South America Rice Market Analysis by Mordor Intelligence

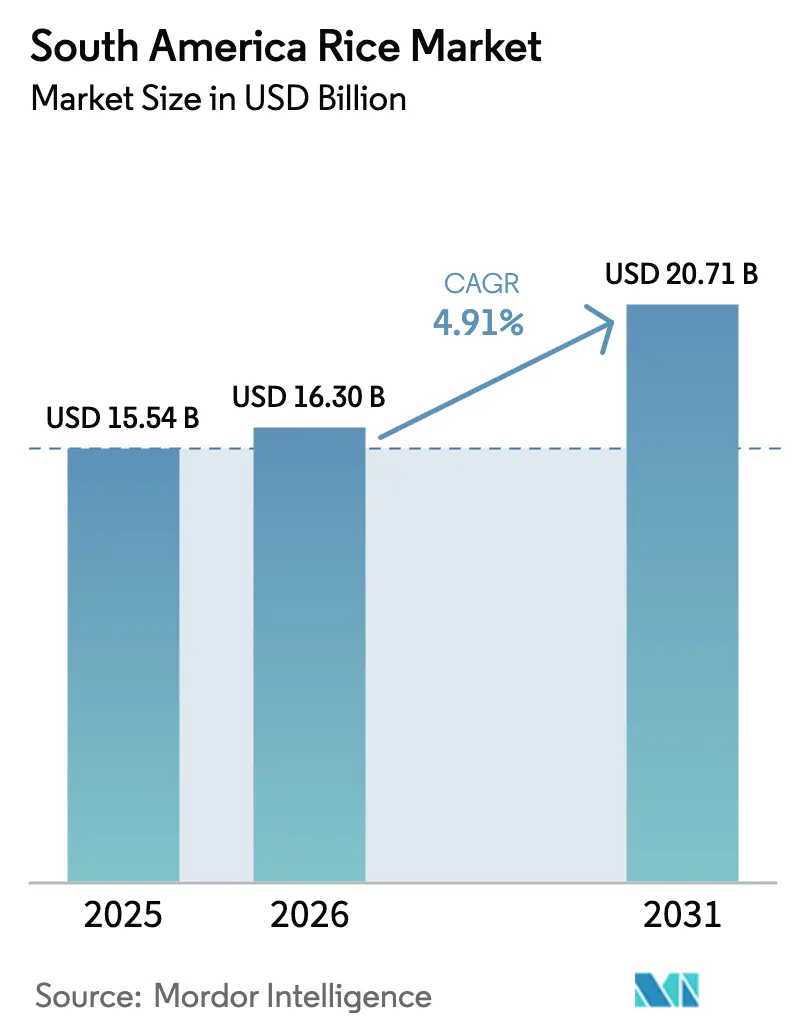

The South America rice market size is projected to expand from USD 15.54 billion in 2025 and USD 16.30 billion in 2026 to USD 20.71 billion by 2031, registering a CAGR of 4.91% between 2026 to 2031. Productivity gains from hybrid-seed adoption, mechanization on farms above 100 hectares, and expanding irrigated acreage in the La Plata Basin are sustaining growth even as El Niño-linked weather swings add year-to-year volatility. Brazil remains the production anchor, but land competition from soy and corn constrains its medium-term output. Peru’s concerted import-substitution push, together with rising per-capita consumption in coastal cities, positions it as the fastest-expanding national segment. Export-oriented suppliers in Argentina and Uruguay benefit from favorable tax regimes but face tightening pesticide-residue rules in Europe and Japan, accelerating the shift toward blockchain-based traceability.

Key Report Takeaways

By geography, Brazil led with 48.9% South America rice market share in 2025, whereas Peru is forecast to expand at a 6.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Rice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising rice productivity through hybrid-seed adoption | +0.8% | Brazil, Argentina, and Uruguay core adoption zones | Medium term (2-4 years) |

| Mechanization upgrades on medium and large farms | +0.7% | Brazil, Argentina, and Uruguay with farm consolidation | Medium term (2-4 years) |

| Expansion of irrigated acreage along La Plata Basin | +0.6% | Argentina, Uruguay, and Paraguay riparian zones | Long term (≥ 4 years) |

| Government export-revenue incentives | +0.5% | Argentina and Uruguay export-focused policies | Short term (≤ 2 years) |

| Growing intra-regional demand from food processors | +0.6% | Brazil, Peru, and Chile urban consumption hubs | Medium term (2-4 years) |

| Blockchain-based traceability premiums | +0.3% | Brazil and Argentina premium export channels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Rice Productivity Through Hybrid-Seed Adoption

Hybrid varieties deliver 15%-20% higher yields but cost more than inbred lines, which slows their uptake outside pilot programs. Embrapa commercialized two hybrids for southern Brazil in 2024, targeting farmers who accept a 30% seed premium for shorter maturity and improved lodging resistance[1]Source: EMBRAPA, “Hybrid Rice Cultivars for Irrigated Systems,” embrapa.br. Argentina’s National Institute of Agricultural Technology (INTA) is field-testing private-sector hybrids in Entre Ríos and Corrientes, with releases projected by 2026. Peru subsidized certified hybrid seed for 5,000 coastal smallholders in 2025, narrowing the yield gap between irrigated and rain-fed districts. The resulting output stability supports export commitments, even when land is shifted to soy or corn.

Mechanization Upgrades on Medium and Large Farms

Farm consolidation enables the use of capital-intensive machinery, which cuts input costs by 8%-12%. Combine-harvester deliveries to Rio Grande do Sul climbed 12% in 2024, financed by Banco do Brasil credit lines. GPS-guided planters in Argentina’s Litoral region reduced seed waste by 18% the same year. Ecuador’s Rice Cluster, backed by the Inter-American Development Bank, laser-leveled 280,000 hectares in 2024-2025, lowering water use by 20% [2]Source: Inter-American Development Bank, “Laser Land Leveling in Ecuador’s Rice Sector,” iadb.org. Profitability at mechanized farms remains positive even when prices dip below USD 400 per metric ton.

Expansion of Irrigated Acreage Along La Plata Basin

The basin supports 70% of the regional paddy land. Uruguay added 4,000 hectares of irrigated land in 2024 through public-private reservoir projects. Argentina cleared 12 new irrigation permits for Corrientes in 2025, targeting 15,000 hectares by 2027. An Inter-American Development Bank (IDB)-funded study is optimizing multistate reservoir releases to balance hydropower, navigation, and agricultural withdrawals. Reliable irrigation reduces weather-driven yield fluctuations, allowing for long-term supply contracts.

Government Export-Revenue Incentives

Argentina’s rice export tax remained at 12% in 2025, far below the 33% levy on soy, creating a relative incentive for rice cultivation in irrigated provinces. Uruguay eliminated its rice export tax in 2024, improving net-back margins by about 12% and strengthening its competitiveness in regional and Middle Eastern markets. Paraguay launched a USD 20 million program in 2025 to co-fund phytosanitary certifications and quality audits for exports to Chile and Colombia. These policy differentials shift relative returns between crops, steering acreage toward rice when soy prices soften.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| El Niño-driven flood and drought cycles | -0.9% | Brazil (Rio Grande do Sul) and Argentina (Litoral region) | Short term (≤ 2 years) |

| Competition from soy and corn for prime farmland | -0.6% | Brazil, Argentina, and Paraguay rotation zones | Medium term (2-4 years) |

| Low farm-gate prices in oversupply years | -0.4% | Argentina and Uruguay export regions | Medium term (2-4 years) |

| Logistics bottlenecks at inland waterways | -0.3% | Paraguay and Argentina Hidrovía corridor | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

El Niño-Driven Flood and Drought Cycles

The 2023-2024 El Niño slashed Rio Grande do Sul’s harvest by 15% and prompted Argentina’s first rice imports in a decade. La Niña rainfall in early 2025 then delayed planting in Uruguay’s Treinta y Tres district. International Monetary Fund (IMF) analysis indicates that a 10% deviation in rainfall leads to a 6%-8% change in rice yields, compared to 3%-5% for soybeans [3]Source: International Monetary Fund, “El Niño and Commodity Yields,” imf.org. Higher yield risk inflates insurance costs, deterring capital outlays for irrigation. The Food and Agriculture Organization of the United Nations (FAO) deployed anticipatory action plans in Bolivia, Ecuador, and Peru in 2024 to support smallholders.

Competition from Soy and Corn for Prime Farmland

In 2024, Brazil expanded its soybean cultivation by 1.2 million hectares, primarily in regions where rice and soy are rotated. Argentina's corn acreage grew by 8%, driven by favorable export prices and reduced input costs. In contrast, Paraguay's rice acreage decreased by 5% as farmers shifted to soybean cultivation due to improved crush margins and prices exceeding USD 450 per ton. Soybean and corn crops benefit from simpler agronomic practices, more developed commodity-finance markets, and higher returns per hectare. These factors continue to exert pressure on rice cultivation, which faces challenges in retaining land unless supported by export-tax relief, government incentives, or long-term contracts with processors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Brazil holds 48.9% of the South America rice market share in 2025. Demand stability masks short-term supply swings driven by weather and crop rotation. Rice imports of 2.4 million metric tons in 2025 helped balance a domestic shortfall, underscoring the continued regional interdependence. Government price-support mechanisms and public stock management further cushioned domestic volatility, reinforcing Brazil’s role as the anchor market in the region.

Peru’s segment expands at a 6.6% CAGR, the fastest in the South America rice market, aided by coastal irrigation and hybrid-seed subsidies. Domestic output rose 9% year-on-year in 2025/26 while consumption of 2.8 million metric tons still required imports, positioning Peru as a reliable outlet for Uruguayan and Paraguayan surpluses. The interplay of these two geographies illustrates how consumption growth can outpace production even in high-yield zones, preserving intra-regional trade flows despite localized weather adversity.

Argentina and Uruguay benefited from lower or zero export taxes on rice production. Both countries channel a large share of their output to neighboring Brazil and Peru. Uruguay’s long-grain competitiveness improved after it abolished export taxes in 2024, while Argentina’s remaining levy is still well below that applied to soy, which continues to make rice acreage attractive in Corrientes and Entre Ríos. This favorable tax environment supports export-oriented planting decisions and strengthens the Southern Cone’s role as a swing supplier within the South America rice market.

Regulatory Landscape

Public policy in South America continues to influence rice margins through price-support measures, trade instruments, and export-compliance requirements. In Brazil, the National Supply Company (Conab) reinforced market intervention for the 2025/2026 crop with additional commercialization support (R$ 73.6 million announced in February 2026) and authorization to run Pepro/PEP-style outflow-support auctions (up to R$ 70 million). The first auction is scheduled for May 5, 2026, targeting the outflow of 350,750 tons, and these tools are used to stabilize farm-gate prices in key producing states such as Rio Grande do Sul and Santa Catarina.

At the bloc level, Mercosur policy flexibility has been maintained via the National List of Exceptions to the Common External Tariff (LETEC), which gives members room to adjust import duties on selected tariff lines when managing shortages or inflation. For export-oriented suppliers, market access and residue compliance remain central constraints, and the EU-Mercosur agreement framework includes a phased-in, tariff-free quota for rice (rising to 60,000 tons annually after five years) managed on a first-come, first-served basis across the bloc. That structure intensifies competition among Mercosur suppliers for quota utilization and increases the need for traceability and quality systems in premium channels.

Value Chain Analysis

The regional rice value chain runs from seed and crop-protection inputs through irrigated paddy production, drying and storage, milling (including parboiling), packaging and branding, and distribution into retail, food processors, and export channels. Upstream productivity gains are supported by hybrid-seed programs (for example, Embrapa commercialized two hybrids for southern Brazil in 2024) and mechanization financed through local credit lines, while irrigation expansion in the La Plata Basin underpins more stable paddy supply for mills and exporters.

Midstream and downstream control is increasingly concentrated in integrated millers and branded players alongside global traders that manage bulk logistics. Brazil remains exposed to logistics and storage constraints, with storage concentrated off-farm and port/export capacity pressure increasing the importance of on-farm storage, efficient inland transport, and coordinated outflow programs such as Conab auctions. Cross-border supply-chain integration is also visible, including Camil Alimentos expanding its operational footprint in Paraguay (acquisition of Rice Paraguay and Villa Oliva Rice in 2025), which supports sourcing diversification and improves mill-to-market connectivity for intra-regional trade and exports.

Competitive Landscape

The South America rice market operates under a two-tier structure. Regional integrated companies dominate activities such as milling, branding, and retail, while global commodity traders primarily focus on bulk exports and logistics. In Brazil, Camil Alimentos holds approximately 30% of retail milled rice sales. Meanwhile, SLC Agrícola and Adecoagro concentrate on large-scale farming, adjusting rice acreage based on comparative returns from soy and corn. In Argentina, Molinos Río de la Plata leads the milling segment, competing with SAMAN (Ebro Foods) in Uruguay, while Alicorp plays a significant role in Peru’s milling sector.

Multinational traders such as Cargill Incorporated, Archer Daniels Midland Company, Louis Dreyfus Company Holdings B.V., Olam International Limited, and COFCO Corporation continue to manage substantial export volumes. However, increasing downstream integration by regional players is compressing their margins. SunRice Uruguay, for example, targets export markets by adhering to strict quality and phytosanitary standards, reflecting a shift toward differentiated, higher-value rice products rather than traditional bulk trading.

Recent market strategies emphasize vertical integration, capacity expansion, automation, and the introduction of convenience formats. In 2024, Josapar expanded its parboiled rice production capacity in Brazil. Similarly, Urbano Agroindustrial upgraded its processing lines in 2025 to supply supermarkets directly. Chile’s Tucapel remains a significant importer and distributor, sourcing rice from Argentina and Uruguay. Regional firms are increasingly moving closer to end consumers, thereby reducing the role of global traders in value-added segments.

Market Opportunities and Future Outlook

Differentiated exports and compliance-led segmentation create room for Southern Cone suppliers that can deliver segregated, traceable rice into demanding markets. Argentina and Uruguay are already using this pathway, and tightening pesticide-residue scrutiny in Europe and Japan is driving greater adoption of traceability systems and quality audits. This has reinforced premiums for identity-preserved lots compared with bulk shipments.

On-farm and supply-chain technology adoption is another opportunity area supported by ongoing programs and easing enabling costs. In July 2026, the Inter-American Institute for Cooperation on Agriculture (IICA) launched a technical cooperation project in Brazil, Chile, Ecuador, and Uruguay focused on sustainable rice production, including emissions measurement and public-policy work linked to climate funds. The program supports standardized reporting and farm practice upgrades. Precision agriculture tools, including UAVs, satellite imagery, and AI-based analysis, are beginning to enter regional rice agronomy, while execution gaps such as digital literacy constraints documented in Peru point to demand for service models (advisory, bundled finance, and cooperative-led deployment) rather than hardware-only offerings.

Recent Industry Developments

- July 2026: Brazil recorded its highest first-half rice export volume in the historical series tracked by Secex, increasing outflow from the domestic market. The surge affected price formation in Rio Grande do Sul and raised attention on logistics and policy tools used to manage marketing of the 2025/2026 crop.

- May 2025: Camil Alimentos completed acquisition of Rice Paraguay and Villa Oliva Rice, expanding its operational footprint in Paraguay. The transaction improves sourcing diversification and strengthens mill-to-market connectivity for intra-regional trade.

- May 2024: Brazil removed import tariffs on specific rice HS codes through the end of 2024 following floods in Rio Grande do Sul. By lowering border costs for selected rice categories, the measure supported short-term supply balancing and influenced trade flows into Brazil during a period of weather-driven production disruption.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the South America rice market is defined as the annual value of rice produced and traded across South American countries. The assessment is linked to observable production, trade, and price signals, and is expressed in USD.

Scope exclusions: We exclude downstream retail markups, retail marketing expenses, and logistics add-ons that sit outside the rice value being traded as an agricultural commodity.

Segmentation Overview

- By Geography

- Brazil

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Argentina

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Chile

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Peru

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Uruguay

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Paraguay

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Ecuador

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Bolivia

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Brazil

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with building a consistent fact base for rice area, yield, production, trade flows, and reference prices across the region. We mainly use public agricultural statistics and trade series, including FAOSTAT, USDA PSD, national agriculture ministries and statistical agencies, and UN Comtrade, to align volume totals and cross-border movements.

To translate volumes into value, we use price trend disclosures and trade unit values, then test timing around inflation, exchange rates, and local market commentary. Additional context comes from customs and port authority releases, central bank and government macro series, and peer-reviewed agronomy papers that inform yield and crop-cycle signals. For market participation cues, we also review company filings and investor presentations. When needed, paid subscriptions for company financials and an import-export shipment-level database help sanity-check directional trade movements and pricing consistency. The sources listed here are illustrative, and we also refer to other public datasets and documents for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focuses on validating the practical story behind the numbers, especially for country-level supply changes, export availability, and pricing behavior through the season. We speak with producers, millers, exporters, importers, and large buyers, and then cross-check those views with agriculture advisors and logistics-linked stakeholders across APAC, EMEA, and the Americas so assumptions stay aligned with real trade conditions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 12% | APAC: 42% |

| Mid tier: 51% | Functional/Unit leaders: 40% | EMEA: 31% |

| Smaller Players: 15% | Managers: 48% | Americas: 27% |

Market-Sizing & Forecasting

Market sizing is built using top-down and bottom-up checks, so the total value stays tied to measurable crop and trade realities. The top-down view reconstructs value by country using harvested area, yield, paddy-to-milled conversion norms, import-export volumes, and price references, and then rolls those results up to the South America total in USD.

We corroborate those totals with selective bottom-up approximations, such as sampling export unit values by major corridors, checking representative wholesale price ranges, and applying reasonable volume splits between domestic use and exportable surplus when supply tightens. When a data gap shows up, for example missing monthly price points or delayed trade reporting, we fill it with nearby proxies like trade unit values, adjacent-period averages, and interview-confirmed ranges, and then re-check that the outcome fits production and trade constraints.

For forecasting, we use scenario analysis because rice outcomes in South America are shaped by weather variability and shifts in export demand. The forward view is shaped by expected planted area intentions, yield outlook, irrigation availability, fertilizer cost direction, exchange-rate assumptions, and trade policy signals, and then adjusted based on what regional experts expect for price progression and export pull in the next seasons.

Data Validation & Update Cycle

Validation is done through multiple rounds of cross-checks so the final series behaves like the market in practice. We compare model outputs against independent signals such as production totals, export availability, importer demand cues, and price movements, and then investigate any large variances before sign-off.

If a mismatch persists, we trigger follow-ups with the same respondent groups to re-check assumptions, especially around conversion ratios, seasonality, and currency timing. Reports are refreshed annually, and interim updates are made when material events occur, including sharp weather disruptions or sudden policy shifts. Before delivery, a final analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's South America Rice Market Size Versus Other Published Estimates

Published market values for rice in South America often differ because the market can be counted at different points in the chain, and the scope can also be extended to different geographies and price bases. Even when the same crop is discussed, the choice of value definition, the year used for currency conversion, and the refresh timing can shift the final number.

The table shows a noticeable spread, and in Mordor Intelligence's model the scope is kept to the South America geography set, with value tied to production and trade linked pricing signals, rather than expanding to broader Latin America and the Caribbean or adding retail markups to reach a final consumer price.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.54 B (2025) | |

| Regional Consultancy A | USD 15.60 B (2024) | Uses a LATAM total and a 2024 base, which can pull in countries outside South America and can also reflect a different value boundary depending on whether the series is treated as packaged and retail-aligned revenue. |

| Trade Journal B | USD 18.40 B (2024) | Defines the value as revenues of producers and importers for Latin America and the Caribbean, and the wider geography plus a different price-year and currency timing can lift the reported value versus a South America-only roll-up. |

Overall, the differences mainly come from geography coverage and what part of the value chain is counted, followed by base-year pricing and exchange-rate choices. By grounding value in repeatable production, trade, and price inputs and then checking those assumptions with field feedback, the resulting estimate stays transparent and easier to reconcile across countries and seasons.

Key Questions Answered in the Report

How large is the South American rice market in 2026?

The South American rice market size is projected to be USD 16.30 billion in 2026, keeping it on track for a 4.91% CAGR to 2031.

Which country accounts for the biggest share of regional production in 2025?

Brazil holds about 48.9% South American rice market share in 2025.

Why is Peru considered the fastest-growing national segment?

Peru’s 6.6% CAGR through 2031, stems from expanding coastal irrigation, hybrid-seed subsidies, and an import-substitution program that narrows its supply gap.

How do El Niño and La Niña events affect regional output?

Rainfall extremes tied to the oscillation can swing yields by 6%-8%, prompting higher insurance costs and reinforcing investment in irrigation.

Page last updated on: