South Korea Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

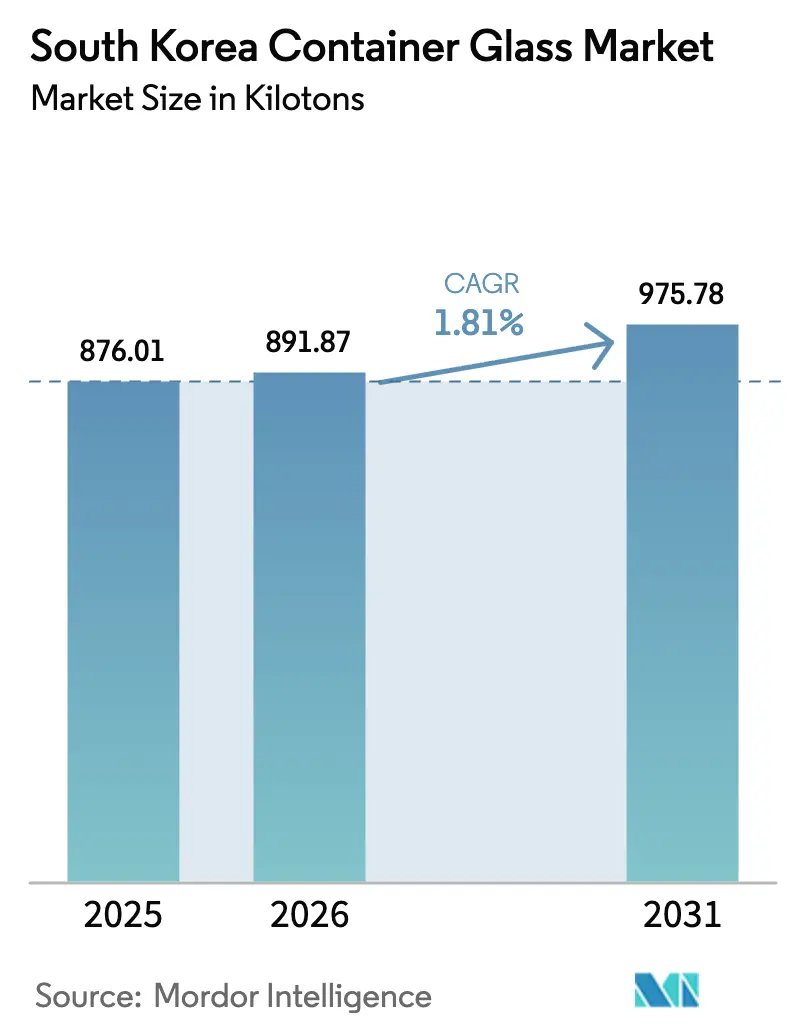

| Base Year Market Size (2025) | 876.01 kilotons |

| Market Volume (2026) | 891.87 kilotons |

| Market Volume (2031) | 975.78 kilotons |

| Growth Rate (2026 - 2031) | 1.81% CAGR |

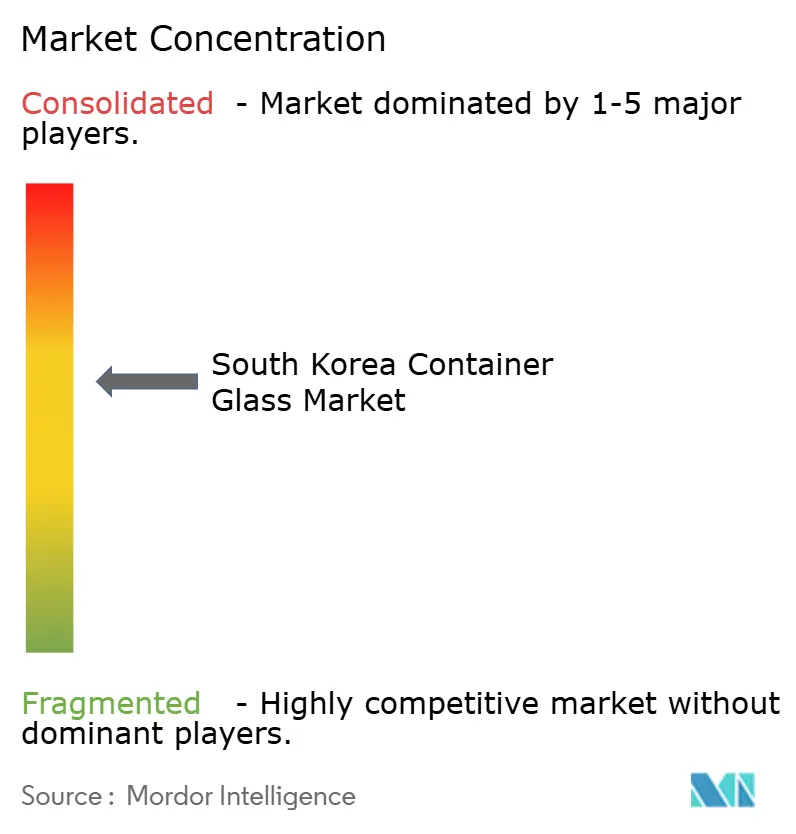

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Container Glass Market Analysis by Mordor Intelligence

South Korea container glass market size in 2026 is estimated at 891.87 kilotons, growing from 2025 value of 876.01 kilotons with 2031 projections showing 975.78 kilotons, growing at 1.81% CAGR over 2026-2031. Demand is concentrated in beverages, which accounted for 67.85% of the 2024 volume, while cosmetics and personal care led incremental growth. An 85.8% national glass-recycling rate supplies an abundant supply of cullet, lowering energy requirements and reinforcing the circular economy's credentials. However, industrial electricity costs rose 70% between 2022-2024 to USD 133/MWh in December 2024, tightening margins for furnace operations. Political turbulence since late 2024 clouds short-term investment sentiment, yet export-oriented manufacturers leverage K-beauty, pharmaceutical, and premium beverage opportunities to mitigate domestic headwinds.

Key Report Takeaways

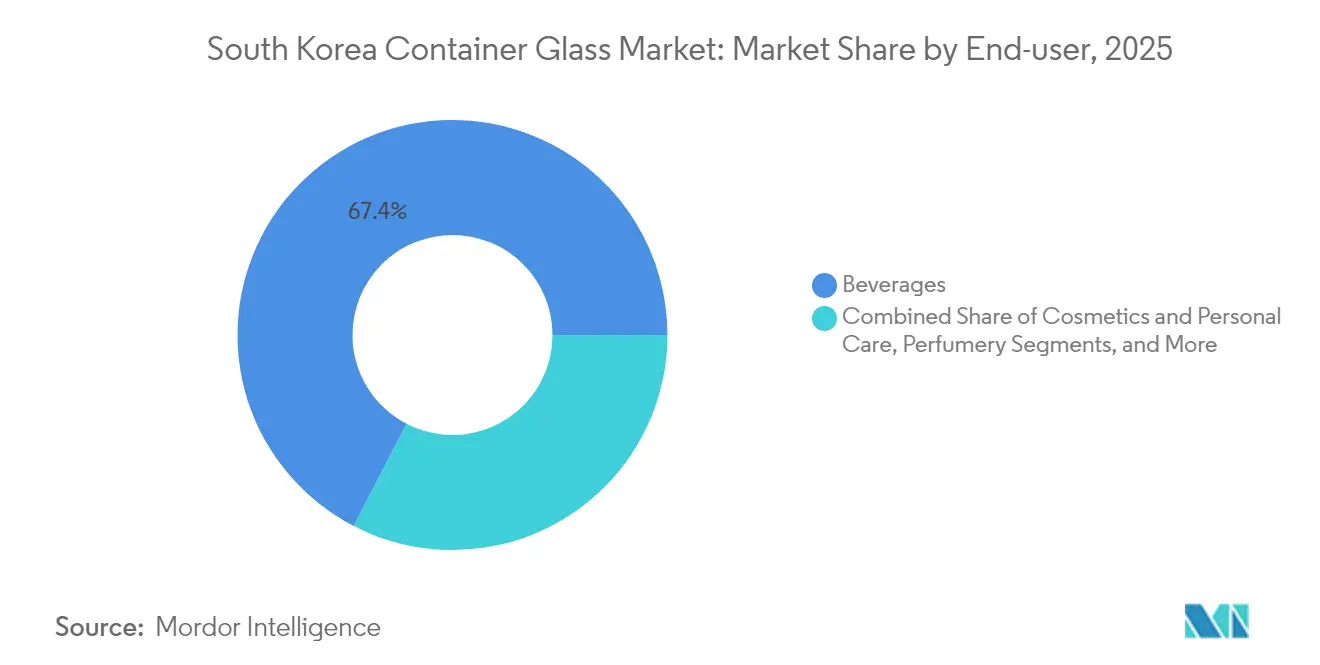

- By end-user, beverages captured 67.40% of the South Korea container glass market share in 2025.

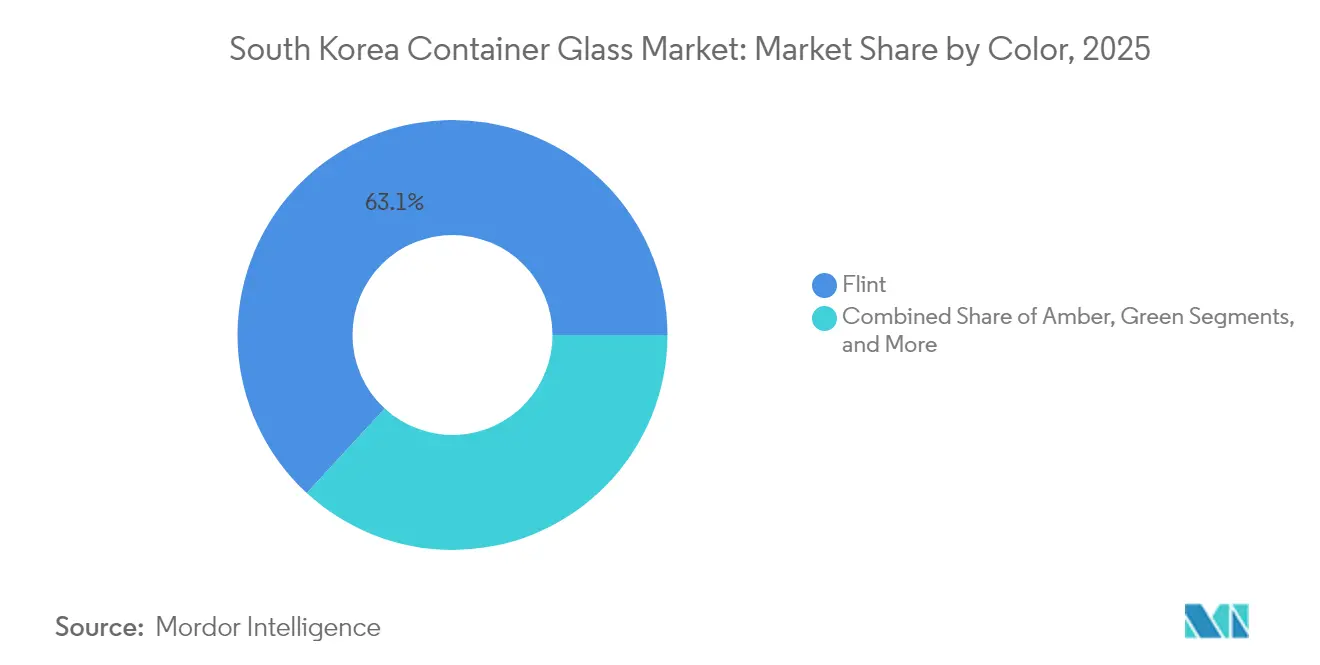

- By color, the South Korea container glass market for amber glass is projected to grow at a 3.09% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government support for eco-friendly manufacturing and recycling | +0.4% | National, with stronger implementation in metropolitan areas | Medium term (2-4 years) |

| Growth in pharmaceutical packaging needs | +0.3% | National, concentrated in Gyeonggi and Seoul pharmaceutical hubs | Long term (≥ 4 years) |

| Consumer preference for inert and safe packaging materials | +0.2% | National, with premium segment concentration in urban markets | Medium term (2-4 years) |

| Expansion of K-beauty and perfumery exports | +0.5% | National, with manufacturing clusters in Gyeonggi and Chungcheong | Short term (≤ 2 years) |

| Innovation in lightweight glass production | +0.2% | National, driven by major manufacturers | Long term (≥ 4 years) |

| Increased adoption of glass in food and beverage sectors | +0.3% | National, with stronger uptake in premium beverage segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Support for Eco-Friendly Manufacturing and Recycling

The Extended Producer Responsibility (EPR) regime obliges bottle producers to meet annual recycling quotas, driving continuous demand for cullet that stabilizes input costs and lowers furnace temperatures by up to 4%.[1]ChemLinked Team, “South Korea Extended Producer Responsibility (EPR) System,” chemlinked.com Recycling facilities increased from 1,568 in 1998 to 6,910 in 2022, generating USD 15.8 billion in secondary material sales and supporting 154,000 jobs. High recovery rates enhance brand equity for beverage, food, and cosmetics exporters that cater to the strict EU packaging directives. Municipal governments in Seoul, Busan, and Incheon subsidize cullet logistics, reducing transport costs for manufacturers. The policy also incentivizes furnace upgrades, as subsidies target electric-boost technologies that cut CO₂ intensity. Consequently, the South Korean container glass market benefits from both fiscal relief and reputational advantages that plastic rivals struggle to match.

Growth in Pharmaceutical Packaging Needs

Stringent MFDS regulations require drug manufacturers to use containers proven to be free of leachables, driving reliance on Type I and Type II borosilicate bottles and vials. Seoul and Gyeonggi house more than 70% of Korean pharma production, assuring nearby offtake for glass converters. Tax credits for biologics plants in Songdo amplify demand for pre-filled syringes and ampoules. Domestic companies partner with furnace designers to embed rapid annealing lines that meet particulate contamination limits. Rising vaccination campaigns targeting aging demographics are elevating the usage of small-volume injectables, further boosting demand for high-value glass formats. Over the forecast horizon, pharmaceutical buyers prioritize long-term supply contracts, securing baseline volume for the South Korea container glass market even during beverage-cycle volatility.

Expansion of K-Beauty and Perfumery Exports

Viral unboxing videos and K-pop endorsements position ornate glass jars and droppers as key tools for brand storytelling. SMCG’s share price jumped 85% in April 2025 after clinching supply deals with local startups and L’Oréal, lifting 2025 operating-profit guidance to USD 9.2 million. Demand skews toward flint and specialty tinted flacons that highlight product color while satisfying EU recyclability rules. Beauty conglomerates are stipulating lightweight bottles to reduce freight emissions, prompting suppliers to thin sidewalls by 12% without compromising durability. The trend extends to niche perfumery, where small-run artisanal brands seek bespoke molds produced in Ansan and Cheonan. Fast product cycles require agile capacity, encouraging converters to adopt interchangeable gob systems and digital printing that shorten lead times to under two weeks.

Innovation in Lightweight Glass Production

Energy-intensive furnaces account for more than 20% of production cost; weight reduction lowers both melt energy and transport fuel. Domestic leaders retrofit furnaces with oxy-fuel burners and electric boosting, trimming gas use by 18%. Lightweight designs now average 265 g for a 330 ml beer bottle, compared to 290 g in 2022, resulting in a 9% reduction in material usage. Pilot projects are testing hydrogen-assisted melting, scheduled for commercial rollout by 2028. Collaborative R&D with vehicle-glass firms transfers thin-wall knowledge, enabling the production of cosmetics bottles under 100 g while meeting drop-test norms. Such efficiencies cushion the impact of the USD 133/MWh electricity tariff spike and position local suppliers for export bids premised on carbon scoring.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy costs in glass manufacturing | -0.6% | National, with particular impact on energy-intensive operations | Short term (≤ 2 years) |

| Competition from PET and aluminum packaging | -0.4% | National, strongest in beverage and food packaging segments | Medium term (2-4 years) |

| Fluctuating raw material prices | -0.2% | National, affecting all manufacturers | Medium term (2-4 years) |

| Limited domestic silica sand availability | -0.2% | National, requiring increased imports | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Energy Costs in Glass Manufacturing

Electricity rates increased by 70% between 2022 and 2024, raising monthly power bills to USD 0.38 million for some mid-sized plants and forcing margin compression. Korea’s 58.5% fossil-fuel generation mix exposes producers to LNG price swings, adding USD 16.9 billion to national power costs in 2022. To cope, firms negotiate direct purchase agreements with renewable generators and deploy rooftop solar for batch-house operations. Some consider offshore capacity in Vietnam, which could threaten domestic job retention. Elevated tariffs also delay furnace rebuild schedules, risking unplanned shutdowns. Unless the energy mix shifts decisively toward renewables, power cost volatility will persist as the primary drag on the South Korea container glass market.

Competition from PET and Aluminum Packaging

Lightweight PET and increasingly recyclable aluminum cans are tempting beverage fillers who aim to cut logistics fees. Advanced PET oxygen-scavenging resins narrow shelf-life gaps, making plastic viable for mid-tier wine and juice. Craft brewers favor aluminum for its portability, which is eroding glass volumes in convenience channels. Nevertheless, impending global plastic-pollution treaties keep brand owners cautious about long-term PET reliance, granting glass a defensive moat on sustainability grounds. Converters counter by marketing returnable-bottle programs and life-cycle assessments proving lower CO₂ over multiple re-use cycles. Still, any sustained decline in resin prices or subsidy to canning lines would magnify substitution risk, limiting the CAGR upside for the South Korean container glass market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Beverages Drive Volume While Cosmetics Accelerate Growth

Beverage fillers consumed 590.43 kilotons in 2025, equivalent to 67.40% of the South Korean container glass market share, with beer and soju accounting for the majority of refillable flows. Domestic craft beer, RTD cocktails, and functional drinks sustain baseline volume even as per-capita alcohol intake stabilizes. The sector benefits from refill schemes, which enable up to 20 reuse cycles per bottle, a feature not available with PET. Cosmetics registered a 3.05% CAGR and contributed 64 kilotons in 2025, as K-beauty labels specify elaborate droppers, jars, and airless pumps that leverage glass’s inertness. Influencer-led product launches compress lead times, rewarding suppliers with flexible decoration capabilities such as UV-ink digital printing.

A widening premiumization gap reaches food and pharmaceutical buyers. Artisanal condiments, organic honey, and gourmet sauces command higher shelf prices when packed in clear flint containers that signal purity. Pharmaceuticals add steady, regulation-anchored growth: injectable and liquid-oral forms demand silica-based packaging free from extractables. Perfumery, although it yields revenue margins of less than 5 kilotons, achieves triple those of beverage formats thanks to bespoke molds, metallic coatings, and small-batch runs. As a result, the South Korean container glass market is diversifying away from volume-centric staples toward higher-value niches that buffer revenue against swings in the beverage cycle.

By Color: Flint Dominance Challenged by Amber Growth

Flint retained 63.15% of the South Korea container glass market size in 2025 with 553.25 kilotons shipped, buoyed by cosmetics and premium food brands favoring transparent containers for visual merchandising. Clear glass dovetails with online beauty retail where product color influences click-through rates. Amber volumes reached 165 kilotons in 2025 and are forecast to grow 3.09% CAGR to 2031 on UV-sensitive pharmaceuticals and craft beers emulating European heritage styles. Breweries cite light-strike avoidance as a key quality parameter, making amber indispensable despite glass-lightweighting.

Green holds a niche in wine and olive-oil categories, where provenance storytelling overrides neutrality concerns. Other specialty tints cobalt blue, matte black serve limited-edition cosmetics and perfumery but deliver standout per-kilogram margins due to higher decoration spend. Color choice thus increasingly stems from functional plus branding calculus, rather than default cost considerations. Over the forecast, amber’s technical strengths ensure faster climb, yet transparent flint will preserve plurality given its versatility across booming K-beauty SKUs.

Geography Analysis

The South Korean container glass market clusters around Gyeonggi, Chungcheong, and South Gyeongsang, where established furnaces are situated near port logistics and end-user plants. National recycling infrastructure supplies cullet rates exceeding 60%, trimming batch costs by 12% and ensuring low-iron clarity for cosmetics jars. Incheon’s export terminals expedite outbound shipments to the United States, now accounting for 18.7% of Korean merchandise exports in 2024. Political gridlock since the December 2024 impeachment proceedings has slowed capital-expenditure approvals, but it has not deterred ongoing furnace rebuilds, thanks to multi-year planning cycles. Energy price spikes weigh heaviest on inland plants lacking access to LNG import terminals, prompting some firms to plan photovoltaic arrays on disused factory roofs. Coastal producers leverage seawater cooling and shipborne cullet imports to offset silica shortages. The Ministry of Environment’s nationwide EPR enforcement ensures uniform recycling obligations, but metropolitan regions outperform rural zones in collection efficiency, providing Seoul-area plants with a steadier cullet supply. Looking outward, Australia and the Philippines emerge as high-growth export destinations for Korean skincare and soju, further internationalizing demand for domestically made bottles. This geographic diversification cushions the South Korea container glass market against any cyclical slowdown in local consumption.

Competitive Landscape

Domestic incumbents Hankuk Glass Industries, Chemiglas Corp., and Kukyoung G&M together held almost half of the national volume in 2024, positioning the sector as moderately concentrated. International entrants Verescence Pacific and Saverglass supply luxury perfumery bottles, sharpening the design competition. Rising tariffs galvanize producers to strike renewable power deals. Hankuk Glass announced a 20 MW solar PPA in June 2025, projected to reduce site emissions by 18%. Chemiglas pilots a hydrogen-ready furnace slated for commissioning in 2027, signaling a long-term commitment to decarbonization.

Meanwhile, SMCG rides K-beauty upside-down, integrating hot-stamping and cold-foil units that capture high-margin decoration in-house.[3]CNS Media, packaginginsights.com Compliance capabilities become a competitive moat as MFDS intensifies audits on leachable heavy metals. Firms invest in ICP-MS labs and ISO/IEC 17025 accreditation to ensure batch conformity.

Cost pressures accelerate lightweighting collaborations with German forming-machine makers, enabling up to 16-section IS lines that deliver 550 bottles per minute. Moderate consolidation potential persists, with private-equity interest hovering over cash-strapped mid-tier players grappling with rising energy costs. Nonetheless, entry barriers from capital, technology, and regulatory scrutiny keep the South Korean container glass industry resilient against sudden fragmentation.

South Korea Container Glass Industry Leaders

Kukyoung G & M Co., Ltd.

SGC Solutions Co., Ltd

Verescence Pacific, Inc.

Somang Glass Co., Ltd.

Nihon Yamamura Glass Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SMCG shares surged 85% in six weeks after securing long-term supply agreements with local cosmetics startups and global brand L’Oréal, uplifting 2025 operating-profit forecast to USD 9.2 million.

- March 2025: Samsung Electro-Mechanics expanded its glass-substrate ecosystem for next-generation semiconductors, targeting mass production by 2027, showcasing Korea’s advanced glass-processing capabilities.

- February 2025: The UN Environment Assembly advanced negotiations toward a global plastic pollution treaty, amplifying brand owner interest in infinitely recyclable glass.

- January 2025: AGC Inc. reaffirmed the operations of its subsidiaries, AGC Fine Techno Korea and AGC Display Glass Ochang, maintaining local specialty-glass capacity despite global optimization efforts.

South Korea Container Glass Market Report Scope

Container glass is designed for manufacturing glass containers, including bottles, jars, drinkware, and bowls. Its key attributes include chemical inertness, sterility, and non-permeability, rendering it especially sought after in the beverage, food, pharmaceutical, and cosmetic sectors. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

South Korea's Container Glass Market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, and by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments..

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What is the current volume of the South Korea container glass market?

The market handled 891.87 kilotons in 2026 and is on track to reach 975.78 kilotons by 2031.

Which application contributes most to Korean container-glass demand?

Beverages account for 67.40% of 2025 volume, spanning alcoholic and non-alcoholic drinks.

Why is glass preferred for K-beauty packaging?

Brands value glass’s inertness, aesthetics and recyclability, key for premium image and export compliance.

How are energy costs affecting Korean glass makers?

Electricity tariffs climbed to USD 133/MWh, elevating power costs above 20% of production expenses and spurring efficiency upgrades.

What colors of container glass are growing fastest in Korea?

Amber glass is projected to grow at a 3.09% CAGR through 2031 due to its UV-blocking attributes for pharmaceuticals and craft beverages.

How does Korea’s recycling rate benefit glass producers?

An 85.8% bottle-recycling rate supplies abundant cullet, lowering melting temperatures and improving cost competitiveness.

Page last updated on: