Czech Republic Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

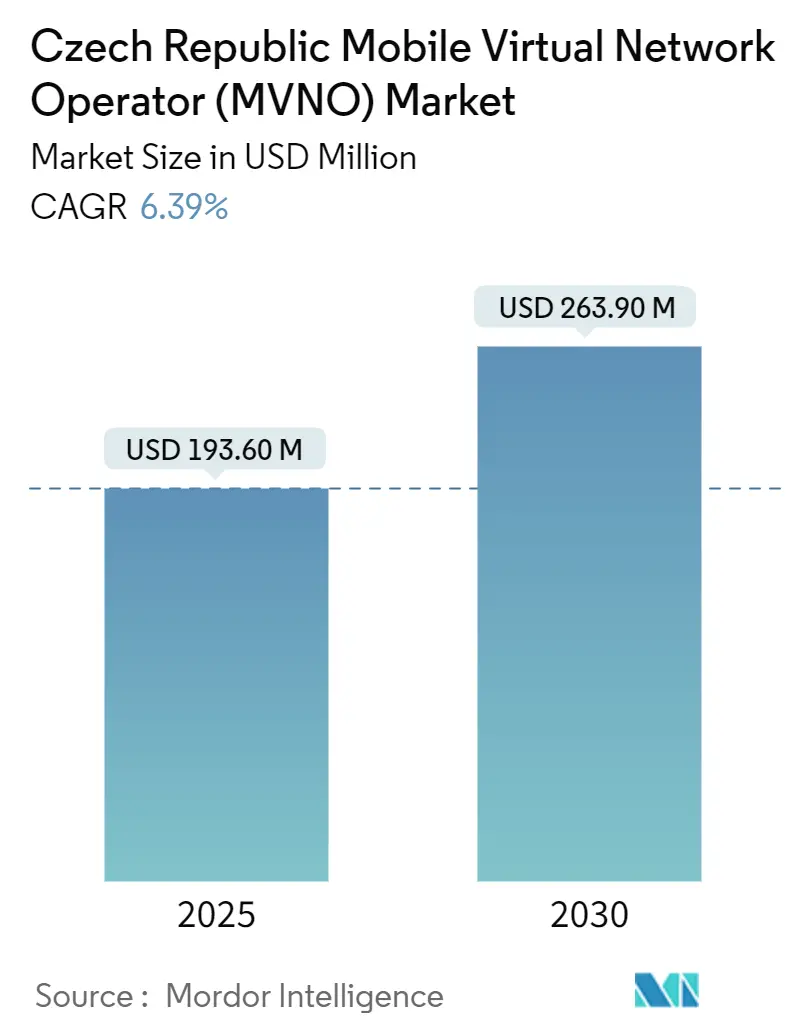

| Market Size (2025) | USD 193.60 Million |

| Market Size (2030) | USD 263.90 Million |

| Growth Rate (2025 - 2030) | 6.39% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Czech Republic Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

The Czech Republic Mobile Virtual Network Operator Market size is estimated at USD 193.60 million in 2025, and is expected to reach USD 263.90 million by 2030, at a CAGR of 6.39% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 1.02 million subscribers in 2025 to 1.35 million subscribers by 2030, at a CAGR of 5.80% during the forecast period (2025-2030). Strong demand for budget-friendly plans, rapid 5G deployment, and streamlined wholesale regulation underpin this growth even as margin pressure from oligopolistic pricing persists. The cloud-centric operating model, accounting for almost three-quarters of active platforms, lowers entry barriers and supports quick service launches. Full MVNOs gain traction because deeper network control improves differentiation, while IoT connectivity adoption opens new revenue streams in manufacturing hubs. Digital-only distribution and eSIM uptake reinforce the channel shift that began during the pandemic, enabling virtual brands to scale nationally without a store footprint.

Key Report Takeaways

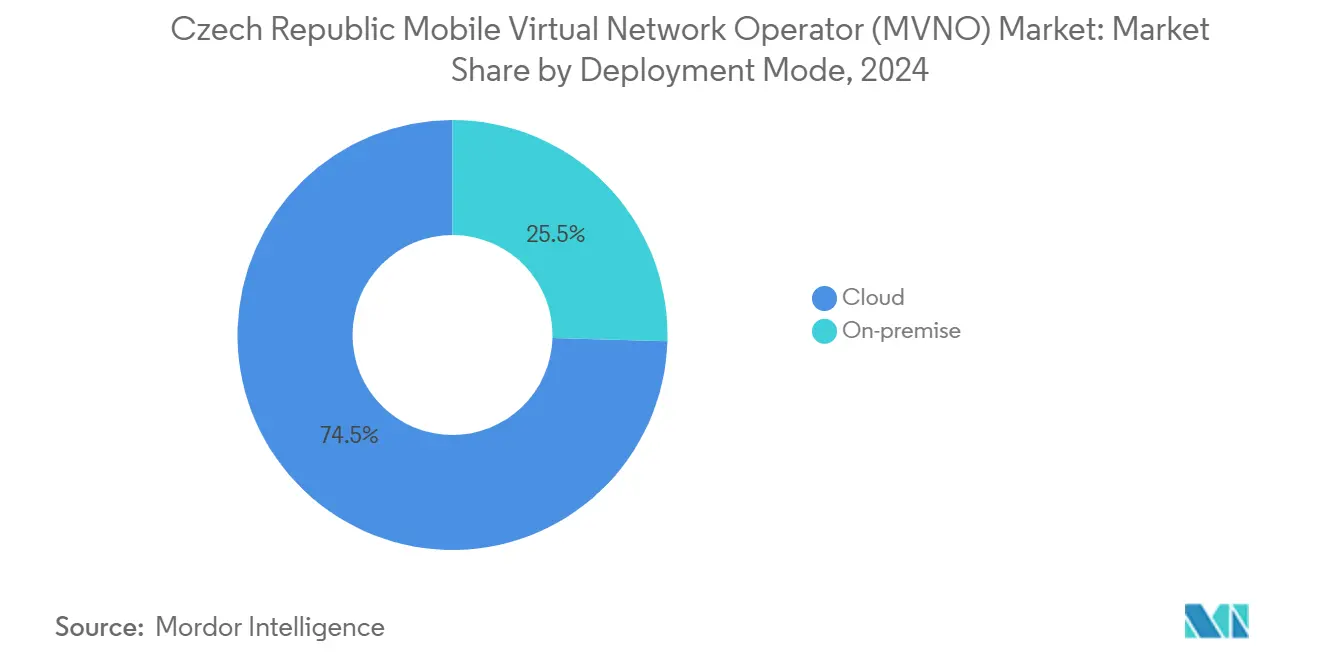

- By deployment, cloud secured 74.54% of the Czech Republic's MVNO market share in 2024, and the segment is expected to advance at a 9.78% CAGR through 2030.

- By operational mode, full MVNOs are growing at a 16.44% CAGR, whereas reseller and light models held the largest 54.22% share in 2024.

- By subscriber type, consumer subscribers accounted for 77.89% of the Czech Republic's MVNO market size in 2024, while IoT SIMs are expected to expand at a 23.66% CAGR to 2030.

- By application, discount propositions captured a 41.09% revenue share in 2024; cellular M2M lines are projected to grow at a 17.73% CAGR over the forecast period.

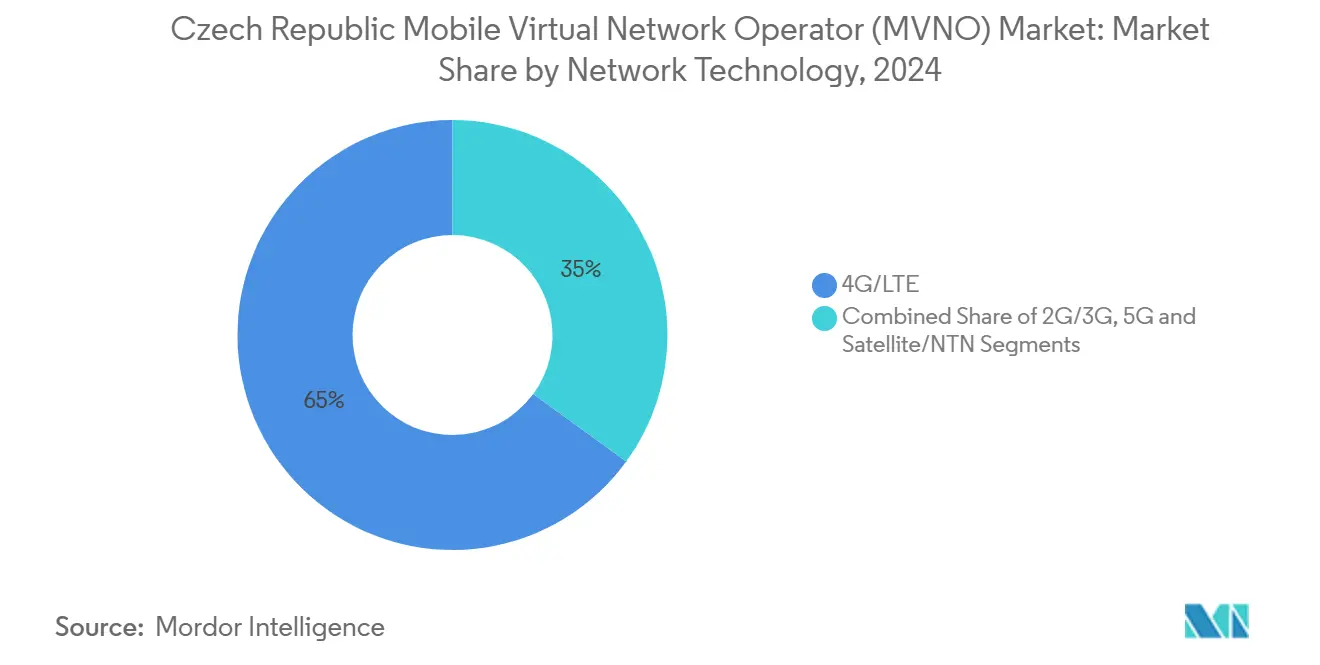

- By network technology, 4G/LTE supported 64.98% of active connections in 2024; 5G connections are rising at 24.42% CAGR thanks to 90% population coverage across all host networks.

- By distribution channel, online and digital-only channels delivered 56.35% of 2024 gross adds and remain the fastest-growing route at a 10.58% CAGR.

Czech Republic Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-driven wholesale-access mandates | +1.8% | Nationwide, linked to EU rules | Medium term (2-4 years) |

| Consumer shift toward low-cost flexible plans | +1.5% | Urban corridors | Short term (≤ 2 years) |

| 5G coverage enabling data-centric offers | +1.2% | Country-wide, Prague leads | Medium term (2-4 years) |

| Enterprise and IoT SIM adoption | +0.9% | Industrial regions | Long term (≥ 4 years) |

| Retail-lottery cross-sell model | +0.6% | Hypermarkets and lottery outlets | Short term (≤ 2 years) |

| 5G network slicing for vertical MVNOs | +0.4% | Enterprise corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU-driven wholesale-access mandates

Regulatory action anchored in the European Electronic Communications Code continues to safeguard cost-oriented wholesale access for new entrants. The Czech Telecommunications Office applies a three-criteria test before lifting price controls, and its 2025 review confirmed the need for sustained oversight to stop tacit collusion among the three host MNOs.[1]Czech Telecommunications Office, “Wholesale Mobile Access Market Review 2025,” ctu.cz BEREC’s 2025 consultation on intra-EU call charges also highlights the burden of high transit rates on small MVNOs, prompting debate on simplified rule-making that favors virtual operators.[2]BEREC, “BoR (24) 76: Intra-EU Communications Consultation,” berec.europa.eu Together, these initiatives reinforce predictable input costs and open the door for brand-led entrants to scale nationally. They also compel MNOs to publish transparent reference offers, shortening negotiation cycles. The outcome is a clear positive swing in entry viability that encourages investment, especially for cloud-native platforms able to launch within weeks.

Consumer shift toward low-cost flexible plans

Forty percent of Czech mobile users buy tariffs priced below headline rates, revealing pronounced price sensitivity that virtual brands exploit through digital channels.[3]Michal Marek, “Czech Families Hunt for Cheaper Tariffs,” ihned.cz Unlimited data continues to replace capped bundles; O2 disclosed that such plans formed 44% of 2025 activations, with a matching rise in monthly data traffic. MVNOs like Kaktus respond by introducing no-commitment packages that bundle voice, data, and OTT chat without credit checks. Younger users regard mobile service as a commodity, intensifying the race to strip out overhead and pass savings to subscribers. These forces keep churn high and ensure continued demand for discount propositions that support the Czech Republic MVNO market.

5G coverage enabling data-centric offers

All three host networks surpassed 90% population coverage with 5G by early 2025, creating a nationwide platform for advanced MVNO services. Vodafone leads at 93.7%, while O2’s 5G upgrade in North Moravia added 618 base stations and introduced full coverage in Prague’s metro tunnels. Wholesale access now includes network slicing pilots that let full MVNOs reserve bandwidth for premium tiers or latency-sensitive use cases such as cloud gaming. The government’s Very High Capacity Networks plan channels CZK 11.5 billion in public funds to close rural gaps, meaning future buyer segments will experience uniform performance. Resulting improvements support the Czech Republic MVNO market as operators craft differentiated data bundles and upsell converged fixed-mobile products.

Enterprise and IoT SIM adoption

LoRaWAN coverage already reaches 80% of residents after ČRa and Netmore extended gateways across utility corridors. Manufacturing, logistics, and smart-building projects are shifting to managed connectivity that full MVNOs can deliver with customized SLAs. Global forecasts place IoT MVNO connections at 658 million by 2025, outpacing traditional consumer growth and validating the segment’s potential. Czech firms embrace predictive maintenance and energy management, spurring demand for bulk SIM provisioning tools and remote lifecycle management. MVNOs that own their core can integrate API-driven activation and monetize data analytics, turning what was once a low-ARPU niche into a margin-accretive business. Over time these enterprise wins reshape revenue mix and lift the Czech Republic MVNO market beyond price competition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oligopolistic wholesale pricing | -1.4% | Across all MVNOs | Short term (≤ 2 years) |

| Slow eSIM enablement for MVNO brands | -0.8% | Urban centers adopt faster | Medium term (2-4 years) |

| MNO acquisition wave reducing independents | -0.6% | Large MVNOs in consolidation spotlight | Short term (≤ 2 years) |

| Scarce private band and NTN spectrum access | -0.4% | Rural and industrial coverage gaps | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Oligopolistic wholesale pricing

A three-player host market lets MNOs maintain tight control over visitor traffic fees despite regulatory monitoring. CTU’s 2025 review noted repeated attempts to embed punitive data overage rates in reference offers, eroding MVNO margin potential. Data-heavy bundles feel the most pressure, forcing many virtual brands to cap speeds or impose fair-use rules. Where renegotiations fail, some operators exit loss-making tiers, narrowing consumer choice. Although upcoming price ceilings on roaming-like wholesale access are expected to help, the near-term squeeze slows innovation and curbs upside for the Czech Republic MVNO market.

MNO acquisition wave reducing independents

Vodafone’s 2024 purchase of SAZKAmobil removed the country’s biggest standalone MVNO and raised the host’s retail base by 200,000 lines. Similar deals are rumored for other high-growth brands, echoing wider European consolidation. Each takeover eliminates a price-aggressive competitor, steering prepaid customers back into incumbent bundles. The Office for the Protection of Competition now attaches strict wholesale obligations to such mergers, yet integration still dulls the disruptive edge of virtual entrants. Fewer independent players could cap subscriber churn and temper the velocity of market-wide tariff reductions, softening overall growth of the Czech Republic MVNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Scalability

Cloud deployment held 74.54% of the Czech Republic MVNO market share in 2024 and the category is expanding at a 9.78% CAGR. Its appeal stems from pay-as-you-grow economics that align costs with customer acquisition pace. Vendors bundle OSS/BSS, policy, and analytics, making feature launches faster than on-premise builds. Cloud cores also support CI/CD pipelines that cut time-to-market for new tariffs from months to days.

On-premise solutions still matter for segments governed by strict data containment rules, including financial services and critical infrastructure clients. GDPR and local cybersecurity law prompt some enterprises to keep sensitive subscriber data inside private racks. These operators often adopt hybrid designs that isolate customer databases while sourcing signaling and billing from the cloud. Even so, most new entrants default to full SaaS platforms, suggesting cloud will keep steering the Czech Republic MVNO market.

By Operational Mode: Full MVNOs Emerge Despite Reseller Dominance

Reseller and light variants delivered 54.22% of 2024 revenue, reflecting low complexity and modest capital needs. They rely on their host for critical network elements and focus spending on marketing. This structure fits retail chains and digital sub-brands targeting price-sensitive youth.

Full MVNOs, though smaller, are progressing at 16.44% CAGR and increasingly represent the innovation frontier. Owning a mobile core lets them deploy eSIM, IoT provisioning APIs, and differentiated QoS tiers unavailable to resellers. Capital costs are higher, yet cloud-native cores reduce upfront spend and shift expenses to operating budgets. Enterprises seeking device management or multi-IMSI roaming gravitate to these offers, driving the Czech Republic MVNO market size for full operators higher each year.

By Subscriber Type: Consumer Base Stable While IoT Accelerates

Consumers contributed 77.89% of 2024 lines and create steady cash flow that funds marketing and retention programs. Churn averages 2.8% per month, so brands invest in loyalty apps and bundle OTT video to lengthen tenure.

IoT SIMs, advancing at 23.66% CAGR, fuel the fastest incremental revenue. Smart meters, fleet trackers, and security sensors need predictable low-data connections, and MVNOs can undercut MNO minimum commit levels. Enterprise contracts sitting between the two segments offer higher ARPU than consumers and more predictable lifecycles than IoT, positioning them as the stabilizer that underpins longer-term expansion of the Czech Republic MVNO market.

By Application: Discount Models Lead While M2M Accelerates

Discount propositions enjoyed 41.09% of 2024 service revenue thanks to massive deal-seeking behavior in Czech urban centers. No-frills voice, SMS, and fixed-data allowances dominate this tier. Brand MVNOs tied to supermarkets gain share by marketing at checkout lines and funding user incentives with retail loyalty points.

Cellular M2M subscriptions rise 17.73% per year as manufacturers digitize assembly lines. These lines consume small payloads but run in the network for a decade, giving MVNO portfolios a high-lifetime value component. The confluence of energy-meter mandates and smart-city pilots means M2M will capture an increasing slice of the Czech Republic MVNO market size throughout the forecast horizon.

By Network Technology: 5G Momentum Builds on 4G Foundation

4G/LTE delivered 64.98% of active SIMs in 2024, providing dependable voice and broadband coverage. VoLTE interconnect enables seamless termination even for cross-network calls. 5G connections are scaling at 24.42% CAGR as all hosts migrate to SA architecture.

MVNOs can now resell speed tiers up to 1 Gbps and exploit slicing trials for event venues. Future network evolution is expected to push URLLC functions into edge clouds, opening yet another layer of differentiation that keeps the Czech Republic MVNO market vibrant.

By Distribution Channel: Digital Transformation Accelerates

Digital-only sales drove 56.35% of SIM activations in 2024 and are projected to rise at 10.58% CAGR. Simple KYC via BankID and instant eSIM downloads mean a user can switch within minutes. AI chatbots answer support queries, slashing care costs and reinforcing low-tariff economics.

Physical stores remain relevant for device bundling and elderly users seeking human advice. Hybrid shop-and-scan models combine QR code activations with take-home SIM packs. Lottery kiosks demonstrate a high-traffic niche that merges micro top-ups with impulse purchases, reflecting the creativity fueling distribution diversity inside the Czech Republic MVNO market.

Geography Analysis

Prague commands the country’s densest subscriber clusters and highest ARPU levels. The capital benefits from 100% 5G coverage inside the metro and averages 242 Mbps downlink speeds, well above the national mean. Virtual brands exploit this network quality to pitch unlimited plans bundled with streaming add-ons that appeal to commuters. The Czech Republic MVNO market size in Prague remains structurally larger than any other region because of population density and a tech-savvy workforce.

Industrial corridors stretching from Central Bohemia to Ostrava host thousands of factories that anchor enterprise and IoT demand. LoRaWAN gateways cover most industrial parks, enabling sensor deployments in logistics, mining, and automotive assembly. These regions value uptime over speed, promoting hybrid LTE-M and unlicensed spectrum solutions delivered by full MVNOs. Public funding in the Very High Capacity Networks program allocates CZK 11.5 billion for rural fiber backhaul, indirectly fostering wholesale mobile upgrades that feed the Czech Republic MVNO market.

Border areas with Poland, Austria, and Slovakia still face patchy indoor coverage. CTU’s 900 MHz and 1800 MHz license renewals tied spectrum to obligations covering 200 identified white zones by 2030. Wholesale partners gain from these new sites without capital exposure. As coverage equalizes, MVNOs can run nationwide promotions with uniform SLAs, removing a historic barrier to rural customer acquisition and unlocking fresh growth pockets for the Czech Republic MVNO market.

Competitive Landscape

Seventy-one active MVNOs share the stage, translating to moderate fragmentation by European standards. The top five brands account for roughly 48% of subscribers, keeping switching costs low and price pressure high. Vodafone’s SAZKAmobil buyout in 2024 nudged its hosted share to 26%, yet no single group exceeds one-third of total virtual lines. Tesco Mobile leverages retail footfall to drive SIM sales at checkout aisles, proving the retail-telecom convergence thesis.

Platform strategy is now a key battleground. Several operators have migrated to cloud cores on AWS or Google Cloud, gaining elasticity that supports flash-sale promotions. AI-driven churn analytics and dynamic voucher engines filter heavy data users into upsell paths. Host MNOs counter by introducing own low-cost sub-brands, hoping to repatriate value without cannibalizing flagship ARPU. Such layered positioning sustains intense rivalry that ultimately benefits the Czech Republic MVNO market.

Regulatory guardrails maintain wholesale openness, yet CTU has shown willingness to impose behavioral remedies on mergers, as in the 2024 PPF–Nordic Telecom case. These commitments include five-year wholesale guarantees that preserve access parity for smaller virtual players. The result is a competitive equilibrium where innovation, rather than outright price wars, defines success.

Czech Republic Mobile Virtual Network Operator (MVNO) Industry Leaders

SAZKAmobil

Tesco Mobile (CZ)

BLESKmobil

GoMobil

OpenCall

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: O2 Czech Republic rolled out NEO tariffs with multi-device connectivity at CZK 99 per extra line, signaling convergence ambitions.

- January 2025: CTU renewed Vodafone’s 900 MHz and 1800 MHz licenses with white-spot coverage duties benefiting wholesale customers.

- December 2024: ČRa chose Netmore’s Operator Platform-as-a-Service to expand LoRaWAN, covering 80% of residents.

Czech Republic Mobile Virtual Network Operator (MVNO) Market Report Scope

| Cloud |

| On-premise |

| Reseller |

| Service Operator |

| Full MVNO |

| Light / Brand MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Other Applications |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller |

| Service Operator | |

| Full MVNO | |

| Light / Brand MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Other Applications | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

How large is the Czech Republic MVNO market in 2025?

The Czech Republic MVNO market size is USD 193.6 million in 2025 and is set to reach USD 263.9 million by 2030.

Which deployment model dominates virtual operators in Czech Republic?

Cloud deployment leads with 74.54% market share in 2024 and continues to expand due to rapid scalability advantages.

What is the fastest-growing subscriber segment?

IoT SIMs are rising at 23.66% CAGR through 2030 as factories and utilities adopt connected devices.

How quickly is 5G being adopted by MVNO customers?

5G connections are advancing at 24.42% CAGR because all host MNOs now cover more than 90% of the population.

Which channel captures most new MVNO customers?

Online and digital-only channels account for 56.35% of activations and record the highest 10.58% CAGR.

How is regulation affecting MVNO entry?

EU-aligned wholesale rules enforced by the Czech regulator ensure transparent network access, lowering entry barriers for new MVNO brands.

Page last updated on: