Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

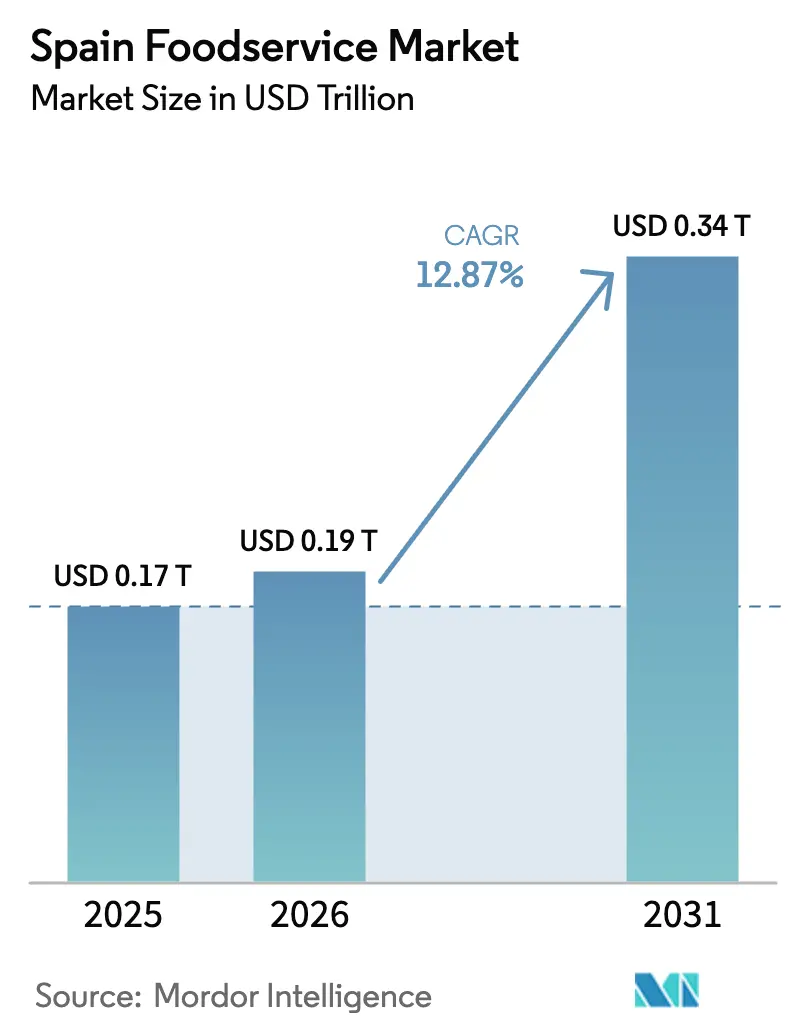

| Base Year Market Size (2025) | USD 0.17 Trillion |

| Market Size (2026) | USD 0.19 Trillion |

| Market Size (2031) | USD 0.34 Trillion |

| Growth Rate (2026 - 2031) | 12.87% CAGR |

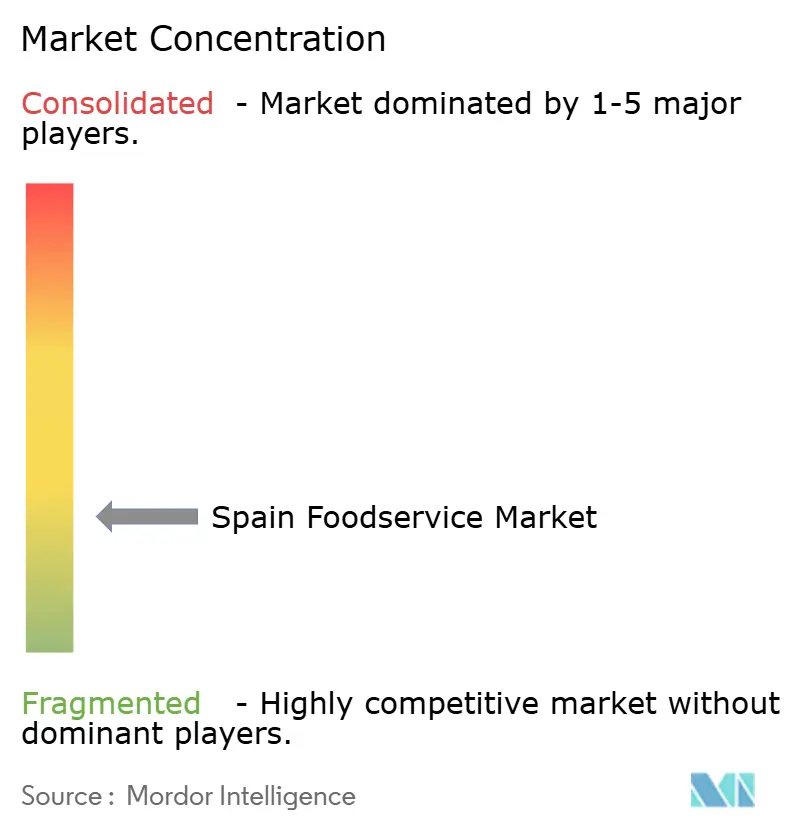

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spain Foodservice Market Analysis by Mordor Intelligence

The Spain foodservice market size was valued at USD 0.17 trillion in 2025 and estimated to grow from USD 0.19 trillion in 2026 to reach USD 0.34 trillion by 2031, at a CAGR of 12.87% during the forecast period (2026-2031). This trajectory reflects a structural shift beyond pandemic recovery, driven by accelerated digital ordering infrastructure, cloud-kitchen proliferation, and persistent tourist inflows that contributed EUR 2.11 billion to food and beverage spending in September 2025 alone, up 5.7% year-on-year. Spain's services sector turnover climbed 5.2% in August 2025, with GDP growth at 2.8% in Q3 2025, signalling robust domestic consumption alongside tourism-led demand. Independent outlets remain numerous, yet chained concepts now attract more private-equity capital, accelerating store counts and nudging the competitive field toward scalable formats.

Key Report Takeaways

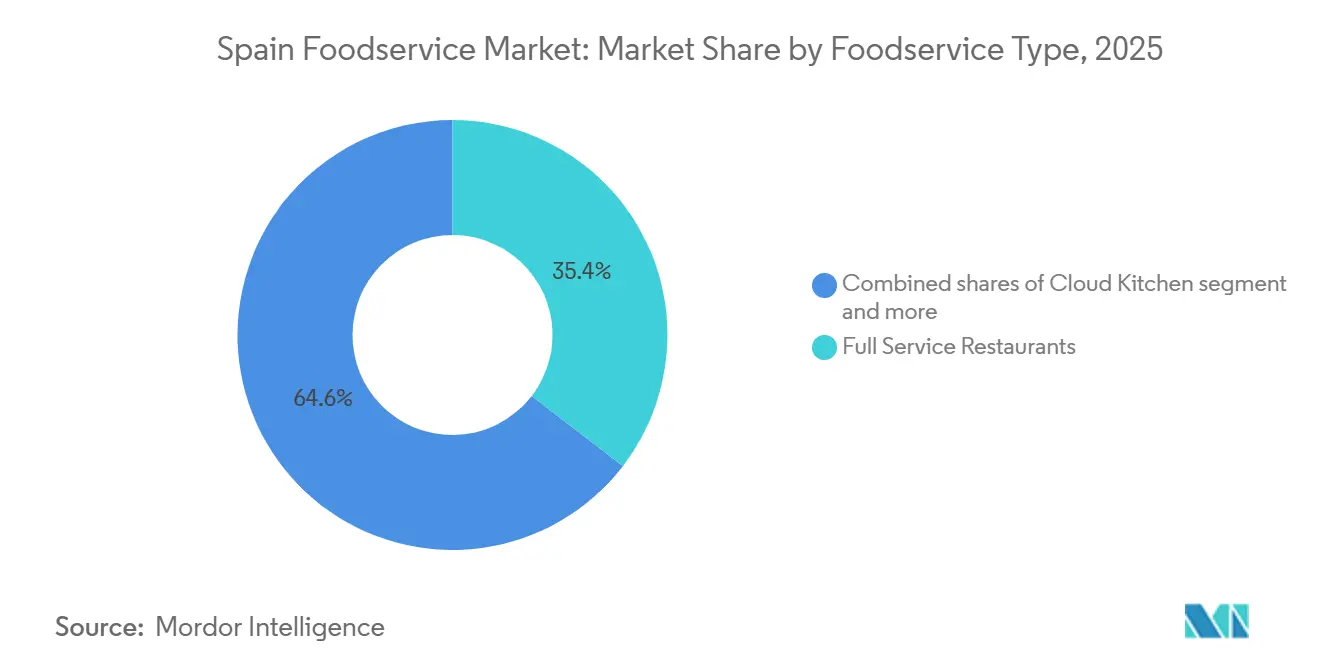

- By foodservice type, full-service restaurants led with 35.44% revenue share in 2025; cloud kitchens are advancing at a 13.01% CAGR through 2031.

- By outlet, independent operators controlled 65.77% of the Spain foodservice market share in 2025, while chained formats are projected to grow at a 13.56% CAGR to 2031.

- By location, standalone premises captured 75.87% of the Spain foodservice market size in 2025, and travel hubs are estimated to post a 14.52% CAGR to 2031.

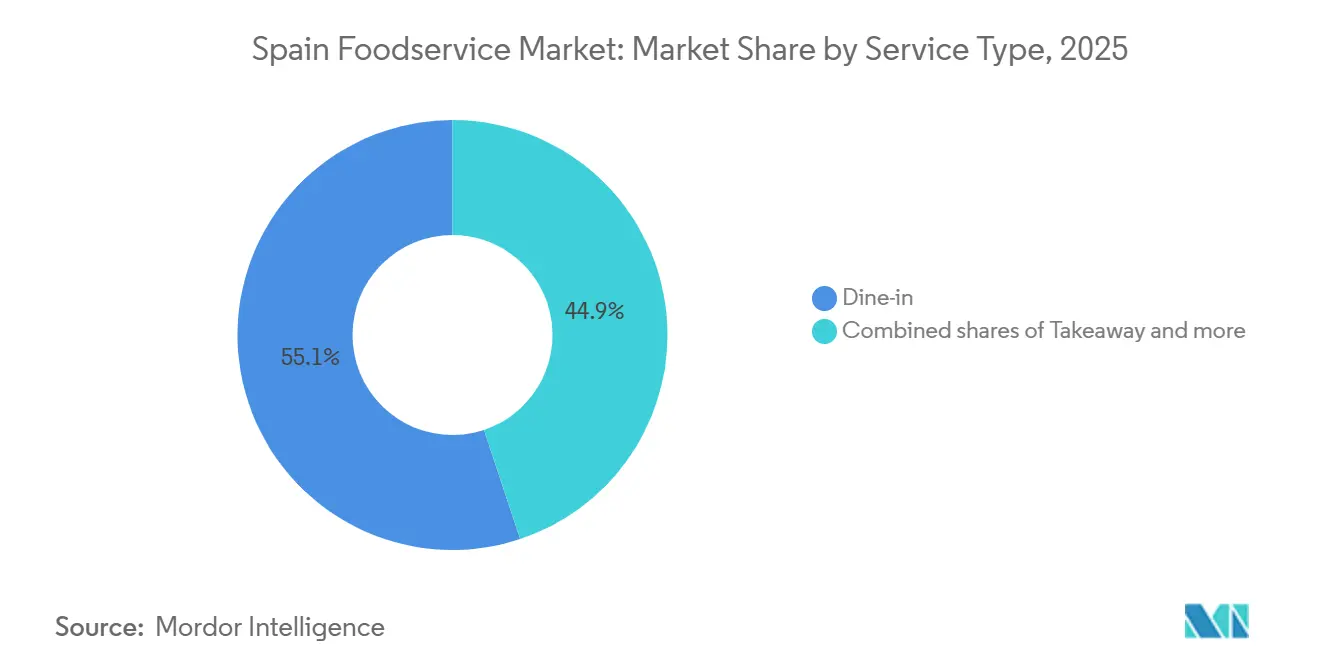

- By service style, dine-in retained 55.11% of the Spain foodservice market size in 2025; takeaway orders are slated to expand at a 14.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Branded café formats and specialty coffee chains rolling out at accelerated pace | +2.5% | National, with concentration in Madrid, Barcelona, Valencia, Seville | Medium term (2–4 years) |

| Cloud kitchens and delivery-only models scaling up rapidly | +3.2% | National, with early density in Madrid, Barcelona, and coastal tourism zones | Short term (≤ 2 years) |

| Halal-compliant positioning gaining prominence in brand architecture | +1.8% | National, with higher relevance in urban centers with diverse populations | Medium term (2–4 years) |

| Mobile app-based ordering seeing high penetration and fluency | +2.8% | National, with stronger adoption in metropolitan areas | Short term (≤ 2 years) |

| Dine-out habits deeply entrenched, bolstered by culture of socializing | +2.3% | National, particularly strong in Andalusia, Catalonia, Balearic Islands | Long term (≥ 4 years) |

| International operators progressively localizing menus | +1.6% | National, with emphasis on regional cuisine adaptation | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Branded Café Formats and Specialty Coffee Chains Rolling Out at Accelerated Pace

Specialty coffee chains are leveraging Spain's café culture to convert traditional bar-and-terrace operators into branded, premium-priced destinations. Starbucks, operated under AmRest's franchise agreement, expanded its international footprint by 264 net stores in Q1 fiscal 2025, though the segment faced a 4% comparable-sales decline due to promotional intensity and wage investments that compressed operating margin by 40 basis points to 12.7%. This margin pressure signals that even established coffee brands must discount aggressively to defend traffic, eroding the pricing power that once justified premium real estate. Independent specialty roasters are capturing share by emphasizing single-origin beans and barista craftsmanship, a positioning that resonates with younger consumers willing to pay EUR 3 to EUR 4 for espresso-based drinks versus EUR 1.50 at traditional bars. The shift toward third-wave coffee aesthetics, minimalist interiors, pour-over stations, transparency in sourcing, creates a differentiation moat that legacy chains struggle to replicate without alienating their core convenience-seeking customer base.

Cloud Kitchens and Delivery-Only Models Scaling Up Rapidly

Cloud kitchens are rewriting unit economics by eliminating front-of-house labor and prime-location rent, enabling operators to test multiple virtual brands from a single production facility. The segment is expanding at 13.01% CAGR through 2031, the fastest pace across all foodservice types, as delivery platforms provide turnkey customer acquisition and logistics. However, Glovo's reclassification of riders as employees in 2024 imposed an estimated EUR 100 million in additional costs, forcing the platform to renegotiate commission structures with restaurant partners and pass through higher delivery fees to consumers. This regulatory shift compresses margins for delivery-dependent operators, particularly those without dine-in or takeaway channels to absorb volume fluctuations. Ghost-kitchen aggregators are responding by consolidating production into fewer, larger hubs to achieve density-driven efficiency, yet this centralization increases vulnerability to single-point failures in food safety or equipment downtime.

Mobile App-Based Ordering Seeing High Penetration and Fluency

Mobile ordering penetration reached 67% of Spanish consumers in 2024, with digital wallets and contactless payments becoming the default transaction method across QSR and casual-dining formats. This fluency reduces friction at checkout and enables operators to capture zero-party data, order history, dietary preferences, and location, which fuels personalized promotions and dynamic pricing. McDonald's Spain integrated app-based ordering across its 640-plus locations, allowing customers to customize meals, skip queues, and earn loyalty points, a strategy that lifted average order value by encouraging add-ons and upsells. Yet the proliferation of restaurant-specific apps fragments the consumer experience, prompting aggregators like Just Eat and Uber Eats to bundle multiple brands into a single interface. The Spanish competition authority CNMC investigated exclusivity clauses in 2022, finding that 10% to 27% commission reductions were tied to 6- to 18-month exclusivity agreements affecting up to 35% of restaurants per platform [1]Source: CNMC Investigation, "Exclusivity clauses", cnmc.es. These clauses lock operators into single-platform relationships, limiting their ability to arbitrage commission rates or diversify customer-acquisition channels.

Dine-Out Habits Deeply Entrenched, Bolstered by Culture of Socializing

Spain's dine-out frequency remains among the highest in Europe, sustained by a cultural norm of multi-generational meals and late-evening socializing that extends restaurant operating hours beyond 23:00. Dine-in accounted for 55.11% of service-type share in 2025, reflecting resilience despite the rise of delivery and takeaway. The Instituto Nacional de Estadística reported that bars and cafés represent the majority share of Spain's 232,000 foodservice establishments, underscoring the sector's reliance on beverage-led, low-ticket transactions that depend on high table turnover. Tourism amplifies this dynamic, with international visitors contributing disproportionately to coastal and urban dine-in revenue during peak summer months. However, labor shortages in seasonal markets force operators to curtail service hours or reduce table sections, capping revenue potential even as demand surges. Full-service restaurants must balance experiential elements, live music, outdoor seating, and extended menus, with operational efficiency, a tension that favors concepts with streamlined kitchen workflows and cross-trained staff.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-chain logistics and perishable goods face reliability challenges | -1.2% | National, with acute issues in rural and island regions | Medium term (2–4 years) |

| Food safety practices and hygiene compliance show notable variability | -1.5% | National, with enforcement gaps in smaller autonomous communities | Short term (≤ 2 years) |

| Independent operators and street-food vendors intensify competitive pressures | -0.9% | National, with higher concentration in urban centers and tourist zones | Long term (≥ 4 years) |

| Concepts face rapid imitation, resulting in differentiation fatigue | -0.8% | National, affecting both chain and independent operators | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Cold-Chain Logistics and Perishable Goods Face Reliability Challenges

Temperature-controlled distribution remains a bottleneck for operators sourcing fresh produce, dairy, and proteins, particularly in Spain's island territories and rural interior regions where infrastructure investment lags coastal corridors. EU Regulation 852/2004 mandates continuous cold-chain integrity from farm to fork, yet compliance audits reveal gaps in last-mile delivery, where ambient temperatures during summer months can exceed 35°C and compromise product safety[2]Source: EU Regulation 852/2004, "EU Regulation 852/2004", eur-lex.europa.eu. Independent restaurants lacking centralized procurement absorb higher spoilage rates and must source locally to mitigate risk, a strategy that increases ingredient costs and limits menu standardization. Chains with vertically integrated supply networks, such as McDonald's, which operates dedicated distribution centers, achieve tighter quality control and negotiate volume discounts that independents cannot match. CaixaBank However, this relief is unevenly distributed, benefiting large buyers with forward contracts while spot-market purchasers remain exposed to seasonal volatility.

Food Safety Practices and Hygiene Compliance Show Notable Variability

Spain's decentralized enforcement model delegates food-safety inspections to autonomous communities, creating inconsistencies in audit frequency, penalty severity, and corrective-action follow-up. AESAN oversees national policy but lacks direct enforcement authority, resulting in a patchwork where Madrid and Catalonia conduct rigorous inspections while smaller regions prioritize tourism promotion over regulatory oversight[3]Source: ASEAN- Spanish Agency for Food Safety and Nutrition, "National policy", aesan.gob.es. This variability disadvantages compliant operators who invest in HACCP training, stainless-steel equipment, and third-party audits, only to compete against non-compliant rivals offering lower prices without incurring those costs. Street-food vendors and food trucks operate in a regulatory gray zone, often exempt from the same licensing and inspection regimes that govern brick-and-mortar establishments, enabling them to undercut traditional restaurants on price while avoiding fixed-cost burdens. The reputational risk of a food-safety incident, amplified by social media, can devastate a brand overnight, yet the absence of real-time monitoring systems means contamination often surfaces only after consumer complaints trigger reactive investigations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Cloud Kitchens Outpace Traditional Formats

Cloud kitchens will expand at 13.01% CAGR through 2031, the fastest rate among foodservice types, as operators exploit asset-light models to serve delivery demand without front-of-house costs. Full-service restaurants held 35.44% market share in 2025, anchored by Spain's entrenched dine-out culture, where lunch spans 2 to 4 pm, and dinner extends from 9 to 11 pm, reflecting social dining norms. Café and bar formats benefit from specialty coffee momentum, with Starbucks adding 16 Iberian stores in 2025 and McCafé capturing urban commuters. Vicio's hybrid model, 6 physical restaurants plus 24 dark kitchens generating EUR 55 million revenue in 2024, illustrates how operators blend formats to maximize reach while controlling capital expenditure. Regulatory compliance under AESAN applies uniformly, yet cloud kitchens' lack of dine-in seating exempts them from front-of-house hygiene inspections, compressing compliance costs.

The segment's evolution reflects a broader unbundling of foodservice economics. Traditional full-service restaurants absorb rent, labor, and ambiance costs that cloud kitchens avoid, yet they capture higher average tickets. Quick-service operators such as Goiko Grill, which operates 130 locations and targets 250-plus units, compete on speed and consistency, leveraging standardized menus and centralized procurement. Café and bar formats occupy a middle ground, offering lower ticket sizes but higher frequency, as remote workers and students use them as co-working spaces. The interplay among these formats will determine whether cloud kitchens cannibalize dine-in traffic or expand the total addressable market by serving occasions, late-night cravings, and office lunches that traditional formats underserve.

By Outlet: Independents Hold Share, Chains Capture Growth

Independent outlets commanded 65.77% market share in 2025, reflecting Spain's fragmented ownership structure, where family-run bars, neighborhood restaurants, and single-unit concepts outnumber corporate chains. Yet chained outlets are expanding at 13.56% CAGR through 2031, driven by franchising models that transfer capital risk to franchisees while preserving brand control and royalty streams for franchisors. Goiko Grill exemplifies this trajectory: the premium-burger chain operates 130 locations in 2025 and plans to exceed 250 units within 5 to 7 years, fueled by L Catterton's 80% equity stake and a disciplined site-selection process that prioritizes urban cores with high foot traffic. Restaurant Brands Iberia opened Burger King's first Cantabria location in July 2024, creating 30 jobs and bringing the region's total to 10 outlets, while Popeyes launched its third Palma de Mallorca restaurant the same month, expanding the brand to 139 Spanish units.

Independents face structural disadvantages in procurement, marketing, and technology. They pay higher per-unit costs for ingredients, lack national advertising budgets, and often rely on third-party delivery platforms that charge 15% to 30% commissions, eroding already thin margins. However, independents retain agility to customize menus, pivot concepts, and cultivate local loyalty that chains cannot easily replicate. The OECD noted in 2024 that Spanish SMEs, 99% of businesses and 67% of employment, depend on bank loans for 90% of financing, with limited access to public equity markets, constraining their ability to scale or invest in digital infrastructure. Chains, by contrast, access private equity, venture capital, and securitized franchise royalties to fund multi-unit rollouts, creating a bifurcated market where scale begets further scale.

By Service Type: Takeaway Surges as Dine-In Holds Ground

Dine-in captured 55.11% of service-type share in 2025, sustained by Spain's late-evening dining culture and tourism-driven demand for experiential meals. Takeaway, however, is expanding at 14.27% CAGR through 2031, the fastest growth among service types, as consumers prioritize convenience and operators invest in dedicated pickup windows, curbside zones, and app-based order-ahead functionality. Delivery, though smaller in absolute terms, benefits from platform aggregation, Glovo, Just Eat, Uber Eats, which bundles restaurant selection, payment processing, and logistics into a single consumer interface. The CNMC's 2022 investigation revealed that exclusivity clauses tied 10% to 27% commission reductions to 6- to 18-month platform commitments, affecting up to 35% of restaurants per platform and locking operators into single-channel relationships.

The service-type mix varies by format: QSR skews heavily toward takeaway and delivery, with drive-thru lanes accounting for a significant share of transactions, while full-service restaurants derive a significant share of revenue from dine-in. Cloud kitchens operate exclusively on delivery and takeaway, eliminating dine-in infrastructure to maximize kitchen utilization and minimize real estate costs. McDonald's Spain reported continued growth in digital ordering channels (mobile app, kiosk, and delivery) as the company integrates loyalty programs and personalized offers. This shift pressures traditional dine-in operators to invest in off-premises capabilities or risk ceding share to competitors with omnichannel strategies.

By Locations: Standalone Sites Dominate, Travel Hubs Accelerate

Standalone locations held 75.87% market share in 2025, and travel held the fastest-growing segment at 14.52% CAGR through 2031, reflecting operators' preference for street-level visibility, lower rent relative to enclosed malls, and freedom from revenue-share agreements that shopping centers impose. Travel locations, airports, train stations, and highway rest stops are expanding rapidly as passenger volumes recover to pre-pandemic levels. In September 2024, Dabiz Muñoz's Grupo UniverXO partnered with Avolta to open Hungry Club at Madrid Terminal 4, with plans for 9 locations across Madrid, Barcelona, Málaga, and Palma, signaling that celebrity-chef concepts are entering travel retail to capture premium-paying international passengers.

Retail locations, shopping malls, and department stores face headwinds from e-commerce migration and declining foot traffic, forcing landlords to convert retail square footage into dining and entertainment to retain tenant mix and visitor dwell time. Leisure locations, stadiums, cinemas, and theme parks offer captive audiences but impose exclusivity and revenue-share terms that limit operator profitability. Lodging locations, hotels, and resorts provide stable demand but require 24-hour service capabilities and menu customization to accommodate international guests. Ibersol Travel operates 66 restaurants in Spain, concentrated in airports and AVE high-speed rail stations, and opened a 656-square-meter food market at Lanzarote airport in March 2024, featuring the first Pizza Hut in the Canary Islands and the sixth KFC operated by Ibersol. This multi-brand hub model maximizes revenue per square meter by offering diverse cuisines under a single roof, reducing consumer decision fatigue and increasing average spend per visit.

Geography Analysis

Madrid and Central Spain form one of the most important foodservice hubs in the country, supported by high population density, strong purchasing power, business travel, and year-round tourism. Madrid has one of the highest concentrations of foodservice establishments in Spain and serves as a key market for full-service restaurants, quick-service restaurants (QSRs), cafés, bars, and delivery-focused operators. The region benefits from a large office workforce and a vibrant dining culture, driving demand across breakfast, lunch, dinner, and late-night occasions. International restaurant chains often prioritize Madrid for new store launches due to its large consumer base and strong economic activity.

Catalonia, led by Barcelona, represents another major foodservice concentration area owing to its large tourism sector, international visitor traffic, and established culinary reputation. Catalonia’s foodservice industry comprises thousands of businesses and generates significant economic output, reflecting the region’s importance within Spain’s out-of-home dining landscape. Barcelona attracts both domestic and international consumers, supporting a diverse mix of fine dining, casual dining, cafés, bars, and takeaway formats. The region’s strong tourism infrastructure and large hospitality ecosystem continue to support foodservice demand throughout the year.

Southern and coastal regions, particularly Andalusia, Valencia, the Balearic Islands, and the Canary Islands, are heavily influenced by leisure and tourism-related consumption. Andalusia, Catalonia, the Valencian Community, and Madrid together account for around 60% of Spain’s catering and restaurant establishments, highlighting the concentration of foodservice activity in these regions. Tourist destinations such as the Balearic and Canary Islands experience strong seasonal demand, benefiting restaurants, cafés, bars, and hotel foodservice operators. Spain’s record tourism inflows and the continued importance of hospitality-related employment further reinforce foodservice growth across these leisure-oriented regions.

Competitive Landscape

Spain's foodservice market registers a moderate concentration, indicating fragmentation where no single operator commands pricing power or format dominance. This fragmentation creates white-space opportunities for concepts that can scale rapidly through franchising or private-equity backing. Goiko Grill's plan to grow from 130 to 250-plus units within 5 to 7 years, supported by L Catterton's 80% equity stake, exemplifies how niche, experience-led brands can carve out growth trajectories independent of legacy QSR giants. McDonald's EUR 500 million investment over 2025–2028 to reach 800 locations signals that even market leaders must deploy significant capital to defend their share against emerging challengers.

Technology adoption is the primary battleground for share gains. Mobile ordering, self-service kiosks, and loyalty programs reduce labor costs, increase average order value through upselling, and capture zero-party data that enables personalized promotions. AmRest achieved a 21.5% EBITDA margin in Spain during Q1 2025, up 1.9 percentage points year-on-year, by integrating digital ordering across its KFC, Pizza Hut, Burger King, and Starbucks portfolios.

Delivery platforms, Glovo, Just Eat, Uber Eats, function as both enablers and competitors, providing customer acquisition and logistics for a 15% to 30% commission while simultaneously launching private-label virtual brands that bypass restaurant partners entirely. The CNMC's 2022 investigation into exclusivity clauses revealed that platforms offered 10% to 27% commission reductions in exchange for 6- to 18-month exclusivity, affecting up to 35% of restaurants per platform and locking operators into single-channel relationships that limit their ability to arbitrage rates. Emerging disruptors include ghost-kitchen aggregators that consolidate multiple virtual brands into shared production facilities, achieving density-driven efficiency while testing new concepts without the sunk cost of physical buildouts.

Spain Foodservice Industry Leaders

-

Alsea SAB de CV

-

AmRest Holdings SE

-

Restaurant Brands Iberia

-

Áreas SAU

-

McDonald's

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Key hospitality and foodservice associations (including Hostelería de España and major restaurateur groups) signed partnership and collaboration agreements to support the Alimentaria + Hostelco 2026 hospitality and catering trade show. This aims to drive innovation, networking, and business development across the foodservice ecosystem.

- November 2025: Subway has expanded its partnership with Grupo Vierci, giving the Paraguayan/Uruguayan group exclusive rights to operate and develop the brand in Spain and Portugal. Under this agreement, about ~400 Subway restaurants are planned in Spain over the next decade, significantly boosting QSR's footprint and long-term growth potential in the region.

- March 2025: Restaurant Brands Europe, which operates major QSR brands including Burger King and Popeyes in Spain, increased sales by ~12 % in 2024 and added 147 new restaurant locations, reflecting strong expansion activity across its brands in the Spain market.

Spain Foodservice Market Report Scope

Foodservice refers to the business of preparing, serving, and selling ready-to-eat food and drinks for immediate consumption, encompassing diverse establishments like restaurants, cafes, catering, and institutions, focusing on providing meals outside the home for profit or service. The spain foodservice market is segmented by foodservice type, outlet, service type, and location. By foodservice type, the market is segmented into cafes and bars, cloud kitchen, full-service restaurants, quick service restaurants and more. By outlet, the market is segmented into chained outlets and independent outlets. By location, the market is segmented into leisure, lodging, retail, standalone, and more. By service type, the market is segmented into takeaway, delivery and more. The market forecasts are provided in terms of value (USD).

By Foodservice Type

| Café and Bars | By Cuisine | Bars and Pubs |

| Café | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

By Outlet

| Chained Outlets |

| Independent Outlets |

By Locations

| Leisure |

| Lodging |

| Retail |

| Sandalone |

| Travel |

By Service Type

| Dine-in |

| Takeaway |

| Delivery |

| By Foodservice Type | Café and Bars | By Cuisine | Bars and Pubs |

| Café | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| By Outlet | Chained Outlets | ||

| Independent Outlets | |||

| By Locations | Leisure | ||

| Lodging | |||

| Retail | |||

| Sandalone | |||

| Travel | |||

| By Service Type | Dine-in | ||

| Takeaway | |||

| Delivery | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms