Southeast Asia Agricultural Tractors Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

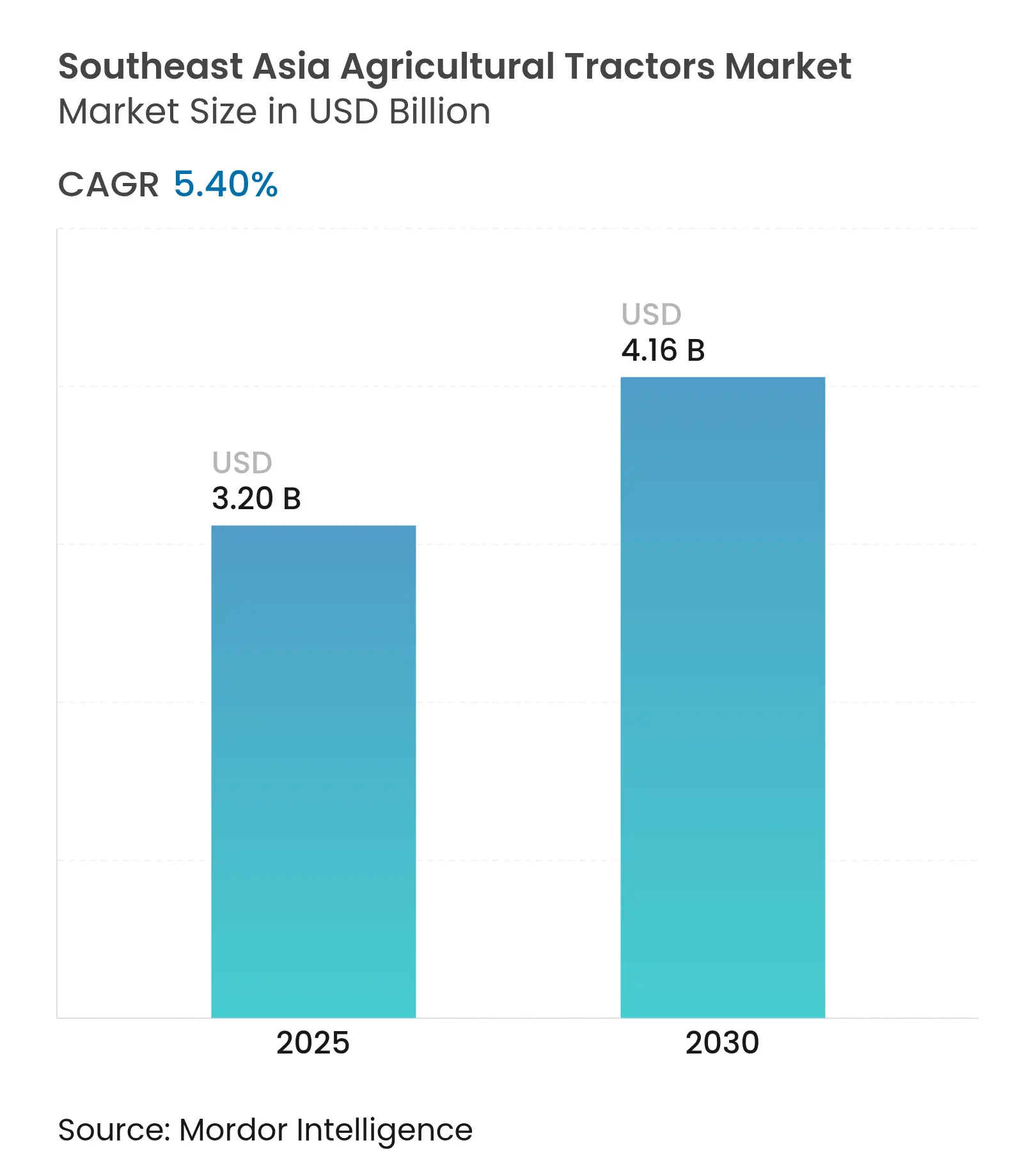

| Market Size (2025) | USD 3.20 Billion |

| Market Size (2030) | USD 4.16 Billion |

| Growth Rate (2025 - 2030) | 5.40 % CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Southeast Asia Agricultural Tractors Market Analysis by Mordor Intelligence

The Southeast Asia agricultural tractor market has a current market size of USD 3.2 billion in 2025 and is forecast to reach USD 4.16 billion by 2030, advancing at a 5.4% CAGR over the period. Growth is fueled by accelerating mechanization in rice and sugarcane production, persistent labor shortages, and widening precision-farming incentives across the Association of Southeast Asian Nations (ASEAN). Demand concentrates in Thailand and Vietnam, where La Niña-linked irrigation spending supports sales of moisture-tolerant orchard and utility models. Electrification in the 20-75 HP class is rising on the back of ASEAN carbon-credit schemes, while rural leasing platforms and micro-lending programs are lowering ownership barriers for smallholders. Market concentration is intensifying through strategic partnerships, exemplified by AGCO's February 2025 alliance with SDF to strengthen its position in the low-mid horsepower segment.

Key Report Takeaways

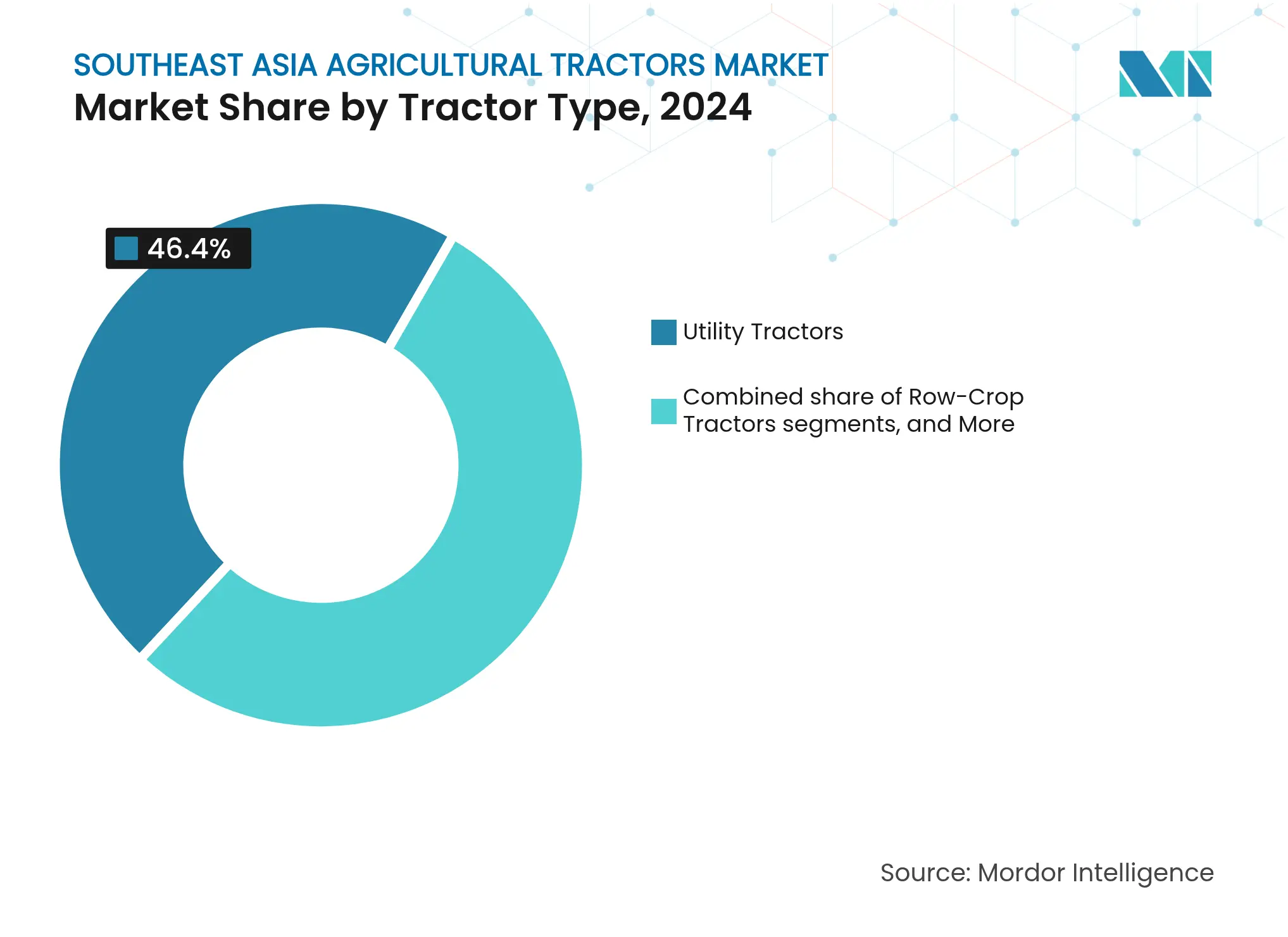

- By tractor type, Utility tractors held 46.40% of the Southeast Asia agricultural tractor market share in 2024 and remain the revenue leader through 2030. Orchard Tractors are expanding at a 11.20% CAGR to 2030, the fastest rate among all types.

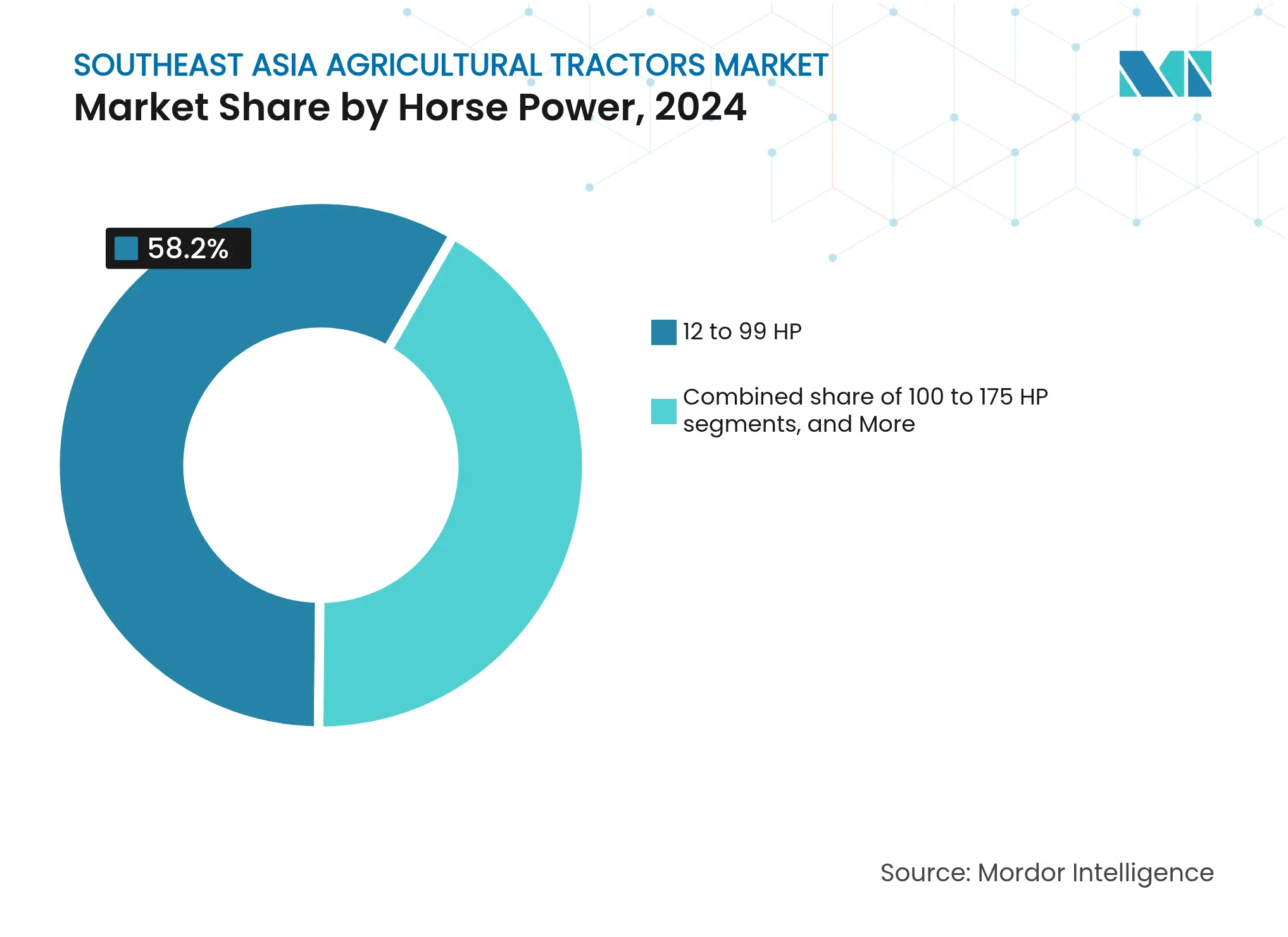

- By horsepower, the 12- to 99-hp range accounted for 58.20% of the Southeast Asia agricultural tractor market size in 2024 and continues to dominate demand. Tractors in the 100 to 175 HP band are projected to post a 10.50% CAGR, the quickest horsepower-based growth through 2030.

- By geography, Indonesia held 34.2% of the Southeast Asia agricultural tractor market in 2025. Vietnam is projected to record the fastest expansion at an 11.4% CAGR from 2025 to 2030.

Southeast Asia Agricultural Tractors Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising shortage of skilled farm labor

Rising shortage of skilled farm labor

| +1.8% | Thailand, Vietnam, Malaysia, and Indonesia | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.8%

|

Geographic Relevance

:

Thailand, Vietnam, Malaysia, and Indonesia

|

Impact Timeline

:

Medium term (2-4 years)

|

High adoption of precision-farming

subsidies High adoption of precision-farming

subsidies | +1.2% | Thailand, Vietnam, Singapore, and Malaysia | Short term (≤ 2 years) | |||

Electrification of 20-75 HP tractors for rice and

sugarcane farms

Electrification of 20-75 HP tractors for rice and

sugarcane farms

| +0.9% | Thailand, Vietnam, Philippines, and Indonesia | Long term (≥ 4 years) | |||

Expansion of rural leasing and micro-lending platforms

Expansion of rural leasing and micro-lending platforms

| +0.7% | Indonesia, Philippines, Cambodia, and Myanmar | Medium term (2-4 years) | |||

La Nina-linked irrigation investments

La Nina-linked irrigation investments

| +0.6% | Vietnam, Thailand, the Philippines, and Cambodia | Short term (≤ 2 years) | |||

ASEAN-wide carbon-credit schemes rewarding low-tillage

tractor use

ASEAN-wide carbon-credit schemes rewarding low-tillage

tractor use

| +0.4% | Global, Asia Pacific coverage | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Shortage of Skilled Farm Labor

Labor scarcity has emerged as the primary catalyst for tractor adoption across Southeast Asia, with traditional agricultural workers increasingly migrating to urban manufacturing and service sectors. Myanmar exemplifies this trend, where mechanization service providers have rapidly expanded to address acute labor shortages during peak cropping periods, fundamentally altering the economics of smallholder farming. This labor-driven mechanization creates a self-reinforcing cycle where increased productivity enables farmers to afford more sophisticated equipment, accelerating the transition from manual to mechanized operations. The demographic shift toward non-farm employment ensures sustained demand for labor-saving technologies, making this driver particularly resilient to economic fluctuations.

High Adoption of Precision-Farming Subsidies

ASEAN governments are outspending earlier plans on smart-farm incentives. Singapore’s Agri-food Cluster Transformation Fund reimburses a share of capital outlays for approved equipment until December 2025[1]Source: Singapore Food Agency, “Agri-Food Cluster Transformation Fund,” sfa.gov.sg. The Philippines' digital agriculture transformation emphasizes integrating digital solutions into farming practices, with recommendations for centralized platforms and public-private partnerships to enhance accessibility. These subsidy programs are creating market distortions that favor technologically advanced tractors over basic models, fundamentally altering purchasing patterns and accelerating the adoption timeline for precision farming equipment.

Electrification of 20-75 HP Tractors for Rice and Sugarcane Farms

The electrification of mid-range tractors is gaining momentum as governments prioritize carbon reduction and farmers seek to reduce diesel dependency in rice and sugarcane cultivation. Thailand's climate-smart agriculture strategy targets net-zero emissions by 2065, with biogas energy and clean technology identified as key indicators for policy formulation, creating substantial incentives for electric tractor adoption. Consistent torque, lower noise, and eligibility for carbon credits make electric powertrains attractive to smallholders cultivating rice paddies and sugarcane blocks, positioning the segment for long-term Southeast Asia agricultural tractor market growth.

Expansion of Rural Leasing and Micro-Lending Platforms

Indonesia’s People’s Business Credit program reached 100.4% of lending targets between 2020 and 2022, supporting an average of 2.27 million borrowers annually[2]Source: Asian Productivity Organization, “People’s Business Credit Program Supporting Agricultural Development in Indonesia,” ap.fftc.org.tw. Digital loan origination shortens approval cycles and broadens reach into remote districts, while agribusiness microfinance institutions layer technical guidance onto credit delivery. Similar schemes in Myanmar and the Philippines are widening eligibility, sustaining demand in the Southeast Asia agricultural tractor industry even when farm cash flows are volatile. The digitization of financial flows enables more efficient risk assessment and loan processing, reducing transaction costs and expanding access to previously underserved farming communities.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Persistent land-holding fragmentation

Persistent land-holding fragmentation

| -1.1% | Indonesia, Philippines, Vietnam, and Myanmar | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

-1.1%

|

Geographic Relevance

:Indonesia, Philippines, Vietnam, and Myanmar |

Impact Timeline

:

Long term (≥ 4 years)

|

Proliferation of custom-hiring centers dampening ownership

Proliferation of custom-hiring centers dampening ownership

| -0.8% | Indonesia, Myanmar, Cambodia, and Philippines | Medium term (2-4 years) | |||

High import tariffs on above 100 HP tractors

High import tariffs on above 100 HP tractors

| -0.6% | Thailand, Malaysia, and Indonesia | Short term (≤ 2 years) | |||

Limited after-sales service network

Limited after-sales service network

| -0.4% | Cambodia, Myanmar, and Rest of Southeast Asia | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Persistent Land-Holding Fragmentation

Average farm sizes across ASEAN remain too small to ensure efficient use of large equipment. The Asian Development Bank highlights that sub-two-hectare plots prevail, limiting economies of scale for mechanization[3]Source: Futoshi Yamauchi, “Changing Farm Size and Agricultural Productivity in Asia,” Asian Development Bank, adb.org. In Indonesia and the Philippines, even generous machinery grants achieve mixed success because individual owners cannot secure enough acreage to maximize asset utilization, restraining the premium end of the Southeast Asia agricultural tractor market. However, the fundamental economics of fragmented holdings limit the return on investment for high-capacity equipment, constraining market growth in premium segments and perpetuating demand for smaller, less efficient machinery.

Proliferation of Custom-Hiring Centers Dampening Ownership

Rental services provide affordable access but divert sales away from individual farmers. Indonesia’s government-funded machinery pools often struggle with maintenance but still satisfy seasonal demand peaks, curbing direct purchases. While custom hiring enables smallholders to access advanced machinery without ownership commitments, it fundamentally alters market dynamics by concentrating equipment purchases among service providers rather than individual farmers. This shift reduces the total addressable market for manufacturers while creating demand for higher-utilization, more durable equipment designed for commercial service applications.

Segment Analysis

By Type: Utility Tractors Anchor Multi-Purpose Demand

Utility tractors captured 46.40 of % Southeast Asia agricultural tractor market share in 2024, reflecting their ability to handle tillage, hauling, and spraying on mixed-crop farms. Orchard Tractor variants are surging at a 11.20% CAGR as subsidy programs narrow the cost gap. Manufacturers adopt modular chassis that accommodate a broad range of implements, helping smallholders manage rice, sugarcane, and horticulture tasks with a single platform. Orchard and row-crop tractors serve specialized niches, fruit groves in Malaysia and precision corn rows in Thailand, yet lack the volume to threaten utility dominance. Government carbon incentives continue to support utility models with power ratings suitable for conservation tillage practices, maintaining the largest share of the Southeast Asia agricultural tractor market size through 2030.

Row-crop tractors experience consistent replacement demand due to specific requirements for precise row spacing and adequate ground clearance, which necessitate specialized equipment. Orchard tractors address narrow alleys in fruit estates, and AGCO’s 2025 upgrades emphasize operator comfort and telematics. Segment competition hinges on fuel efficiency and attachment compatibility, prompting manufacturers to integrate IoT diagnostics for remote maintenance. During the forecast period, utility platforms are projected to maintain higher sales compared to specialized alternatives, as the majority of ASEAN farms remain diversified.

Note: Segment shares of all individual segments available upon report purchase

By Horsepower: Mid-Range Units Mirror Farm-Scale Reality

Tractors rated 12-99 HP controlled 58.20% Southeast Asia agricultural tractor market size in 2024, as average plot sizes seldom exceed a few hectares. These machines deliver adequate draft power for rice paddies while remaining price-accessible. The introduction of battery-electric drivetrains in the 20-75 HP band aligns with micro-lending criteria and carbon-credit frameworks, further pushing mid-range adoption.

Demand for 100-175 HP machines is accelerating at a 10.50% CAGR because plantation consolidation and custom hiring centers want higher throughput per machine. Above 175 HP units still face tariff and support hurdles, but may gain traction in palm and sugar estates as import duties ease. Sub-12 HP walk-behind and compact tractors fill greenhouse and urban-farm niches in Singapore but remain a fractional market share. Across horsepower bands, connectivity and precision-capable hydraulics are becoming standard, reinforcing brand differentiation and boosting recurring revenue from software subscriptions.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Indonesia held 34.2% of the Southeast Asia agricultural tractor market in 2025. Thailand remains the single-largest contributor to the Southeast Asia agricultural tractor market revenue. More than 50 units per 1,000 ha operate nationwide, and lead the Southeast Asia agricultural tractor market with significant market share in 2024, leveraging its position as the region's largest agricultural machinery producer and exporter. A manufacturing base lets firms serve neighboring Cambodia and Vietnam efficiently. Thailand's export capabilities to Cambodia, Vietnam, and the Philippines position it as a regional hub for agricultural machinery distribution, while Chinese smart farm technology integration is enhancing safety and sustainability across the sector.

Vietnam is the fastest expansion at an 11.4% CAGR from 2025 to 2030, outpacing regional CAGR on the back of a zero-tariff regime for tractor imports and expanding service-provider networks. The Central Coastal Area demonstrates successful machinery service models where farmers expand operations to other provinces, though income variations between communes highlight the need for better market information and policy adjustments. Precision subsidies expedite the adoption of GPS-enabled mid-range tractors, sustaining robust Southeast Asia agricultural tractor market growth.

Malaysia and Indonesia represent sizable upside as policy packages funnel credit into agritech. Malaysia’s development budget improves rural roads and irrigation, indirectly lifting tractor usage. Indonesia’s credit and microfinance initiatives have met or exceeded lending goals, energizing orders for 20-75 HP units favoured by smallholders. The Philippines pursues digital platforms to coordinate equipment grants, yet uneven rural transformation restrains penetration outside top rice belts. Singapore’s high-tech vertical farms create a boutique market for compact autonomous models. Emerging economies such as Cambodia and Myanmar rely heavily on custom-hiring centers, but as infrastructure improves, ownership rates are projected to climb, widening the addressable Southeast Asia agricultural tractor market.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

The Southeast Asia agricultural tractor market is concentrated. Kubota Corporation, CNH Industrial N.V., and AGCO Corporation command strong brand loyalty, yet regional and Chinese entrants intensify price competition. AGCO Corporation allied with SDF group in February 2025 to reinforce its low- and mid-HP product lines, while CNH Industrial N.V.’s stake in AI startup Bem Agro aims to embed machine-vision autonomy in future releases. New Holland has begun integrating Bluewhite’s technology to cut orchard tractor operating costs by up to 85%.

White-space opportunities exist in service-based business models and financing innovation, where custom hiring centers and micro-lending platforms are democratizing equipment access for smallholder farmers. Emerging disruptors include Chinese technology providers offering smart farm solutions and Korean manufacturers like LS Tractor, which secured a contract with CNH Industrial N.V. for 28,500 units in 2022 and partnered with Vietnam's THACO for KAM50 tractor production.

Weichai Lovol reported high revenue in 2024 and unveiled higher-efficiency tractors targeting Southeast Asia. Disruptive competition also comes from digital leasing firms bundling finance, maintenance, and data services, eroding the advantage of pure-play manufacturers. Success increasingly depends on localized assembly, rapid parts fulfillment, and embedded telematics for predictive service, rather than horsepower alone.

Southeast Asia Agricultural Tractors Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: AGCO Corporation announced a strategic partnership with SDF Group to strengthen its global position in the low-mid horsepower tractor segment, enhancing product offerings and competitiveness in Southeast Asian markets where utility tractors dominate demand patterns.

- August 2024: CNH Industrial showcased cutting-edge equipment at the Farm Progress Show, debuting new harvesters, combines, and digital farm management solutions, including autonomous tractor functions and precision innovations that may influence future Southeast Asian market applications.

- June 2024: New Holland Agriculture, a CNH Industrial brand, partnered with Bluewhite to enhance autonomous capabilities of New Holland tractors, focusing on specialty crops like orchards and vineyards with potential applications in Southeast Asian fruit cultivation.

Table of Contents for Southeast Asia Agricultural Tractors Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising shortage of skilled farm labor

- 4.2.2High adoption of precision-farming subsidies

- 4.2.3Electrification of 20-75 HP tractors for rice and sugarcane farms

- 4.2.4Expansion of rural leasing and micro-lending platforms

- 4.2.5La Nina-linked irrigation investments

- 4.2.6ASEAN-wide carbon-credit schemes rewarding low-tillage tractor use

- 4.3Market Restraints

- 4.3.1Persistent land-holding fragmentation

- 4.3.2Proliferation of custom-hiring centers dampening ownership

- 4.3.3High import tariffs on above 100 HP tractors

- 4.3.4Limited after-sales service network

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter's Five Forces Analysis

- 4.6.1Bargaining Power of Suppliers

- 4.6.2Bargaining Power of Buyers

- 4.6.3Threat of New Entrants

- 4.6.4Threat of Substitute Products

- 4.6.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value)

- 5.1By Tractor Type

- 5.1.1Orchard Tractors

- 5.1.2Row-Crop Tractors

- 5.1.3Utility Tractors

- 5.2By Horse Power

- 5.2.1Less than 12 HP

- 5.2.212 to 99 HP

- 5.2.3100 to 175 HP

- 5.2.4Above 175 HP

- 5.3By Geography

- 5.3.1Thailand

- 5.3.2Vietnam

- 5.3.3Malaysia

- 5.3.4Indonesia

- 5.3.5Singapore

- 5.3.6Philippines

- 5.3.7Cambodia

- 5.3.8Myanmar

- 5.3.9Rest of Southeast Asia

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Kubota Corporation

- 6.4.2Deere & Company

- 6.4.3CNH Industrial N.V.

- 6.4.4Yanmar Holdings Co. Ltd

- 6.4.5CLAAS KGaA mbH

- 6.4.6AGCO Corporation

- 6.4.7Mahindra and Mahindra (Mahindra Group)

- 6.4.8Iseki and Co. Ltd

- 6.4.9Same Deutz-Fahr (SDF Group)

- 6.4.10Kioti Tractor (Daedong Corporation)

- 6.4.11Sonalika Group (International Tractors Ltd)

- 6.4.12LS Mtron Co., Ltd. (LS Group)

- 6.4.13TAFE (Amalgamations Group)

7. Market Opportunities and Future Outlook

Southeast Asia Agricultural Tractors Market Report Scope

An agricultural tractor is a vehicle designed to deliver a high tractive effort at slow speeds to haul a trailer or machinery. The market does not cover other agricultural machinery and attachments to the tractor. The tractor used for industrial and construction purposes is also excluded from the study.

The Southeast Asia agricultural tractor market is segmented by type (orchard tractors, row-crop tractors, and utility tractors), horsepower (less than 12 HP, 12 HP to 99 HP, 100 HP to 175 HP, and Above 175 HP), and geography (Thailand, Vietnam, Malaysia, Indonesia, Singapore, Philippines, Cambodia, Myanmar, and Rest of Southeast Asia).

The market sizing has been done in value terms in USD for all the above-mentioned segments.