Poland Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

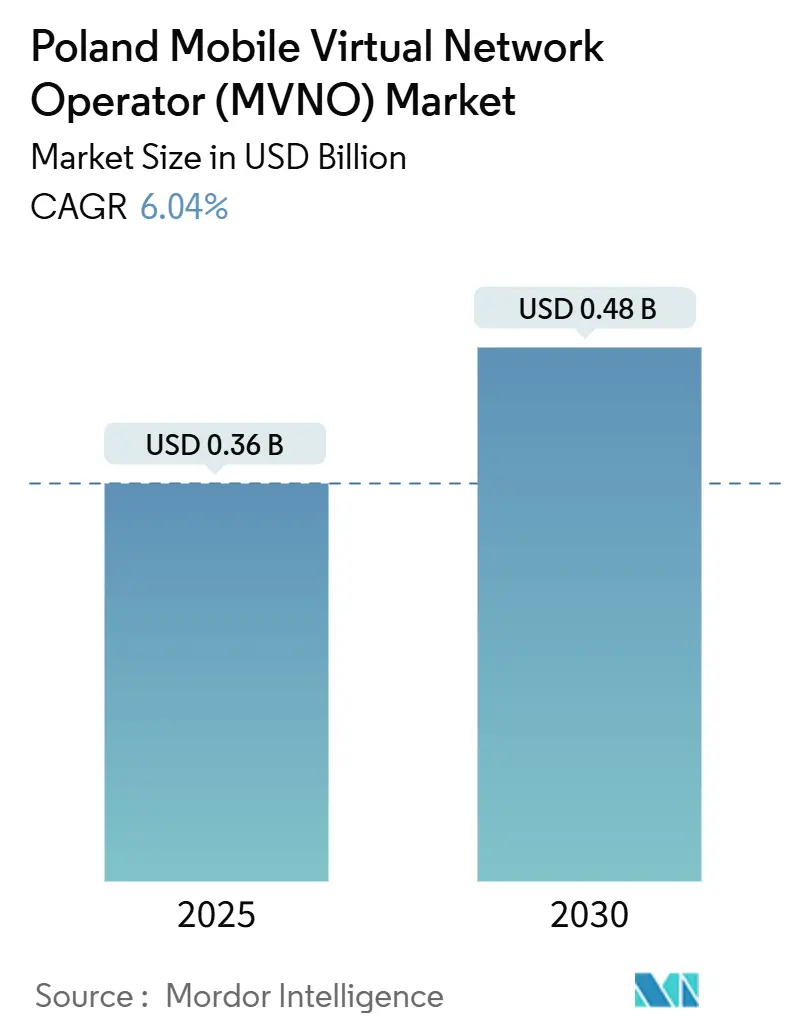

| Market Size (2025) | USD 0.36 Billion |

| Market Size (2030) | USD 0.48 Billion |

| Growth Rate (2025 - 2030) | 6.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

The Poland Mobile Virtual Network Operator Market size is estimated at USD 0.36 billion in 2025, and is expected to reach USD 0.48 billion by 2030, at a CAGR of 6.04% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 2.06 million Subscribers in 2025 to 2.71 million Subscribers by 2030, at a CAGR of 5.61% during the forecast period (2025-2030).

Heightened wholesale 5G availability, regulatory fee cuts, and the continuing price sensitivity of Polish consumers keep the growth trajectory steady even as competition tightens. Operators that deploy cloud-native cores, negotiate multi-host network deals, and embrace digital-only customer journeys are outperforming peers on time-to-market and cost control. At the same time, full-scale MVNOs that own critical core functions are positioning to monetize 5G network slicing and enterprise SLA-based contracts ahead of lighter reseller models. The convergence of satellite, 5G, and private LTE networks is opening niche but high-margin propositions in remote coverage, industrial automation, and emergency connectivity.

Key Report Takeaways

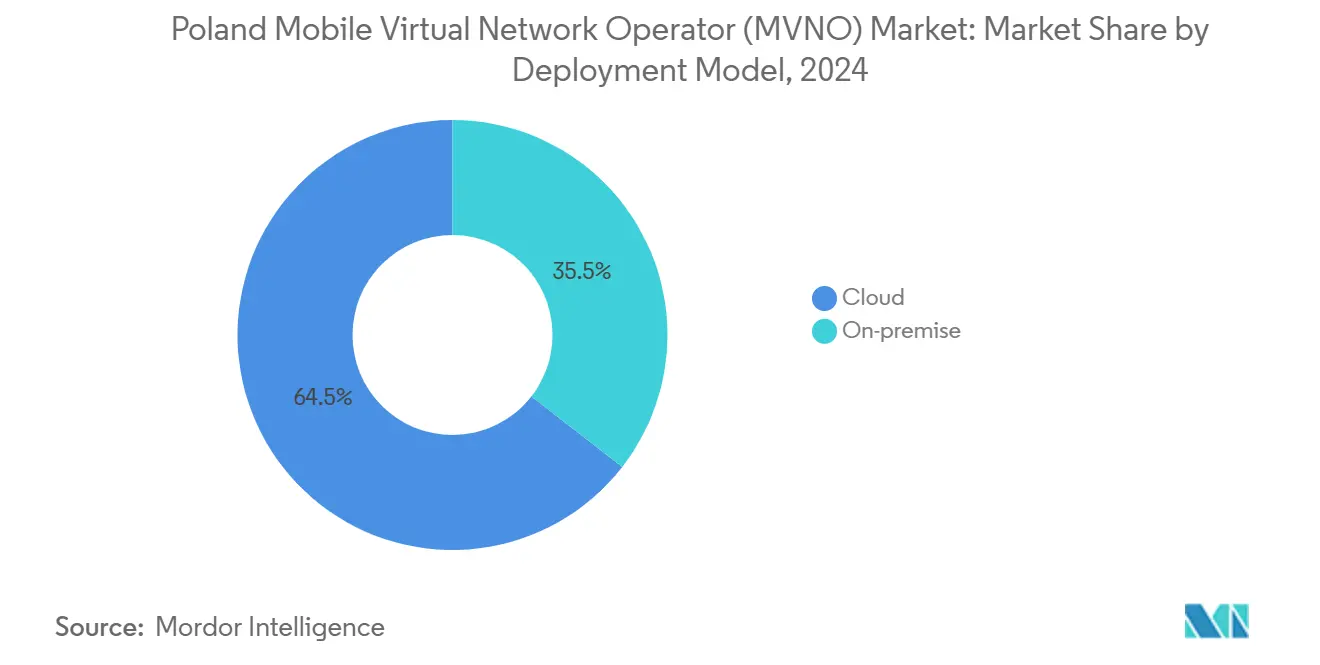

- By deployment model, cloud solutions led with a 64.47% revenue share in 2024, while on-premise deployments are projected to expand at a 9.92% CAGR through 2030.

- By operational mode, reseller/light/brand MVNOs accounted for 64.35% of the Poland MVNO market share in 2024; full MVNOs are advancing at a 21.59% CAGR to 2030.

- By subscriber type, consumer lines held 84.54% of the Poland MVNO market size in 2024, whereas IoT-specific subscriptions are growing at a 31.85% CAGR between 2025-2030.

- By application, the other category captured a 41.60% share of the Poland MVNO market size in 2024, and cellular M2M is expanding at a 27.97% CAGR.

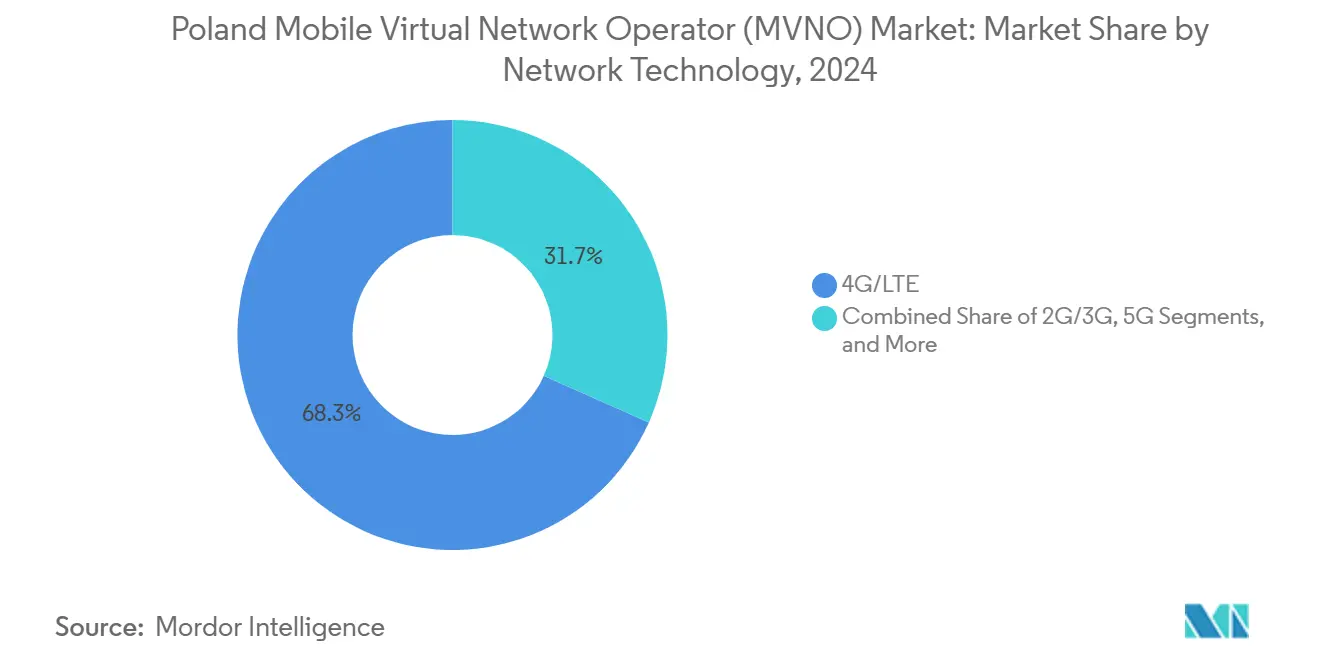

- By network technology, 4G/LTE delivered 68.33% of the Poland MVNO market share in 2024, yet satellite/NTN services are set to surge at a 101.86% CAGR.

- By distribution channel, online/digital-only sales contributed 50.20% revenue share in 2024 and are pacing ahead at 10.52% CAGR.

Poland Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for low-cost mobile connectivity | +1.8% | National (urban clusters) | Short term (≤ 2 years) |

| Expansion of 5G wholesale capacity | +1.2% | National (major cities) | Medium term (2-4 years) |

| Regulatory cuts in wholesale access fees | +0.9% | National | Short term (≤ 2 years) |

| Accelerating enterprise/IoT connectivity needs | +1.5% | Industrial regions | Long term (≥ 4 years) |

| Energy retailers bundling MVNO offers | +0.7% | Nationwide retail grids | Medium term (2-4 years) |

| Diaspora-focused roaming propositions | +0.4% | Large metro areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Low-Cost Mobile Connectivity

The average Polish mobile bill escalated to PLN 47.41 in June 2025, up 6.9% in one quarter, sharpening consumer focus on wallet-friendly plans. MVNOs captured the resulting churn by advertising contract-free bundles priced 20-30% below MNO offers, leveraging lean digital care to sustain margins. Entry-level tariffs under PLN 30 now resonate strongly with students and seniors, while small businesses gravitate toward flat-data SIMs that strip out entertainment extras. Promotional SIM portability incentives further amplify defections from the incumbent brands.

Expansion of 5G Wholesale Capacity

T-Mobile’s 2,800 live 5G sites and Orange’s 1,200 C-band nodes already cover two-thirds of residents, and each operator has earmarked spectrum carve-outs for wholesale clients [1]5G Observatory, “Biannual Report June 2024,” 5gobservatory.eu. New network-slice APIs give full MVNOs latitude to tailor latency, throughput, and security, spawning premium offers for live video, real-time control, and AR field service. The regulator’s release of the 3.8-4.2 GHz band for campus networks adds another dimension, letting MVNOs aggregate private 5G cells into national footprints to serve logistics hubs and manufacturing zones.

Accelerating Enterprise/IoT Connectivity Needs

Utilities, mining firms, and smart-city operators increasingly demand narrow-band, low-power IoT links. T-Mobile’s nationwide NB-IoT grid underpins metering and flood-alarm projects, offering MVNO partners wholesale terms with embedded device-management portals. LTE-M modules providing up to 10-year battery life drive traction in vehicle telemetry, refrigerated transport, and asset tracking, use-cases where MVNOs can bundle managed services and analytics. The Polish MVNO market, therefore, shifts from volume-centric consumer SIMs to value-centric enterprise contracts that exhibit multi-year stickiness.

Regulatory Cuts in Wholesale Access Fees

EU-wide roaming cost caps trimmed data surcharges to PLN 6.88 per GB and lowered voice termination to PLN 0.98 per 10-minute block in May 2025 [2]European Commission, “2025 Update of the Mobile Cost Model for Roaming and Voice Call Termination,” digital-strategy.ec.europa.eu . For MVNOs, the drop translates into mid-single-digit gross-margin uplift that can be redeployed into customer acquisition or feature enrichment. The 2024 Electronic Communications Law further simplifies licensing and enforces transparency on MNO wholesale tariffs, diluting incumbents’ pricing leverage and smoothing MVNO cash-flow forecasting [3]Mondaq, “New Telecom Law in Poland: Electronic Communications Law,” mondaq.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin squeeze from price wars | -1.4% | National | Short term (≤ 2 years) |

| Volatile wholesale rates amid MNO consolidation | -0.8% | National | Medium term (2-4 years) |

| Limited access to 5G SA core and network APIs | -0.6% | Advanced services zones | Long term (≥ 4 years) |

| Costly KYC/SIM-registration compliance | -0.3% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Margin Squeeze from Price Wars

While headline bills have inched up, the effective unit price of data keeps falling as MNOs double allowances without raising fees. Play’s zero-zloty prepaid account-maintenance policy undercut typical MVNO administrative charges, forcing rivals to forgo ancillary revenue lines. Light MVNOs, which pay per-MB wholesale fees, feel the pinch most acutely because they lack scale to renegotiate network costs. In response, operators bundle over-the-top perks, cloud storage, antivirus, or fuel discounts, to protect ARPU without violating price-leadership claims.

Volatile Wholesale Rates Amid MNO Consolidation

Network-sharing pacts and upcoming 3G sunset programs let host operators reclaim spectrum for 5G, but also reshape wholesale-rate algorithms that MVNOs depend on. A two-tier tariff emerges: premium for low-latency 5G slices, discounted for legacy LTE traffic. Sudden rate resets can erode MVNO margin forecasts and require tariff re-design within weeks. Diversifying across multiple host networks and adopting multi-IMSI SIMs has become a risk-mitigation imperative, yet raises operational complexity and certification overhead.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Operational Efficiency

Cloud-based cores generated 64.47% revenue in 2024, cementing their role as the backbone of most entrants to the Poland MVNO market. Rapid horizontal scaling, pay-as-you-grow licensing, and built-in analytics help operators launch sub-brands in days rather than months. The segment will preserve a healthy 9.92% CAGR because even established full MVNOs are refactoring legacy EPCs into virtualized network functions on public clouds. Operators cite 25-30% opex savings over on-premise stacks, savings that directly buffer thin prepaid margins.

On-premise still resonates where data sovereignty or ultra-low-latency mandates prevail, such as defense contractors and bank-led MVNOs. These stakeholders value deterministic performance and the ability to integrate custom security appliances. Hybrid deployments, such as a control plane in a public cloud, a user plane on edge servers, are gaining favor as a middle path, balancing cost and compliance. Overall, the Poland MVNO market size attributable to on-premise installations will keep shrinking in share terms even as absolute spending rises moderately.

By Operational Mode: Full MVNOs Emerge Despite Complexity

Reseller and brand MVNOs held 64.35% of 2024 revenues due to their ease of launch, absence of spectrum fees, and limited technical overhead. Yet full MVNOs, growing 21.59% annually, are rewriting the competitive script by controlling SIM provisioning, billing, and service creation. Full ownership of the core allows granular quality of service enforcement and differentiated 5G slices, capabilities crucial for enterprise SLAs. The Polish MVNO market, therefore, shows a clear bifurcation: low-touch brands stay volume-centric while full MVNOs chase high-yield specialized verticals.

Early movers pairing full-core autonomy with data-science-driven tariff engines report churn that is 30% lower than light peers, thanks to the rapid introduction of bespoke bundles. However, the capital intensity remains high; Evolved Packet Core licenses, lawful interception platforms, and 24/7 NOC staffing add millions of PLN to year-one budgets. Consequently, investor appetite tilts toward operators with multi-country ambitions that can amortize the stack across several national markets.

By Subscriber Type: Consumer Dominance Masks Enterprise Opportunity

Consumer SIMs delivered 84.54% of the Polish MVNO market revenue in 2024. Budget plans under PLN 35 remain the workhorse product, especially for urban millennials and migrant workers. Yet IoT lines are the fastest-growing cohort, expanding 31.85% annually off a small base as smart meters, trackers, and sensors proliferate. Bulk deals can exceed 10,000 SIMs each and exhibit churn below 5% due to device-embedded profiles. Enterprise handheld subscriptions are the middle ground, attracting higher ARPU but demanding field-support SLAs and integration with corporate MDM systems.

MVNOs that master unified subscriber management, consumer, handheld enterprise, and machine, unlock operational synergies in billing, lifecycle management, and analytics. Cross-selling rate-limited IoT SIMs to existing handset customers with industrial operations represents a sizable untapped cross-segment play.

By Application: M2M Services Drive Innovation

The other application segment claimed 41.60% of 2024 turnover, covering everything from e-learning SIMs to charity-branded prepaid cards. Cellular M2M, however, is sprinting ahead at 27.97% CAGR as electric-vehicle charging, cold-chain monitoring, and predictive maintenance gain funding. MVNOs leverage self-care APIs so clients can activate thousands of SIMs programmatically, a decisive advantage over MNO portals still tuned for retail subscribers. Discount voice-and-text products retain relevance for older demographics but now generate lower margins, prompting some operators to sunset legacy tariffs in favor of data-centric bundles.

By Network Technology: 5G Transition Accelerates Despite 4G Dominance

4G/LTE contributed 68.33% of Poland's MVNO market traffic in 2024 due to ubiquitous coverage and mature device ecosystems. Still, satellite/NTN lines, though tiny in absolute numbers, post a 101.86% CAGR as logistics, maritime, and first-responder services demand ubiquitous fail-over. The first MVNO-satellite roaming agreements are live, offering sub-300 ms latency suitable for basic messaging and telemetry. Looking forward, 5G SA adoption will pivot on host-operator readiness: Orange plans nationwide core upgrade by 2026, while Plus and Play target mid-2027.

Legacy 2G/3G sunsets free low-band spectrum for 5G NR, indirectly lowering wholesale LTE pricing and enabling MVNOs to upsell higher speed tiers without raising input costs. The Poland MVNO market size linked to pure 3G traffic will vanish before 2028, simplifying network-testing matrices and device certification.

By Distribution Channel: Digital Transformation Reshapes Customer Acquisition

Online/self-service sign-ups represented 50.20% of 2024 gross additions and are still expanding 10.52% yearly as eSIM adoption climbs. Customers finalize KYC through bank-verified digital IDs, cutting activation time to under five minutes. Carrier sub-brand stores and supermarket tills remain vital for older, cash-paying demographics, but their share slips gradually. Third-party wholesalers such as energy retailers and fintech apps see MVNO bundles as loyalty perks, yet program economics hinge on cross-selling uptake.

Digital-first operators typically report customer-support opex that is one-third of call-center-heavy incumbents, freeing budget for data-allowance boosts. In turn, that fuels the perception of superior value among heavy data users, reinforcing the cycle of digital acquisition dominance in the Polish MVNO market.

Geography Analysis

Poland’s nationwide 4G coverage already surpasses 99% population reach, positioning the country as a fertile ground for MVNO expansion. Urban hubs like Warsaw, Kraków, and Poznań contribute more than 55% of total MVNO ARPU as early adopters embrace unlimited 5G plans bundled with music or video OTT. In these cities, the Poland MVNO market size for enterprise IoT is also the largest because industrial parks co-locate with robust fiber backhaul.

Silesia and Greater Poland, anchored by automotive, mining, and heavy-manufacturing plants, drive concentrated demand for private LTE and NB-IoT grids. MVNOs collaborating with system integrators offer end-to-end packages, connectivity, sensors, and analytics dashboards, shortening procurement cycles for mid-cap firms. Along the Baltic coast, seasonality shapes sales; tourist influx doubles data traffic in July-August, encouraging MVNOs to introduce 30-day roaming bundles with embedded EU allowances.

Border regions with Germany and Czechia create unique roaming rings where commuters desire single-rate SIMs that operate seamlessly across frontiers. Diaspora-oriented brands aggregate international calling minutes to Ukraine and Belarus, leveraging low wholesale termination rates negotiated under the EU regime. Satellite/NTN overlays further support sparsely populated Bieszczady mountains in the southeast, ensuring emergency call compliance and promoting MVNO participation in public-safety tenders.

Competitive Landscape

Roughly 16 active providers jostle for a share, leaving the Polish MVNO market semi-consolidated. The top five account for an estimated 42% of gross revenue, implying ample runway for niche entrants. Cost-leadership specialists, notably supermarket-backed brands, pursue high-volume SIM sales coupled with retail loyalty points. Service-differentiators such as enterprise-focused full MVNOs emphasize SLA guarantees, private APNs, and network-slice offerings to justify ARPU premiums approaching PLN 60.

MNO sub-brands Heyah (T-Mobile) and nju mobile (Orange) wield customer-acquisition budgets far exceeding independent peers, yet their strategies focus on churn containment within parent groups rather than market expansion. Independent disruptors secure mind-share by embedding digital community features that lower marketing spend. Play’s extended partnership with Netcracker equips its wholesale arm with a convergent BSS that shortens onboarding cycles for new MVNOs to under eight weeks.

Technological arms races are evident. Operators deploying cloud-native cores boast 99.995% service availability and push CI/CD updates weekly, a cadence unattainable for legacy bare-metal stacks. Some fintech and energy retailers continue to evaluate white-label MVNO programs but grapple with compliance overhead, particularly GDPR and SIM-registration audits. Still, their vast customer bases make them latent disruptors should they overcome regulatory inertia.

Poland Mobile Virtual Network Operator (MVNO) Industry Leaders

Virgin Mobile Polska Sp. z o.o.

Premium Mobile Sp. z o.o.

Lycamobile Poland Sp. z o.o.

Otvarta Sp. z o.o.

Mobile Vikings (VikingCo Poland Sp. z o.o.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Orange Flex introduced summer promos with free 25 GB domestic data and supplementary EU roaming, simultaneously activating seasonal mobile base stations in tourist zones.

- June 2025: Netia revamped mobile internet tariffs, enabling unlimited 5G plans via Plus infrastructure and multi-device support for smartphones and CPE routers.

- June 2025: Mobile Vikings consolidated subscription and prepaid lines into a four-tier card model priced between PLN 25 and PLN 45, offering up to 180 GB of data and automatic plan upgrades.

- March 2025: Orange Polska unveiled a 2025-2028 roadmap targeting 30% additional fiber coverage and 12-15% price lifts across convergent bundles.

Poland Mobile Virtual Network Operator (MVNO) Market Report Scope

| Cloud |

| On-premise |

| Reseller/ Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller/ Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

How large is the Poland MVNO market in 2025?

The Poland MVNO market size is USD 0.36 billion in 2025, with a projected rise to USD 0.48 billion by 2030.

What is the expected growth rate for Polish MVNOs?

Aggregate revenue is forecast to increase at a 6.04% CAGR between 2025-2030.

Which subscriber segment is expanding the fastest?

IoT-specific SIMs post the highest growth, registering a 31.85% CAGR over the forecast window.

How dominant are cloud deployments among MVNOs?

Cloud cores already support 64.47% of Poland MVNO market revenues and keep expanding thanks to lower opex and rapid scaling.

What technology will drive next-wave differentiation?

Full 5G SA slicing, combined with satellite/NTN overlays, will let MVNOs offer ultra-reliable coverage and latency-sensitive enterprise services.

Are price wars hurting MVNO profitability?

Yes. Margin compression from aggressive prepaid pricing is the leading short-term restraint, subtracting about 1.4 percentage points from forecast CAGR.

Page last updated on: