Saudi Arabia Indoor Farming Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

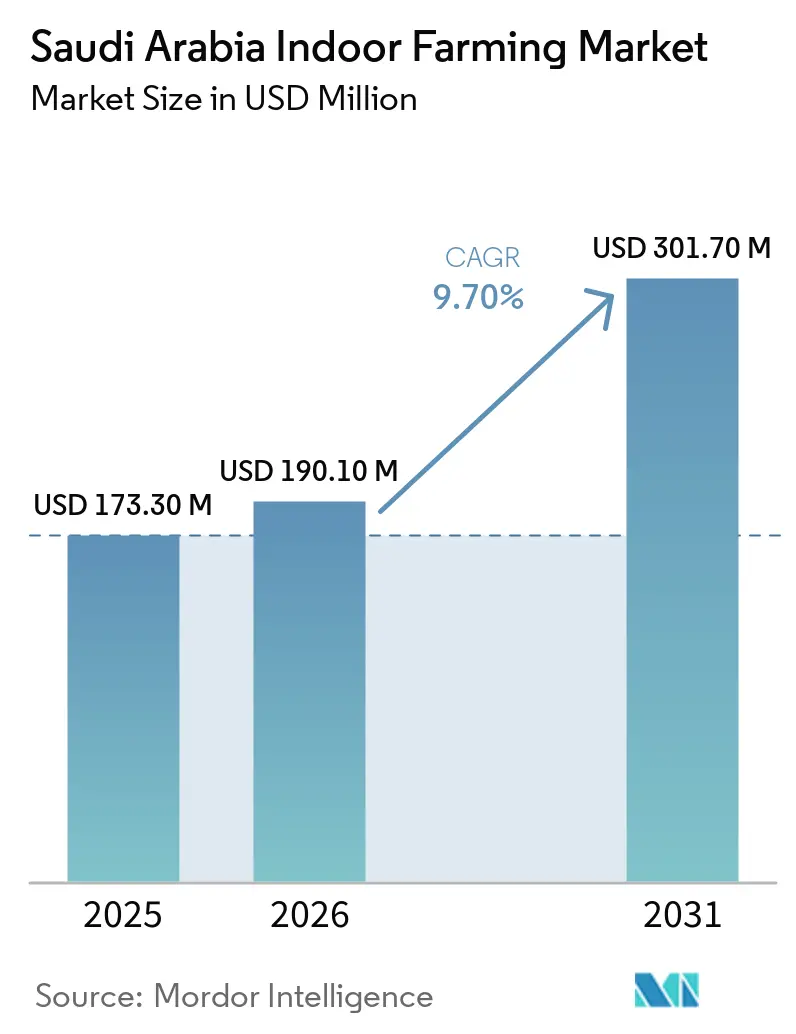

| Base Year Market Size (2025) | USD 173.30 Million |

| Market Size (2026) | USD 190.10 Million |

| Market Size (2031) | USD 301.70 Million |

| Growth Rate (2026 - 2031) | 9.70% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Indoor Farming Market Analysis by Mordor Intelligence

The Saudi Arabia indoor farming market size was valued at USD 173.30 million in 2025 and estimated to grow from USD 190.10 million in 2026 to reach USD 301.70 million by 2031, at a CAGR of 9.70% during the forecast period (2026-2031). The Saudi Arabia indoor farming market is supported by physical limits in conventional agriculture, as Saudi Arabia directed close to 88% of its freshwater to agriculture, while renewable freshwater availability stayed below 100 cubic meters per person each year, a level associated with absolute water scarcity[1]Source: John Calabrese, “Saudi Arabia's Water Future Addressing Scarcity and Ensuring Sustainability,” agsi.org. This makes recirculating production systems a practical response to water stress rather than a niche premium format, which keeps baseline demand steady even when imported produce prices move up and down. Policy support is further strengthening market demand, as Saudi Arabia continues to prioritize food security, encourage higher domestic self-sufficiency in key food categories, and expand investment in the agricultural sector under Vision 2030 initiatives. In 2026, supply-chain pressure along Gulf shipping routes is tightening fresh produce imports and helping indoor operators secure faster contract demand from premium retail and hospitality buyers. At the same time, better solar economics and integrated greenhouse design are improving the operating case for cooling-heavy facilities, although salinity treatment costs and long payback periods still limit expansion in smaller cities.

Key Report Takeaways

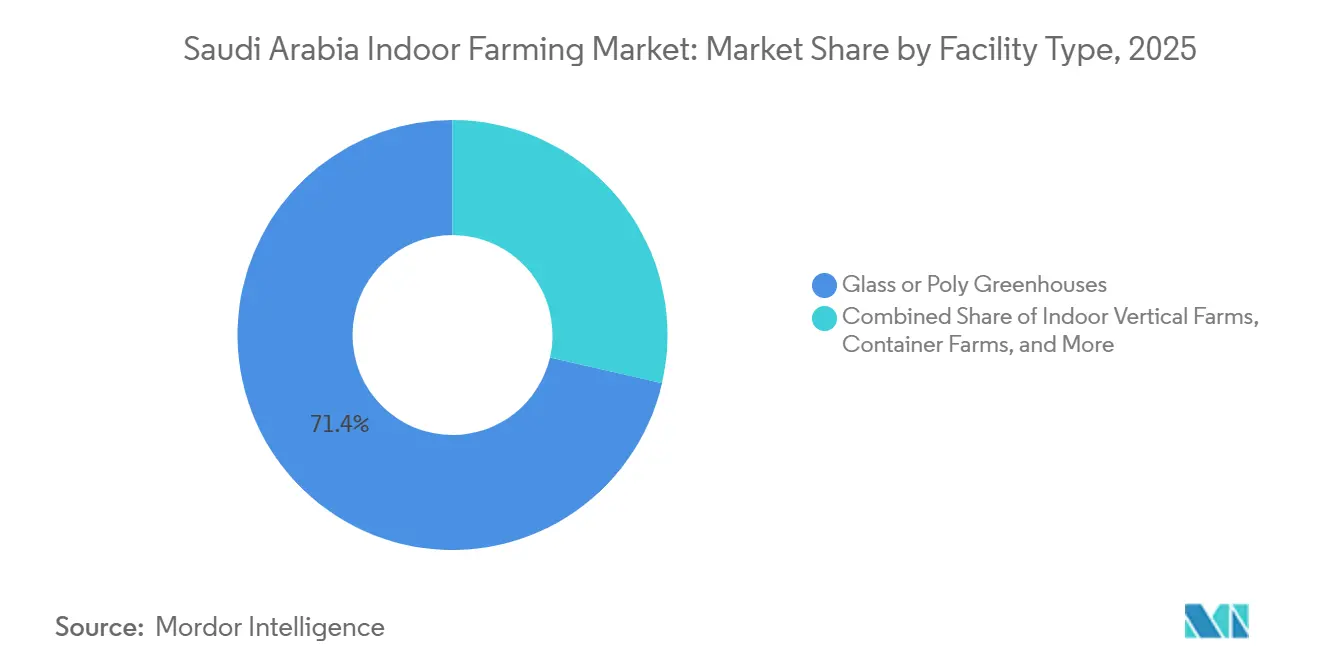

- By facility type, glass and poly greenhouses held 71.4% of the Saudi Arabia indoor farming market share in 2025, while indoor vertical farms are projected to expand at a 14.2% CAGR through 2031.

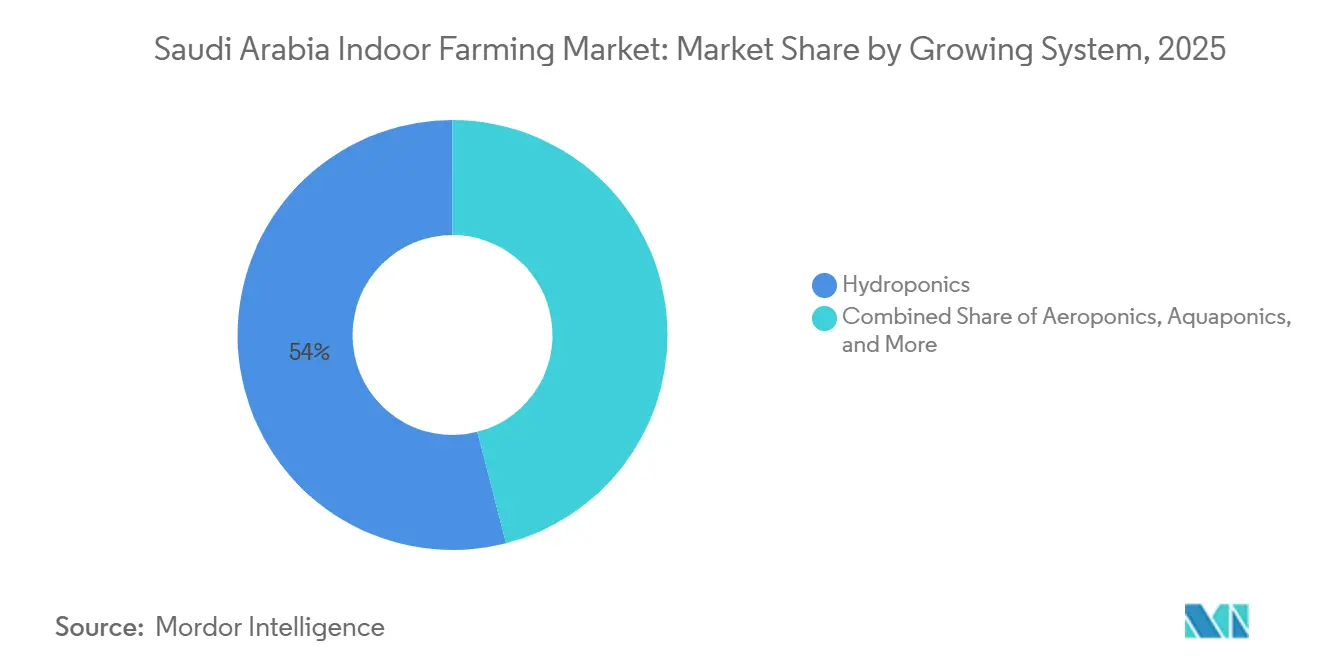

- By growing system, hydroponics held 54.0% of revenue in 2025, while aeroponics is forecast to grow at a 13.6% CAGR through 2031.

- By crop type, fruits and vegetables accounted for 63.0% of Saudi Arabia indoor farming market size in 2025, while herbs and microgreens are anticipated to grow at an 11.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Indoor Farming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water-efficient production under extreme scarcity | +1.5% | National, highest intensity in Riyadh, Eastern Province, and Madinah | Long term (≥ 4 years) |

| Food security and import substitution agenda | +1.3% | National, with spillover to secondary cities and NEOM project zones | Medium term (2-4 years) |

| Vision 2030 funding for protected agriculture | +1.1% | National, with early gains in Riyadh, Hail, Asir, and Jazan corridors | Medium term (2-4 years) |

| Retail demand for local pesticide-free produce | +0.7% | Riyadh and Jeddah urban cores, expanding to Khobar and Madinah | Short term (≤ 2 years) |

| Hotel and premium retail demand for consistent local SKUs | +0.5% | Riyadh, Jeddah, and Makkah corridor, with spillover to Red Sea and NEOM resort zones | Short term (≤ 2 years) |

| Solar-linked greenhouse economics improving unit returns | +0.4% | National, strongest in Al-Kharj, Al-Qassim, and Hail | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Water-Efficient Production Under Extreme Scarcity

Water stress remains the clearest long-term support for the Saudi Arabia indoor farming market because the country operates with renewable freshwater availability below 100 cubic meters per person each year. Agriculture consumed 12,298 million cubic meters of water in 2023, and the production base continues to rely heavily on non-renewable groundwater even as withdrawals from those aquifers are under pressure[2].Source: Mishkat Agritech Farms, “Vertical Farming in Saudi Arabia Investor Guide,” mishkat.com This is a structural constraint, not a short weather event, because aquifer depletion cannot be reversed on a commercial planning horizon. The government has already moved away from highly water-intensive cropping, including restrictions on central pivot irrigation and the phaseout of alfalfa in areas where water use is unsustainable. Hydroponic tomato production can use close to 5 liters of water per kilogram, compared with more than 200 liters in conventional field systems, which sharply changes the exposure of growers to tighter water allocation. That efficiency is why the Saudi Arabia indoor farming market keeps attracting capital even when cooling and labor costs remain high. Metering programs and possible future water pricing changes would further improve the relative economics of recirculating systems over open-field agriculture. This means water policy and water scarcity are working in the same direction for controlled-environment farming across the Saudi Arabia.

Food Security and Import Substitution Agenda

Food security policy is giving the Saudi Arabia indoor farming market a second layer of demand beyond water efficiency. Saudi Arabia imports close to 80% of its food, and annual food imports are highly significant, which keeps domestic supply resilience high on the policy agenda. The National Food Security Strategy is targeting a rise in self-sufficiency from close to 20% to 40% in priority categories by 2030[3]Source: Vision 2030, “Food Security Programme KPI Tracker,” vision2030.ai. Protected cultivation is playing a growing role in vegetable production, particularly for tomatoes, where greenhouse farming contributes significantly to overall output and supports high levels of domestic self-sufficiency. Cucumber and eggplant also reached or exceeded full self-sufficiency through a mix of open-field and protected cultivation, which shows that controlled agriculture is already affecting national food balances in selected crops. In 2026, shipping constraints around the Hormuz route are adding a direct commercial reason for retailers and institutional buyers to lock in local supply agreements with indoor operators. Multi-year offtake arrangements matter more than spot prices for new projects because they improve revenue visibility during the payback period. This gives import substitution a contract-based path into the Saudi Arabia indoor farming market rather than a purely policy-led one.

Vision 2030 Funding for Protected Agriculture

Public financing and licensing standards are strengthening the Saudi Arabia indoor farming market by lowering early capital barriers for large projects and raising the quality threshold for participation. The Agricultural Development Fund allocated SAR 825 million (USD 220 million) to high-tech greenhouse development between 2021 and 2025, with support structures that can cover up to 70% of capital costs and provide repayment periods of up to 10 years. This matters because indoor farming assets in Saudi Arabia are capital heavy from day 1 due to cooling, water treatment, automation, and cold-chain requirements. Funding support is being paired with operating standards, especially Saudi Good Agricultural Practices (GAP) and Saudi Food and Drug Authority labeling rules, which favor larger operators that can document traceability and food safety systems. That creates a market filter that is likely to keep informal growers at the edge of premium retail channels while helping structured operators move into national supply programs. The scale target for controlled-environment agriculture also remains significant, with operating area needing to rise from close to 800 hectares to more than 2,500 hectares before the end of the decade. That gap leaves room for greenhouse developers, system integrators, and crop specialists to expand together rather than compete only for replacement demand. As a result, Vision 2030 support is shaping both the investment pace and the structure of competition in this market.

Retail Demand for Local Pesticide-Free Produce

Urban retail demand is giving the Saudi Arabia indoor farming market a steady near-term demand channel, especially in Riyadh and Jeddah where modern grocery formats are well developed. Consumer preference has shifted toward local and pesticide-free produce, and retailers are responding by creating visible shelf space for domestic fresh brands. The Riyadh vertical farm began nationwide retail supply in 2026 under the Jana Farm brand, starting with Panda stores and targeting daily output of 2 metric tons within 12 months. That rollout shows that retail demand is no longer limited to trial volumes or single-store pilots. Local sourcing also gives supermarkets fresher produce with shorter transport time and less exposure to import delays, which supports repeat ordering and more stable shelf planning. In Riyadh, concentration of premium chains and higher awareness of food quality make these purchase patterns easier to scale than in smaller cities. This is one reason retail demand remains a practical growth driver for the Saudi Arabia indoor farming market even before secondary regions catch up in scale. It also supports product formats such as packaged leafy greens, herbs, and ready-to-merchandise premium vegetables that indoor facilities can supply consistently.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and long payback periods | -1.2% | National, most acute for mid-sized operators outside Riyadh and Jeddah | Medium term (2-4 years) |

| High cooling and electricity intensity | -1.0% | National, highest burden in inland sites such as Al-Kharj, Hail, and Al-Qassim | Long term (≥ 4 years) |

| Salinity and pretreatment risk in recirculating water loops | -0.6% | National, highest in Eastern Province and Red Sea coastal zones with brackish groundwater | Long term (≥ 4 years) |

| Imported seed, pollinator, and spare-part dependence | -0.5% | National, with spillover risk from GCC logistics disruptions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex and Long Payback Periods

Capital intensity continues to limit the speed of expansion in the Saudi Arabia indoor farming market, especially for new local operators without large balance sheets. Commercial vertical farms can cost USD 10-30 million per acre, which immediately narrows the field of possible entrants. Even a more standard greenhouse model can require a payback period of 5 years in favorable scenarios once cooling systems, solar integration, and cold-chain assets are included. That slows reinvestment because operators must wait longer before one asset can fund the next phase of expansion. Concessionary lending helps, but it does not fully remove the need for upfront equity and operating buffers during ramp-up. The challenge is sharper outside Riyadh and Jeddah, where premium buyer density is lower and utilization risk is harder to absorb. The Saudi-China Forum agreements signed in 2025 may lower equipment costs through technology partnerships, but that benefit is more likely to reach larger projects first. As a result, the market is expanding, but the pipeline of middle-tier operators remains limited compared to the level of demand.

High Cooling and Electricity Intensity

Thermal management remains a direct operating challenge for the Saudi Arabia indoor farming market because summer temperatures frequently move above 45°C. Energy can account for 25-35% of operating costs in facilities without renewable integration, which keeps margins exposed to cooling demand. The cost problem is not uniform across facility types. Glass greenhouses can use evaporative cooling, shading, and heat-blocking materials, while fully enclosed vertical farms rely on active refrigeration across the entire production envelope. Iyris developed SecondSky covers that have reduced energy use by more than 40% and water use by 30% at customer installations, which shows that greenhouse formats still have room to improve under Saudi climate conditions. Vertical farms do not have the same passive relief options, so their cost base is harder to manage unless crop value is very high. This is why blended production models, where greenhouses handle bulk output and vertical modules focus on premium crops, are often more practical than fully enclosed formats across an entire crop mix. Inland regions such as Al-Kharj, Hail, and Al-Qassim face an even heavier burden because heat loads are prolonged and cooling cycles are longer. Until design efficiency improves further, energy intensity will remain one of the main limits on wider regional spread.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Facility Type: Glass and Poly Greenhouses Dominate While Vertical Farms Scale

Glass and poly greenhouses accounted for 71.4% of the Saudi Arabia indoor farming market size in 2025, which kept them as the core commercial format for large-volume production. Their lead reflects decades of operating experience in the Kingdom and the ability of large glasshouses to produce at scale under severe summer conditions. Saudi Greenhouses Management and Agri. Marketing Co. manages 115 hectares across 12 farms, while DAVA Agricultural expanded from 85 hectares to 107 hectares of high-tech glass hydroponic greenhouses and reached a daily output of close to 170 metric tons of vegetables. These formats suit tomatoes, cucumbers, peppers, and strawberries because they support scale, crop control, and retailer-grade quality in a single system.

Indoor vertical farms are projected to grow at a 14.2% CAGR through 2031, making them the fastest-growing facility type in the Saudi Arabia indoor farming industry. These systems are particularly well-suited for premium leafy greens, herbs, and specialty crops, where high yield density and consistent quality are more important than bulk output. Meanwhile, container farms and deep-water culture systems continue to address modular and niche applications, including pilot projects and urban supply models. As a result, the market is evolving into a two-track structure, with greenhouses leading in large-scale production and vertical farms driving growth in the premium segment.

By Growing System: Hydroponics Leads While Aeroponics Gains Traction

Hydroponics held 54.0% of Saudi Arabia indoor farming market share in 2025, which kept it as the main operating model across the Saudi Arabia indoor farming market. Its lead comes from compatibility with the Kingdom’s water conditions and from the fact that growers can pair selective pretreatment with precise nutrient delivery instead of relying on soil under saline conditions. Its scalability has already been demonstrated under local conditions, reinforcing confidence among commercial operators. In addition, public financing frameworks continue to favor hydroponic systems, particularly those that can demonstrate high water-use efficiency, such as Nutrient Film Technique (NFT) and deep-water culture setups.

Aeroponics is projected to grow at a 13.6% CAGR through 2031, making it the fastest-growing system type in the Saudi Arabia indoor farming market. The system can use up to 40% less water than equivalent hydroponic setups and can lift growth rates by up to 30%, which makes it attractive as water pricing pressure rises. Aquaponics is advancing through government-supported projects, reflecting growing interest in integrated fish and plant production systems. At the same time, soil-based and hybrid approaches remain important for operators targeting a wider crop mix, particularly in flowers and ornamentals where root-zone flexibility is beneficial. Overall, hydroponics continues to serve as the commercial foundation, while aeroponics and aquaponics are expanding from a smaller but rapidly developing base.

By Crop Type: Fruits and Vegetables Dominate Revenue While Herbs and Microgreens Accelerate

Fruits and vegetables held 63.0% of revenue in 2025 and represented the broadest commercial demand base in the Saudi Arabia indoor farming market. Tomatoes, cucumbers, peppers, lettuce, and strawberries dominate this segment because they align well with greenhouse economics and national food-security priorities. Advancements in greenhouse cultivation and varietal trials are further supporting the expansion of premium fruit production within protected systems.

Herbs and microgreens are projected to expand at an 11.9% CAGR through 2031, and this segment is building share through premium retail and hospitality demand rather than volume alone. Products such as basil, rosemary, thyme, sage, dill, oregano, and arugula are increasingly cultivated to meet the need for a consistent, high-quality, year-round supply. Flowers and ornamentals, while smaller in overall market contribution, are benefiting from rising demand linked to events, hospitality, and premium gifting. This results in a differentiated crop mix, where staple vegetables drive production scale, while specialty greens and ornamentals contribute to higher-margin growth within the Saudi Arabia indoor farming market.

Geography Analysis

Riyadh held 38% of the Saudi Arabia indoor farming market share in 2025, making it the largest regional base for demand, financing, and commercial execution. The region benefits from dense logistics networks, premium supermarkets, hotel demand, and a consumer base that is more familiar with local pesticide-free produce. Retail adoption by Panda and other large chains has improved shelf access for local brands and created steadier offtake for indoor growers in and around the capital. Riyadh also benefits from applied agritech activity around research and startup formation, which shortens the time between technology testing and commercial deployment.

The Jeddah and Makkah corridor is emerging as the fastest-growing regional cluster in the Saudi Arabia indoor farming market, supported by strong demand from hospitality, premium retail, and urban consumption centers. Its proximity to major ports and its role in serving pilgrimage-driven demand make it well-suited for high-value crops such as herbs, berries, leafy greens, and packaged specialty produce. The presence of advanced indoor farming operations in Jeddah, including commercial greenhouses and vertical farms, highlights the region’s ability to support diverse production formats within a single, integrated ecosystem.

Other regions remain smaller in scale but are gradually expanding the national supply footprint as investment activity moves beyond the primary urban hubs. The eastern production belt around Al-Kharj is gaining importance, supported by established greenhouse operators producing export-grade output and serving both domestic and international markets. Hail has also emerged as a notable location, with the development of integrated aquaculture and agriculture systems that combine fish production with crop cultivation. Meanwhile, Jazan is opening new opportunities for hydroponic greenhouse investments, particularly in soilless vegetable production. These developments indicate that future market expansion is likely to be concentrated in specific regional corridors that benefit from strong policy backing, favorable land availability, and improving solar-linked economics, rather than a uniform expansion across the country.

Competitive Landscape

The Saudi Arabia indoor farming market remains fragmented, with the leading players collectively accounting for a limited share of total market presence. Companies such as DAVA Agricultural Company and Saudi Greenhouses Management and Agri. Marketing Co. lead in large-scale greenhouse operations, while Pure Harvest Smart Farms, MOWREQ Specialized Agriculture Company, and Mishkat Agritech Farms are prominent in controlled-environment technologies, premium crop production, and branded retail supply. This structure indicates that no single company dominates the market, with different players holding strong positions across distinct operating models. It also suggests potential for future consolidation as access to financing improves and project sizes continue to scale up.

Strategic activity in the Saudi Arabia indoor farming market is increasingly centered on expanding distribution reach, improving technology efficiency, and building scalable operating platforms. Companies are forming partnerships to expand market access beyond domestic boundaries while also investing in advanced technologies, such as smart lighting systems that optimize energy use and crop performance. For instance, DAVA Agricultural Company has strengthened its regional presence through partnerships that expand the trade of fresh produce across the Gulf Cooperation Council (GCC).

Open opportunities remain strongest in premium herbs and microgreens, aquaponics, and localized greenhouse development services, particularly for projects supported by government financing. Emerging players are also addressing equipment and deployment challenges by offering faster and more cost-effective hydroponic system installations through localized sourcing. This is particularly relevant for smaller operators that require lower upfront investment alongside reliable demand channels. However, established companies with strong retail linkages, certified quality standards, and integrated logistics are anticipated to maintain their position in bulk vegetable production, leaving specialty and premium segments as the more accessible entry point for new entrants.

Saudi Arabia Indoor Farming Industry Leaders

DAVA Agricultural Company

Saudi Greenhouses Management and Agri. Marketing Co.

Pure Harvest Smart Farms

MOWREQ Specialized Agriculture Company

Mishkat Agritech Farms

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: DAVA Agricultural Company partnered with NRTC Holding Group to enhance GCC agri-food sector cooperation and fresh produce trade, leveraging DAVA's 107 hectares of hydroponic greenhouses producing approximately 170 metric tons of vegetables daily. The alliance signals DAVA's intent to expand its distribution reach beyond Saudi Arabia into regional GCC markets.

- January 2026: MOWREQ Specialized Agriculture Company began nationwide retail supply of fresh produce from their Riyadh vertical farm to Panda stores across Saudi Arabia under the Jana Farm brand, targeting a daily output of 2 metric tons within 12 months of launch.

- March 2025: Saudi Greenhouses Management and Agri. Marketing Co. partnered with Topian, the NEOM food company, to establish the Horticulture Innovation Center at the University of Tabuk, supporting controlled-environment agriculture training and innovation, thereby driving market growth through faster technology adoption and skill development.

Saudi Arabia Indoor Farming Market Report Scope

Indoor farming is the practice of growing crops or plants inside enclosed structures such as buildings, warehouses, greenhouses, or containers, where environmental conditions like light, temperature, humidity, and nutrients are controlled artificially to improve plant growth and productivity.

The Saudi Arabia Indoor Farming Market is segmented by Facility Type (Glass or Poly Greenhouses, Indoor Vertical Farms, Container Farms, Indoor Deep-Water Culture Systems, and Other Facility Types), by Growing System (Hydroponics, Aeroponics, Aquaponics, Soil-Based and Substrate-Based, and Hybrid), and by Crop Type (Fruits and Vegetables, Herbs and Microgreens, and Flowers and Ornamentals). The report provides market size and forecasts in terms of value (USD).

| Glass and Poly Greenhouses |

| Indoor Vertical Farms |

| Container Farms |

| Indoor Deep-Water Culture Systems |

| Other Facility Types |

| Hydroponics |

| Aeroponics |

| Aquaponics |

| Soil-Based and Substrate-Based |

| Hybrid |

| Fruits and Vegetables | Tomatoes |

| Cucumbers | |

| Bell Peppers | |

| Lettuce and Leafy Greens | |

| Strawberries | |

| Other Fruits and Vegetables | |

| Herbs and Microgreens | Basil |

| Mint | |

| Parsley | |

| Arugula | |

| Other Herbs and Microgreens | |

| Flowers and Ornamentals | Cut Flowers |

| Ornamental Plants | |

| Other Flowers and Ornamentals |

| By Facility Type | Glass and Poly Greenhouses | |

| Indoor Vertical Farms | ||

| Container Farms | ||

| Indoor Deep-Water Culture Systems | ||

| Other Facility Types | ||

| By Growing System | Hydroponics | |

| Aeroponics | ||

| Aquaponics | ||

| Soil-Based and Substrate-Based | ||

| Hybrid | ||

| By Crop Type | Fruits and Vegetables | Tomatoes |

| Cucumbers | ||

| Bell Peppers | ||

| Lettuce and Leafy Greens | ||

| Strawberries | ||

| Other Fruits and Vegetables | ||

| Herbs and Microgreens | Basil | |

| Mint | ||

| Parsley | ||

| Arugula | ||

| Other Herbs and Microgreens | ||

| Flowers and Ornamentals | Cut Flowers | |

| Ornamental Plants | ||

| Other Flowers and Ornamentals | ||

Key Questions Answered in the Report

What will be the size of Saudi Arabia's indoor farming market by 2031?

The Saudi Arabia indoor farming market is projected to reach USD 301.70 million by 2031 from USD 190.10 million in 2026, growing at a 9.70% CAGR over 2026-2031.

What is driving demand for indoor farming in Saudi Arabia?

Water scarcity, food security policy, import substitution, and rising demand for local pesticide-free produce are the main demand drivers. Renewable freshwater availability is below 100 cubic meters per person each year.

Which facility type leads revenue in Saudi Arabia?

Glass and poly greenhouses led with 71.4% of facility-type revenue in 2025 because they support large-scale commercial vegetable production under Saudi climate conditions.

Which crop category is growing the fastest?

Herbs and microgreens are the fastest-growing crop category, with an anticipated 11.9% CAGR through 2031, supported by hospitality and premium retail demand.

Page last updated on: