Weight Loss Supplements Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

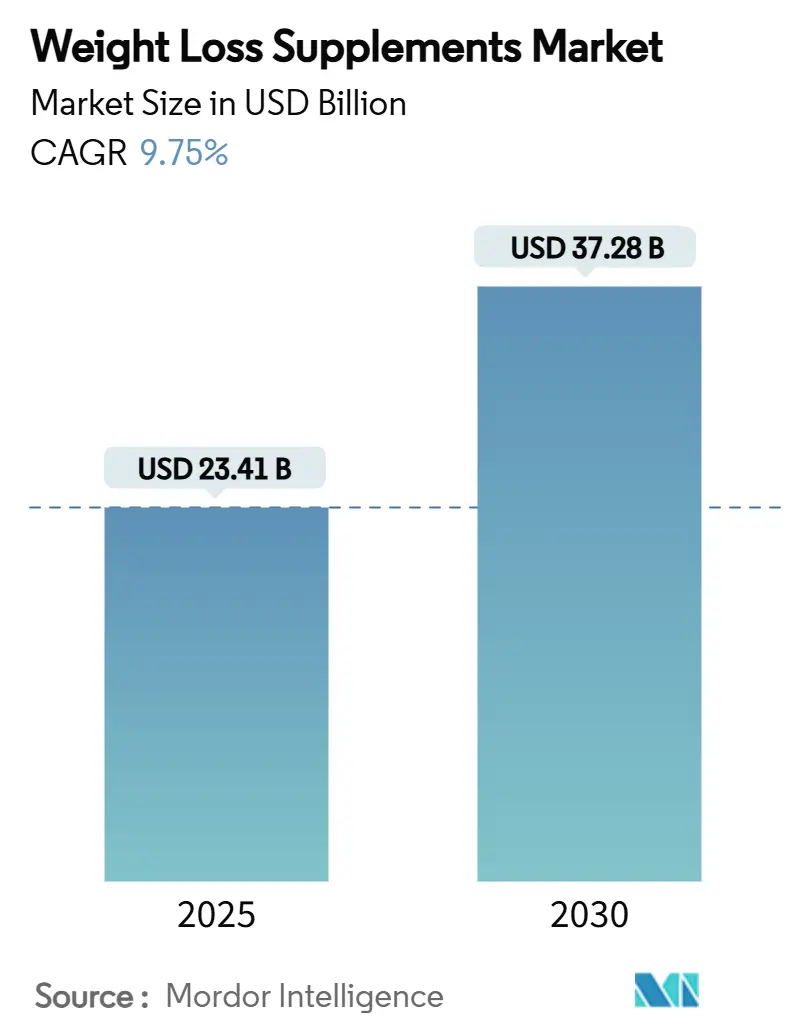

| Market Size (2025) | USD 23.41 Billion |

| Market Size (2030) | USD 37.28 Billion |

| Growth Rate (2025 - 2030) | 9.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Weight Loss Supplements Market Analysis by Mordor Intelligence

In 2025, the weight loss supplements market size was valued at USD 23.41 billion. Projections indicate it will reach USD 37.28 billion by 2030, marking a robust CAGR of 9.75%. The surge in demand is driven by a global uptick in obesity rates, a rising inclination towards natural formulations, and a robust digital marketing push. Meanwhile, the emergence of companion products for Glucagon-like peptide-1 therapies is reshaping the competitive landscape. While North America continues to lead in revenue, the Asia-Pacific region is witnessing the fastest growth, spurred by rising disposable incomes and heightened health awareness. Brands are now prioritizing clean-label ingredients, swift e-commerce deliveries, and substantiated claims to bolster consumer trust, especially amidst tightening regulations. Traditional direct-selling giants are feeling the heat from digitally-savvy newcomers, who are leveraging micro-targeted marketing and subscription models, amplifying competition in the weight loss supplements arena.

Key Report Takeaways

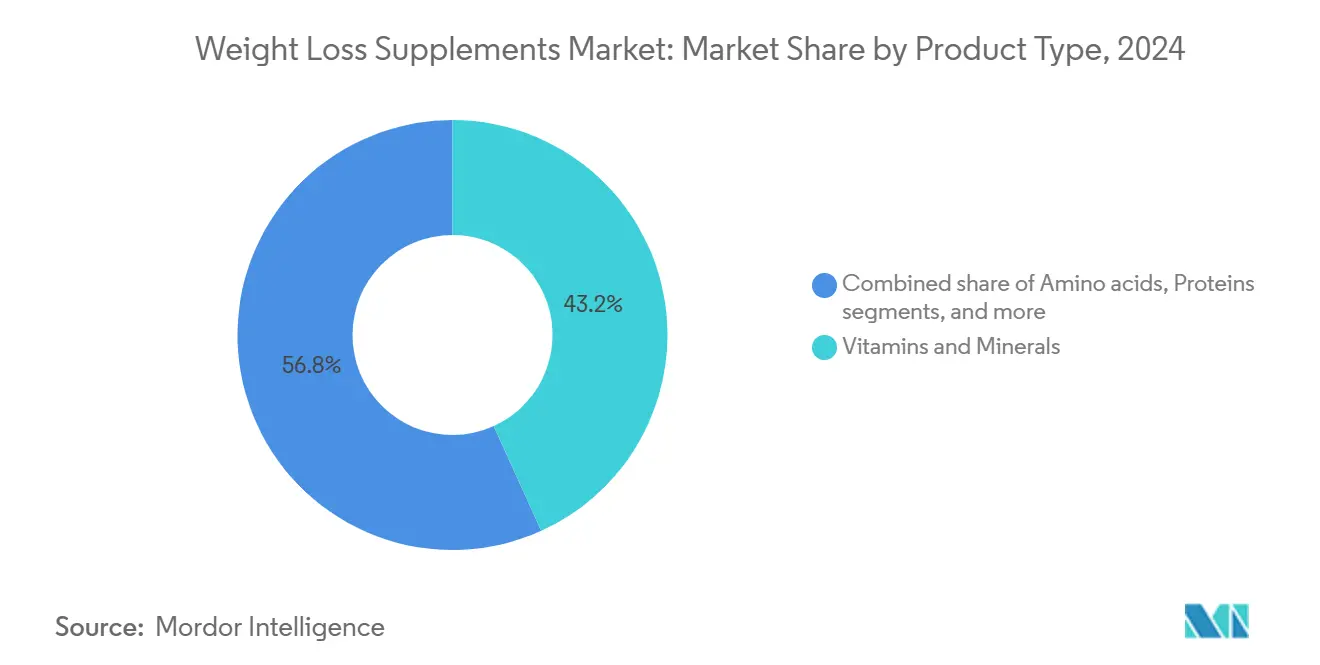

- By product type, vitamins and minerals led with a 43.23% revenue share in 2024, while botanical extracts are projected to post a 9.85% CAGR through 2030.

- By end user, women accounted for 52.99% of the Weight loss supplements market share in 2024; the men’s segment is forecast to expand at an 11.63% CAGR between 2025 and 2030.

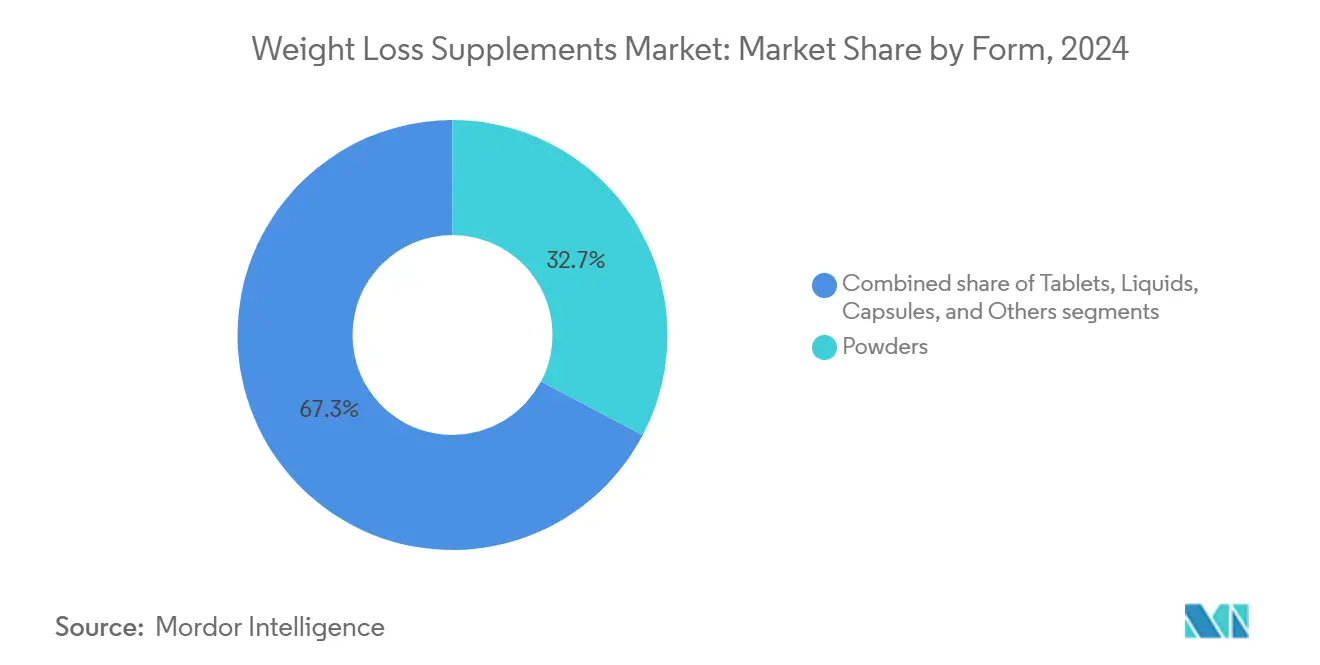

- By form, powders captured 32.71% of the Weight loss supplements market size in 2024, whereas liquids are poised to advance at an 8.63% CAGR to 2030.

- By distribution channel, online retail stores commanded 35.83% of revenue in 2024 and are projected to grow at a 12.73% CAGR through 2030.

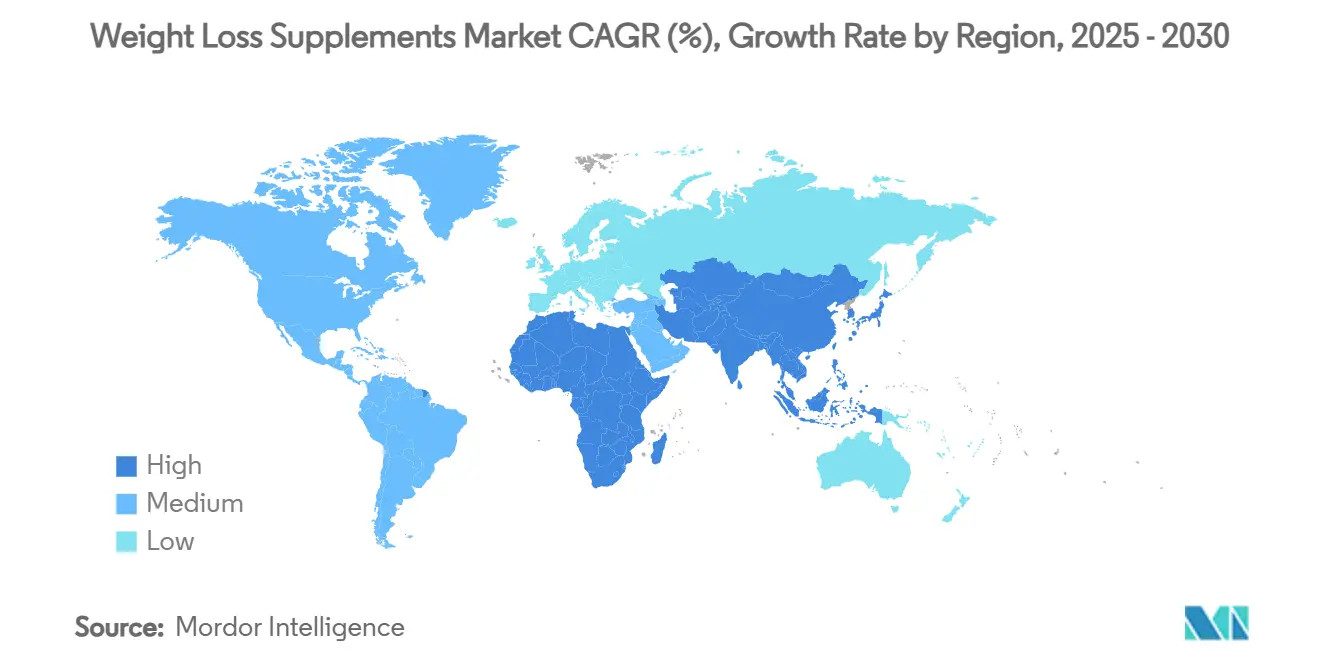

- By geography, North America held 38.49% of global sales in 2024, while Asia-Pacific is forecast to record the fastest 10.85% CAGR between 2025 and 2030.

Global Weight Loss Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fitness and active lifestyle movements | +2.5% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Influence of social media and digital marketing | +1.8% | Global, particularly strong in Asia-Pacific and North America | Short term (≤ 2 years) |

| Technology-driven product innovation | +1.2% | North America and Europe leading, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Surge in obesity and associated health risks | +0.9% | Global, with highest impact in North America and Middle East | Long term (≥ 4 years) |

| Demand for natural and clean-label ingredients | +0.7% | North America and Europe primarily, growing in Asia-Pacific | Medium term (2-4 years) |

| Convenient access via e-commerce and retail innovations | +0.6% | Global, with fastest adoption in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fitness and active lifestyle movements

The growing emphasis on fitness culture and the adoption of active lifestyles are significantly transforming the demand for weight loss supplements. According to the Council for Responsible Nutrition (CRN), 74% of U.S. adults used dietary supplements in 2023, reflecting a substantial rise compared to previous years[1]Council for Responsible Nutrition, "2023 CRN Consumer Survey on Dietary Supplements", www.crnusa.org. This trend is no longer limited to traditional gym-goers but has expanded to include workplace wellness programs, community fitness initiatives, and digital fitness platforms that seamlessly incorporate supplement recommendations into their ecosystems. Younger demographics are leading this shift, viewing weight management as a core component of a holistic wellness approach rather than a short-term solution. Social media fitness influencers and wellness advocates play a pivotal role in driving this adoption by sharing authentic testimonials and integrating supplements into their daily routines, thereby creating sustained demand that surpasses seasonal weight loss trends. Additionally, CRN data indicates that supplement usage increases with age, peaking at 40% among individuals aged 55 and older. This demonstrates the fitness movement's ability to engage older demographics, who have traditionally relied on conventional weight loss methods, further broadening the market's reach and influence.

Influence of social media and digital marketing

Digital marketing is changing how weight loss supplements are sold, but new regulations are both helping and limiting this growth. In August 2024, the Federal Trade Commission introduced a rule banning fake reviews, with penalties of up to USD 51,744 for each violation[2]Federal Trade Commission, "Federal Trade Commission Announces Final Rule Banning Fake Reviews and Testimonials", www.ftc.gov. This has pushed companies to move away from focusing on the number of reviews and instead focus on real customer experiences and clinical proof. Another proposed rule by the FTC, expected in January 2025, will limit how companies promote income opportunities tied to weight loss products. This will especially impact direct-selling companies like Herbalife and Amway. Social media platforms like TikTok and Instagram are now key places where people discover new supplement brands, often making certain ingredients and products go viral. Established companies face the challenge of keeping their brand stories genuine while competing with new brands that use targeted digital ads to grow quickly. Companies now need to balance strong digital marketing strategies with the following rules that require proof for all health claims and income promises.

Technology-driven product innovation

The convergence of biotechnology and nutritional science is driving the development of next-generation weight loss supplements that target specific metabolic pathways. Companies such as Herbalife are introducing GLP-1 Nutrition Companion Product Combos, designed to complement pharmaceutical weight loss drugs. This strategic shift highlights the industry's recognition that traditional appetite suppressants and metabolism boosters must evolve to remain competitive in an era dominated by highly effective pharmaceutical interventions. The FDA's updated guidance on New Dietary Ingredient Notification Procedures, released in March 2024, is streamlining the approval process for innovative formulations. This regulatory change is expected to accelerate the introduction of novel compounds and advanced delivery systems, fostering innovation in the market. Technological advancements, including microencapsulation and time-release formulations, are enabling precise dosing and improving the bioavailability of active ingredients, enhancing the efficacy of these supplements. Companies are increasingly investing in proprietary research to develop evidence-based formulations that meet stringent regulatory requirements while delivering measurable outcomes. Additionally, the integration of personalized nutrition platforms with supplement recommendations is creating significant opportunities for customized weight loss solutions. These platforms leverage individual metabolic profiles and genetic markers to offer tailored strategies, aligning with the growing demand for personalized healthcare solutions.

Surge in obesity and associated health risks

The global obesity epidemic is fueling a rising demand for weight loss interventions. The National Institutes of Health highlights that complications from obesity are unveiling new therapeutic targets for supplement manufacturers. Developed markets, grappling with sedentary lifestyles and a penchant for processed foods, are witnessing a pronounced demand for weight management solutions. Initially perceived as rivals, the advent of GLP-1 weight loss drugs is, in fact, broadening the weight management market. These drugs are not only legitimizing pharmaceutical methods but also emphasizing weight loss as a medical imperative, overshadowing its previous image as merely a cosmetic concern. Healthcare providers are now endorsing supplement regimens alongside prescription weight loss medications, paving the way for new distribution avenues through medical practices and specialized clinics. The Centers for Disease Control and Prevention endorsement of programs like Herbalife's Lifestyle Intervention Program as certified Diabetes Prevention Programs underscores the deepening integration of supplements into mainstream healthcare. This endorsement is not just a nod from the medical community; it's a powerful tool diminishing consumer skepticism and amplifying the weight of healthcare professionals' recommendations, far surpassing traditional marketing efforts.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent and inconsistent regulatory scrutiny | -1.4% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

| Counterfeit and unregulated products | -0.8% | Global, particularly problematic in Asia-Pacific and online channels | Short term (≤ 2 years) |

| Environmental and supply chain concerns | -0.6% | Europe and North America leading, expanding globally | Long term (≥ 4 years) |

| Negative perceptions of synthetic ingredients | -0.5% | North America and Europe primarily, growing in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent and inconsistent regulatory scrutiny

Regulatory enforcement is increasing across many regions, with the FDA sending several warning letters in 2024 to companies selling unapproved weight loss products with hidden drug ingredients. In December 2024, the FDA warned Veronvy for selling unapproved weight loss supplements, showing its ongoing efforts to stop companies from making unauthorized drug claims. At the same time, the FDA's 2025 restructuring, which included cutting about 3,500 staff members, including 170 from the Office of Inspections and Investigations, is raising concerns about how consistent enforcement and inspections will be. This situation, where stricter enforcement standards meet reduced oversight capacity, is making it harder for legitimate companies to comply while possibly letting problematic products stay in the market longer. The FDA's inability to meet inspection targets, covering only 5% of known dietary supplement facilities in fiscal 2024, indicates that regulatory gaps may continue despite stronger enforcement messages. Companies need to adapt by setting up strong self-regulation measures and preparing for inconsistent enforcement actions that could disrupt their operations unexpectedly.

Counterfeit and unregulated products

Counterfeit weight loss supplements are eroding consumer trust and jeopardizing safety, casting a shadow over the industry's reputation. This challenge was underscored by the FDA's March 2025 alert regarding perilous online products laced with concealed active ingredients. Testing by the agency unveiled that a notable fraction of items bought from prominent online platforms harbored undeclared pharmaceutical components, endangering consumers who believed they were acquiring mere dietary supplements. Furthermore, the FDA's August 2024 caution about tejocote root supplements being tampered with toxic yellow oleander underscores the immediate health dangers posed by such counterfeit products. E-commerce platforms grapple with the challenge of overseeing third-party sellers, allowing counterfeit goods to infiltrate the market, despite their attempts at verification. This issue is magnified for international suppliers, often escaping the stringent regulatory scrutiny faced by domestic producers. Meanwhile, legitimate businesses, facing these challenges, are compelled to pour resources into anti-counterfeiting initiatives, such as blockchain verification and public awareness drives. These measures, while crucial, inflate operational costs without yielding direct financial returns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vitamins Lead While Botanicals Accelerate

In 2024, vitamins and minerals hold the largest market share at 43.23%, driven by their widespread acceptance, established safety profiles, and frequent recommendations by healthcare professionals for weight management. According to the CDC's National Health and Nutrition Examination Survey, vitamin D and multivitamin-mineral products rank among the most commonly used supplements, with 18.5% of adults reporting vitamin D usage. This segment's dominance highlights the critical role of micronutrients in supporting metabolic processes and the consumer perception that vitamin-based weight loss supplements are safer compared to synthetic alternatives. The Food and Drug Administration's Current Good Manufacturing Practice regulations further strengthen consumer confidence by ensuring the quality and consistency of vitamin and mineral formulations. Additionally, healthcare providers often recommend these supplements as part of comprehensive weight management strategies, particularly for individuals with dietary limitations or metabolic conditions that hinder nutrient absorption.

Natural and botanical extracts are emerging as the fastest-growing segment, with a projected CAGR of 9.85% from 2025 to 2030, reflecting a significant consumer shift toward plant-based solutions and clean-label formulations. The Food and Drug Administration's March 2024 guidance on New Dietary Ingredient Notification Procedures plays a pivotal role in this segment, requiring botanical extract manufacturers to navigate complex approval processes for novel plant compounds while demonstrating their safety and efficacy. This growth is fueled by increasing consumer awareness of traditional medicine practices and the perception that natural ingredients are associated with fewer side effects compared to synthetic compounds. Companies are heavily investing in advanced extraction technologies and standardization processes to ensure consistent potency and bioavailability of active botanical compounds. Furthermore, the segment benefits from growing scientific research validating the effectiveness of specific plant extracts for weight management, enabling companies to make evidence-based marketing claims that appeal to health-conscious consumers.

By End User: Women Dominate While Men's Segment Surges

In 2024, women dominate the market, holding a 52.99% share, consistent with historical trends of heightened supplement usage and a proactive approach to weight management. Data from the Council for Responsible Nutrition reveals that 52% of women turn to dietary supplements, outpacing the 48% of men. This female predominance is bolstered by a pronounced health consciousness, a proactive stance on preventive health investments, and more frequent consultations with healthcare providers, often leading to supplement recommendations. Women gravitate towards supplements that promise holistic wellness, prioritize natural ingredients, and address multiple health concerns concurrently. This trend paves the way for innovative formulations that seamlessly blend weight management with beauty, energy, and hormonal support. Furthermore, this segment's stability is underscored by long-standing purchasing habits and a deep-rooted brand loyalty, cultivated over decades of market evolution.

Meanwhile, the men's segment is witnessing a surge, boasting an impressive 11.63% CAGR from 2025-2030. This growth signals a pivotal shift in male perceptions regarding weight management and supplement consumption. Data from the National Center for Biotechnology Information highlights a rising trend in supplement usage among men, especially pronounced among non-Hispanic Blacks, Hispanics, and low-income adults. This male-centric growth can be attributed to a diminishing stigma surrounding weight loss, a change largely fueled by the fitness narratives proliferating on social media and a heightened awareness of health risks tied to obesity, such as cardiovascular diseases and diabetes. Men's supplement choices lean towards performance enhancement, muscle preservation, and formulations rooted in scientific validation. This creates a niche for products that seamlessly integrate weight loss into the broader narrative of fitness and performance enhancement. Notably, the segment's growth is most pronounced among the 25-45 age bracket, driven by career demands and lifestyle choices that amplify health awareness and a readiness to invest in supplements.

By Form: Powders Maintain Leadership While Liquids Gain Traction

In 2024, powders command a 32.71% market share, capitalizing on their versatility, cost-effectiveness, and the ability to tailor serving sizes to individual preferences. Their popularity stems from compatibility with diverse consumption methods: whether mixed in beverages, added to food recipes, or combined with other supplements for personalized nutrition. From a manufacturing standpoint, powders boast advantages like a longer shelf life, lower shipping costs, and the capacity to incorporate higher concentrations of active ingredients, sidestepping the stability issues often seen with liquids. The FDA's nutrition labeling mandates for dietary supplements offer clear directives for powder formulations, ensuring uniformity in serving size declarations and accuracy in nutrient content. Fitness enthusiasts, in particular, favor powders, valuing the control they offer over supplement timing and dosage, solidifying the segment's market dominance.

Liquids are emerging as the fastest-growing segment, projected to achieve an 8.63% CAGR from 2025-2030. This surge is largely attributed to consumer desires for convenience and a belief in quicker absorption rates compared to solids. Enhanced taste profiles and the ready-to-consume nature of liquids eliminating prep time make them especially appealing to busy professionals and those seeking instant supplementation. Innovations in liquid manufacturing now allow for higher concentrations of active ingredients without compromising taste or stability. This not only paves the way for premium market positioning but also bolsters efficacy claims. Furthermore, advancements in packaging technology are addressing past stability issues, extending shelf life and preserving ingredient potency. While consumer sentiment leans towards viewing liquid supplements as more bioavailable and quicker-acting than their solid counterparts despite scant scientific backing, this presents a lucrative marketing avenue for companies that can validate such claims through clinical research.

By Distribution Channel: Online Retail Dominates and Accelerates

In 2024, online retail stores not only captured the largest market share at 35.83%, but also boasted the fastest growth rate, projected at a 12.73% CAGR from 2025 to 2030. This trend underscores a significant and lasting shift in consumer purchasing behavior towards digital channels. Such a dual dominance is a first for the supplement industry, highlighting a fundamental transformation in retail dynamics. While the COVID-19 pandemic accelerated this shift, it has been further bolstered by enhanced logistics networks and growing consumer comfort with purchasing health products online. Online platforms empower consumers with detailed product information, ingredient transparency, and comparison tools, facilitating informed purchasing decisions. Simultaneously, these platforms allow companies to forge direct-to-consumer relationships, sidestepping traditional retail markups and enabling tailored marketing strategies.

The growth of the online channel is bolstered by several inherent advantages: round-the-clock availability, subscription models that guarantee steady revenue, and the capability to cater to niche segments often overlooked by traditional retailers. E-commerce platforms are now harnessing advanced recommendation algorithms, suggesting complementary products and tailored nutrition solutions based on individual health aspirations and past purchases. This expansion is especially notable in the direct-to-consumer realm. Here, supplement companies enjoy elevated profit margins and cultivate direct customer relationships through educational content, personalized assistance, and loyalty initiatives. Data reveals that online supplement buyers are not only more diligent in product research and label scrutiny but also more attuned to evidence-based marketing claims. This presents a golden opportunity for companies prioritizing educational content and scientifically substantiating their product benefits.

Geography Analysis

In 2024, North America leads the market with a 38.49% share, fueled by high obesity rates, a well-entrenched supplement culture, and stringent regulatory frameworks that prioritize product quality and safety. The region's market is characterized by sophisticated distribution networks, strong brand loyalty, and consumers willing to pay a premium for scientifically-backed formulations. While the FDA's heightened enforcement poses compliance challenges, it simultaneously bolsters consumer trust in legitimate products and offers a competitive edge to companies with stringent quality control. The integration of weight loss supplements into healthcare, exemplified by programs like Herbalife's CDC-certified Diabetes Prevention Program, underscores the growing medical endorsement of these interventions.

Asia-Pacific is set to be the fastest-growing region, with a projected CAGR of 10.85% from 2025-2030. This growth is attributed to rising disposable incomes, heightened health awareness, and the adoption of Western lifestyle habits, including supplement consumption. Highlighting this trend, the National Bureau of Statistics of China reports a rise in the average annual per capita disposable income for Chinese households, jumping from 39,218 yuan in 2023 to approximately 41,300 yuan in 2024[3]National Bureau of Statistics of China, "Average annual per capita disposable income of households in China from 1990 to 2024", www.stats.gov.cn. Urban centers, with their fast-paced lifestyles and reliance on processed foods, are witnessing a pronounced demand for convenient weight management solutions. Yet, companies like USANA are noting a cautious consumer sentiment in certain Asia-Pacific markets, suggesting that growth may vary across countries and demographics. As countries in the region roll out new standards for supplement safety and efficacy, the initial slowdown in market entry could pave the way for heightened consumer trust.

Europe, with its mature market, places a premium on natural and organic formulations, a trend driven by strict regulatory mandates and a consumer preference for clean-label products. The continent's commitment to sustainability and environmental responsibility is shaping product development and packaging choices, presenting opportunities for companies that prioritize environmental stewardship. Meanwhile, South America and the Middle East and Africa stand as emerging markets with vast growth potential. However, their development is hampered by regulatory ambiguities, distribution hurdles, and varying degrees of consumer awareness regarding supplement benefits and safety.

Competitive Landscape

The weight loss supplements market is moderately fragmented, with global players and regional brands competing across diverse product formats, including pills, powders, and gummies. Key players in the market include Herbalife Nutrition Ltd., Amway Corporation, Nestlé S.A., Glanbia PLC, and GNC Holdings, LLC. Companies strive to differentiate themselves through innovative ingredients, targeted formulations such as fat burners and appetite suppressants, and clean-label positioning. Additionally, strategic partnerships, celebrity endorsements, and digital marketing campaigns further intensify the competitive landscape.

Strategic differentiation is increasingly shifting toward scientific validation, regulatory compliance, and technology integration, moving away from traditional marketing approaches. This trend is highlighted by the FTC's recent enforcement rules targeting fake reviews and unsubstantiated claims. In response, companies are significantly investing in clinical research, developing proprietary formulations, and leveraging digital platforms to offer personalized recommendations and tracking capabilities, enhancing consumer engagement and trust.

The fragmented nature of the market creates opportunities for specialized players to capture niche segments while enabling rapid scaling for companies that effectively utilize e-commerce platforms and social media marketing. White-space opportunities are emerging in areas such as personalized nutrition, male-focused formulations, and products designed to complement pharmaceutical weight loss interventions. These trends indicate that innovation, rather than scale, will be the critical factor in achieving competitive success in this evolving market landscape.

Weight Loss Supplements Industry Leaders

-

Herbalife Nutrition Ltd.

-

Amway Corporation

-

Nestlé S.A

-

Glanbia PLC

-

GNC Holdings, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Herbalife has launched MultiBurn, a science-backed, multi-action dietary supplement designed to support weight loss, healthy fat reduction, and metabolic health. According to the brand, it is formulated with clinically studied botanicals—Morosil from Moro blood oranges, Metabolaid (hibiscus and lemon verbena), and Capsifen (red chili pepper and fenugreek)—the supplement also includes caffeine and chromium to boost metabolism and maintain blood sugar levels.

- March 2025: The Vitamin Shoppe has launched GLP-1 Support from Whole Health Rx, a new line of dietary supplements specifically formulated to support individuals using GLP-1 medications for weight management. According to the brand, the line includes seven targeted formulas addressing nutrient absorption, digestive health, hydration, energy levels, and muscle support, all developed with input from healthcare professionals.

- February 2025: Euromed has launched PerFix, a persimmon extract made from Mediterranean persimmons using a patented, gentle water-based process that preserves key bioactive compounds. According to the brand, the extract is formulated to support fat loss and body composition.

- December 2024: ProSupps has expanded its product line with the launch of its new ProSupps Thermo, a fat-burning powder engineered to empower women and individuals at every stage of their fitness journey. According to the brand, ProSupps® Thermo features a blend of ingredients, including Chromax, Purecaf, InnoSlim, Neurorush, and SunPS.

Global Weight Loss Supplements Market Report Scope

| Vitamins and Minerals |

| Amino Acids |

| Proteins |

| Natural/Botanical Extracts |

| Others (Collagen) |

| Men |

| Women |

| Powders |

| Tablets |

| Capsules |

| Liquids |

| Others (Gummies) |

| Supermarkets/Hypermarkets |

| Health and Wellness Stores |

| Online Retail Stores |

| Other Distribution Channels (Convenience stores) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Vitamins and Minerals | |

| Amino Acids | ||

| Proteins | ||

| Natural/Botanical Extracts | ||

| Others (Collagen) | ||

| By End User | Men | |

| Women | ||

| By Form | Powders | |

| Tablets | ||

| Capsules | ||

| Liquids | ||

| Others (Gummies) | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Health and Wellness Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels (Convenience stores) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Weight loss supplements market?

The market was valued at USD 23.41 billion in 2025 and is forecast to reach USD 37.28 billion by 2030 at a 9.75% CAGR.

Which region leads sales of weight loss supplements?

North America held 38.49% of global revenue in 2024 due to high obesity rates, strong retail infrastructure, and rigorous quality standards.

Which product type is growing fastest?

Botanical extracts are projected to expand at a 9.85% CAGR through 2030, outpacing all other ingredient categories.

Why are online channels important for supplement sales?

Online stores already account for 35.83% of revenue and are growing at a 12.73% CAGR thanks to convenience, broad assortments, and robust review systems.

Page last updated on: