South America Maize Market Analysis by Mordor Intelligence

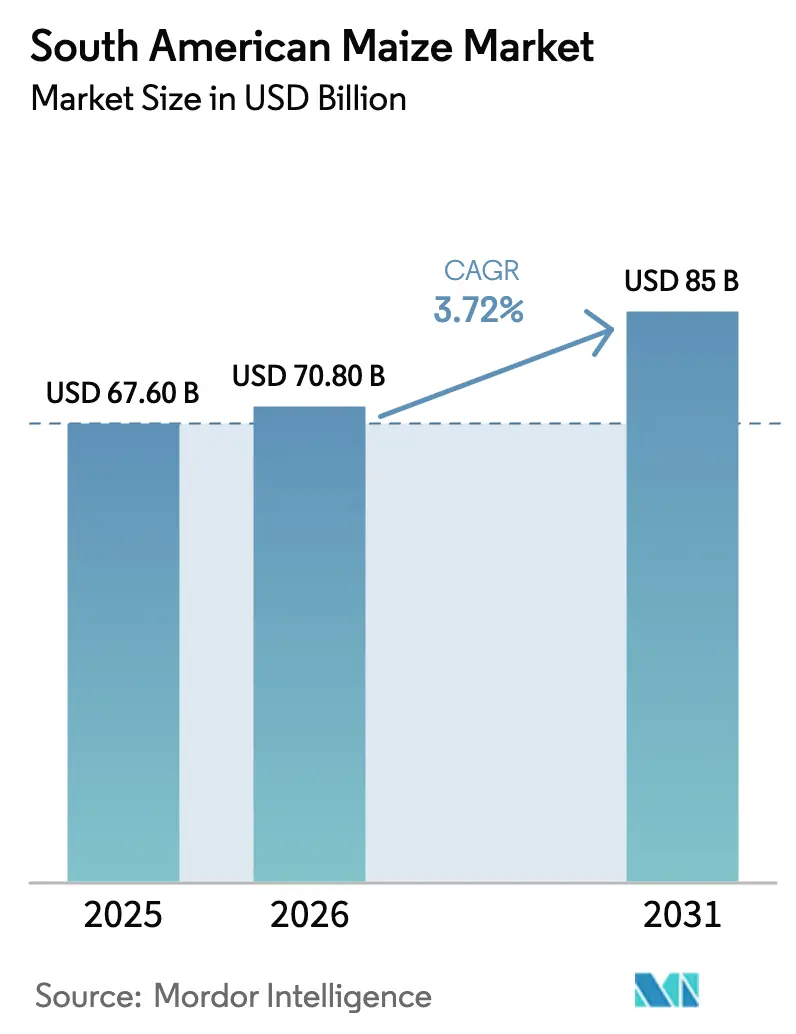

The South America Maize Market size was valued at USD 67.6 billion in 2025 and is estimated to grow from USD 70.8 billion in 2026 to reach USD 85 billion by 2031, at a CAGR of 3.72% during the forecast period (2026-2031). Strong animal-feed demand from Asia-Pacific livestock integrators, rising bioethanol blending mandates across Brazil and Argentina, and the rapid commercialization of stacked-trait hybrids that deliver 12-18% yield gains under water stress are accelerating the trajectory of the South America Maize Market. Bioethanol’s expansion is further fueled by Brazil’s RenovaBio decarbonization credit program, which priced credits at BRL 85 (USD 17) in December 2025, drawing new dry-mill investments from Archer Daniels Midland and Bunge. Trade liberalization under the African Continental Free Trade Area and the Regional Comprehensive Economic Partnership is enlarging the importer base, while digitized grain-handling infrastructure is trimming post-harvest losses and strengthening traceability credentials. Simultaneously, climate-induced yield fluctuations and port bottlenecks highlight ongoing supply chain vulnerabilities that may affect short-term export reliability.

Key Report Takeaways

- By geography, Brazil led the South America Maize Market size in 2025, accounting for 46.0%, and Paraguay is anticipated to grow at a 6.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Maize Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding animal-feed demand | + 1.2% | Global, with a concentration in Asia-Pacific, the Middle East, and South America | Medium term (2-4 years) |

| Growing bioethanol blending mandates | + 1.0% | South America (Brazil, Argentina, Paraguay), with spillover to North America | Short term (≤ 2 years) |

| Trade liberalization in key importing nations | + 0.8% | Asia-Pacific, Middle East, Africa | Medium term (2-4 years) |

| Advances in stacked-trait maize hybrids | + 0.9% | South America, Africa, with early gains in Brazil, Argentina, and Paraguay | Long term (≥ 4 years) |

| Digitized grain-handling infrastructure | + 0.4% | South America, particularly Brazil and Argentina, has export corridors | Medium term (2-4 years) |

| Carbon-credit monetization for low-carbon maize | + 0.3% | South America (Mato Grosso, Goiás in Brazil), with pilot programs in Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding animal-feed demand

Surging poultry and swine output in the Asia Pacific and the Middle East is translating into higher feed-maize inclusion rates, lifting import demand for South American maize [1]Source: Foreign Agricultural Service, “Grain and Feed Reports,” United States Department of Agriculture, fas.usda.gov. China’s hog herd recovered to 440 million head by mid-2025, while Southeast Asian broiler volumes climbed 7.4% year on year, raising incremental demand for competitively priced Brazilian maize delivered during its March-to-July harvest window. Importers in Vietnam and Indonesia substituted maize for wheat as wheat prices rose 19% in early 2025, moving ration inclusion from 52% to 58% and adding 3.2 million metric tons of annual demand. Gulf Cooperation Council members are also ramping up strategic poultry self-sufficiency programs that will require additional long-term maize offtake contracts with South American suppliers.

Growing bioethanol blending mandates

Brazil’s RenovaBio raises fuel-distributor obligations to purchase decarbonization credits, underpinning double-digit growth in maize-based ethanol production and stimulating the South America Maize Market [2]Source: National Agency of Petroleum, Natural Gas and Biofuels, “RenovaBio Program Updates,” ANP, gov.br/anp . Argentina raised its compulsory blend ceiling to 12% in March 2025, creating demand for an additional 1.1 million metric tons of maize feedstock and triggering commitments for USD 340 million in new crushing capacity. Paraguay’s pilot E5 (5% ethanol) mandate, scheduled for nationwide rollout by 2027, will channel local maize away from export outlets into domestic fuel production. Meanwhile, China’s provincial trials consumed 2.3 million metric tons of South American maize in 2025 and could scale nationwide by 2030 if Beijing finalizes an E10 (10% ethanol) mandate.

Trade liberalization in key importing nations

Tariff cuts under the African Continental Free Trade Area (AfCFTA) and the Regional Comprehensive Economic Partnership (RCEP) lowered landed costs for South America Maize Market exporters by USD 9–14 per metric ton, encouraging re-exports through North African hubs into sub-Saharan destinations. Saudi Arabia and the United Arab Emirates secured a duty-free quota of 3.5 million metric tons under their 2024 agreement with Mercosur, financing silo construction in Brazilian ports to anchor supply chains [3]Source: Gulf Cooperation Council Secretariat, “Agricultural Trade Agreements,” GCC, gcc-sg.org. Vietnam abolished its 5% maize duty by January 2025, purchasing an additional 680,000 metric tons from Brazil that year. Indonesia’s relaxation of Genetically Modified Organism (GMO) import restrictions added 1.2 million metric tons of Argentine and Brazilian shipments in 2025, expanding the South America Maize Market beyond traditional non-GMO niches.

Advances in stacked-trait maize hybrids

The commercial release of Corteva’s Conkesta E3, Bayer’s SmartStax PRO, and Syngenta’s Agrisure Duracade is boosting field performance and improving the competitiveness of the South America Maize Market amid erratic rainfall. In Mato Grosso, SmartStax PRO adoption saw widespread acceptance among large growers by the 2025-2026 planting season, with a significant reduction in insecticide usage observed. Public research center Brazilian Agricultural Research Corporation (Embrapa) launched BRS 3046 for smallholders, raising yields 11% while lowering nitrogen inputs by 25%. Such technology diffusion supports long-run supply elasticity despite mounting climatic stress.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile farm-gate prices | -0.9% | Global, with acute effects in South America and Africa | Short term (≤ 2 years) |

| Climate-driven yield variability | -0.7% | South America (Argentina, southern Brazil, Paraguay), and Africa | Short term (≤ 2 years) |

| Logistics bottlenecks at South American ports | -0.5% | South America, particularly Santos, Paranaguá, and Rosario | Medium term (2-4 years) |

| Rising scrutiny of glyphosate residues | -0.3% | Global, with regulatory pressure from the European Union and China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile farm-gate prices

Maize prices in Brazil fluctuated between USD 180 and USD 260 per metric ton in 2025, prompting 42% of farmers to postpone hybrid-seed purchases and compress ideal planting windows. Argentina growers withheld 8.2 million metric tons amid a 19% devaluation of the peso, triggering temporary export curbs that unsettled Asian buyers. Liquidity on Brazil’s B3 exchange fell 23%, weakening hedging capacity for exporters during the South America Maize Market peak window. Reduced forward-contracting uptake among Paraguayan cooperatives steered spot discounts and eroded long-term buyer relationships.

Climate-driven yield variability

Argentina’s La Niña drought cut 2024-2025 output by 21 million metric tons, spurring a four-month export suspension that tightened world balances and magnified price spikes benefiting other origins. Flooding in Rio Grande do Sul in May 2025 submerged 340,000 hectares at grain-fill, slashing yields by 38% and incurring USD 680 million in losses. Paraguay’s rain shortfall turned the country into a net importer for the first time since 2019, drawing 290,000 metric tons from Brazil. Bolivia’s Santa Cruz department experienced delayed sowings, cutting yields by 9%, shrinking exportable surplus for neighboring Andean markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

In 2025, Brazil accounted for 46% of South America Maize Market value, driven by its significant poultry and swine industries, increasing bioethanol production under the RenovaBio program, and consistent demand from food processors in São Paulo and Paraná. The safrinha second-crop system ensures year-round domestic supply and mitigates market disruptions during Northern Hemisphere planting periods. However, severe floods in Rio Grande do Sul in 2025 disrupted local feed mills, necessitating short-term imports from Argentina to maintain poultry feed supplies. Paraguay, while a smaller market, is the fastest-growing, with maize consumption projected to increase at a 6.8% CAGR from 2026 to 2031, supported by the development of new poultry-integration complexes and the planned implementation of a nationwide E5 ethanol mandate, boosting feed and industrial demand.

Argentina's maize consumption is concentrated in the livestock regions of Buenos Aires province and Córdoba's ethanol corridor. In these areas, dry-mill plants operated by companies such as Bunge and Archer Daniels Midland utilized additional feedstock after the blend ceiling increased to 12% in March 2025. In Uruguay, maize is used primarily in beef and dairy feed mills. A portion of the grain passing through the upgraded Nueva Palmira terminal is retained for domestic use, although the majority continues to export markets. In Bolivia, the poultry industry in Santa Cruz depends on local harvests, supplemented by Brazilian imports during periods of rainfall delays that shorten the growing season, causing the country to become a net importer. Colombia, Peru, and Chile remain structural deficit buyers, relying on Argentine or Brazilian shipments to address feed shortages caused by limited arable land and recurring droughts in the Andean and Pacific coastal regions.

Brazil's USD 2.8 billion port-modernization program is projected to reduce demurrage costs and enhance the efficiency of domestic supply chains. In Argentina, the removal of the 12% export tax starting January 2026 is anticipated to mitigate local price spikes and improve crusher margins. Landlocked Paraguay continues to face higher freight costs. However, the expansion of the Villeta terminal and the implementation of electronic warehouse receipts are improving credit access, which may encourage growers to increase production. Smaller Andean markets are projected to continue being impacted by currency fluctuations, influencing the relative cost of imported maize compared to domestic cereal substitutes, thereby introducing short-term volatility in regional trade flows. As regulations on genetically modified crops and deforestation become stricter, countries investing in traceability and climate-smart agronomy are better positioned to capture a larger share of future South American maize demand.

Competitive Landscape

The South American maize export market is led by Bunge Global S.A and Cargill Inc., two companies with extensive origination networks spanning from Mato Grosso to the Paraná River. In 2025, Bunge expanded its operations by acquiring Viterra’s elevators, increasing regional storage capacity, and enhancing its crushing network. Cargill invested in a new terminal in Santarém, aimed at reducing sailing times to Asian markets and alleviating congestion at Santos. Alongside Archer Daniels Midland, Louis Dreyfus Company, and Cofco International, the top five traders accounted for a significant share of South American maize export turnover, indicating moderate market concentration while maintaining options for farmers.

Archer Daniels Midland improved its competitiveness by integrating its dry-mill ethanol plant, integrating origination with value-added processing. Louis Dreyfus Company introduced blockchain-based sustainability certificates, which secured premiums from Japanese feed buyers and established repeat contracts for low-carbon grain. Cofco International obtained financing to construct new elevators in Mato Grosso and Goiás, enabling maize procurement in Chinese yuan and reducing currency risks for growers. These initiatives highlight a strategic focus on vertical integration, digital traceability, and currency innovation, setting each company apart in a competitive origination landscape.

Growth opportunities in the South America Maize Market depend on scaling carbon-credit programs, automating port logistics, and incorporating artificial intelligence into yield forecasting models. Bunge, Cargill, and Archer Daniels Midland are testing machine-learning tools capable of predicting farm yields before harvest, enabling pre-positioned vessels to capitalize on freight arbitrage. Louis Dreyfus Company and Cofco aim to expand farmer training in no-till farming and cover cropping, targeting additional low-carbon maize eligible for European premiums. As importers enforce stricter deforestation and residue standards, companies that integrate digital traceability with agronomic support are anticipated to capture a larger share of future South American maize exports.

Recent Industry Developments

- December 2025: India's Council of Agricultural Research (ICAR) and Argentina's National Institute of Agricultural Technology (INTA) have signed a work plan for 2025–2027 to strengthen agricultural cooperation. The agreement focuses on joint research, germplasm exchange (including maize), and sustainable technologies. Key areas of collaboration include improving food security through advancements in oilseeds, pulses, and maize, as well as technology transfers in zero tillage, drone applications, and digital agriculture.

- December 2024: The International Maize and Wheat Improvement Center released four new tropical and subtropical maize hybrids includes CIM22LAPP1A-10, CIM22LAPP1A-11, CIM22LAPP1C-10, and CIM22LAPP2A-28, offering high yields and resistance to tar spot complex, gray leaf spot, and ear rots, now available for licensing across South America

- July 2024: The Brazilian company Produce has introduced Nobre VIP3, a hybrid maize seed designed with tolerance to the fungus Pythium aphanidermatum, a known cause of stem rot. It also offers enhanced resistance to breakage and lodging, along with improved nutrient absorption. This hybrid incorporates VIP3 technology, providing protection against specific lepidopteran insect pests and tolerance to glyphosate herbicides.

South America Maize Market Report Scope

Maize, also known as corn, is a cereal grain with high productivity and geographic adaptability. There are various hybrids of maize in the market, each with its specific properties. However, it is generally categorized into two groups: white maize and yellow maize, depending on its color and taste. The South America Maize Market Report is Segmented by Geography (Brazil, Paraguay, Uruguay, Bolivia, and More). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Import Analysis (Value and Volume), Export Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, List of Key Players, Regulatory Framework, Logistics and Infrastructure, and Seasonality Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Geography

| Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Paraguay | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Uruguay | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Bolivia | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Colombia | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Peru | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Chile | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis |

| By Geography | Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Paraguay | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Uruguay | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Bolivia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Colombia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Peru | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Chile | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

Key Questions Answered in the Report

How large will the South America Maize Market be by 2031?

It is forecast to reach USD 85 billion by 2031 on a 3.72% CAGR from 2026 to 2031.

Which end-use segment is expanding fastest?

Bioethanol is projected to experience rapid growth, outpacing demand for feed, food, and industrial starch.

Why is the Middle East importing more South American maize?

Saudi Arabia and the United Arab Emirates are funding port and silo projects in Brazil to secure feed supplies as they pursue poultry self-sufficiency goals.

What challenges threaten export reliability?

Short-term risks include volatile farm-gate prices, logistics congestion at Santos, Paranaguá, and Rosario, and weather-related yield variability across Argentina and southern Brazil.

Can farmers earn additional income from carbon credits?

Yes, growers enrolled in verified no-till and cover-crop programs in Brazil and Argentina earned USD 8-12 per credit in 2025, improving profitability by up to 9%.

Page last updated on: