Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

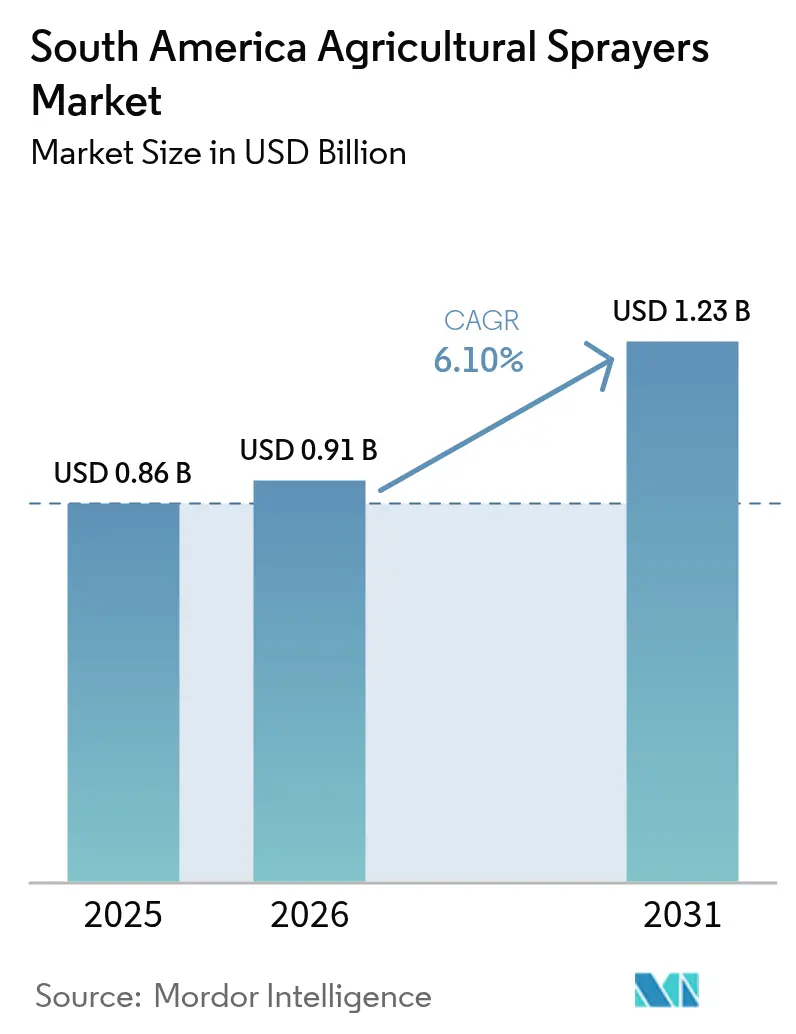

| Base Year Market Size (2025) | USD 0.86 Billion |

| Market Size (2026) | USD 0.91 Billion |

| Market Size (2031) | USD 1.23 Billion |

| Growth Rate (2026 - 2031) | 6.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Agricultural Sprayers Market Analysis by Mordor Intelligence

The South America agricultural sprayers market size is expected to grow from USD 0.86 billion in 2025 to USD 0.91 billion in 2026 and is forecast to reach USD 1.23 billion by 2031 at 6.10% CAGR over 2026-2031. The market growth is driven by increased mechanization as farmers address labor shortages and expand soybean cultivation across the region. Brazil’s Moderfrota financing line injected USD 2.46 billion in 2024/25 to modernize machinery fleets, while parallel 4G roll-outs in Argentina now cover 15 million hectares, easing real-time machine guidance across vast row-crop zones.[1]CNH Industrial, “CNH supports expanded rural connectivity in Latin America,” CNH.COM Farmers are adopting precision spraying systems with GPS guidance to reduce chemical usage and improve operational efficiency. Government-supported machinery financing programs and improved digital infrastructure enable real-time equipment monitoring and control. Increased pest pressure and climate variability contribute to market demand, while battery-powered and ultra-low-volume sprayers are gaining popularity due to reduced fuel consumption and lower operational costs. The adoption of efficient and environmentally sustainable farming practices influences equipment selection across South America.

Key Report Takeaways

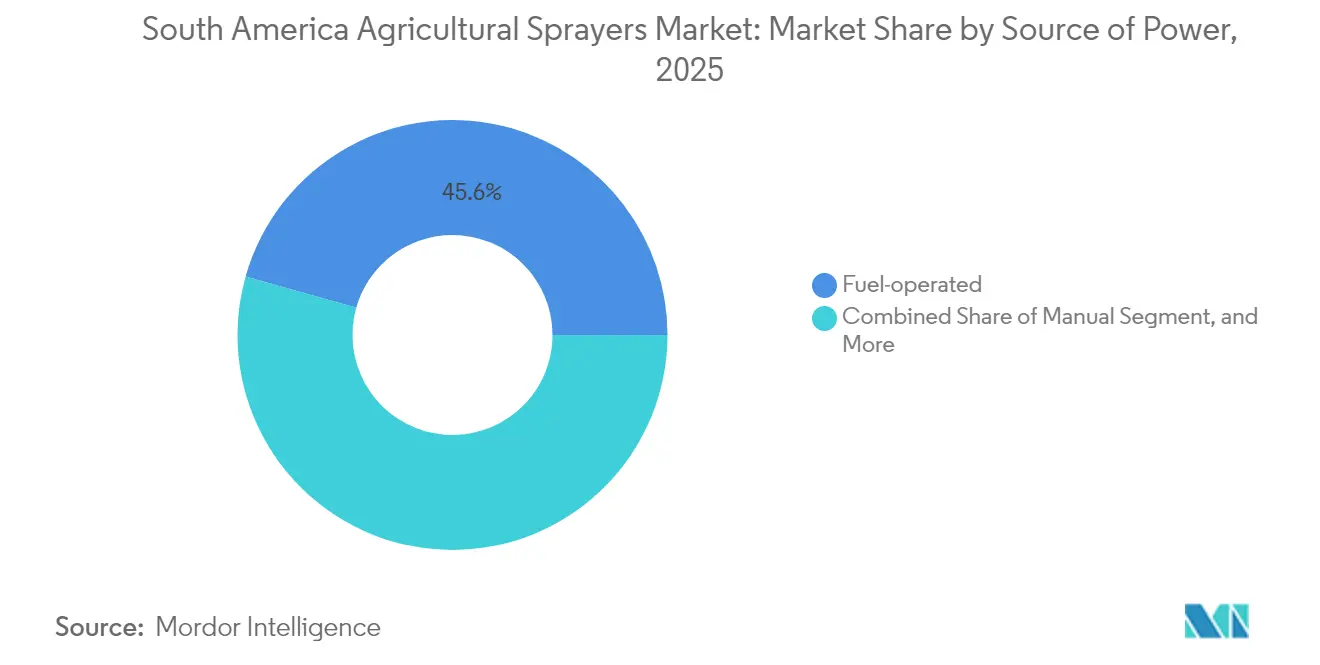

- By source of power, fuel-operated units led with 45.62% of the South American agricultural sprayers market share in 2025, and battery-operated systems are advancing at a 7.34% CAGR through 2031.

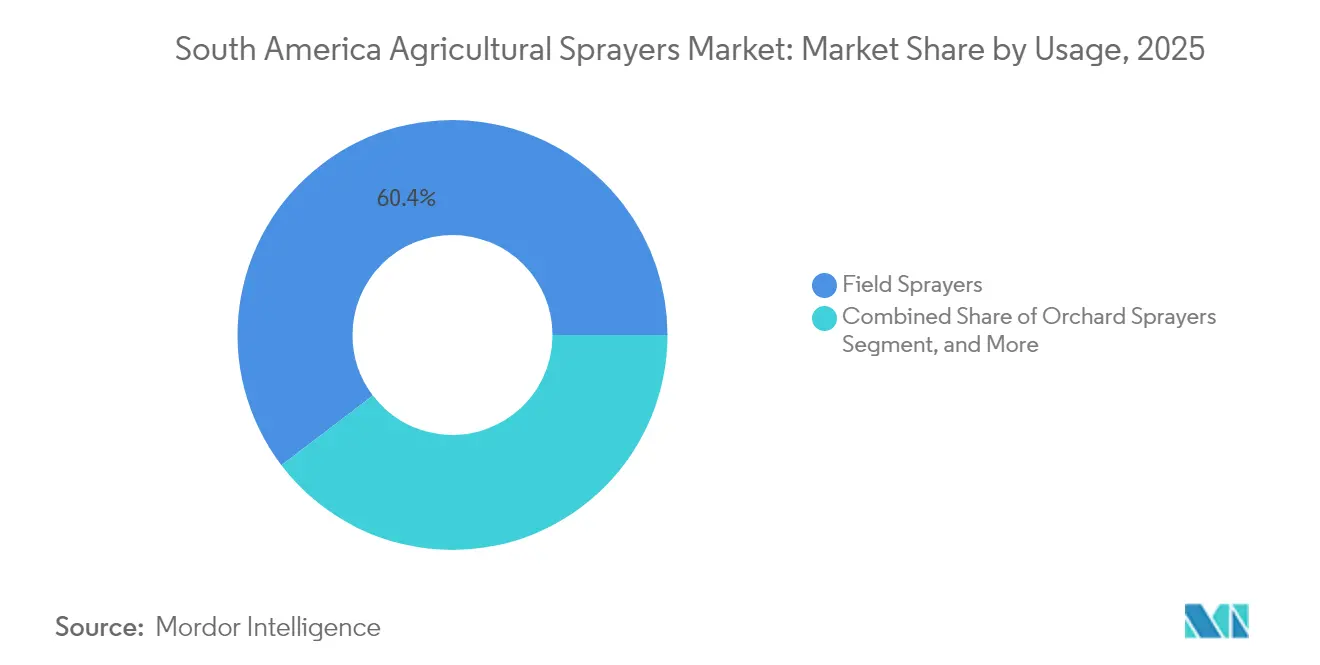

- By usage, field sprayers commanded a 60.35% share of the South American agricultural sprayer market size in 2025, and orchard sprayers are projected to grow at a 6.18% CAGR to 2031.

- By mode of capacity, high-volume equipment accounted for a 51.20% share of the market in 2025, whereas ultra-low-volume technology is expanding at a 6.88% CAGR through 2031.

- By geography, Brazil held a 67.10% share of the market in 2025, and Argentina is growing the fastest with a 7.06% CAGR to 2031.

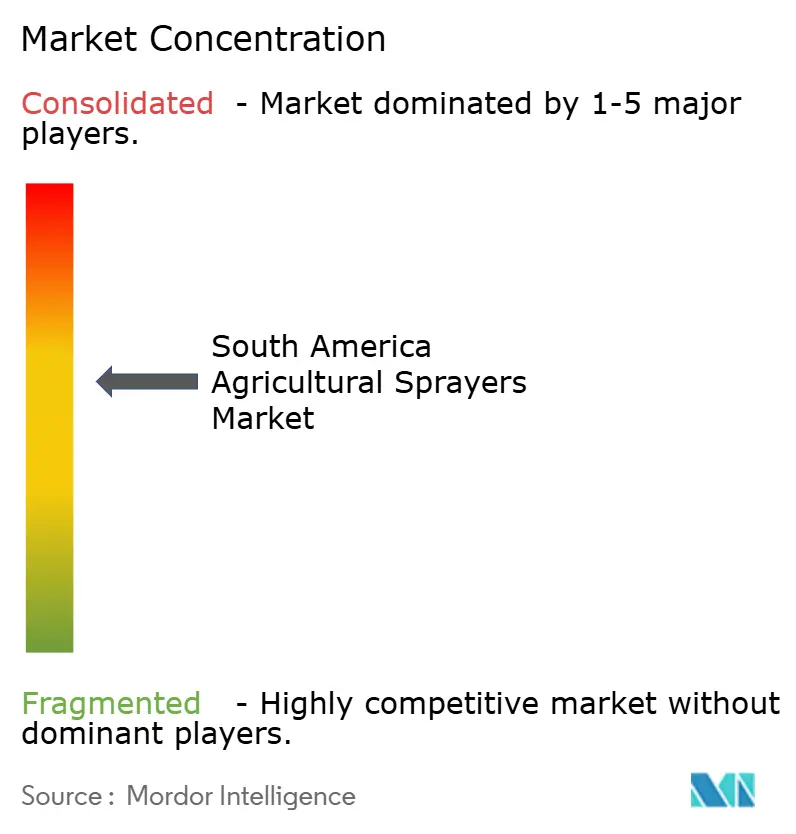

- Deere and Company, AGCO Corporation, CNH Industrial N.V., Jacto S.A., and Stara S/A together controlled nearly half of the market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Agricultural Sprayers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking Rural Labor Pool | +1.8% | Global, with acute impact in Brazil and Argentina | Medium term (2-4 years) |

| Expansion of Soybean Acreage and Agrochemical Intensity | +1.5% | Brazil core, spill-over to Argentina and Paraguay | Long term (≥ 4 years) |

| Government Subsidies for Crop-protection Mechanization | +1.2% | Brazil and Argentina primary, emerging in Colombia | Short term (≤ 2 years) |

| Adoption of GPS-guided Precision Spraying | +0.9% | Brazil and Argentina leading, expanding to Chile and Uruguay | Medium term (2-4 years) |

| Climate-linked Pests and Diseases Pressure Spikes | +0.7% | Global, with varying intensity across sub-regions | Long term (≥ 4 years) |

| Carbon-credit Premiums for Input-efficient Farms | +0.4% | Brazil leading, Argentina following, and early adoption in Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shrinking Rural Labor Pool

South America's agricultural labor force continues to decline as younger generations move to urban areas and older farmers retire, creating a shortage of skilled operators for complex spraying operations. This workforce reduction has led to increased wages and shorter spraying windows, compelling growers to invest in self-propelled or autonomous machines for extended, efficient operations. Robotic systems that combine scouting and spraying functions are increasing in adoption, offering reduced input costs. Brazil leads the region in agricultural automation, with Argentina following closely. This shift in the regional workforce continues to drive growth in the agricultural sprayers market across South America.

Expansion of Soybean Acreage and Agrochemical Intensity

The rapid expansion of soybean cultivation in South America has intensified the need for crop protection equipment. The presence of diseases such as Asian Soybean Rust requires multiple applications during growing seasons, making efficient and timely spraying crucial. Farmers managing larger fields with limited operational windows are investing in high-capacity sprayers to increase coverage rates. Precision spraying technologies have gained adoption as farmers seek to control costs amid variable commodity prices. These systems enhance application accuracy while reducing waste. The combination of increased acreage and agrochemical requirements continues to support market growth for agricultural sprayers in the region.

Government Subsidies for Crop-protection Mechanization

Government initiatives are accelerating mechanization in South America's agricultural sector. Credit programs and subsidies reduce financing costs and improve capital access for farmers investing in modern spraying equipment.[2]Governo de São Paulo, “Pró-Trator subsidy,” AGRICULTURA.SP.GOV.BR These programs align with agricultural seasonal cash flows, enabling better budget management for producers. Favorable interest rates and loan terms reduce equipment payback periods, encouraging rapid adoption of advanced machinery. This has accelerated fleet modernization and increased the adoption of advanced sprayers. Government support continues to strengthen the agricultural sprayers market across South America.

Adoption of GPS-guided Precision Spraying

GPS-guided spraying systems are becoming standard in South American agriculture. Farmers are implementing digital solutions that enhance chemical application accuracy, decrease input usage, and improve operational efficiency. Modern equipment, including drones and smart sprayers, enables sectional and targeted treatments, reducing environmental impact while improving crop protection effectiveness. Equipment manufacturers are developing hardware with integrated vision systems for real-time control and data-based operations. Satellite partnerships are addressing connectivity issues, expanding digital farming access in remote regions. The increasing adoption of technology continues to drive demand for precision-equipped sprayers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Farm Income Tied to Soft-commodity Prices | -1.4% | Global, with acute impact in export-dependent regions | Short term (≤ 2 years) |

| High Upfront Cost of Self-propelled Units | -1.1% | Regional, affecting small to medium producers primarily | Medium term (2-4 years) |

| Patchy Rural Broadband Hampers Telematics | -0.8% | Brazil and Argentina core, improving gradually | Medium term (2-4 years) |

| Fuel Price Inflation Raising Operating Costs | -0.6% | Global, with varying impact by operational intensity | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Farm Income Tied to Soft-commodity Prices

Fluctuating commodity prices affect farm income across South America, creating uncertainty in agricultural equipment investments. Rising global grain stockpiles often lead to price decreases, reducing farmers' margins for machinery upgrades. This financial pressure results in delayed purchases, loan restructuring, and limited credit access for new sprayers. Market momentum can stall even during periods of strong demand due to revenue volatility. These cyclical downturns affect the agricultural sprayers market's growth, making it dependent on commodity trends and rural producers' financial stability.

High Upfront Cost of Self-propelled Units

Self-propelled sprayers require significant financial investment from South American farmers, with costs exceeding annual earnings for many diversified operations. Strict lending requirements limit credit access for smaller producers despite available financing options. Equipment depreciation accelerates due to technological advancements, particularly in crops like sugarcane and cotton. While cooperative ownership and flexible payment options exist, their use remains minimal. These financial constraints limit mechanization progress and agricultural sprayers market growth, especially among small and medium-sized farms unable to manage the initial investment costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source of Power: Fuel Dominance Meets Electric Innovation

Fuel-operated equipment retained 45.62% of the South American agricultural sprayers market share in 2025 because diesel technology offers ample power density and rapid refueling over thousands of hectares of soy and corn. The South American agricultural sprayers market size for battery models, however, is climbing at 7.34% CAGR as large growers test solar-charged fleets to cut fuel costs and qualify for low-carbon premiums.

Autonomous battery sprayers slash herbicide bills and mitigate operator shortages, sharpening their payback profile despite higher acquisition costs. Solar support trailers from Jacto and field-scale charging hubs are addressing range concerns. Manual and solar units still fill niche needs among smallholders or protected-crop growers, but are gradually conceding share to powered alternatives. The power-source mix illustrates the South American agricultural sprayers market evolution toward greener, data-ready solutions.

By Usage: Field Applications Lead Orchard Expansion

Field sprayers covered 60.35% of usage in 2025, mirroring the dominance of row crops across Brazil’s Cerrado and Argentina’s Pampas regions. Long-reach booms and 4,000-liter tanks ensure timely coverage across contiguous soybean blocks where a single application can protect yields worth millions of dollars.

Orchard units are advancing at a 6.18% CAGR as specialty fruit acreage grows in Brazil’s south and in Chile’s export corridors. Autonomous GUSS sprayers are undergoing trials for citrus and nut groves, indicating a broader move toward precision canopy treatments. Gardening or greenhouse sprayers remain a stable but small slice, catering to high-value vegetables and floriculture. These divergent growth paths underscore how crop diversification is reshaping demand patterns within the South American agricultural sprayers market.

By Mode of Capacity: High-Volume Efficiency Versus Ultra-Low Precision

High-volume platforms commanded 51.20% of the South American agricultural sprayers market size in 2025 because large tanks and broad booms reduce downtime and maximize weather windows. Such rigs dominate soybean belts where one missed fungicide pass can trigger steep yield penalties.

Ultra-low-volume systems, growing at 6.88% CAGR, deploy AI cameras and PWM valves to place droplets only where needed, cutting herbicide use by 54.2% in Stara’s Eco Spray field trials. Medium-capacity low-volume rigs still serve mid-scale farms, bridging throughput and precision needs. This capacity spectrum demonstrates how the South America agricultural sprayers market balances productivity and sustainability imperatives.

Geography Analysis

Brazil holds 67.10% of South America's agricultural sprayers market share in 2025. This dominance stems from extensive soybean cultivation areas, agricultural credit programs, and increased adoption of domestically manufactured precision spraying systems. While recent economic conditions have temporarily reduced machinery purchases, market growth is anticipated to resume due to equipment replacement needs and sustainability initiatives. The expansion of satellite internet coverage in rural farming regions is improving digital connectivity, enabling broader implementation of precision agriculture practices and strengthening Brazil's position in the regional sprayers market.

Argentina shows the highest growth rate at 7.06% CAGR through 2031. This growth is supported by improved digital infrastructure and increased use of drone-assisted spraying technology, which enhances operational efficiency and reduces input costs. Export-linked financing options enable farmers to invest in advanced sprayer systems. The introduction of new equipment with selective spraying features is raising performance standards. The combination of technological innovation, flexible financing, and enhanced network coverage establishes Argentina as an emerging leader in South America's precision agriculture sector.

Colombia, Chile, Paraguay, Uruguay, and Bolivia are gradually implementing precision spraying technologies. Chilean orchards are testing autonomous spraying systems, while Paraguayan farmers are addressing weed resistance issues through targeted application methods. Colombia demonstrates potential for increased mechanization through improved crop yields, despite challenges from land fragmentation and limited financing options. These markets, though smaller in scale, present growth opportunities for manufacturers looking to expand their presence and meet the increasing demand for agricultural technology solutions in South America.

Competitive Landscape

The South American agricultural sprayers market size is moderate consolidated, with the top five suppliers accounting for approximately 62% market share in 2024. Deere & Company holds a significant share, supported by its extensive service network and vision technology integration. AGCO Corporation maintains market presence through its Valtra and Massey Ferguson brands among mid-size agricultural operations, while CNH Industrial N.V. focuses on enhancing connectivity through telecom partnerships and implementing AI-enabled spraying systems.

The market competition has evolved from equipment specifications to software capabilities. Stara S/A and Bosch BASF Smart Farming have introduced precision weed-management systems in South America, integrating camera technology, analytics, and automated dosing systems. The market has also expanded to include companies like Psyche Aerospace, which offers electric drone platforms. This transformation indicates an industry-wide shift toward data-driven application systems that optimize input usage and provide alternatives to conventional ground equipment.

Market expansion opportunities focus on telematics and autonomous systems, with manufacturers developing partnerships with telecommunication providers and implementing cloud platforms to utilize agricultural data. Partnerships with SpaceX, Telecom Argentina, and regional internet service providers enable connectivity in remote agricultural areas. These technological integrations improve equipment performance and strengthen customer relationships through integrated data services, allowing companies to increase long-term customer value in the South American agricultural sprayers market.

South America Agricultural Sprayers Industry Leaders

Deere & Company

AGCO Corporation

CNH Industrial N.V.

Jacto S.A.

Stara S/A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Stara S/A launched the Eco Spray spot spraying system, integrated into the Imperador 3000 and 4000 sprayers. The system uses AI-powered cameras and LED sensors to detect and target weeds precisely, reducing agrochemical usage and operational costs across South America's farming landscapes.

- June 2024: Jacto S.A. launched the Jacto SB-20B battery-powered backpack sprayer. The ergonomically designed product features a pump with five times longer durability compared to existing market alternatives.

- April 2024: Deere & Company began production of its See & Spray Select smart spraying technology at an expanded factory in Goias, investing over USD 120.7 million. The system combines computer vision, artificial intelligence, and machine learning to apply herbicides precisely to target areas, minimizing overall herbicide consumption.

South America Agricultural Sprayers Market Report Scope

An agricultural sprayer is a piece of equipment that is used to apply herbicides, pesticides, and fertilizers on crops. The South America agricultural sprayers market is segmented by the Source of Power (Manual, Battery-operated, Solar Sprayers, and Fuel-operated), Usage (Field Sprayers, Orchard Sprayers, and Gardening Sprayers), Mode of Capacity (Ultra Low Volume, Low Volume, and High Volume) and Country (Brazil, Argentina, and Rest of South America). The report offers market size and forecasts in terms of value (USD) for all the above segments.

By Source of Power

| Manual |

| Battery-operated |

| Solar |

| Fuel-operated |

By Usage

| Field Sprayers |

| Orchard Sprayers |

| Gardening Sprayers |

By Mode of Capacity

| Ultra-Low Volume |

| Low Volume |

| High Volume |

By Geography

| Brazil |

| Argentina |

| Rest of South America |

| By Source of Power | Manual |

| Battery-operated | |

| Solar | |

| Fuel-operated | |

| By Usage | Field Sprayers |

| Orchard Sprayers | |

| Gardening Sprayers | |

| By Mode of Capacity | Ultra-Low Volume |

| Low Volume | |

| High Volume | |

| By Geography | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current South America agricultural sprayers market size, and how is it projected to grow by 2031?

It stands at USD 0.91 billion and is on track for USD 1.23 billion by 2031 at 6.10% CAGR (2026-2031).

Which country dominates demand for crop sprayers across South America?

Brazil leads with 67.10% share, driven by vast soybean acreage and subsidized machinery credit.

What is the fastest-growing product category in regional spraying equipment?

Battery-operated sprayers are expanding at 7.34% CAGR due to lower fuel use and carbon-credit incentives.

What is the main restraint on sprayer investment in the region?

Volatile commodity prices and high interest rates compress margins and delay capital purchases, especially for self-propelled units.

Which segment shows the highest market share by capacity?

High-volume sprayers hold 51.20% share because they maximize field coverage during narrow spray windows.

Page last updated on: