Nigeria Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

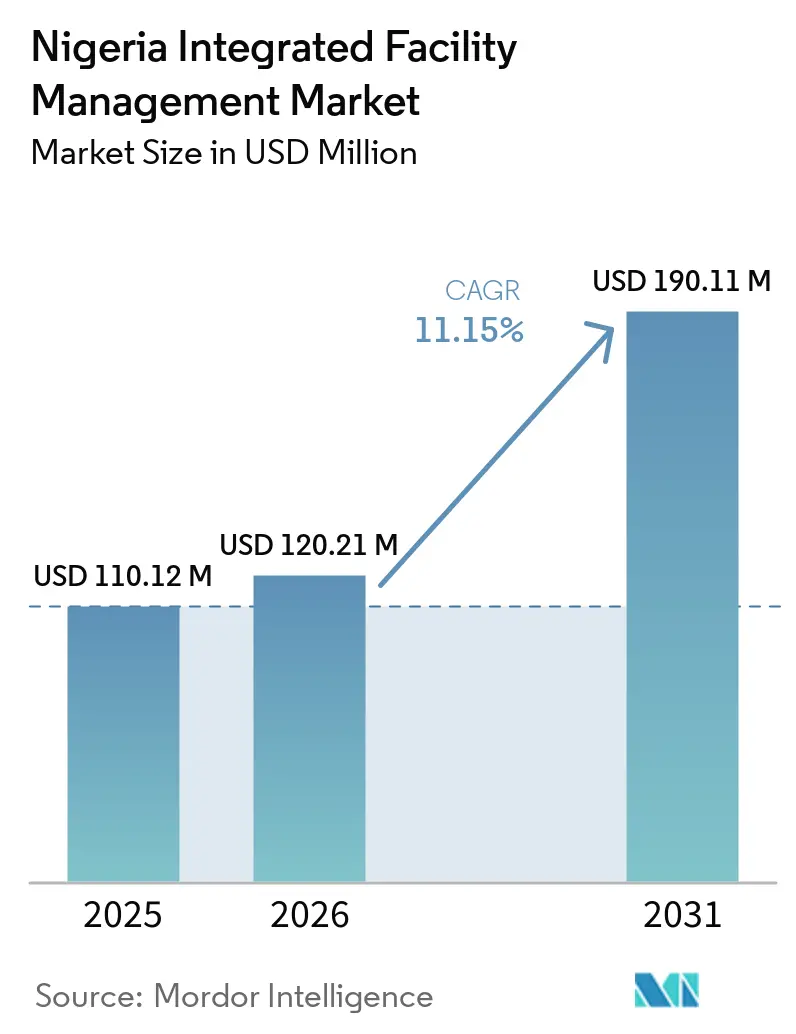

| Base Year Market Size (2025) | USD 110.12 Million |

| Market Size (2026) | USD 120.21 Million |

| Market Size (2031) | USD 190.11 Million |

| Growth Rate (2026 - 2031) | 11.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Integrated Facility Management Market Analysis by Mordor Intelligence

The Nigeria integrated facility management market size is projected to expand from USD 110.12 million in 2025 and USD 120.21 million in 2026 to USD 190.11 million by 2031, registering a CAGR of 11.15% between 2026 to 2031. Nigeria’s 2025 GDP rebasing showed that real estate services contributed 13.4% of real GDP in Q3 2025, which points to a larger and more operationally demanding built environment for the Nigeria integrated facility management (IFM) market. Commercial property transactions reached USD 336 million in 2024, and that stronger investment cycle is pulling more buildings into formal operating models that depend on professional FM contracts rather than informal maintenance support. That ownership shift matters because more corporations now carry direct responsibility for uptime, safety, asset life, and tenant experience, which moves FM from routine procurement into a strategic operating function in the Nigeria IFM market. At the same time, logistics facilities, Grade-A offices, and data centers are raising the technical standard for maintenance, while board-level attention to sustainability and workplace performance is improving the case for integrated contracts. Predictive maintenance tools and IoT-based monitoring are widening the gap between organized providers and informal operators, which supports consolidation opportunities across the Nigeria integrated facility management market over the forecast period.

Key Report Takeaways

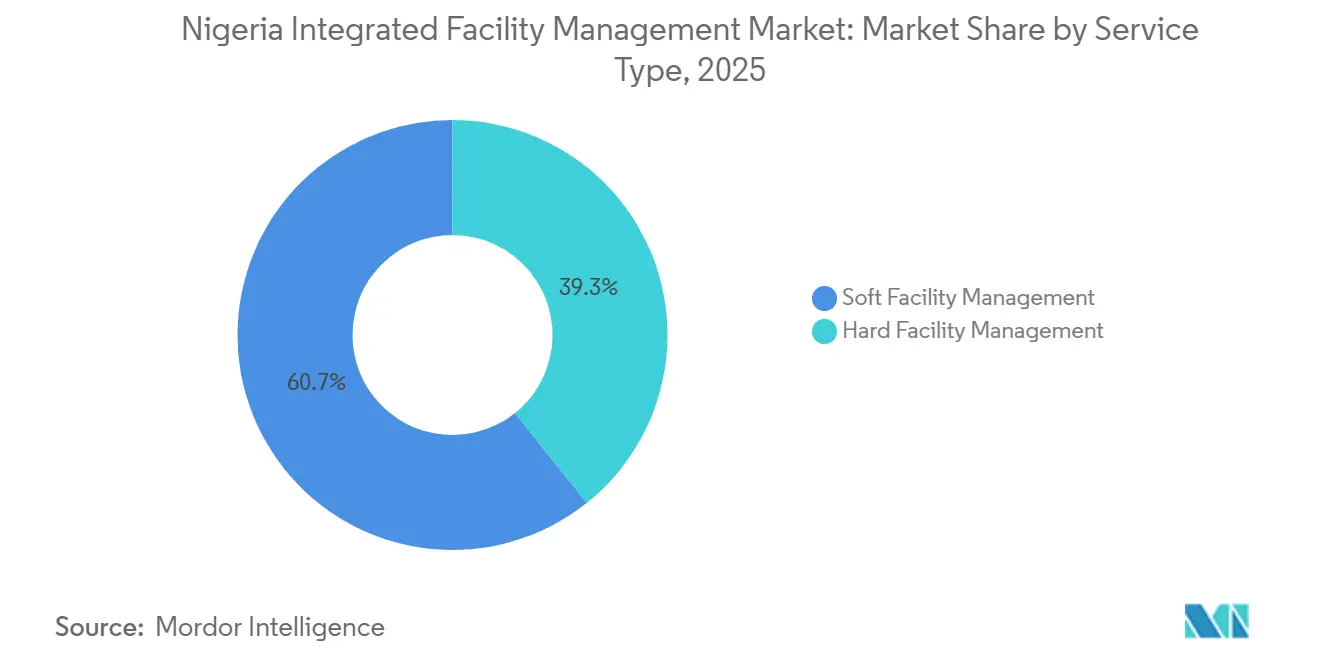

- By service type, soft facility management segment held 60.73% share of revenue in 2025, while hard facility management segment in the Nigeria integrated facility management market is projected to expand at a 11.83% CAGR through 2031.

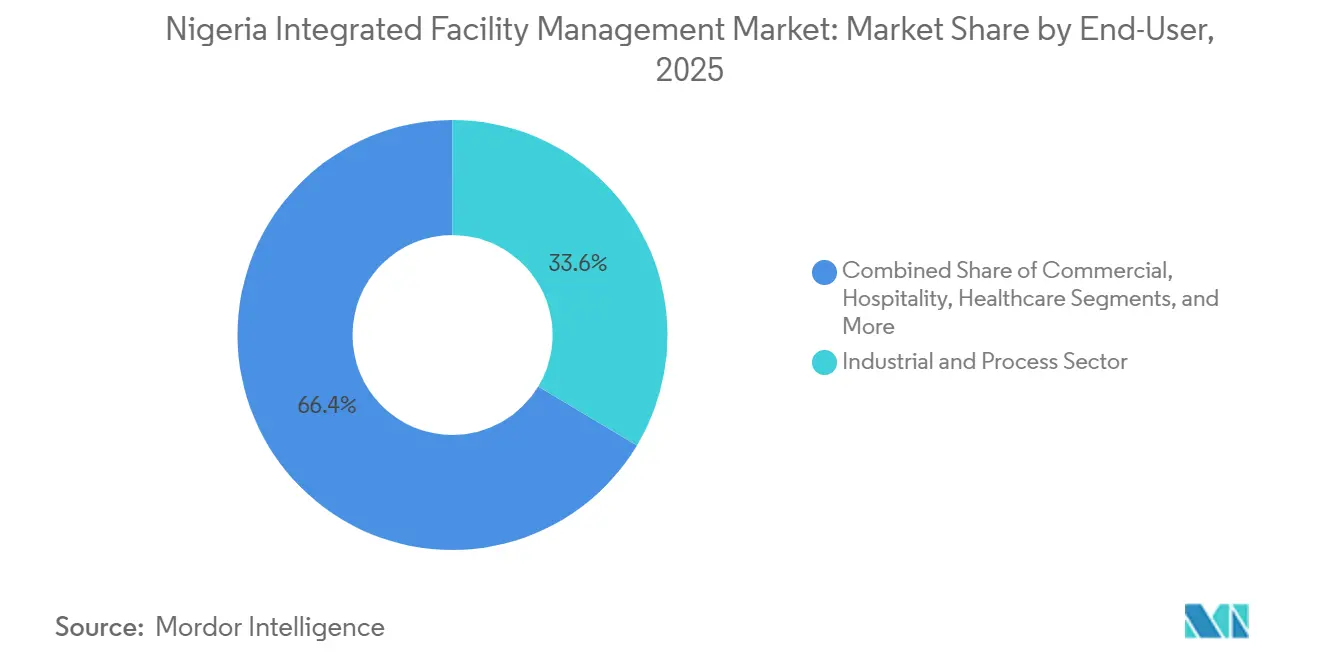

- By end user, the industrial and process segment held 33.59% share in 2025, while the commercial segment in the Nigeria integrated facility management (IFM) market is projected to grow at a 11.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nigeria Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Private Investments In Commercial Real Estate | +2.8% | Lagos, Abuja, with spill-over to Port Harcourt | Short term (≤ 2 years) |

| Rapid Expansion Of Retail And Warehouse Space In Lagos Corridor | +2.3% | Lagos, including Lekki, Alaro, and Ikeja axes | Short term (≤ 2 years) |

| Mandatory Compliance With National Fire Safety Code 2022 | +1.9% | National, with enforcement concentrated in Lagos and Abuja | Medium term (2-4 years) |

| Proliferation Of Smart-Building Retrofits In Grade-A Offices | +1.6% | Lagos, including Victoria Island, Ikoyi, and Lekki, and Abuja central business district | Medium term (2-4 years) |

| Rising Demand For Energy-Efficient HVAC Retro-Commissioning | +1.2% | Lagos industrial and commercial zones, Abuja federal assets | Medium term (2-4 years) |

| Increasing Outsourcing By Oil And Gas Majors For Core-Focus Realignment | +1.0% | Niger Delta, including Port Harcourt, Warri, and Bonny Island | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Private Investments in Commercial Real Estate

Private investment is expanding the addressable asset base for the Nigeria integrated facility management market because owned commercial properties require continuous operating support after acquisition. Knight Frank stated that corporations were buying Grade-A offices at the lowest entry point of the current real estate cycle during 2024 and 2025, which improves the case for long-duration FM planning after the transaction closes. Commercial property transactions reached USD 336 million in 2024, which shows that more office and mixed-use assets are moving into the hands of owners that must manage energy systems, safety compliance, and service quality directly. Real estate services also contributed 13.4% of real GDP in Q3 2025, which indicates enough depth in the built environment to support formal FM supply chains rather than loose contractor networks. As ownership increases, the Nigeria integrated facility management (IFM) market gains a steadier base of recurring contracts tied to building life cycle performance rather than short-term tenant demand.

Rapid Expansion Of Retail and Warehouse Space in Lagos Corridor

New warehouse and logistics assets are creating a more technically demanding workload for the Nigeria integrated facility management market, especially along the Lagos corridor. Jumia Nigeria launched a 30,000 sq.m. warehouse in Isolo in June 2024, adding a large modern facility that depends on reliable power, HVAC control, security, and maintenance coordination.[1]Jumia Group, “Jumia Nigeria Launches 30,000 Sq.mt. Warehouse to Boost Efficiency,” Jumia Group, group.jumia.com TY Logistics Park FZE then inaugurated a 29,000 sq.m. EDGE-certified Grade-A logistics facility in Alaro City in December 2025, which raised the benchmark for warehouse operating standards in the country. Knight Frank expects logistics and e-commerce operators to keep driving warehouse demand along the Lekki corridor and the Ikeja axis, which means more assets will need formal engineering support from commissioning onward. This shift is important because the Nigeria integrated facility management market has historically leaned toward soft services, while logistics parks require stronger hard FM skills from day 1.

Mandatory Compliance with National Fire Safety Code 2022

Fire compliance is turning into a recurring revenue source for the Nigeria integrated facility management (IFM) market because regulated buildings need annual verification rather than one-time installation work. The Federal Fire Service requires commercial, institutional, and industrial buildings to obtain a Fire Safety Compliance Certificate each year, and inspection fees were cited at NGN 100,000 to NGN 150,000 (approximately USD 73 to USD 110) at the federal level. Nigeria recorded more than 1,200 fire outbreaks with property losses estimated at NGN 18 billion (USD 13.15 million) in 2023, and that background has strengthened the case for tighter enforcement in later years. Because the certificate remains valid for only 12 months, building owners need regular testing, servicing, recertification, and documentation that informal maintenance teams often cannot deliver. That gives certified providers in the Nigeria IFM market a stronger position in hard FM contracts linked to safety and compliance.

Proliferation Of Smart-Building Retrofits in Grade-A Offices

Smart retrofits are upgrading the service mix in the Nigeria integrated facility management market because digitally managed buildings need continuous calibration, analytics, and system optimization after installation. A 2025 peer-reviewed study found that smart HVAC, lighting automation, and energy management systems in Nigerian commercial facilities improved energy efficiency, reduced operating costs, and supported return on investment.[2]Peter Oluwole Akadiri, “Assessing the Impact of Smart Building Technologies on Energy Efficiency in Nigeria, Case Study Insights from Real-World Applications,” Civil and Environmental Research, iiste.org InfraCredit Nigeria’s Lagos head office achieved EDGE Advanced certification in 2024 with 58% energy savings, 44% water savings, and a 53% reduction in embodied energy, which shows the performance targets owners now expect from modern facilities.[3]Sintali, “Case Study, InfraCredit Head Office, Nigeria,” Sintali, sintali.com Alpha Mead stated in 2024 that it uses predictive maintenance tools with IoT sensors and machine learning to track equipment performance and intervene before failures escalate. As more offices are upgraded to lower occupation costs and improve reporting standards, the Nigeria integrated facility management (IFM) market is moving further toward data-enabled service delivery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage Of Certified Facility Management Professionals | -1.4% | National, most acute outside Lagos and Abuja | Long term (≥ 4 years) |

| Naira Volatility Increasing Contract-Cost Risk | -1.2% | National, with amplified impact where imported equipment or expatriate talent is required | Medium term (2-4 years) |

| Fragmented Regulatory Oversight Across States | -0.8% | National, across 36 states with inconsistent enforcement | Long term (≥ 4 years) |

| Low Adoption Of Computer-Aided FM Platforms Outside Tier-1 Cities | -0.6% | Secondary cities, including Kano, Ibadan, Benin, and Enugu | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage Of Certified Facility Management Professionals

The skills shortage is a direct constraint on the Nigeria integrated facility management market because supply cannot scale at the same speed as the formal asset base. AFMPN estimated in October 2024 that nearly 500,000 untrained building managers were active in the country, many working under administrative or maintenance titles without formal FM credentials. Industry commentary published in January 2025 also linked growth constraints to skill gaps, funding pressure, and uneven enforcement, which means the problem is not limited to training alone. This shortage raises labor costs for qualified providers and slows rollout outside the main urban centers where certified staff are harder to deploy. The result is that the Nigeria IFM market can win new contracts faster than it can build a consistent national delivery bench.

Naira Volatility Increasing Contract-Cost Risk

Currency volatility is limiting margin visibility in the Nigeria integrated facility management market because many contracts are priced in naira while major inputs are linked to foreign exchange. Industry commentary in 2025 noted that energy can exceed 60% of total FM expense in some commercial developments, and fuel inflation had pushed operating budgets up by as much as 40% in certain cases. A legal analysis published in April 2025 warned that fixed-price FM contracts without escalation clauses become difficult to sustain when the naira weakens and imported components rise sharply in local currency terms. Reporting in 2024 also showed how quickly exchange-rate pressure could damage balance sheets for firms carrying foreign currency exposure. This makes the Nigeria integrated facility management (IFM) market more favorable for providers that can negotiate indexed contracts or access financing support during volatile periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft FM Dominates, Hard FM Defines The Growth Curve

Soft Facility Management (Soft FM) held 60.73% of the market in 2025, giving it the largest share of the Nigeria integrated facility management (IFM) market share for that year. The segment remained dominant because a large portion of the formal building stock still sits in offices, hospitality sites, and mixed-use properties that prioritize visible day-to-day services. Office support and security carry the largest budgets within soft FM because tenant retention in Grade-A buildings depends heavily on perceived safety, front-desk quality, and service reliability. Cleaning and catering also remain important, especially on larger corporate campuses where service consistency affects employee experience and space utilization. IFMA Nigeria’s December 2025 partnership with Venco Africa shows that digital tools are beginning to automate access control, service charge collection, and operational workflows within this part of the Nigeria integrated facility management industry.

Hard Facility Management Market (Hard FM) is projected to grow at 11.83% CAGR through 2031, making it the faster-expanding service category in the Nigeria integrated facility management market. That faster pace reflects stronger demand from data centers, logistics parks, industrial plants, and smart-retrofitted offices that need skilled support for MEP systems, HVAC, and life-safety infrastructure. The launch of a 29,000 sq.m. Grade-A logistics facility in Alaro City in December 2025 illustrates the kind of asset that requires professional engineering oversight from commissioning through steady-state operations. Fire systems and safety should remain one of the more defensible hard FM niches because annual compliance checks create recurring work that owners cannot defer without regulatory risk. Lagos’s Industrial PMI improved from 49.1 in August 2025 to 57% in December 2025, which points to a larger installed base of mechanical systems that will need ongoing maintenance in the Nigeria integrated facility management industry.

By End User: Industrial Anchors Revenues, Commercial Leads Growth

The industrial and process sector held 33.59% of the market in 2025, which gave it the largest share of the Nigeria integrated facility management market size among end users. This lead came from oil and gas sites, manufacturing facilities, and mining assets that operate continuously and place a high value on uptime, preventive maintenance, and safe handling of critical systems. Energy-sector facilities also need technical FM depth because equipment failure can lead to downtime costs that are much larger than the annual FM contract value. SPIE Global Services Energy was selected to provide operations and maintenance services for the ERHA offshore project in Nigeria, and it also unveiled a 15kWp Off-Grid Hybrid Solar Diesel Energy Plant at Port Harcourt Refining Company in February 2025. As international oil companies continue transferring selected onshore assets to indigenous operators, outsourcing support is becoming a standard operating requirement for the Nigeria integrated facility management (IFM) market rather than an occasional add-on.

Commercial end users are forecast to grow at 11.73% CAGR through 2031, making them the fastest-expanding customer group in the Nigeria integrated facility management market. Telecoms, BFSI, retail, and warehousing clients are increasing their use of bundled contracts because they operate multi-site estates that need both soft FM and hard FM under a single service framework. Alpha Mead’s portfolio information shows that its MTN Nigeria contract covers more than 50 locations, including head offices, regional offices, call centers, and data centers, which reflects the scale that organized commercial clients now demand. Healthcare is also opening up as a formal opportunity as public operators look to move non-clinical responsibilities away from care staff and into specialist support arrangements. Institutional and public infrastructure demand should remain relevant as federal and state assets expand, although payment cycles and budget variability will continue to shape provider appetite within the Nigeria IFM market.

Geography Analysis

Lagos remained the dominant demand zone in the Nigeria integrated facility management market because it concentrated the largest share of corporate offices, logistics assets, and high-value mixed-use real estate. The city’s Industrial PMI rose to 57% in December 2025, and the Lekki-Alaro corridor continued to emerge alongside Victoria Island and Ikoyi as a strong source of new commercial and industrial activity. The Lagos Free Zone and Alaro City also pulled in technically complex assets, while the local data center market was valued at USD 1.4 billion in H2 2025, which supports stronger hard FM demand than the national average. Major infrastructure projects, including the Lagos-Calabar Coastal Highway, the Green Line Rail project, and the Omi Eko waterway program, should widen the future serviceable asset base for the Nigeria integrated facility management market as these corridors move toward operation.

Abuja and the Federal Capital Territory formed the second-largest concentration of formal demand in the Nigeria integrated facility management (IFM) market. Demand in the capital is supported by government buildings, embassies, international institutions, and a commercial office stock that is shifting toward integrated and technology-enabled assets. New road links to Guzape II, Katampe, and Karsana have improved site accessibility and encouraged new development, which adds to the pool of properties that need organized operations and maintenance support. Abuja also has a meaningful base of institutional and healthcare facilities where integrated non-clinical support is becoming more important as asset standards rise.

Port Harcourt and the broader Niger Delta anchored the oil and gas side of the Nigeria IFM market. Sites in this corridor need remote-site management, engineering support, safety supervision, and specialist technical staffing that only a narrow group of providers can supply. Eliezer Group states that it serves clients including NLNG, ExxonMobil, Chevron, and TotalEnergies across the Onne to Lagos and Bonny Island to Port Harcourt corridor, which shows how geographically concentrated this energy-linked opportunity remains. Secondary cities such as Kano, Ibadan, Benin, and Enugu remain underpenetrated because informal operators still dominate a large part of building maintenance outside Tier-1 locations. Low adoption of CAFM platforms in those cities also restricts contract visibility and pricing discipline, which slows broader geographic expansion in the Nigeria integrated facility management market.

Competitive Landscape

The Nigeria integrated facility management market is moderately fragmented, with local specialists holding a broad contract base and global firms competing more selectively for large corporate accounts. Alpha Mead Facilities & Management Services Ltd stands out among domestic players because it has secured multi-site work across telecoms, BFSI, and industrial accounts and has also invested in financing capacity to navigate a high-cost environment. Global platforms such as CBRE, ISS, and JLL benefit from multinational client relationships and standardized procurement systems, but their most visible presence remains concentrated in Lagos and Abuja. Competitive position in the Nigeria integrated facility management (IFM) market depends less on low pricing and more on the ability to mobilize certified technical staff, document compliance, and deliver consistent service across several sites.

Technology is becoming the main differentiator in the commercial segment of the Nigeria integrated facility management market. Alpha Mead has described a stack that includes in-house mobile apps, CMMS integration, and IoT-enabled systems for temperature, humidity, energy, and occupancy monitoring, which helps it compete on uptime and data visibility rather than labor alone. Provast stated in May 2026 that it was integrating IoT-enabled monitoring and AI-driven analytics across power, HVAC, water, and sewage systems in its managed portfolio. The IFMA Nigeria and Venco Africa agreement signed in December 2025 also points to broader digital standardization across the sector, especially in access control, service charges, and property operations. Smaller firms such as Cxall Facilities are trying to compete through building intelligence, condition indexing, and planning support, which suggests that the Nigeria integrated facility management market is starting to separate into scale players and tech-led specialists.

Recent strategic moves show that competition in the Nigeria integrated facility management market is being shaped by financing, digital tools, and long-cycle industrial relationships. Alpha Mead registered a NGN 5 billion (USD 3.65 million) Commercial Paper programme in 2024, which strengthened its short-term funding flexibility at a time when operating costs and liquidity pressure were rising. Provast’s 2026 rollout of AI-enabled monitoring and a phased renewable energy roadmap shows how providers are broadening their value proposition beyond routine maintenance into system performance and energy management. Security-led operators also remain relevant in specialized contracts, with G4S linked to infrastructure security mandates for both IHS Nigeria and Nigerdock, which reinforces the importance of service specialization inside the wider market structure.

Nigeria Integrated Facility Management Industry Leaders

Alpha Mead Facilities & Management Services Ltd.

Global Property & Facilities International Ltd.

Broll Property Services Ltd.

FilmoRealty Ltd.

G4S Secure Solutions Nigeria Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Alpha Mead Group issued a public advisory on deferred maintenance practices, stating that every NGN 1 (USD 0.001) spent on preventive maintenance can save NGN 4-5 (USD 0.003-0.004) in future repairs, citing billions in annual property losses for Nigerian owners who delay servicing of electrical, plumbing, elevator, HVAC, and roofing systems.

- May 2026: Provast Limited announced the active integration of IoT-enabled monitoring systems and AI-driven analytics across its managed portfolio, covering power, HVAC, water, and sewage infrastructure, and outlined a phased renewable energy transition roadmap combining solar hybridization with energy-as-a-service models for high-load commercial facilities.

- April 2026: JMG Clima commissioned a high-efficiency Variable Refrigerant Flow and Trane ODYSSEY HVAC system for a prominent snacking company's Lagos facility, engineering the solution to global high-efficiency standards with the stated goal of improving cooling stability, energy utilization, and long-term maintenance value.

- April 2026: Lagos Free Zone and CEVA Logistics established a joint venture to operate integrated warehousing and logistics infrastructure near Lekki Deep Sea Port, strengthening industrial asset operations and facility management demand in Nigeria.

Nigeria Integrated Facility Management Market Report Scope

The Nigeria Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial [includes BFSI, IT and Telecom, Retail and Warehouses, etc.], Hospitality [includes Eateries, Restaurants and Large-Scale Hotels], Institutional and Public Infrastructure [includes Government Establishments, Education, Transportation such as Airports and Railways, etc.], Healthcare [includes Public and Private Healthcare Facilities], Industrial and Process Sector [includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.], and Other End-User Industries [includes Multi-House Residential, Entertainment, Sports and Leisure]). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-Users |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management | ||

| By End-User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-Users | ||

Key Questions Answered in the Report

What is the size outlook for Nigeria integrated facility management through 2031?

The sector is expected to rise from USD 120.21 million in 2026 to USD 190.11 million by 2031, growing at an 11.15% CAGR.

Which service type leads revenue in Nigeria?

Soft FM led in 2025 with 60.73% share, supported by demand for security, cleaning, catering, and office support across commercial buildings.

Which service category is growing fastest in Nigeria?

Hard FM is forecast to grow fastest at 11.83% CAGR through 2031 as data centers, logistics parks, and engineered buildings require stronger technical support.

Which end-user group contributes the most revenue?

The industrial and process sector led with 33.59% share in 2025 because oil and gas, manufacturing, and mining sites require continuous technical maintenance.

Why is Lagos so important for facility management demand?

Lagos concentrates Grade-A offices, logistics parks, industrial assets, and data centers, which creates the deepest pipeline for both hard FM and integrated multi-site contracts.

What is the main operational risk for FM providers in Nigeria?

The biggest near-term risk is the combination of skilled labor shortages and naira volatility, which raises delivery costs and makes fixed-price contracts harder to manage.

Page last updated on: