Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

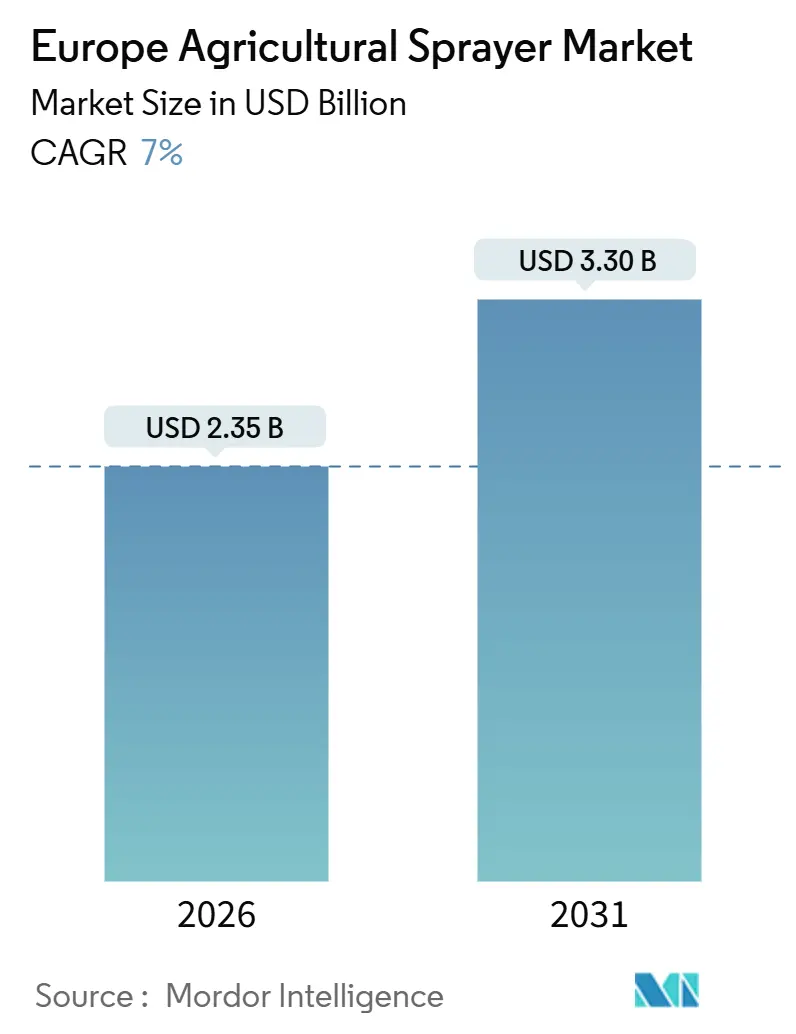

| Market Size (2026) | USD 2.35 Billion |

| Market Size (2031) | USD 3.30 Billion |

| Growth Rate (2026 - 2031) | 7.00% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Agricultural Sprayer Market Analysis by Mordor Intelligence

The Europe agricultural sprayer market size is estimated to be USD 2.35 billion in 2026 and is projected to expand at a 7.0% CAGR, reaching USD 3.30 billion by 2031. Farmers are accelerating equipment upgrades in response to the European Union's Farm-to-Fork pesticide-reduction mandate, rising labor shortages, and increased input costs. Precision spraying, which utilizes machine-vision weed detection, now reduces herbicide volumes by up to 80% while maintaining stable yields. Battery-electric and hybrid platforms are gaining traction because Common Agricultural Policy eco-schemes reimburse as much as 40% of qualifying equipment purchases. At the same time, drone sprayers are opening new revenue pools among vineyard and orchard operators seeking drift-reduction compliance on steep terrain. Competitive intensity remains pronounced as incumbents race to embed artificial-intelligence guidance, carbon-credit data logging, and semi-autonomous operation to secure a share in the fast-modernizing Europe agricultural sprayer market.

Key Report Takeaways

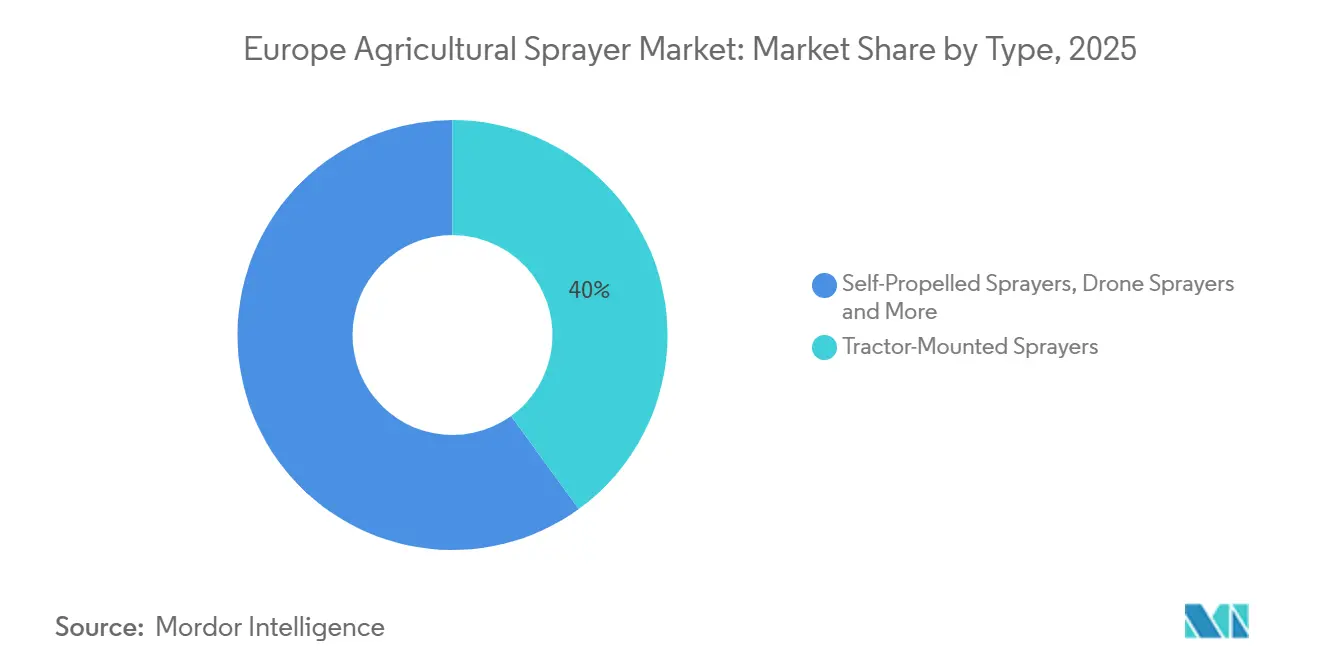

- By type, tractor-mounted sprayers led with a 40% market share in 2025, while drone sprayers are projected to expand at a 22.0% CAGR through 2031.

- By capacity, sprayers in the 500–1,500 liter range held a 43% market share in 2025 and are also projected to be the fastest-growing segment, expanding at an 8.0% CAGR from 2026 to 2031.

- By usage, field sprayers captured a 55% market share in 2025, and aerial sprayers are projected to grow at an 18.5% CAGR through 2031.

- By source of power, fuel-operated units held 46% of the Europe agricultural sprayer market share in 2025, whereas battery-operated units are forecast to record a 12.0% CAGR from 2026 to 2031.

- By technology level, Conventional sprayers captured a 52% share of the market in 2025, while AI-enabled and Autonomous sprayers are expanding at a 15% CAGR between 2026 and 2031.

- By geography, Germany led with 19% of the Europe agricultural sprayer market size in 2025, and Poland is the fastest-growing national market with a 4.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Agricultural Sprayer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| European Union (EU) Farm-to-Fork pesticide-reduction mandates | +1.8% | France, Netherlands, and Denmark | Medium term (2–4 years) |

| Rising Adoption of Global Positioning System (GPS)-Guided Precision Spraying | +1.5% | Germany, France, the United Kingdom, and Belgium | Short term (≤ 2 years) |

| Common Agricultural Policy (CAP) Pillar II grants for battery and hybrid sprayers | +1.2% | All member states, strongest in Germany, Austria, and Finland | Medium term (2–4 years) |

| Labor shortages accelerating autonomous sprayer uptake | +1.0% | Western Europe | Long term (≥ 4 years) |

| Orchard and vineyard drift-reduction retrofits | +0.4% | Spain, Italy, France, and Greece | Short term (≤ 2 years) |

| Carbon-credit programs rewarding variable-rate applications | +0.3% | Netherlands, Denmark, and Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

European Union (EU) Farm-to-Fork pesticide-reduction mandates

The binding 50% cut in pesticide use by 2030 is reshaping capital-spending cycles, as farms must meet compliance requirements to preserve subsidy eligibility [1]Source: European Commission, “Common Agricultural Policy at a Glance,” agriculture.ec.europa.eu. Section control and pulse-width modulation nozzles enable operators to reduce chemical volumes by 20% to 40% without compromising yield. France and the Netherlands now require digital spray logs that can only be supplied by Global Positioning System (GPS)-enabled machines, effectively forcing upgrades on holdings exceeding 50 hectares. Equipment lifecycles have shortened from 10-12 years to 6-8 years in Western Europe as replacement accelerates. The mandate also drives the development of artificial-intelligence spot sprayers, such as the ARA platform, which maps treated weeds for audit trails.

Rising Adoption of Global Positioning System (GPS)-Guided Precision Spraying

Variable-rate application trims input bills by 10% to 30%, translating to EUR 15 to EUR 40 (USD 16.50 to USD 44) per hectare on cereals and oilseeds. More than 60% of German farms larger than 100 hectares already run Global Positioning System (GPS)-enabled sprayers, taking advantage of high-accuracy correction signals. Three- to four-year payback periods improve further as carbon-credit programs reimburse documented reductions [2]Source: Climate Farmers, “Carbon Credit Programs,” climatefarmers.org. Manufacturers are cascading the feature set downmarket; mid-tier trailed sprayers now bundle precision kits below EUR 1 million (USD 1.1 million).

Common Agricultural Policy (CAP) Pillar II Grants for Battery and Hybrid Sprayers

Eco-schemes reimburse up to 40% of low-emission sprayer costs, capping out at EUR 80,000 (USD 88,000) in Austria, Finland, and Germany. Battery-electric sprayers cut diesel exhaust and lower noise by 70%, an advantage for peri-urban and organic farms [3]Source: European Environment Agency, “Rural Infrastructure and Energy,” eea.europa.eu. Hardi’s Alpha Evo series offers 6-8 hour runtimes and 90-minute fast charging, aligning with vineyard duty cycles. Eastern Europe still lags because fewer than 40% of farms hold three-phase power connections, so hybrid architectures that switch between diesel and electric fill the gap.

Labor Shortages Accelerating Autonomous Sprayer Uptake

Farm operator age is climbing, with more than 30% of German, French, and Italian farmers being 65 years or older. Autonomous sprayers run day and night and let one operator supervise multiple units, halving labor needs on large estates. Germany’s 2024 Road Traffic Act amendment now allows driverless vehicles on private land and designated rural routes. Smaller robotic sprayers such as Ecorobotix’s ARA reduce manual weeding costs by 70%, unlocking adoption in organic transition fields.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of advanced sprayers | −0.8% | Spain, Italy, Poland, Romania, and Bulgaria | Short term (≤ 2 years) |

| Fragmented European Union (EU) drone-flight regulations | −0.5% | All member states, most acute in Germany, France, and Italy | Medium term (2–4 years) |

| Limited rural charging infrastructure for battery units | −0.3% | Poland, Romania, Bulgaria, and Hungary | Medium term (2–4 years) |

| Shortage of certified calibration technicians | −0.2% | Spain, Poland, and Romania | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced Sprayers

Self-propelled precision sprayers with GPS, section control, and variable-rate technology cost EUR 2 million to EUR 3.5 million (USD 2.2 million to USD 3.85 million), a level unaffordable for most farms under 50 hectares. Credit approval rates are 20% lower in Southern and Eastern Europe than in Germany and France, limiting access to financing. Shared-equipment cooperatives reduce investment barriers yet also curb direct sales. Trailed sprayers priced below EUR 50,000 (USD 55,000) dominate the volume but lack the features necessary for forthcoming regulatory audits, thereby widening the technology gap.

Fragmented European Union (EU) drone-flight regulations

Despite a 2024 European Union Aviation Safety Agency framework, altitude limits differ: Germany caps at 25 meters, France at 50 meters, and Italy imposes tight visual-line-of-sight requirements. Pilot licensing reciprocity remains incomplete, forcing operators to sit multiple exams. Spain’s no-fly habitat zones exclude 30% of farmland from drone treatments, constraining contractors. Manufacturers defer pan-European rollouts until harmonization improves, tempering the expected 18.5% drone-sprayer growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Drone-Based Platforms Outpace Traditional Formats

Tractor-mounted sprayers remained the leading format, accounting for 40% of the Europe agricultural sprayer market share in 2025, due to their compatibility with existing tractor fleets and lower upfront costs compared to self-propelled rigs. Precision upgrades are propelling these units forward; factory-fit GPS guidance and section control on models priced below EUR 1 million (USD 1.1 million) now enable mid-sized farms to meet Farm-to-Fork digital-logging requirements. Drone sprayers form a smaller base today but represent the fastest-growing type, projected to register a 22.0% CAGR between 2026 and 2031 as vineyards and orchards seek drift control and labor savings. Their capacity to work on steep slopes, over waterlogged soils, and within narrow rows is widening adoption across specialty-crop belts.

Self-propelled machines held a prominent share in 2025, dominated by large estates and contractors that value higher field speeds and 24-hour autonomy to justify investments of EUR 2 million to EUR 3.5 million (USD 2.2 million to USD 3.85 million). Handheld and backpack sprayers accounted for an 18% share, and they are transitioning to battery power with electronic pressure regulation to deliver a consistent droplet size, particularly for greenhouse and high-value vegetable growers. Trailed sprayers made up the remaining limited share, providing an economical entry point for farms in Southern and Eastern Europe where retrofit kits priced EUR 5 thousand to EUR 15 thousand (USD 5.5 thousand to USD 16.5 thousand) add basic precision functions. Together, these formats illustrate a spectrum of cost, capacity, and compliance trade-offs that producers balance as regulations tighten and labor remains scarce.

By Capacity: Mid-Range Tanks Dominate Mixed Farms

Sprayers in the 500-liter to 1,500-liter band captured 43% of the Europe agricultural sprayer market size in 2025, the largest slice of demand, because they balance productivity with maneuverability on the continent’s patchwork of mixed farms. This same band is also forecast to be the fastest-growing, advancing at an 8.0% CAGR from 2026 to 2031 as cooperative ownership models and retrofit precision kits make the format affordable for mid-sized operators. Manufacturers continue to roll out factory-fit Global Positioning System (GPS) and section-control packages on these units, enabling growers to meet Farm-to-Fork digital-logging requirements without upgrading to more expensive self-propelled rigs. Subsidy eligibility for battery-electric versions further boosts uptake, especially among vineyards and peri-urban holdings that need low-noise, low-emission equipment.

Units below 500 liters held a significant share in 2025 and remain popular in orchards, greenhouses, and steep vineyards where compact footprints prevent soil compaction and ease canopy access. Many of these compact sprayers are transitioning to battery propulsion with electronic pressure regulation, which delivers a steady droplet size during short, repetitive spray cycles. Large-capacity rigs above 1,500 liters accounted for a prominent share, dominated by contractors and cereal growers who value fewer refill stops across expansive fields. Hybrid diesel-electric drivetrains and autonomous steering are now being added to these high-volume machines, yet higher acquisition costs and tightening axle-weight rules temper their growth relative to the mid-range category.

By Usage: Aerial Sprayers Surge in Specialty Crops

Field sprayers led the Europe agricultural sprayer market with a 55% share in 2025, a position secured by the region’s extensive cereal, oilseed, and sugar-beet acreage that favors 36-meter to 42-meter boom widths for fast ground coverage. Their dominance is reinforced by precision upgrades, such as machine-vision weed detection, which reduces herbicide use by up to 80% while maintaining high field capacity. Aerial sprayers, although only a relatively small slice of revenue, represent the fastest-growing usage segment and are forecast to register an 18.5% CAGR from 2026 to 2031 as vineyards and orchards adopt aerial platforms for drift control on steep terrain. Lower labor needs and the ability to fly over waterlogged or compact-sensitive soils further strengthen the adoption case for drones across specialty-crop belts.

Orchard and vineyard ground sprayers accounted for a prominent share in 2025, relying on axial-fan and tower designs to penetrate dense canopies while meeting newly expanded 20-meter buffer-zone rules in Spain and Italy. Garden and greenhouse units held a decent share and are steadily shifting toward battery-powered backpacks with electronic pressure regulation, which deliver a constant droplet size inside protected environments. Drone technology is now moving beyond vineyards into spot-treating headland weeds in cereal and oilseed fields, although fragmented national flight rules still hinder cross-border contractor deployment. Together, these remaining segments illustrate how specialized operating conditions and regulatory nuances shape equipment preferences across Europe’s diverse production landscape.

By Source of Power: Battery Units Gain Despite Diesel Dominance

Fuel-operated sprayers captured 46% of the Europe agricultural sprayer market in 2025, anchored by compatibility with widespread tractor power-take-off systems and legacy service networks. Battery units are forecast to post a 12.0% CAGR through 2031, driven by eco-schemes that reimburse 40% of costs and the need for vineyard operators to use quieter, emission-free machinery in residential zones. Manual backpack sprayers held a prominent share but continue sliding as labor costs escalate and ergonomic directives tighten. Solar-powered rigs remain a niche market, constrained by the limited energy density that caps tank volumes at under 200 liters.

Three-phase charging availability, still below 40% in Eastern Europe, limits battery horsepower during critical spray windows. Solar-powered carports bridge part of the gap but extend payback timelines. Manual units persist in greenhouses, yet battery backpacks with electronic pressure control are starting to displace pump-action models. Hybrid diesel-electric sprayers that switch to electric mode on headlands qualify for partial subsidies, while maintaining diesel range for broadacre coverage, thereby reinforcing their appeal during the transition phase.

By Technology Level: Autonomous Systems Accelerate Upgrade Cycle

Conventional sprayers remained the largest cohort with 52% of the Europe agricultural sprayer market share in 2025, favored by small and mid-sized farms that cannot yet justify premium electronics. The fastest-growing tier is the artificial-intelligence and autonomous category, which is projected to advance at a 15.0% CAGR from 2026 to 2031 as labor shortages push large estates toward round-the-clock, driverless operation. Early adopters report 40% labor savings and 95% spot-spray accuracy, making payback achievable within three seasons on high-input crops. National rules that now permit driverless equipment on private farmland in Germany and the Netherlands further accelerate the uptake by removing regulatory uncertainty.

Precision and GPS-guided sprayers held a prominent share in 2025 and are forecast to grow at a solid CAGR as Farm-to-Fork compliance requires digital application logs and input-reduction proof. Retrofit kits costing EUR 5,000 to EUR 15,000 (USD 5,500 to USD 16,500) are enabling incremental upgrades on legacy booms, especially in Spain, Italy, and Eastern Europe, where financing is tight. Manufacturers now bundle satellite correction services and three-year agronomic software subscriptions, which improve return on investment and lock growers into proprietary ecosystems. Together, these technology tiers illustrate a stepwise modernization path, with precision systems serving as the bridge between basic hardware and fully autonomous, vision-guided platforms.

Geography Analysis

Germany led the regional landscape with 19% market share in 2025, a position anchored by larger average farm sizes, dense correction-signal coverage, and favorable rules that now allow driverless equipment on private land. Precision adoption already tops 60% of holdings above 100 hectares, which keeps replacement cycles brisk and parts demand high. Poland is the fastest-growing country and is projected to advance at a 4.6% CAGR from 2026 to 2031 as farm consolidation improves credit access and European Union grants subsidize precision upgrades. The divergent growth rates of these two markets highlight how structural scale and funding availability influence the pace of technology adoption across the continent.

France sits just behind Germany and combines large cereal estates in the Paris Basin with high-value vineyards that are early adopters of low-drift nozzles and drone spraying for buffer-zone compliance. The United Kingdom is steering post-Brexit farm payments toward measurable environmental outcomes, which positions precision sprayers as a key compliance tool. Spain and Italy continue to retrofit orchard and vineyard fleets with tunnel sprayers and aerial platforms that navigate steep terraces while meeting expanded 20-meter buffer rules. Scandinavia, the Netherlands, and Austria focus on battery-electric models to reduce noise and emissions near peri-urban zones where farms coexist with residential areas.

Looking ahead, Western Europe will continue to push the frontier in autonomy and artificial-intelligence weed detection, aided by well-developed telematics and service infrastructures. Central and Eastern member states are expected to accelerate equipment replacements as rural grid upgrades and shared-ownership cooperatives lower the barriers to battery and precision adoption. Harmonization of drone-flight rules and the expansion of carbon-credit programs should lift aerial-sprayer demand across multiple climates, narrowing the technology gap between early and late adopters. Collectively, these regional dynamics will sustain a steady upgrade cycle that supports the 7.0% CAGR projected for the overall Europe agricultural sprayer market through 2031.

Regulatory Landscape

Agricultural sprayers in Europe operate under the EU framework for the sustainable use of pesticides, including Directive 2009/128/EC requirements that member states implement for regular inspection of pesticide application equipment in use. Compliance is commonly demonstrated through harmonized inspection and performance standards (for example, the ISO 16122 series referenced by national inspection schemes), which pushes fleets toward calibrated, drift-aware hardware and GPS-enabled documentation where digital spray logs are required.

On machinery compliance, manufacturers are aligning development and conformity processes with the EU Machinery Regulation (EU) 2023/1230, which applies from January 2027 and tightens market-access expectations for agricultural machinery. In March 2026, a European Commission implementing act (Commission Implementing Decision (EU) 2026/546) updated the set of harmonized standards supporting essential safety and environmental requirements for agricultural and forestry machinery, reinforcing standards-led conformity for agricultural and forestry equipment placed on the EU market.

Competitive Landscape

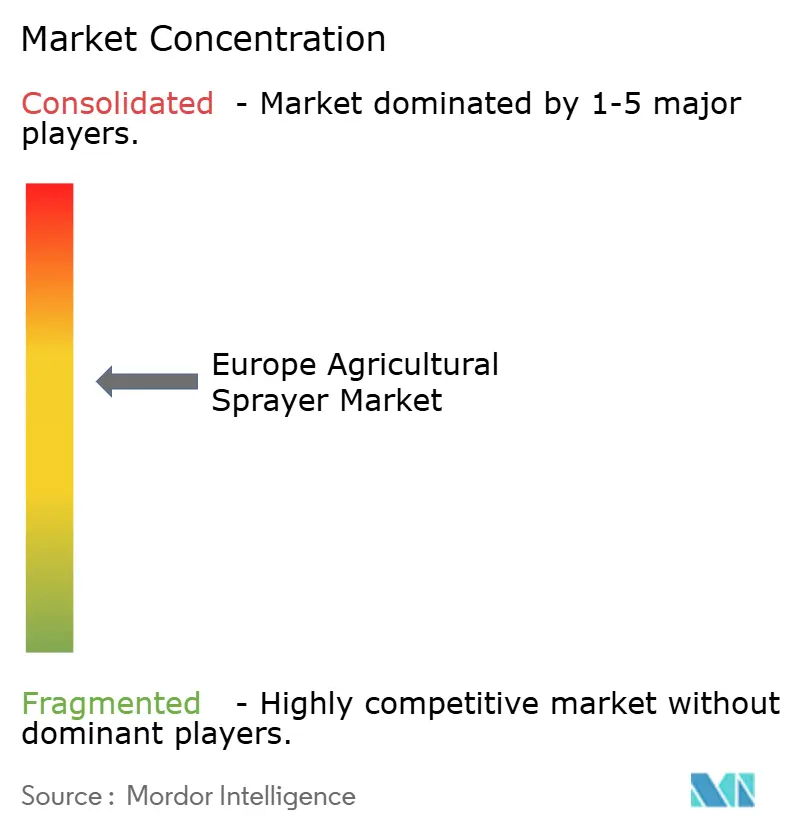

Exel Industries and Deere and Company set the competitive pace in Europe, backed by multi-brand portfolios and deep dealer networks that provide sub-24-hour parts support during critical spray windows. Both offer factory-integrated machine-vision systems that cut herbicide volumes by up to 80%, satisfying Farm-to-Fork compliance and lowering operating costs. Their ongoing investments in battery powertrains and over-the-air software updates anchor brand loyalty among large estates and contractors. Together with three other leading suppliers, the top five firms control the majority of regional revenue, signaling moderate concentration in the Europe agricultural sprayer market.

Kuhn Group, CNH Industrial, and Amazonen-Werke round out the top tier and use precision software ecosystems to differentiate in price-sensitive districts. Kuhn is adding hybrid diesel-electric drivetrains that qualify for eco-scheme subsidies without sacrificing field range. CNH Industrial leverages the Raven Autonomy platform so one operator can manage multiple sprayers from a single console, cutting labor needs by 40% on large farms. Amazonen-Werke complements high-capacity booms with retrofit section-control kits that help mixed-crop growers meet digital-log mandates at lower upfront cost.

Across the board, research budgets are being allocated to artificial-intelligence weed detection, autonomous navigation, and subscription-based agronomic decision support. Patents filed between 2024 and 2025 span drift-reduction nozzles, battery-management software, and machine-learning algorithms, demonstrating a race to lock in proprietary advantages. Suppliers also expand through strategic partnerships with carbon-credit platforms and rural lenders that bundle equipment financing with sustainability incentives. These initiatives are anticipated to widen technology adoption and sustain the market’s 7.0% compound annual growth rate through 2031.

Europe Agricultural Sprayer Industry Leaders

Exel Industries SA

Deere and Company

Kuhn Group (Bucher Industries AG)

CNH Industrial N.V.

Amazonen-Werke H. Dreyer GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Precision retrofits and in-orchard automation remain an actionable gap, since many farms need auditability and input-reduction outcomes without replacing entire fleets. Funding and validation activity supports this direction: in April 2026, Dutch startup BBLeap raised EUR 5 million to scale its modular pulse-width modulation nozzle control approach, positioning retrofit-ready precision components as a faster route to chemical-use reduction on installed sprayer bases. This complements the observed shift toward GPS-guided spraying and digital spray logging in markets such as France and the Netherlands.

Specialty crops also offer a clear runway for vision-guided and canopy-adaptive spraying, where tree geometry and drift constraints shape equipment choice. In January 2026, Munckhof reported completion of field research for its Vision Spray technique in fruit growing, demonstrating automated adjustment of application based on canopy structure. In parallel R&D across Europe focuses on aerial and ultra-low-volume approaches: the FAUVE project (Rovensa Next with Universite de Technologie de Compiegne) is scheduled to conclude in July 2026 with an emphasis on drone and ultra-low-volume spraying to reduce drift, aligning with drift-reduction compliance needs in vineyards and orchards and the requirement to document sustainability outcomes.

Recent Industry Developments

- June 2026: Deere and Company announced major updates to its 500R self-propelled sprayer lineup for model year 2027, including a new 6,000 L flagship configuration and boom widths reaching 42 m. The updates target higher daily output within tightening spray windows while keeping factory-integrated precision capabilities central to compliance-driven upgrades across large arable operations.

- June 2026: Kuhn debuted the Karan trailed sprayer range at Cereals 2026 in the UK, with tank capacities spanning 4,500 L to 8,000 L and boom widths from 18 m to 45 m. Positioning a high-capacity trailed platform broadens options for farms and contractors seeking near self-propelled productivity without moving into the highest price tiers.

- August 2025: Deere and Company completed its full acquisition of autonomous sprayer manufacturer GUSS Automation, while keeping the brand and manufacturing operations in Kingsburg, California. The transaction strengthens Deere’s autonomy stack for specialty-crop spraying and supports solutions aimed at labor constraints and repeatable, data-rich application workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from agricultural sprayer equipment sold and used across Europe to apply crop-protection products, fertilizers, and similar liquids on farms and controlled growing environments.

Scope exclusions: Excludes on-farm chemical inputs themselves, spare parts and consumables sold separately, and standalone contract spraying service fees when not bundled with equipment sales.

Segmentation Overview

- By Source of Power

- Manual

- Battery-Operated

- Fuel-Operated

- Solar-Powered

- By Usage

- Field Sprayers

- Orchard/Vineyard Sprayers

- Garden and Greenhouse Sprayers

- Aerial Sprayers

- By Capacity

- Less than 500 L

- 500 to 1,500 L

- More than 1,500 L

- By Type

- Self-Propelled Sprayers

- Tractor-Mounted Sprayers

- Trailed / Pull-Type Sprayers

- Handheld and Backpack Sprayers

- Drone Sprayers

- By Technology Level

- Conventional

- Precision and GPS-Guided

- AI-Enabled and Autonomous

- Geography

- Germany

- France

- United Kingdom

- Spain

- Italy

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure of the market and to ground key assumptions in public data series. We relied on agriculture and equipment context sources such as Eurostat farm structure and crop area statistics, FAOSTAT crop and input indicators, European Commission CAP and pesticide policy publications, and ECHA guidance on active substances and use restrictions. Trade and production signals were also reviewed through Eurostat COMEXT style import and export tables and customs summaries where available.

To connect demand with real purchasing behavior, we screened company annual reports, investor presentations, product catalogs, and credible press coverage around new sprayer launches and upgrades. In a few cases, paid subscriptions for company financials and intelligence and for shipment-level import and export data helped verify ownership structures and cross-border equipment flows. These examples are not exhaustive, and many other public sources were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what sprayers are actually bought, how replacement cycles are changing, and how pricing moves with technology features. We spoke with a mix of equipment manufacturers, dealers and distributors, large farms and cooperatives, and crop-advisory voices across major European markets. Follow-up questions were used to close gaps on technology adoption, compliance-driven upgrades, and country-to-country differences in demand patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 12% | |

| Mid tier: 43% | Functional/Unit leaders: 29% | |

| Smaller Players: 22% | Managers: 59% |

Market-Sizing & Forecasting

The core model starts from a top-down demand pool that is rebuilt from country-level cropped area, crop mix, and sprayer intensity, and then linked to typical replacement timing and new purchase triggers. To keep the totals realistic, results are corroborated with selective bottom-up checks such as dealer channel checks, sampled average selling prices by sprayer class, and a light roll-up of visible supplier revenue exposure to Europe.

Inputs used in the sizing and forecast include, in an illustrative way, arable and permanent crop area by country, the split of field versus orchard and vineyard use, tank capacity preferences that steer unit values, the share of self-propelled versus trailed and mounted formats, and the adoption pace of precision features like GPS guidance and variable-rate capability. We also tracked policy pressure points that influence upgrades, including drift-reduction requirements and pesticide use reduction targets, which tend to pull demand toward newer, better-controlled application systems.

Forecasts were built using scenario analysis supported by expert views on subsidy continuity, farm profitability, and labor availability, which were then translated into penetration and replacement adjustments. Where bottom-up evidence was thin for smaller countries, we used calibrated proxies based on crop area and mechanization similarity, then rechecked the outputs against regional trade direction and pricing trends.

Data Validation & Update Cycle

Validation was done by comparing the modeled values against independent signals like equipment shipment and trade direction, visible pricing bands by sprayer category, and country-level farming activity indicators. Any large jumps were reviewed for unit mix shifts, currency timing, and one-off policy effects before numbers were signed off, and we re-contacted sources when an assumption moved the market materially.

Each report is refreshed on an annual cycle, and interim updates are made when material events occur, such as a major regulatory change or a step-change in technology adoption. Before delivery, a final analyst pass is completed so clients receive the latest updated view with consistent definitions across years.

Mordor Intelligence's Europe Agricultural Sprayer Market Estimate Compared With Other Published Estimates

Published values for this market can look far apart even when they talk about the same region, because the math changes with what is counted as a sprayer, which years are used as the base, and whether the estimate leans more on unit demand or on revenue proxies.

The main gap comes from scope and base-year alignment, where Mordor Intelligence counts Europe agricultural sprayer equipment across the full set of major sprayer formats (including handheld and drone sprayers) and anchors the current market value to the 2026 sizing year, while other sources often start from earlier base years and may emphasize only a narrower set of categories or distribution channels.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.35 B (2026) | |

| Global Consultancy A | USD 1.93 B (2023) | Uses an earlier base year and a different forecast window, and the published scope appears more dependent on selected type groupings and channel tracking, which can understate newer technology-driven upgrades in later years. |

| Regional Consultancy B | USD 4.75 B (2022) | Starts from a different base year and may include broader categories and technology groupings that can pull in adjacent equipment definitions, which increases totals when compared with a tighter equipment-only view. |

The table shows that most differences are explained by year choice and how wide the equipment definition is kept when revenues are added up. By keeping inputs tied to farm area, format mix, and technology adoption, the final estimate stays traceable to practical demand drivers and can be repeated as new data points emerge.

Key Questions Answered in the Report

How large is the Europe agricultural sprayer market today?

The market generated USD 2.35 billion in 2026 and is on track to reach USD 3.30 billion by 2031.

What is the projected growth rate for Europe agricultural sprayers?

Revenue is projected to rise at a 7.0% compound annual growth rate between 2026 and 2031.

Which power source is expanding fastest in European sprayers?

Battery-operated units are advancing at a 12.0% CAGR due to eco-scheme subsidies and low-emission advantages.

What policy is shaping equipment investment decisions?

The European Union's Farm-to-Fork Strategy mandates a 50% reduction in pesticide use by 2030, compelling farms to adopt precision spraying technologies.

Page last updated on: