South America Indoor Farming Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

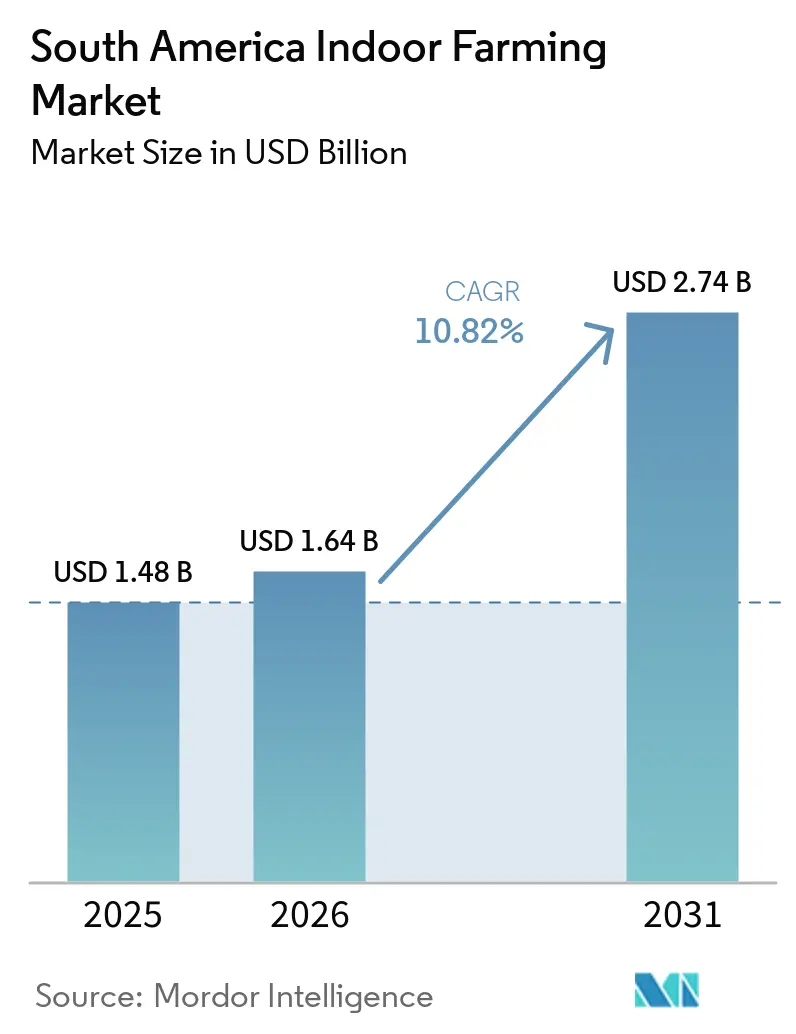

| Base Year Market Size (2025) | USD 1.48 Billion |

| Market Size (2026) | USD 1.64 Billion |

| Market Size (2031) | USD 2.74 Billion |

| Growth Rate (2026 - 2031) | 10.82% CAGR |

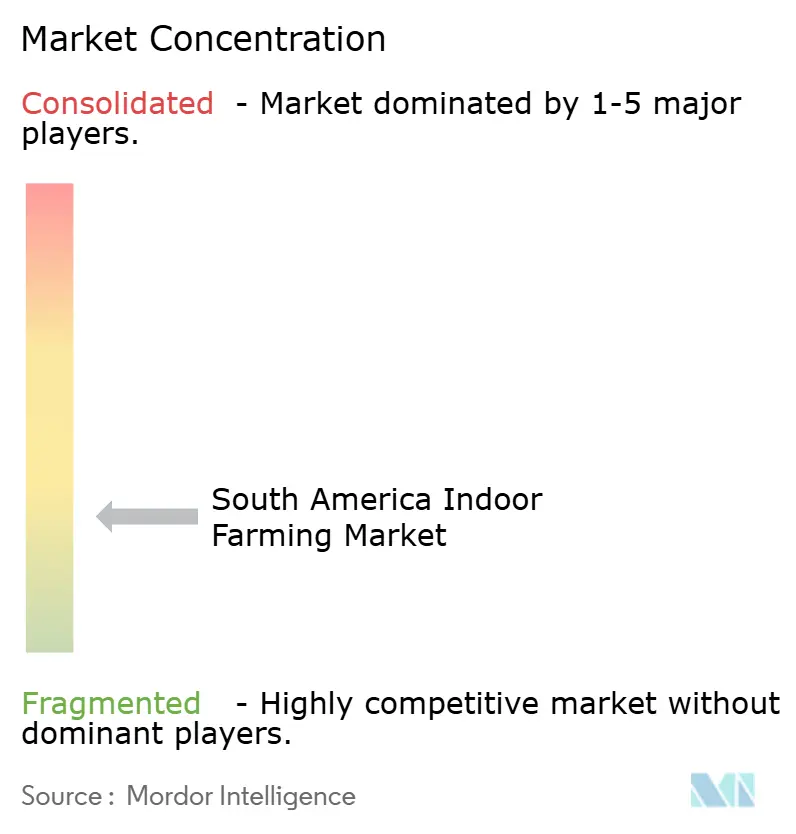

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Indoor Farming Market Analysis by Mordor Intelligence

The South America indoor farming market size is projected to grow from USD 1.48 billion in 2025 and USD 1.64 billion in 2026 to USD 2.74 billion by 2031, registering a CAGR of 10.82% between 2026 and 2031. The South America indoor farming market is benefiting from a highly urbanized food system, which is increasing demand for short, reliable, and traceable supply chains for fresh produce across major metropolitan consumption centers. The South America indoor farming market is also gaining support from climate change pressures. Brazil has been experiencing an increase in the frequency of droughts, with two occurring annually, according to an International Monetary Fund analysis published in 2025. This trend has heightened the appeal of controlled cultivation for both growers and investors. Expanding cold-chain capacity and modern retail formats in Brazil, Chile, and Colombia are making commercial indoor output easier to absorb through formal buyer channels, which improves revenue visibility for operators. The South America indoor farming market remains fragmented, and this limited purchasing scale still limits operators when negotiating for imported LED hardware, climate systems, and substrates. A second commercial pattern is also becoming clearer, as BeGreen Fazendas Urbanas partnered with Vale S.A. under a five-year agreement to convert an underutilized industrial area in Nova Lima into a 6,000-square-meter controlled-environment farming facility for the production of fresh vegetables and leafy greens, showing how anchor customers can reduce payback risk and open new expansion paths across hospitality and industrial locations.

Key Report Takeaways

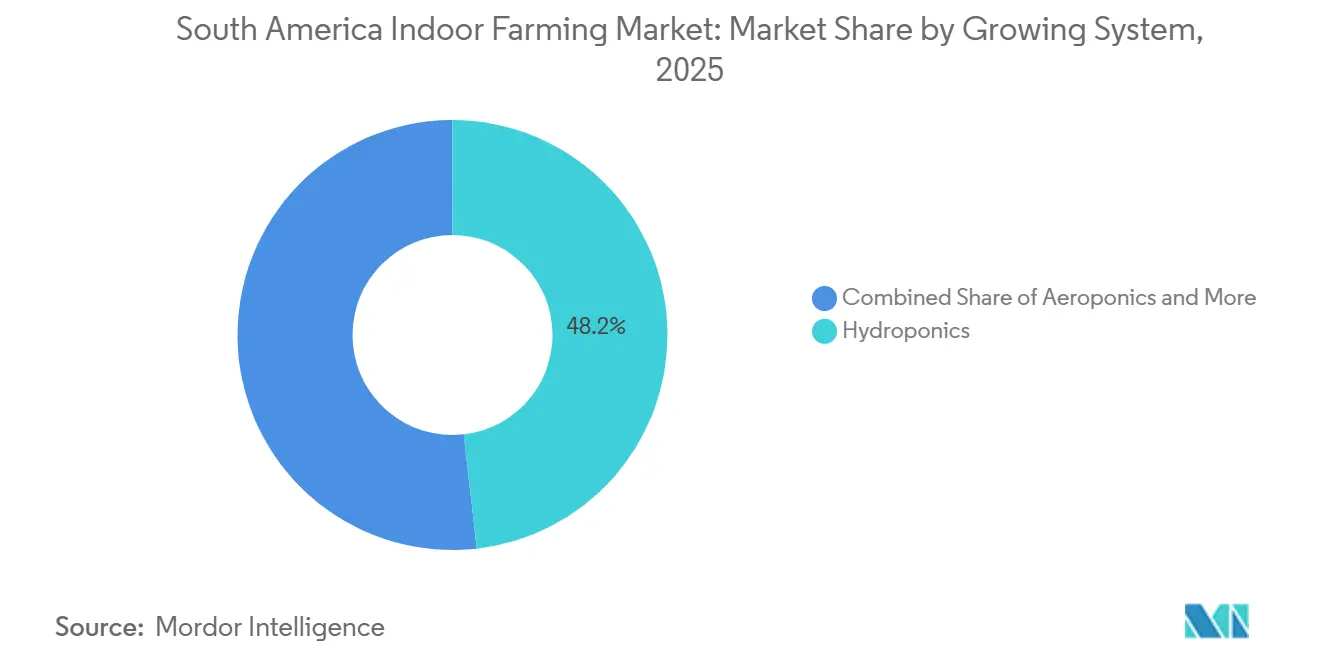

- By growing system, hydroponics accounted for 48.2% of the South America indoor farming market in 2025, while aeroponics is forecast to grow at a 15.1% CAGR through 2031.

- By facility type, glass or poly greenhouses captured 53.1% of the South America indoor farming market share in 2025, and container farms are forecast to grow at a 14.8% CAGR through 2031.

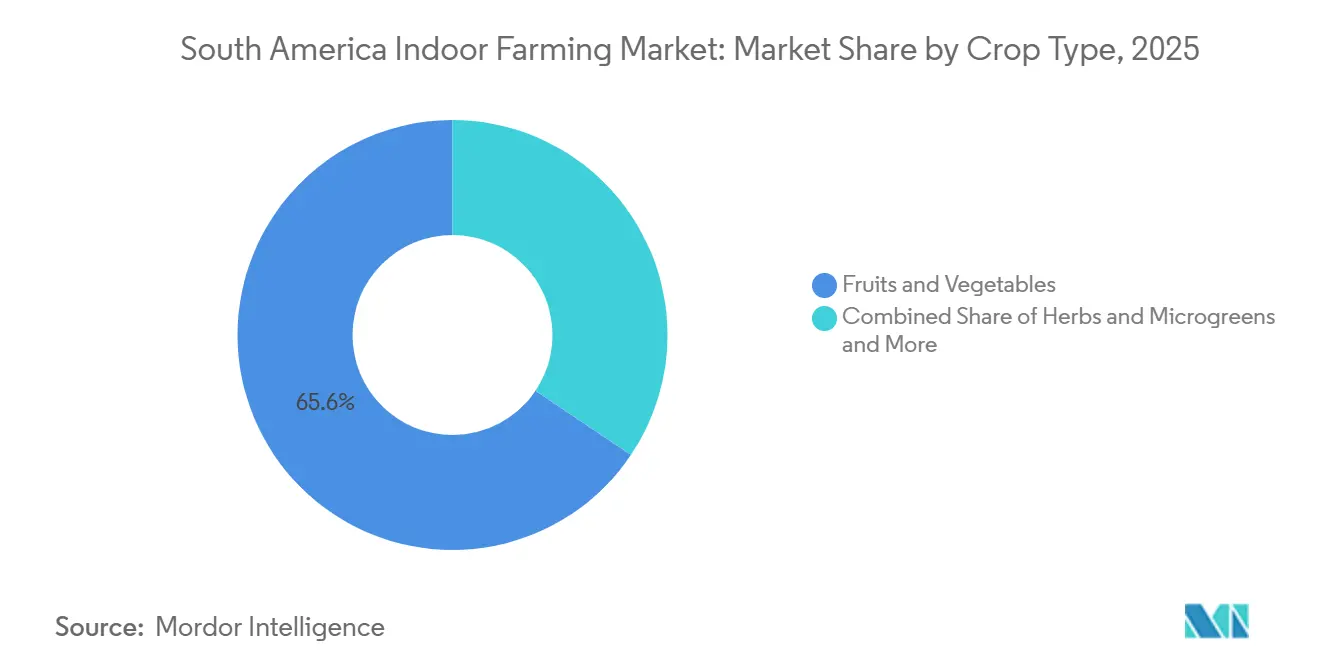

- By crop type, fruits and vegetables accounted for 65.6% of the indoor farming market size in 2025, whereas herbs and microgreens are anticipated to grow with the highest CAGR of 13.2% through 2031.

- By country, Brazil led the South America indoor farming market with a 49.1% share in 2025, whereas Chile is projected to post the highest CAGR of 9.5% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Indoor Farming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urban demand for fresh produce | +2.8% | Brazil, Chile, Colombia, and Peru urban centers | Short term (≤ 2 years) |

| Climate volatility increasing protected cultivation adoption | +2.2% | Brazil, Chile, and Argentina | Short term (≤ 2 years) |

| Expanding greenhouse and hydroponic investments | +1.9% | Brazil, Chile, and Paraguay | Medium term (2-4 years) |

| Improving light emitting diode and automation cost economics | +1.6% | Global, with concentrated impact in Brazil and Chile | Long term (≥ 4 years) |

| Growing modern retail and foodservice expansion | +1.4% | Brazil, Chile, and Colombia | Short term (≤ 2 years) |

| Adoption of tropicalized hybrid seed varieties | +0.9% | Brazil, Colombia, and Peru | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Urban Demand for Fresh Produce

Urbanization is changing how fresh food is bought across the South America indoor farming market. Brazil’s Census, published in 2024, showed an urbanization rate of 87.4%[1]Source: Government of Brazil, “Census: 87% of the Brazilian Population Lives in Urban Areas,” Brazilian Institute of Geography and Statistics (IBGE), agenciadenoticias.ibge.gov., which placed a very large share of the population inside metro supply zones where quality, shelf life, and frequency matter more than seasonal availability. The same broad pattern is visible across Latin America and the Caribbean, where 81% of people were urban, which narrowed the distance between food insecurity concerns and commercial sourcing decisions. March 2026 retail data in Brazil also showed record monthly sales, with the food segment outperforming broader retail activity, which signaled sustained urban demand for fresh products sold through formal channels. This matters for the South American indoor farming market because urban supermarkets and food-service buyers need year-round volumes, stable specifications, and traceability that open-field supply does not always provide. The strongest demand is no longer limited to São Paulo, Santiago, and Bogotá, because secondary cities such as Curitiba, Recife, Medellín, and Lima Norte are also expanding their formal retail footprint. That widening urban map gives indoor operators more room to replicate their model near demand centers instead of depending only on a few primary metros.

Climate Volatility Increasing Protected Cultivation Adoption

Climate instability is pushing more growers and investors toward protected production in the South America indoor farming market. An International Monetary Fund working paper published in March 2025 linked South America’s weather stress to recurring droughts, and it recorded Brazil at 2 drought events per year under an El Niño-amplified pattern[2]Source: International Monetary Fund, “South America Drought Frequency and Macroeconomic Implications,” IMF Working Paper 2025/052, elibrary.imf.org. Brazil’s official crop survey released in December 2024 showed that the country’s harvest declined significantly year over year, which reinforced the production risk attached to open-field farming. Food inflation also increased in 2025, which showed that weather pressure was reaching consumers and retailers rather than staying only at the farm level. AgroUrbana’s Quilicura vertical farm in Chile offers a practical counterpoint, because it reported 52 crop cycles per year with 95% less water than field farming, proving that controlled environments can separate output from rainfall volatility. This shift is changing how agricultural risk is priced, since indoor assets are increasingly treated as resilience infrastructure inside food supply chains. That reclassification improves the case for capital deployment in the South America indoor farming market, especially for operators with clear offtake and strong technical control.

Expanding Greenhouse and Hydroponic Investments

Investment activity strengthened the South America indoor farming market through 2024 and 2025. AgroUrbana completed a USD 6 million pre-Series B round in 2024 to expand its Quilicura site to 4,000 square meter[3]Source: Agrourbana, “AgroUrbana to Expand Vertical Farming Operations After Successful USD 6 Million Round," agrourbana.ag. Pink Farms continued expanding its indoor farming operations through additional funding rounds that supported new production capacity and higher operational throughput, highlighting sustained investor interest in scalable controlled-environment agriculture in Brazil. Meanwhile, HidroBio S.A. expanded large-scale greenhouse tomato cultivation in Paraguay in 2025, demonstrating the commercial viability of protected farming in emerging regional markets. Furthermore, Paraná’s hydroponic certification framework strengthened market access opportunities for indoor-grown produce across supermarket and food-service channels, supporting broader commercialization of the South America indoor farming market.

Improving Light Emitting Diode and Automation Cost Economics

Technology cost improvement is becoming a long-term growth enabler for the South America indoor farming market as declining LED costs, expanding automation integration, and renewable energy adoption improve operational efficiency across controlled-environment facilities. Since electricity and climate-control systems remain the largest operating cost components, indoor farming companies are increasingly focusing on energy optimization and automated cultivation systems to improve profitability, production consistency, labor efficiency, and crop scheduling reliability. Consequently, continued improvements in lighting efficiency, precision automation, and renewable power integration are projected to strengthen the commercial viability of indoor farming operations and gradually expand the range of crops economically produced under controlled environments across South America.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and energy requirements | -2.5% | Brazil, Argentina, and Chile nationwide | Short term (≤ 2 years) |

| Limited controlled-environment agronomy expertise | -1.3% | Global, most acute in Peru and Colombia | Medium term (2-4 years) |

| Currency volatility affecting imported technologies | -1.1% | Argentina, Brazil, Colombia, and Peru | Short term (≤ 2 years) |

| Inconsistent infrastructure and electricity availability | -0.8% | Peru, Colombia, and Rest of South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Energy Requirements

High upfront cost is still the clearest barrier to wider deployment across the South America indoor farming market. Pink Farms’ disclosures showed that energy represented 40% of operating expenditure in 2025, and this alone explains why many facilities struggle to scale beyond pilot size without access to favorable power terms. The capital burden is even harder in markets where debt remains expensive and long-tenor project finance is limited. This slows expansion in places where food insecurity is strong but commercial funding is weak, including inland Colombia, northern Brazil, and parts of Peru. Argentina faces a sharper version of the same issue because imported climate systems and lighting become far more expensive after currency depreciation cycles. Smaller operators can enter with greenhouse models, but dense indoor vertical farms still need large investment before they reach a viable cost base. The result is that the South America indoor farming market grows faster in wealthier urban corridors than in the places where local production could solve the biggest supply gaps.

Limited Controlled-Environment Agronomy Expertise

Talent remains a real operating bottleneck for the South America indoor farming market. Reporting in May 2026 noted that many Brazilian agricultural institutions still do not offer formal controlled-environment agriculture pathways, which leaves operators to train staff internally after hiring[4]Source: Conexão Safra, “Especialistas em Agricultura de Ambiente Controlado Ainda São Escassos no Brasil,” Conexão Safra, conexaosafra.com. That approach takes time and introduces avoidable variation in yield, nutrient management, and crop timing. The challenge is more severe in Peru and Colombia, where the commercial base is smaller and formal extension networks in this field are still limited. Indoor production depends on precise execution, so weak training can quickly translate into crop loss and delayed scaling. The operators that invest early in structured training or university partnerships can build a durable human-capital advantage. This matters commercially because supermarkets and institutional buyers judge suppliers on consistency, not just on the ability to complete a harvest. Until the skill base deepens, the South America indoor farming market will continue to face a slower roll-out outside the most experienced hubs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Growing System: Hydroponics Anchors Revenue as Niche Systems Emerge

Hydroponics accounted for 48.2% of the South America indoor farming market share in 2025, maintaining its leading position due to the preference of commercial greenhouse operators for standardized nutrient delivery, faster crop cycles, and efficient water management systems. At the same time, soil-based indoor cultivation gained traction among transitional greenhouse farms seeking lower technological complexity and compatibility with organic cultivation. As a result, hydroponic systems remained commercially dominant for leafy vegetables, herbs, and premium horticultural crops produced within controlled-environment farming operations.

Aeroponics is estimated to grow at a 15.1% CAGR through 2031, making it the fastest-growing system in the South America indoor farming market. This growth is driven by increasing prioritization of water efficiency, precision nutrient management, and climate-resilient production systems. Since Paraná introduced hydroponic certification pathways in 2026 and Embrapa advanced research on closed-loop aeroponic cultivation, commercial confidence in advanced indoor growing technologies has steadily increased. Additionally, hybrid cultivation systems that combine hydroponic stability with aeroponic efficiency are attracting growing investment for high-value crop production across the region.

By Facility Type: Vertical Farms Lead Growth, Greenhouses Drive Volume

Glass and poly greenhouses accounted for the 53.1% of the South American indoor farming market in 2025, driven by lower capital requirements, broader crop adaptability, and their suitability for commercial vegetable cultivation under regional climatic conditions. These greenhouse systems partially utilize natural sunlight, allowing operators to reduce energy dependence while maintaining controlled environments for crops such as tomatoes, cucumbers, peppers, and leafy vegetables. As a result, greenhouse facilities remained the preferred choice for large-scale horticultural operations seeking a balance of productivity, scalability, and operational efficiency.

Container farms are estimated to grow at a 14.8% CAGR through 2031, emerging as the fastest-growing facility type in the South American indoor farming market. This growth is attributed to the rising demand for modular deployment, localized food production, and the ability to rapidly install systems in urban and infrastructure-constrained areas. Compact container-based systems enable year-round cultivation near consumption centers, making them increasingly popular for growing leafy greens, herbs, and premium vegetables, thereby shortening supply chains. Additionally, indoor vertical farms continue to attract investment as advancements in AI-enabled climate management, water efficiency, and high-frequency crop production enhance their commercial scalability in metropolitan markets.

By Crop Type: Fruits and Vegetables Dominate, Specialty Crops Expand Margins

Fruits and vegetables held 65.6% share in 2025, the highest share in this segment of the South America indoor farming industry. Leafy greens, tomatoes, cucumbers, and bell peppers drove that lead through frequent supermarket and food-service demand. Herbs and microgreens followed as a smaller but higher-value class. Flowers and ornamentals formed a separate premium niche.

Herbs, microgreens, and specialty produce are poised to grow faster, with an estimated CAGR of 13.2% through 2031, as they deliver higher revenue per kilogram and fit urban farms with a limited footprint. Fruits and vegetables represent the largest segment of the South America indoor farming market due to demand from retailers, food-service chains, and urban consumers for consistent, year-round supplies of fresh produce with reliable quality and shorter delivery times. Additionally, large-scale greenhouse tomato cultivation projects in Paraguay highlight the commercial viability of controlled-environment farming for high-yield fruit and vegetable production in emerging regional markets. Concurrently, localized seed-adaptation programs in Chile are facilitating the growth of premium cultivars tailored to tropical and subtropical indoor-farming conditions.

Geography Analysis

Brazil held 49.1% of the South American indoor farming market share in 2025, making it the clear regional leader by value. That position is tied to strong metropolitan demand, as Greater São Paulo alone exceeds 21.6 million residents in 2025 and creates a dense fresh-produce catchment for commercial operators. Brazil also had the region’s deepest early-mover base, led by Pink Farms and BeGreen Fazendas Urbanas, which helped build investor familiarity and operating know-how in the South American indoor farming market. BeGreen Fazendas Urbanas strengthened that advantage through its Vale S.A. partnership in Nova Lima, where a 6,000-square-meter site is set to produce under an anchor-customer model that reduces commercial risk.

Chile is projected to post the highest CAGR of 9.5% through 2031. The country's growth is being driven by the need for year-round crop production and rising investments in controlled-environment agriculture. AgroUrbana’s Quilicura operation and the Atacama hydroponic expansion backed by INIA Intihuasi demonstrate how private and public initiatives are strengthening the technical and production infrastructure for indoor farming. These developments are positioning Chile as the fastest-growing market in the South America indoor farming market. Argentina plays a smaller role in total value, but it offers an important test of resilience under macroeconomic pressure.

Colombia is building capacity through urban demand in Bogotá and Medellín, but it still lacks a nationally dominant dedicated indoor operator. Peru’s development path is more public-sector led and livelihood support are major near-term drivers there. Paraguay added a strong reference point in 2025 when HidroBio S.A. completed its first commercial greenhouse tomato harvest, which created a benchmark for newer markets in the region. The rest of South America still relies more on smallholder and pilot-scale projects, which leaves room for Brazil- and Chile-based operators to expand as commercial conditions improve.

Competitive Landscape

The South America indoor farming market remains highly fragmented, with multiple regional operators competing across urban farming, greenhouse horticulture, and vertically integrated fresh produce systems. Companies including Pink Farms, BeGreen Fazendas Urbanas, HidroBio S.A., Hidrohorta Zangalli, and Cubo Farm continue expanding production capacity and distribution presence across selected metropolitan and commercial cultivation regions. Consequently, the absence of a fully integrated regional platform limits procurement efficiency, particularly for imported lighting systems, sensors, automation technologies, and climate-control infrastructure required for advanced indoor farming operations.

Two competitive models are becoming more visible in the South America indoor farming market. The first is the anchor-customer model, in which long-term institutional demand lowers sales risk and supports expansion financing. BeGreen Fazendas Urbanas used this route with Vale S.A., first through an early deployment at Águas Claras and then through a broader 5-year arrangement in Nova Lima. The second model is technology-led differentiation, in which farm software, crop recipes, and operational data become proprietary assets. AgroUrbana’s artificial intelligence system called Carmelo and Pink Farms’ accumulated operating data from Brazil’s vertical farming base show how technical control is turning into a commercial advantage.

A third pattern is replication into under-served geographies through standardized mid-scale facilities. HidroBio S.A.’s greenhouse project in Paraguay is a useful example, because it proved commercial output in a market that had little prior indoor farming infrastructure. White space remains broad in Colombia, Peru, and smaller South American markets, where no operator yet holds clear leadership. Technology, certification, and energy procurement are also converging as competitive tools rather than separate decisions. Pink Farms’ move toward Brazil’s free energy market shows how operating strategy is starting to matter as much as cultivation design in the South America indoor farming market. The companies that combine reliable buyers, disciplined expansion, and stronger technical systems are likely to shape the next phase of regional consolidation.

South America Indoor Farming Industry Leaders

-

Pink Farms

-

BeGreen Fazendas Urbanas

-

HidroBio S.A.

-

Hidrohorta Zangalli

-

Cubo Farm

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: HidroBio S.A., based in Paraguay, partnered with Froniva to deploy artificial intelligence-powered crop-monitoring and greenhouse-optimization systems, enhancing data-driven cultivation management and improving operational efficiency in controlled-environment vegetable production.

- August 2025: BeGreen Fazendas Urbanas signed a 5-year comodato agreement with Vale S.A. to operate a 6,000 m² growing facility at Vale's Nova Lima mining complex in Minas Gerais. The partnership establishes a scalable model for converting idle corporate infrastructure into food-producing assets, with clear replication potential across Vale's broader network of mining facilities across Brazil.

- May 2024: AgroUrbana raised USD 6 million to enhance its vertical farming operations in Chile, building on the success of its existing controlled-environment production systems. This expansion bolsters South America’s indoor farming infrastructure by increasing year-round production capacity for leafy greens and promoting the adoption of AI-enabled cultivation technologies.

South America Indoor Farming Market Report Scope

Indoor farming refers to the cultivation of crops within controlled-environment facilities where temperature, light, humidity, water, and nutrient conditions are actively managed to enable year-round agricultural production independent of external climatic conditions. The South America Indoor Farming Market Report is segmented by Growing System (Hydroponics, Aeroponics, Aquaponics, Soil-based, and Hybrid), by Facility Type (Glass or Poly Greenhouses, Indoor Vertical Farms, Container Farms, Indoor Deep-Water Culture Systems, and Other Facility Types), by Crop Type (Fruits and Vegetables, Herbs and Microgreens, Flowers and Ornamentals, and Others), and by Country (Brazil, Argentina, Chile, Colombia, Peru, and Rest of South America). The market forecasts are provided in terms of value (USD).

| Hydroponics |

| Aeroponics |

| Aquaponics |

| Soil-based |

| Hybrid |

| Glass or Poly Greenhouses |

| Indoor Vertical Farms |

| Container Farms |

| Indoor Deep-Water Culture Systems |

| Other Facility Type |

| Fruits and Vegetables | Leafy Greens |

| Tomato | |

| Cucumber | |

| Bell Pepper and Chili Pepper | |

| Strawberry | |

| Other Fruits and Vegetables | |

| Herbs and Microgreens | Basil |

| Mint | |

| Parsley and Cilantro | |

| Other Herbs and Microgreens | |

| Flowers and Ornamentals | Cut Flowers |

| Potted Ornamentals | |

| Others |

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Growing System | Hydroponics | |

| Aeroponics | ||

| Aquaponics | ||

| Soil-based | ||

| Hybrid | ||

| By Facility Type | Glass or Poly Greenhouses | |

| Indoor Vertical Farms | ||

| Container Farms | ||

| Indoor Deep-Water Culture Systems | ||

| Other Facility Type | ||

| By Crop Type | Fruits and Vegetables | Leafy Greens |

| Tomato | ||

| Cucumber | ||

| Bell Pepper and Chili Pepper | ||

| Strawberry | ||

| Other Fruits and Vegetables | ||

| Herbs and Microgreens | Basil | |

| Mint | ||

| Parsley and Cilantro | ||

| Other Herbs and Microgreens | ||

| Flowers and Ornamentals | Cut Flowers | |

| Potted Ornamentals | ||

| Others | ||

| By Country | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the South America indoor farming space?

T stood at USD 1.64 billion in 2026 and is projected to reach USD 2.74 billion by 2031, rising at a 10.8% compound annual growth rate.

Which country leads regional revenue?

Brazil led with 49.1% of total value in 2025, supported by its large urban consumer base, early-mover operators, and stronger investor participation.

Which growing system has the strongest position?

Hydroponics led with 48.2% revenue share in 2025 because it aligns well with formal retail standards and established controlled-environment practices.

Why are buyers moving toward controlled-environment supply?

Urban retail and food-service buyers need year-round quality, traceability, and supply consistency, while climate volatility is reducing the predictability of open-field output.

Page last updated on: