Mexico NOR Flash Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

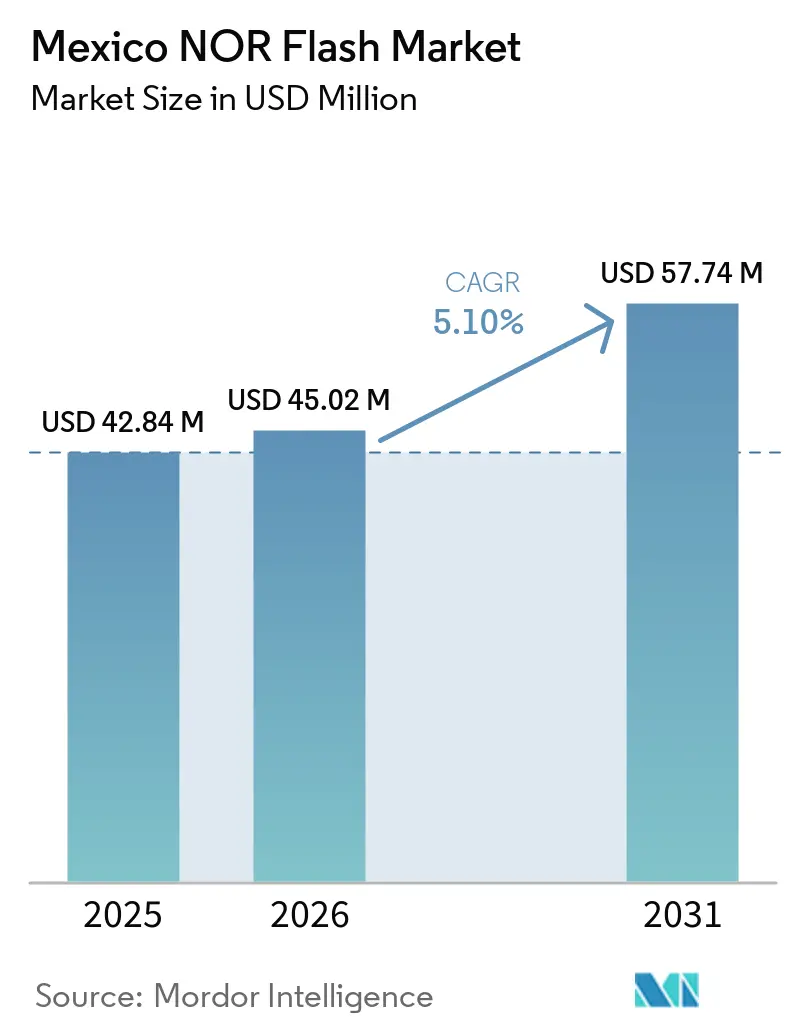

| Base Year Market Size (2025) | USD 42.84 Million |

| Market Size (2026) | USD 45.02 Million |

| Market Size (2031) | USD 57.74 Million |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico NOR Flash Market Analysis by Mordor Intelligence

The Mexico NOR Flash Market size is expected to grow from USD 42.84 million in 2025 to USD 45.02 million in 2026 and is forecast to reach USD 57.74 million by 2031 at 5.10% CAGR over 2026-2031. In terms of shipment volume, the market was valued at 144.40 million units in 2025 and is expected to grow from 156.36 million units in 2026 to 218.13 million units by 2031, at a CAGR of 6.89% during the forecast period (2026-2031). Growth in the Mexican NOR Flash market is tied to the country’s role in North American electronics and vehicle supply chains, where assembly, testing, and final integration remain the main drivers of demand. Automotive electrification, data infrastructure build-outs, and high-volume electronics assembly continue to widen the installed base for firmware, secure boot, and code storage devices across Mexico. The market also reflects Mexico’s downstream manufacturing profile, since local demand is driven more by assembly and final testing than by domestic wafer fabrication. Competition remains moderate, with leading suppliers holding a combined share below 40%, leaving room for pricing pressure and second-source adoption in consumer and industrial programs. Over the forecast period, the clearest opportunities for the Mexico NOR Flash market will come from higher-content automotive controllers, industrial automation upgrades, and low-voltage designs for compact edge devices.

Key Report Takeaways

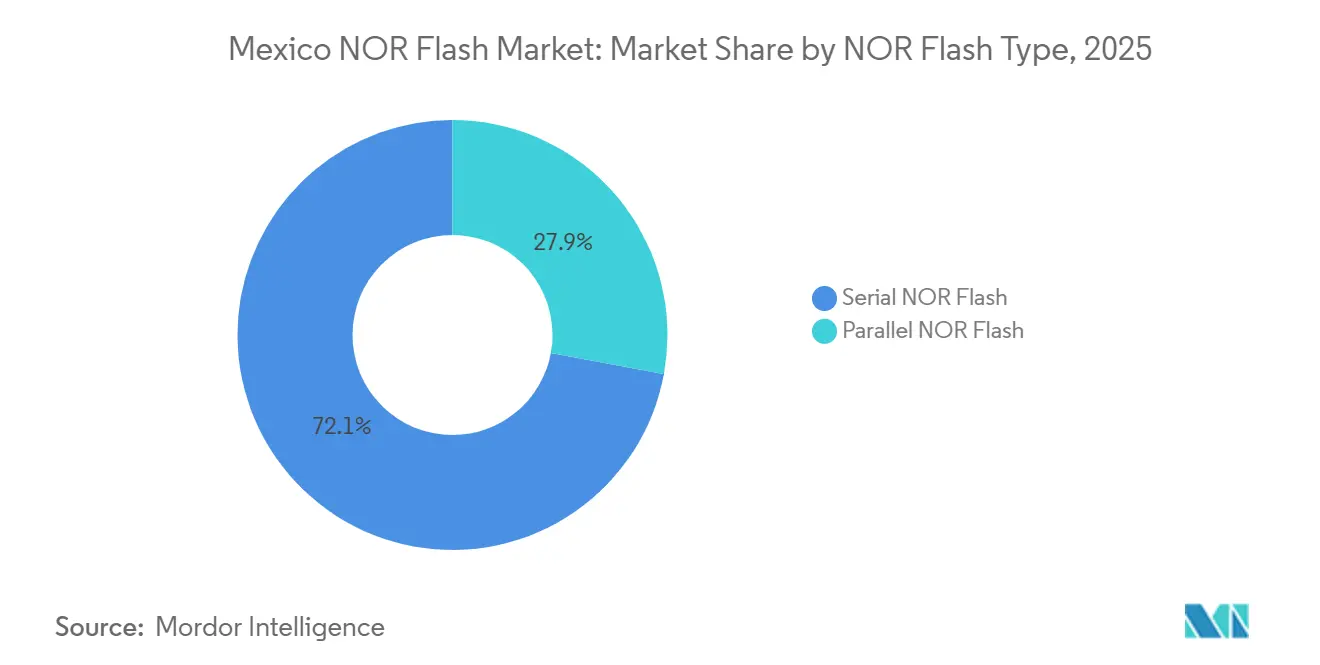

- By NOR flash type, serial NOR Flash led with 72.1% revenue share of the Mexico NOR flash \market in 2025, while parallel NOR Flash is forecast to grow at a 7.2% CAGR through 2031.

- By interface, SPI Single and Dual accounted for 54.8% of revenue in the Mexico NOR flash \market in 2025, while Octal and xSPI recorded the fastest projected CAGR of 7.4% through 2031.

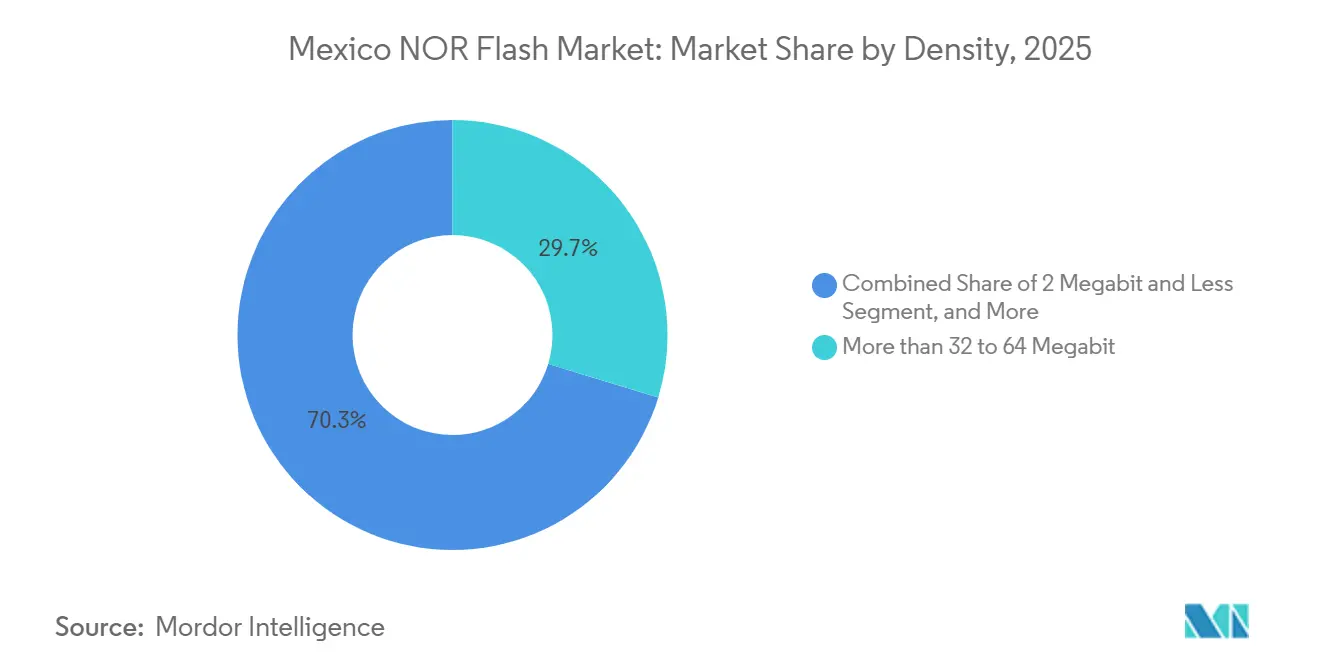

- By density, the more than 32 to 64 Megabit tier accounted for 29.7% of revenue in the Mexico NOR flash \market in 2025, while the greater than 256 Megabit tier is advancing at a 7.6% CAGR through 2031.

- By voltage, the 3 V class accounted for 40.4% of revenue in the Mexico NOR flash market in 2025, while the ≤1.2 V class is projected to expand at a 6.9% CAGR through 2031.

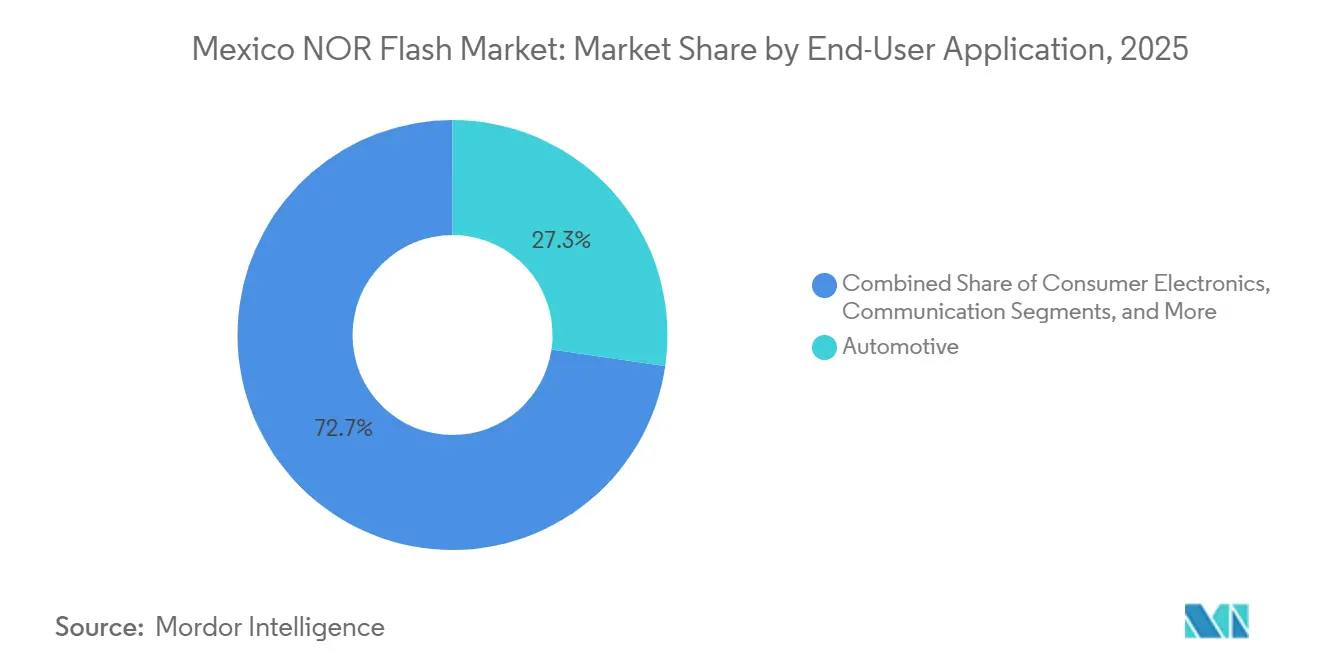

- By end-user application, automotive accounted for 27.3% of revenue in the Mexico NOR flash market in 2025, while industrial and factory automation is forecast to grow at a 7.1% CAGR through 2031.

- By process node, the 55/58 nm tier accounted for 25.2% of revenue in the Mexico NOR flash market in 2025, while 28 nm and below is expected to grow at a 7.3% CAGR through 2031.

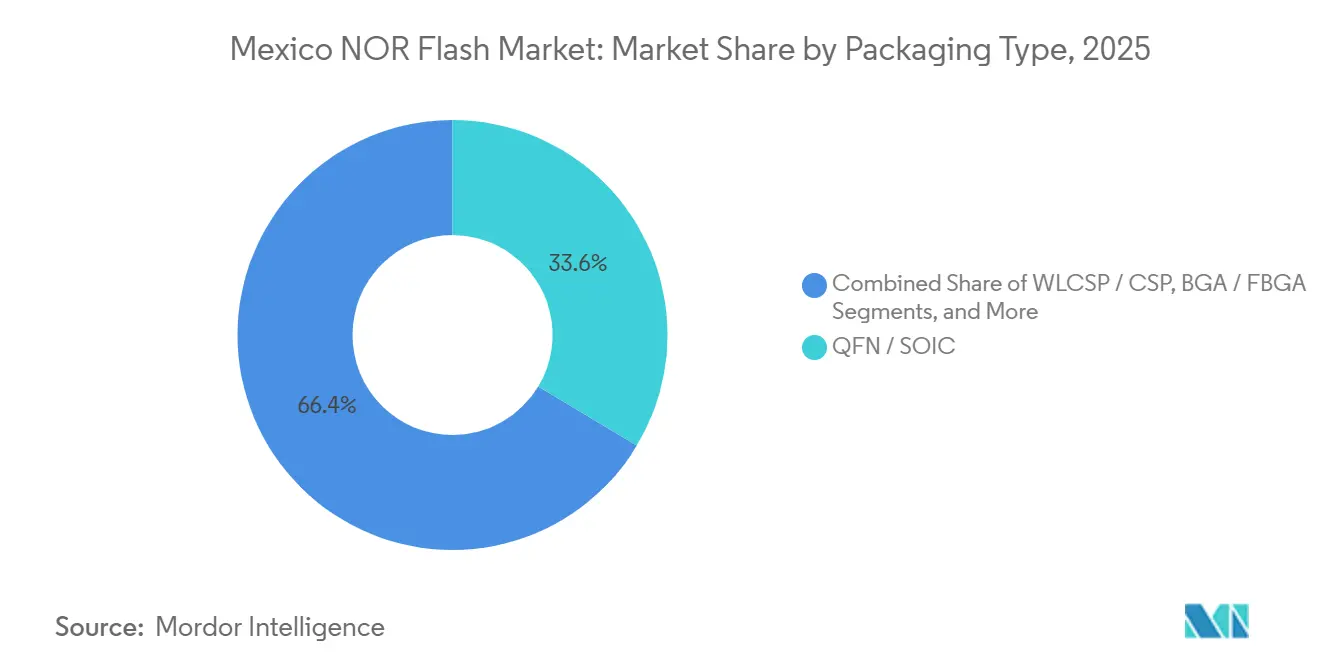

- By packaging type, QFN/SOIC accounted for 33.6% of revenue in the Mexico NOR flash market in 2025, while WLCSP/CSP is projected to grow at a 6.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Mexico representing one among them. The global report on nor flash market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Mexico NOR Flash Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion Of The Automotive Industry In Mexico | +1.5% | North and Bajío corridor, Monterrey, Saltillo, Guadalajara, Aguascalientes | Medium term (2-4 years) |

| Data-Center And Digital-Infrastructure Boom | +1.2% | Central Mexico, Querétaro, Mexico City, Guadalajara | Short term (≤ 2 years) |

| Rising Consumer-Electronics Assembly In Northern Mexico | +0.9% | Northern border belt, Tijuana, Ciudad Juárez, Mexicali | Short term (≤ 2 years) |

| Government Tax Incentives For Semiconductor Investment | +0.7% | National, with early gains in Jalisco, Sonora, Puebla, Querétaro | Medium term (2-4 years) |

| Industrial IoT Adoption Across Maquiladora Plants | +0.6% | Maquiladora corridors, Monterrey, Chihuahua, Tijuana | Medium term (2-4 years) |

| Increasing Demand For Code Storage In Autonomous Vehicles | +0.4% | North America integrated OEM supply chain, centered in Nuevo León and Bajío | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion Of The Automotive Industry In Mexico

Mexico’s automotive base remains the strongest structural demand source for the Mexico NOR Flash market. Auto parts output reached USD 10.01 billion in January 2026, up 9.35% year over year, which shows that vehicle electronics programs are still expanding across the country. Local sourcing by automotive OEMs also rose 18% year over year in the first quarter of 2026 as stricter USMCA content rules pushed more procurement into domestic supply chains. That matters for NOR Flash because engine control units, body controllers, gateway modules, digital cockpits, and ADAS platforms all require firmware storage and boot memory. Mexico attracted USD 9.26 billion in automotive foreign direct investment across 204 projects in 2025, which gives the installed manufacturing base more depth and keeps design wins in the country for longer production cycles. IMMEX and USMCA together also strengthen this driver because they support nearshoring into electronics assembly lines that consume automotive-grade NOR Flash in large volumes.

Data-Center And Digital-Infrastructure Boom

Data center construction is creating a second demand stream for the Mexico NOR Flash market outside its traditional vehicle focus. Mexico’s data center association projected USD 18.14 billion in direct investment from 2025 to 2030, which supports steady demand for memory used in servers, accelerators, network cards, and power systems.[1]BNAmericas, “The Main Data Center Projects Under Development in Mexico,” BNAmericas, bnamericas.com Flex announced a USD 1 billion investment to design, manufacture, and test data center and AI infrastructure components across Jalisco, Chihuahua, and Aguascalientes, which expands the local hardware base that consumes NOR Flash for firmware functions. Foxconn also invested an additional USD 136 million in Mexico in March 2026 to expand AI server capacity, reinforcing Guadalajara and Chihuahua as major hardware nodes for North American hyperscalers.[2]Focus Taiwan, “Foxconn to Invest More in Mexico, Likely to Expand AI Server Capacity,” Focus Taiwan, focustaiwan.tw Each server board, accelerator module, and network interface requires boot code and configuration memory, which lifts unit demand even when the end system value comes mainly from processors and networking silicon. This means the Mexico NOR Flash market benefits not only from local data center construction, but also from Mexico’s role in assembling AI equipment that will be deployed across the wider region.

Rising Consumer-Electronics Assembly In Northern Mexico

Northern Mexico remains a major electronics assembly corridor, and that keeps the Mexico NOR Flash market closely tied to consumer and connected-device output. OECD data showed that maquila operations accounted for 78% of total semiconductor and electronics sector income in Mexico in 2024, confirming that downstream assembly remains the dominant channel for component demand.[3]Organisation for Economic Co-operation and Development, “Examining the Domestic Semiconductor Ecosystem, Promoting the Development of the Semiconductor Ecosystem in Mexico,” OECD, oecd.org Taiwan accounted for 38% of Mexico’s technology imports in 2025, and that share rose to 50% in the fourth quarter as Taiwanese firms increasingly used Mexico as an assembly platform for AI hardware and advanced electronics. NOR Flash is widely used in routers, set-top boxes, appliances, smart-home hubs, and wearables for secure boot and firmware storage, so assembly growth directly supports volume demand across this channel. The practical effect is that the Mexico NOR Flash market stays anchored in high-throughput, cost-sensitive production programs, especially in Tijuana, Ciudad Juárez, and Mexicali.

Government Tax Incentives For Semiconductor Investment

Tax policy is beginning to support a broader demand base for NOR Flash memory in Mexico. The January 2025 Plan México decree granted immediate tax deductions of 56% to 89% on fixed-asset investments in technology, R&D, and electronics manufacturing for fiscal years 2025 and 2026. Total fiscal incentives under the decree were capped at MXN 30 billion (USD 1.73 billion), with MXN 28.5 billion (USD 1.64 billion) allocated to fixed assets and MXN 1.5 billion (USD 862.5 million) to training and innovation programs. In February 2025, the Kutsari National Semiconductor Design Center was announced with planned design units in Puebla, Jalisco, and Sonora, and the Jalisco unit entered operations in 2025. These measures do not create local wafer capacity, but they do expand testing, prototyping, and design-linked electronics activity that can pull more qualified NOR Flash into domestic workflows. Over time, this shifts policy support away from passive assembly incentives and toward a more technology-focused manufacturing model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Advanced Lithography Tools And IP Royalties | -1.2% | National, particularly relevant for Querétaro and Jalisco semiconductor clusters | Long term (≥ 4 years) |

| Limited Domestic Foundry Capacity And Ecosystem | -0.9% | National, front-end wafer fabrication is essentially absent | Long term (≥ 4 years) |

| Supply-Chain Exposure To Geopolitical Shocks | -0.7% | Northern border corridor, US-Mexico trade arteries, USMCA-dependent sectors | Medium term (2-4 years) |

| Shortage Of Skilled Semiconductor Talent | -0.5% | National, with regional concentration in Monterrey, Guadalajara, Mexico City | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost Of Advanced Lithography Tools And IP Royalties

The Mexican NOR Flash market still faces a clear ceiling on domestic value addition because advanced process economics remain difficult to absorb locally. QSM Semiconductores launched Mexico’s first MEMS-focused semiconductor plant in Querétaro in February 2026, investing MXN 777 million (USD 45 million), which is still far below the capital intensity associated with a competitive NOR Flash fab. The cost gap matters because 28 nm and below requires deep process control, expensive equipment, and long qualification cycles that are hard to justify without a large domestic design base. The input also notes that interface-related IP royalties can add 5% to 10% to chip licensing costs, which compresses margin headroom for any local production effort that depends on imported technology. That burden is felt most sharply in advanced automotive and high-speed interface programs, where qualification requirements are strict and redesign timelines are long. Until more local design capability is translated into commercial IP and scale manufacturing, Mexico will remain more exposed to imported cost structures than to internally generated semiconductor value.

Limited Domestic Foundry Capacity And Ecosystem

A second structural restraint for the Mexico NOR Flash market is the lack of front-end wafer fabrication at commercially relevant NOR Flash nodes. OECD data showed that foreign firms invested a cumulative USD 1.6 billion in Mexico’s semiconductor and electronics industry through just 29 investments between January 2003 and August 2025, which shows how limited the local fabrication ecosystem still is relative to Asian supply bases. This means chips consumed in Mexico are still imported mainly from established foreign producers, leaving local assemblers exposed when supply lanes tighten, or second-source qualification becomes necessary. The absence of domestic foundry access also slows design activity because engineers need process design kits, shuttle runs, and local technical support to build products around embedded and discrete memory devices. Mexico’s current semiconductor policy recognizes this gap, but it prioritizes design capability before wafer fabrication, which means the ecosystem constraint will remain in place through most of the forecast horizon. As a result, demand can grow in assembly and testing, while the country still captures only a limited share of the total semiconductor value chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By NOR Flash Type: Serial Architecture Holds The Lead While Parallel Gains In Automotive

Serial NOR Flash held 72.1% of revenue in 2025, which keeps it as the dominant architecture in the Mexico NOR Flash market. Its position reflects wide compatibility with SPI-based microcontrollers used across appliances, communications equipment, and factory automation products assembled in Mexico. OECD data on maquila dominance support this pattern because downstream assembly rewards low-cost, mature, and readily sourced components over architectural shifts that would require broader redesign. In practical terms, serial devices fit the main production logic of the Mexican NOR Flash market, where board compatibility and procurement stability often matter more than absolute speed.

Parallel NOR Flash is forecast to grow at a 7.2% CAGR through 2031, driven by high-content vehicle platforms that require more deterministic access behavior and larger code storage footprints. Automotive-grade memory programs continue to move toward stricter safety requirements, and supplier activity around ASIL-D qualified product families shows that the performance end of the category is still attracting investment. This does not displace serial volume, but it does expand a narrower and more valuable set of sockets in digital cockpit, gateway, and ADAS systems. The result is a split architecture pattern where broad-volume assembly stays with serial designs, while advanced automotive builds support faster growth for parallel devices.

By Interface: SPI Keeps Scale While Octal And xSPI Accelerate

SPI Single and Dual held 54.8% of revenue in 2025, reflecting the scale of legacy controller platforms already in use across the Mexican NOR Flash market. That installed base remains large in consumer electronics, smart metering, and industrial control applications, where redesign costs are closely monitored. Suppliers still support this interface with high-performance product extensions, which allow OEMs to improve throughput and reliability without forcing an immediate migration across the entire hardware stack.[4]New Electronics, “High Performance, Low Power, Small Form-Factor Flash Memory for Next Generation Devices,” New Electronics, newelectronics.co.uk This keeps SPI at the center of volume shipments even as the technical ceiling for newer platforms keeps rising.

Octal and xSPI is projected to grow at a 7.4% CAGR through 2031 because new vehicle and edge-compute systems need faster read speeds and shorter secure boot times. Infineon’s ASIL-D-certified SEMPER family spans JEDEC xSPI and related automotive interfaces, indicating that major suppliers are aligning product roadmaps with this upgrade path. The user input also noted that a Mexico-based ADAS supplier reduced cold-start time to 0.4 seconds by switching to OSPI, which reflects how interface choice now affects system behavior more directly in safety-sensitive designs. As these performance demands spread, the Mexico NOR Flash market will keep a large SPI base while higher-value automotive programs move more decisively toward Octal and xSPI.

By Density: Mid-Range Leads Current Demand While More Than 256 Mbit Expands Fastest

The more than 32 to 64 Megabit tier accounted for 29.7% of 2025 revenue and remains the volume center of the Mexico NOR Flash market. This density band serves mainstream firmware sockets in automotive ECUs, industrial controllers, and communications hardware, where the code base is meaningful but still contained. It works well for products with long replacement cycles because OEMs can hold proven designs for years without reopening the memory architecture. That stable demand base is one reason the Mexico NOR Flash market continues to rely heavily on mature and broadly qualified density ranges.

The greater than 256 Megabit tier is expected to grow at a 7.6% CAGR through 2031 as software-defined vehicles, gateway modules, and domain controllers require larger boot images, update buffers, and execute-in-place storage. Macronix introduced ArmorBoot MX76 in August 2025 with capacities up to 1 GB, directly targeting automotive electronics, AI, and IoT use cases that need secure boot and higher firmware content. SST and UMC also announced in January 2026 the immediate availability of an embedded 28 nm SuperFlash Gen 4 automotive platform, supporting the broader move toward denser, faster memory subsystems in next-generation ECUs. This means future growth will be less about replacing mid-range sockets and more about adding larger memory footprints to advanced vehicle and industrial platforms.

By Voltage: Legacy 3 V Designs Stay Broad While ≤1.2 V Becomes More Important

The 3 V class accounted for 40.4% of revenue in 2025, underscoring how much of the Mexican NOR Flash market still depends on long-established automotive and industrial power rails. That position is rooted in qualification history, because many existing systems were designed around 3.3 V environments and do not justify rapid redesign. In these programs, electrical familiarity and thermal reliability carry more weight than the efficiency gains of a lower-voltage shift. The large installed base, therefore, keeps 3 V products at the core of present shipments across the Mexican NOR Flash market.

The ≤1.2 V class is projected to grow at a 6.9% CAGR through 2031 as edge AI processors, compact IoT nodes, and battery-sensitive devices adopt lower I/O standards. GigaDevice expanded the GD25UF series in March 2026 to cover 8 MB to 256 MB densities at 1.2 V, with the company stating that read power consumption can be up to 50% lower than standard 1.8 V alternatives. That product move reflects a wider change in the Mexican NOR Flash market, where low-voltage support is becoming a design requirement rather than a niche feature in compact electronics. The transition will support new demand but will also require requalification of assembly lines built to older voltage standards.

By End-User Application: Automotive Leads Revenue While Industrial And Factory Automation Gains Speed

Automotive accounted for 27.3% of revenue in 2025 and remained the single largest end-user segment in the Mexico NOR Flash market. Mexico’s large vehicle manufacturing base, coupled with increasing local sourcing, supports stable demand for memory in body electronics, safety systems, digital cockpits, and electrified powertrains. This makes automotive the most established demand channel, with strong links to long program cycles and rigorous qualification standards. In segment terms, automotive still anchors the Mexico NOR Flash market share because it combines high volume with rising electronic content per vehicle platform.

Industrial and factory automation is forecast to grow at a 7.1% CAGR through 2031 as maquiladora facilities continue to modernize with connected systems, remote monitoring, and more automated production lines. Mexico Business News reported rising cyber and machine-to-machine risks as factories adopt more IoT technology, which confirms that industrial hardware is moving toward more connected control architectures. Those architectures depend on firmware integrity, secure updates, and consistent boot behavior, all of which support the use of NOR Flash in controllers and edge nodes. As a result, industrial demand is becoming the fastest-moving application stream inside the Mexico NOR Flash market even though automotive still leads current revenue.

By Process Technology Node: 55/58 Nm Balances Cost And Reliability While 28 Nm And Below Gains Premium Programs

The 55/58 nm tier represented 25.2% of 2025 revenue and remains the largest process-node range in the Mexico NOR Flash market. Its lead comes from a practical balance between cost, maturity, thermal performance, and endurance for mainstream automotive and industrial sockets. Mature nodes also support easier sourcing across large production runs, which matters for Mexico’s assembly-heavy manufacturing profile. This node range, therefore, continues to shape the core procurement pattern across the Mexico NOR Flash market.

The 28 nm and below tier is forecast to grow at a 7.3% CAGR through 2031 as automotive safety and high-performance applications ask for faster access times and more advanced embedded memory options. SST and UMC announced in January 2026 that their embedded SuperFlash Gen 4 on 28HPC+ had reached automotive Grade 1 qualification, with read access below 12.5 ns and endurance above 100,000 cycles. GigaDevice’s ASIL-D-certified GD25 and GD55 automotive NOR Flash series on 55- and 45-nm nodes also shows that suppliers are competing through certification and application fit, not just by moving to smaller nodes. This means node leadership will remain mature in volume terms, while sub-28 nm products capture the safety-critical premium.

By Packaging Type: QFN And SOIC Stay Mainstream While WLCSP And CSP Benefit From Miniaturization

QFN and SOIC packaging held 33.6% of revenue in 2025 and continued to lead the Mexico NOR Flash market because thermal stability and mechanical reliability remain central in automotive and industrial use. These formats are well understood on production lines and fit the operating conditions of under-hood electronics, industrial controls, and other rugged environments. Their position also reflects the installed base of legacy programs that prioritize process consistency over footprint reduction. In current terms, this packaging family remains the broadest physical format base in the Mexican NOR Flash market.

WLCSP and CSP are projected to grow at a 6.8% CAGR through 2031 as smaller consumer devices and low-voltage designs seek tighter board layouts. GigaDevice launched the GD25NX xSPI NOR Flash family in November 2025, with WLCSP and TFBGA24 package options for direct integration with 1.2 V SoCs, demonstrating how packaging is aligned with miniaturized system design. That shift is especially relevant in IoT endpoints and compact smart-home products assembled in Mexico, where board-space efficiency has become a stronger purchasing factor. The package mix will therefore remain bifurcated, with rugged formats holding large, established programs and chip-scale formats gaining share in smaller, more integrated devices.

Geography Analysis

Northern Mexico remains the main demand cluster in the Mexico NOR Flash market because it concentrates the country’s highest-throughput assembly activity. OECD data showed that maquila operations generated 78% of semiconductor and electronics sector income in Mexico in 2024, and that production model is heavily concentrated along the northern corridor. This region links Tijuana, Mexicali, Ciudad Juárez, Monterrey, and Reynosa through a manufacturing base that absorbs NOR Flash into televisions, appliances, communications hardware, and automotive modules. Ciudad Juárez is shifting toward server and semiconductor-adjacent exports, with Taiwanese investment in the city reaching USD 3 billion over the prior 4 years and supporting more than 25,000 jobs. Nuevo León is also reinforcing this pattern, with Intretech opening a USD 60 million smart electronics plant in Apodaca for automotive rearview mirrors, IoT devices, and navigation systems that all rely on embedded firmware memory.

Central Mexico is the fastest-evolving regional demand pocket in the Mexico NOR Flash market because it combines automotive electrification with data infrastructure projects. Guadalajara is central to that shift because Foxconn is expanding AI server capacity in Mexico and the Kutsari design center established a Jalisco unit in 2025, linking design activity with high-volume electronics production. Querétaro continues to attract semiconductor-related manufacturing after QSM opened Mexico’s first precision semiconductor plant there in February 2026. The broader data center build-out also supports this region, with major projects under development in Querétaro and a deepening hardware ecosystem around server, networking, and power equipment. In the Bajío, electromobility-related investment announcements totaling USD 1.57 billion in 2025 are strengthening demand for automotive-grade memory in Aguascalientes, Guanajuato, and San Luis Potosí.

Emerging regions are still smaller, but they add new long-term nodes for the Mexico NOR Flash market. USAT announced an MXN 2,430 million investment, already translated in the input to USD 140 million, in a semiconductor and solar-cell manufacturing plant in Kanasín, Yucatán in March 2026. Sonora gains strategic weight from its planned Kutsari design unit and its proximity to Arizona’s semiconductor base, which can support design collaboration and faster technical linkages. The Inter-Oceanic Corridor and south-southeast industrial planning are not yet major volume markets, but they widen the future map for electronics manufacturing and memory demand inside Mexico.

Mordor Intelligence provides coverage of the nor flash market across other key regional markets, including Europe and Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United States, Italy, India, China, Japan, United Kingdom, and South Korea incorporating local coverage and market participation, as required.

Competitive Landscape

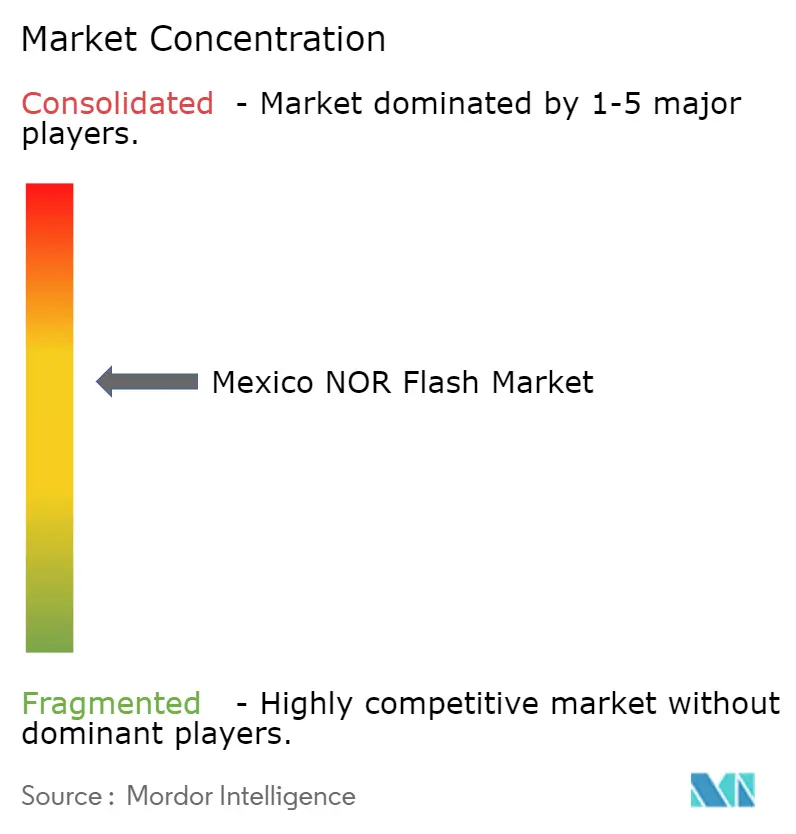

The Mexico NOR Flash market remains moderately concentrated, with Infineon Technologies, Winbond Electronics, and Micron Technology collectively accounting for less than 40% of revenue in 2025. That structure gives leading suppliers room to benefit from qualification depth and distributor reach, while still leaving meaningful space for second-source vendors and price-based challengers. The leading group is strongest in automotive and industrial programs, where long validation cycles, product longevity, and established Tier-1 relationships still shape purchasing behavior. In practice, the Mexican NOR Flash market rewards suppliers that combine technical support with consistent availability across multiple production cycles. This is why certification and application fit still matter as much as list pricing in the higher-value parts of the market.

Infineon has strengthened its position through a certification-driven product strategy. In May 2025, its SEMPER NOR Flash family received full ASIL-D certification under ISO 26262:2018 from SGS-TÜV for QSPI, HyperBus, and JEDEC xSPI octal interfaces across densities from 256 Mbit to 2 Gbit. Macronix also expanded its automotive posture when the MXSMIO family achieved full ISO 26262 ASIL-D compliance in January 2026 for safety-critical uses such as ADAS, gateway modules, and digital cluster controllers. These moves support long-duration design wins in the Mexico NOR Flash market because vehicle programs tend to lock in qualified memory suppliers well before full-scale production ramps.

Chinese challengers are tightening competition, especially in industrial and cost-sensitive consumer programs. GigaDevice reached ASIL-D certification for its automotive NOR Flash series and then added the GD25NX xSPI family in November 2025 and expanded the 1.2 V GD25UF line in March 2026, giving it a stronger position in both advanced automotive and low-power edge applications. This matters because the Mexico NOR Flash market still contains a large base of price-sensitive industrial, communications, and appliance sockets where buyers value functional qualification but remain open to newer vendors. The competitive opening is widest in mid-tier industrial and networking applications, where distributor coverage and in-country support can shift socket wins faster than in tightly controlled automotive programs. Overall, the market is not dominated by a single supplier group, and that keeps rivalry active across both performance-led and cost-led tiers.

Mexico NOR Flash Industry Leaders

Winbond Electronics Corporation

Macronix International Co. Ltd.

GigaDevice Semiconductor Inc.

Infineon Technologies AG

Micron Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Foxconn, Hon Hai Precision Industry Co., invested an additional USD 136 million in Mexico through its Singapore subsidiary, with industrial sources indicating the funds target expansion of AI server production capacity in Guadalajara and Chihuahua to serve North American hyperscalers. This reinforces Mexico as a primary NOR Flash consumption node for AI infrastructure memory demand.

- March 2026: Ultimate Solar Advanced Technology, USAT, announced an MXN 2,430 million, approximately USD 140 million, investment in a semiconductor and solar-cell manufacturing plant in Kanasín, Yucatán, executing in two phases and positioning the state as a new technology manufacturing hub in southeastern Mexico.

- March 2026: GigaDevice expanded the density range of its GD25UF series 1.2 V ultra-low-power SPI NOR Flash from 8 Mb to 256 Mb, announcing the expansion at Embedded World 2026 in Nuremberg and targeting AI computing platforms, edge-AI ASICs, and compact battery-operated devices with up to 50% lower read-power versus standard 1.8 V alternatives.

- February 2026: QSM Semiconductores officially launched Mexico's first precision semiconductor plant in El Marqués, Querétaro, representing an MXN 777 million, approximately USD 45 million, investment in MEMS-based integrated circuit manufacturing. The plant, inaugurated with federal and state government officials, represents the first vertically integrated design-fabrication-commercialization model in Mexico.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Mexico's NOR flash memory market as revenue generated inside the country from newly fabricated serial and parallel NOR chips, across all densities up to >256 Mb, that are soldered onto consumer, industrial, communication, and automotive boards for code storage or execute in place functions. Values are tracked in USD and unit volumes.

Scope exclusion: NAND, embedded eMMC/UFS, OTP PROM, and refurbished devices are outside this assessment.

Segmentation Overview

- By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less

- More than 2 to 4 Megabit

- More than 4 to 8 Megabit

- More than 8 to 16 Megabit

- More than 16 to 32 Megabit

- More than 32 to 64 Megabit

- More than 64 to 128 Megabit

- More than 128 to 256 Megabit

- More than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65-3.6 V)

- ≤1.2 V Class

- By End-user Application (Value, Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial and Factory Automation

- Rest of Applications

- By Process Technology Node (Value)

- 90 nm and More

- 65 nm

- 55 / 58 nm

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Rest of Packaging Types

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews with Guadalajara contract assemblers, Tier 1 automotive ECU makers in Guanajuato, and SPI flash distributors that cover Baja California. These discussions clarified inventory turns, typical density mixes, and price compression, allowing us to fine tune preliminary desk estimates.

Desk Research

We extracted baseline volumes from open sources such as INEGI's electronics manufacturing census, Banco de México trade tables, UN Comtrade HS 854232 shipment data, and WSTS semiconductor bulletins, then enriched them with association white papers from CANIETI and SEMI. Financial clues from listed suppliers' 20-F filings and D&B Hoovers profiles helped anchor average selling prices. Paid datasets, Dow Jones Factiva for deal news and Questel for patent counts, filled historic gaps. These sources illustrate, not exhaust, our wider literature sweep.

Market-Sizing & Forecasting

We apply a top down import plus local assembly reconstruct, adjusted for in country retention after re export under IMMEX, then validate with selective bottom up supplier roll ups. Key variables like SMT line utilization, automotive light vehicle output, average SPI attach rates per MCU, peso denominated ASP trends, and government semiconductor tax incentives drive the model. A multivariate regression projects each variable to 2030; gaps in bottom up samples are bridged with weighted regional benchmarks before final triangulation.

Data Validation & Update Cycle

Outputs undergo variance checks against WSTS regional totals and customs anomalies; senior reviewers sign off only when swings sit inside +/-5%. Reports refresh yearly, and we trigger interim revisions when tariff shifts or fab outages materially alter outlooks.

Why Our Mexico NOR Flash Baseline Stays Dependable

Published figures often differ because some firms pool NOR with NAND, quote continental totals, or lock forecasts to single scenario ASP paths.

Key gap drivers here include rival studies rolling Mexico into North America roll ups, counting legacy EEPROM lines, assuming flat peso dollar rates, and updating less than once a year; factors we screen out through the disciplined approach above.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 42.84 million (2025) | Mordor Intelligence | - |

| USD 5.27 billion (2025) | Global Consultancy A | Global coverage, includes NAND and MCP combos |

| USD 4.10 billion (2025) | Regional Consultancy B | North America total, omits IMMEX re exports |

| USD 3.22 billion (2025) | Trade Journal C | Global, uses blended flash densities and 2024 Fx rates |

Taken together, the comparison shows how Mordor's country specific scope, fresh data cadence, and variable level cross checks provide decision makers with a balanced, traceable baseline that is ready for boardroom use.

Key Questions Answered in the Report

What is the 2026 value of Mexico NOR Flash market?

The Mexico NOR Flash market is valued at USD 45.02 million in 2026 and is projected to reach USD 57.74 million by 2031 at a 5.1% CAGR.

Which end-user segment leads demand in Mexico?

Automotive is the largest end-user segment, accounting for 27.3% of revenue in 2025 because vehicles use NOR Flash in control units, ADAS, gateways, and digital cockpit systems.

Which interface is growing the fastest in Mexico?

Octal and xSPI is the fastest-growing interface segment with a 7.4% CAGR through 2031, supported by faster read speeds and secure boot needs in advanced automotive systems.

Why does serial NOR Flash still dominate in Mexico?

Serial NOR Flash held 72.1% of revenue in 2025 because it fits SPI-based microcontrollers widely used in consumer electronics, communications equipment, and factory automation products assembled in Mexico.

What is driving low-voltage NOR Flash adoption in Mexico?

The ≤1.2 V class is growing at a 6.9% CAGR through 2031 as edge-AI chipsets, compact IoT nodes, and battery-sensitive devices move toward lower I/O standards.

How competitive is supplier activity in Mexico?

Competition is moderate because the top 3 players held below 40% of the market in 2025, while certified challengers such as GigaDevice continue to expand in automotive, industrial, and low-power applications.

Page last updated on: