes prevalence by 2045, underscoring the growing market for targeted nutritional interventions amid a global surge in lifestyle-related diseases. For instance, NHS Digital, a division of NHS England, reported that between 2023 and 2024, over 3.5 million individuals in England were diagnosed with type 2 diabetes, while nearly 277,000 had type 1[2]Source: NHS Digital, a division of NHS England, "National Diabetes Audit Core Report 1: Care Processes and Treatment Targets 2023-24, Underlying data", digital.nhs.uk. As urbanization sweeps through developing nations, it's ushering in sedentary lifestyles and a penchant for processed foods, mirroring health issues once seen only in the West. This shift fuels a growing demand for supplements that target metabolic health, heart function, and weight management. Today's consumers are not just looking for any solution; they're gravitating towards evidence-backed formulations that target specific biomarkers linked to chronic diseases. With the advent of continuous glucose monitoring and similar health tech, individuals can now monitor their body's reactions to supplements. This real-time feedback not only reinforces their purchasing decisions but also propels market growth. Moreover, as healthcare providers increasingly endorse specific supplements for prediabetic and metabolic syndrome management, they're not just validating these products but also broadening their appeal beyond the conventional wellness market.

An aging global population

As the global population aged 65 and older is projected to double by 2050, both developed and emerging economies are experiencing a sustained demand for supplements addressing age-related health concerns. For instance, in 2024, Monaco topped the charts with 36% of its population aged 65 or older, followed closely by Japan at 29%, and Portugal and Bulgaria, each at 24%, as reported by the Population Reference Bureau. This demographic shift is driving a surge in demand for supplements that support cognitive health, bone density, cardiovascular function, and the immune system. Notably, older consumers are showing a pronounced willingness to invest in premium, clinically validated formulations. In the Asia-Pacific markets, where rapid economic development aligns with demographic transitions, there's a notable emergence of health-conscious consumer segments with disposable income. Recognizing the unique nutritional needs of this aging demographic, regulatory bodies, such as Japan's Consumer Affairs Agency, are paving the way for market growth by establishing specific health claim categories for age-related functional foods. Moreover, the confluence of aging demographics and technological advancements is birthing opportunities for personalized supplement regimens. By leveraging genetic testing, biomarker analysis, and health tracking data, companies can command premium pricing and bolster customer loyalty.

Innovation in product formulation

Technological advances in supplement formulation are enhancing bioavailability, enabling targeted delivery, and improving the consumer experience. This evolution is driving both market premiumization and category expansion. In 2024, the European Food Safety Authority approved novel ingredients like BioPQQ and magnesium L-threonate. This move underscores the regulatory acceptance of innovative compounds that effectively address specific health concerns. Innovations in manufacturing, such as CONFIXX gelatin technology and advanced encapsulation methods, are paving the way for gummies and softgels. These advancements ensure improved stability and nutrient protection, catering to consumer preferences for convenient and palatable formats. With personalization technologies, manufacturers can now craft customized supplement formulations. By leveraging individual health data, genetic profiles, and lifestyle factors, these tailored products command premium pricing and cultivate customer loyalty. Furthermore, the integration of artificial intelligence in formulation development is revolutionizing the industry. AI accelerates the discovery of synergistic ingredient combinations and optimal dosing protocols, streamlining development timelines and enhancing product efficacy. Such innovations not only provide a competitive edge to companies that bolster their research and development capabilities but also heighten entry barriers for smaller players without adequate technological resources.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of substitute products | -0.7% | Global, particularly in developed markets with diverse options | Short term (≤ 2 years) |

| Regulatory challenges and inconsistencies | -1.1% | Global, with varying intensity across jurisdictions | Medium term (2-4 years) |

| Potential for side effects and drug interactions | -0.5% | Global, heightened in markets with aging populations | Long term (≥ 4 years) |

| Consumer skepticism regarding claims | -0.8% | Developed markets with sophisticated consumers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory challenges and inconsistencies

Global markets' divergent regulatory frameworks complicate compliance, hindering market expansion and inflating operational costs for supplement manufacturers. Companies face distinct approval processes, labeling mandates, and health claim substantiation standards across various jurisdictions. Agencies such as Singapore's Health Sciences Authority, Japan's Ministry of Health, Labour and Welfare, and India's Food Safety and Standards Authority uphold varied classification systems for the same products. These regulatory inconsistencies pose challenges, especially for novel ingredients and innovative formulations. Here, approval timelines and evidence requirements differ markedly between markets, leading to delayed product launches and diminished returns on research and development investments. The absence of unified international standards not only hampers cross-border trade but also curtails economies of scale in manufacturing and marketing. Recent regulatory shifts in the Asia-Pacific markets present a mixed bag of opportunities and challenges. For instance, while India rolls out new health supplement regulations, it simultaneously restricts certain botanical ingredients, leaving manufacturers eyeing regional expansion in a state of uncertainty.

Consumer skepticism regarding claims

In developed economies, where regulatory enforcement is stringent and consumer education is prioritized, the market faces challenges. These challenges arise from heightened media scrutiny and growing consumer sophistication, especially concerning supplement marketing claims. Misinformation and conflicting research on supplement efficacy further muddle the waters, leading to consumer confusion and hesitance in purchasing. A 2024 survey by the Council for Responsible Nutrition revealed that 41% of non-users cited a perceived lack of need as a primary barrier to adoption. Negative experiences and skeptical views, often amplified by social media and online forums, can quickly tarnish the credibility of the supplement category and individual brands. This issue is exacerbated by the industry's historical tendency towards exaggerated marketing claims and lapses in quality control. To counteract this skepticism, companies are now investing significant resources in clinical research, third-party testing, and promoting transparent communication. Meanwhile, regulatory agencies are tightening their grip, scrutinizing marketing communications, and penalizing misleading claims. As a result, companies are adopting more conservative messaging, a shift that could dampen marketing effectiveness and slow down market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Weight Management Drives Market Leadership

In 2025, weight-management supplements hold a dominant 26.72% market share, underscoring the global obesity crisis and a growing consumer demand for formulations that promote healthy weight maintenance. This segment's leadership is bolstered by its widespread appeal across demographics and its alignment with broader wellness aspirations, such as energy enhancement, metabolic health, and cardiovascular well-being. Digestive-health supplements are on a robust growth path, projected to expand at an 8.45% CAGR through 2031. This surge is fueled by burgeoning research highlighting the gut-brain connection and the importance of microbiome diversity, underscoring the pivotal role of digestive wellness in overall health. Meanwhile, heart-health supplements are reaping benefits from an aging population and the prevalent threat of cardiovascular diseases. At the same time, brain-health supplements are resonating with younger audiences, particularly those pursuing cognitive boosts and stress relief. Data from the Centers for Disease Control and Prevention indicates that in 2024, approximately 3% of U.S. adults reported a prior heart attack diagnosis from a health professional.

Bone and joint-health supplements cater to a stable market, driven by the needs of an aging demographic. However, they grapple with competition from functional foods and alternative therapies, which deliver similar benefits through varied means. The category labeled "other lifestyle-focused supplements" is gaining traction, encompassing niches like sleep aids, stress relief, and immune boosters. These reflect shifting consumer health priorities and the challenges of modern living. Furthermore, product innovation is reshaping the landscape. Multi-functional supplements are emerging, blending ingredients for weight management, digestive health, and energy support. This trend not only addresses diverse consumer needs in one package but also opens avenues for premium market positioning and share growth.

By Form: Gummies Challenge Traditional Softgel Dominance

In 2025, softgels command a dominant 35.10% market share, capitalizing on their superior bioavailability, ingredient protection, and established consumer trust. This solidifies their status as the go-to choice for oil-soluble vitamins and botanical extracts. Meanwhile, gummies are surging ahead with a robust 9.35% CAGR. This growth is fueled by a shift in consumer preferences towards more convenient and enjoyable consumption methods. Gummies particularly resonate with younger audiences, who prioritize taste and convenience over conventional pharmaceutical forms. Thanks to manufacturing breakthroughs, such as CONFIXX gelatin systems and cutting-edge coating techniques, gummy technology has evolved. These innovations enable the integration of previously incompatible ingredients while ensuring product stability and an extended shelf life.

Capsules cater to budget-minded consumers and those loyal to traditional pharmaceutical forms. In contrast, powder formulations appeal to fitness aficionados and those seeking tailored dosing. Effervescent tablets, while offering rapid absorption and hydration benefits, grapple with challenges stemming from their intricate manufacturing processes and ingredient stability issues. The form segment reveals distinct generational trends: younger consumers are leaning towards gummies and powders, whereas older individuals show a steadfast preference for capsules and softgels. This generational divide presents ripe opportunities for targeted marketing and product development, tailored to meet the unique needs and preferences of each demographic.

By Distribution Channel: Digital Transformation Accelerates Online Growth

In 2025, specialty and drug stores command a leading 37.10% market share, capitalizing on consumer trust and the allure of professional consultations. These traditional outlets, as highlighted by the Council for Responsible Nutrition, offer credibility and expertise, guiding consumers in selecting supplements, especially for complex health issues or potential drug interactions. Meanwhile, online retail stores surge ahead with a robust 10.15% CAGR, fueled by the rise of digital health trends, subscription models, and direct-to-consumer tactics that prioritize personalized marketing and relationship management.

Supermarkets and hypermarkets cater to everyday consumers, seamlessly blending supplement shopping with their grocery runs. In contrast, "other distribution channels", encompassing health food stores, fitness centers, and direct sales, hone in on niche markets with tailored product offerings. The distribution landscape is shifting towards omnichannel strategies, merging physical and digital experiences. Retailers are finding success by blending online ordering with in-store pickup and expert consultations, catering to the varied needs of consumers. E-commerce platforms, with their advanced targeting and personalization, outpace traditional retail methods, granting brands a competitive edge when they invest in digital marketing and data analytics.

Geography Analysis

In 2025, North America commanded a 31.85% share of the lifestyle-related disease supplements market. This dominance is bolstered by a deep-rooted supplement culture, strong direct-selling networks, and the favorable DSHEA regulations that expedite product turnover. Furthermore, physicians routinely recommend omega-3 fatty acids, vitamin D, and probiotics in electronic medical records, thereby solidifying their everyday use. Marketing strategies have evolved, now emphasizing longevity and metabolic vitality over individual nutrients, ensuring sustained consumer engagement.

Europe's unwavering demand is bolstered by stringent regulations that foster consumer trust. In 2024, the European Food Safety Authority's Ingredient Correction Process streamlined dossier reviews by 15%, enhancing the availability of products across borders. While Latin America and the Middle East & Africa boast a burgeoning urban middle class, challenges like fragmented logistics and income disparities temper their growth. Notably, e-commerce leaders in South America are investing in cold-chain solutions for temperature-sensitive probiotics, indicating an impending surge in the market.

Asia-Pacific is on a trajectory with an 8.20% CAGR projected through 2031, positioning it as a pivotal arena. In nations like China, India, and across Southeast Asia, swift urbanization, expanded insurance coverage, and public health initiatives targeting diabetes are driving the demand. Traditional practices, such as Ayurveda and Traditional Chinese Medicine, are melding with modern supplementation, leading to innovative formulations that marry age-old botanicals with contemporary delivery methods. To bolster domestic production and lessen import dependence, governments are rolling out incentives like tax breaks and expedited approvals for facilities adhering to international Good Manufacturing Practice standards.

Competitive Landscape

The global lifestyle-disease supplements market is fragmented as multinationals acquire specialist brands to scale and diversify. The lifestyle-related disease supplements market is trending toward consolidation, despite its moderate level of fragmentation. Nestlé Health Science’s 2025 acquisition of The Bountiful Company, which includes Nature’s Bounty and Solgar, enhances its multichannel reach and solidifies its scientific credentials. Meanwhile, Amway’s USD 375 million capacity expansion highlights a broader industry trend toward vertical integration, emphasizing the importance of raw material traceability and availability amid potential supply shocks.

Digital natives are disrupting traditional players by offering subscription-based, personalized nutrition powered by AI-driven quizzes. These newcomers leverage detailed data, enabling swift product iterations and a quicker turnaround from identifying consumer needs to launching products. Collaborations between ingredient suppliers and wearable tech firms are paving the way for new, data-backed claims, setting a high bar for companies without advanced research and development capabilities.

Purchasing choices, particularly among millennial and Gen Z consumers, are swayed by sustainability markers like marine-stewardship certifications and upcycled plant inputs. In response, larger industry players are auditing their supply chains and releasing third-party life-cycle assessments. Concurrently, retailers are tightening shelf-entry criteria, emphasizing clinical backing and manufacturing transparency. This trend further narrows shelf space, favoring top-tier brands with strong compliance frameworks.

Lifestyle-Related Disease Supplements Industry Leaders

-

Abbott Laboratories

-

Bayer AG

-

Amway Corporation

-

Herbalife Nutrition Limited

-

Nestle S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Zeroharm launched Ayurvedic formulas for heart health, including Holo Heart Tablets, a plant-based supplement. Formulated with traditional herbs such as Shuddha Guggulu, Arjun chhal, and black garlic powder, it aimed to prevent coronary artery disease, lower cholesterol and triglyceride levels, and reduce inflammation.

- June 2025: Bioma launched Bioma Probiotics, a synbiotic supplement targeting digestive health, immune support, and mental clarity through microbiome balance. The vegan, non-GMO, and gluten-free capsules contain over 40 billion CFUs from 11 probiotic strains, a prebiotic complex (including xylooligosaccharides), and a postbiotic complex (including tributyrin) to support gut health and balance.

- February 2025: Omega-3 ingredient specialist GC Rieber VivoMega introduced two new proprietary production technologies, VivoTech and VivoSure, along with Algae 1060 TG Premium, a high-quality, cost-effective, algal-based DHA and EPA omega-3 concentrate. The new product was vegan-certified, made from non-GMO algae, and processed using gentle technology to ensure superior quality and bioavailability, positioning it as a sustainable option for a range of heart-health supplements.

- February 2025: Ingredient supplier Balchem signed a multi-year partnership with the FC Bayern Women's soccer team to promote its patented vitamin K2 brand, K2VITAL. This collaboration aims to raise consumer awareness about the benefits of vitamin K2 for cardiovascular and bone health through joint campaigns, dynamic in-game branding, and social media content.

Global Lifestyle-Related Disease Supplements Market Report Scope

Lifestyle-related disease supplements are majorly consumed with a prime intention to enhance the intake of essential nutrients for the body. The global lifestyle-related disease supplements market (henceforth referred to as the market studied) is segmented by product type, form, distribution channel, and geography. By product type, the market is segmented into Heart Health Supplements, Bone and Joint Health supplements, Digestive Health Supplements, Brain Health Supplements, and Other Supplements. Based on form, the market is segmented into Tablets, Powder, and Others. Based on the distribution channel, the market studied is segmented into Supermarkets/Hypermarkets, Pharmacies & Drug Stores, Online Retail Stores, and Other Distribution channels. It provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Heart-Health Supplements |

| Bone & Joint-Health Supplements |

| Digestive-Health Supplements |

| Brain-Health Supplements |

| Weight-Management Supplements |

| Other Lifestyle-Focused Supplements |

By Form

| Powder |

| Capsules |

| Softgels |

| Gummies |

| Effervescent Tablets |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty/Drug Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Heart-Health Supplements | |

| Bone & Joint-Health Supplements | ||

| Digestive-Health Supplements | ||

| Brain-Health Supplements | ||

| Weight-Management Supplements | ||

| Other Lifestyle-Focused Supplements | ||

| By Form | Powder | |

| Capsules | ||

| Softgels | ||

| Gummies | ||

| Effervescent Tablets | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty/Drug Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the lifestyle-related disease supplements market in 2031?

The sector is forecast to reach USD 89.22 billion by 2031.

Which region shows the fastest growth for lifestyle-focused supplements?

Asia Pacific leads with an 8.20% CAGR through 2031, driven by urbanization and preventive-care policies.

Which product category currently dominates sales?

Weight-management formulations held 26.72% of 2025 revenue.

Why are gummies gaining popularity as a delivery format?

Gummies combine taste, convenience, and improved heat-stable technology, fueling a 9.35% CAGR.

How are regulatory differences affecting global expansion?

Disparate approval and labeling rules compel companies to tailor dossiers by market, extending launch timelines and inflating costs.

What sustainability measures resonate with supplement consumers?

Certifications such as Friend of the Sea and transparent ingredient sourcing increasingly influence purchasing decisions.

Page last updated on: