Brazil Agricultural Sprayers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

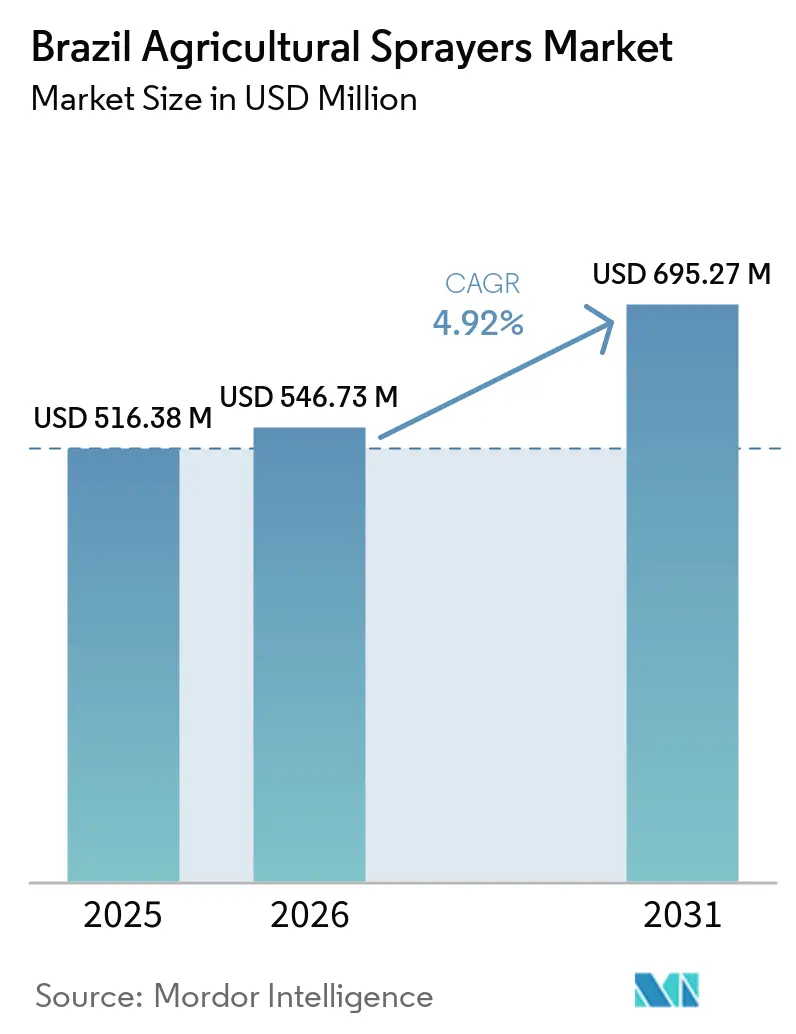

| Base Year Market Size (2025) | USD 516.38 Million |

| Market Size (2026) | USD 546.73 Million |

| Market Size (2031) | USD 695.27 Million |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Agricultural Sprayers Market Analysis by Mordor Intelligence

The Brazil agricultural sprayers market size is anticipated to increase from USD 516.38 million in 2025 to USD 546.73 million in 2026 and reach USD 695.27 million by 2031, growing at a CAGR of 4.92% during 2026-2031. Brazil's robust crop production underpins the agricultural sprayers market, with soybean output forecasted at 180.1 million metric tons and total grain production estimated at 358.0 million metric tons for the 2025/26 season, according to the National Supply Company (CONAB)[1]Source: National Supply Company (Conab), Federal Government of Brazil, “Brazilian Grain Harvest Could Reach a Record and Total 358 Million Metric Tons,” gov.br.. Demand is also rising because application intensity is increasing faster than crop area, with Brazil’s potential treated area reaching 2.68 billion hectares in 2025, up from 1.63 billion hectares compared to the past 5 years, keeping sprayer utilization high even as machinery purchases slow. The market is also being reshaped by frontier farming in the North and the MATOPIBA corridor, where terrain limits ground access, strengthening the case for aerial spraying platforms. Competition remains moderately concentrated, with the top 5 players holding a major share of the market, while domestic manufacturers continue to close the capability gap in precision and selective application systems. Near-term financing pressure and drone compliance gaps are slowing purchase timing in some channels, but the Brazil agricultural sprayers market continues to hold its forward path because farm spraying remains a recurring operational need rather than a discretionary one.

Key Report Takeaways

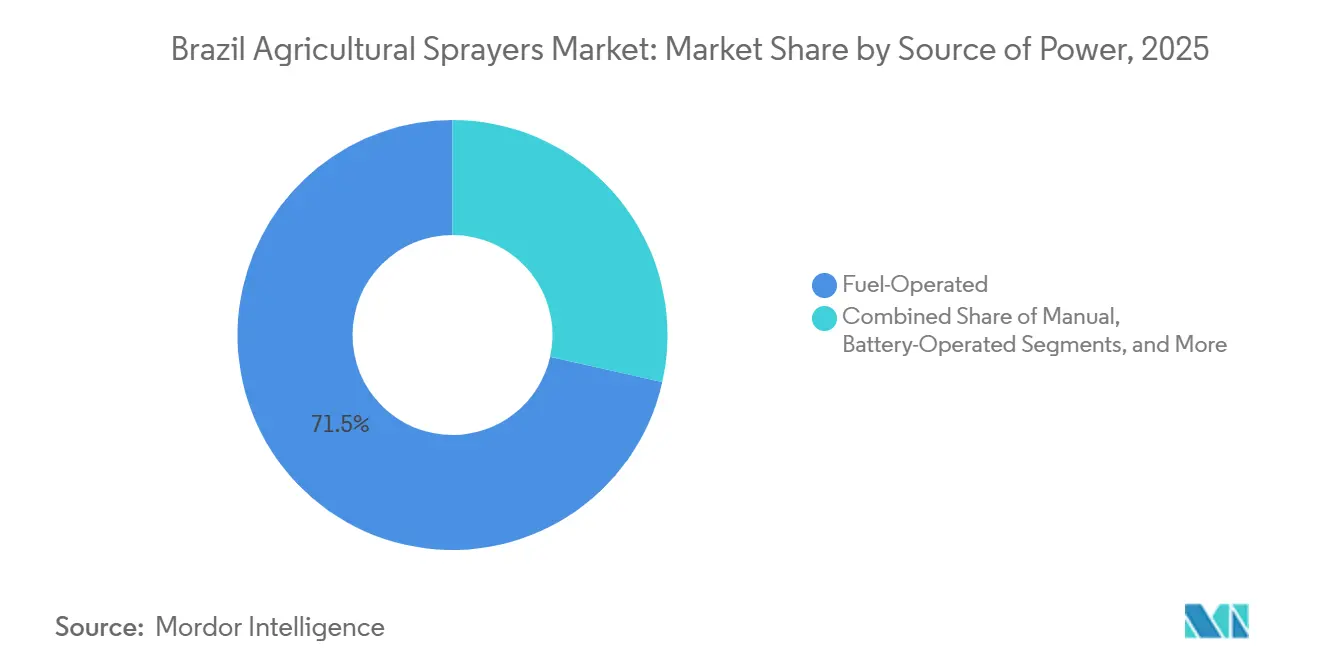

- By source of power, fuel-operated was the largest segment, and accounted for 71.5% of the Brazil agricultural sprayers market size 2025, while battery-operated will record the fastest growth with a 6.8% CAGR during 2026-2031.

- By product type, tractor-mounted sprayers led with 46.8% of the Brazil agricultural sprayers market size in 2025, while unmanned aerial vehicle sprayers will be the fastest-growing segment with a 10.9% CAGR during 2026-2031.

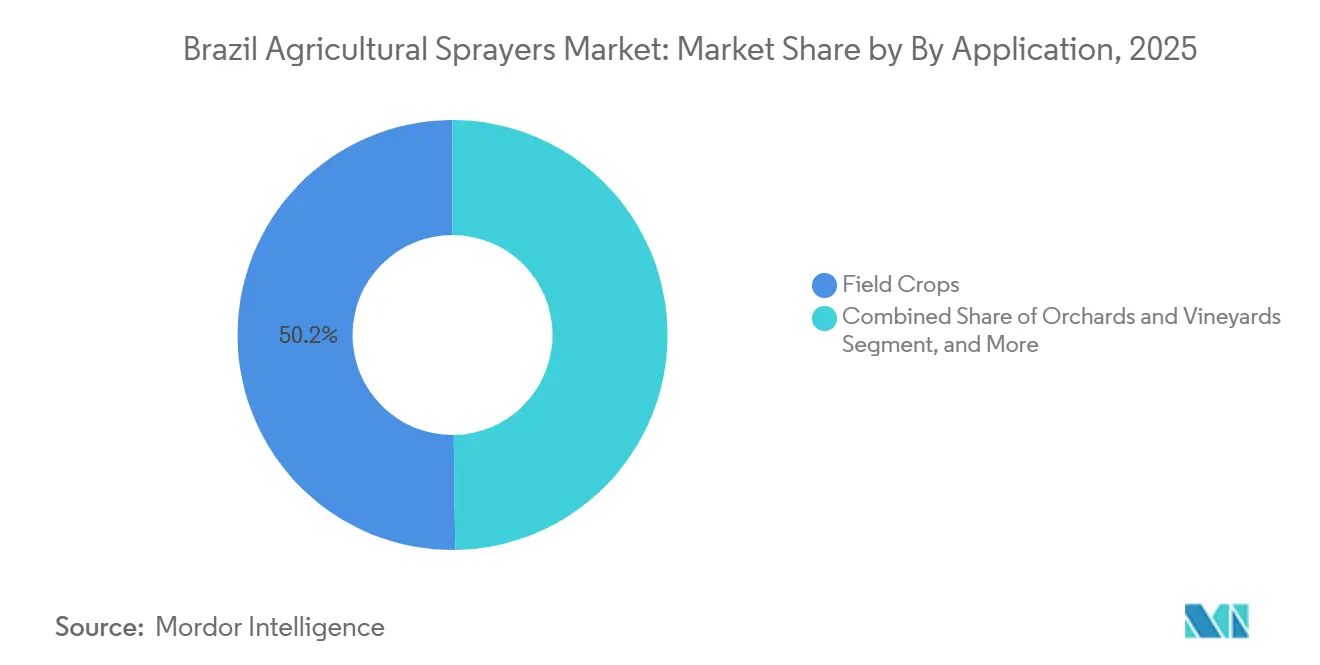

- By application, field crops were the largest segment with 50.2% share in 2025, while orchards and vineyards will post a 6.2% CAGR during 2026-2031.

- By spray volume capacity, low-volume sprayers were the largest segment with 48.3% share in 2025, while ultra-low-volume sprayers will be the fastest-growing segment with a 10.2% CAGR during 2026-2031.

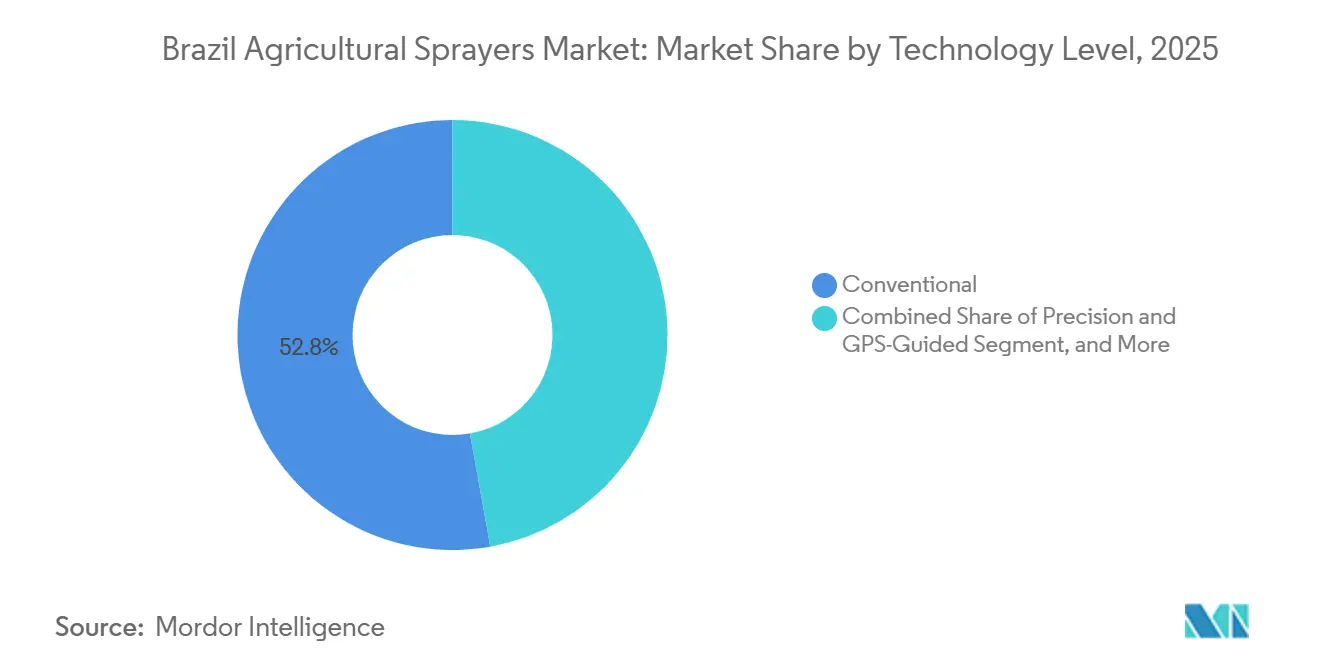

- By technology level, conventional sprayers were the largest segment with 52.8% share in 2025, while artificial intelligence-enabled and autonomous sprayers are projected to register a 10.5% CAGR during 2026-2031.

- By pump mechanism, diaphragm pumps were the largest segment with 42.9% share in 2025, while centrifugal pumps will be the fastest segment with a 6.6% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Agricultural Sprayers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soybean and corn acreage expansion in Brazil | +1.80% | Center-West, Northeast, and South, where crop area expansion continues to drive equipment demand. | Short term (≤ 2 years) |

| Higher pesticide-treated area and resistance-driven application intensity | +1.20% | Center-West and MATOPIBA, with widespread relevance across Brazil due to intensive spraying practices. | Medium term (2–4 years) |

| Precision spraying adoption in large commercial farms | +0.80% | Center-West, South, and Northeast, where large-scale farms are leading technology adoption. | Medium term (2–4 years) |

| Fleet renewal demand and rental-led access expansion | +0.50% | Center-West, South, and Southeast, supported by fleet replacement and equipment rental growth. | Short term (≤ 2 years) |

| Drone adoption in hard-to-access Brazilian production zones | +0.90% | North, Northeast, and Southeast, where terrain and field access favor aerial spraying. | Short term (≤ 2 years) |

| Citrus and mountain coffee automation demand | +0.40% | Southeast, South, and Northeast, driven by orchard and coffee-growing regions. | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Soybean and Corn Acreage Expansion in Brazil

Brazil’s soybean and corn footprint remains the clearest volume base for the Brazil agricultural sprayers market. According to the National Supply Company (Companhia Nacional de Abastecimento, CONAB), soybean planted area reached 48.7 million hectares in the 2025/26 season, while corn occupied 22.8 million hectares across Brazil's three annual crops. Total planted grain area stood at 83.9 million hectares. That scale matters because each additional hectare creates recurring application demand for herbicides, fungicides, and insecticides, rather than a one-time machinery event. Expansion is also not evenly distributed, and newer farming zones in the Northeast and northern frontier areas place more pressure on flexible spraying formats where access can be difficult during narrow field windows. The result is that acreage growth supports the installed base for conventional boom sprayers and also broadens the runway for aerial formats that can reach fields faster in remote areas. With total grain production projected at 358.0 million metric tons in 2025/26 as per the National Supply Company (CONAB), the agricultural sprayers market in Brazil continues to rest on a crop base that remains both large and operationally intensive[2]Source: National Supply Company (Conab), Federal Government of Brazil, “Grain Production and Planted Area for the 2025/26 Crop Season Continue to Show Prospects for New Records,” gov.br..

Higher Pesticide-Treated Area and Resistance-Driven Application Intensity

Application intensity is growing faster than field expansion, and that is one of the strongest supports for the agricultural sprayers industry in the country. According to the National Union of the Plant Protection Products Industry, Brazil's potential treated area exceeded 2.5 billion hectares in 2024, representing a 12.2% increase from 2023. During the first quarter of 2025, the potential treated area expanded by a further 1.8% year-on-year to more than 831 million hectares, reflecting continued growth in crop protection activity across major agricultural regions. The continued rise in spray applications reflects increasing pest, disease, and weed management requirements, supporting higher sprayer utilization rates across major crop-producing regions. This pattern means sprayer utilization hours can rise even in years when the farm machinery cycle is soft, because the same land requires more interventions across the season. It also moves buyer attention toward durability, capacity, and selective application features, since replacement decisions are increasingly tied to wear and operating intensity rather than area growth alone.

Precision Spraying Adoption in Large Commercial Farms

Large farms are steadily shifting toward selective application, which keeps the premium end of the market active. Stara S.A. Indústria de Implementos Agrícolas launched the Imperador 3000 Eco Spray and Imperador 4000 Eco Spray in Brazil in February 2025. The sprayers use cameras and AI, with nozzle-level activation to spray only detected weeds[3]Source: Stara S.A., “Eco Spray – A Pioneer in Precision Agriculture,” stara.com.br.. The company states that the system operates in pre-emergent and post-emergent modes and can run day and night, increasing field flexibility for large operators. One producer cited by the company reported average product savings of 54.2% after using the system from October 2024, which illustrates the economic case for precision spraying in areas with high chemical bills. Adoption remains strongest on large commercial farms because these operators have the scale, field data, and management systems to turn selective spraying into a measurable return on investment. This pushes the Brazil agricultural sprayer market toward a more tiered structure, where conventional units still dominate volume, but digital and selective systems capture a larger share of premium spending.

Drone Adoption in Hard-to-Access Brazilian Production Zones

Drone adoption is now a visible growth engine within the Brazil agricultural sprayers market. Brazil moved from an estimated 3,000 agricultural drones sold in 2021 to around 35,000 units in operation by June 2025, following the regulatory framework introduced by the Ministry of Agriculture and Livestock. The same official source states that only 2,618 remotely piloted aircraft were registered for spraying at that point, indicating how much of the operating base still sits outside formalization. SZ DJI Technology Co., Ltd stated in April 2026 that precise spot spraying with drones in Brazil can reduce herbicide use by up to 35.0%, thereby improving the economics of adoption in large, difficult fields. These platforms gain the most traction in production zones with weak road access, irregular terrain, or narrow weather windows, where the value of faster deployment can outweigh the smaller tank size. This is why drone demand in Brazil is expanding for operational reasons, not only for novelty or technology appeal.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High financing costs and constrained machinery credit | -0.70% | Center-West, South, and Southeast, where equipment purchases rely heavily on machinery financing. | Short term (≤ 2 years) |

| Bureaucratic loan approval slows fleet renewal | -0.30% | Center-West, South, and Southeast, where replacement purchases depend on subsidized or structured credit programs. | Short term (≤ 2 years) |

| Limited farm connectivity for digital spraying workflows | -0.40% | North, Northeast, and Center-West, where weak connectivity limits adoption of connected spraying systems. | Medium term (2–4 years) |

| Drone compliance and pilot training gaps | -0.20% | North, Northeast, and Center-West, where drone adoption is expanding faster than formal operating standards. | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Financing Costs and Constrained Machinery Credit

Financing conditions remain the most immediate restraint on the agricultural sprayers market in Brazil. Banco Central do Brasil showed the Selic benchmark rate at 14.5% on its public economic dashboard, keeping borrowing costs elevated for capital equipment decisions[4]Source: Central Bank of Brazil (Banco Central do Brasil), “Selic Interest Rate Data,” bcb.gov.br.. At the same time, the federal government launched the 2025/2026 Plano Safra with USD 102.5 billion (BRL 516.2 billion) in support for agribusiness, indicating that credit remains available but is increasingly selective in its allocation. The first 2 months of the 2025/2026 crop year recorded USD 19.7 billion (BRL 99.1 billion) in contracted rural credit, down 1.75% from the same period in the prior cycle, suggesting weaker early momentum in farm financing. High rates do not eliminate demand for spraying, but they do delay upgrades and push many farms toward repairs, used equipment, or outsourced application rather than new machinery. This restraint weighs most on mid-sized buyers, who usually need formal credit but lack the financial flexibility available to the largest farm groups.

Bureaucratic Loan Approval Slows Fleet Renewal

Administrative complexity also slows the conversion of demand into orders in the Brazil agricultural sprayers market. The 2025/2026 Plano Safra broadened compliance rules for agricultural climate risk zoning for operations above USD 39,703.8 (BRL 200,000), adding another layer of documentation to many financed transactions. Ministry data also show a gap between contracted and granted values in early-cycle rural credit, suggesting that approvals and releases do not move at the same pace. That matters for sprayers because purchases are often time-sensitive and tied to seasonal windows, so a delayed decision can mean another year of using older equipment. Slow approvals are especially disruptive for fleet renewal because farmers may postpone premium or self-propelled purchases rather than risk missing agronomic timing. The effect is not a collapse in demand, but a more uneven order flow that reduces visibility for manufacturers and dealers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source of Power: Fuel-Operated Platforms Hold the Largest Base While Battery Formats Advance Faster

Fuel-operated sprayers held 71.5% of the Brazil agricultural sprayers market share in 2025, making them the largest power segment by a wide margin. Their lead reflects the operating needs of broadacre farms in the Center-West and South, where long working hours, larger tanks, and heavier-duty cycles still favor combustion platforms. This installed base has been built over years of soybean and corn mechanization, and it remains closely tied to tractor-mounted and self-propelled field spraying. Manual sprayers still play an active role on smaller holdings, in horticulture, and for localized applications where a low upfront cost matters more than operating speed. Solar-powered formats remain a small niche, mainly where off-grid use and basic field mobility make practical sense.

Battery-operated sprayers are the fastest segment, with a 6.8% CAGR during 2026-2031, although growth is concentrated in handheld and backpack formats rather than large boom systems. This part of the Brazil agricultural sprayers market benefits from lower noise, simpler maintenance, and easier use in tasks where tank size is limited and mobility matters most. Battery models are also gaining acceptance among smaller farms seeking to reduce operator strain and simplify routine spraying. Even so, battery power is unlikely to displace fuel-operated systems in the large-capacity field tier before 2031, as energy density and duty-cycle requirements still favor conventional platforms. The result is a two-speed structure where fuel systems remain the operational backbone while battery formats expand more quickly from a smaller base.

By Product Type: Tractor-Mounted Units Stay Largest while UAV Sprayers Set the Fastest Pace

Tractor-mounted sprayers accounted for 46.8% of the Brazil agricultural sprayers market size in 2025, making them the largest product segment by value. Their position reflects the country’s strong installed tractor base and the need for practical, scalable crop protection across soybean, corn, cotton, and sugarcane fields. These units remain attractive because they balance performance, cost, and compatibility with farms that already own tractors and do not need a separate self-propelled machine. Trailed sprayers also remain relevant for farms that need greater capacity than handheld or mounted systems, but are still cost-sensitive. Self-propelled units occupy a premium tier with higher value per machine, especially in large commercial operations that need long daily coverage and strong field efficiency.

Unmanned aerial vehicle sprayers (UAVs) are the fastest product segment, with a 10.9% CAGR during 2026-2031. The drone base in Brazil has expanded rapidly, confirming that aerial spraying has already moved beyond a pilot stage. In July 2025, the Brazilian Agricultural Research Corporation (Embrapa) released the publication "Use of Agricultural Drones in Brazil: From Research to Practice", consolidating research findings, operational guidelines, and field applications across multiple crops, highlighting the increasing institutional and technical maturity of drone spraying within Brazilian agriculture. SZ DJI Technology Co., Ltd. also unveiled the Agras T100, T70P, and T25P in Brazil in April 2025, which supports the view that product development is shifting quickly toward this segment. Handheld and trailed products will continue to serve specific farm profiles, but the market's growth narrative is increasingly defined by drones rather than by traditional product additions alone.

By Application: Field Crops Remain Largest While Orchards and Vineyards Expand Faster

Field crops represented 50.2% of the Brazil agricultural sprayers market share in 2025, making them the largest application segment. That position is directly linked to Brazil’s scale in soybean, corn, cotton, wheat, and sugarcane production, which sustains demand for agricultural spraying equipment across the country's major farming regions. According to the National Union of the Plant Protection Products Industry, soybeans alone accounted for 55% of the national treated area in 2025, underscoring how closely sprayer demand is tied to row-crop protection cycles. This makes field crops the core demand engine for tank capacity, boom width, and throughput across the Brazil agricultural sprayers market. Greenhouse crops, turf, and gardening stay smaller in value, but they provide a stable outlet for handheld and compact equipment.

Orchards and vineyards are the fastest application segment, with a 6.2% CAGR during 2026-2031. The demand pattern here is different because farms need better canopy targeting, more maneuverability, and equipment that can work on uneven ground or in irregular planting layouts. A 2026 study by researchers from the Federal University of Technology, Paraná, Brazil, found that spray drones used across Brazilian crops, including citrus, improved droplet deposition and access to difficult-to-manage areas, supporting their suitability for orchard conditions. The Southeast remains central to this segment because citrus and coffee production there provide a strong operational case for specialized, automated spraying systems. This means field crops account for the largest value pool, while specialty crops drive technology adoption into areas where precision matters more than raw field coverage.

By Spray Volume Capacity: Low Volume Leads the Installed Base While Ultra-Low-Volume Sprayers Grow Faster

Low-volume sprayers held 48.3% of the market in 2025 and remain the largest segment by spray volume capacity. This reflects the dominant operating model for broadacre crop protection, where tractor-mounted and self-propelled boom sprayers typically work in a low-volume range that balances coverage and application quality. Low-volume use suits soybean, corn, and sugarcane operations well, as these crops require efficient movement across large field areas. High-volume formats still retain a place in older fleets and in denser crop conditions where deeper penetration and heavier liquid loads remain useful. The market, therefore, still leans toward capacity ranges that match conventional field agronomy rather than aerial minimal-volume logic.

Ultra-low-volume sprayers will be the fastest segment, with a 10.2% CAGR during 2026-2031. Their growth is tightly linked to drone adoption because agricultural UAV systems typically work at much lower liters per hectare than conventional ground rigs. SZ DJI Technology Co., Ltd stated in April 2026 that more than 600,000 DJI agricultural drones were operating globally by the end of 2025, and Brazil was one of the markets highlighted for active use across coffee, soybean, corn, sugarcane, and forage grass. Ultra-low-volume growth is also helped by short spray windows in frontier zones, where faster aerial passes can be more practical than slower ground applications. Even so, the segment is growing from a smaller base, so its percentage expansion is stronger than its absolute value movement in the Brazil agricultural sprayers market.

By Technology Level: Conventional Systems Stay Largest While AI-Enabled and Autonomous Models Move the Premium Tier

Conventional sprayers held 52.8% of the market in 2025 and remain the largest technology level by value. Their scale comes from a wide installed base of farms that still prioritize lower purchase cost, familiar maintenance, and straightforward operating logic. This is especially relevant in regions where connectivity, technician access, and data integration are not yet strong enough to justify a premium technology jump. Precision and Global Positioning System (GPS)-guided systems already serve a meaningful middle tier, especially in large fields where boom section control and route guidance deliver clear savings. The Brazil agricultural sprayer industry, therefore, remains broad and mixed, with conventional machines still accounting for most unit volume while more advanced systems expand at the top end.

AI-enabled and autonomous sprayers are anticipated to be the fastest segment, with a 10.5% CAGR during 2026-2031. Stara S.A. Indústria de Implementos Agrícolas Eco Spray line demonstrates how the premium tier is evolving, with real-time weed detection, nozzle-by-nozzle response, and support for both pre-emergent and post-emergent use. This movement is important because it shifts value toward software, sensing, and decision support, rather than relying solely on mechanical performance. Larger commercial farms are still the natural entry point, since they can capture bigger savings from selective application and document that return across wider acreage. For the Brazil agricultural sprayers market, this means the fastest technology growth is coming from features that reduce chemical waste and improve precision rather than from raw horsepower alone.

By Pump Mechanism: Diaphragm Pumps Keep the Largest Position While Centrifugal Pumps Track Drone Expansion

Diaphragm pumps represented 42.9% of the market in 2025, making them the largest pump mechanism segment. Their lead is tied to reliability in handling agrochemical formulations, pressure stability, and field durability in conventional boom sprayers. These qualities fit Brazilian broadacre use well, where machines operate in demanding conditions and need consistent spray performance across long workdays. Piston pumps continue to serve higher-pressure specialty tasks where finer control can be more important than general field versatility. The industry still depends on diaphragm systems as the practical standard across a large share of the installed base.

Centrifugal pumps will be the fastest segment, with a 6.6% CAGR during 2026-2031. Their rise is closely linked to drone spraying, as aerial platforms require lighter, more compact pump systems that can support variable flow and lower payload weight. XAG’s P150 and P60 launch in Brazil in 2025 through CNH Industrial N.V.’s network adds to that installed base, since these drone platforms directly expand the use case for pump designs suited to aerial application. As drone adoption widens across the North, Northeast, and specialty crop zones, centrifugal pump demand should continue to outpace traditional mechanisms. Even so, diaphragm pumps are likely to retain leadership in total value because ground-based field sprayers remain the core of the Brazil agricultural sprayers market through 2031.

Geography Analysis

The Center-West is the largest regional base for the Brazil agricultural sprayers market, supported by its scale in soybeans, corn, and other broadacre crops. Mato Grosso and Rondônia accounted for 33.0% of Brazil’s treated area in 2025, which provides the clearest public indicator of the country’s installed spraying demand concentration. This regional structure favors self-propelled and tractor-mounted equipment, because flat terrain and large fields reward high daily coverage and broad boom use. It also explains why leading multinational and domestic brands remain highly active in this zone, as large farm accounts here drive a disproportionate share of premium machinery demand. Credit conditions matter more in the Center-West than in many other regions because the average equipment ticket is higher and fleet renewal is closely tied to access to financing.

The North and Northeast are the fastest-growing geographies in the Brazil agricultural sprayers market. In these areas, planted area expansion is combining with harder field access, shorter operating windows, and more uneven terrain, which shifts demand toward aerial platforms and flexible service models. The BAMATOPIPA corridor accounted for 18.0% of the treated area in 2025, while the North and Northeast continue to benefit from above-average frontier farm development. These regions are growing faster because they often need access-based solutions first, and that lowers the entry barrier for drones and spraying services compared with large self-propelled purchases.

The Southeast and South remain mature but strategically important parts of the Brazil agricultural sprayers market. The Southeast benefits from citrus and coffee production, where orchard conditions support selective, targeted, and automated spraying systems rather than broadacre-scale operations. The South, by contrast, combines a strong machinery culture, a stable replacement base, and a large population of mid-sized to large commercial farms that continue to invest when economics allow. These 2 regions may not grow as quickly as the frontier areas, but they remain important because they sustain steady value demand, dealer networks, and adoption of newer precision features across the Brazil agricultural sprayers market.

Competitive Landscape

The Brazil agricultural sprayers market is moderately concentrated, with key players in the market including Deere & Company, Maquinas Agricolas Jacto S.A., CNH Industrial N.V., Stara S.A. Indústria de Implementos Agrícolas, and AGCO Corporation. This structure leaves room for a fragmented lower tier of domestic and imported brands, but leadership still rests with companies that combine product breadth, dealer reach, and field service. The competitive split is also becoming more nuanced because domestic manufacturers are proving stronger in selective application and localized adaptation than a simple scale ranking would suggest. The market is influenced not only by the presence of multinational companies but also by suppliers' ability to tailor their equipment to Brazilian crops, field conditions, and operator requirements. Competitive intensity remains elevated because customers are weighing cost, uptime, financing access, and application efficiency simultaneously, rather than choosing on price alone.

Several strategic moves show how leading players are trying to protect or extend their positions in the Brazil agricultural sprayers market. Deere and Company expanded its precision application portfolio in 2026 through the launch of the 400R series in Brazil, reinforcing its focus on integrated spraying and nutrient application systems. XAG Co., Ltd. formally entered Brazil’s aerial spraying channel in 2025 with the launch of new drones through CNH Industrial N.V.’s distribution structure, demonstrating that established dealer networks are also being used to accelerate drone adoption. These moves show that competitive advantage is increasingly tied to precision, access, and application efficiency rather than only to conventional machinery scale.

White-space opportunities remain open even in a market with clear leaders. One of the most visible is the formalized drone service channel, because the large gap between operating and registered agricultural drones suggests that organized suppliers can still capture share as the category regularizes. Another is the mid-farm access model, where leasing, shared fleets, and service-led spraying can bridge the gap between strong agronomic demand and tight equipment credit. The Brazil agricultural sprayer market also has room for more crop-specific solutions in orchards, coffee, and other specialty uses where general-purpose field platforms are less effective. Companies that pair equipment with training, compliance support, agronomic data, and rapid service response are likely to perform better than those that compete only on hardware. This is why competition remains active below the top tier, even though market share remains concentrated among the leading 5 players.

Brazil Agricultural Sprayers Industry Leaders

Deere & Company

Máquinas Agrícolas Jacto S.A.

CNH Industrial N.V.

AGCO Corporation

Stara S.A. Indústria de Implementos Agrícolas

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Deere and Company launched the 400R series sprayer and nutrient distribution line at Casa John Deere 2026 in Ribeirão Preto, adding more than 20 new products focused on integrated precision application for Brazil. The launch included more than 20 new agricultural equipment products focused on precision farming, automation, and integrated spraying efficiency for large-scale soybean, corn, and sugarcane operations.

- January 2026: Deere and Company inaugurated a new industrial plant in Canoas, Rio Grande do Sul, with an investment of USD 7.43 million (BRL 42 million) to manufacture the 1025E self-propelled sprayer, which replaced the legacy PLA brand in Brazil. The expansion strengthened the company’s local sprayer production capacity and supported demand from soybean, corn, wheat, potato, cassava, and horticulture growers across Brazil.

- April 2025: SZ DJI Technology Co., Ltd. unveiled the Agras T100, T70P, and T25P next-generation drone line for the Brazilian market at Agrishow 2025 and released the Agricultural Drone Industry Insight Report 2025/2026, which stated that more than 600,000 DJI agricultural drones were operating globally by the end of 2025 and that drone spot spraying in Brazil can reduce herbicide use by up to 35.0%

Brazil Agricultural Sprayers Market Report Scope

The Brazil agricultural sprayers market covers equipment used to apply crop protection products, liquid nutrients, and related farm inputs across field crops, orchards, vineyards, greenhouse crops, and turf applications in Brazil. The Brazil Agricultural Sprayers Market Report is Segmented by Source of Power (Manual, Battery-Operated, Solar-Powered, and Fuel-Operated), by Product Type (Handheld, Tractor-Mounted, Trailed, Self-Propelled, and Unmanned Aerial Vehicle Sprayers), by Application (Field Crops, Orchards and Vineyards, Greenhouse Crops, and Turf and Gardening), by Spray Volume Capacity (Ultra-Low Volume, Low Volume, and High Volume), by Technology Level (Conventional, Precision and GPS-Guided, and Artificial Intelligence-Enabled and Autonomous), and by Pump Mechanism (Diaphragm, Piston, and Centrifugal Pumps). The Market Forecasts are provided in Value (USD).

| Manual |

| Battery-Operated |

| Solar-Powered |

| Fuel-Operated |

| Handheld |

| Tractor-Mounted |

| Trailed |

| Self-Propelled |

| Unmanned Aerial Vehicle Sprayers |

| Field Crops |

| Orchards and Vineyards |

| Greenhouse Crops |

| Turf and Gardening |

| Ultra-Low Volume |

| Low Volume |

| High Volume |

| Conventional |

| Precision and GPS-Guided |

| Artificial Intelligence-Enabled and Autonomous |

| Diaphragm Pumps |

| Piston Pumps |

| Centrifugal Pumps |

| By Source of Power | Manual |

| Battery-Operated | |

| Solar-Powered | |

| Fuel-Operated | |

| By Product Type | Handheld |

| Tractor-Mounted | |

| Trailed | |

| Self-Propelled | |

| Unmanned Aerial Vehicle Sprayers | |

| By Application | Field Crops |

| Orchards and Vineyards | |

| Greenhouse Crops | |

| Turf and Gardening | |

| By Spray Volume Capacity | Ultra-Low Volume |

| Low Volume | |

| High Volume | |

| By Technology Level | Conventional |

| Precision and GPS-Guided | |

| Artificial Intelligence-Enabled and Autonomous | |

| By Pump Mechanism | Diaphragm Pumps |

| Piston Pumps | |

| Centrifugal Pumps |

Key Questions Answered in the Report

What is the 2026 size of the Brazil agricultural sprayers market and forest for 2031?

The Brazil agricultural sprayers market is valued at USD 546.73 million in 2026 and is forecast to reach USD 695.27 million by 2031.

Which product type leads demand in Brazil?

Tractor-mounted sprayers are the largest product type, with 46.8% share in 2025, because they fit the country’s large installed tractor base and broadacre crop structure.

Why are agricultural drones gaining ground in Brazil?

Drones are gaining ground because they improve access in remote and terrain-constrained fields, and official data showed around 35,000 units in operation by June 2025.

Which crop application drives the most revenue?

Field crops are the largest application segment, with 50.2% share in 2025, supported by Brazil’s scale in soybeans, corn, cotton, wheat, and sugarcane.

What is the main short-term challenge for sprayer purchases?

The biggest short-term challenge is financing pressure, with high benchmark interest rates and slower rural credit momentum delaying fleet renewal decisions.

Which technology is expanding the fastest in Brazil?

AI-enabled and autonomous sprayers are the fastest technology segment, with a 10.5% CAGR during 2026-2031, as growers look for selective spraying and lower chemical waste.

Page last updated on: