Europe Indoor Farming Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

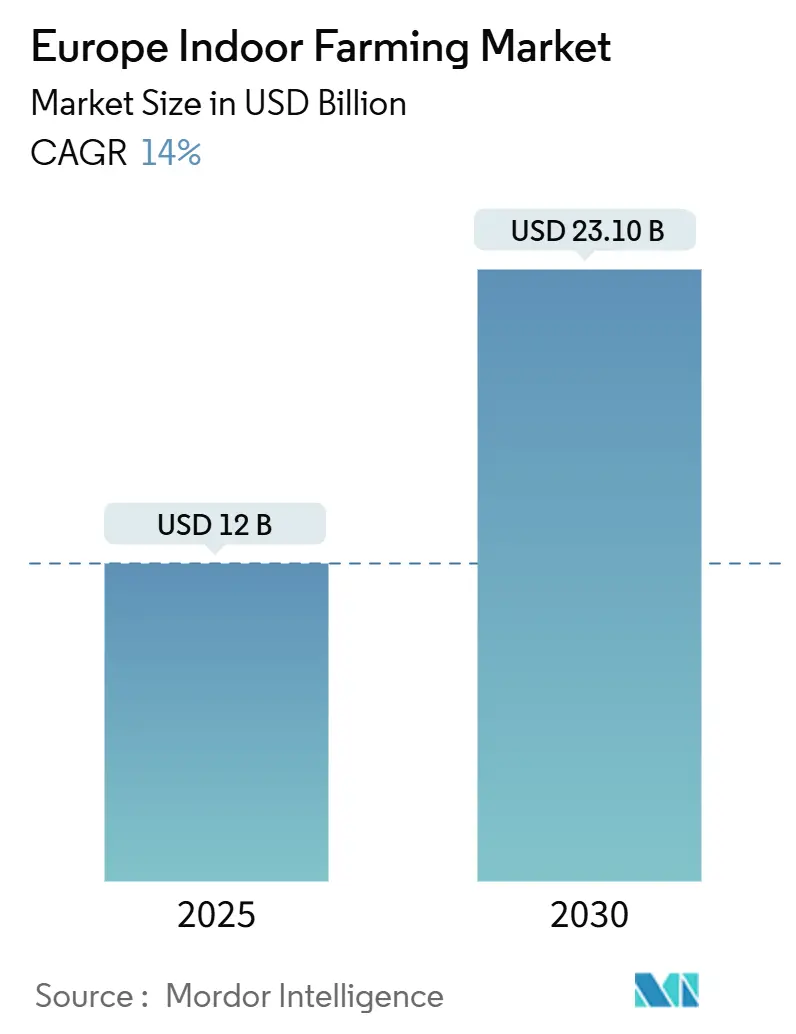

| Market Size (2025) | USD 12 Billion |

| Market Size (2030) | USD 23.10 Billion |

| Growth Rate (2025 - 2030) | 14.00% CAGR |

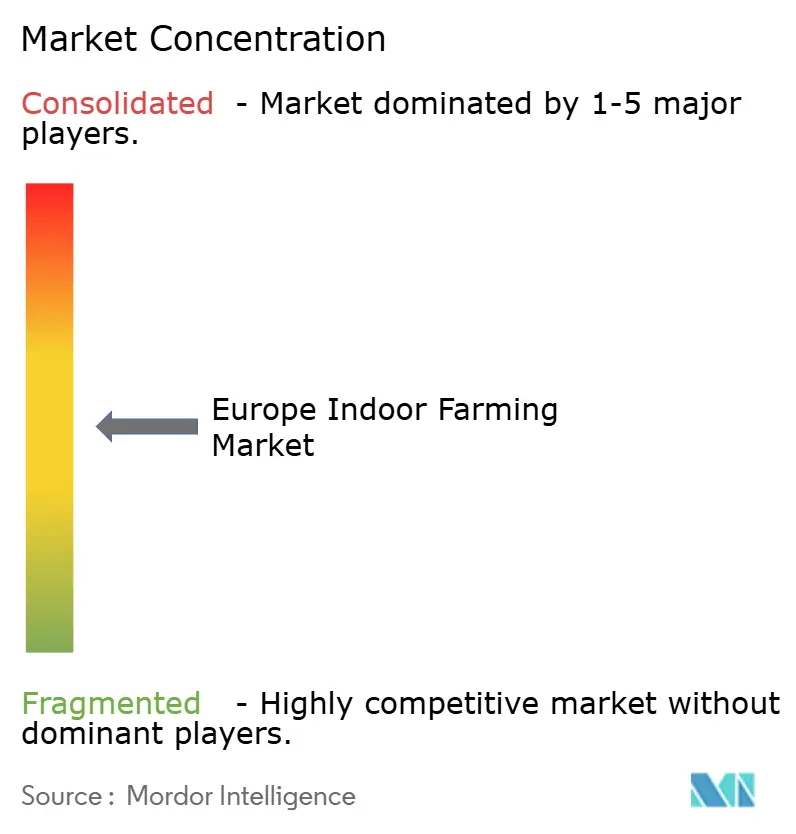

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Indoor Farming Market Analysis by Mordor Intelligence

The Europe indoor farming market size is valued at USD 12 billion in 2025 and is projected to reach USD 23.1 billion by 2030, reflecting a 14% CAGR during 2025-2030. Technology cost declines, stringent EU pesticide rules, premium retail demand, Green Deal incentives, solar-retrofitted greenhouses, and district-heat partnerships together create a strong runway for revenue growth. The market favors capital-intensive players able to integrate energy-efficient LEDs, automation software, and circular-economy heating solutions. The Netherlands leads with a 24.5% share because of its mature Westland greenhouse cluster, while Germany records the fastest expansion at a 14.5% CAGR through 2030 as urban vertical farms scale in Berlin, Munich, and Frankfurt. Hardware lighting still commands the largest revenue slice, yet software and data analytics platforms post the strongest gains thanks to AI-driven yield optimization. Energy volatility, fragmented permitting, and talent shortages remain headwinds but continue to be offset by favorable policy and financing frameworks that reward low-carbon local food production.[1]Source: European Environment Agency, “Green Deal Funding,” eea.europa.eu

Key Report Takeaways

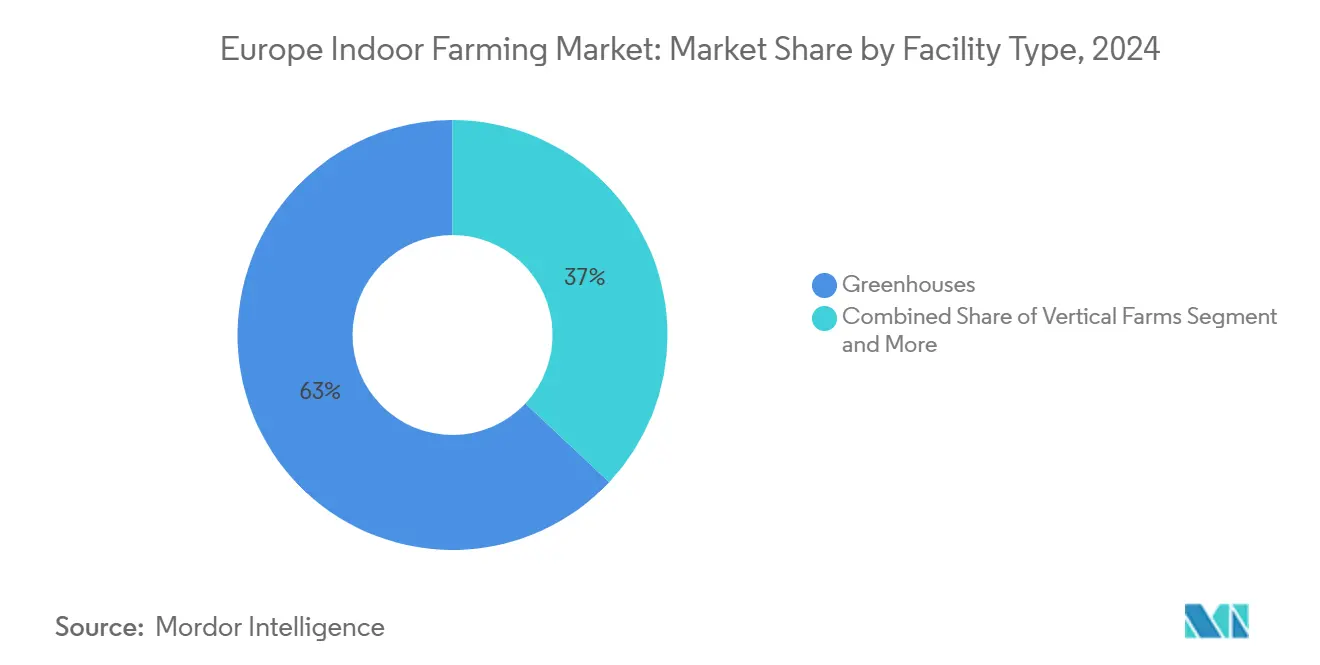

- By facility type, greenhouses led with a 63% share in 2024, while vertical farms are projected to post the fastest 18.5% CAGR through 2030.

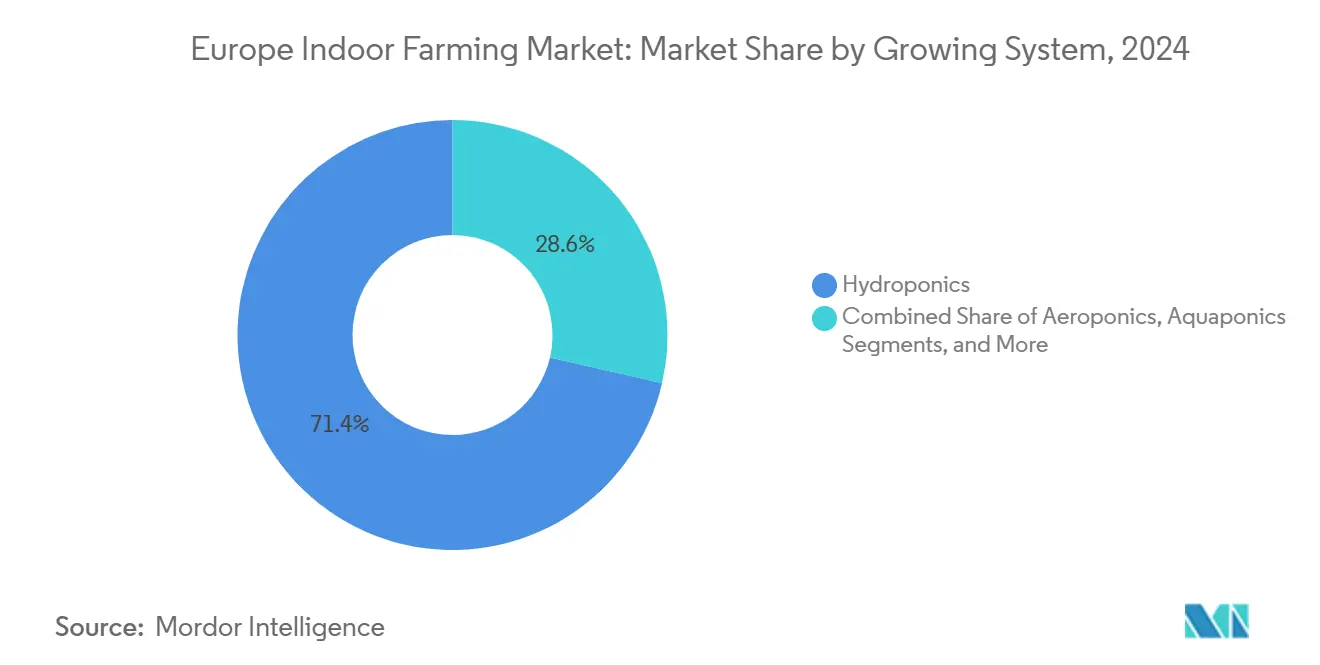

- By growing system, hydroponics dominated with 71.4% share in 2024, while aeroponics is set to expand at the highest 19.3% CAGR during 2025-2030.

- By component, lighting hardware captured 46.2% revenue share in 2024, while software solutions are forecast to advance at a 20.1% CAGR through 2030.

- By crop type, leafy greens accounted for a 58% share in 2024, while berries are on track to grow at a 17.4% CAGR to 2030.

- By geography, the Netherlands held a 24.5% share in 2024, while Germany is projected to register the quickest 14.5% CAGR over the forecast period.

Global valuation is built by aggregating outputs from multiple regions, with Europe forming one of the important contributors. Mordor Intelligence's global indoor farming market size report represents that cumulative total.

Europe Indoor Farming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid technology cost decline in LED horticultural lighting | +2.8% | Global, strongest in Netherlands and Germany | Medium term (2-4 years) |

| Tightening EU pesticide-residue regulations accelerating controlled-environment adoption | +2.1% | European Union-wide, particularly Netherlands, France, and Germany | Long term (≥ 4 years) |

| Growing demand from high-margin specialty retail chains and Michelin-star restaurants | +1.9% | Western Europe core markets, expanding to Eastern Europe | Short term (≤ 2 years) |

| EU Green Deal incentives for year-round local produce | +1.6% | European Union-wide with focus on Germany, Netherlands, and France | Long term (≥ 4 years) |

| Solar-integrated greenhouse retrofits unlocking dual-income streams | +1.4% | Southern Europe (Spain and Italy), expanding northward | Medium term (2-4 years) |

| Municipal heat-recovery partnerships with district-heating networks | +1.2% | Northern Europe (Netherlands, Germany, and Denmark) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid technology cost decline in LED horticultural lighting

Component prices for horticultural LEDs have fallen 35% over the last five years, while wall-plug efficiencies now reach 83.5%. Lower capex plus smaller power bills let growers expand lit area without raising total energy spend. Dutch tomato producers who shifted to high-efficiency toplights report up to 25% electricity savings during winter cycles. Price reductions also shorten payback periods for vertical farms whose lighting load can exceed 40% of operating cost. Equipment vendors expect another 10% efficiency gain by 2027, further lifting margins across the Europe indoor farming market.

Tightening EU pesticide-residue regulations accelerating controlled-environment adoption

The European Commission continues to phase out active substances and cut maximum residue levels, pushing field growers toward costly mitigation steps.[2]Source: European Commission, “Pesticide Residue Regulation,” ec.europa.eu Indoor systems that run hydroponics or aeroponics meet new standards without chemical inputs, giving them an advantage with retailers that audit compliance. The Farm-to-Fork goal of 50% pesticide reduction by 2030 effectively positions controlled environments as the lowest-risk supply source, stimulating investment across the Europe indoor farming market.

Growing demand from high-margin specialty retail chains and Michelin-star restaurants

Urban grocers and high-end restaurants want flavorful local produce 12 months a year. Retailers, including John Lewis, now test in-store cultivation walls to reduce shrink and raise shopper engagement. Michelin-starred chefs partner with vertical farms to secure rare leaf varieties harvested hours before plating, paying price premiums that cushion production costs. This revenue reliability encourages new entrants and accelerates the deployment of modular farms in dense European cities.

EU Green Deal incentives for year-round local produce

EU Green Deal funds cover up to 25% of capex for projects that cut food-mile emissions and reuse waste heat. Germany's sustainability mandates and urban agriculture initiatives particularly benefit vertical farming projects in major metropolitan areas, while the Netherlands leverages its existing greenhouse expertise to develop next-generation controlled environment systems. These policy frameworks address multiple EU objectives simultaneously, including food security, emission reduction, and rural economic development, creating sustained political support for indoor farming investments. Such incentives underpin the long-term bankability of Europe's indoor farming market assets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex payback periods versus open-field horticulture | -2.3% | European Union-wide, particularly affecting new market entrants | Long term (≥ 4 years) |

| Energy-price volatility post-2022 limits operating margins | -1.8% | Northern Europe (Netherlands, Germany, and United Kingdom) | Short term (≤ 2 years) |

| Fragmented EU permitting rules slowing facility build-outs | -1.2% | European Union-wide with variations by member state | Medium term (2-4 years) |

| Scarcity of agronomy talent specialized in vertical systems | -0.9% | Western Europe, expanding to Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High capex payback periods versus open-field horticulture

Advanced vertical farms cost EUR 4-8 million (USD 4.3-8.7 million) per hectare, with paybacks stretching 7-10 years. Traditional lenders still perceive technology risk, demanding 200-basis-point premiums above standard agricultural loans. The high capital requirements limit market entry to well-funded operators and create financing challenges that slow industry expansion, particularly for smaller-scale projects that cannot achieve economies of scale. Traditional lending institutions often view indoor farming as a higher-risk investment due to limited operational track records and technology risks, resulting in higher borrowing costs that further extend payback periods.

Energy-price volatility post-2022 limits operating margins

Post-2022 gas spikes lifted some Dutch heating bills from EUR 500,000 to EUR 2.5 million (USD 2.7 million) per year, prompting output cuts of 60% for vine tomatoes.[3]Source: Statistics Netherlands, “Energy Costs in Greenhouses,” cbs.nl Energy costs can represent 25-40% of total operating expenses for controlled environment agriculture, making facilities highly sensitive to price fluctuations that traditional outdoor farming does not experience. This volatility creates planning challenges for operators who must balance optimal growing conditions with energy cost management, often resulting in suboptimal crop yields during high-price periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Facility Type: Greenhouses Retain Scale while Vertical Farms Accelerate

Greenhouses generated 63% of 2024 revenue within the Europe indoor farming market. Their large footprints, mature supply chains, and proven climate controls provide economies of scale that lower unit costs on tomatoes, cucumbers, and peppers. Dutch growers routinely achieve yields above 500 metric tons per hectare, double the best open-field records, by integrating CO₂ enrichment and diffuse glass. Yet vertical farms post the highest growth at 18.5% CAGR through 2030, propelled by urban real-estate efficiencies and 20-layer racking systems that multiply square-foot output. Operators such as Jones Food Company run fully automated farms that harvest 1,000 metric tons of leafy greens per year inside repurposed warehouses.

Container farms hold a 7.5% share. Their modular shipping-container format lets retailers, campuses, and airlines deploy turnkey production near end consumers, shortening cold-chain losses. Urban Crop Solutions claims water savings of 90% versus soil cultivation thanks to closed-loop irrigation. Despite smaller capacities, container fleets create distributed networks resilient to logistics disruptions and complement large greenhouse hubs across the Europe indoor farming industry.

By Component: Lighting Hardware Leads while Software Drives Margins

Lighting hardware represented 46.2% of 2024 component sales, underscoring LEDs’ role in yield formation. Signify’s newest toplighting modules hit 83.5% efficacy and slice light-related energy costs by up to 35%. Climate control hardware ranks second, with integrated HVAC systems modulating temperature, humidity, and CO₂ at the zone level to sustain photosynthesis around the clock.

Software grows fastest at 20.1% CAGR. Platforms such as iFarm’s Growtune synthesize sensor data and machine learning to adjust light spectra, nutrient dosing, and airflow on the fly. Analytics shave 5-10% off variable costs and lift yields 10-15% by preventing abiotic stress. Service revenues follow as operators outsource calibration, remote monitoring, and agronomy consulting to vendor teams. For many investors, recurring SaaS fees enhance valuation multiples within the Europe indoor farming industry.

By Crop Type: Leafy Greens Stay on Top yet Berries Surge

Leafy greens claimed 58% of 2024 turnover. Romaine, arugula, and baby spinach prosper under vertical LEDs that tailor red-blue ratios to maximize chlorophyll synthesis. Retailers value pesticide-free labels and a two-week shelf life, reducing shrink. Berries now log the quickest growth at 17.4% CAGR. LED top-lighting tuned to far-red wavelengths improves pollination while precision cooling protects flavor volatiles, enabling year-round strawberry harvests near Paris and Milan.

Tomatoes remain a stable greenhouse staple with Dutch vine yields above 500 metric tons per hectare. Herbs such as basil and mint enjoy rising restaurant demand for just-in-time micro-bunches that retain aroma longer than field equivalents. Flower production occupies a niche where climate control guarantees Valentine’s Day and Mother’s Day supply regardless of external weather.

By Growing System: Hydroponics Dominates though Aeroponics Gains Traction

Hydroponics controls 71.4% of system revenue and remains the go-to choice for scale producers because nutrient film techniques stabilize pH and EC while minimizing root disease. Dutch lettuce farms running deep-water rafts report 25% faster cycle times versus soil beds. Meanwhile, aeroponics expands at a 19.3% CAGR. Fog nozzles deliver oxygen-rich mist, accelerating biomass accumulation and reducing water use by another 30% over hydroponics. Startups in Germany retrofit high-rise basements with aeroponic towers to maximize height and cut pumping energy.

Aquaponics combines plant and fish production to close nutrient loops. French pioneer Les Nouvelles Fermes produces 60 metric tons of vegetables and 12 metric tons of trout annually from a 5,000 square-meter site, marketing zero-waste credentials to premium shoppers. Soil-based greenhouse plots now account for only 4.4% of the Europe indoor farming market, limited to specialty crops where terroir perception commands pricing premiums.

Geography Analysis

The Netherlands secured 24.5% of 2024 revenue in the Europe indoor farming market share thanks to Westland’s cluster of climate-tech suppliers, growers, and R&D labs. Priva alone equips roughly 60% of the world’s high-tech greenhouses with automation systems. Yet high gas prices and carbon taxes push Dutch operators to electrify heating and adopt geothermal wells, keeping the market innovative.

Germany posts the continent’s fastest uptake at 14.5% CAGR. Municipalities in Berlin and Hamburg fast-track zoning for rooftop greenhouses and basement vertical farms. State-backed loans cover up to 40% of smart-sensor investment, accelerating digital adoption. France advances integrated aquaponics and vertical-soil hybrids, while the United Kingdom compensates labor shortages via robotics. Spain and Italy retrofit shade houses with PV panels to capture dual revenue streams.

Southern Europe leverages abundant sunlight. Spanish pepper houses in Almería now overlay semi-transparent PV glazing that harvests electricity without hindering PAR light. Italian basil growers in Liguria deploy seawater-cooled greenhouses to maintain humid microclimates during hot summers. These innovations illustrate regional adaptation, broadening the resilience of the Europe indoor farming market against climatic and economic shocks.

Coverage of the indoor farming market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for North America, alongside detailed country-level intelligence for Canada, each shaped by local operating conditions.

Competitive Landscape

The Europe Indoor Farming Market displays moderate concentration. Signify leads lighting components, Priva dominates climate controls, and KUBO specializes in turnkey glasshouse structures. Vertical-farm operators such as Infarm and Jones Food Company pioneer high-rise solutions but still capture single-digit shares. Competitive intensity rises as providers adopt technology-as-a-service contracts, bundling hardware, software, and agronomy for monthly fees that lower entry barriers but lock clients into proprietary ecosystems.

Strategic moves highlight convergence. In December 2024, Signify launched an 83.5% efficient toplighting range that promises 35% electricity savings, directly challenging smaller LED vendors. Jones Food Company doubled capacity at its JFC2 site to 1,000 metric tons per year, showcasing scale economics in rack-based farming. Urban Crop Solutions formed a partnership with a leading retailer to install in-store mini-farms, blending retail logistics and agriculture.

Mergers are anticipated to accelerate as energy volatility prompts growers to seek financially robust partners capable of underwriting retrofit projects. Early evidence is a cross-border joint venture between 80 Acres Farms Europe and a Dutch greenhouse builder that marries American operational playbooks with Dutch engineering pedigree. Investors focus on differentiated IP in sensors, AI, and automation to avoid commoditization within the Europe indoor farming industry.

Europe Indoor Farming Industry Leaders

Infarm Holding GmbH

Signify N.V.

Intelligent Growth Solutions (IGS Ltd.)

Jones Food Company Ltd.

Nordic Harvest A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Avisomo secured EUR 5 million (USD 5.4 million) in Series A funding to expand its vertical farming operations across European markets, with plans to deploy standardized growing modules in urban locations throughout Germany and the Netherlands. The funding round demonstrates continued investor confidence in controlled environment agriculture despite broader economic uncertainties affecting technology investments.

- December 2024: Nordic Harvest announced a partnership with a Danish district heating provider to utilize waste heat for its Østerild facility, reducing energy costs by an estimated 40% while contributing to circular economy objectives.

Europe Indoor Farming Market Report Scope

| Greenhouses |

| Vertical Farms |

| Container Farms |

| Hydroponics |

| Aeroponics |

| Aquaponics |

| Soil-based |

| Hardware | Lighting |

| Climate Control | |

| Sensors and Monitoring | |

| Software | |

| Services |

| Fruits and Vegetables | Leafy Greens |

| Tomatoes | |

| Berries | |

| Herbs | |

| Flowers | |

| Others |

| Germany |

| Netherlands |

| France |

| United Kingdom |

| Spain |

| Italy |

| Rest of Europe |

| By Facility Type | Greenhouses | |

| Vertical Farms | ||

| Container Farms | ||

| By Growing System | Hydroponics | |

| Aeroponics | ||

| Aquaponics | ||

| Soil-based | ||

| By Component | Hardware | Lighting |

| Climate Control | ||

| Sensors and Monitoring | ||

| Software | ||

| Services | ||

| By Crop Type | Fruits and Vegetables | Leafy Greens |

| Tomatoes | ||

| Berries | ||

| Herbs | ||

| Flowers | ||

| Others | ||

| By Geography | Germany | |

| Netherlands | ||

| France | ||

| United Kingdom | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the projected value of the Europe indoor farming market by 2030?

The market is forecast to reach USD 23.1 billion by 2030, expanding at a 14% CAGR.

Which country currently leads in revenue in European indoor farming?

The Netherlands holds a 24.5% share owing to its advanced Westland greenhouse cluster.

Which facility type is growing fastest across Europe?

Vertical farms record the highest growth, advancing at an 18.5% CAGR through 2030.

How are energy costs being mitigated by indoor growers?

Operators adopt high-efficiency LEDs, rooftop solar, and district-heat partnerships to lower power and heating expenses.

Page last updated on: