Germany Agricultural Sprayers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

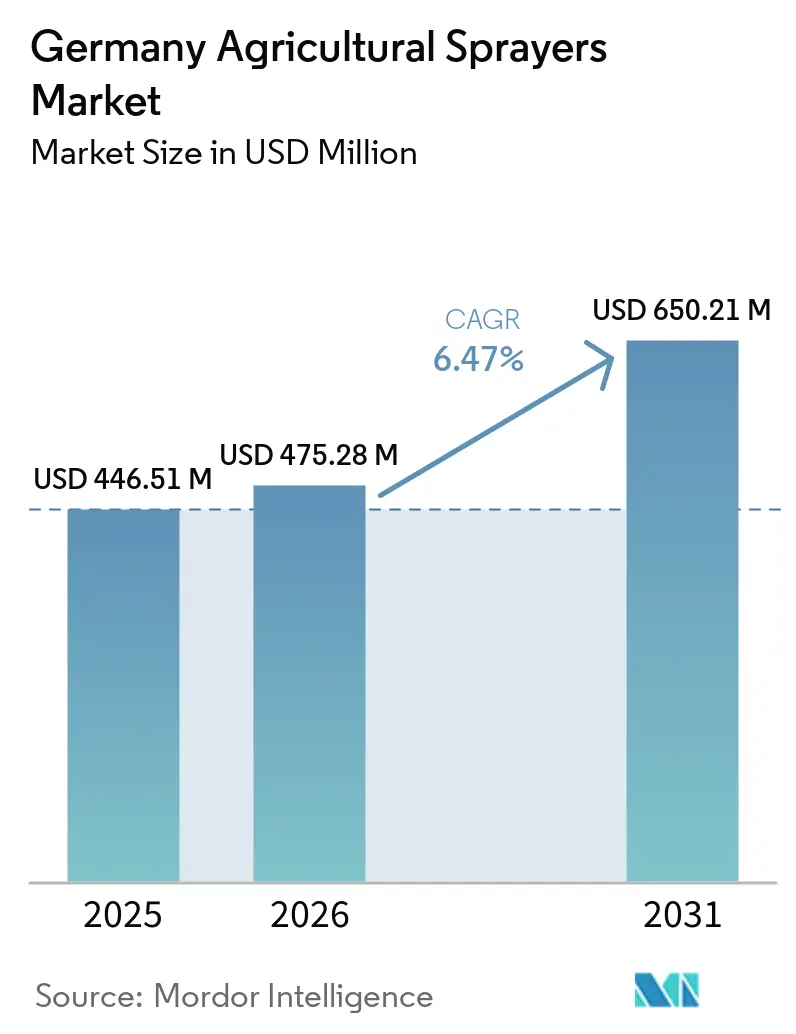

| Base Year Market Size (2025) | USD 446.51 Million |

| Market Size (2026) | USD 475.28 Million |

| Market Size (2031) | USD 650.21 Million |

| Growth Rate (2026 - 2031) | 6.47% CAGR |

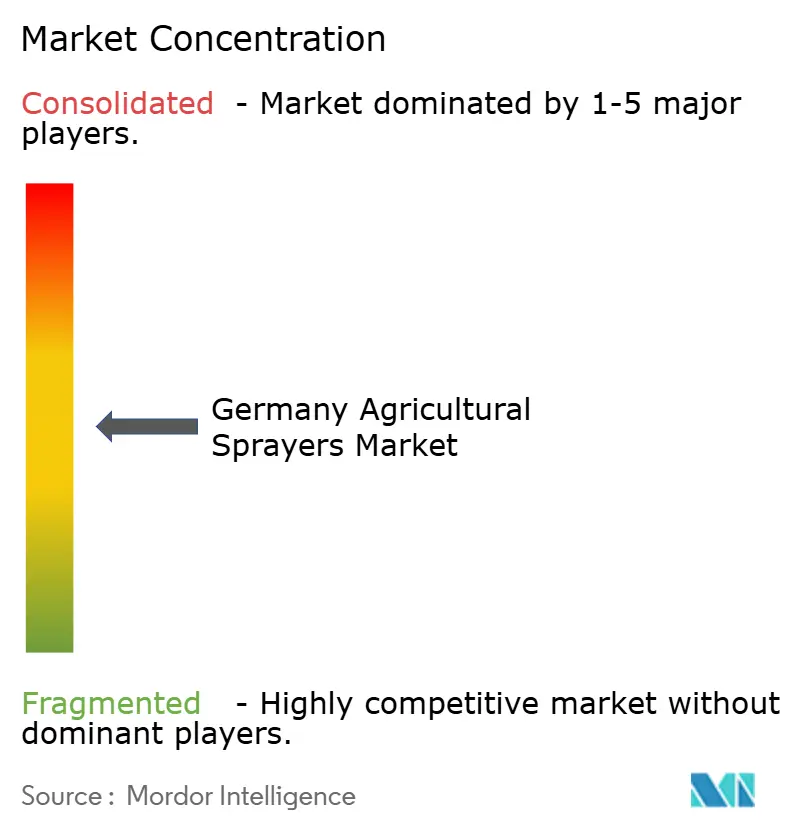

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Agricultural Sprayers Market Analysis by Mordor Intelligence

The Germany agricultural sprayers market size is estimated to increase from USD 446.51 million in 2025 and USD 475.28 million in 2026 to USD 650.21 million by 2031, growing at a CAGR of 6.47% during 2026 to 2031. Growth is being driven by Germany's stringent crop protection compliance framework, which is accelerating demand for connected and precision-ready spraying equipment. Revised German crop protection regulations that took effect on January 1, 2026, introduced additional documentation requirements, increasing the value of machine-native telemetry and automated record-keeping capabilities for growers and contractors[1]Source: Redaktion, “Pflanzenschutzmittel, Das Müssen Landwirte Ab 1. Januar Dokumentieren,” Land und Forst, landundforst.de. Market expansion is also supported by stricter drift-reduction requirements, mandatory sprayer inspection programs, and rising adoption of section control, direct injection, and prescription-based application technologies that help reduce input consumption and improve operational efficiency. In addition, competition is increasingly shifting beyond equipment performance toward software integration, operator training, and agronomic support services, particularly as unmanned aerial vehicle spraying, orchard automation, and artificial intelligence-enabled spot spraying gain commercial traction across Germany's agricultural sector.

Key Report Takeaways

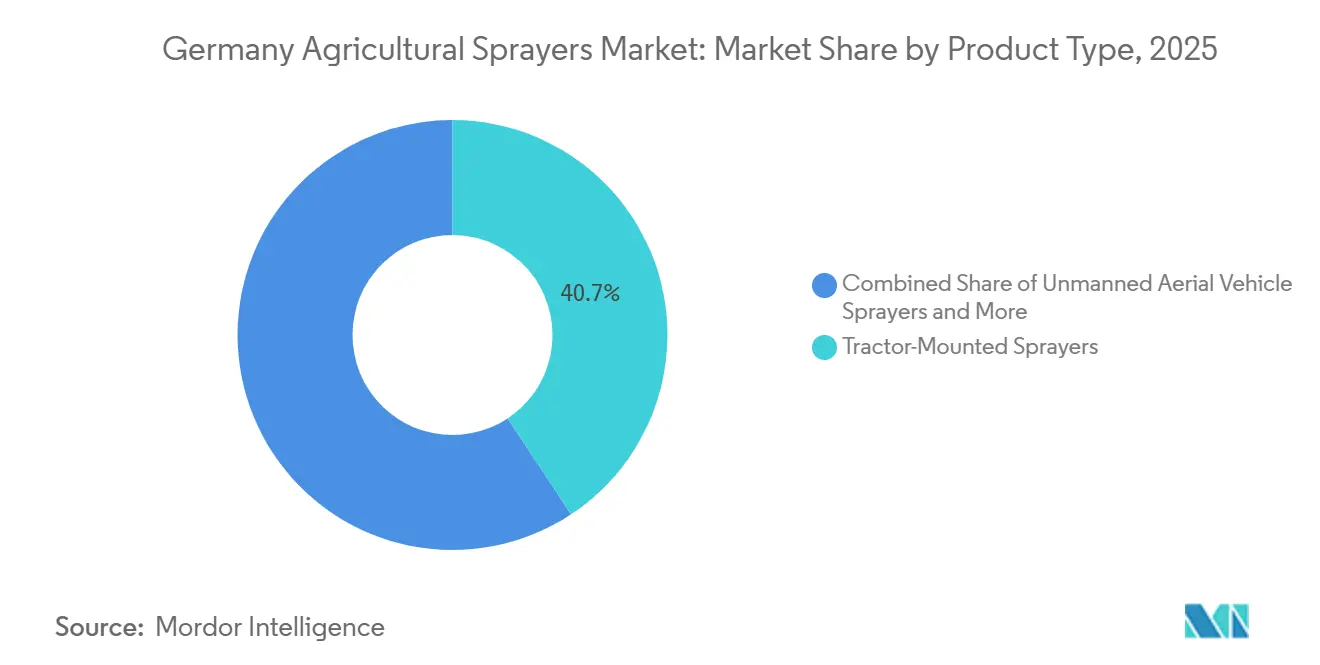

- By product type, tractor-mounted sprayers accounted for 40.7% of the Germany agricultural sprayers market size in 2025, while unmanned aerial vehicle sprayers are anticipated to grow at a 9.4% CAGR during the forecast period 2026-2031.

- By source of power, fuel-operated systems accounted for 41.2% of Germany agricultural sprayers market share in 2025, while battery-operated systems are projected to grow at a 7.1% CAGR during the forecast period 2026-2031.

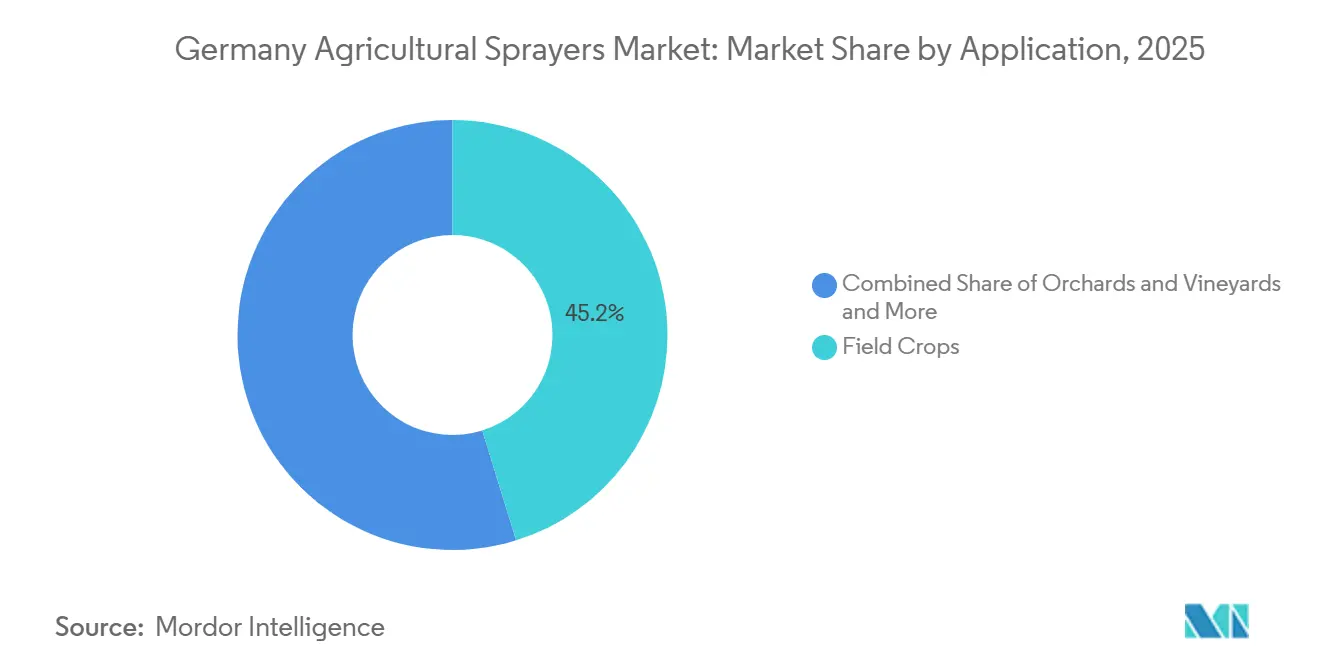

- By application, field crops represented 45.2% of Germany agricultural sprayers market size in 2025, while orchards and vineyards are forecast to grow at a 6.8% CAGR during the forecast period 2026-2031.

- By technology level, conventional sprayers accounted for 52.4% of Germany agricultural sprayers market share in 2025, while artificial intelligence-enabled and autonomous sprayers are projected to grow at a 8.3% CAGR during the forecast period 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Agricultural Sprayers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision spraying mandates from drift reduction and buffer-zone compliance | +1.20% | Nationwide across all German states, with the strongest enforcement in Lower Saxony and North Rhine-Westphalia | Short term (≤ 2 years) |

| Labor scarcity and rising custom-application costs | +0.90% | Nationwide, with the strongest pressure in Brandenburg, Mecklenburg-Vorpommern, Saxony-Anhalt, Thuringia, Bavaria, and Baden-Württemberg | Medium term (2-4 years) |

| Subsidies for targeted plant protection and drift avoidance | +0.60% | Nationwide through federal support, with strong state-level impact in Bavaria, Hesse, and Baden-Württemberg, and fruit and viticulture support through the FISU program | Short term (≤ 2 years) |

| Precision retrofits on large arable farms | +0.50% | Concentrated in large farms in Mecklenburg-Vorpommern, Brandenburg, Saxony-Anhalt, and Lower Saxony | Medium term (2-4 years) |

| Site-specific pesticide savings from direct injection and application assistants | +0.40% | Strongest return profile in northern German arable regions including Lower Saxony and Schleswig-Holstein | Medium term (2-4 years) |

| Connected sprayers supported by digital documentation workflows | +0.30% | Nationwide, with the clearest near-term impact on farms using digitally compatible equipment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Precision Spraying Mandates from Drift Reduction and Buffer-Zone Compliance

Germany’s crop protection regime is giving the market a compliance-based demand base rather than a purely discretionary replacement cycle. The Niedersachsen Pflanzenschutzdienst has laid out clear requirements on drift-reduction nozzle classes, boom-height settings, and border-nozzle use, and those rules directly influence which machines and retrofit packages can remain compliant in the field. When a grower uses a nozzle that is not recognized for drift reduction, the practical effect is a wider buffer requirement and a smaller sprayable area at field edges, turning compliance into a clear financial issue rather than a simple technical one. That is why investment in certified precision hardware is moving faster than the typical equipment replacement cycle in many parts of the market. The three-year equipment inspection requirement also creates a recurring decision point, because older conventional machines that fail inspection often require costly repairs or a full replacement to remain in service. This makes demand in the Germany agricultural sprayers market steadier than in several other farm machinery categories. The policy direction is also becoming tighter, with Germany targeting a 50% reduction in plant protection product use by 2030 from the 2004 to 2023 average[2]Source: Redaktion, “50% Weniger Pflanzenschutz Bis 2030,” Agrarheute, agrarheute.com, which keeps precision application systems relevant to both compliance and cost control.

Labor Scarcity and Rising Custom-Application Costs

Labor shortages are increasing the value of capacity, speed, and automation across the market. Farms and contractors in Northern and Western Europe are working within shorter spray windows, and each operator hour now carries more value during peak treatment periods. This is pushing buyers toward larger booms, bigger tanks, better route efficiency, and more automated functions that let one operator cover more hectares in a day. The change is especially visible in the contractor segment, where machine utilization across multiple farms matters more than single-farm ownership economics. HORSCH Maschinen GmbH expanded its Leeb PT self-propelled line in June 2025 with a 5,000-liter entry-level model aimed at a broader contractor base, underscoring manufacturers' stronger demand for high-capacity machines at a slightly lower entry point than the premium end of the category[3]Source: Tractors and Machinery, “5,000-Liter Entry Level Horsch Leeb Sprayer,” 2025, tractors-and-machinery.com. Labor scarcity is also supporting autonomous development in specialty crops, where navigation accuracy and repeatability can offset the shortage of trained seasonal operators. Kubota’s second-generation KFAST autonomous orchard sprayer moved from field trials in Spain and Portugal toward a limited commercial launch in mid-2026, with full European availability targeted for 2027.

Subsidies for Targeted Plant Protection and Drift Avoidance

Public funding programs are helping the market move from interest to actual procurement. Germany has approved funding for digital plant protection and drift-avoidance systems since 2022, reducing the payback risk for farms considering higher-value precision upgrades. The scale mentioned is based on approximately 4,200 approved applications, indicating that support is substantial enough to shape purchase timing rather than simply support pilot projects. Additional pathways also opened in 2026 for recycling sprayers in fruit and viticulture, broadening the benefits beyond broad-acre arable operations. Regional support programs, such as BaySL Digital, have been noted for providing co-financing ranging from 25% to 40% for software, sensors, and crop protection equipment. These programs are significant as they often consolidate purchases from one budget cycle into the subsequent procurement cycle, creating a more predictable demand pattern for dealers and manufacturers. In the context of the Germany agricultural sprayers market, the timing of subsidies has emerged as a critical commercial factor, particularly for technology upgrades that exceed the financial capacity of many mid-sized farms.

Precision Retrofits on Large Arable Farms

Retrofit demand is becoming an important and durable revenue stream within the Germany agricultural sprayers market. Large farms in Germany already show strong adoption of precision technologies on holdings above 100 hectares, meaning many buyers are no longer making a first precision purchase and instead moving from basic section control to individual-nozzle control, advanced sensors, and artificial intelligence-based spot treatment. That installed base matters because it lowers the learning curve and makes incremental upgrades more commercially acceptable than full machine replacement. The economics also support this stepwise path, since retrofit packages can extend the useful life of older platforms while adding measurable gains in chemical efficiency and documentation quality. This creates a second channel of growth beside new machine sales, and that channel can stay active even when farmers delay larger capital commitments. It also suits the Germany agricultural sprayers market because many commercial growers already operate compatible guidance and terminal systems. As a result, pulse-width modulation kits, camera-based add-ons, telemetry modules, and direct injection upgrades are all positioned to capture budget from farms that want precision gains without moving immediately to a new flagship platform.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of precision and autonomous sprayers | -1.30% | Strongest among farms below 50 hectares in Baden-Württemberg, Bavaria, and Rhineland-Palatinate | Medium term (2-4 years) |

| Operator know-how gap for advanced precision systems | -0.70% | Nationwide, with stronger friction in eastern German farms undergoing structural consolidation | Medium term (2-4 years) |

| Drone-use approvals remain narrow and multi-step | -0.50% | Germany-wide, with current practical use concentrated in steep-vineyard areas in Baden-Württemberg and Rhineland-Palatinate | Short term (≤ 2 years) |

| Documentation, inspection, and nozzle-compliance burden | -0.40% | Nationwide, with a heavier burden on smaller farms in Bavaria and Baden-Württemberg | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Precision and Autonomous Sprayers

High purchase prices still limit how quickly the Germany agricultural sprayers market can move toward precision-heavy fleets. Studies conducted by the German Association for Technology and Structures in Agriculture on farm machinery economics indicate that direct-injection self-propelled sprayers and precision retrofit systems require significant upfront capital expenditure, slowing adoption among cost-sensitive farming operations. In Germany, large arable farms and agricultural service providers can spread these costs across more hectares, whereas smaller operations often rely on subsidies, financing programs, or equipment-sharing arrangements to justify adoption. Although increased competition is estimated to reduce entry-level pricing for technologies such as unmanned aerial vehicle platforms and precision retrofit systems, the substantial upfront capital requirements remain a significant barrier to the widespread adoption of advanced agricultural sprayers.

Operator Know-How Gap for Advanced Precision Systems

Knowledge barriers remain a practical restraint in the market, especially beyond the most advanced commercial farms. According to a study on site-specific pesticide application in Germany, approximately 40% of German farmers in a precision application study cited limited agronomic knowledge as a major barrier to adopting site-specific plant protection. The issue goes beyond terminal operation, because users must interpret prescription maps, verify artificial intelligence-based weed detection outputs, calibrate sensors, and convert machine data into field decisions. That makes training and after-sales support almost as important as the machine itself. Manufacturers are responding, and DJI Technology Co., Ltd. expanded its DJI Academy curriculum in Europe from November 2025 to include precision spraying, spreader safety, and automated operations[4]Source: DJI Agriculture, “DJI Agriculture Unveils Agras T100, T70P, and T25P at Agritechnica 2025 in Hannover,” DJI Newsroom, dji.com. Even with that progress, adoption still slows when farms lack internal expertise or reliable local dealer support. This means the Germany agricultural sprayers market may continue to favor suppliers that can pair equipment sales with agronomic training, software guidance, and operator onboarding rather than selling hardware as a standalone product.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tractor Mounted Platforms Hold the Lead While Unmanned Aerial Vehicle Sprayers Grow Fastest

Tractor-mounted sprayers led product revenue with 40.7% in 2025, giving them the largest share of the Germany agricultural sprayers market. Trailed sprayers followed, then self-propelled units, while unmanned aerial vehicle sprayers and handheld models remained smaller categories shaped by narrower use cases and smaller starting bases. Their dominance is further supported by broad compatibility with existing tractors, lower ownership costs, and widespread availability across Germany.

Unmanned aerial vehicle sprayers are projected to expand at a 9.4% CAGR through 2031, giving them the fastest growth path in this segmentation and the strongest expansion in market size among product categories. Self-propelled and trailed platforms are also advancing as contractors seek higher daily coverage, while tractor-mounted systems remain central because they fit established farm fleets and field-scale economics. Handheld sprayers continue to serve smaller horticultural and greenhouse tasks rather than broad-acre field work. Growth is additionally supported by labor shortages, precision application benefits, and increasing acceptance of digital farming technologies.

By Source of Power: Fuel Operated Machines Still Dominate While Battery Systems Gain Ground

Fuel-operated systems accounted for 41.2% of 2025 revenue, making them the largest power-source segment for the Germany agricultural sprayers market. Manual systems remained relevant for small-scale use, while solar-powered units remained niche, and battery-operated machines were still smaller in terms of revenue despite stronger technology momentum. Their established infrastructure, proven field performance, and ability to support intensive spraying operations continue to strengthen adoption across Germany.

Battery-operated sprayers are projected to grow at a 7.1% CAGR during the forecast period 2026-2031, the fastest rate across power-source categories in the market. This rise is supported by orchard robots, greenhouse systems, and electric specialty-crop platforms, where tank size and endurance requirements are lower than in broad-acre spraying. Fuel-operated platforms will remain central throughout the forecast period, as large booms, higher horsepower, and long working hours still favor diesel-based machines. Manual and solar-powered systems should continue to play limited, crop-specific roles rather than drive mainstream fleet demand. Increasing sustainability targets and advances in battery efficiency are also encouraging wider adoption across specialized agricultural applications.

By Application: Field Crops Anchor Revenue While Orchards and Vineyards Expand Faster

Field crops accounted for 45.2% of 2025 revenue, making them the largest application segment and the main source of the Germany agricultural sprayers market size in current value terms. Orchards and vineyards followed, then greenhouse crops, while turf and gardening remained the smallest revenue category due to a narrower commercial equipment base. Their leadership is supported by extensive cultivation areas, consistent crop protection requirements, and widespread adoption of mechanized spraying equipment.

Orchards and vineyards are forecast to grow at a 6.8% CAGR through 2031, the fastest pace across application categories and the clearest growth pocket within the market. Greenhouse crops also support demand for precise low-drift equipment, while turf and gardening stay specialized and relatively small. Field crops continue to anchor total value due to larger treated areas and recurring application frequency, but specialty-crop investment is rising faster as estate owners seek precision canopy control, contractor independence, and autonomous operation amid tighter labor conditions. Growing emphasis on spray accuracy, labor efficiency, and input optimization is further accelerating technology adoption in specialty crops.

By Technology Level: Conventional Fleets Still Lead While Artificial Intelligence Platforms Advance Quickly

Conventional sprayers accounted for 52.4% of 2025 revenue, giving them the largest share of the German agricultural sprayers market within the technology benchmark. Precision and Global Positioning System-guided sprayers ranked next as the main upgrade tier, while artificial intelligence-enabled and autonomous machines remained smaller in current revenue because they are newer and more capital-intensive. Their strong presence reflects broad farmer familiarity, established service networks, and lower acquisition costs than those of advanced technologies.

Artificial intelligence-enabled and autonomous sprayers are projected to grow at a 8.3% CAGR through 2031, the fastest rate in this segmentation and the strongest technology-led market size expansion in growth terms. Precision and Global Positioning System-guided platforms should continue to absorb the broadest near-term upgrade demand, as their return on investment has already been proven on larger farms. Conventional fleets will continue to lose relative weight as digital reporting, section control, spot spraying, and machine connectivity become more important to both compliance and operating efficiency. Increasing investments in automation, data-driven agriculture, and labor-saving technologies are further accelerating adoption across commercial farming operations.

Geography Analysis

Germany's demand for agricultural sprayers is supported by 11.7 million hectares of arable land in 2025, according to the European Union. Additionally, the country has one of the largest average farm sizes in Western Europe, which supports ongoing investments in high-capacity and wide-boom equipment within the German agricultural sprayers market. The federal compliance framework also keeps replacement demand active because growers must work within drift-reduction nozzle classes, comply with mandatory 3-year equipment inspections, and meet Julius Kühn-Institut-approved nozzle requirements under the Pflanzenschutzgesetz (Plant Protection Act). This renewal pressure is especially visible in states such as Lower Saxony and North Rhine-Westphalia, where inspection enforcement is applied with greater consistency and commercial farming intensity is high. Germany also widened its crop protection documentation rules from January 2026, requiring growers to record EPPO crop codes, parcel identifiers, and treatment scope, while mandatory electronic filing begins from January 2027. That change is pushing more farms toward connected machines that can generate records directly from the cab, rather than relying on manual entry after the job is done.

The strongest commercial activity is concentrated in northern and eastern Germany, where Lower Saxony, Schleswig-Holstein, Brandenburg, Mecklenburg-Vorpommern, Saxony-Anhalt, and Thuringia contain many large arable holdings that can support investment in trailed and self-propelled sprayers with working widths above 30 meters. The eastern states are especially important because their larger field structures, shaped by post-reunification consolidation, make the economics of advanced boom sprayers and retrofit systems more attractive. Bavaria and Baden-Württemberg serve as Germany’s main specialty-crop sprayer centers, with horticulture and vineyard demand supporting precision atomizers, canopy-focused equipment, and recycling sprayers. Bavaria also stands out in the Germany agricultural sprayers market, with the BaySL Digital program remaining active in 2025 and providing co-financing of 25% to 40% for eligible investments in digital agriculture solutions, including sensors, software, and precision plant protection equipment. This support helps mid-sized farms overcome investment barriers and modernize their spraying operations.

North Rhine-Westphalia and the Rhine-Main corridor remain important western demand zones, where smaller average field sizes support mounted and compact trailed sprayers alongside larger contractor-operated machines. Contractor density is high in North Rhine-Westphalia and Lower Saxony, and that supports demand for self-propelled platforms serving intensive arable and vegetable production. The more urban-adjacent nature of these western farming areas also increases the practical importance of buffer distances and drift-reduction compliance, since applications near residential zones and public paths carry higher legal and operational sensitivity. Central Germany is also becoming more relevant to near-term investment, because Hesse opened a dedicated digitalization grant for agricultural enterprises, which widened the state-level support base beyond Bavaria and Lower Saxony.

Competitive Landscape

The competitive structure is moderately concentrated at the top, with Amazonen-Werke H. Dreyer GmbH & Co. KG, CNH Industrial N.V., Deere and Company, AGCO Corporation, and Kuhn Group accounting for a significant share of market revenue. That level of concentration gives the Germany agricultural sprayers market a clear leader set, but it still leaves meaningful room for specialist and mid-tier suppliers in orchard, retrofit, and contractor-focused niches. German incumbents benefit from close proximity to precision-intensive farming regions and from dealer networks that support electronics, calibration, and software updates. The competition is now moving beyond mechanical specifications alone toward connected workflows, deeper training, and compliance support.

One of the clearest disruptive moves came from DJI Technology Co., Ltd., which introduced the Agras T100, T70P, and T25P at Agritechnica in November 2025. That launch mattered because it gave the market a more visible commercial drone offering through authorized channels rather than isolated pilot activity. DJI Technology Co., Ltd. also expanded DJI Academy training in Germany, which shows that operator readiness is being treated as part of market entry rather than a separate support issue. Kubota also advanced specialty crops with the KFAST autonomous orchard sprayer commercial launch in 2026 signals that orchard automation is moving closer to normal commercial availability. These moves show that the Germany agricultural sprayers market is being shaped by both established field-equipment leaders and newer entrants focused on automation and crop-specific precision.

The mid-tier remains important because it serves white-space areas that large groups do not always cover with the same intensity. Nexus acquired Chafer Machinery Ltd in 2026 and rebranded the company as Nexus Chafer Ltd, while also introducing an 8,000-liter Sentry trailed sprayer and upgraded plumbing and steering systems in the same year. That move suggests there is still investment appetite in technically specialized sprayer businesses despite pressure from larger continental manufacturers. In specialty crops, suppliers remain relevant because crop-specific agronomy still matter a great deal. This leaves a competitive pattern where scale favors the leaders, but application knowledge, software fit, and local support still protect narrower specialist positions.

Germany Agricultural Sprayers Industry Leaders

Amazonen-Werke H. Dreyer GmbH & Co. KG

CNH Industrial N.V.

Deere and Company

AGCO Corporation

Kuhn Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: NEXUS Technology & Engineering Ltd has commercially launched a series of upgrades to its crop sprayer portfolio. These include the introduction of a new high-capacity Sentry trailed sprayer featuring an 8,000-liter tank. These enhancements aim to improve precision in application and reduce maintenance requirements for professional spraying operations.

- May 2026: Amazonen-Werke H. Dreyer GmbH & Co. KG partnered with CultiWise to integrate satellite- and drone-based prescription maps with AmaSelect and AmaXact precision-nozzle hardware via the AmaConnect cloud platform, expanding the practical use of variable-rate spraying workflows.

- November 2025: DJI Technology Co., Ltd. expanded its agricultural drone portfolio in Germany by introducing the Agras T100, equipped with a 100-liter spray payload, the Agras T70P with a 70-liter payload, and the Agras T25P with a 20-kg payload. Additionally, the company enhanced its DJI Academy training programs in Germany by integrating autonomous precision spraying operations, promoting the adoption of advanced aerial application technologies.

Germany Agricultural Sprayers Market Report Scope

Agricultural sprayers are equipment designed to apply crop protection chemicals, liquid fertilizers, and other agricultural solutions to crops in a controlled and efficient manner. The Germany agricultual sprayers market report is segmented by product type (handheld sprayers, tractor-mounted sprayers, trailed sprayers, self-propelled sprayers, and unmanned aerial vehicle sprayers), by source of power (manual, solar-powered, fuel-operated, and battery-operated), by application (field crops, orchards and vineyards, greenhouse crops, and turf and gardening), and by technology level (conventional, precision and GPS-guided, and AI-enabled and autonomous). The market forecasts are provided in terms of Value (USD).

| Handheld Sprayers |

| Tractor-Mounted Sprayers |

| Trailed Sprayers |

| Self-Propelled Sprayers |

| Unmanned Aerial Vehicle Sprayers |

| Manual |

| Solar-Powered |

| Fuel-Operated |

| Battery-Operated |

| Field Crops |

| Orchards and Vineyards |

| Greenhouse Crops |

| Turf and Gardening |

| Conventional |

| Precision and GPS-Guided |

| AI-Enabled and Autonomous |

| By Product Type | Handheld Sprayers |

| Tractor-Mounted Sprayers | |

| Trailed Sprayers | |

| Self-Propelled Sprayers | |

| Unmanned Aerial Vehicle Sprayers | |

| By Source of Power | Manual |

| Solar-Powered | |

| Fuel-Operated | |

| Battery-Operated | |

| By Application | Field Crops |

| Orchards and Vineyards | |

| Greenhouse Crops | |

| Turf and Gardening | |

| By Technology Level | Conventional |

| Precision and GPS-Guided | |

| AI-Enabled and Autonomous |

Key Questions Answered in the Report

What is pushing sprayer upgrades in Germany most strongly?

Tighter compliance rules expanded documentation from 2026, electronic submission from 2027, and recurring inspection requirements are pushing farms toward connected and precision-capable equipment.

Which product type is growing the fastest?

Unmanned aerial vehicle sprayers are forecast to grow at a 9.4% CAGR through 2031.

Which application is projected to register the highest growth?

Orchards and vineyards are forecast to grow at a 6.8% CAGR during the forecast period 2026-2031.

Where is the strongest application growth coming from?

Orchards and vineyards are projected to grow at a 6.8% CAGR through 2031, supported by canopy-focused precision spraying, labor pressure, and rising interest in autonomous platforms.

Page last updated on: