Asia-Pacific NOR Flash Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.88 Billion |

| Market Size (2026) | USD 1.99 Billion |

| Market Size (2031) | USD 2.65 Billion |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific NOR Flash Market Analysis by Mordor Intelligence

The Asia-Pacific NOR Flash market size is expected to grow from USD 1.88 billion in 2025 to USD 1.99 billion in 2026 and is forecast to reach USD 2.65 billion by 2031 at a 5.9% CAGR over 2026-2031. Design-win activity in automotive electronics and advanced serial interfaces is lifting value growth even as consumer-electronics unit volumes level off. Taiwanese foundry strength, China’s push for chip self-sufficiency, and Japan’s mature automotive-memory ecosystem keep the region at the center of global production and demand. Automotive OEM qualification cycles, export-control frictions, and emerging ReRAM alternatives are reshaping supplier strategies toward higher-density, highly reliable parts. Mature-node wafer tightness in Taiwan continues to dictate pricing power, with 55-nanometer and 40-nanometer capacity booked through 2027.

Key Report Takeaways

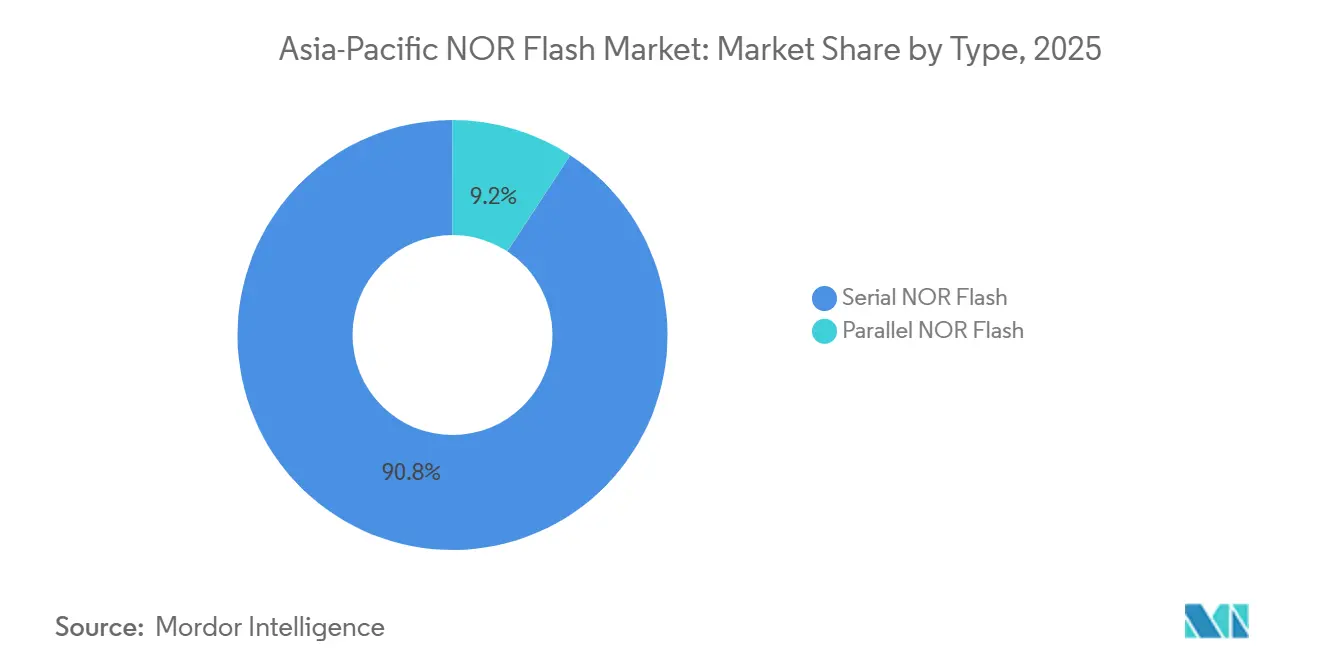

- By type, Serial NOR Flash led with 71.8% of the Asia-Pacific NOR Flash market share in 2025, while Parallel NOR Flash is projected to post a 7.3% CAGR through 2031.

- By interface, SPI Single/Dual accounted for 47.6% share of the Asia-Pacific NOR Flash market in 2025, whereas Octal and xSPI variants are set to advance at a 9.6% CAGR to 2031.

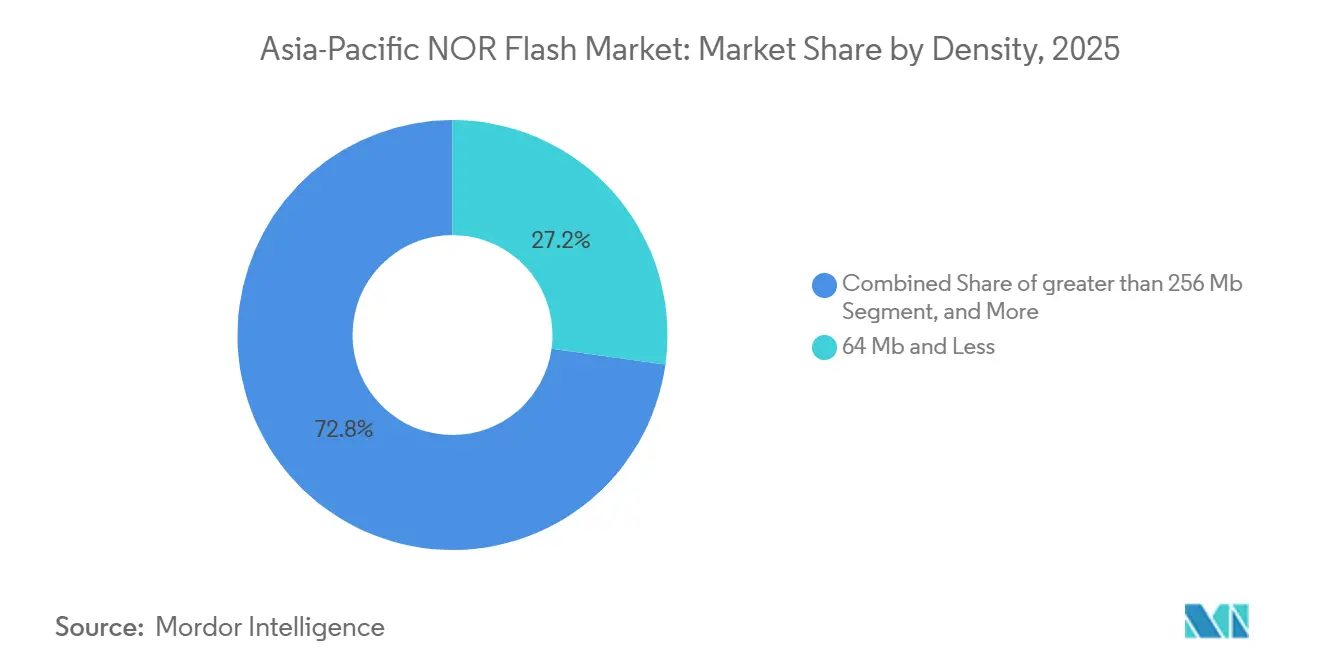

- By density, the 64-Megabit-and-less bracket captured 27.2% of the Asia-Pacific NOR Flash market size in 2025, while parts above 256 Megabit are slated to expand at a 10.9% CAGR over 2026-2031.

- By voltage, the 3 Volt class held a 44.1% of the Asia-Pacific NOR Flash market share in 2025, yet Wide-Voltage (1.65-3.6 V) devices are on track for a 6.8% CAGR through 2031.

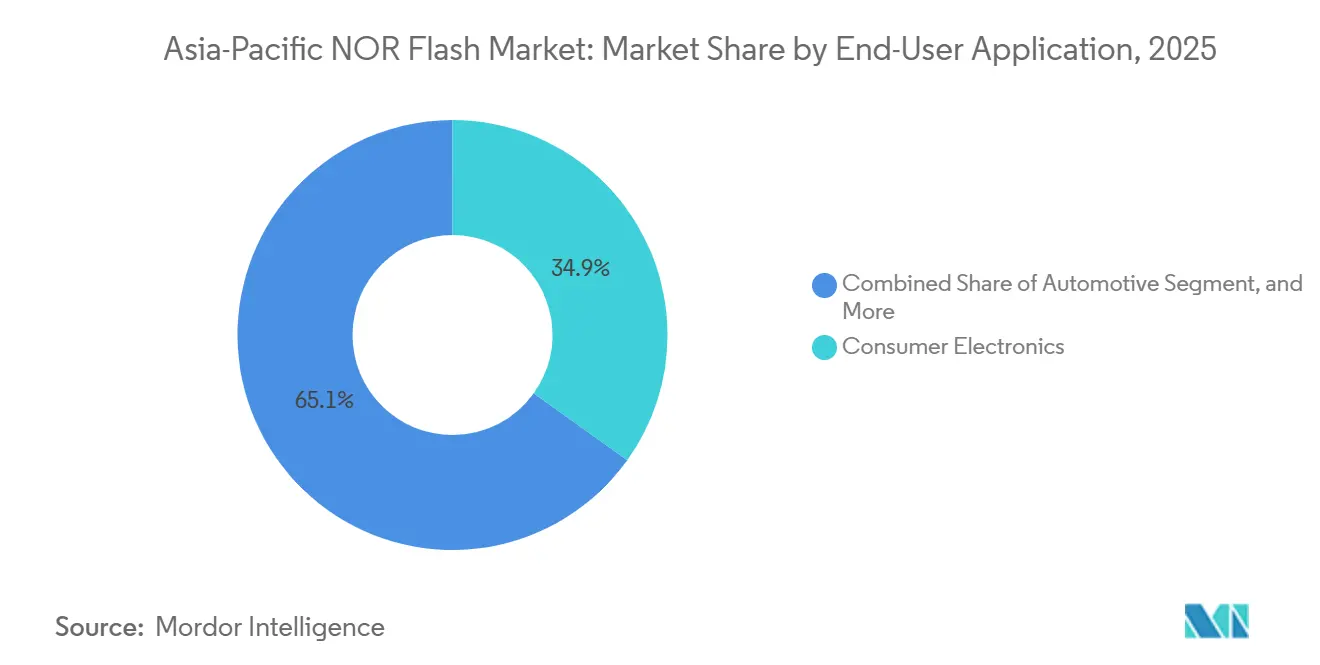

- By end-user application, consumer electronics represented 34.9% of the Asia-Pacific NOR Flash market in 2025 revenue, while automotive is poised for a 7.1% CAGR during 2026-2031.

- By process node, 55 nanometer technology commanded 31.7% share of the Asia-Pacific NOR Flash market in 2025, with 28 nanometer-and-below nodes forecast to grow at a 10.2% CAGR.

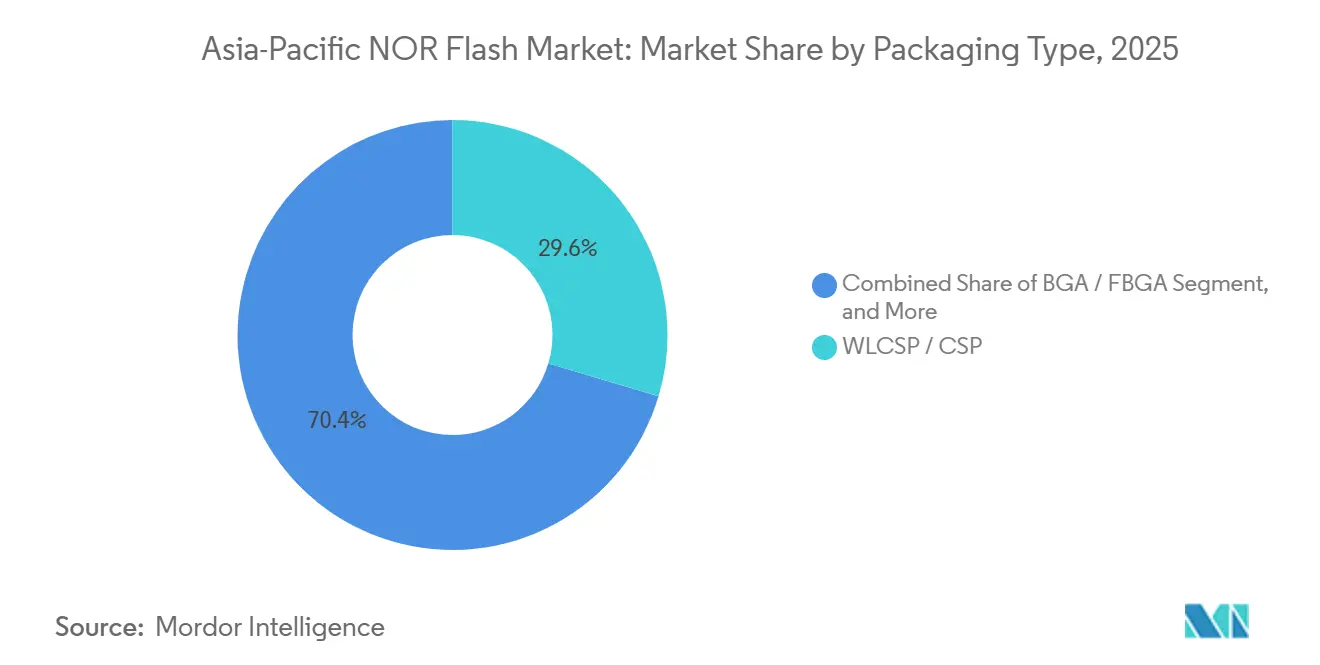

- By packaging, WLCSP/CSP formats contributed 29.6% of the Asia-Pacific NOR Flash market revenue in 2025 and BGA/FBGA packages are projected to rise at a 9.4% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Proportional positioning is established by comparing regional contributions against the global total, including that of Asia. The nor flash market share in our global report expresses these relative weights.

Asia-Pacific NOR Flash Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming ADAS and Infotainment Memory Demand in China-Japan Automotive Electronics | +1.8% | China, Japan, South Korea | Medium term (2-4 years) |

| Shift to Octal and HyperBus NOR Architectures Across Asia-Pacific Design Houses | +1.5% | Global, APAC core | Short term (≤ 2 years) |

| Chip-Self-Sufficiency Incentives in China and India | +1.2% | China, India | Long term (≥ 4 years) |

| OLED-Centric Smartphone Designs Pushing High-Density Serial NOR | +0.9% | China, South Korea | Medium term (2-4 years) |

| IoT Manufacturing Clusters in ASEAN Requiring Low-Power Code Storage | +0.6% | ASEAN | Medium term (2-4 years) |

| Industry 4.0 Upgrades in Taiwan and South Korea Industrial Automation | +0.5% | Taiwan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Booming ADAS and Infotainment Memory Demand in China-Japan Automotive Electronics

Automotive systems in China and Japan increasingly rely on redundant NOR arrays for safe-boot and fail-operational functions, pushing average vehicle content from 32 megabits in 2024 to a projected 128 Megabits by 2028.[1]China Semiconductor Industry Association, “China Semiconductor Self-Sufficiency Report,” csia.net.cn Japanese Tier-1 suppliers embed dual-channel NOR to achieve ISO 26262 ASIL-D compliance. Infineon’s SEMPER devices qualified with Renesas R-CAR Gen4 in 2025, evidencing the two-to-three-year design-win horizon common in this market.[2]Infineon Technologies AG, “SEMPER X1 NOR Flash,” infineon.com ADAS alone already represents more than half of automotive NOR revenue in the region. With China delivering 27 million vehicles in 2025 and electrification rising, the segment anchors long-term demand.

Shift To Octal and HyperBus NOR Architectures Across Asia-Pacific Design Houses

Octal and xSPI interfaces delivered only 15-18% of 2025 volumes yet are scaling fast on the back of bandwidth needs above 400 MB/s in edge-AI and automotive gateway controllers. Infineon introduced an LPDDR-compatible NOR in March 2026, doubling read throughput to 800 MB/s and simplifying routing. GigaDevice’s 1.2 V Octal parts serve battery-powered IoT nodes, cutting active current by up to 40%. As Taiwanese and Korean design houses migrate edge-AI accelerators to xSPI, suppliers secure multi-year, higher-margin contracts that offset consumer-electronic price pressure.

Chip-Self-Sufficiency Incentives in China and India

China earmarked roughly CNY 150 billion (USD 22.17 billion) for memory fabs, lifting domestic vendors such as GigaDevice to 15% local share in 2025. India’s INR 1.2 lakh-crore (USD 12.62 Billion) Production-Linked Incentive, however, has yet to spawn a discrete NOR fab, leaving the country import-dependent until at least 2028.[3]Ministry of Electronics and Information Technology, “India Semiconductor Mission 2.0,” meity.gov.in Wuhan XMC and Puya expand 12-inch capacity but face advanced-tool restrictions, making 28-nanometer migration costly. The policy mix is therefore accelerating sub-40-nanometer supply in China while maintaining high-reliability demand for Taiwanese and Japanese parts.

OLED-Centric Smartphone Designs Pushing High-Density Serial NOR

OLED display controllers need external NOR to store gamma tables, touch firmware, and secure boot code, lifting density demand above 256 megabits. Macronix launched a 1 Gigabit secure-boot part in August 2025 aimed at flagship Chinese smartphones, integrating hardware root of trust. Samsung Display began co-designing OLED modules with dedicated NOR sockets to cut boot latency by up to 20%.[4]Samsung Display, “OLED Display Technology Whitepaper,” samsungdisplay.comThe segment remains capped at 2 Gigabit, beyond which serial NAND economics dominate, yet high-density NOR’s execute-in-place advantage will sustain a growing value niche.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-Control Curbs on EUV and DUV Tools Into Mainland China | -1.3% | China, spillover to ASEAN | Medium term (2-4 years) |

| 12-Inch Foundry Tightness in Taiwan Driving Price Volatility | -1.1% | Global, Taiwan foundry-dependent regions | Short term (≤ 2 years) |

| Escalating 28 nm and 22 nm NOR R&D Capex Versus Mainstream Logic Lines | -0.7% | Taiwan, South Korea, China | Long term (≥ 4 years) |

| Low-Cost NAND and ReRAM Cannibalization in Shenzhen Design Wins | -0.6% | China, ASEAN | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Export-Control Curbs on EUV and DUV Tools Into Mainland China

Expanded Foreign Direct Product Rule measures implemented in October 2024 bar advanced lithography shipments to Chinese memory fabs, limiting mainland processes to 40-nanometer and older for the foreseeable future. Automotive-grade NOR at 28 nanometers promises 30-40% power savings, so the restriction hampers mainland suppliers seeking vehicle design wins. Japan’s alignment with U.S. policy cut access to Tokyo Electron etch systems, reinforcing the technology split: Taiwan and South Korea advance to 22 nanometers while China remains at mature nodes.

12-Inch Foundry Tightness in Taiwan Driving Price Volatility

TSMC and UMC increased mature-node wafer prices by 5-20% during 2025, with further hikes anticipated in late 2026. This price escalation has significantly impacted industries reliant on mature nodes, particularly the automotive sector. Winbond’s 12-inch production lines are already fully booked through 2027, leaving limited options for additional capacity. Spot prices for certain memory densities surged by over 30% month-over-month in early 2026, compelling automotive Tier-1 suppliers to maintain six-to-nine-month safety stock to mitigate risks. The situation is further exacerbated by the delayed arrival of new capacity from Macronix, which is not expected until mid-2027. This delay is likely to prolong the volatility in the market, creating challenges for stakeholders dependent on stable supply chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Serial NOR Consolidates Design Wins

Serial NOR retained 71.8% of the Asia-Pacific NOR Flash market share in 2025, as SPI and Quad SPI interfaces satisfy most consumer and IoT boot-code needs. Parallel NOR, although only 28.2% of revenue, benefits from a 7.3% CAGR driven by deterministic-latency requirements in industrial control and safety-critical automotive modules. Parallel devices remain embedded in airbags and ABS, where sub-50 ns access cannot be compromised.

In response, serial suppliers add hardware root-of-trust and redundancy to challenge parallel incumbents, foreshadowing tighter competition in the next platform refresh. Serial architectures are also creeping upward in density and reliability. Macronix’s ArmorBoot MX76 brings 1 Gigabit secure-boot capability, showing that execute-in-place and security, once exclusive to parallel NOR, can migrate to serial designs. Suppliers that fail to offer these enhancements risk confinement to cost-sensitive consumer devices, where price wars with Chinese entrants squeeze margins.

By Interface: Quad SPI Maturity Versus Octal Disruption

SPI Single/Dual dominated the market with a 47.6% share in 2025. However, its bandwidth ceilings, capped at approximately 80 MB/s, restrict its application in data-intensive systems. Despite this limitation, it remains a preferred choice for cost-sensitive applications where high-speed performance is not critical. Quad SPI, holding around 35% of the market share, is at a pivotal stage, catering to mid-range smartphones and industrial gateways that require faster firmware updates. Meanwhile, Octal and xSPI interfaces, though accounting for less than 20% of total units, are experiencing significant growth. These advanced interfaces are growing at a 9.6% CAGR, driven by increasing demand for automotive Ethernet gateways and edge-AI accelerators that require read performance of up to 800 MB/s.

Interface fragmentation is playing a critical role in shaping supplier roadmaps. Taiwanese design houses are quickly adopting xSPI interfaces and securing multiyear commitments from automotive clients, helping stabilize their revenue streams. Manufacturers of legacy appliances and white goods continue to rely on SPI Single/Dual interfaces. This choice is primarily driven by the need to minimize controller pin counts and ensure cost efficiency. As a result, mature interfaces like SPI Single/Dual maintain a long revenue tail, supported by their relevance in applications where advanced performance is not a priority.

By Density: 64 Megabit Anchor Versus 256 Megabit-Plus Surge

Devices at 64 megabits or below accounted for 27.2% of the Asia-Pacific NOR Flash market in 2025, driven by the widespread use of low-cost microcontrollers across various applications. These devices remain popular due to their affordability and compatibility with legacy systems. However, densities above 256 megabits are growing rapidly, with a CAGR of 10.9%, as OLED smartphones, ADAS controllers, and edge-AI modules increasingly require larger firmware storage. Macronix’s 1 Gigabit ArmorBoot technology supports isolated secure partitions for over-the-air updates, encouraging flagship smartphones to adopt half-gigabit NOR footprints. This trend highlights the growing demand for higher-density NOR Flash in advanced applications.

Mid-tier densities, ranging from 128 to 256 megabits, strike a balance between cost and capacity, making them ideal for automotive infotainment systems and industrial human-machine interfaces (HMIs). These densities cater to applications that require moderate storage without significantly increasing costs. 2-8 Megabit parts continue to find use in ultra-low-cost sensors, where minimal storage is sufficient. However, these lower-density parts are gradually losing market share each year to embedded flash solutions integrated within system-on-chips, which offer better performance and efficiency for modern applications.

By Voltage: 3 Volt Legacy Versus Wide-Voltage Flexibility

The 3 Volt class still accounted for 44.1% of 2025 revenue, as many legacy boards in consumer appliances and automotive body modules continue to rely on 3.3 V rails for their operations. Despite advancements in technology, these older systems remain prevalent, driving demand for 3 Volt components. Wide-Voltage (1.65-3.6 V) parts, which are projected to grow at a 6.8% CAGR, are gaining traction due to their suitability for IoT gateways and battery-powered devices that experience fluctuating power supply. GigaDevice’s 1.2 V Octal NOR technology has extended coin-cell battery life to over two years, making it an attractive option for wearable devices. This innovation highlights the growing demand for energy-efficient solutions in the market.

Manufacturers are increasingly adopting wide-voltage variants to streamline their product portfolios and reduce SKU proliferation. However, the adoption rate in automotive and industrial sectors remains slow due to the lengthy qualification cycles required for these applications. As a result, the market is expected to continue supporting multiple voltage classes for the foreseeable future. This trend underscores the need for manufacturers to balance innovation with compatibility to meet the diverse requirements of various end-user industries.

By End-User Application: Consumer Scale Meets Automotive Growth

Consumer electronics accounted for 34.9% of 2025 revenue, driven by consistent demand for smartphones, tablets, and wearables. However, intense price competition and the growing substitution of NOR flash with NAND flash have limited the segment's growth potential. Automotive applications are projected to grow at a 7.1% CAGR, driven by the proliferation of Level 2+ ADAS platforms that require multiple redundant code storage points. Additionally, the communications infrastructure segment, which contributes approximately one-fifth of revenue, is benefiting from ongoing 5G rollouts in regions such as India and ASEAN, further supporting market expansion.

Industrial automation upgrades in advanced manufacturing hubs such as Taiwan and South Korea are driving demand for deterministic-latency NOR flash, which is critical for real-time operations. Meanwhile, the medical and aerospace sectors are increasingly adopting extended-temperature and radiation-hardened NOR flash components, which are essential for harsh operating environments. These specialized parts command a significant premium, often 3-5× higher than standard components, reflecting their value in high-reliability applications.

By Process Technology Node: Advanced Nodes Unleash Density Economics

The 55-nanometer node led with a 31.7% share in 2025, offering proven yield and broad foundry support. This node remains a preferred choice for many applications due to its balance of cost efficiency and performance. Meanwhile, sub-28-nanometer nodes are witnessing a 10.2% CAGR, driven by the demand for automotive microcontrollers requiring lower standby power. Microchip’s 28-nanometer SuperFlash technology, which achieves 100,000 cycles and AEC-Q100 Grade 1 qualification, highlights the industry's focus on reliability and advanced features. These advancements are critical as the automotive sector increasingly adopts sophisticated electronic systems.

Chinese fabs are restricted to 40-nanometer nodes due to export-control limitations, which has solidified Taiwan and South Korea as the primary suppliers of advanced automotive NOR technology. This restriction has created a significant technological gap, limiting China's ability to compete in cutting-edge processes. In contrast, companies like Winbond are planning to migrate to 16-nanometer technology, further widening the disparity. Such advancements in Taiwan and South Korea are expected to strengthen their dominance in the global semiconductor market. These developments underline the critical role of geopolitical factors in shaping the semiconductor supply chain.

By Packaging Type: WLCSP Cost Efficiency Versus BGA Thermal Performance

WLCSP/CSP accounted for 29.6% of the market share in 2025, driven by the demand for slim-form-factor solutions in smartphones and wearables. These packaging technologies cater to the miniaturization needs of modern consumer electronics. Meanwhile, BGA/FBGA is projected to grow at a CAGR of 9.4%, offering superior thermal management capabilities essential for Octal NOR devices operating above 133 MHz in high-temperature automotive environments. QFN/SOIC packages continue to hold significance due to their compatibility with through-hole assembly lines, which are still widely used in white goods manufacturing. The diverse applications of these packaging types highlight their importance across various industries.

Advanced fan-out tools for WLCSP are increasingly overlapping with RF device requirements, creating additional complexities in the supply chain. This overlap becomes particularly challenging when mature-node wafer availability tightens, leading to potential bottlenecks in production. Such constraints exacerbate delivery risks, especially in scenarios where demand for these technologies surges. The reliance on advanced packaging solutions underscores the critical need for efficient supply chain management to mitigate these risks and ensure timely delivery of components.

Geography Analysis

China is a significant contributor to the Asia-Pacific NOR Flash market, driven by its position as a leading manufacturing hub for the automotive and smartphone industries. The implementation of import-substitution policies has enabled local suppliers to increase their market presence. However, domestic production still falls short in meeting the demand for automotive-grade NOR Flash. U.S. export controls have limited mainland China’s process technology, resulting in continued reliance on Taiwanese components for high-reliability modules. This dependency underscores the challenges China faces in achieving self-sufficiency in advanced NOR Flash production.

Taiwan remains a central hub for NOR Flash production, with key players operating at full capacity to meet strong demand. While government incentives support technological advancements, extended lead times for wafer tooling are expected to keep capacity constrained for the foreseeable future. Japan’s market is heavily focused on automotive applications, with companies integrating redundant NOR arrays and qualifying devices for automotive-grade applications. South Korea’s NOR Flash market is divided between high-density serial NOR used in OLED displays and automotive modules supplied to local automakers.

India is experiencing growing demand for NOR Flash in electric vehicles and telecom sectors. However, the country remains entirely dependent on imports until new semiconductor fabs are established under its Production-Linked Incentive scheme. ASEAN economies, led by Vietnam, play a significant role in the region’s electronics exports. These economies primarily source NOR Flash from Taiwan and China. The overall supply chain remains concentrated in the Taiwan Strait corridor, posing significant risks to the region’s stability.

Mordor Intelligence examines the nor flash market across diverse other regional markets as well, including Europe, while also offering granular country-level perspectives for China, India, Japan, South Korea, France, Italy, United Kingdom, and Germany and more.

Competitive Landscape

The Asia-Pacific NOR Flash market demonstrates moderate concentration, with the top three players accounting for approximately 50-55% of the revenue share in 2025. Winbond and Macronix have focused on automotive and industrial design wins, each committing over USD 600 million to expand their 12-inch production capacity. Meanwhile, Chinese competitors such as GigaDevice, Puya, and XMC leverage state subsidies to offer lower prices in consumer and IoT applications. This strategy has enabled them to capture local market share, pressuring established players to retreat from low-margin segments. The competitive dynamics highlight the growing influence of Chinese suppliers in the regional market.

Interface innovation has emerged as a critical differentiator in the NOR Flash market. Infineon’s LPDDR-compatible NOR technology has secured contracts with Japanese OEMs, allowing the company to charge a 20-30% premium for its products. Process technology leadership also plays a significant role, with Winbond’s 16-nanometer roadmap targeting 2028 vehicle platforms. This positions the company ahead of ReRAM competitors, which are still maturing. Suppliers that lack automotive-grade certification face challenges, as they risk being confined to segments where alternatives like serial NAND or MRAM can replace NOR at a lower cost. The emphasis on innovation underscores the importance of technological advancements in maintaining a competitive edge.

Consolidation trends are becoming increasingly evident in the NOR Flash market. For instance, Renesas’ acquisition of Adesto Technologies has allowed the company to integrate NOR Flash into its broader microcontroller portfolios. This move reflects a growing trend among major players to diversify their offerings and strengthen their market positions. Additionally, the focus on automotive-grade certifications and advanced process technologies is driving further consolidation, as smaller players struggle to keep up with the high costs of innovation. These trends indicate a shift toward a more consolidated market structure, with leading players leveraging acquisitions to enhance their capabilities and expand their market share.

Asia-Pacific NOR Flash Industry Leaders

Winbond Electronics Corp.

GigaDevice Semiconductor Inc.

Macronix International Co., Ltd.

Micron Technology Inc.

Infineon Technologies AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: GigaDevice launched 1.2 V Octal NOR in 8-256 Megabit densities targeting ultra-low-power IoT nodes.

- March 2026: Infineon unveiled SEMPER X1 NOR with an LPDDR physical layer, achieving 800 MB/s throughput for automotive Ethernet gateways.

- January 2026: Microchip introduced 28 nanometer SuperFlash Gen 4 embedded NOR for automotive microcontrollers, cutting standby current by 35%.

- January 2026: Macronix committed NTD 22 billion (USD 680 million) to lift 12-inch capacity to 30,000 wafers per month by Q4 2026.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Asia-Pacific NOR flash memory market as all newly manufactured serial and parallel NOR devices shipped into China, Japan, South Korea, Taiwan, India, and the wider region for code-storage or fast-boot uses across consumer, automotive, industrial, and communications equipment. According to Mordor Intelligence, figures are expressed in factory-gate revenue, so resale mark-ups and refurbished units are kept out of scope.

Scope Exclusions: NAND flash, NOR-emulated eMMC, and emerging ReRAM, MRAM, or 3D-XPoint devices are excluded.

Segmentation Overview

- By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less NOR

- 4 Megabit and Less (greater than 2 MB) NOR

- 8 Megabit and Less (greater than 4 MB) NOR

- 16 Megabit and Less (greater than 8 MB) NOR

- 32 Megabit and Less (greater than 16 MB) NOR

- 64 Megabit and Less (greater than 32 MB) NOR

- 128 Megabit and Less (greater than 64 MB) NOR

- 256 Megabit and Less (greater than 128 MB) NOR

- Greater than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V - 3.6 V)

- Others - 1.2 V Class (and similar sub-1.8 V: 2.5 V, 5 V)

- By End-User Application (Value, Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other End-User Applications

- By Process Technology Node (Value)

- 90 nm and Older

- 65 nm

- 55 nm (including 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

- By Geography

- China

- Japan

- South Korea

- Taiwan

- India

- Rest of Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with foundry engineers, memory-marketing managers, channel distributors, and contract EMS buyers across Greater China, Japan, India, and ASEAN. Their insights confirmed density-mix shifts, refreshed price curves, and highlighted niche automotive and industrial IoT use cases that desk research alone would overlook.

Desk Research

We opened with public data from WSTS semiconductor statistics, customs import ledgers in China and India, and shipment dashboards from JEITA and the Korea Semiconductor Industry Association. Peer-reviewed IEEE papers, central-bank exchange rates, and trade-association white papers enriched the historical view. Company 10-Ks, investor decks, and press releases refined average selling prices and mapped new fab ramps, while proprietary feeds from D&B Hoovers and Dow Jones Factiva let us double-check vendor revenue splits and capacity additions. The sources listed are illustrative; many more were referenced during data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down build starts with WSTS unit shipments aligned with country-level import volumes; these are multiplied by segmented ASP curves and then filtered through end-use penetration rates. Selective bottom-up checks, supplier roll-ups, and distributor channel calls help us refine totals. Smartphone output, vehicle production with ADAS content, industrial-robot installations, SPI-to-Octal interface adoption, and 55 nm wafer utilization are the model's key fingerprints. Forecasts rely on multivariate regression, which we stress-test with scenario analysis; interview-based anchor ratios close any remaining gaps.

Data Validation & Update Cycle

Outputs face a three-step peer review, anomaly thresholds trigger reruns, and the file refreshes every twelve months. Interim tweaks are issued when plant outages, currency shocks, or major design wins materially shift the baseline.

Why Our Asia-Pacific NOR Flash Baseline Earns Trust

Published estimates often diverge because publishers vary device scope, price assumptions, and refresh cadence.

By focusing strictly on NOR shipments, applying live ASP curves, and updating yearly, we limit those distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.88 Billion (2025) | Mordor Intelligence | - |

| USD 4.20 Billion (2024) | Global Consultancy A | Combines NOR with small SLC NAND volumes; biennial refresh |

| USD 2.80 Billion (2023) | Industry Portal B | Uses shipment × global ASP without local currency or channel checks |

| USD 0.91 Billion (2021) | Regional Analyst C | Focuses on industrial-grade chips only; older base year |

The comparison shows that Mordor's disciplined scope, device-level variables, and timely refresh provide a balanced, transparent baseline that decision-makers can retrace and rely on.

Key Questions Answered in the Report

What is the current size of the Asia-Pacific NOR Flash market and how fast is it projected to grow?

The Asia-Pacific NOR Flash market size stands at USD 1.99 billion in 2026 and is forecast to reach USD 2.65 billion by 2031, advancing at a 5.9% CAGR .

Which end-use sector is expected to post the strongest growth through 2031?

Automotive electronics is projected to register the fastest rise, expanding at a 7.1% CAGR on the back of ADAS and over-the-air update requirements.

How much larger is serial NOR compared with parallel NOR today?

Serial NOR commanded 71.8% share in 2025, while parallel NOR accounted for the remaining 28.2%.

Why are Octal and xSPI interfaces attracting design wins across the region?

They deliver up to 800 MB/s read bandwidth that edge-AI accelerators and automotive gateway controllers need, driving a 9.6% CAGR for these interfaces.

What supply-chain risks should sourcing teams monitor over 2026-2027?

Tight 12-inch foundry capacity in Taiwan and export-control limits on advanced lithography keep lead times long and pricing volatile, especially for 55 nm and 40 nm nodes.

How concentrated is the supplier landscape?

The top three vendors-Winbond, Macronix and GigaDevice, hold roughly 50-55% regional revenue, reflecting moderate concentration that still leaves room for challengers.

Page last updated on: