South America Cashew Market Analysis by Mordor Intelligence

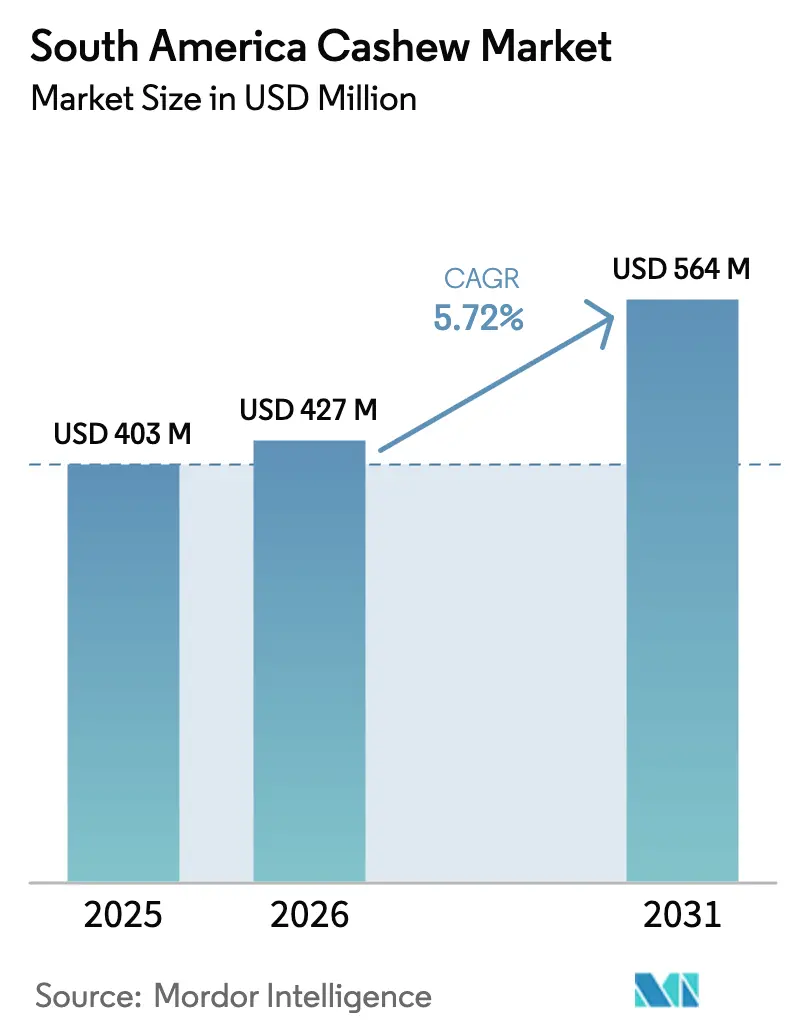

The South America cashew market size was valued at USD 403.00 million in 2025 and is estimated to grow from USD 427.00 million in 2026 to reach USD 564.00 million by 2031, at a CAGR of 5.72% during the forecast period (2026-2031). Structural shifts in global sourcing are steering multinational snack and confectionery brands toward Brazilian kernels, while integrated cashew-cocoa agroforestry is lifting smallholder resilience and raw-nut availability. State-backed drip irrigation, carbon credit monetization, and port upgrades at Pecém are compressing production and logistics costs, enabling suppliers to defend margins despite lower world reference prices. Simultaneously, droughts associated with La Niña and labor shortages during the harvest season continue to pose challenges that constrain the growth trajectory. Overall, the South America cashew commodity market is transitioning from a purely raw-nut exporter to a kernel-processing and value-added hub that can meet rising demand for traceable, non-Asian-origin products in Europe and North America.

Key Report Takeaways

- By geography, Brazil accounted for 82.5% of the South America cashew market size in 2025, while Colombia is anticipated to grow at a 12.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of South America Cashew Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of integrated cashew–cocoa agro-forestry systems | +0.8% | Brazil (Bahia, Ceará) and Colombia (Magdalena) | Medium term (2-4 years) |

| Shift of multinational roasters toward Brazilian kernel sourcing contracts | +1.2% | Global demand felt primarily in Brazil and Colombia | Short term (≤ 2 years) |

| Emergence of carbon-credit revenue streams for cashew orchards | +0.6% | Brazil (Northeast), and Peru (Piura) | Long term (≥ 4 years) |

| Digitized farm-gate procurement boosting smallholder throughput | +0.7% | Brazil (Ceará, Piauí, Bahia), and Colombia (Atlántico) | Medium term (2-4 years) |

| State-backed irrigation in Brazil’s Northeast cerrado | +0.9% | Brazil (Ceará, Piauí, and Rio Grande do Norte) | Medium term (2-4 years) |

| Port corridor upgrades lowering export freight costs | +0.5% | Brazil, with spillovers to Argentina and Chile | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Integrated Cashew–Cocoa Agro-Forestry Systems

Dual-crop planting of cashew and cocoa has shifted land-use economics in Bahia and southern Ceará, where trials posted net income 35% to 40% higher than in cashew monoculture between 2024 and 2025 [1]Source: Center for International Forestry Research and World Agroforestry, “Agroforestry Trials 2024-2025,” CIFOR-ICRAF, cifor-icraf.org. World Bank climate-smart funding of USD 22 million in 2025 accelerated adoption across 12,000 hectares by subsidizing seedlings and drip-irrigation. Cocoa’s off-season cash flow smooths farmer revenue and reduces orchard abandonment, securing processors’ raw-nut supply. Shade from cashew trees lowers cocoa heat stress, while cocoa’s deeper roots improve soil moisture retention. Colombia began pilot programs in 2025, demonstrating early replication potential along the Caribbean coast.

Shift of Multinational Roasters Toward Brazilian Kernel Sourcing Contracts

Global snack brands decreased reliance on Vietnam, which supplied 65% of world kernels in 2024, by signing multi-year Brazilian contracts in 2025 [2]Source: International Trade Centre, “Cashew Kernel Trade Statistics,” ITC Trade Map, trademap.org. Olam International added 15 cooperatives to its Vitória da Conquista buying desk, covering 4,500 smallholders. European Union imports of Brazilian kernels jumped 22% in 2025 as processors met stringent aflatoxin limits without fumigation. Locked-in 2026-2027 volumes offer processors the confidence to expand capacity, and spillover supplies are improving kernel availability for Chile and Argentina.

Emergence of Carbon-Credit Revenue Streams for Cashew Orchards

Brazilian orchards under the Verified Carbon Standard earned USD 18 per hectare in carbon credits in 2025, adding 12% to farm income in low-yield zones. Nine projects covered 18,000 hectares and issued 42,000 credits that sold at USD 12–15 per metric ton. Peru’s Piura region enrolled 1,200 hectares under Gold Standard to attract beverage-sector buyers seeking nature-based offsets [3]“Agroforestry Trials 2024-2025,” CIFOR-ICRAF, cifor-icraf.org Source: Verra, “Verified Carbon Standard Project Database,” VERRA, verra.org. High transaction fees challenge smallholders, but aggregation platforms are reducing per-hectare costs. The revenue diversifies income, delays orchard abandonment, and supports sustainability branding in premium export channels.

Digitized Farm-Gate Procurement Boosting Smallholder Throughput

Mobile platforms in Ceará and Piauí reduced intermediary margins by 15% to 20% in 2025, enabling farmers to secure real-time bids and receive earlier payments. Usibras’ WhatsApp pilot reached 2,300 growers and cut post-harvest loss by 10% through faster collection. Colombia’s AgroNet added cashew pricing dashboards, empowering cooperatives with transparent market data. Digital records also meet the traceability requirements of European buyers, who pay 20% premiums for fully documented kernels. Smartphone adoption still lags at 58% in rural Piauí, but public connectivity programs are narrowing the gap.

Restraints Impact Analysis of South America Cashew Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recurring La Niña–linked drought cycles | -0.9% | Brazil (Ceará, Piauí, Rio Grande do Norte) and Peru (Piura) | Short term (≤ 2 years) |

| Labor shortages during peak harvest in Ceará and Piauí | -0.6% | Brazil (Northeast) and Colombia | Medium term (2-4 years) |

| Limited phytosanitary labs delaying export clearances | -0.4% | Brazil with backlogs in Fortaleza and Natal | Short term (≤ 2 years) |

| Vietnam kernel oversupply suppressing global reference prices | -1.1% | Global with acute impact in Brazil, Colombia, and Peru | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recurring La Niña–Linked Drought Cycles

Rainfall in Ceará’s cashew belt was 35% to 45% below normal during the 2024-2025 season, cutting flowering and nut-set rates by up to 22% in rain-fed orchards. Peru’s Piura registered a 40% deficit in the same window, causing similar stress. Tree vigor does not fully recover in the next season, compounding losses. Climate models from the Intergovernmental Panel on Climate Change project a 15% increase in La Niña frequency by 2030, urging a faster rollout of irrigation. Only 8% of Brazilian cashew acreage held weather-indexed insurance in 2025, leaving most farmers exposed.

Labor Shortages During Peak Harvest in Ceará and Piauí

The rural labor pool in Ceará shrank 12% between 2020 and 2025 as workers moved to coastal service jobs. Daily wages reached BRL 95 (USD 19) in 2025, yet 12% of the Piauí crop remained unharvested due to a shortage of pickers. Prototype tree shakers achieved 70% efficiency but cost USD 80,000, limiting uptake to large estates. Colombia’s Atlántico region mirrors this trend, with labor shifting to banana and palm oil plantations. Mobile harvest crews are trialed, but housing and transport overheads erode savings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Brazil Cashew Market

Brazil accounts for 88.7% of regional production, utilizing 520,000 hectares of bearing orchards. However, it trails behind Colombia's growth rate of 12.5% CAGR due to the near saturation of irrigated land in Ceará and Piauí. Ceará contributes significantly to national output, but recurrent droughts have reduced rain-fed yields for 2024-2025 by 18%. The country operates 38 shelling plants, providing scale economies and enabling Brazil to secure 90.6% of exports. Despite this, per-capita domestic consumption remains low at 0.18 kg, indicating potential for increased retail demand.

Colombia Cashew Market

Colombia acts as the growth engine, centered in Atlántico, Magdalena, and Cesar, where bimodal rainfall allows two flowering cycles. Dwarf varieties enter bearing 18 months sooner and yield 30% more than traditional clones, though only four shelling lines operate domestically. Raw-nut exports to Brazil rose 40% year on year, indicating integration of cross-border processing. Investment in Colombian shelling could capture the margin now ceded to Brazilian processors.

Chile and Argentina Cashew Market

Chile and Argentina pull regional demand via imports, with Chile’s supermarket nut sections expanding 22% in volume sales during 2025. Argentina’s currency controls cap volume but lift unit value as importers focus on high-margin organic and flavored kernels. Peru’s Piura and Tumbes contribute modestly with 2,200 hectares, and new traceability laws align with the United States Food Safety Modernization Act rules to unlock North American buyers. Divergent sanitary regulations across the region invite third-party certification firms to standardize audits and lower compliance costs.

Competitive Landscape

The South America cashew commodity market is moderately concentrated. The top five processors accounted for a significant share of 2025 revenue. Usibras is one of the leading players, with 18,000 hectares and three plants with a capacity of around 45,000 metric tons. Amêndoas do Brasil follows, partnering with 4,200 smallholders and investing in roasting lines to enter retail-ready formats. Cione Alimentos holds a substantial market share by providing processing services to cooperatives that do not have the capital to invest in shellfish processing infrastructure.

Olam International’s Brazil operations have been growing steadily, integrating cashew into a broader tree-nut portfolio that shares logistics and quality control, thereby lowering per-unit costs. Grupo Agrocaju is one of the significant players focusing on organic and fair-trade kernels, exporting the majority of its output to specialty retailers in Europe and North America. Only three of the top five operate automated color sorters, leaving manual graders in smaller plants and limiting uniform quality. European buyers pay an additional 8% to 12% for blockchain-verified traceability, which Olam piloted in 2025 and has since been adopted by competitors.

Opportunities exist in value-added products such as cashew butter and milk alternatives, which currently have lower consumption levels but exhibit higher growth rates. Colombian processors are exploring joint ventures with Brazilian firms to access shelling technologies and export channels, which could recast the regional balance. In 2025, the number of Brazilian plants certified under the International Organization for Standardization Food Safety System Certification 22000 jumped from 7 to 12, becoming the baseline for European Union access. Capital intensity remains the main barrier. A 30,000 metric-ton automated facility costs over USD 15 million, discouraging new entrants.

Recent Industry Developments in South America Cashew Market

- July 2025: A field mission was conducted across Togo and Benin under the GIZ Matching Grant Fund (MGF) program. The primary objective was to evaluate the impact of efforts aimed at enhancing the sustainability of the cashew industry. The mission focused on key areas, including organic and Rainforest Alliance (RA) certification, promoting women's empowerment through innovative product ideas, and strengthening farmer groups.

- September 2025: Trade and Industry authorities in Ghana have announced emergency policy measures following a warning from Usibras Ghana about the potential relocation of its 35,000 metric-ton plant to Côte d’Ivoire. The company cited high electricity tariffs, raw nut shortages, and a 15% United States export duty as key challenges. The Brazil-based group has emphasized that resolving these issues is essential before it commits additional capital to its expansion in Africa.

- May 2025: Olam Food Ingredients Ghana Limited (ofi), has collaborated with the GIZ project Market Oriented Value Chain for Jobs and Growth in the ECOWAS Region (GIZ/MOVE-ComCashew) to officially launch the 'Cashew Apple as a Recipe for Women and Youth Empowerment' Matching Grant Fund project in Techiman. Supporting the livelihoods of cashew-producing households is a core component of ofi’s 2030 sustainability targets under its Cashew Trail initiative.

South America Cashew Market Report Scope

The South America Cashew Market Report is Segmented by Geography (Argentina, Brazil, Chile, Colombia, and More). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Import Analysis (Value and Volume), Export Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, List of Key Players, Regulatory Framework, Logistics and Infrastructure, and Seasonality Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Segmentation Overview

By Geography

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Chile | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Colombia | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Peru | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis |

| By Geography | Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Chile | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Colombia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Peru | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

Key Questions Answered in the Report

What is the current value of the South America cashew commodity market?

The market was worth USD 427 million in 2026 and is projected to reach USD 564 million by 2031.

Which country is growing the fastest in cashew production?

Colombia is forecast to grow at 12.5% CAGR from 2026 to 2031 due to new coastal plantations and policy support.

How are port upgrades influencing regional competitiveness?

The Pecém terminal expansion cut transit time to Europe by six days and lowered refrigerated-container costs by 22%, improving delivered pricing for Brazilian kernels.

What are the main threats to growth?

Recurring La Niña droughts, harvest labor shortages, and global price pressure from Vietnamese oversupply are the principal restraints on market expansion.

Page last updated on: