United States Indoor Farming Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.02 Billion |

| Market Size (2026) | USD 5.53 Billion |

| Market Size (2031) | USD 8.98 Billion |

| Growth Rate (2026 - 2031) | 10.20% CAGR |

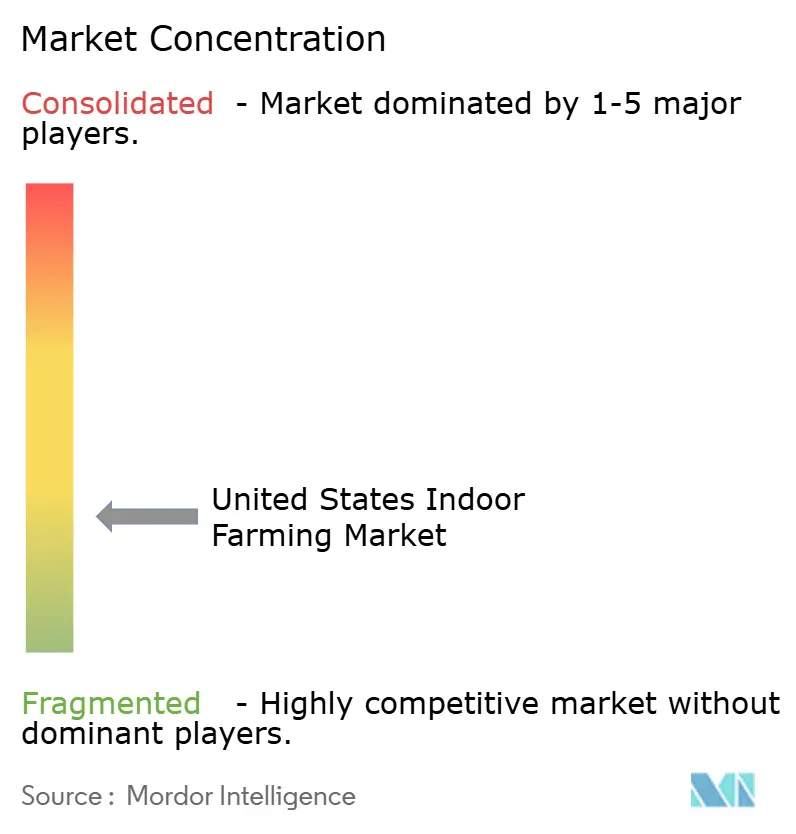

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Indoor Farming Market Analysis by Mordor Intelligence

The United States indoor farming market size was valued at USD 5.02 billion in 2025 and is projected to grow to USD 5.53 billion in 2026 and reach USD 8.98 billion by 2031, at a CAGR of 10.2% during the forecast period of 2026-2031. The market is expanding as investments continue to flow into greenhouse structures, climate control systems, fertigation technologies, and automation tools that enable controlled growing environments. Consumer demand for traceable, pesticide-free produce, along with a preference for production closer to demand centers, is driving growth. Additionally, public sourcing commitments from major grocery chains have accelerated momentum, as local and traceable produce aligns with supplier sustainability initiatives, strengthening the commercial viability of indoor farming. The 2024-2025 period saw a consolidation among vertical farm operators, which reduced interest in speculative new projects but redirected investments toward retrofitting and proven automation solutions from established providers. Research published in 2026 found that improved lighting strategies can reduce unit costs and enhance energy efficiency, thereby supporting the broader adoption of indoor farming practices over time.

Key Report Takeaways

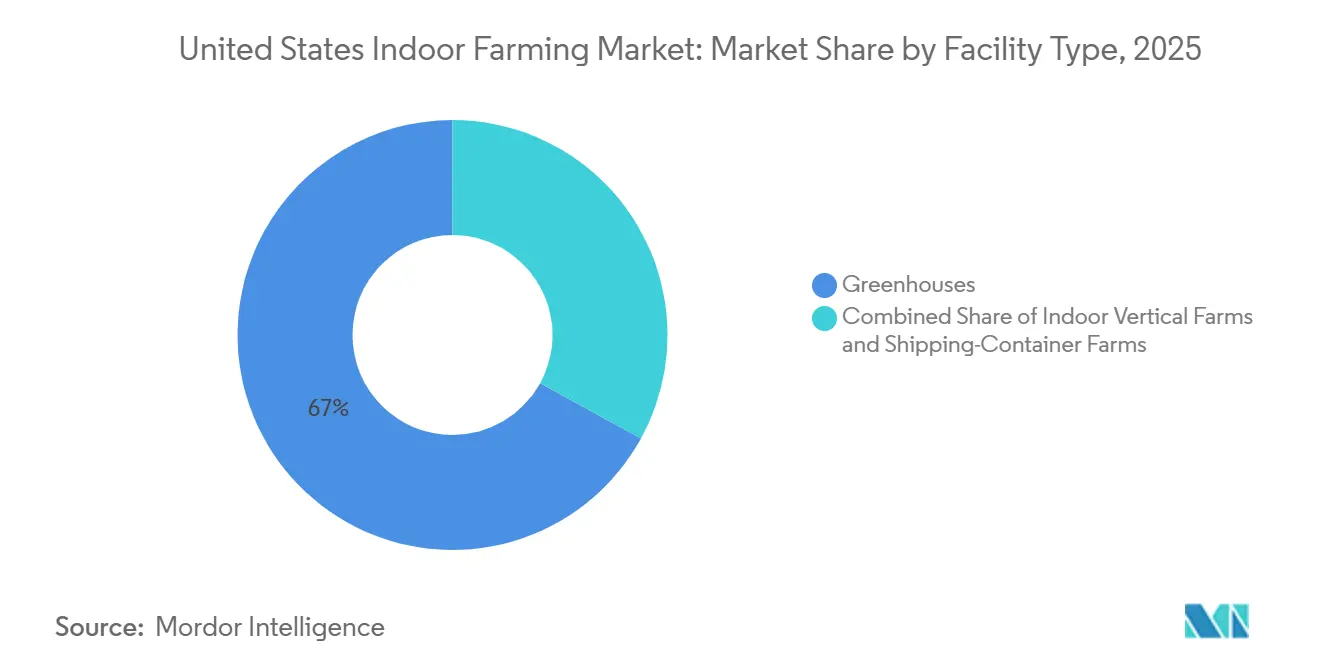

- By facility type, greenhouses held 67% of the United States indoor farming market size in 2025, while indoor vertical farms are projected to grow at a 12.5% CAGR through 2031.

- By growing system, hydroponics accounted for 56.8% of the United States indoor farming market share in 2025, while aeroponics is projected to expand at a 16% CAGR through 2031.

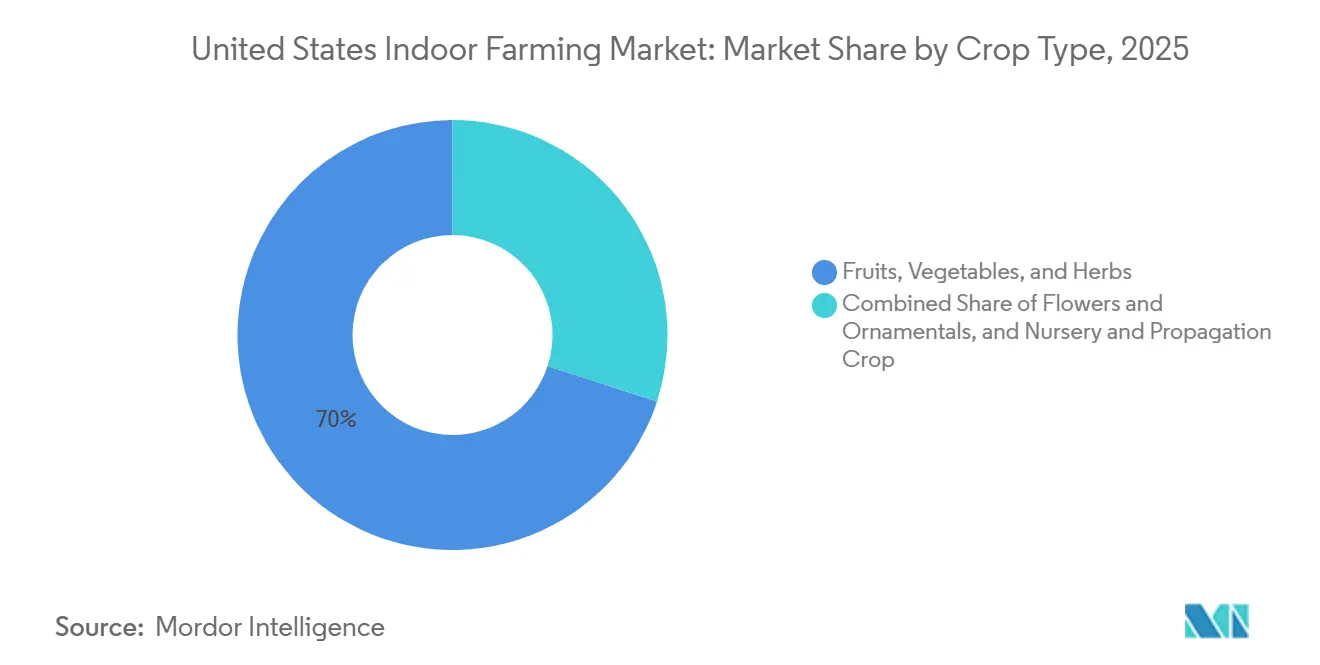

- By crop type, fruits, vegetables, and herbs captured 70% market share in 2025, while fruits, vegetables, and herbs are forecast to grow at a 10.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Indoor Farming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for Pesticide-Free Local Produce | +2.0% | Strongest in West and Northeast metro areas of the United States | Short term (≤ 2 years) |

| Year-Round Supply Resilience Requirements | +1.8% | National, with early traction in Midwest and South | Short term (≤ 2 years) |

| Water-Efficiency and Land-Productivity Gains | +1.4% | National, strongest in California and Arizona | Medium term (2-4 years) |

| LED, Automation, and Climate-Control Advances | +2.2% | National, with technology deployment led by major greenhouse operators | Medium term (2-4 years) |

| Retail Offtake Contracts Improving Project Financeability | +0.9% | National, shaped by concentrated retail buying power | Medium term (2-4 years) |

| USDA (United States Department of Agriculture) Grants and Technical Assistance for CEA Buildouts | +0.5% | National, with early uptake in rural and Midwest states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Demand for Pesticide-Free Local Produce

The demand for clean-label produce is providing the indoor farming market with a stable, sustained base, moving beyond a temporary premium niche. Consumers increasingly seek products with clear information about their origin and handling processes before reaching retail and foodservice channels. A 2024 FAO assessment reported near-zero pesticide detections in hydroponically grown lettuce, tomatoes, and strawberries, reinforcing the appeal of indoor farming as a cleaner growing method for both retailers and consumers[1]Source: Food and Agriculture Organization of the United Nations, “Pesticide Residue Profiles in Hydroponic Produce,” fao.org. These benefits are particularly significant in Western states, where stricter water policies and grocery procurement standards are being implemented. Furthermore, large retailers are transitioning local sourcing and traceability initiatives from pilot programs to mandatory supplier requirements, driving increased demand for indoor-grown produce. Participation in certified, traceable supply programs often requires enhanced monitoring, environmental controls, and automation, which, in turn, drives higher system investments across the indoor farming market.

Year-Round Supply Resilience Requirements

The indoor farming market is also gaining support from buyers who want fewer disruptions in fresh produce supply. Repeated recall events and weather-related disruptions in field agriculture pushed retailers and foodservice operators to examine production systems that can reduce exposure to soil and surface-water contamination risks. Indoor facilities offer a more controlled setting, which helps buyers manage food safety, timing, and consistency in ways open-field supply cannot always match. This shift matters because produce contracts are now judged not only on price but also on reliability throughout the year. Institutional buyers such as hospitals, universities, and correctional systems are becoming more active in local procurement models because stable supply matters as much as product quality in those settings. AmplifiedAg’s September 2025 harvest at the first United States prison vertical farm in South Carolina showed that this model can supply around 21.7 metric tons of leafy greens annually, giving a practical example of year-round institutional demand. As more buyers treat resilient local sourcing as a procurement need, the market stands to benefit from longer and more stable purchase agreements.

Water-Efficiency and Land-Productivity Gains

Water pressure in western states is turning resource efficiency into a direct growth factor for the indoor farming market. The USDA (United States Department of Agriculture) reported an 18% increase in the United States controlled environment agriculture growing area between 2022 and 2025, with a clear concentration in states facing tighter groundwater and land constraints[2]Source: USDA Agricultural Research Service, “Controlled Environment Agriculture for Food Security in North Dakota,” ars.usda.gov. The 2025 npj Science of Food study showed that controlled systems can deliver yields 10-100 times higher per unit area than open-field farming, which matters where urban-adjacent land is expensive and scarce. Indoor systems also use recirculating water layouts that help growers serve water-stressed metro markets with a more predictable resource profile. That changes the economic discussion because land and water productivity begin to offset the higher upfront equipment cost for selected crops and regions. The benefit is strongest in places such as California and Arizona, where water rules are affecting long-term crop planning and capital decisions. As more growers and buyers work within those constraints, resource efficiency remains one of the clearest structural supports for the indoor farming market.

LED, Automation, and Climate-Control Advances

Technology improvement is one of the strongest operating supports for the market because it addresses the cost gap that has historically limited large-scale adoption. A 2026 study in Frontiers in Plant Science found that continuous low-intensity lighting protocols reduced per-unit LED operating costs by 16.5% and improved energy use efficiency by 21%. A 2025 study in Scientific Reports also found that targeted deep-red and far-red LED supplementation increased fresh-weight yield by 76-79% in lettuce and basil, demonstrating that lighting quality is now directly linked to output performance. These results matter because operators no longer need to view lighting only as a fixed burden. They can increasingly manage it as a performance tool tied to yield, crop timing, and labor efficiency. At the system level, suppliers are also moving climate control from isolated site hardware to connected operating platforms, as shown by Argus Control Systems Limited’s Axia launch in October 2025, which features encrypted traffic and 5G and LoRaWAN connectivity. As these tools become easier to deploy and prove out in commercial settings, the market is shifting toward higher software and automation content per project.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex and Energy Intensity | -2.4% | National, most acute in Northeast and West | Long term (≥ 4 years) |

| Skilled Labor and Agronomy-Automation Talent Shortages | -1.1% | National, with visible gaps in Midwest and South | Medium term (2-4 years) |

| Financing Gap after Vertical Farming Failures | -1.4% | The United States is focused, strongest among venture-backed operators | Short term (≤ 2 years) |

| Zoning, Permitting, and Utility-Interconnection Delays | -0.7% | National, strongest in dense metro areas in the Northeast and West | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capex and Energy Intensity

High upfront spending remains the single largest limit on the indoor farming sector because project economics must cover both complex infrastructure and energy-heavy operations. A 2025 study found that lighting, temperature control, and ventilation accounted for around 25% of total operating costs at large United States vertical farms, which confirms that utility spending is central rather than secondary. Artificial lighting accounts for the largest energy burden in enclosed vertical farms, consuming 60-85% of total energy. These cost layers are challenging because they sit on top of depreciation from structures, controls, irrigation systems, and other installed equipment. A 2025 Energy Journal study found that combined photovoltaic and battery storage could reduce excessive energy costs in controlled environment agriculture by 25%, but the added system integration costs still raise the starting capital requirement. High industrial electricity costs in markets such as California and New York deepen this challenge because those states are often among the most commercially attractive for local produce demand. Until efficiency gains outweigh those burdens across more crop types and facility models, cost intensity will remain a major brake on the indoor farming industry.

Skilled Labor and Agronomy-Automation Talent Shortages

The indoor farming industry also faces a labor issue that goes beyond a typical hiring cycle. Operators need people who understand plant science, climate management, automation systems, data interpretation, and equipment integration. A 2025 review in the Journal of Horticultural Science and Biotechnology showed that gains in yield and energy efficiency over the last 40 years have depended on increasingly specialized and cross-functional knowledge in controlled environment systems. That means a grower can buy advanced software and hardware but still struggle to achieve performance without the right internal skill base. The burden then shifts back to equipment and platform vendors, increasing post-installation support costs and slowing scalable deployment. In September 2024, the United States Department of Agriculture and the National Institute of Food and Agriculture awarded a grant of USD 733,330 to the University of Missouri for a controlled environment agriculture undergraduate certificate program, which is a practical response but will deliver benefits over several years rather than immediately[3]Source: USDA National Institute of Food and Agriculture, “CEA Undergraduate Certificate Program, University of Missouri,” cris.nifa.usda.gov. There is also a dependence risk because operators without strong in-house agronomy teams can become tied closely to vendor service contracts and proprietary growing models. This ongoing talent mismatch will continue to limit execution quality across parts of the indoor farming market, even when equipment demand remains healthy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Facility Type: Greenhouses Remain the Primary Revenue Driver While Vertical Farms Accelerate Growth

Greenhouses accounted for 67% of the United States indoor farming market share in 2025, leading the sector due to lower capital requirements and reduced energy dependence compared to fully enclosed farms. Meanwhile, indoor vertical farms are projected to be the fastest-growing segment, growing at a 12.5% CAGR through 2031, driven by denser layouts, automation, and more efficient use of urban space. Recent projects, such as AmHydro’s Harvest Singularity facility in Florida, reflect a shift toward crop-stage-specific automation and more disciplined expansion strategies following the 2024–2025 industry shakeout.

Shipping-container farms remain a niche segment, mainly serving remote, institutional, and research applications. AmplifiedAg’s USDA (United States Department of Agriculture)-funded container projects and correctional facility partnerships highlight their continued practical relevance despite limited contribution to overall market revenue growth. Greenhouses continue to provide the industry’s stable revenue base due to their scalability, operational familiarity, and lower reliance on artificial lighting. The segment is also becoming more domestically focused. GrowSpan’s 25,000-square-foot Venlo greenhouse expansion in Iowa and Prospiant’s push toward United States-manufactured greenhouse solutions indicate a broader shift toward local sourcing, reduced import dependence, and stronger support for greenhouse retrofits and expansions across the United States.

By Growing System: Hydroponics Leads Market Volume While Aeroponics Drives Premium Yield Performance

Hydroponics held 56.8% of the United States indoor farming market size in 2025, making it the dominant growing system due to its technical familiarity, broad crop compatibility, and widespread use in commercial greenhouse production. Techniques such as the nutrient film technique and deep water culture remain popular because they enable consistent large-scale output without major operational changes. Recent innovations, including Hort Americas’ partnership with Meteor Systems, highlight how incremental upgrades can reduce costs and improve efficiency while retaining the core hydroponic model.

Aeroponics is the fastest-growing segment, projected to expand at a 16% CAGR through 2031. Its growth is driven by superior root-zone oxygenation and its suitability for high-value crops where quality outweighs volume. Research published in 2025 demonstrated that targeted deep-red and far-red LED lighting significantly improved yields of lettuce and basil, reinforcing the shift toward precision-controlled, premium production. At the same time, Lotus AgTech’s patented integration of programmable LED lighting with aeroponic feedback systems reflects the segment's increasing technological sophistication and proprietary development. Together, aeroponics and precision lighting are emerging as a key pathway for premium crop production and differentiated economics in the indoor farming industry.

By Crop Type: Fruits, Vegetables, and Herbs Segment Leads Market Share While Berries Increase Value per Square Foot

Fruits, vegetables, and herbs remained the dominant category in 2025, with a 70% share, and the fastest-growing segment at a CAGR of 10.3% during the forecast period, driven by short crop cycles, compatibility with hydroponic and aeroponic systems, and retailer demand for year-round, pesticide-free produce. Market leadership is highly concentrated in leafy greens, with AeroFarms being a major player in the United States retail microgreens market through its large Danville, Virginia, vertical farm powered by renewable energy and distributed via Costco and Whole Foods, while Little Leaf Farms leads in the indoor lettuce market and is expanding with a major Tennessee greenhouse campus launching in 2026. Indoor berries are also emerging as a premium growth segment, with Oishii raising major funding and expanding retail distribution across the United States, showing broader commercial acceptance of premium indoor-grown fruit.

Other crop categories continue to play important but more specialized roles in controlled-environment agriculture. Tomatoes, cucumbers, peppers, and herbs remain stable greenhouse revenue generators, supported by ongoing research into nutrient optimization and lighting strategies for herb production. Nursery and propagation crops are gaining attention because controlled-environment systems can improve propagation efficiency and plant health, while ornamental crops benefit from LED-based indoor production that enhances quality and uniformity. Cannabis remains one of the largest indoor-grown crop categories, though producers continue to face pressure from pricing declines, oversupply, and high energy costs tied to indoor cultivation.

Geography Analysis

The West United States maintains its position as the leading regional segment. Factors such as California’s stringent food safety and pesticide standards, recurring water stress, and the presence of dense premium retail markets drive higher demand for indoor-grown produce in the region. According to the USDA (United States Department of Agriculture), the United States controlled environment agriculture growing area increased by 18% between 2022 and 2025, with much of this growth concentrated in western states. This highlights the region's role as the most active deployment zone for newer systems. Additionally, Priva’s May 2025 partnership with a California cannabis cultivation facility for integrated climate control, fertigation, and automated vapor pressure deficit management underscores the West's leadership in system sophistication, extending beyond food crops.

The South United States is growing, with lower commercial electricity tariffs in states such as Texas, Georgia, and those along the Gulf Coast, giving growers a cost advantage over higher-cost coastal regions. Additionally, demand is expanding as institutional buyers in corrections, healthcare, and education increasingly support local production models. While the Midwest remains smaller in revenue terms, it is gaining importance as a manufacturing and engineering center for the indoor farming sector.

The Northeast is a mature market characterized by strong local produce demand but tighter project economics. Challenges such as permitting complexity and utility coordination are significant, particularly in dense metropolitan areas where land and power costs are high. Grownetics’ 2026 HiFEC benchmark, which demonstrated a 30% energy reduction in San Diego greenhouse deployments, is now relevant to operators in the Northeast, where cost control is critical due to the region's electricity pricing environment. These regional trends illustrate a multi-speed expansion path for the indoor farming market. The West and Northeast maintain greater installed depth, while the South and Midwest exhibit faster incremental growth, driven by favorable cost structures and emerging opportunities in manufacturing and institutional procurement.

Competitive Landscape

The United States indoor farming market remains fragmented, with the top five producers including Mastronardi Produce Ltd.(Sunset), Cox Enterprises, LLC, Windset Farms, Nature Fresh Farms, and Little Leaf Farms. Despite their prominence, a significant portion of the market is distributed among regional greenhouse growers, specialty vertical farm operators, and niche crop producers. In June 2025, Mastronardi Produce expanded its operations by 48 acres across Minnesota and Iowa, increasing its U.S. greenhouse footprint to over 600 acres across 15 states. This expansion supports its regional supply model, enabling faster delivery to end markets and reducing reliance on a single production base. Meanwhile, Little Leaf Farms is focusing on scaling its leafy greens production at its McAdoo, Pennsylvania campus. An April 2026 filing with the Pennsylvania Department of Community and Economic Development confirmed its next expansion phase through a contract with VB Greenhouses.

Consolidation has become a key competitive factor in the industry. Failures in 2024 and 2025 prompted retailers and lenders to favor operators with stronger revenue visibility and disciplined operations. In August 2025, 80 Acres Farms and Soli Organic merged, creating a combined entity with projected first-year revenue of approximately USD 200 million. The merged company serves over 17,000 retail locations across seven vertical farm sites, providing it with a broader commercial reach than most competitors. This merger highlights the growing importance of combining production capabilities, retail access, and brand strength to achieve scale, rather than relying solely on new standalone site developments.

Competitive opportunities are narrowing around premium specialty crops and institutional foodservice channels, where retail-led operators have yet to fully meet demand. These channels require reliable fulfillment, precise crop specifications, and strong customer relationships, favoring growers with production control and channel-specific planning. Operators lacking branded shelf presence, proprietary growing systems, or premium crop positioning face greater challenges, as capital providers have tightened underwriting standards following recent business failures. Consequently, leadership in this market is increasing defined by acreage expansion, crop-category depth, and merger-driven consolidation, rather than by footprint growth alone.

United States Indoor Farming Industry Leaders

Mastronardi Produce Ltd. (Sunset)

Cox Enterprises, LLC

Windset Farms

Nature Fresh Farms

Little Leaf Farms

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The Pennsylvania Department of Community and Economic Development recorded a VB Greenhouses contract tied to the next expansion phase of Little Leaf Farms’ McAdoo, Pennsylvania campus, confirming continued capacity growth at one of the country’s largest controlled environment leafy greens operations.

- August 2025: 80 Acres Farms and Soli Organic announced a merger to form a combined entity projecting around USD 200 million in first-year revenue and serving more than 17,000 retail locations across 7 vertical farm sites

- June 2025: Mastronardi Produce added 48 acres across Minnesota and Iowa, extending its U.S. greenhouse footprint to more than 600 acres across 15 states and reinforcing its regional distribution strategy

United States Indoor Farming Market Report Scope

Indoor farming is the practice of growing crops in controlled environments, such as buildings, warehouses, greenhouses, or shipping containers, rather than in open fields. Farmers use technologies such as artificial lighting, climate control, hydroponics, aeroponics, and vertical farming systems to manage temperature, humidity, water, and nutrients.

The United States indoor farming market report is segmented by Facility Type (Greenhouses, Indoor Vertical Farms, and Shipping-Container Farms), by Growing System (Hydroponics, Aeroponics, Aquaponics, Soil-Based, and Hybrid), and by Crop Type (Fruits, Vegetables, and Herbs, Flowers and Ornamentals, Nursery and Propagation Crops). The Market Forecasts are Provided in Terms of Value (USD).

| Greenhouses |

| Indoor Vertical Farms |

| Shipping-container Farms |

| Hydroponics |

| Aeroponics |

| Aquaponics |

| Soil-based and Hybrid Systems |

| Fruits, Vegetables, and Herbs | Leafy Greens |

| Herbs | |

| Tomatoes | |

| Cucumbers | |

| Peppers | |

| Strawberries and Berries | |

| Microgreens | |

| Flowers and Ornamentals | |

| Nursery and Propagation Crops |

| By Facility Type | Greenhouses | |

| Indoor Vertical Farms | ||

| Shipping-container Farms | ||

| By Growing System | Hydroponics | |

| Aeroponics | ||

| Aquaponics | ||

| Soil-based and Hybrid Systems | ||

| By Crop Type | Fruits, Vegetables, and Herbs | Leafy Greens |

| Herbs | ||

| Tomatoes | ||

| Cucumbers | ||

| Peppers | ||

| Strawberries and Berries | ||

| Microgreens | ||

| Flowers and Ornamentals | ||

| Nursery and Propagation Crops | ||

Key Questions Answered in the Report

What is the projected value of the United States indoor farming market by 2031?

The market is projected to reach USD 8.98 billion by 2031, rising from USD 5.53 billion in 2026 at a 10.2% CAGR over 2026-2031.

Which facility type currently leads revenue generation?

Greenhouses led in 2025 with 67% of revenue because they offer a lower-cost path than fully enclosed vertical farm formats.

Which growing system is expanding the fastest through 2031?

Aeroponics is the fastest-growing segment, with a projected 16% CAGR through 2031, supported by stronger performance in premium crops and tighter process control.

Why is local and pesticide-free produce important for commercial growth?

It supports retailer traceability goals, improves food-safety positioning, and aligns with consumer demand for cleaner produce, which helps indoor growers win longer-term supply relationships.

Page last updated on: