South East Asia NOR Flash Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

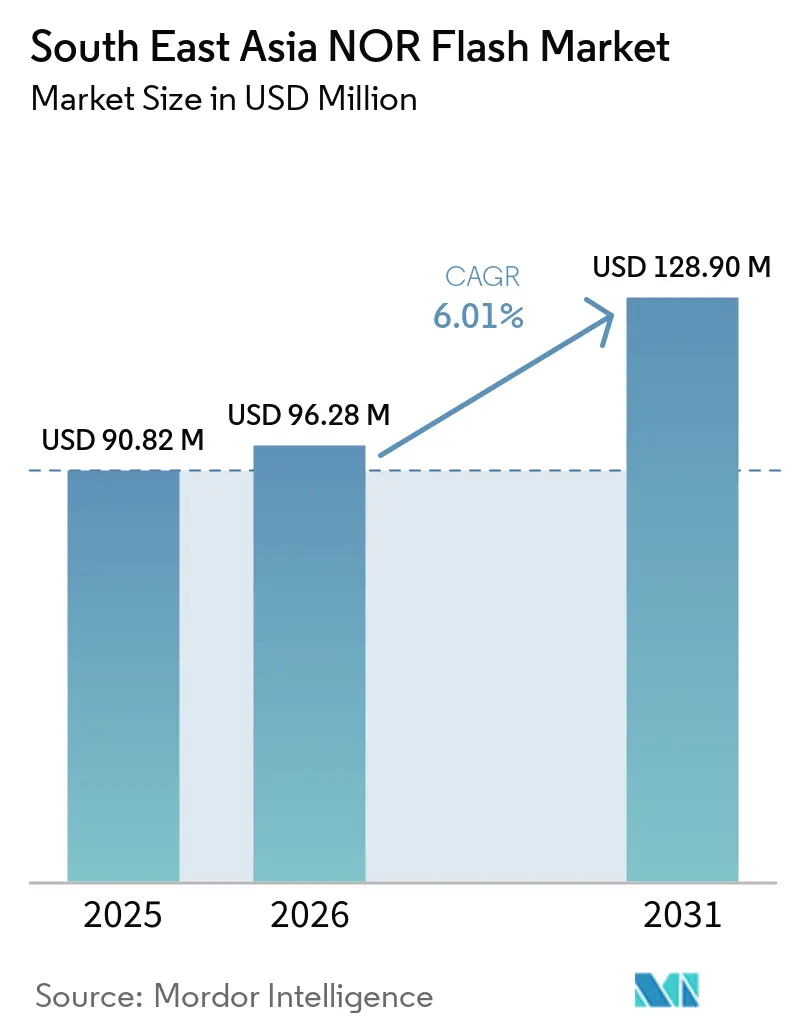

| Base Year Market Size (2025) | USD 90.82 Million |

| Market Size (2026) | USD 96.28 Million |

| Market Size (2031) | USD 128.90 Million |

| Growth Rate (2026 - 2031) | 6.01% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South East Asia NOR Flash Market Analysis by Mordor Intelligence

The South East Asia NOR Flash Market size is expected to grow from USD 90.82 million in 2025 to USD 96.28 million in 2026 and is forecast to reach USD 128.90 million by 2031 at 6.01% CAGR over 2026-2031. In terms of shipment volume, the market was valued at 28.38 million units in 2025 and is expected to grow from 30.64 million units in 2026 to 39.62 million units by 2031, at a CAGR of 5.27% during the forecast period (2026-2031). The Southeast Asia NOR Flash Memory market is being supported by policy-led manufacturing expansion in Vietnam, Thailand, and Malaysia, which is shortening investment approval cycles and widening the regional base of electronics assembly. Demand is also rising because vehicle platforms, communications equipment, and medical devices are carrying more firmware, stronger boot security, and more frequent software updates than before. The Southeast Asia NOR Flash Memory market is also benefiting from 5G and FTTH rollouts, as each optical line terminal, base station controller, and home gateway needs non-volatile memory for boot code and configuration storage. Competitive activity remains centered on product upgrades in high-density, low-voltage, automotive-grade, and high-speed interface families, while supply risk stays elevated because wafer fabrication remains concentrated outside the region. This leaves the South East Asia NOR Flash Memory market exposed to allocation swings, yet it also creates room for suppliers with long product life, safety certification, and strong capacity planning to win more business from regional assemblers.

Key Report Takeaways

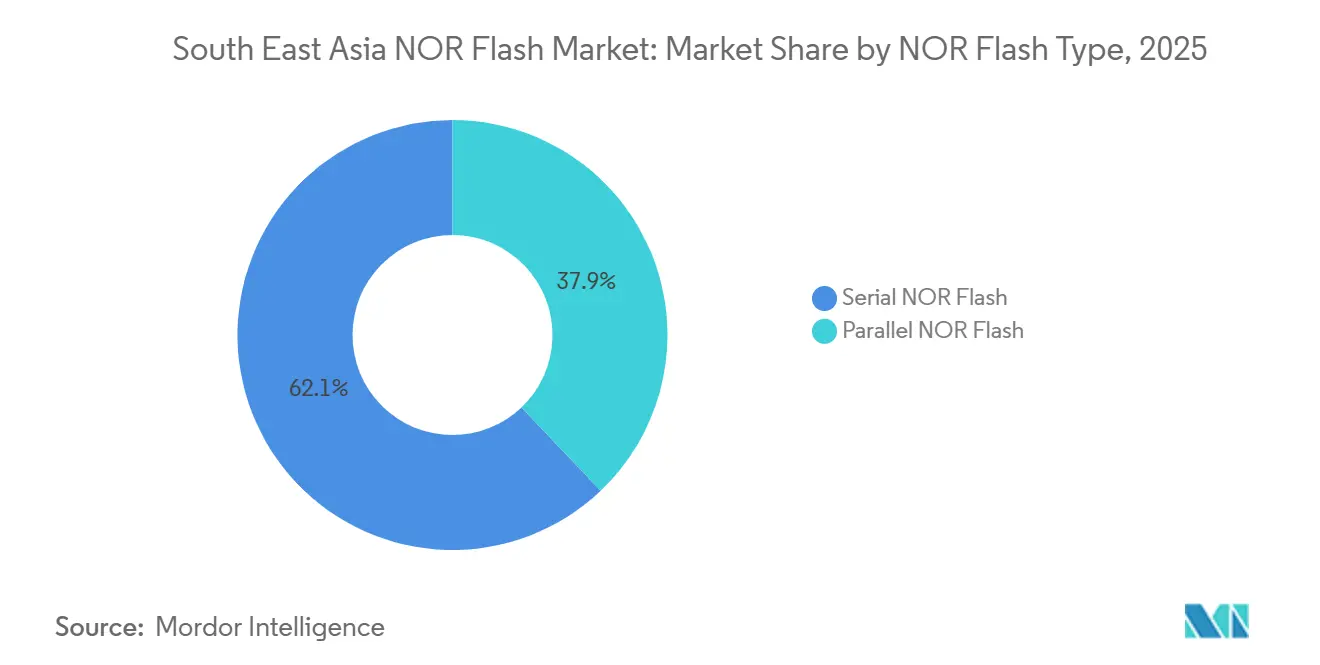

- By type, Serial NOR Flash led with a 62.1% revenue share of the South East Asia NOR Flash Market in 2025 and is also forecast to record the highest CAGR at 7.5% through 2031.

- By interface, Quad SPI held the largest revenue share at 44.8% in 2025, while Octal and xSPI are projected to expand at the fastest CAGR of 7.7% through 2031.

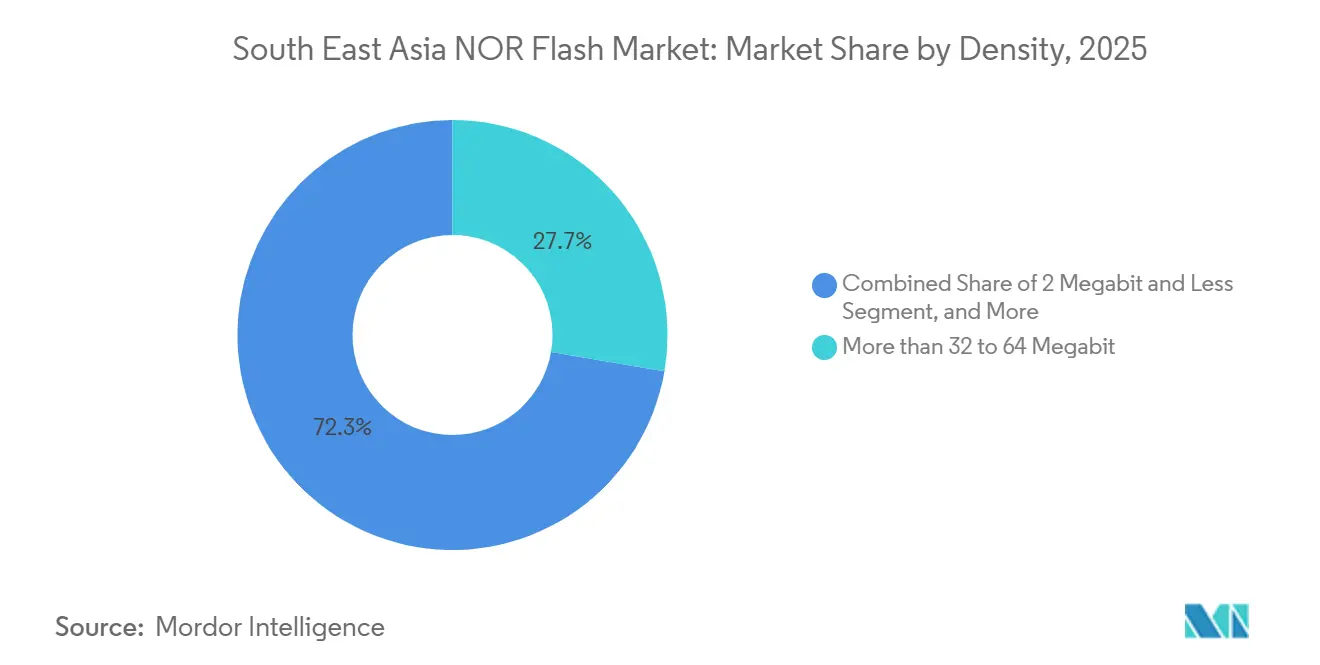

- By density, the more than 32 to 64 megabit segments accounted for 27.7% of revenue share in 2025, while the greater than 256 megabit segment is forecast to grow at the fastest CAGR of 7.3% through 2031.

- By voltage, the 1.8 V class held the largest share at 39.4% in 2025, while the 1.2 V class is projected to advance at the highest CAGR of 8.1% through 2031.

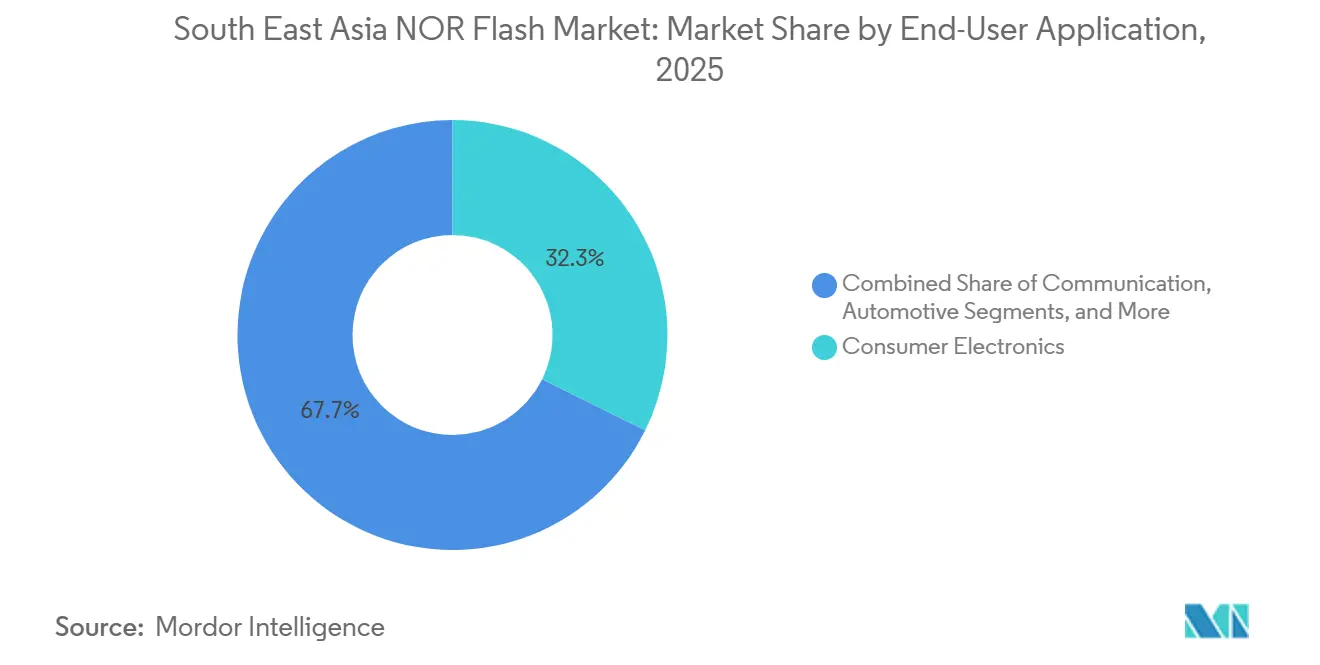

- By end-user application, consumer electronics held the largest share at 32.3% in 2025, while automotive is forecast to register the fastest CAGR of 7.9% through 2031.

- By process technology node, the 65 nm node held the dominant share at 31.9% in 2025, while the 28 nm and below segment is projected to grow at the fastest CAGR of 7.8% through 2031.

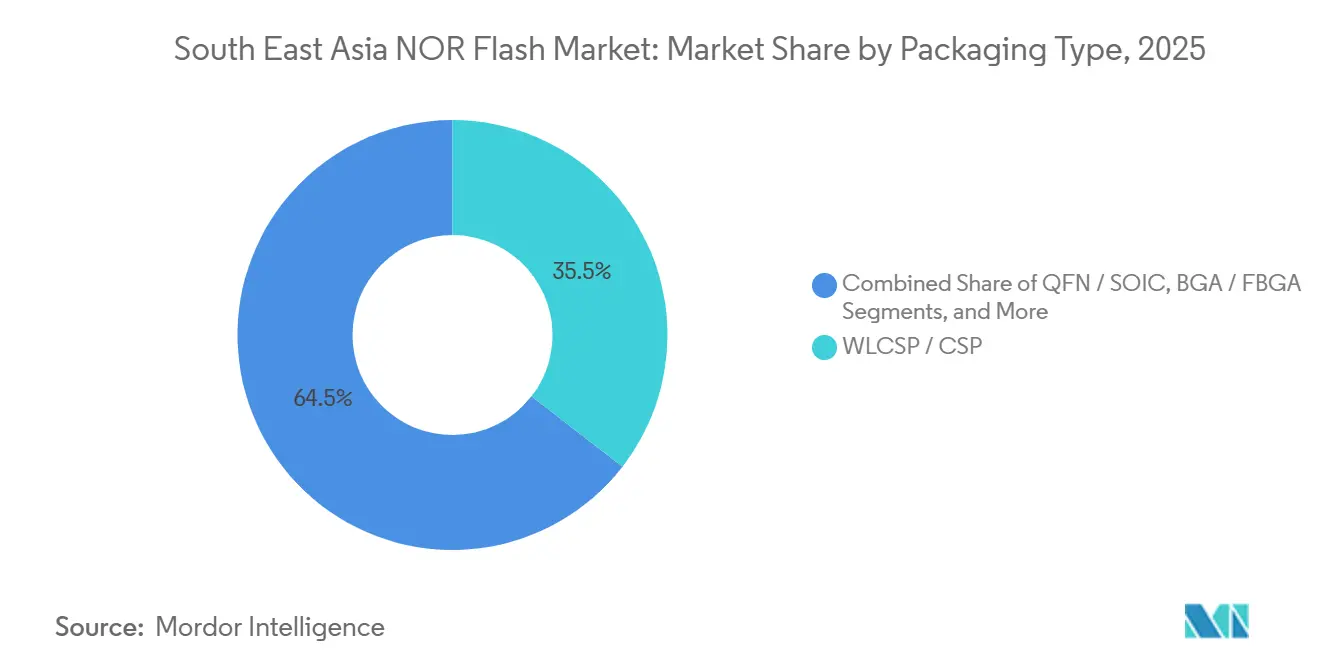

- By packaging type, WLCSP and CSP held the largest share at 35.5% in 2025, and this segment is also forecast to expand at the fastest CAGR of 7.2% through 2031.

- By geography, Vietnam accounted for 27.6% of regional revenue of the South East Asia NOR Flash Market in 2025 and is also projected to record the fastest CAGR of 6.9% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South East Asia NOR Flash Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led incentives driving expansion in electronics manufacturing | +1.4% | Vietnam, Thailand, Malaysia, Philippines, Indonesia | Short term (≤ 2 years) |

| Formation and growth of automotive electronics clusters in the region | +1.1% | Thailand, Malaysia, Vietnam | Medium term (2-4 years) |

| Rising trend of outsourcing in wearable and point-of-care device manufacturing | +0.8% | Malaysia, Philippines, Vietnam | Medium term (2-4 years) |

| Accelerated deployment of 5G and fiber-to-the-home network infrastructure | +0.7% | Indonesia, Philippines, Vietnam, Malaysia | Short term (≤ 2 years) |

| Supply-chain re-shoring initiatives by global Tier-1 OEMs | +0.6% | Vietnam, Malaysia, Thailand | Medium term (2-4 years) |

| Surging demand for NOR Flash in edge AI microcontrollers | +0.5% | Global, with early gains in Vietnam, Malaysia, Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Led Incentives Driving Expansion In Electronics Manufacturing

Government policy has become one of the clearest near-term demand supports for the Southeast Asia NOR Flash Memory market because incentive programs are drawing more assembly, packaging, and electronics manufacturing projects into the region. Vietnam's Circular 33/2025/TT-BKHCN set four eligibility criteria for tax relief for electronics manufacturers, including the use of Vietnam-designed or manufactured semiconductors and at least 30% domestic supply-chain participation, which encourages more localized component sourcing around chip-based products. The Johor-Singapore Special Economic Zone launched in January 2025 and offers a 5% corporate tax rate for qualifying electronics and semiconductor operations for up to 15 years, which improves the case for suppliers that want to stay close to OEM design and assembly centers. Thailand's national semiconductor roadmap targets more than 230,000 highly skilled personnel over a 25-year period, showing that the country is treating semiconductor capability as a long-cycle industrial priority rather than a short policy window.[1]Thailand Board of Investment, “BOI Unveils Draft National Semiconductor Roadmap Aiming to Attract Over 2.5 Trillion Baht in Investments,” The Legal, thelegal.co.th Malaysia's New Incentive Framework became operational on March 1, 2026, and reshaped manufacturing support around electronics, semiconductor packaging, and precision engineering, which broadens the base of plants that consume code storage and boot memory. As these frameworks shorten location decisions for Tier-1 OEMs, they increase the installed base of electronics production lines that generate direct and repeat NOR Flash demand.

Formation And Growth Of Automotive Electronics Clusters In The Region

Automotive electronics clusters are driving the Southeast Asia NOR Flash Memory market higher, as every move toward smart cockpits, ADAS, EV power management, and OTA software increases demand for reliable firmware storage. Multi-Code Electronics and Huizhou Foryou General Electronics signed a manufacturing and development agreement in September 2025 to localize cockpit domain controllers and connected-vehicle technology across ASEAN, with MCE investing RM150 million to RM200 million (USD 34 million to USD 45 million) near Perodua's manufacturing hub. VinFast reached more than 60% EV localization in 2025 and is targeting 84% by 2026, implying increased procurement of automotive-grade memory for ECUs and battery management systems. Malaysia also has a structural advantage because its semiconductor export base and automotive development agenda are converging under national policies supported by the Malaysia Automotive, Robotics and IoT Institute. In practice, this means more vehicle programs in the region are moving from basic memory needs toward safety-qualified devices with stronger reliability and retention requirements. That shift raises entry barriers, concentrates approved vendor lists, and supports higher-value content in the Southeast Asia NOR Flash Memory market.

Rising Trend Of Outsourcing In Wearable And Point-Of-Care Device Manufacturing

Outsourcing in wearable and point-of-care manufacturing is adding a durable demand layer to the Southeast Asia NOR Flash Memory market, as these products rely on boot storage, calibration data, and stable firmware across long qualification cycles. South East Asia was described in 2025 as a geopolitically neutral, increasingly high-tech medtech manufacturing ecosystem, with companies such as Boston Scientific and Medtronic expanding operations in the region, and healthcare spending projected to grow at a 9% CAGR from 2025 to 2029. Philips entered manufacturing partnerships in Indonesia in January 2026 with PT PHC Indonesia and PT Graha Teknomedika to produce ultrasound systems and patient monitors under domestic content rules, showing that OEMs are building local production rather than relying only on imports.[2]Philips, “Philips Enters Local Manufacturing Partnerships to Advance Healthcare Access in Indonesia,” Philips, philips.com.sg These programs matter because medtech products often remain in production for 8 to 15 years and incur high switching costs once regulatory approvals are in place. That gives memory suppliers a steadier, less seasonal demand profile than in pure consumer electronics. It also means that density tiers such as 8 MB to 64 MB remain relevant in the Southeast Asia NOR Flash Memory market, even as public attention shifts to higher-capacity devices.

Accelerated Deployment Of 5G And Fiber-To-The-Home Network Infrastructure

The communications build-out across the region is creating a direct equipment-driven lift for the Southeast Asia NOR Flash Memory market because network gear cannot function without stored boot code and configuration data. Indonesia, Philippines, Vietnam, and Thailand collectively committed more than USD 15 billion to FTTH deployment between 2025 and 2028, and each network termination unit uses NOR Flash for firmware and setup storage. The International Finance Corporation and PT Link Net Tbk announced a March 2026 transaction that mobilized USD 150 million, with co-financing from the Asian Development Bank, to extend fixed broadband services into Indonesia's secondary and tertiary cities.[3]International Finance Corporation, “IFC and Linknet Partner to Expand Fixed Broadband Connectivity Across Indonesia,” IFC, ifc.org Malaysia's U Mobile had already reached 83% 5G population coverage by late 2025, and Telekom Malaysia committed RM430 million (USD 97 million) in 2026-2027 capital expenditure to support 5G fiber backhaul. Telecom hardware orders from these rollouts support both mainstream and mid-range densities, which broadens the regional demand base beyond handheld devices. As a result, infrastructure spending is not an indirect signal for the Southeast Asia NOR Flash Memory market; it is a direct driver of consumption tied to equipment deployment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy dependence on foundries located outside South East Asia | -1.2% | Vietnam, Indonesia, Philippines, Thailand, Malaysia | Long term (≥ 4 years) |

| Intensified margin pressures from cost-competitive Chinese vendors | -0.9% | Vietnam, Indonesia, Philippines | Short term (≤ 2 years) |

| Increased adoption of emerging alternative non-volatile memory technologies | -0.7% | Global, with early adoption in Malaysia and advanced automotive segments | Long term (≥ 4 years) |

| Chronic skilled-labor gaps in sub-20 nm lithography | -0.5% | Vietnam, Indonesia, Philippines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heavy Dependence On Foundries Located Outside South East Asia

The biggest structural constraint on the South East Asia NOR Flash Memory market is that the region consumes large volumes of NOR Flash but does not control the wafer fabrication base that produces it. South East Asia still faces a persistent fab gap, with chipmaking concentrated in China and Taiwan even as the region tries to build a deeper semiconductor ecosystem. Earlier allocation shifts in China toward mature logic node expansion have already put pressure on NOR Flash output, tightening supply for assemblers in countries such as Vietnam and Malaysia. U.S.-Taiwan trade and investment commitments announced in January 2026 directed USD 250 billion in Taiwanese semiconductor investment toward the United States, reinforcing the view that new upstream fab capacity is not moving to Southeast Asia at scale. Because the qualified supplier base in NOR Flash is narrow, local manufacturers cannot easily diversify when allocation is tight. This leaves the Southeast Asia NOR Flash Memory market exposed to geopolitical shocks and supplier prioritization decisions for most of the forecast period.

Intensified Margin Pressures From Cost-Competitive Chinese Vendors

Price pressure from Chinese suppliers remains a significant restraint, as many buyers in the Southeast Asia NOR Flash Memory market operate in highly cost-sensitive consumer and industrial categories. NOR Flash prices for some models rose by more than 30% within a single month in late 2025, exposing how little margin room distributors had when upstream quotations moved sharply. Puya Semiconductor adjusted quotations across its SPI NOR product lines from November 2025 onward, and its 55 nm charge-trap process remains a core source of cost competitiveness even as contract prices rise. Supply chain commentary in 2025 and 2026 also pointed to allocation concentration among Winbond, GigaDevice, and Macronix, especially at 256 Mb and above, making smaller assemblers more vulnerable when competing against higher-margin AI server demand.[4]Ineltek, “How to Secure NOR Flash, SLC NAND and Specialty DRAM Supply, 2025-2026 Crisis Solutions,” Ineltek, ineltek.co.uk The result is that distributors and contract manufacturers in Vietnam, Indonesia, and the Philippines often face both sides of the squeeze at once: unstable input pricing and intense end-market price competition. That pressure can delay purchasing, compress profitability, and limit the pace at which some customers move toward higher-value parts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By NOR Flash Type: Serial NOR Flash Sustains Leadership Through Interface Fit And Board Efficiency

Serial NOR Flash accounted for 62.1% of revenue in 2025, representing 62.1% of the South East Asia NOR Flash market share that year. It also posted the fastest projected CAGR among type segments at 7.5% for 2026-2031, showing that leadership is being reinforced rather than eroded. The segment aligns with the regional manufacturing base because SPI connectivity, lower pin counts, and compact board requirements match the microcontroller-heavy designs used in consumer electronics, communications equipment, and a broad range of industrial products. Execute-in-place capability also reduces the need for shadow RAM, which keeps bill-of-materials pressure under control in a region where cost discipline shapes product architecture. In 2026, Winbond continues to extend its higher-density serial NOR and automotive-grade product roadmap, with faster interfaces and low-power form factors that align with this demand pattern.

The practical outcome is that serial NOR serves both high-volume consumer platforms and newer edge devices without forcing major design changes across the Southeast Asia NOR Flash Memory market. Wearables, Wi-Fi modules, IoT endpoints, and smart appliances all benefit from the segment's space efficiency and standardized controller compatibility. That is why the Southeast Asia NOR Flash Memory industry continues to treat serial NOR as the default option for most new designs unless a specific bandwidth or legacy system condition points elsewhere. Parallel NOR Flash still has a role, but it is mostly tied to older industrial controllers, automotive displays, and boot-intensive systems where a wider bus remains operationally useful. Automotive-grade parallel offerings from Infineon and Winbond preserved a protected niche in 2024 for ECUs and infotainment platforms that still require that architecture. Even so, the long-term direction of the Southeast Asia NOR Flash Memory market remains clearly aligned with serial products, as most new regional assembly programs prioritize compact layouts, lower pin count, and easier platform reuse.

By Interface: Quad SPI Holds The Base While Octal And xSPI Drive The Upgrade Cycle

Quad SPI held the largest interface revenue share at 44.8% in 2025, reflecting its wide installation base across mainstream electronics assembly. Octal and xSPI are forecast to grow at the fastest CAGR of 7.7% from 2026 to 2031, indicating a steady shift in performance requirements as processors and vehicle systems demand higher read bandwidth. This split captures the current shape of the South East Asia NOR Flash market, where legacy volume and forward-looking design wins are moving at different speeds. Quad SPI remains deeply embedded because many existing microcontroller platforms already support it, and the installed base across communications modules and consumer products is large. That gives it continued volume strength even as engineering teams prepare for faster standards.

Octal and xSPI are gaining ground as real-time code execution becomes more common in automotive processors, AI-capable controllers, and higher-performance embedded systems in the Southeast Asia NOR Flash Memory market. Infineon's SEMPER portfolio supports Octal SPI and HYPERBUS with endurance and retention characteristics optimized for industrial and automotive use, demonstrating that interface upgrades are already aligned with demanding applications. STMicroelectronics also supports XSPI 8-bit and 16-bit configurations in its newer STM32N-series devices, confirming that controller ecosystems are now being built with xSPI readiness in mind. Single and dual SPI channels still matter in low-cost Bluetooth modules, IoT sensors, and entry wearables, especially in cost-sensitive markets such as Vietnam and Indonesia. Yet the direction of platform design is clear, and the South East Asia NOR Flash Memory market will increasingly reward suppliers that can support both the large Quad SPI base and the migration path toward Octal and xSPI.

By Density: Mid-Range Volumes Anchor Demand While Above 256 Mb Gains The Most Momentum

The more than 32 to 64 megabit category held 27.7% of revenue in 2025, making it the largest density tier in the regional market. This band aligns closely with the firmware needs of mainstream Wi-Fi chips, Bluetooth SoCs, smart meters, and many low-to-mid-tier wearables, which explains its volume advantage in core assembly hubs. It also benefits from broad product catalogs and shorter procurement lead times, which matter for manufacturers running lean inventories. In that sense, the segment captures a large part of the installed base that has kept the Southeast Asia NOR Flash Memory market stable across consumer and communications demand cycles. It is the tier most closely tied to everyday electronics output rather than to specialized high-end applications.

At the top end, the greater than 256 megabit segment is projected to grow at a 7.3% CAGR from 2026 to 2031, which makes it the fastest-growing density range. AI-driven server demand is a major reason, because a GB200-based rack requires far more NOR Flash devices than a conventional rack and has begun to reallocate resources toward higher-capacity parts. Macronix stated that sampling of 3D NOR Flash devices is planned for the second half of 2026, with mass production targeted for 2027, which signals a direct industry response to density limits in traditional 2D NOR structures. Intermediate ranges from 8 megabit to 32 megabit remain important for IoT and portable diagnostics, while 128 megabit to 256 megabit supports network equipment, secure access devices, and vehicle subsystems. This produces a layered demand pattern in the South East Asia NOR Flash Memory market where no single density family can serve every growth pocket. It also means suppliers that span mainstream and high-capacity nodes are better placed to capture demand as purchasing shifts between consumer cycles, infrastructure build-outs, and AI-led allocation pressure.

By Voltage: 1.8 V Keeps The Installed Base While 1.2 V Becomes The Main Growth Track

The 1.8 V class held the largest share at 39.4% in 2025, accounting for a leading share of the Southeast Asia NOR Flash Memory market at the segment level. Its lead reflects broad compatibility with the dominant SoC generation used in wearables, smartphones, and communications equipment assembled across the region. Manufacturers have had little reason to retool legacy platforms away from 1.8 V, given that performance, board design, and supply chains already support it well. The 3 V class also retained a meaningful role in industrial controllers, automotive ECUs, and legacy communications equipment, where noise margin and voltage tolerance remain important. That has kept the installed base broad, especially in applications with long replacement cycles.

The strongest growth, however, is moving to 1.2 V, which is projected to rise at an 8.1% CAGR from 2026 to 2031. This is the highest growth rate among voltage segments, and it tracks the spread of 1.2 V I/O SoCs in AI inference chips, premium wearables, and next-generation wireless modules that need lower power draw. GigaDevice expanded the GD25UF family in March 2026 from 8 Mb to 256 Mb at 1.2 V, directly targeting AI computing, hearables, medical devices, and other battery-sensitive products. Wide-voltage components from 1.65 V to 3.6 V continue to serve industrial and defense-adjacent uses where supply precision is harder to guarantee. That gives the Southeast Asia NOR Flash Memory market a clear split between legacy scale and future growth, with 1.8 V preserving volume while 1.2 V captures design wins in lower-power devices. Over time, suppliers that support both classes cleanly will be better positioned as the regional mix shifts toward smaller, smarter, and more power-aware products.

By End-User Application: Consumer Electronics Leads Current Revenue While Automotive Expands The Fastest

Consumer electronics accounted for the largest share at 32.3% in 2025, underscoring the region's continued ties to the global device manufacturing chain. Smartphone subassemblies in Vietnam, smart home appliances in Malaysia, and set-top box production across ASEAN continue to support a wide base of firmware memory consumption. That installed base gives scale to the South East Asia NOR Flash Memory market even when other end-user categories move unevenly. It also sustains demand across multiple densities, interfaces, and package formats rather than concentrating it in a narrow product set. Communications and industrial equipment add a stable supporting demand, but consumer electronics still define the revenue base.

Automotive is the fastest-growing application, with a projected CAGR of 7.9% from 2026 to 2031, making it the clearest growth engine by end use. In software-defined vehicle platforms, NOR Flash handles ADAS firmware, cluster initialization, secure boot, and OTA update staging, which lifts both content per vehicle and qualification requirements. ISO 26262 ASIL D has become a central procurement threshold, and Macronix expanded its MXSMIO family in January 2026 to include this certification level for automotive ECUs, clusters, and ADAS systems. Infineon's SEMPER NOR family is also positioned toward safety-critical automotive and industrial applications, reinforcing the move toward validated suppliers. The communications segment remains supported by 5G and FTTH infrastructure, while industrial applications depend on long-life, lower-density devices with strict temperature and longevity requirements. Together, these shifts show that the Southeast Asia NOR Flash Memory market is no longer driven solely by consumer volume, as automotive and infrastructure demand are steadily boosting the value of qualified memory content.

By Process Technology Node: 65 nm Leads On Cost And Fit While 28 nm And Below Takes The Growth Edge

The 65 nm node held the largest share at 31.9% in 2025, and it remains the core process balance point for cost, endurance, and performance. At this node, suppliers can deliver the read speeds and 100,000 program and erase cycle endurance that many mainstream microcontroller-based products still require without the yield and cost risk of pushing deeper scaling. That is why the node continues to anchor a large portion of the Southeast Asia NOR Flash Memory market across both consumer and industrial use. It is mature enough for dependable output and efficient enough for a wide range of embedded designs. This gives OEMs a stable procurement base while newer nodes move into more selective applications.

The faster growth lies in the 28 nm and below segment, which is projected to expand at a 7.8% CAGR from 2026 to 2031. That demand is tied to low-power automotive SoCs and AI-capable edge processors that need better efficiency and tighter integration. Winbond's W25QxxRV family, built on updated 58 nm technology, shows that incremental node improvements in the 65 nm range still deliver real performance and power benefits without crossing into the highest process risk zones. At the same time, published research in MRS Communications notes that conventional NOR Flash faces major cell-level scaling challenges below 28 nm, which helps explain why vendors are exploring 3D structures rather than relying only on planar shrink. The 90 nm and older segment remains important for legacy industrial and automotive programs with very long life cycles, while 55 nm and 45 nm continue to serve much of the mid-range embedded volume. This leaves the South East Asia NOR Flash Memory market with a practical split: mature nodes dominate current demand, while advanced nodes and new architectures shape the next phase of growth.

By Packaging Type: WLCSP And CSP Lead Both Current Scale And Future Product Direction

WLCSP and CSP held the largest packaging share at 35.5% in 2025, and they are also projected to record the fastest CAGR at 7.2% through 2031. That means the same package family is leading both present demand and future adoption, which points to a structural shift rather than a temporary cycle. The driver is straightforward; smaller wearables, hearables, compact IoT sensors, and portable medical devices all need tighter board footprints and lighter packaging. This gives WLCSP and CSP a central role in the Southeast Asia NOR Flash Memory market as product miniaturization spreads across consumer, medical, and low-power industrial designs. It also explains why packaging strategy has become a product roadmap issue rather than a back-end manufacturing detail.

GigaDevice's GD25UF family is available in WLCSP alongside USON8 and WSON8 formats, showing that suppliers are aligning low-voltage devices with package choices favored by compact electronics. QFN and SOIC remained the second-largest packaging group in 2025 because they still fit industrial and communications equipment where legacy PCB compatibility matters more than absolute miniaturization. BGA and FBGA are gaining traction in high-density and automotive-grade uses where solder reliability under heat and vibration is critical. The Others category, which includes TSOP, DIP, and older parallel NOR formats, is losing ground as new designs move toward serial interfaces and smaller footprints. This shift is gradual because industrial customers change slowly, but the direction is clear across the South East Asia NOR Flash Memory market. Packaging is now closely linked to end-product design priorities, and suppliers that support both miniaturized consumer formats and rugged automotive layouts will keep the strongest position.

Geography Analysis

Vietnam accounted for 27.6% of regional revenue in 2025 and is also the fastest-growing country market, with a projected CAGR of 6.9% from 2026 to 2031. Its lead is tied to the dense concentration of electronics OEM assembly anchored by Samsung, LG, Foxconn, and Intel, which keeps the country at the center of regional device output. Intel Products Vietnam has exported more than 4 billion units and contributed more than USD 100 billion to Vietnam's cumulative export turnover as of Q2 2025, which underlines the country's role in global electronics supply chains. Automotive electronics are becoming a second support layer, with Biel Crystal announcing a fully integrated Haiphong plant for automotive cover glass and smart cockpit display modules in November 2025. VinFast's localization push toward 84% by 2026 also points to rising procurement of automotive-grade memory through Vietnam's supplier base.

Malaysia and Thailand form the second tier, though their demand profiles differ in useful ways for the Southeast Asia NOR Flash Memory market. Malaysia combines OSAT strength with automotive electronics and new manufacturing investment, and AIXTRON signed a USD 47 million greenfield facility agreement with MIDA in Penang in May 2026. Malaysia's incentive framework and the Johor-Singapore Special Economic Zone are also attracting more electronics and semiconductor activity into the installed manufacturing base. Thailand brings a different advantage through its large automotive platform and long-range workforce plan under the national semiconductor roadmap, which supports growing demand for qualified memory in vehicle electronics.

Indonesia and the Philippines round out the regional picture with different demand drivers. Indonesia is closely tied to communications infrastructure, and the IFC and Link Net financing package announced in March 2026 will expand fiber broadband into underserved cities, lifting demand for optical network terminals that carry boot storage. Local analysis in May 2026 also pointed to mature-node semiconductors for automotive, IoT, power electronics, and industrial use as Indonesia's more realistic near-term manufacturing path, which fits NOR Flash's broad 45 nm to 90 nm profile. The Philippines, meanwhile, remains important because semiconductors accounted for 60% to 62% of merchandise exports at USD 39 billion in 2024 and the country supplies close to 10% of global assembly, testing, and packaging output. Its fiber backbone efforts and SEZ-based manufacturing base also support rising communications and medtech equipment demand, which keeps the country relevant even without the same scale of automotive activity.

Competitive Landscape

The Southeast Asia NOR Flash Memory market is moderately concentrated, with Winbond Electronics Corporation, GigaDevice Semiconductor Inc., and Macronix International Co. Ltd. holding a dominant share of regional shipments. The market structure highlights a significant concentration of volume among a small group of suppliers, which provides scale leaders with advantages in allocation, product breadth, and long-life support programs, particularly for customers requiring automotive or industrial qualifications. At the same time, smaller vendors such as Puya Semiconductor, Elite Semiconductor Microelectronics Technology, AMIC Technology, and AP Memory continue to exert pricing pressure in lower-value tiers. This dynamic creates a market environment where leadership is evident, but no single supplier can fully dictate pricing or customer choices across all densities and interfaces.

Recent strategy in the Southeast Asia NOR Flash Memory market has centered on product specialization and capacity planning rather than only on headline share defense. Winbond announced a record NTD 42.1 billion (USD 1.33 billion) capital expenditure plan for 2026 and targeted a 30% to 40% year-on-year increase in NOR and NAND shipments, while reporting capacity booked through 2027. Macronix introduced ArmorBoot MX76 in August 2025 with secure boot, hardware authentication, and data integrity verification, and then extended its MXSMIO family to ASIL D in January 2026, signaling a deliberate move into security- and safety-focused niches with higher entry barriers. GigaDevice is pushing from another angle by expanding its dual-voltage xSPI product line and growing the 1.2 V GD25UF line from 8 Mb to 256 Mb, which strengthens its presence in wearables, AI edge devices, and medical electronics. These moves show that differentiation now comes from interface speed, voltage efficiency, safety certification, and security features as much as from basic memory supply.

Chinese suppliers remain important challengers, but a clear trade-off between price appeal and supply stability shapes their role in the Southeast Asia NOR Flash Memory market. Cost-first positioning helps vendors such as Puya win business in entry-level consumer and industrial products, yet allocation can tighten quickly when domestic demand or AI-linked orders absorb output. That has pushed procurement teams in the region to look more closely at diversification, product longevity, and manufacturing location when approving suppliers. It also favors companies with Taiwan-based manufacturing, longer support commitments, and validated automotive or industrial portfolios. As a result, competition is becoming less about who can simply offer NOR Flash and more about who can offer qualified NOR Flash with stable delivery through the forecast period.

South East Asia NOR Flash Industry Leaders

Winbond Electronics Corporation

Macronix International Co. Ltd.

GigaDevice Semiconductor Inc.

Infineon Technologies AG

Micron Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: AIXTRON SE concluded a USD 47 million greenfield semiconductor manufacturing facility agreement with MIDA in Penang, Malaysia at SEMICON Southeast Asia 2026, marking AIXTRON's first Malaysia-based production site for compound semiconductor deposition equipment and reinforcing Penang's position as an advanced semiconductor manufacturing cluster with production scheduled to begin in the second half of 2027.

- March 2026: The International Finance Corporation and PT Link Net Tbk, Linknet, announced a financing transaction mobilizing USD 150 million from the Asian Development Bank to expand fiber broadband connectivity across Indonesia's secondary and tertiary cities, deploying optical network terminals that incorporate NOR Flash for boot code storage in underserved markets.

- February 2026: Winbond Electronics Corporation announced a record capital expenditure plan of TWD 42.1 billion, USD 1.33 billion, for 2026, targeting a 30-40% year-on-year increase in NOR and NAND flash shipments. Winbond's president James Chen confirmed that capacity is fully booked through 2026 and 2027, with each NVIDIA GB200-based AI server rack requiring more than 120 NOR Flash chips, equivalent to the consumption of 120 PCs, underscoring the AI-driven upshift in high-capacity NOR demand.

- January 2026: Macronix International Co. Ltd. expanded its MXSMIO flash memory family to include ISO 26262 ASIL D compliance, the highest automotive functional-safety certification level, with Octal Flash and QSPI multi-I/O interface variants targeting automotive ECUs, instrument clusters, and ADAS systems. This product expansion directly addresses the fastest-growing automotive end-user segment across South East Asia's vehicle electronics manufacturing hubs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South-East Asia NOR flash memory market as sales, in value terms, of serial and parallel NOR chips that are newly fabricated on 90 nm to sub-28 nm nodes and shipped to device makers across Indonesia, Malaysia, the Philippines, Thailand, and Vietnam for code-storage and fast-boot functions in consumer, automotive, industrial, and communication equipment.

Scope exclusion: Emerging alternatives such as MRAM, RRAM, and all forms of NAND flash fall outside this boundary.

Segmentation Overview

- By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less

- More than 2 to 4 Megabit

- More than 4 to 8 Megabit

- More than 8 to 16 Megabit

- More than 16 to 32 Megabit

- More than 32 to 64 Megabit

- More than 64 to 128 Megabit

- More than 128 to 256 Megabit

- More than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V - 3.6 V)

- Others - 1.2 V Class and Similar Sub-1.8 V (2.5 V, 5 V, etc.)

- By End-user Application (Value, Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other End-user Applications

- By Process Technology Node (Value)

- 90 nm and More

- 65 nm

- 55 nm (including 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

- By Geography (Value, Volume)

- Vietnam

- Indonesia

- Philippines

- Thailand

- Malaysia

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed wafer foundries, OSAT houses, module makers, and procurement managers across Singapore, Bangkok, and Ho Chi Minh City to validate die-size cost curves, SPI interface preferences, and channel inventory norms. Follow-up surveys with automotive Tier-1 electronics and IoT gateway firms filled critical gaps on future density migration and price-elastic demand.

Desk Research

We gathered baseline supply, trade, and consumption cues from open datasets released by WSTS, UN Comtrade, ASEANstats, and national customs portals, which together signal production shifts, import reliance, and average selling prices. Industry white papers and design-win notes from JEDEC, GSMA, and SEMI, alongside corporate 10-Ks and investor decks, added color on density road maps and end-market attach rates. Subscription sources, including D&B Hoovers for fabless revenue splits, Dow Jones Factiva for capacity announcements, and Questel for key NOR-related patent families, helped us map competitive intensity and innovation velocity. This list is illustrative; many additional publications were reviewed to verify and refine evidence.

Market-Sizing & Forecasting

A top-down model converts HS 854232 trade and in-region wafer output into dollar demand, adjusted for local value-add and re-exports. It then corroborates totals with selective bottom-up checks, sampled vendor shipments, and average selling price benchmarks to align reality. Key inputs feeding the model include smartphone assembly volumes, 5G base-station rollout counts, automotive ECU penetration, industrial robot shipments, and SPI NOR blended ASP trends. Multivariate regression projects these drivers through 2030, while scenario analysis buffers for capex swings and ASP compression. Any bottom-up gaps are bridged using channel check ratios agreed upon in expert calls.

Data Validation & Update Cycle

Outputs pass variance scans against independent indicators such as quarterly WSTS revenue and ASEAN import tallies; anomalies trigger analyst re-checks before sign-off. Reports refresh each year, with interim updates when material events, such as capacity fires, export controls, and major design wins, arise. A final analyst pass ensures clients receive the latest consensus view.

Why Our South East Asia NOR Flash Baseline Commands Reliability

Published numbers often diverge because firms pick dissimilar geographies, interface mixes, and refresh cadences.

Key gap drivers include broader APAC or global scopes, exclusion of low-density SPI devices, one-off currency conversions, and shorter forecast windows, which together inflate or deflate totals relative to Mordor's disciplined SEA-only lens and annual recalibration.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 90.82 Mn (2025) | Mordor Intelligence | - |

| USD 2.8 Bn (2023, APAC) | Regional Consultancy A | Uses full Asia-Pacific scope and older base year, no trade-flow adjustment |

| USD 1.2 Bn (2023, APAC) | Global Consultancy B | Bundles SEA with North Asia and omits sub-65 nm die splits |

| USD 3.22 Bn (2025, Global) | Industry Association C | Global roll-up, mixes NOR with niche industrial NV-RAM, different currency base |

Taken together, the comparison shows that when region, interface type, and density tiers are aligned, Mordor's SEA baseline offers a balanced, transparent figure that decision-makers can confidently trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the 2031 value outlook for South East Asia NOR Flash Memory?

The market is projected to reach USD 128.9 million by 2031, rising from USD 96.3 million in 2026 at a 6.0% CAGR over 2026-2031.

Which product type leads demand in South East Asia NOR Flash Memory?

Serial NOR Flash led with 62.1% revenue share in 2025 and is also the fastest-growing type segment with a 7.5% CAGR through 2031.

Why is automotive becoming important for NOR Flash demand in South East Asia?

Automotive is the fastest-growing end-user application at 7.9% CAGR because ADAS, smart cockpits, EV control systems, and OTA software all require reliable firmware storage.

Which country is the strongest growth engine in the region?

Vietnam led the region with 27.6% revenue share in 2025 and is forecast to post the fastest CAGR at 6.9% through 2031 due to its electronics and automotive manufacturing base.

What is driving the move toward higher-speed interfaces in NOR Flash products?

Octal and xSPI are growing fastest at 7.7% CAGR as automotive SoCs, AI-capable processors, and advanced embedded systems need more read bandwidth than Quad SPI can provide.

What is the main supply-side risk for buyers in this space?

The key risk is the region's heavy dependence on wafer fabs located outside South East Asia, which leaves local assemblers exposed to allocation pressure, pricing swings, and geopolitical disruption.

Page last updated on: