Pre-Workout Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

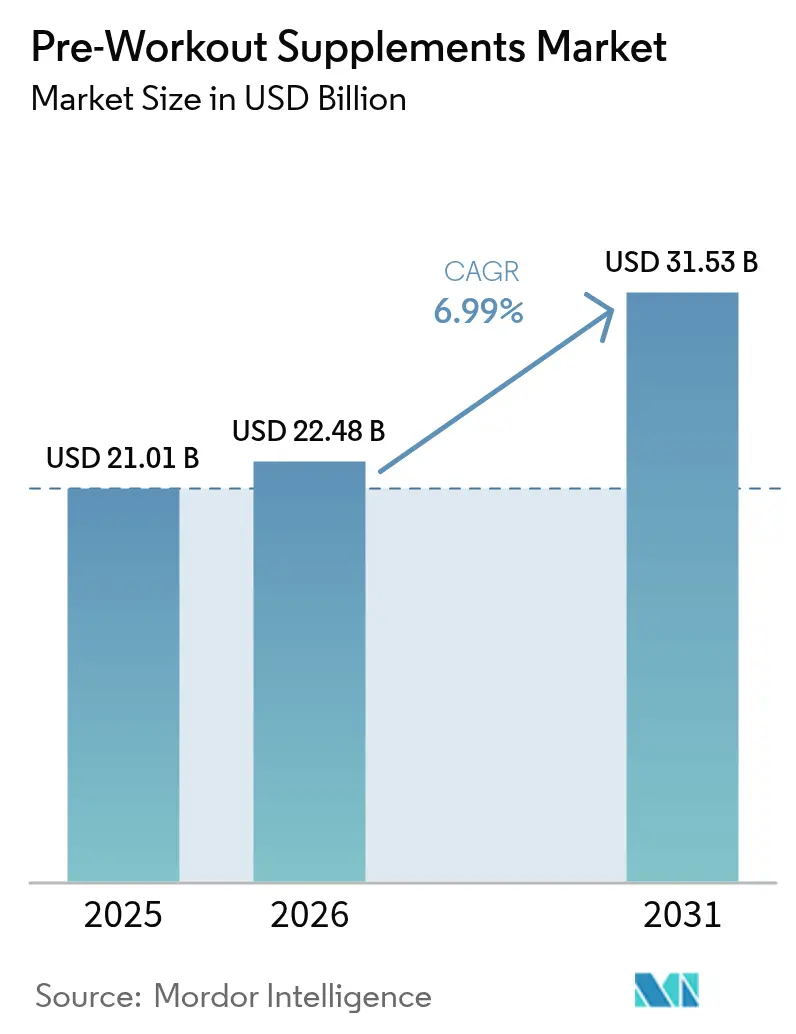

| Market Size (2026) | USD 22.48 Billion |

| Market Size (2031) | USD 31.53 Billion |

| Growth Rate (2026 - 2031) | 6.99% CAGR |

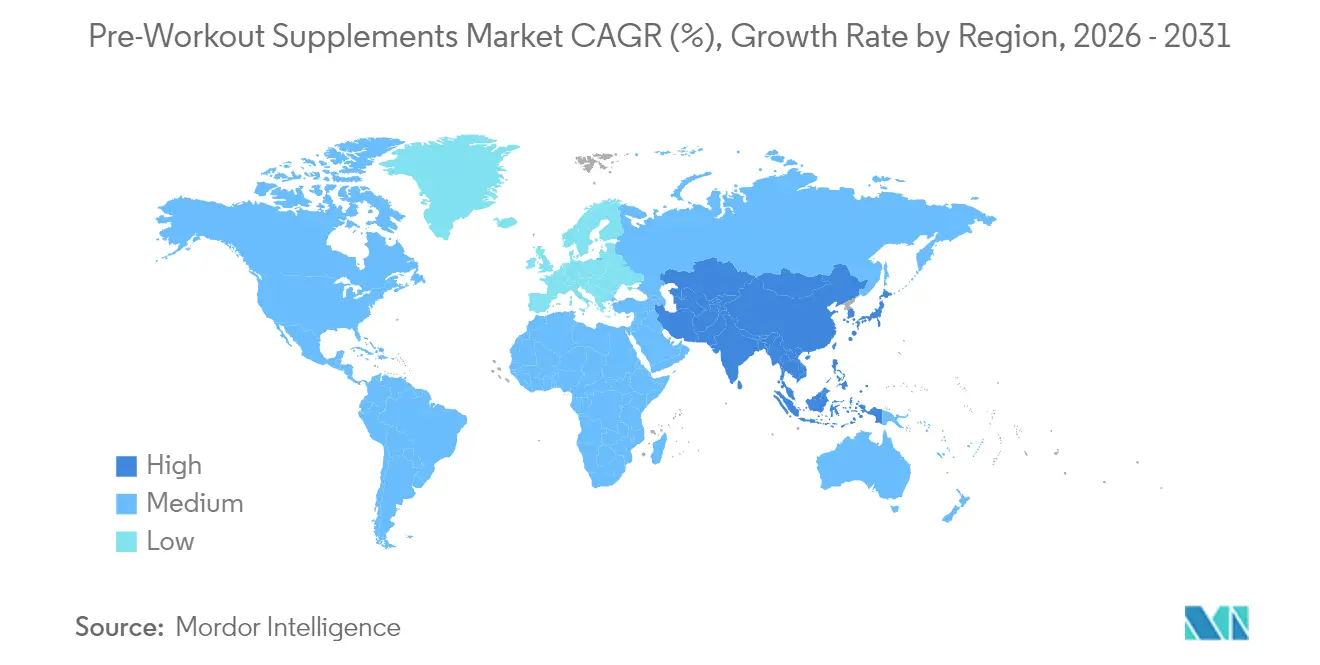

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

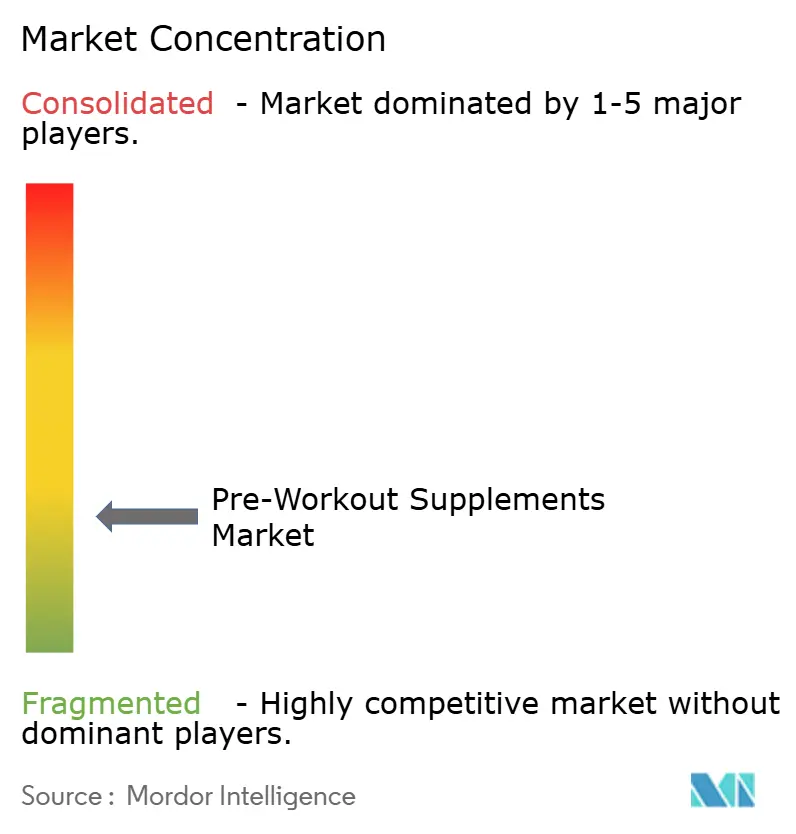

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pre-Workout Supplements Market Analysis by Mordor Intelligence

The pre-workout supplements market size was valued at USD 21.01 billion in 2025. The pre-workout supplements market was valued at USD 21.01 billion in 2025 and estimated to grow from USD 22.48 billion in 2026 to reach USD 31.53 billion by 2031, at a CAGR of 6.99% during the forecast period (2026-2031). This growth underscores a heightened consumer interest in performance nutrition, a more defined regulatory environment, and continuous ingredient innovations. March 2024 saw the U.S. FDA roll out updated guidelines on New Dietary Ingredient notifications. These changes offer formulators clearer pathways to safely introduce novel compounds. North America remains the dominant player, boasting the largest revenue share. In contrast, the Asia-Pacific region is witnessing swift growth, driven by an expanding fitness infrastructure and increasing disposable incomes. While powder formats lead the market, ready-to-drink liquids are surging in popularity, thanks to their convenience. Stimulant-based products dominate consumption, yet there's a notable rise in stimulant-free options, especially among women and those training later in the day. Caffeine remains the ingredient of choice, but adaptogens and nootropics are swiftly carving out their niche. In response to new tariffs on imports from Canada, Mexico, and China, manufacturers are recalibrating their sourcing strategies, facing heightened costs for both raw materials and finished products.

Key Report Takeaways

- By form, powder products captured 64.42% of the pre-workout supplements market share in 2025, whereas liquid formats are projected to expand at a 7.59% CAGR to 2031.

- By nature, stimulant-based offerings led with 79.42% revenue share in 2025; stimulant-free lines are advancing at a 9.32% CAGR through 2031.

- By ingredient type, caffeine commanded 86.45% share of the pre-workout supplements market size in 2025, while adaptogens and nootropics are forecast to grow at 9.34% CAGR.

- By distribution channel, specialty and health stores held 63.15% share in 2025; online retail is anticipated to rise at an 7.95% CAGR between 2026-2031.

- By geography, North America led with 37.72% of global revenue in 2025, while Asia-Pacific records the fastest regional CAGR of 8.33% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pre-Workout Supplements Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing gym memberships and fitness club enrollments boosts growth of supplements | +1.2% | Global, with strongest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Influence of fitness influencers and athletes promoting supplement routines | +0.8% | Global, particularly strong in North America and Europe | Short term (≤ 2 years) |

| Expanding awareness of sports nutrition among millennials and Generation Z | +1.0% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Availability of stimulant-free and vegan pre-workout options broadening appeal | +0.9% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Women's participation in strength training expands non-stimulant supplement market | +0.7% | Global, with strongest growth in developed markets | Long term (≥ 4 years) |

| Rising disposable incomes leading to increased spending on health products | +1.1% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing gym memberships and fitness club enrolments boosts growth of supplements

The global expansion of fitness infrastructure is significantly driving the adoption of pre-workout supplements. The ACSM's 2025 Worldwide Fitness Trends report identifies wearable technology and mobile exercise apps as leading trends, highlighting a growing reliance on data-driven fitness solutions. This technological integration aligns seamlessly with the optimization of supplement usage, as consumers increasingly use these tools to enhance their workout performance and track progress. Fitness facilities are increasingly collaborating with supplement brands to establish in-gym retail setups, creating strategic opportunities to capture immediate post-workout sales. These partnerships not only enhance brand visibility but also leverage the heightened motivation of gym-goers, driving impulse purchases. Furthermore, the presence of qualified exercise professionals within gym environments plays a pivotal role in educating consumers about the benefits and proper usage of pre-workout supplements. This guidance helps mitigate consumer hesitations and fosters informed decision-making. Gym partnerships often extend to these affiliated retail locations, enhancing product accessibility and driving additional sales. The convergence of fitness infrastructure, technological advancements, and strategic retail collaborations is reshaping the pre-workout supplement market, creating a robust ecosystem that supports sustained growth.

Influence of fitness influencers and athletes promoting supplement routines

Social media has significantly transformed supplement marketing, shifting the approach from traditional advertising to peer-driven recommendation systems. Influencers, with their perceived authenticity, have become key drivers of purchasing decisions, often outperforming conventional promotional strategies. The rise of female-focused sports nutrition brands, such as Alani Nu and Women's Best, highlights how targeted influencer collaborations can effectively penetrate and expand market segments that were historically male-dominated. By transparently sharing their supplement stacks and timing protocols, athletes provide consumers with actionable insights that traditional marketing methods fail to replicate. This trend influences not only product selection but also consumption behaviors, as influencers shape preferences for specific ingredient combinations and usage timings. Consequently, manufacturers are compelled to align their product development strategies with these evolving consumer demands. Furthermore, the growing emphasis on authenticity in influencer marketing has heightened the importance of clinical research. As consumers increasingly scrutinize supplement claims, they seek evidence-based recommendations, making scientific validation a critical factor in building trust and credibility.

Expanding awareness of sports nutrition among millennials and Generation Z

Millennials and Gen Z are driving a transformative shift in the sports nutrition market by adopting a research-driven approach to optimize their performance outcomes. Leveraging digital tools, these tech-savvy consumers actively seek detailed insights into ingredient mechanisms and product efficacy. According to the U.S. Census Bureau, millennials, who represent 21.81% of the U.S. population in 2024, are the largest generational group, followed closely by Generation Z at 20.81%. This demographic composition underscores a growing demand for sports nutrition products tailored to their preferences[1]US Census Bureau, "Population distribution in the United States in 2024, by generation", www.census.gov. Additionally, the increasing preference for plant-based and sustainable options among millennials and Gen Z has accelerated the development of vegan pre-workout formulations. This trend has significantly contributed to the stimulant-free segment's robust 9.43% compound annual growth rate (CAGR) during the forecast period. The consumption of educational content through platforms such as podcasts, YouTube channels, and fitness-focused websites has further cultivated a well-informed consumer base. These consumers prioritize scientific evidence to validate supplement claims and ingredient efficacy, shaping the trajectory of the sports nutrition market and driving innovation in product development.

Availability of stimulant-free and vegan pre-workout options broadening appeal

The development of effective stimulant-free formulations has significantly expanded the addressable market by including consumers previously excluded due to caffeine sensitivity, late-day training schedules, or medical contraindications to stimulant consumption. Several studies on ashwagandha supplementation highlights its substantial benefits for enhancing sports performance and brain function, offering a natural and appealing alternative to synthetic stimulants for health-conscious consumers. Additionally, vegan formulations are gaining traction within the growing plant-based consumer segment. These formulations often incorporate innovative ingredients such as beetroot extract and plant-based amino acids, which deliver unique performance benefits. The availability of such alternatives has played a crucial role in reducing the stigma surrounding pre-workout supplements, which were once perceived as extreme or unnecessary by mainstream fitness enthusiasts. Despite recent EU restrictions on 117 substances, regulatory support for botanical ingredients continues to foster innovation, creating opportunities for the development of advanced stimulant-free formulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened FDA and EFSA scrutiny on high-dose stimulants leading to product reformulation costs | -0.8% | North America and Europe | Short term (≤ 2 years) |

| Negative perceptions around synthetic additives and artificial flavors | -0.6% | Global, with stronger impact in developed markets | Medium term (2-4 years) |

| Competition from natural energy alternatives like matcha or beetroot juice | -0.4% | Global, particularly strong in health-conscious markets | Medium term (2-4 years) |

| Challenges in sourcing high-quality, safe ingredients can disrupt production and affect product quality | -0.7% | Global, with acute impact in Asia-Pacific supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened FDA and EFSA scrutiny on high-dose stimulants leading to product reformulation costs

Regulatory agencies are intensifying their oversight of stimulant dosages in pre-workout supplements, creating significant implications for manufacturers. The FDA's updated guidance on New Dietary Ingredient notifications now requires detailed safety data for any novel stimulant compounds introduced after October 1994. Similarly, the European Food Safety Authority's revised novel foods guidance, effective February 2025, introduces stricter safety assessment protocols. These changes are expected to increase both the time and costs associated with developing and launching new stimulant-based formulations. Manufacturers are facing substantial reformulation expenses, particularly for high-caffeine products that must be adjusted to comply with newly established regional safety limits. The 75-day premarket notification requirement for new dietary ingredients further extends development timelines, delaying product launches and impacting competitive positioning in the market. These regulatory developments are driving a shift toward stimulant-free alternatives, as companies seek to mitigate compliance risks and adapt to evolving consumer preferences. However, this transition is not without challenges. The shift has led to temporary market disruptions and increased compliance costs, as manufacturers navigate the complexities of reformulating existing products and developing new offerings. Despite these hurdles, the growing focus on stimulant-free alternatives presents opportunities for innovation and differentiation in the pre-workout supplement market.

Negative perceptions around synthetic additives and artificial flavors

Growing awareness of supplement adulteration has significantly heightened consumer skepticism toward synthetic ingredients. The Botanical Adulterants Prevention Program has revealed widespread dilution of herbal extracts with substances like maltodextrin and other fillers, further fueling concerns. This shift in consumer preference has driven manufacturers to prioritize clean-label products, compelling them to adopt costlier natural flavoring systems and coloring agents. While these changes align with consumer demands, they have also increased production costs and, in some cases, altered taste profiles that are critical to consumer satisfaction. The role of social media in amplifying negative supplement experiences has intensified scrutiny of ingredient lists, with consumers increasingly conducting detailed research on individual components before making purchase decisions. This heightened awareness has created significant challenges for manufacturers, particularly in maintaining product efficacy while eliminating synthetic enhancers. Reformulation efforts to meet these demands have led to delays and increased research and developmental expenditures across the industry. Powder formulations are especially impacted, as they rely heavily on flavoring and coloring systems to meet consumer expectations. The difficulty in achieving the desired taste and appearance with natural ingredients is accelerating a shift toward liquid formats, which are better suited to masking the flavors of natural components. This trend underscores the evolving dynamics of the supplement market, where balancing consumer preferences, production costs, and product efficacy remains a critical challenge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Dominance Faces Liquid Convenience Challenge

In 2025, powder formulations dominate the market with a 64.42% share, thanks to their cost-effectiveness, stable ingredients, and flexible dosages. This flexibility allows consumers to tailor serving sizes to their individual tolerance and training intensity. The powder format's lead is bolstered by efficient manufacturing and a longer shelf life. This advantage permits brands to present a rich ingredient profile at competitive prices, all while ensuring product potency remains intact throughout distribution. Traditional users of powder formulations cherish the ritual of mixing and the freedom to adjust concentration levels. This is especially true for seasoned fitness enthusiasts who are well-versed in ingredient interactions and optimal timing. Yet, powder formulations grapple with challenges: concerns over packaging waste and the inconvenience of preparation. These issues are particularly pronounced among younger consumers, who lean towards ready-to-consume options.

Liquid pre-workout supplements are emerging as the fastest-growing format, boasting a 7.59% CAGR from 2026 to 2031. Their rise is largely attributed to convenience and enhanced bioavailability, making them especially appealing to consumers pressed for time or those desiring immediate consumption. The liquid format sidesteps the need for mixing, diminishing the chances of undissolved particles—a common gripe with powders. Additionally, it allows for precise dosing, bolstering safety. Ready-to-drink variants are a hit among fitness enthusiasts on the move, especially those training in venues lacking proper mixing stations. This trend broadens the market's reach, extending beyond conventional gyms. Current trends in the sports nutrition market highlight a surging appetite for beverages, seen as both hydration and energy solutions. Ingredients such as creatine and plant-based proteins are increasingly favored in these liquid formulations. While capsules and other formats occupy a smaller niche, they cater to specific consumers. These include those desiring precise dosing without the taste or individuals with dietary restrictions that preclude powder and liquid choices.

By Nature: Stimulant-Based Formulations Face Growing Stimulant-Free Challenge

In 2025, stimulant-based pre-workout supplements hold an 79.42% market share, highlighting their established role in delivering immediate energy and focus benefits that meet consumer expectations for pre-exercise performance enhancement. This dominance is primarily attributed to caffeine's extensively documented ergogenic effects and the widespread consumer familiarity with stimulant-driven energy experiences. These factors have cultivated strong brand loyalty, as users often associate the effectiveness of pre-workout supplements with the intensity of stimulants. Traditional stimulant formulations are supported by substantial research, with studies demonstrating significant improvements in upper body resistance exercise performance when using multi-ingredient pre-workout supplements containing caffeine, beta-alanine, and L-citrulline. However, increasing regulatory scrutiny on high-dose stimulants and the introduction of caffeine limits in functional beverages are creating formulation challenges that could influence future product development strategies.

Stimulant-free pre-workout supplements are emerging as the fastest-growing segment, with a projected CAGR of 9.32% from 2026-2031. This growth is driven by the rising participation of women in strength training and an increasing preference for non-stimulant performance enhancement options. The growing involvement of women in resistance training has generated demand for supplements that enhance performance without disrupting sleep or causing stimulant-related side effects, particularly for those who train during evening hours. Research on creatine supplementation in active females has demonstrated notable performance benefits without reliance on stimulants, reinforcing the potential of stimulant-free formulations for female athletes. Additionally, the stimulant-free segment is benefiting from advancements in adaptogens and nootropics, which offer cognitive and physical performance improvements through mechanisms distinct from traditional stimulants. Sex-based research on branched-chain amino acids has further revealed varying effects on strength training performance and body composition, providing valuable insights for developing targeted stimulant-free product formulations.

By Ingredient Type: Caffeine Dominance Challenged by Adaptogen Innovation

In 2025, caffeine holds a commanding 86.45% share of the pre-workout formulation market, reaffirming its position as the primary ergogenic ingredient. Its widespread use is driven by its ability to deliver immediate energy, enhance focus, and improve performance, aligning with consumer expectations. This dominance is further supported by extensive scientific research validating its efficacy, regulatory acceptance across global markets, and cost-effectiveness, which allows manufacturers to produce high-performing formulations at competitive prices. However, upcoming regulatory changes in 2025 across the United States and European Union, which impose new caffeine limits in functional beverages, are expected to introduce formulation challenges. These changes could impact product development and dosing strategies. Additionally, the UK Food Standards Agency's updated guidance on caffeine-containing food supplements reflects increasing regulatory scrutiny, particularly concerning dosing and labeling requirements, which manufacturers must address to remain compliant.

Adaptogens and nootropics are emerging as the fastest-growing ingredient category, with a projected CAGR of 9.34% from 2026 to 2031. This growth is fueled by rising consumer interest in cognitive performance, stress management, and holistic wellness alongside physical performance benefits. Ashwagandha, a key adaptogen, has gained significant attention due to research demonstrating its benefits for brain function and sports performance. These findings provide strong scientific backing for its inclusion in pre-workout formulations. Industry players are actively investing in adaptogen research and commercialization, as evidenced by Arjuna Natural's showcase of its ashwagandha extract for cognitive support at Vitafoods Europe 2025. Clinical studies highlight its efficacy, showing a 12.22% improvement in visuospatial processing after 30 days and a 31.67% improvement after 60 days. Meanwhile, essential ingredients such as beta-alanine, creatine, citrulline, BCAAs, and electrolytes continue to play critical roles in comprehensive formulations, each targeting specific performance mechanisms to enhance overall product efficacy. The growing focus on cognitive enhancement reflects a shift in consumer preferences, emphasizing mental clarity and holistic wellness during training sessions, rather than solely prioritizing physical performance metrics.

By Distribution Channel: Specialty Stores Lead While E-commerce Accelerates

In 2025, specialty and health stores dominate the market with a significant 63.15% share, attributed to their ability to offer expert consultations, in-depth product education, and a carefully curated selection of supplements. These factors play a critical role in building consumer trust and confidence in their supplement choices. The prominence of this channel underscores the intricate nature of pre-workout supplements, where consumers rely on knowledgeable staff for personalized guidance on ingredient interactions, dosing protocols, and product recommendations tailored to their unique fitness goals and tolerance levels. Additionally, specialty stores act as discovery hubs for new brands and innovative formulations, leveraging in-store sampling and demonstration programs that traditional retail channels often fail to replicate effectively. Their competitive edge lies in fostering long-term customer relationships through personalized service and ongoing support, which extends beyond the initial purchase to include usage optimization and results tracking, ensuring sustained customer loyalty and satisfaction.

Online retailers are poised to be the fastest-growing distribution channel, with a projected CAGR of 7.95% from 2026 to 2031. This growth is driven by the convenience of online shopping, competitive pricing, and an expansive product selection that appeals to informed consumers seeking specific formulations or brands. However, the FDA's heightened scrutiny of online supplement sales, following incidents involving harmful products on platforms like Amazon, has led to stricter regulatory requirements for dietary supplement sellers, which could impact the growth trajectory of this channel. Subscription-based purchasing models and direct-to-consumer strategies are gaining momentum, enabling brands to build stronger customer relationships and capture higher profit margins compared to traditional retail distribution. On the other hand, supermarkets, hypermarkets, and other distribution channels remain vital for improving market accessibility and driving impulse purchases. However, these channels face significant challenges in providing adequate product education and standing out in crowded supplement aisles, which may limit their ability to compete effectively in the evolving market landscape.

Geography Analysis

North America commands a 37.72% market share in 2025, buoyed by its entrenched fitness culture, clear regulatory landscape, and affluent consumers leaning towards premium supplements. The region's dominance is anchored in its well-established fitness infrastructure, deep gym membership penetration, and a populace well-versed in sports nutrition, all of which foster a conducive environment for pre-workout supplement uptake. North America's regulatory frameworks offer more defined routes for product development and marketing than those in other regions, facilitating swifter innovation and market entry for novel formulations. The region's market growth is bolstered by the presence of leading supplement manufacturers and robust distribution networks, ensuring competitive pricing and product accessibility. Yet, challenges loom as the region grapples with heightened regulatory scrutiny on stimulant dosages and a burgeoning consumer preference for natural and organic formulations, necessitating costly reformulations.

Asia-Pacific is set to be the fastest-growing region, projected to grow at an 8.33% CAGR from 2026 to 2031. This growth is fueled by an expanding fitness infrastructure, rising disposable incomes, and a heightened health consciousness among the youth. The region's upward trajectory is a testament to swift urbanization, deeper gym membership penetration, and a cultural pivot towards Western fitness norms, where supplement use is becoming a staple in training regimens. Economic advancements in pivotal markets like China, India, and Southeast Asia have birthed a burgeoning middle class, eager to spend on health and fitness. Data from the State General Administration of Sports highlights that by December 2024, China boasted approximately 152 thousand gyms. With a growing emphasis on health and fitness, China has witnessed a boom in new sports and fitness facilities. Meanwhile, Europe, South America, and the Middle East and Africa stand out as vital growth markets, each with unique regulatory landscapes and consumer tastes, underscoring the need for tailored product development and marketing approaches.

Europe, while a major player, grapples with unique regulatory hurdles and prospects. A 2024 recommendation from the EU expert group to limit 117 substances in food supplements poses challenges, yet offers a competitive edge to manufacturers who comply. The European Food Safety Authority's novel foods guidance, rolling out in February 2025, lays down stringent safety assessment criteria. This not only benefits established ingredients but also erects hurdles for introducing new compounds. South America, along with the Middle East and Africa, are burgeoning markets witnessing a surge in fitness engagement and a burgeoning middle class. However, they contend with economic fluctuations and ambiguous regulatory landscapes, posing challenges for global manufacturers eyeing entry. Notably, these regions exhibit a pronounced preference for stimulant-free formulations, aligning with local inclinations for natural ingredients and steering clear of the regulatory pitfalls tied to high-stimulant products.

Competitive Landscape

The global pre-workout supplements market remains fragmented, with numerous regional and international brands competing across a wide range of formulations and price points. This competitive landscape fosters continuous innovation in ingredient compositions, flavor variations, and packaging designs to attract and retain consumer interest. Key players in the market include QNT SA, FitLife Brands, Inc., Nutrabolt LLC, BioTech USA Kft., and GNC Holdings, LLC. Smaller niche brands differentiate themselves through unique product blends or clean-label claims, while established players leverage extensive distribution networks and significant marketing budgets to sustain their market share. This fragmentation drives dynamic product development but also introduces challenges such as pricing pressures and difficulties in building brand loyalty.

Strategic trends within the industry highlight a growing focus on vertical integration and supply chain optimization. Leading companies are investing in manufacturing capabilities and establishing robust ingredient sourcing partnerships to ensure consistent quality and cost efficiency. For instance, Glanbia's Performance Nutrition segment, which includes the Optimum Nutrition and Isopure brands, exemplifies this approach. Despite facing pricing pressures from promotional activities, the segment achieved a 1.7% increase in revenue and a 3.2% rise in volume during Q3 2024, showcasing the effectiveness of its integrated strategy.

Technology adoption is playing a pivotal role in driving market share growth. Companies are increasingly utilizing direct-to-consumer e-commerce platforms, subscription-based services, and targeted digital marketing strategies to build stronger customer relationships and achieve higher profit margins compared to traditional retail channels. Additionally, white-space opportunities are emerging in areas such as personalized nutrition solutions, cognitive enhancement formulations, and sustainable packaging innovations. These trends not only align with evolving consumer preferences but also enable brands to differentiate themselves in an increasingly crowded market.

Pre-Workout Supplements Industry Leaders

-

QNT SA

-

FitLife Brands, Inc

-

Nutrabolt LLC

-

BioTech USA Kft.

-

GNC Holdings, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Nutrabolt has launched C4 AlphaBomb, a new pre-workout supplement designed to support muscle growth, strength, and performance, featuring ingredients such as myo-inositol, PeakO2, and a patented testosterone support blend. According to the brand, the formula aims to deliver enhanced pumps, energy, and focus for athletes and fitness enthusiasts, and is available in multiple flavors.

- May 2025: Aspire Biopharma has introduced its new BUZZ BOMB, a proprietary sublingual pre-workout supplement delivering 50mg of caffeine via nano-technology for rapid absorption and nearly instant effects. According to the brand, it is available in six flavors and convenient single-serving packets. BUZZ BOMB aims to enhance mental focus and sustained energy, distinguishing itself from traditional powdered pre-workouts that require more time to take effect.

- April 2025: Levo Naturals has expanded its functional product portfolio with the launch of Arena, a next-generation, botanically powered pre-workout supplement designed to boost energy, focus, and endurance. Arena features a blend of adaptogens, nootropics, and plant-based ingredients to provide a clean, sustained performance lift without artificial stimulants or harsh side effects.

- February 2025: Boxing legend Floyd Mayweather has entered the supplement industry with the launch of 1O1, a new brand offering a range of sports nutrition products tailored for both professional athletes and everyday fitness consumers. The 1O1 line includes pre-workout, hydration, and recovery formulas, all developed with a focus on quality, transparency, and performance. Mayweather’s involvement and the brand’s science-driven approach aim to set a new standard in the competitive supplement market.

Global Pre-Workout Supplements Market Report Scope

Pre-workout supplements are supplement products that give energy during exercise. Pre-workout is a dietary enhancement utilized by competitors and weightlifters to improve athletic performance. It is taken to build continuity, vitality, and a center during a workout. The global pre-workout supplements market is segmented by type, distribution channel, and geography. The market is segmented by type: powder, capsules or tablets, drinks, and other types. Based on distribution channels, the market studied is segmented by supermarkets and hypermarkets, specialty stores, online retail stores, and other distribution channels. The study also analyzes the pre-workout supplement market in emerging and established markets worldwide, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Powder |

| Liquids |

| Capsules |

| Other Forms |

| Stimulant-Based |

| Stimulant-Free |

| Caffeine |

| Beta-Alanine |

| Creatine |

| Citrulline |

| BCAAs |

| Adaptogens / Nootropics |

| Electrolytes |

| Others |

| Supermarkets/ Hypermarkets |

| Specialty and Health Stores |

| Online Retailers |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Form | Powder | |

| Liquids | ||

| Capsules | ||

| Other Forms | ||

| By Nature | Stimulant-Based | |

| Stimulant-Free | ||

| By Ingredient Type | Caffeine | |

| Beta-Alanine | ||

| Creatine | ||

| Citrulline | ||

| BCAAs | ||

| Adaptogens / Nootropics | ||

| Electrolytes | ||

| Others | ||

| By Distribution Channel | Supermarkets/ Hypermarkets | |

| Specialty and Health Stores | ||

| Online Retailers | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the pre-workout supplements market?

The pre-workout supplements market is valued at USD 22.48 billion in 2026 and is forecast to reach USD 31.53 billion by 2031 at a 6.99% CAGR.

Which region leads the pre-workout supplements market?

North America leads with 37.72% revenue share in 2025, supported by a mature fitness culture and clear regulatory guidelines.

Which product form is growing fastest?

Liquid ready-to-drink formats show the highest growth at a projected 7.59% CAGR through 2031 due to convenience and precise dosing.

Why are stimulant-free pre-workouts gaining popularity?

Regulatory caps on caffeine, rising female participation in strength training, and increased focus on sleep quality are driving a 9.32% CAGR for stimulant-free formulas.

Page last updated on: