South America Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

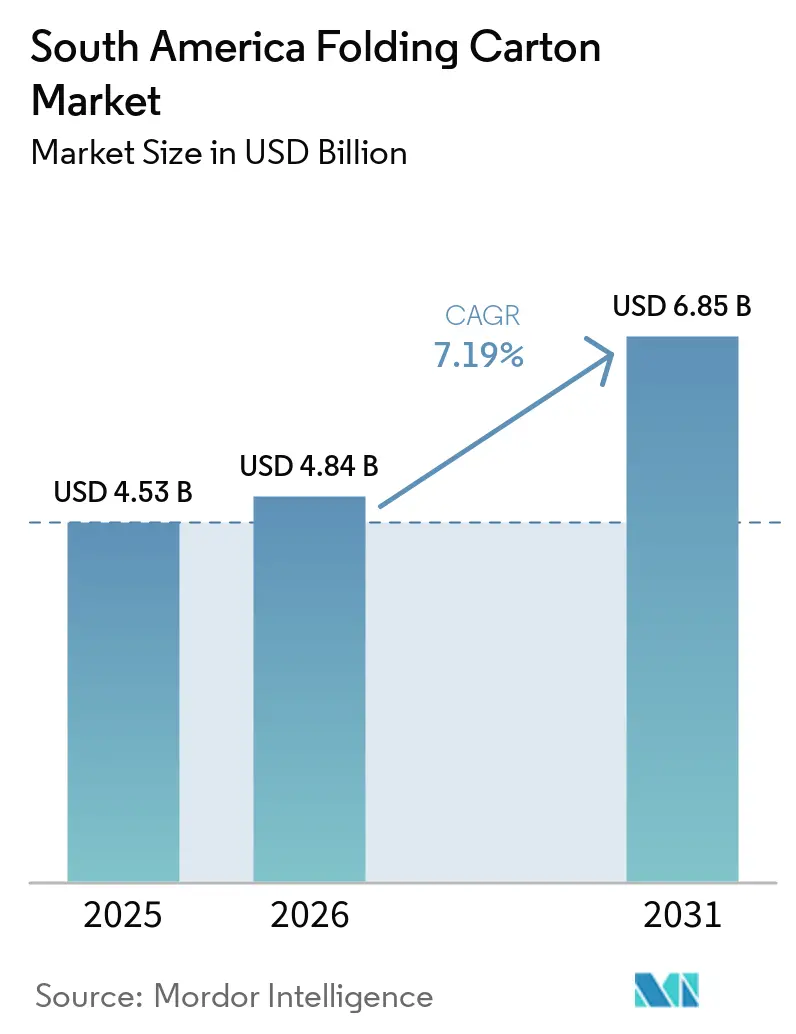

| Base Year Market Size (2025) | USD 4.53 Billion |

| Market Size (2026) | USD 4.84 Billion |

| Market Size (2031) | USD 6.85 Billion |

| Growth Rate (2026 - 2031) | 7.19% CAGR |

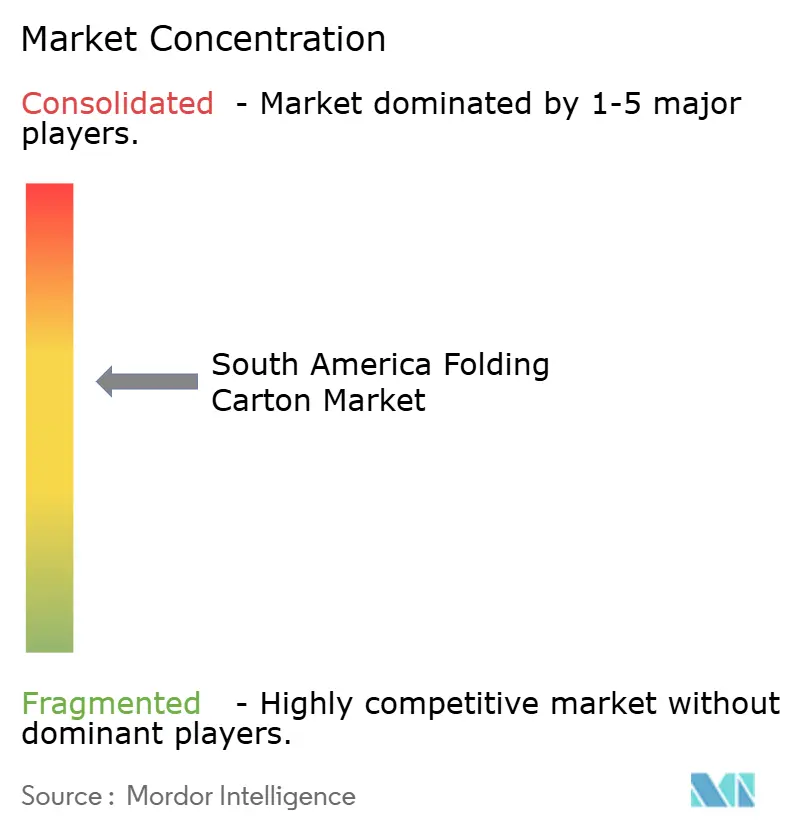

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Folding Carton Market Analysis by Mordor Intelligence

The South America folding cartons market size is expected to increase from USD 4.53 billion in 2025 to USD 4.84 billion in 2026 and reach USD 6.85 billion by 2031, growing at a CAGR of 7.19% over 2026-2031. Rapid e-commerce adoption, brand owner migration to fiber-based monomaterials, and plastics‐reduction rules across MERCOSUR economies are driving demand. Vertically integrated pulp-to-packaging chains in Brazil give domestic converters a cost edge, while capacity additions by Klabin and Suzano are easing supply tightness in specialty boards. Regional retailers are pressing suppliers for shelf-ready secondary packs that cut in-store labor, and multinationals are near-sourcing consumer-goods production to hedge logistics risk. Digital printing, barrier-coated boards, and premium substrates such as solid bleached sulfate are emerging as growth hot spots within the South America folding cartons market.

Key Report Takeaways

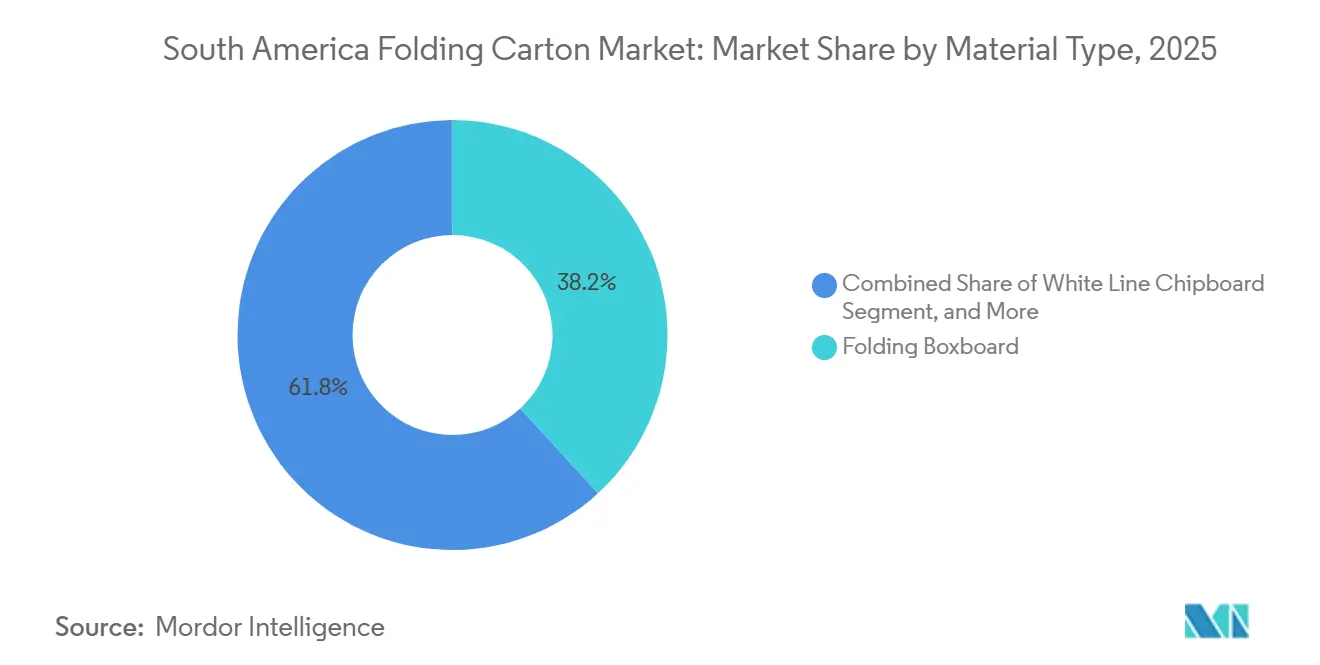

- By material type, folding boxboard captured 38.16% of the South America folding cartons market share in 2025.

- By printing technology, the South America folding cartons market size for the digital printing segment is forecast to advance at a 9.03% CAGR through 2031.

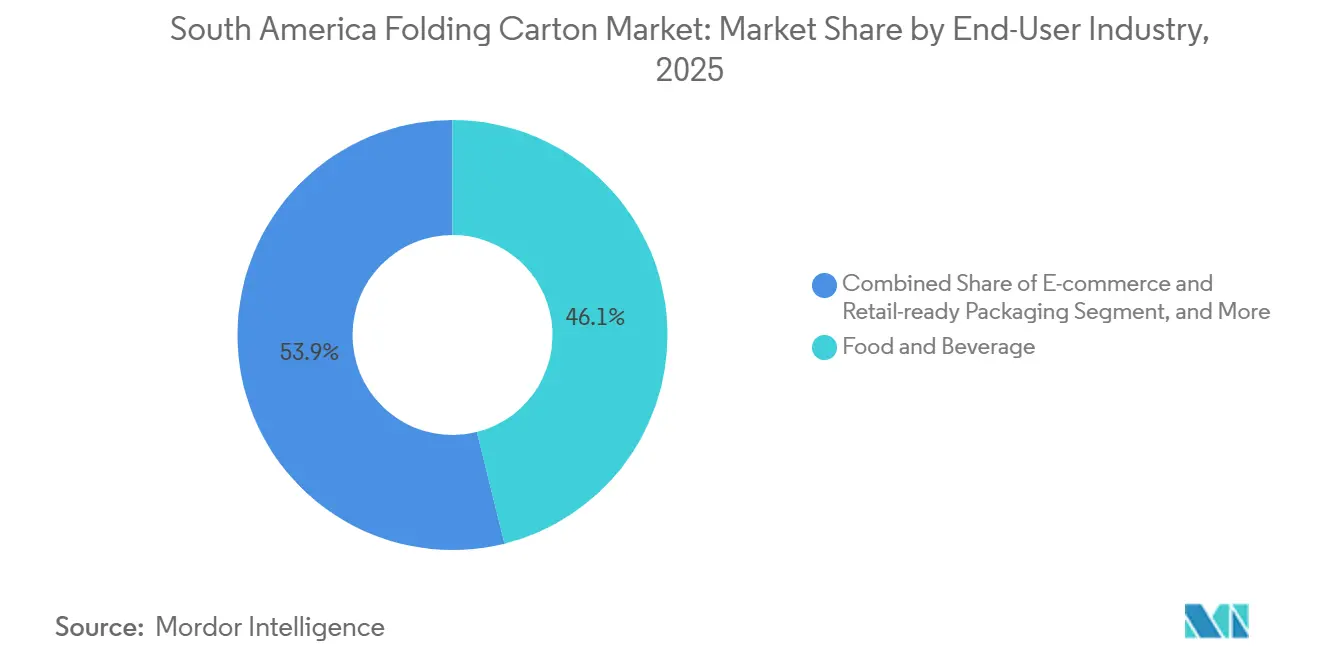

- By end-user industry, food and beverages captured 46.12% of the South America folding cartons market share in 2025.

- By geography, the South America folding cartons market size for Colombia is forecast to advance at an 8.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Growth of Regional E-commerce Fulfillment Networks | +1.8% | Brazil, Colombia, Chile | Medium term (2-4 years) |

| Brand Owner Shift Toward Monomaterial Recyclable Solutions | +1.5% | Brazil and Chile | Medium term (2-4 years) |

| Government-Led Plastics Reduction Mandates in MERCOSUR | +1.2% | Chile, Argentina, Brazil, Uruguay | Long term (≥ 4 years) |

| Rise in Near-sourcing of Consumer Goods to South America | +1.0% | Brazil, Colombia, Argentina | Medium term (2-4 years) |

| Advances in Water-based Barrier Coatings for Food Contact | +0.9% | Brazil, Chile, Argentina | Long term (≥ 4 years) |

| Private-Label Expansion in Modern Retail Channels | +0.7% | Brazil, Argentina, Chile | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Growth of Regional E-commerce Fulfillment Networks

Urban fulfillment hubs in São Paulo, Bogotá, and Santiago are prompting brand owners to specify lighter, retail-ready cartons that minimize dimensional-weight charges and support next-day delivery. New sites such as Klabin’s 240,000 tonnes-per-year Piracicaba II facility supply crash-bottom and straight-tuck styles optimized for automated pick-and-pack lines. Subscription commerce and direct-to-consumer launches demand graphics refreshes every few weeks, a requirement now met by digital presses that eliminate plate lead times. The sustained build-out of last-mile networks is expected to add 1.8 percentage points to the overall CAGR as converters lock in multi-year commitments with third-party logistics providers.[1]Smurfit Westrock, “Investor Presentation 2026,” SMURFITKAPPA.COM

Brand Owner Shift Toward Monomaterial Recyclable Solutions

Multinationals, including Unilever, Danone, and Nestlé, are redesigning South American SKUs around fiber-based monomaterials that align with global recyclability pledges. Klabin’s Advance line, produced on Paper Machine 28, blends long pine and short eucalyptus fibers to deliver stiffness and premium print surfaces while remaining fully recyclable in curbside paper streams. Extended-producer-responsibility fees tied to multi-layer laminates further tilt economics toward folding cartons. This driver will lift market expansion by roughly 1.5 percentage points over the medium term as retailers increasingly favor on-shelf claims of 100% recyclable packaging.[2]Klabin S.A., “Investments - Relatório de Sustentabilidade 2024,” KLABIN.COM.BR

Government-Led Plastics Reduction Mandates in MERCOSUR

Chile’s single-use plastics law and Argentina’s valorized-waste resolutions mandate phase-outs of non-recyclable foodservice packs, opening opportunities for barrier-coated cartons that meet moisture and grease standards. Mondi’s FunctionalBarrier range and Suzano’s kraft-paper wraps illustrate technology solutions that replace polyethylene-laminated boards without sacrificing performance. Enforcement is uneven, but compliance deadlines through 2030 are accelerating brand specification changes, adding a 1.2 percentage point uplift to the forecast CAGR.[3]Mondi, “Our Strategy,” MONDIGROUP.COM

Rise in Near-sourcing of Consumer Goods to South America

Supply-chain shocks from 2024-2025 in ocean freight volatility prompted personal-care and household-cleaning brands to relocate production from Asia to Brazil and Colombia. Smurfit Kappa’s USD 40 million investment in sack paper in Palmira and Cali feeds this localized manufacturing base, reducing lead times for folding-carton blanks and enabling agile pack-size changes. Near-sourcing trims working capital tied up in transit and ensures packaging design stays in sync with regional marketing calendars, adding 1.0 percentage points to the market CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Containerboard Supply-Demand Imbalance | -0.9% | Brazil, Argentina, Chile | Short term (≤ 2 years) |

| Currency Volatility Impact on Imported Pulp Prices | -0.7% | Argentina, Brazil, Colombia | Short term (≤ 2 years) |

| Limited Skilled Labor for High-end Litho Printing | -0.4% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Slow Standardization of Recycling Infrastructure | -0.3% | Colombia, Argentina, Rest of South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic Containerboard Supply-Demand Imbalance

Sharp demand spikes in 2025 left Argentine and Chilean converters scrambling for white-top kraftliner, driving spot prices up and elongating lead times. Although Klabin’s new machines are easing tightness, specialty grades still face bottlenecks that erode converter margins and delay product launches. Short-term impacts shave 0.9 percentage points off growth until fresh capacity stabilizes regional inventories.[4]Klabin S.A., “Investimentos - RS 2023,” KLABIN.COM.BR

Currency Volatility Impact on Imported Pulp Prices

The Brazilian real’s 15% slide against the U.S. dollar between mid-2024 and early 2025 inflated costs for mills lacking captive forestry. Integrated players hedge most exposure, but independent converters pass price jumps downstream, risking contract losses to lower-cost rivals. The hit reduces forecast growth by 0.7 percentage points until currencies regain stability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Premium Grades Outpace Commodity Boards

Folding boxboard captured 38.16% of the South America folding cartons market share in 2025, thanks to its versatility across cereals, snacks, and household cleaners. The grade’s light basis weight keeps unit costs low and supports high-speed filling on legacy lines. Yet solid bleached sulfate is projected to grow at an 8.89% CAGR, contributing disproportionately to the South America folding cartons market as pharmaceutical and cosmetic brands specify brighter white surfaces and odor-neutral fibers.

Converters are repositioning portfolios accordingly. Klabin’s Advance Print variant delivers tight color registration needed for over-the-counter drug cartons, while Advance Cup and Advance Tray grades target foodservice and thermoformable uses. Coated unbleached kraft remains the go-to for rugged packs that flaunt a natural aesthetic, and recycled-content chipboard protects margin in price-sensitive SKUs. As brand owners tighten supplier rosters, mills able to tailor fiber blends for regulatory compliance and luxury appeal will capture outsized share gains over the forecast horizon.

By Printing Technology: Digital Presses Move Mainstream

Flexography accounted for 41.33% of revenue in 2025, underpinning long food-beverage runs where durable plates amortize quickly. The South America folding cartons market is now pivoting toward digital workflows; however, as HP Indigo 35K units print variable graphics up to 25-point board with turnaround measured in hours, not days. Digital volumes are forecast to grow at 9.03% CAGR as online launch cadence accelerates.

Heidelberg’s Boardmaster inline flexo line, clocking 600 m/min and cutting changeover waste by up to 90%, shows flexo technology itself is advancing. Still, scarce litho press crews limit output in premium beauty cartons, steering that business to digital or hybrid lines. Gravure retreats with tobacco volumes, and screen embellishments enter niche security work. Converters that master color consistency across analog and digital fleets stand to lock in multi-channel brand programs.

By End-User Industry: Retail-Ready and E-commerce Surge

Food and beverages accounted for 46.12% of 2025 shipments, yet omnichannel retail is reshaping demand. Shelf-ready packs that workers slide straight to gondolas now proliferate in Carrefour Brasil’s 1,000+ stores, and fulfillment centers prefer crash-bottom cartons that survive parcel carriers. These forces underpin a 9.17% CAGR for e-commerce and retail-ready applications.

Healthcare cartons, though smaller in tonnage, yield attractive margins because of serialization, tamper-evidence, and audit requirements. Personal-care and cosmetics brands pay premiums for unblemished solid bleached sulfate paired with soft-touch varnishes. Electronics and household durables lag in growth, but converters that integrate folding cartons with molded-fiber inserts still reward. Tobacco’s decline lingers, though regulatory warning rotations keep print runs rolling.

Geography Analysis

Brazil, controlling 54.18% of 2025 revenue, benefits from integrated forestry, pulp, and converting complexes. Paper Machines 27 and 28 at Ortigueira, plus the Piracicaba II corrugated hub, invested more than USD 974 million in new capacity, reinforcing domestic self-sufficiency in premium boards. State-by-state plastics-reduction laws complicate compliance, yet robust retail networks in São Paulo and Rio de Janeiro anchor demand, and collection systems, though uneven, surpass regional peers.

Colombia is on track for an 8.19% CAGR through 2031, spurred by near-sourced consumer-goods plants and USD 40 million of Smurfit Kappa sack-paper spend targeting Cali and Palmira. Improving highway corridors to Buenaventura and Cartagena ports shortens inland transit, encouraging multinationals to base Andean-market pack lines locally. Pending producer-responsibility statutes may ignite fresh recycling investments, advancing circularity goals and attracting converters with digital prowess.

Argentina and Chile, while smaller, are strategically important. Currency swings in Buenos Aires deter greenfield builds, locking the market into Brazilian imports, whereas Chile’s single-use plastics ban is funneling bakery and fresh-produce brands toward barrier-coated cartons. Beyond the big four, Smurfit Westrock’s purchase of Cartomanabí brings Ecuador into sharper focus, providing a beachhead for Pacific Rim exports and signaling that the South America folding cartons market will extend east-Andes growth corridors in the coming decade.

Competitive Landscape

Global majors such as Smurfit Westrock and International Paper vie with Brazilian heavyweights Klabin and Suzano in a moderately fragmented arena. Klabin manages 367,000 hectares of FSC-certified forests and 23 mills, giving it a fiber cost hedge unmatched by independents. Paper Machine 28’s 460,000-tonnes slate of white board, plus the Caetê forest acquisition that cut the average haul radius, exemplify its vertical-integration playbook.

Smurfit Westrock’s 2026 pick-up of Ecuador’s Cartomanabí injects 50,000 tonnes of folding-carton headroom and broadens reach beyond Brazilian and Argentine cores. Strategy centers on bolt-on buys in undersupplied geographies, paired with debottlenecking of Baltic-coastboard links feeding South American mills. International Paper still runs Rancagua, Chile, but has largely refocused on North America, ceding share in specialty grades to regional players.

Technological arms races are accelerating. Heidelberg Boardmaster installs and HP Indigo fleets are standardizing across top converters, tightening color tolerance and slashing changeovers. BOBST flexo post-print rigs help corrugated houses chase premium graphics, blurring substrate lines. White-space entrants with water-based coating chemistries and rapid prototyping labs are courting cosmetics startups and plant-based meat brands, niches where sustainability messaging commands margin. The South America folding cartons market therefore rewards scale in fiber plus nimbleness in downstream converting technology, a balance only a handful of players have yet mastered.

South America Folding Carton Industry Leaders

Smurfit Westrock plc

International Paper Company

Graphic Packaging Holding Company

Klabin S.A.

Suzano S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Smurfit Westrock finalized the Cartomanabí acquisition in Ecuador, adding 50,000 tonnes of folding-carton capacity and widening Andean coverage.

- January 2026: Klabin reached full output on Paper Machine 28 at Ortigueira, delivering 460,000 tonnes per year of white board and kraftliner for high-graphic pharmaceutical and foodservice uses.

- December 2025: Klabin closed the Caetê Project forest purchase of 150,000 hectares, saving USD 100 million in harvesting and wood procurement.

- September 2025: Graphic Packaging recorded Americas revenue of USD 5.889 billion, underpinned by its Jundiaí, Brazil, carton plant.

South America Folding Carton Market Report Scope

The South America folding cartons market refers to the production and commercialization of paperboard-based packaging solutions that are folded into cartons for the packaging, protection, and display of a wide range of products across industries such as food and beverage, healthcare, personal care, and retail.

The South America Folding Cartons Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, Other Material Types), Printing Technology (Lithographic, Flexographic, Digital, Gravure, Other Printing Technologies), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, Other End-User Industries), and Geography (United States, Mexico, Canada). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Rest of South America |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

What is the current South America folding cartons market size and its growth outlook?

The South America folding cartons market size stood at USD 4.84 billion in 2026 and is projected to reach USD 6.85 billion by 2031, reflecting a 7.19% CAGR over the forecast period.

Which country is the fastest-growing consumer of folding cartons in South America?

Colombia is forecast to expand at an 8.19% CAGR through 2031 on the back of near-sourcing and rising middle-class consumption.

Which material type is gaining the most share in premium packaging applications?

Solid bleached sulfate is projected to grow at an 8.89% CAGR as pharmaceuticals and cosmetics brands value its high whiteness and recyclability.

How is e-commerce influencing folding carton design in the region?

Fulfillment centers favor crash-bottom and retail-ready cartons that lower dimensional weight and streamline shelf replenishment, supporting a 9.17% CAGR in the e-commerce and retail-ready segment.

What technologies are converters adopting to meet short-run SKU needs?

Digital presses such as HP Indigo 35K allow plate-less, variable-data printing, while new inline flexo systems like Heidelberg Boardmaster cut changeover waste by up to 90%.

Which regulations are accelerating the move away from plastic packaging?

Chile's single-use plastics ban and Argentina's valorized-waste rules require recyclable formats, prompting many brands to specify fiber-based folding cartons.

Page last updated on: