Argentina Folding Carton Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

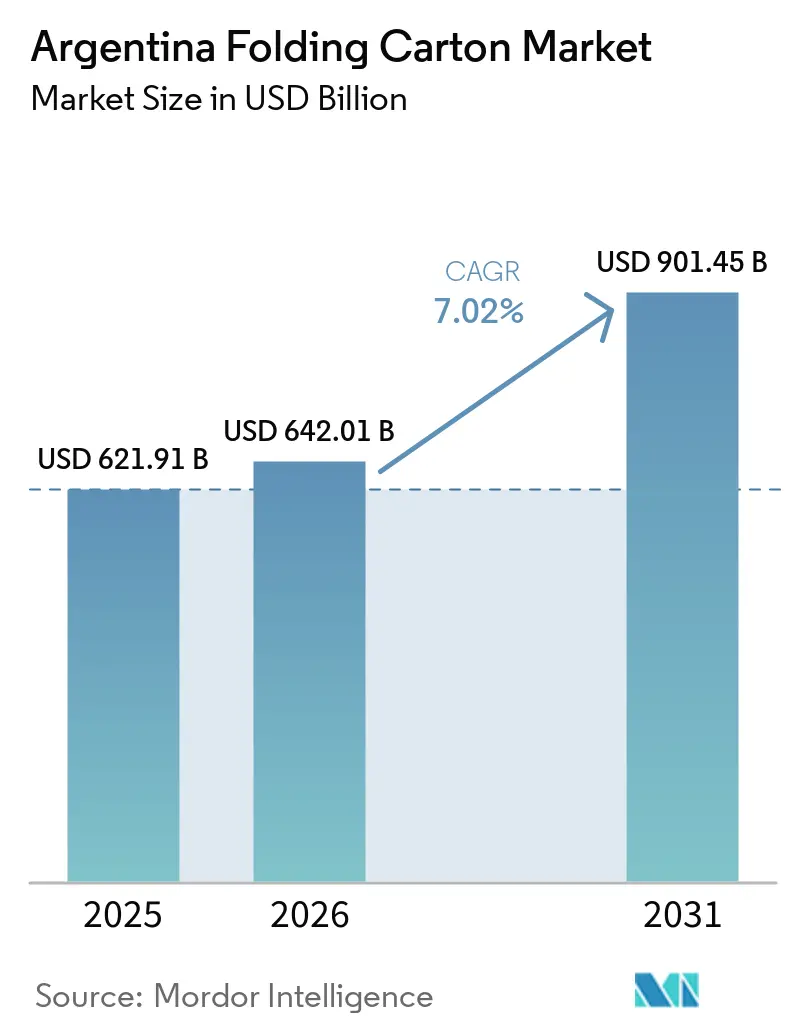

| Base Year Market Size (2025) | USD 621.91 Billion |

| Market Size (2026) | USD 642.01 Billion |

| Market Size (2031) | USD 901.45 Billion |

| Growth Rate (2026 - 2031) | 7.02% CAGR |

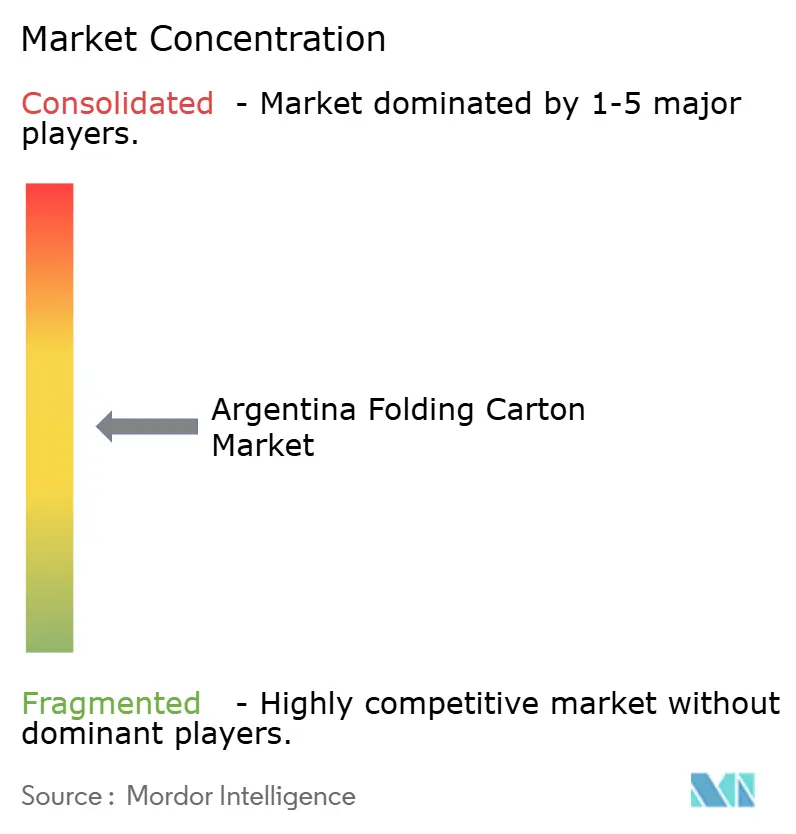

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Folding Carton Market Analysis by Mordor Intelligence

The Argentina folding carton market size is expected to increase from USD 642.01 million in 2026 to USD 901.45 million by 2031, growing at a CAGR of 7.02% over 2026-2031. Accelerating online retail, streamlined food-packaging regulations, and sustained investment in premium substrates are reshaping competitive dynamics. Online penetration reached 18% of total retail in 2025, twice the South American average, and is steering brand owners toward retail-ready cartons that combine rigidity, branding real estate, and protective inserts. Presidential decrees that removed long-standing import barriers now speed access to certified board grades and advanced converting equipment, raising the technological baseline for local converters. Although domestic consumption remains fragile, export-oriented wine, meat, and fruit segments continue to demand high-specification cartons that meet strict destination-country standards.

Key Report Takeaways

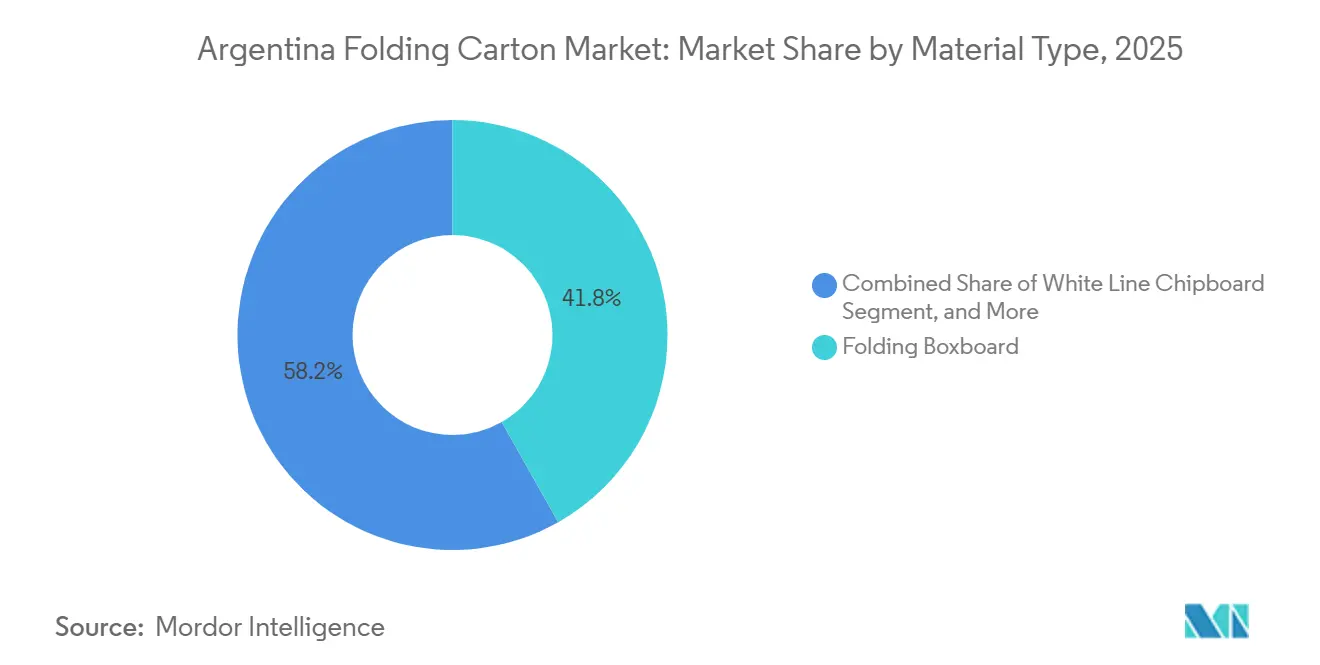

- By material type, folding boxboard captured 41.81% of the Argentina folding cartons market share in 2025.

- By printing technology, the Argentina folding cartons market size for the digital printing segment is forecast to advance at a 9.14% CAGR through 2031.

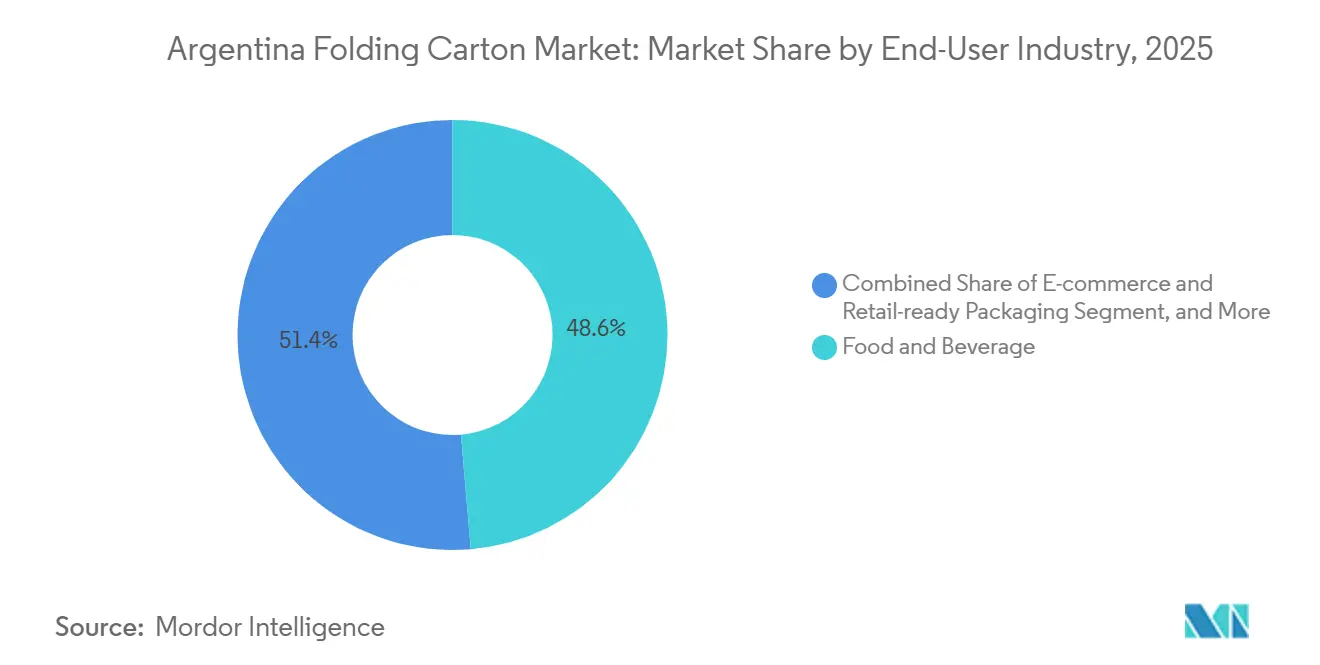

- By end-user industry, food and beverage captured 48.64% of the Argentina folding cartons market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Argentina Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-Commerce Penetration Boosting Demand for Retail-Ready Cartons | +1.8% | National, focused on Buenos Aires, Córdoba, Santa Fe | Short term (≤ 2 years) |

| Growing Preference for Sustainable Packaging Among Argentine Consumers | +1.3% | National, strongest in urban export hubs | Medium term (2-4 years) |

| Expansion of Domestic Processed Food Exports Requiring High-Quality Cartons | +1.1% | Export corridors in Mesopotamia, Mendoza, Buenos Aires | Medium term (2-4 years) |

| Government Incentives for Packaging Recycling Infrastructure | +0.6% | Pilot programs in Buenos Aires, Córdoba, Rosario | Long term (≥ 4 years) |

| Emergence of Micro-Folding Lines Supporting Short-Run Customized Orders | +0.9% | Greater Buenos Aires industrial belt | Short term (≤ 2 years) |

| Increasing Adoption of Water-Based Inks to Meet VOC Regulations | +0.5% | National, compliance-driven | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce Penetration Boosting Demand for Retail-Ready Cartons

Argentina’s e-commerce revenue expanded 60% year-over-year in 2025, elevating online sales to 18% of total retail.[1]Cámara Argentina de Comercio Electrónico, “El comercio electrónico en Argentina creció más de 60% en 2025,” ambito.com.ar Shoppers consolidated items to dilute shipping fees, which heightened demand for multi-item cartons with right-sized cavities that cut dimensional-weight surcharges. Fast-growing categories such as electronics, home décor, and beauty required protective inserts, tamper-evident closures, and high-impact graphics that convey brand personality on crowded digital shelves. Marketplaces Temu and Shein together seized nearly one-fifth of online spend, forcing converters to master variable-data printing for flash promotions and batch traceability. Cartons increasingly outperformed flexible pouches because they stack efficiently, resist crushing, and provide ample surface for personalized unboxing experiences.

Growing Preference for Sustainable Packaging Among Argentine Consumers

L’Oréal research found that 76% of shoppers prefer brands demonstrating positive environmental impact, and 39% actively avoid perceived unsustainable labels.[2]L’Oréal Groupe, “Consumo consciente en alza,” economiasustentable.com Certified virgin and recycled boards carrying FSC or PEFC logos have therefore become hygiene factors for premium and export SKUs. Refillable fragrance and skincare systems trimmed carton tonnage by up to 31%, illustrating that lightweighting can coexist with luxury cues. Kantar’s EcoActive cohort rose to 28% of the population between 2023 and 2024, prompting retailers to demand monomaterial packs and water-based coatings that simplify post-consumer sorting. Cartocor’s dual forestry certificates and 180,000-tonne recycling platform position it to supply brands that link sustainability commitments with purchasing decisions.

Expansion of Domestic Processed Food Exports Requiring High-Quality Cartons

Decree 35/2025 removed redundant domestic certifications, allowing exporters to comply solely with the destination country's labeling and food-contact rules.[3]USDA Foreign Agricultural Service, “Less Paperwork More Trade,” usda.gov Wine, fruit, and premium beef producers now specify Solid Bleached Sulfate cartons whose brightness and grease resistance safeguard shelf appeal across long cold-chain journeys. Smurfit WestRock’s USD 150 million causticizing upgrade at Três Barras secures kraftliner supply for Argentine converters and cushions regional fiber volatility. At the same time, Papel Misionero invested USD 60 million to modernize Misiones operations, reinforcing the supply of export-grade kraft paper. The convergence of lighter regulation and fresh mill capacity is lifting order volumes for converters able to certify FDA, EU, and Japanese compliance on short lead times.

Government Incentives for Packaging Recycling Infrastructure

The 2026 draft Packaging Bill proposes producer-funded municipal collection schemes and allocates 10% of fees to integrate waste pickers, signaling an official pivot toward extended producer responsibility.[4]Ministerio de Ambiente, “Proyecto de Ley de Envases,” packaginglatam.com Decree 1/2025 already authorizes the importation of valorized cardboard and plastic inputs, provided shipments register on the VUCEA single-window portal. Several Buenos Aires converters have piloted neighborhood drop-off programs that guarantee feedstock purity in exchange for loyalty credits redeemable with participating grocers. Early adopters report that brand owners are willing to share surcharges when clear metrics link recycled-content gains to greenhouse-gas reductions. Although nationwide roll-out remains years away, visible policy momentum reduces investment risk for balers, sorters, and reclaimed-fiber pulping lines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin Pulp Prices | -1.2% | National, integrated and importing mills | Short term (≤ 2 years) |

| Limited Availability of High-Grade Recovered Fiber Domestically | -0.9% | Interior provinces, high transport costs | Medium term (2-4 years) |

| Capital-Intensive Nature of Offset Press Upgrades for SMEs | -0.6% | Greater Buenos Aires, Córdoba, Rosario | Long term (≥ 4 years) |

| Competition from Flexible Plastic Pouches in Beverage Segment | -0.5% | Ready-to-drink dairy and juice | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Pulp Prices

Hardwood-pulp import volumes rose 17% in H1 2025 after Celulosa Argentina filed for insolvency, exposing converters to dollar-denominated spot markets. Peso depreciation, coupled with energy-tariff hikes, sent kraftliner quotes gyrating quarter to quarter, undermining budget forecasts. Some converters negotiated index-linked contracts, while smaller firms without hedging tools absorbed margin erosion when input prices spiked, and domestic demand was sluggish. Although a USD 20 billion currency-swap arrangement briefly steadied exchange rates, analysts doubt that fiscal tightening can fully tame cost-push inflation in the near term. Persistent volatility, therefore, discourages capital upgrades and may slow adoption of premium SBS grades among cash-constrained printers.

Limited Availability of High-Grade Recovered Fiber Domestically

Cardboard prices plunged 55% between January 2024 and January 2025, pushing many waste-picker cooperatives below breakeven and cutting the recycling workforce from 18,000 to 10,000 people. De-regulated scrap exports now lure high-quality old corrugated containers to higher-priced overseas buyers, depriving local mills of clean furnish. Interior provinces face prohibitive freight costs: hauling 25 tonnes of baled board from Formosa to Buenos Aires costs ARS 2 million (USD 0.001 million) but yields only ARS 3.03 million (USD 0.002 million) in sales, leaving a scant margin after VAT. Consequently, converters must import secondary fiber from Brazil or Uruguay, inflating logistics footprints and complicating life-cycle assessments. Unless municipal collection funding stabilizes, recovered-fiber scarcity will continue to elevate the cost base for entry-level chipboard cartons.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Premium Grades Capture Growth Momentum

Folding Boxboard maintained 41.81% of the Argentine folding carton market share during 2025, supplying everyday food, beverage, and household applications that demand moderate barrier performance and dependable printability. Solid Bleached Sulfate is projected to deliver the fastest 8.09% CAGR over 2026-2031, driven by cosmetics, pharmaceuticals, and export-grade foods increasingly requiring its brightness, purity, and FDA and ANMAT certifications. Coated Unbleached Kraft appeals to organic brands that seek natural aesthetics combined with strong bulk for heavier retail units, while White Line Chipboard remains cost-competitive for detergents, toys, and industrial goods. Mandatory front-of-pack warning seals introduced in December 2024 favor substrates offering consistent ink holdout and dimensional stability across high-speed presses. Consequently, premium Solid Bleached Sulfate grades are gaining visibility across supermarket aisles and duty-free shelves alike.

The Argentine folding carton market for Solid Bleached Sulfate applications is expanding alongside wine and confectionery gift packs that require embossing, foiling, and fine color gradients. Cartocor leverages FSC-certified forestry assets and 180,000 tonnes of recycled input per year to guarantee responsible sourcing for these premium constructions. Import liberalization under Decree 35/2025 eases access to specialty coatings and laminates, enabling domestic converters to replicate multinational packaging specifications without lengthy compliance delays. Competitive pressure from Asian suppliers keeps commodity board prices subdued, yet premium grades avoid aggressive discounting because their technical attributes closely align with stringent export protocols. Over the forecast horizon, brand owners will continue trading up to high-brightness substrates that enhance shelf impact and protect temperature-sensitive fillings on extended logistics chains.

By Printing Technology: Digital Adoption Accelerates

Lithographic Printing captured 54.36% of revenue in 2025, anchored by its low variable costs on runs exceeding 5,000 impressions and its ability to deliver precise color fidelity required by global consumer-goods groups. However, Digital Printing is expected to grow at a robust 9.14% CAGR, chiefly because e-commerce sellers demand late-stage customization, serialized QR codes, and region-specific promotions that change weekly. HP Indigo and comparable electrophotographic presses enable job changeovers measured in minutes, slicing non-productive downtime and eliminating expensive plates. Flexographic presses continue to serve bulk cereal and detergent cartons where two-color graphics suffice, whereas gravure persists in luxury spirits and tobacco lines that value ultrafine vignette shading. Other specialty methods, including screen and pad, fill tactile-varnish niches but contribute marginal volumes to overall output.

The Argentine folding carton market for Digital Printing is growing because converters have installed micro-folding lines integrating inline UV coating, laser scoring, and die-cutting that accommodate batches as small as 50 cartons. Such agility lets beauty brands launch influencer-collaboration editions or holiday variants without wasting residual inventory once campaigns expire. Water-based ink portfolios now meet VOC ceilings and food-contact migration limits, further strengthening the digital business case for nutraceutical and children’s snack manufacturers. Hybrid workflows that lay down litho base layers while adding digital personalization allow converters to stretch capital budgets, an advantage for mid-sized firms facing tight credit markets. As variable-data printing becomes mainstream, data-rich packaging will anchor brand storytelling while supporting regulatory traceability throughout omnichannel supply chains.

By End-User Industry: E-Commerce Cartons Lead Growth

Food and Beverage generated 48.64% of total demand in 2025, relying on grease-resistant Folding Boxboard and reinforced corner structures that withstand cold-chain condensation without panel bowing. Nonetheless, E-commerce and Retail-ready Packaging is forecast to post an 8.85% CAGR to 2031, driven by Argentina’s 60% surge in online revenue and the expectation that digital share will keep outpacing brick-and-mortar formats. Fulfillment centers prefer cartons with stacking stability, perforated tear strips, and printable interiors that enhance unboxing theatrics during social media reveals. Healthcare and Personal Care segments are also upgrading to Solid Bleached Sulfate, accompanied by covert security inks that deter parallel trade, thereby nudging average price points higher. Meanwhile, Tobacco volumes have plateaued, and beverage pouches threaten share in selected ready-to-drink niches, although carton multipacks still dominate promotional displays across hypermarkets.

The Argentina folding carton market share for online retail parcels will expand as last-mile carriers demand right-sized pack formats that minimize volumetric shipping tariffs. Cartocor’s patented PUSHandLOCK closure eliminates hot-melt adhesives, reducing line stoppages and supporting 100% machine assembly, a crucial requirement for e-grocery operations that dispatch thousands of chilled hampers daily. Electronics sellers equipping cartons with integrated cable organizers and anti-static liners demonstrate how secondary packaging now doubles as product experience rather than simple containment. High-graphics shelf-ready trays that travel from pallet to shelf without extra corrugate layers meet retailer labor-cost mandates and sustainability scorecards simultaneously. Together, these functional and aesthetic shifts confirm that e-commerce remains the most disruptive driver influencing carton performance specifications and production economics through 2031.

Geography Analysis

Greater Buenos Aires accounts for the majority of Argentina's folding carton production because deep-water ports, dense consumer clusters, and skilled labor pools create unrivaled scale efficiencies. Plants in Quilmes, Luján, and Bernal enjoy overnight trucking access to multinational food processors and pharmaceutical fillers headquartered within the metropolitan area. Smurfit WestRock, Cartocor, and Zucamor operate integrated board mills and converting lines here, enabling rapid material changeovers synchronized with just-in-time customer schedules. Government incentives for industrial digitalization, including accelerated depreciation on high-efficiency presses, further anchor new investment within the region. Consequently, Buenos Aires will likely preserve its dominance even as provincial plants pursue regional expansion strategies.

Córdoba and Santa Fe form a secondary hub that balances proximity to agro-industrial complexes with adequate rail links to Rosario and to export terminals in Buenos Aires. Corrugated and folding-carton plants in Río Segundo, Villa María, and San Lorenzo supply beef processors, peanut roasters, and automotive part makers that appreciate shorter lead times versus importing cartons from coastal factories. Provincial governments have rolled out energy tariff rebates tied to on-site biomass boilers, allowing mills to lower steam costs and improve greenhouse gas performance metrics. These benefits are attracting mid-tier converters exploring capacity additions focused on hybrid litho-digital lines for short-run production for regional brands. Over the forecast horizon, Córdoba’s central geography will remain a strategic hedge against supply disruptions concentrated in the capital.

Mesopotamia provinces Misiones, Corrientes, and Entre Ríos anchor Argentina’s virgin-fiber supply thanks to vast pine and eucalyptus plantations managed by Papel Misionero and other forestry groups. The upcoming USD 2 billion fluff-pulp facility in Corrientes promises 800,000 tonnes of annual output, which, although targeted at hygiene grades, may free existing kraft capacity for cartonboard applications post-2030. However, inland logistics costs remain steep; for example, one-way truck rates from Misiones to Buenos Aires typically exceed USD 0.13 per kilogram, eroding the margin advantage of local fiber. Regional authorities are therefore lobbying for a river-barge modernization program on the Paraná to cut freight times and carbon footprints. Successful infrastructure upgrades would tighten the supply loop between plantation forests and downstream converters, thereby rebalancing geographic dependency on coastal corridors.

Competitive Landscape

The Argentine folding carton market features a moderately fragmented structure, with the five largest companies collectively accounting for close to 45% of national output. Smurfit WestRock commands several high-throughput sites and leverages global procurement to secure favorable pulp and ink contracts that smaller rivals cannot match. Cartocor’s integration of forestry, recovered fiber, and patented converting technology affords cost and innovation advantages, particularly in sustainability-driven tenders. Klabin’s cross-border corrugated acquisitions have expanded its regional share and enabled product bundling that appeals to beverage multinationals requiring consistent quality across Mercosur countries. Below these leaders, family-owned converters occupy regional niches, supplying artisanal food, boutique wine, or promotional point-of-sale displays with bespoke service levels.

Strategic priorities currently revolve around vertical integration, circular-economy credentials, and automation that mitigates Argentina’s volatile labor costs. Smurfit WestRock’s BRL 840 million (USD 150.1 million) causticizing expansion in Brazil improves self-sufficiency in kraftliner and reduces exposure to currency swings that periodically inflate import bills. Cartocor’s PUSHandLOCK technology streamlines case erection and eliminates thermoplastic adhesives, aligning with regulatory pressure to curtail volatile organic compounds while trimming factory energy loads. Many mid-sized converters pool resources through purchasing cooperatives to access imported SBS and specialty coatings at tier-one prices, narrowing the raw-material gap with the majors. Digital workflow adoption further democratizes capability, enabling smaller presses to achieve high-quality graphics without eight-color offset units that exceed their financing capacity.

Celulosa Argentina’s 2025 insolvency underscored exposure to exchange-rate shocks and under-investment in energy efficiency; its subsequent USD 18 million rescue plan aims to restore plant capacity by early 2026 and retain domestic pulp supply. Asian board exporters, taking advantage of tariff realignments, have introduced competitively priced coated grades that pressure commodity margins but simultaneously raise quality thresholds in local showrooms. Meanwhile, Klabin and Mondi explore partnership models in Argentina that bundle corrugated trays, folding cartons, and flexible liners under single contracts, appealing to omnichannel retailers seeking vendor consolidation. Competitive dynamics, therefore, hinge on agility rather than sheer scale, rewarding converters capable of quick design iterations, traceable sourcing, and cost-effective logistics across dispersed consumer and export markets.

Argentina Folding Carton Industry Leaders

Smurfit Westrock plc

International Paper Company

Mondi plc

Graphic Packaging Holding Company

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ARPULP announced a USD 2 billion investment for a fluff-pulp mill in Corrientes scheduled to start operations in 2030 and projected to create 13,000 direct and indirect jobs.

- April 2026: Ecopek, owned by Alpek Polyester, shuttered its PET recycling plant in General Pacheco after twelve years because weak domestic demand undermined economic viability.

- May 2025: Smurfit WestRock approved a BRL 840 million (USD 168 million) capacity upgrade at its Três Barras mill that will lift kraftliner output by up to 10% before end-2027.

- February 2025: Resolution 23/2025 detailed procedures for importing valorized industrial inputs via the VUCEA single-window platform, increasing traceability requirements for secondary fibers.

Argentina Folding Carton Market Report Scope

The Argentina folding carton market refers to the production and commercialization of paperboard-based packaging solutions that are folded into cartons for the packaging, protection, and display of a wide range of products across industries such as food and beverage, healthcare, personal care, and retail.

The Argentina Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, Other Material Types), Printing Technology (Lithographic, Flexographic, Digital, Gravure, Other Printing Technologies), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-Commerce and Retail-Ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-Commerce and Retail-Ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the Argentina folding carton market and its 2031 outlook?

The market stands at USD 642.01 million in 2026 and is projected to reach USD 901.45 million by 2031.

Which end-user segment will grow fastest through 2031?

E-commerce and retail-ready packaging is expected to grow at an 8.85% CAGR because online retail penetration continues climbing.

Why are premium Solid Bleached Sulfate grades gaining share in Argentina?

Pharmaceutical and cosmetics brands prefer its brightness, purity, and export-compliant certifications, driving an anticipated 8.09% CAGR for the material.

How are converters addressing sustainability demands from Argentine consumers?

They adopt FSC-certified board, install water-based ink systems, and collaborate with municipal pilots to secure high-quality recovered fiber.

What risks does pulp-price volatility pose to carton producers?

Fluctuating import costs compress margins for mills lacking hedging contracts, delaying equipment upgrades among small and medium converters.

Which companies currently lead the Argentina folding carton competitive landscape?

Smurfit WestRock, Cartocor, and Klabin anchor the market, together supplying roughly 45% of national folding-carton volumes.

Page last updated on: