Southeast Asia Agricultural Sprayers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

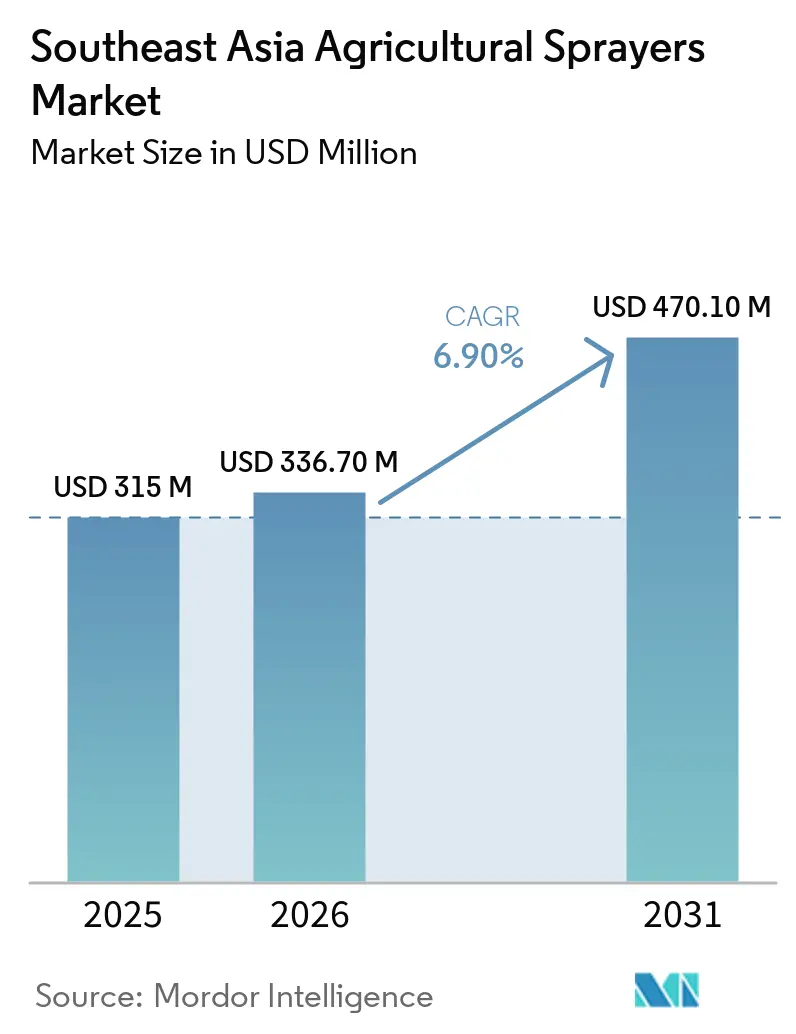

| Base Year Market Size (2025) | USD 315 Million |

| Market Size (2026) | USD 336.70 Million |

| Market Size (2031) | USD 470.10 Million |

| Growth Rate (2026 - 2031) | 6.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Agricultural Sprayers Market Analysis by Mordor Intelligence

The Southeast Asia agricultural sprayers market size was valued at USD 315 million in 2025 and estimated to grow from USD 336.7 million in 2026 to reach USD 470.1 million by 2031, at a CAGR of 6.9% during the forecast period (2026-2031). The Southeast Asia agricultural sprayers market is supported by faster farm mechanization, broader subsidy support for equipment purchases, and a steady decline in farm labor availability across several countries. Demand is holding up because many growers now view mechanized and precision spraying as a direct response to labor scarcity rather than an optional upgrade, making spraying equipment spending more resilient during weaker commodity cycles. The market also reflects a split structure, with low-cost conventional systems continuing to serve smallholder farms, while artificial intelligence-enabled and autonomous platforms gain traction in plantations and organized service networks. This dual structure is widening the product range sold across the region, from manual backpack units for sub-1-hectare farms to drone fleets and tractor-mounted systems for large estates. The same pattern is creating space for both established agricultural machinery brands and drone-focused entrants, keeping competitive pressure high across mid-range and premium equipment categories.

Key Report Takeaways

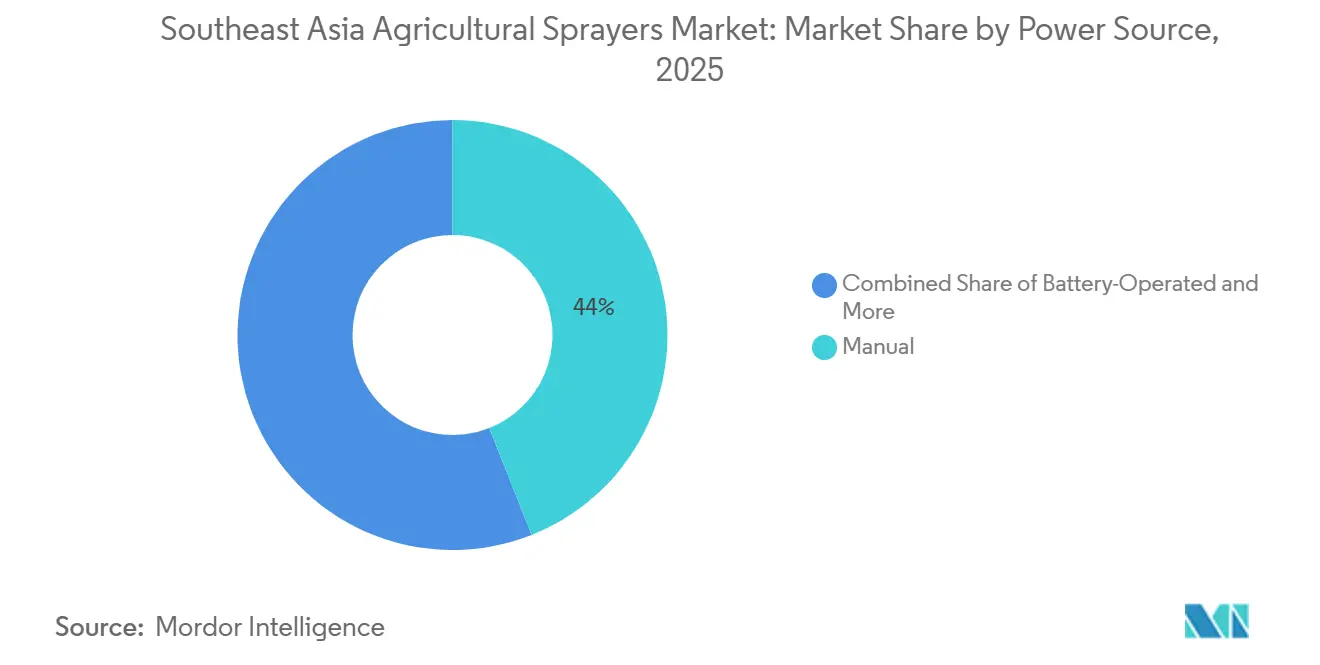

- By power source, manual sprayers led with a 44% market share in 2025, while battery-operated sprayers are projected to grow at a 11.3% CAGR through 2031.

- By product type, handheld sprayers held a 47% share of the Southeast Asia agricultural sprayers market in 2025, while unmanned aerial vehicle sprayers are forecast to expand at a 14.2% CAGR through 2031.

- By application, field crops accounted for 45% of the Southeast Asia agricultural sprayers market size in 2025, while orchards and vineyards are advancing at an 8.6% CAGR through 2031.

- By spray volume capacity, low-volume systems captured 43% of the market in 2025, while ultra-low-volume systems are projected to grow at a 12.1% CAGR through 2031.

- By technology level, conventional systems retained a 69% share in 2025, while Artificial Intelligence-enabled and autonomous systems are estimated to expand at a 15% CAGR through 2031.

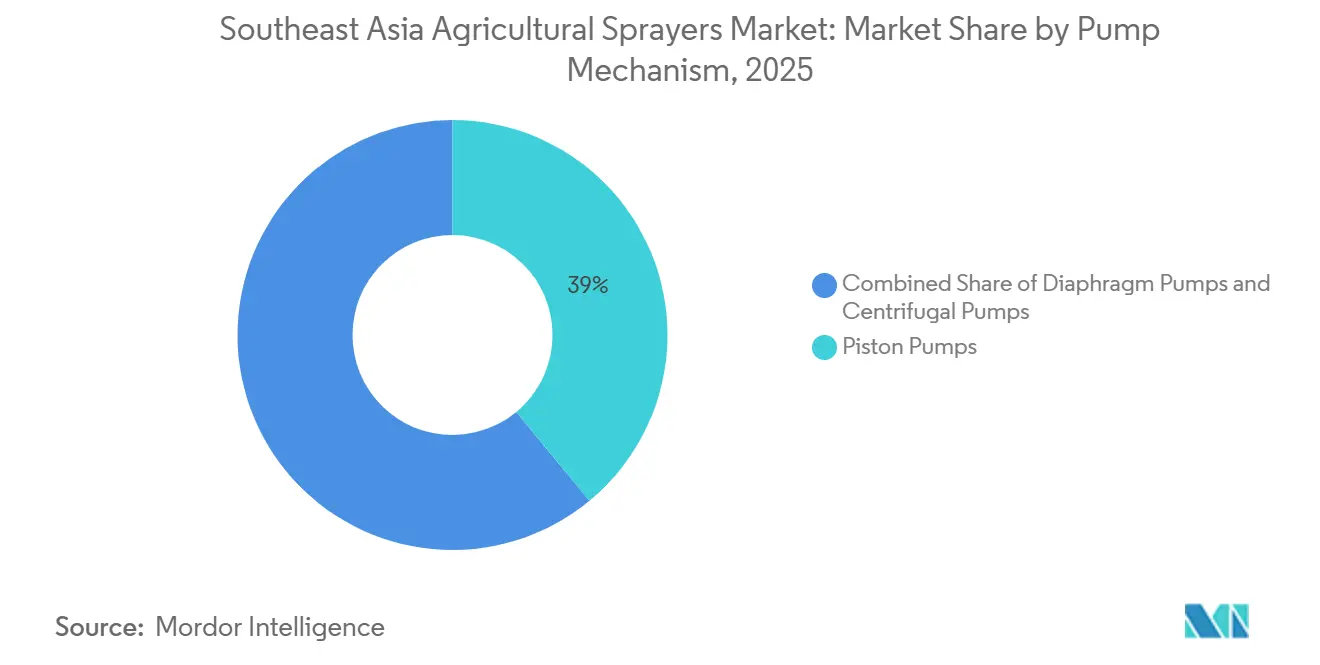

- By pump mechanism, piston pumps held 39% market share in 2025, while diaphragm pumps are projected to grow at a 9.1% CAGR through 2031.

- By geography, Indonesia held 31% revenue share in 2025, while Vietnam is estimated to be the fastest growing at a 8.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia Agricultural Sprayers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Farm labor shortages raise mechanized spraying demand | +1.2% | Indonesia, Vietnam, Thailand and Philippines | Short term (≤ 2 years) |

| Government mechanization subsidies and financing | +1.0% | Thailand, Indonesia, Vietnam and Philippines | Short term (≤ 2 years) |

| Precision agriculture and input-efficiency needs | +1.1% | Asia-Pacific core, with spillover to Myanmar, and Laos | Medium term (2-4 years) |

| Palm oil and rice crop protection drives consistent demand | +0.9% | Indonesia and Malaysia for plantation estates, and Vietnam and Thailand for rice cultivation | Medium term (2-4 years) |

| Low-emission rice programs favor precise spray scheduling | +0.8% | Vietnam, Thailand, and Philippines | Medium term (2-4 years) |

| Expansion of contract drone service networks | +0.7% | Indonesia and Thailand as early adopters, and Vietnam and The Philippines as an emerging market | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Farm Labor Shortages Raise Mechanized Spraying Demand

The rural labor movement in Southeast Asia has become a lasting shift rather than a short cycle, and that is changing spraying decisions at the farm level. In several countries, growers are finding it harder to secure workers for repeated spray passes during narrow crop windows. Manual backpack spraying can require 3 to 5 workers per 50 hectares in a single application round, quickly increasing the labor burden on large farms. As a result, labor scarcity is pushing mechanized sprayers from a convenience purchase into an operating need. Dealers in Indonesia and the Philippines have reported that payback periods for powered spraying equipment are now shortening to under 18 months in higher-value crop systems, which is speeding up purchase decisions that once took years. This is lifting demand for tractor-mounted boom sprayers on medium-scale farms and for drone service contracts on fragmented or difficult terrain where ground access is limited. The Southeast Asia agricultural sprayers market is therefore benefiting from a demand base tied to labor substitution, which is more stable than demand driven only by yield improvement.

Government Mechanization Subsidies and Financing

Public financing initiatives are influencing how farms and cooperatives in Southeast Asia approach sprayer purchases. During 2025, the Philippines' Department of Agriculture’s Drones4Rice program offered subsidized access to drone spraying services through hectare-based vouchers, complemented by broader mechanization funding to support the adoption of precision agriculture. In Thailand, the Smart Farmer initiatives, launched in 2025, promoted modernization and the use of precision equipment, such as GPS-guided sprayers and agricultural drones. Similarly, Indonesia’s KUR Pertanian financing programs launched in 2025 aim to ease the financial burden on smallholder farmers and cooperatives investing in agricultural machinery, including mechanized spraying systems. These programs not only reduce upfront costs but also prioritize higher-performing equipment with enhanced efficiency, control, and traceability through their eligibility criteria. Consequently, subsidy and financing policies are driving changes in the product mix of the Southeast Asia agricultural sprayers market by increasing demand for advanced spraying technologies.

Precision Agriculture and Input-Efficiency Needs

The rise in agrochemical costs since 2022 has changed how growers calculate the value of more precise spraying. Even smaller farms are now paying closer attention to chemical waste because it has become a larger part of total operating costs. GPS-guided boom sprayers and AI-enabled drones can reduce over-application, avoid bare ground, and adjust spray rates to canopy conditions. In rice trials in the Philippines in 2025, XAG Co. Ltd.’s collaboration with IRRI (International Rice Research Institute) documented pesticide savings of up to 30% compared with conventional ground-boom methods, adding weight to precision-spraying decisions in the region. For plantation operators with large annual crop protection budgets, even a 15% gain in application efficiency can materially change cost performance. That shifts sprayer investment from a technology discussion into a financial one. The Southeast Asia agricultural sprayers market is therefore seeing increased demand for systems that deliver measurable savings in chemicals, labor, and pass consistency.

Palm Oil and Rice Crop Protection Drives Consistent Demand

Palm oil and rice cultivation drive consistent demand for agricultural sprayers in Southeast Asia, as these crops require frequent, time-sensitive treatments. Indonesia and Malaysia are the leading global producers of palm oil, necessitating regular herbicide and fungicide applications. Similarly, rice cultivation in Vietnam, Thailand, and the Philippines generates ongoing demand to support crop yield and quality. In January 2025, Terra Drone, in collaboration with Behn Meyer, completed a 2,158-hectare bagworm control drone project across oil palm plantations in Indonesia and Malaysia, showcasing the large-scale adoption of drone spraying technology[1]Source: Terra Drone Corporation, “Terra Agri Deploys Advanced Drones for Bagworm Control Across 2,158 Hectares of Palm Oil Plantations in Indonesia and Malaysia,” Terra Drone, terra-drone.net. These crops ensure steady, year-round spraying demand, providing suppliers with greater predictability in orders and service contracts compared to fragmented smallholder markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of drones and powered sprayers | -1.2% | All 10 Southeast Asia markets, with the highest pressure in Cambodia, Myanmar, Laos, and the Philippines | Short term (≤ 2 years) |

| Fragmented smallholder land limits utilization | -0.8% | Vietnam, Philippines, and Indonesia, especially Java | Long term (≥ 4 years) |

| Drone-compliant pesticide formulations remain limited | -0.5% | Region-wide | Medium term (2-4 years) |

| Flight permits and payload rules slow field operations | -0.6% | All 10 Southeast Asia markets due to regulatory divergence across ASEAN (Association of Southeast Asian Nations) members | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Of Drones And Powered Sprayers

High equipment costs continue to be a significant challenge in the Southeast Asia agricultural sprayers market. Commercial agricultural drones with payload capacities of 20–30 liters are priced between USD 8,000 and USD 20,000, depending on configuration, batteries, and accessories. This pricing restricts ownership primarily to plantations, commercial farms, and well-funded cooperatives. While drone-as-a-service models help reduce upfront investment, operators still incur substantial costs related to equipment, training, and maintenance, leading to higher service prices for small-scale growers. Consequently, advanced spraying systems are being adopted more quickly in organized farming operations, whereas manual and basic powered sprayers remain prevalent on smaller farms.

Fragmented Smallholder Land Limits Utilization

Small farm size continues to limit the value a grower can extract from a mechanized sprayer over the course of a year. A large share of Southeast Asia’s farming households operate on plots of 1 hectare or less, which sharply reduces equipment utilization under an ownership model. In the Mekong Delta, average rice plots are often only 0.5 to 0.7 hectares, while many farms in the Philippine Visayas and Mindanao also operate at less than 1 hectare. Parts of Indonesia, especially Java, exhibit similar fragmentation, making it difficult to justify equipment purchases based on annual hours of use. Cooperative ownership and shared-service arrangements can improve utilization, but they depend on local organization, land records, and financing structures that are uneven across the region. In Cambodia, Myanmar, and several fragmented districts in Indonesia, weak land-tenure formalization makes shared ownership harder to implement at scale. This keeps a ceiling on direct farm-level equipment sales and pushes suppliers to rely more heavily on contractor and service-led distribution models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Source: Battery-Operated Systems Compete with Manual Systems

Manual sprayers accounted for 44% of the Southeast Asia agricultural sprayers market in 2025, while battery-operated sprayers are projected to grow the fastest, with a CAGR of 11.3% through 2031. Manual sprayers remain prevalent due to their affordability, particularly for farms with very small landholdings. Additionally, they are easy to repair and require minimal supporting infrastructure, which is crucial in rural areas with limited dealer networks. These factors ensure their continued relevance in various segments of the Southeast Asia agricultural sprayers market, even as advanced products gain traction.

Battery-operated sprayers are increasingly popular as lithium-ion battery costs decline, runtimes improve, and rural electrification becomes more reliable in several countries. This trend is particularly evident in Thailand and Vietnam, where public procurement initiatives and low-emission farming programs are promoting the adoption of electrified tools. Meanwhile, solar-powered sprayers are emerging as a solution for smaller hillside and terraced farming operations. Fuel-powered systems continue to serve plantation and field-crop operations, where longer runtimes and larger tank capacities are essential. This diverse mix indicates that the Southeast Asia agricultural sprayers market is not entirely transitioning away from traditional power systems but is instead incorporating new power formats alongside the established manual base.

By Product Type: UAV (Unmanned Aerial Vehicle) Sprayers and Their Impact on Market Growth

Handheld sprayers led product demand, with a 47% share in 2025, as they remain the cheapest and most practical option for fragmented plots. Their strength reflects the reality that a large part of regional agriculture still operates under land, cash, and infrastructure constraints. That gives handheld equipment durable volume even when more advanced systems post faster growth. The Southeast Asia agricultural sprayers market, therefore, continues to be led by a large, low-cost installed base.

UAV (Unmanned Aerial Vehicle) sprayers are projected to grow at a 14.2% CAGR through 2031, making them the fastest-growing product type in the market. Much of this expansion is being driven by drone-as-a-service networks that lower the effective cost of aerial spraying for farms that cannot justify ownership. In May 2026, DJI introduced the Agras T55 with a 50-liter payload and the Agras T100 Dual Battery Spraying System at AGRITECHNICA Asia 2026 in Bangkok, extending drone capability into larger field and plantation use cases[2]comSource: DJI Agriculture, “DJI Agriculture Debuts Agras T55 and T100 Dual Battery Spraying System in Thailand at AGRITECHNICA Asia 2026,” AGRITECHNICA 2026, https://digital.agritechnica.com/. Tractor-mounted, trailed, and self-propelled sprayers continue to serve medium and large farms that require consistent boom coverage and higher daily work rates. Over time, the overlap between advanced ground systems and Unmanned Aerial Vehicle's is likely to intensify as buyers compare not only machine price, but also labor savings, turnaround speed, and service availability.

By Application: Field Crops Drive Volume, Orchards Contribute to Margin Growth

Field crops accounted for 45% of the Southeast Asia agricultural sprayers market in 2025, representing the largest application share in the region. This dominance is attributed to extensive paddy fields and broad-acre plantation estates in countries such as Indonesia, Vietnam, and Thailand, where frequent spraying is essential for effective crop management. The large volume base is driven by the significant acreage of these crop systems, which require repeated applications throughout the growing season. Consequently, field crops drive demand for both cost-effective sprayers and higher-capacity mechanized systems.

The orchards and vineyards segment is estimated to grow at a compound annual growth rate (CAGR) of 8.6% through 2031, fueled by increasing demand for export-grade tropical fruits such as durian, mangosteen, dragon fruit, and rambutan. These crops often necessitate precise spray timing and accurate canopy coverage, unlike broad-acre field operations. In 2025, XAG Co. Ltd.’s collaboration with the International Rice Research Institute (IRRI) in the Philippines demonstrated reductions in pesticide use and yield improvements in drone-treated rice plots, highlighting the benefits of precision spraying in crop systems where agronomic consistency is critical. Greenhouse crops represent a smaller but higher-specification niche, particularly in Malaysia and Singapore. Meanwhile, demand for turf and gardening applications remains steady, supported by urban landscaping projects and managed estate maintenance. The Southeast Asia agricultural sprayers market is thus characterized by a balance between the high-volume demand from field crops and the faster growth observed in applications requiring stricter quality standards.

By Spray Volume Capacity: Ultra-Low Volume Drives Drone Adoption

Low-volume systems accounted for 43% of the market share in 2025, driven by the widespread use of conventional hydraulic sprayers across field crops and plantations. These systems are well-suited for application rates typically ranging from 100 to 300 liters per hectare. Their compatibility with established grower practices, chemical calibration methods, and operator familiarity has sustained their leading position, even as newer aerial application formats gain traction.

Ultra-low volume systems are estimated to achieve a compound annual growth rate (CAGR) of 12.1% through 2031, driven by the increasing adoption of drone-spraying technologies. Agricultural drones primarily operate at very low carrier volumes, relying on precise droplet accuracy rather than liquid volume. For instance, Micron Sprayers’ Herbi Duo CDA range applies herbicides at rates of 15 to 30 liters per hectare, utilizing controlled droplet sizing to minimize off-target drift. This feature is particularly advantageous in mixed-crop areas where neighboring plots may contain incompatible crops. Additionally, ultra-low volume systems are practical for upland regions where limited water access and challenging field logistics limit the use of high carrier volumes. High-volume systems continue to play a role in mature plantation settings with established bulk-delivery logistics. However, their market share is anticipated to gradually decline as drone fleets and precision application systems expand their presence and installed bases.

By Technology Level: Conventional Dominance Masks an AI-Led Shift

Conventional spraying systems accounted for 69% of the market in 2025, indicating that traditional equipment continues to dominate daily farming operations across the region. This dominance reflects decades of accumulated installed base and the ongoing cost pressures faced by smallholder farmers. Precision and GPS-guided systems are gradually gaining traction in the mid-tier segment, particularly among farms seeking measurable chemical savings without incurring the full cost of AI-driven equipment. As a result, technology adoption in the Southeast Asia agricultural sprayers market is progressing at a gradual pace rather than undergoing a rapid transformation.

Artificial intelligence-enabled and autonomous systems are anticipated to grow at a compound annual growth rate (CAGR) of 15% through 2031, representing the fastest growth among technology categories. This expansion is being driven by plantation operators, service providers, and public programs aiming to improve targeting, reduce waste, and decrease reliance on manual labor. At CES (Consumer Electronics Show) 2026, KUBOTA Corporation reported that its Agtonomy-linked autonomous spraying and mowing program achieved a fivefold increase in autonomous spraying coverage over the previous two years, demonstrating how established machinery manufacturers are integrating autonomy into commercial platforms. Additionally, Terra Drone Indonesia’s G20 agri-drone met a 31.26% local content threshold in October 2025, qualifying it for Indonesian government procurement and highlighting how local compliance can facilitate technology adoption. Consequently, while the Southeast Asia agricultural sprayers market is anticipated to remain dominated by conventional systems in terms of unit sales, it is steadily transitioning toward smarter systems in terms of market value.

By Pump Mechanism: Diaphragm Pumps Gain on Durability and Chemical Compatibility

Piston pumps led the pump mechanism segment with a 39% share in 2025 because they deliver the high pressure needed for crop penetration in many field and plantation use cases. They remain familiar to buyers and service technicians, which supports replacement demand and continued adoption. Their position is strongest in applications where high-pressure delivery matters more than ease of maintenance. That gives piston systems a durable role even as other pump types gain share.

Diaphragm pumps are projected to grow at a 9.1% CAGR through 2031 as buyers place more value on chemical compatibility, dry-run tolerance, and lower maintenance needs. These features matter in Southeast Asia because spare parts and service access can be inconsistent outside major farming corridors. Smallholder operators are particularly sensitive to downtime during narrow spray windows, so pump durability directly affects equipment choice. Centrifugal pumps still serve high-flow, low-pressure boom systems on flatter terrain, especially where buyers focus on lifecycle cost over peak performance. At the same time, the spread of drone-mounted, battery-powered systems is creating demand for smaller, more vibration-tolerant pump formats that differ from legacy ground-boom designs. This makes pump selection a more strategic product variable in the Southeast Asia agricultural sprayers market than it was when most demand centered on basic manual and tractor-mounted equipment.

Geography Analysis

Indonesia accounted for approximately 31% of the Southeast Asia agricultural sprayers market in 2025, making it the region’s largest market. Its leadership is supported by its extensive agricultural economy, dominant oil palm plantation sector, and mechanization initiatives, although the commonly cited figure of 191 million hectares refers to Indonesia’s total land area rather than agricultural land, which is closer to 55 million hectares in 2025. Vietnam is projected to be the region’s fastest-growing market, expanding at an estimated 8.1% CAGR through 2031 as rising rice cropping intensity and precision agriculture adoption increase spray application frequency and drive demand for both ground-based and aerial spraying systems.

Thailand remains the region’s primary hub for agricultural spraying equipment and services due to its mature dealer network and strong smart farming adoption. DJI Agriculture stated in May 2026 that Thailand contributed around 50% of its Southeast Asia revenue, supported by more than 19,000 certified drone operators and over 300 retail locations across more than 70 provinces. Malaysia continues to represent a concentrated plantation-driven market for large-capacity spraying equipment, particularly in oil palm estates, while the Philippines is emerging as a promising mid-tier growth market through government-supported drone agriculture initiatives such as Drones4Rice.

Cambodia offers favorable conditions for boom and drone spraying adoption, although financing access remains comparatively limited. Myanmar continues to underperform because political and economic instability are constraining mechanization investment, while Laos’ mountainous terrain and subsistence farming structure favor portable sprayers over larger platforms. Singapore and Brunei remain small but higher-specification markets linked to greenhouse farming, public landscape management, and agricultural diversification initiatives, collectively contributing only a modest share of regional agricultural sprayer demand.

Competitive Landscape

The Southeast Asia agricultural sprayers market remains moderately concentrated, led by major global equipment manufacturers such as KUBOTA Corporation, DJI Agriculture, Yanmar Holdings Co. Ltd., Deere & Company, and CNH Industrial N.V in 2025. While market leadership provides advantages in distribution, after-sales service, and installed base. Competition is increasingly dividing between established machinery manufacturers integrating automation into conventional spraying platforms and drone-focused companies expanding through operator ecosystems and service-led deployment models. This dynamic continues to leave room for regional specialists, particularly in UAV (Unmanned Aerial Vehicle) spraying and precision application services.

KUBOTACorporation has accelerated its autonomy strategy through partnership-led innovation. In February 2026, the company participated in a USD 7.4 million funding round for Norwegian agtech firm Kilter AS, developer of the AX-1 autonomous spot-spraying robot. KUBOTA Corporation also expanded its collaboration with Agtonomy for autonomous specialty-crop equipment and showcased Artificial Intelligence (AI) -enabled autonomous farming systems at CES (Consumer Electronics Show) 2026. Meanwhile, DJI Agriculture and XAG Co. Ltd. continue to strengthen their regional positions through operator training, service networks, and partnerships linked to agricultural modernization programs in markets such as Thailand and the Philippines.

Another important competitive trend is the growing role of localization and regulatory compliance. In October 2025, Terra Drone Indonesia obtained Indonesian TKDN (Tingkat Komponen Dalam Negeri) certification for its G20 agricultural drone, enabling broader access to public-sector procurement opportunities and supporting local sourcing requirements[3]Source: Terra Drone Corporation, “Terra Drone Indonesia Obtains TKDN Certification for Its In-House Developed Agricultural Drone G20,” Terra Drone, terra-drone.net. The market also remains open in retrofit spraying kits, service-based ownership models for smallholder farms, and pesticide formulations optimized for drone application. These opportunities are significant because many growers are prioritizing lower-cost upgrades and outsourced spraying services rather than full equipment replacement, ensuring continued competition across both equipment manufacturing and agricultural service models.

Southeast Asia Agricultural Sprayers Industry Leaders

KUBOTA Corporation

DJI Agriculture

Deere and Company

CNH Industrial N.V

Yanmar Holdings Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: DJI Agriculture debuted the Agras T55 (50 L payload) and Agras T100 Dual Battery Spraying System at AGRITECHNICA Asia 2026 in Bangkok.

- May 2026: Yanmar Holdings Co., Ltd. (Thailand) launched the YANMAR Solution Experience Center in Bang Nam Priao District, Chachoengsao Province, dedicated to precision agriculture technology transfer, smart farming demonstration, and integrated farm advisory for Thai farmers. This development provides access to precision spraying through knowledge transfer and advisory services to support purchasing new spraying equipment.

- October 2025: Terra Drone Indonesia obtained TKDN local content certification (31.26% local content ratio, exceeding Indonesia's 30% threshold) for its G20 agri-drone, unlocking eligibility for government and public-sector procurement in Indonesia. Terra Drone Indonesia will further expand its drone-based spraying services in the agricultural field and continue contributing to the advancement of Indonesia’s domestic industries through sustainable business development.

Southeast Asia Agricultural Sprayers Market Report Scope

Agricultural sprayers are specialized equipment designed to apply liquid substances, such as fertilizers, pesticides, herbicides, and fungicides, or water, evenly and in controlled amounts to crops, plants, or soil.

The Southeast Asia Agricultural Sprayers Market Report is segmented by power source (Manual, Battery-Operated, Solar-Powered, and Fuel-Operated), by product type (Handheld, Tractor-Mounted, Trailed, Self-Propelled, and Unmanned Aerial Vehicle Sprayers), by application (Field Crops, Orchards and Vineyards, Greenhouse Crops, and Turf and Gardening), by spray volume capacity (Ultra-Low Volume Systems, Low-Volume Systems, and High-VolumeSystems), by technology level (Conventional, Precision and GPS-Guided, and Artificial Intelligence-Enabled and Autonomous), by pump mechanism (Diaphragm Pumps, Piston Pumps, and Centrifugal Pumps), and geography (Indonesia, Vietnam, Thailand, the Philippines, Malaysia, Cambodia, Myanmar, Singapore, and Rest of Southeast Asia). The market values are provided in USD.

| Manual |

| Battery-Operated |

| Solar-Powered |

| Fuel-Operated |

| Handheld |

| Tractor-Mounted |

| Trailed |

| Self-Propelled |

| Unmanned Aerial Vehicle Sprayers |

| Field Crops |

| Orchards and Vineyards |

| Greenhouse Crops |

| Turf and Gardening |

| Ultra-Low Volume Systems |

| Low-Volume Systems |

| High-Volume Systems |

| Conventional |

| Precision and GPS-Guided |

| Artificial Intelligence-Enabled and Autonomous |

| Diaphragm Pumps |

| Piston Pumps |

| Centrifugal Pumps |

| Indonesia |

| Vietnam |

| Thailand |

| Philippines |

| Malaysia |

| Cambodia |

| Myanmar |

| Singapore |

| Rest of Southeast Asia |

| By Power Source | Manual |

| Battery-Operated | |

| Solar-Powered | |

| Fuel-Operated | |

| By Product Type | Handheld |

| Tractor-Mounted | |

| Trailed | |

| Self-Propelled | |

| Unmanned Aerial Vehicle Sprayers | |

| By Application | Field Crops |

| Orchards and Vineyards | |

| Greenhouse Crops | |

| Turf and Gardening | |

| By Spray Volume Capacity | Ultra-Low Volume Systems |

| Low-Volume Systems | |

| High-Volume Systems | |

| By Technology Level | Conventional |

| Precision and GPS-Guided | |

| Artificial Intelligence-Enabled and Autonomous | |

| By Pump Mechanism | Diaphragm Pumps |

| Piston Pumps | |

| Centrifugal Pumps | |

| By Country | Indonesia |

| Vietnam | |

| Thailand | |

| Philippines | |

| Malaysia | |

| Cambodia | |

| Myanmar | |

| Singapore | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

What is the current size of the Southeast Asia agricultural sprayers market?

The Southeast Asia agricultural sprayers market was valued at USD 315 million in 2025 and stands at USD 336.7 million in 2026, with forecast value reaching USD 470.1 million by 2031.

What is driving sprayer demand across Southeast Asia most strongly right now?

Labor shortages, subsidy-backed mechanization programs, and the need to cut chemical waste are the main demand drivers. In many cases, mechanized spraying is being adopted as a labor substitute rather than as an optional technology upgrade.

Which product category is growing fastest in agricultural spraying equipment?

Uumanned Aerial Vehicle sprayers are the fastest-growing product type, with a forecast CAGR of 14.2% through 2031, supported by wider drone service networks and stronger plantation and rice-sector adoption.

Which country leads regional demand for agricultural sprayers?

Indonesia led the region with a 31% share in 2025 because of its large oil palm estate base, broad agricultural land area, and government-backed mechanization financing.

Page last updated on: