Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

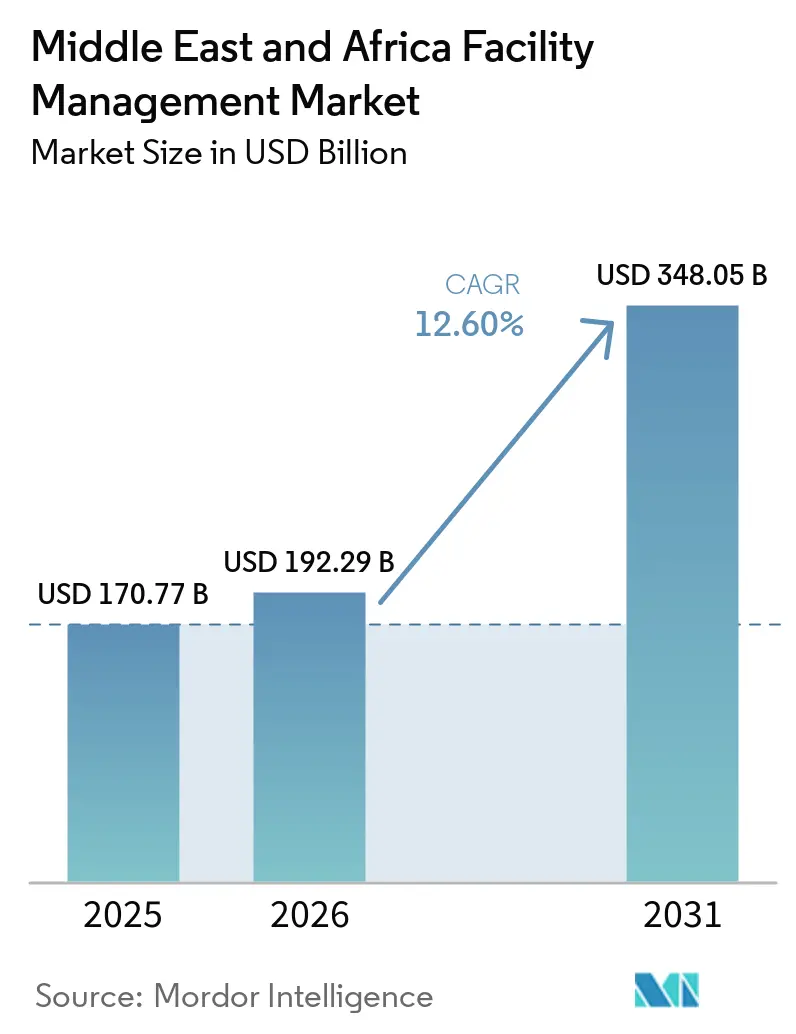

| Base Year Market Size (2025) | USD 170.77 Billion |

| Market Size (2026) | USD 192.29 Billion |

| Market Size (2031) | USD 348.05 Billion |

| Growth Rate (2026 - 2031) | 12.60% CAGR |

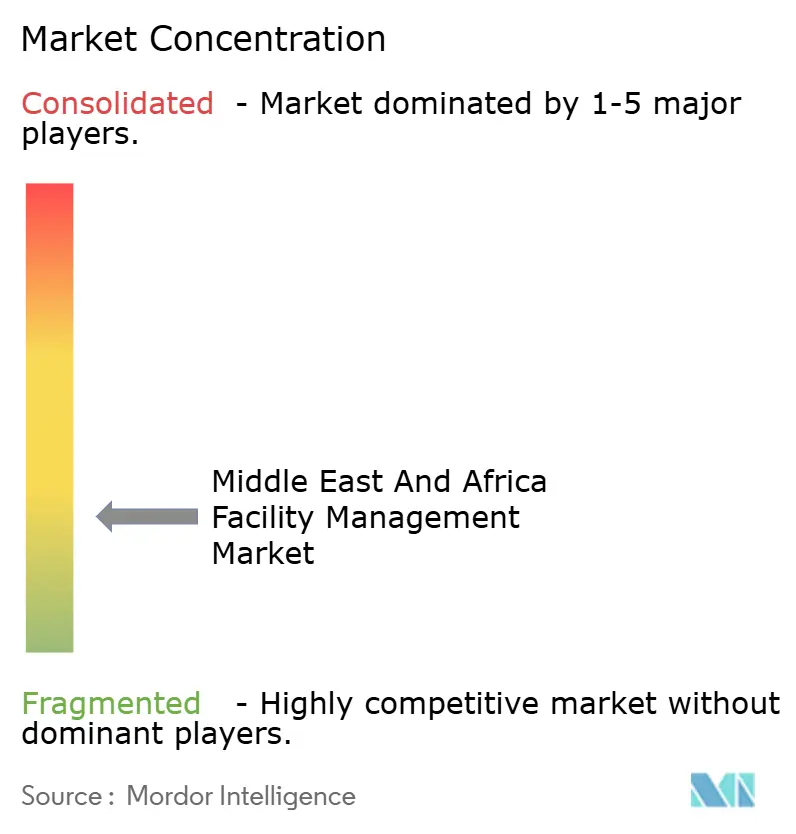

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East and Africa Facility Management Market Analysis by Mordor Intelligence

The Middle East and Africa facility management market size was valued at USD 170.77 billion in 2025 and estimated to grow from USD 192.29 billion in 2026 to reach USD 348.05 billion by 2031, at a CAGR of 12.60% during the forecast period (2026-2031). Mounting infrastructure outlays across Saudi Arabia, the United Arab Emirates, Egypt and South Africa shaped a sizeable pipeline of assets that, in turn, lifted demand for bundled and integrated facility services. Outsourced contracts attracted the bulk of new spending as corporate and public-sector owners increasingly shifted to outcome-based agreements that tied service fees to uptime, energy use and occupant-experience metrics. Digitalisation accelerated across the Middle East and Africa facility management market, with predictive maintenance, IoT-enabled building management systems, and digital-twin platforms optimizing energy consumption and reducing unplanned downtime in critical equipment fleets. Competitive differentiation therefore hinged on data analytics skills and the ability to embed ESG reporting into day-to-day operations, especially on mega projects such as NEOM and the King Abdullah Financial District. At the same time, consolidation quickened as global majors partnered with regional specialists to expand geographic reach and deepen sector know-how.

Key Report Takeaways

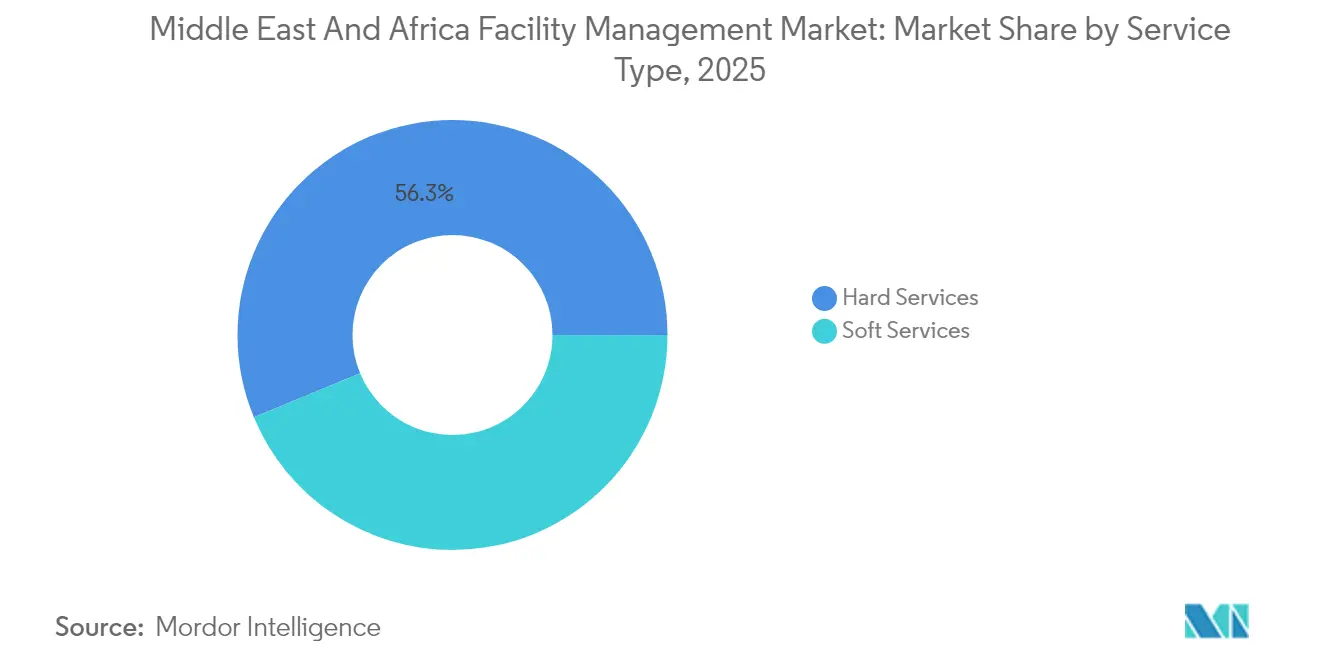

- By service type, hard services led with 56.25% of the Middle East and Africa facility management market share in 2025, whereas soft services recorded the fastest 12.78% CAGR through 2031

- By offering, outsourced models captured 63.20% of the Middle East and Africa facility management market share in 2025, and were forecast to expand at 13.85% CAGR to 2031.

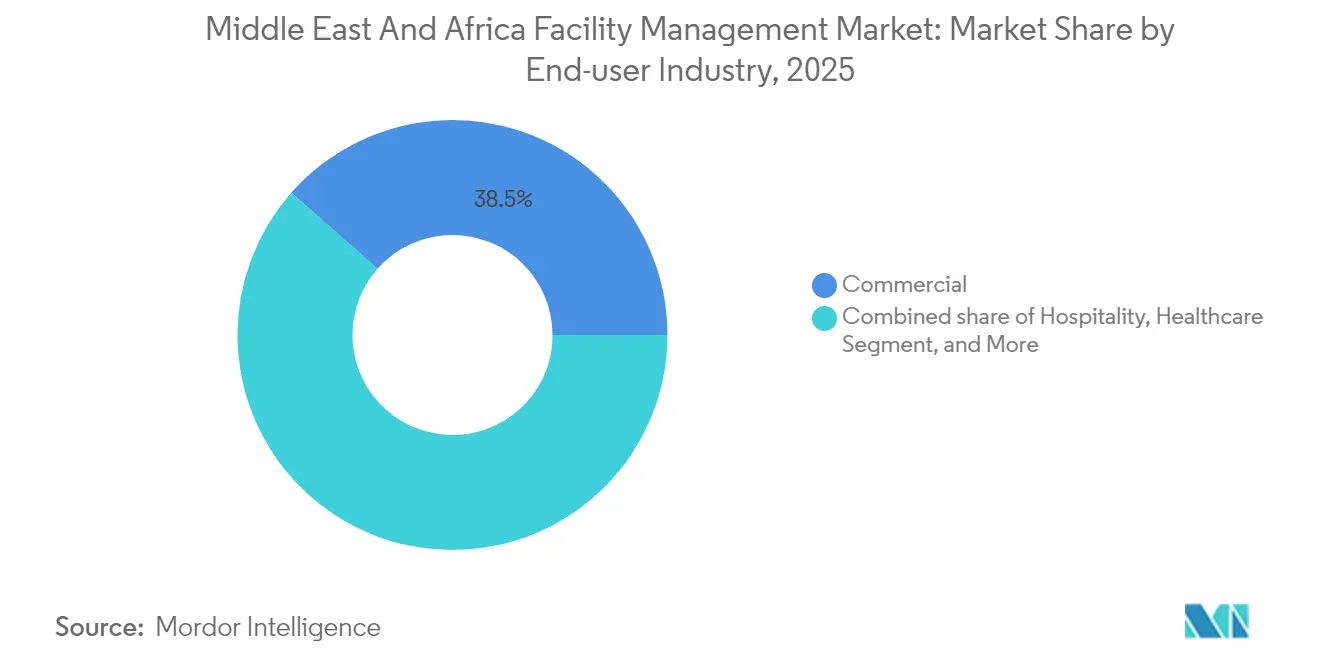

- By end-user sector, the commercial category held 38.50% of the Middle East and Africa facility management market share in 2025, while the industrial and process segment was projected to post the highest 14.55% CAGR between 2026 and 2031.

- By geography, Saudi Arabia accounted for 17.75% of the Middle East and Africa facility management market share in 2025; Bahrain represented the fastest-growing geography at 12.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East and Africa Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing infrastructure development | +3.2% | Saudi Arabia, UAE, Qatar, Egypt | Long term (≥ 4 years) |

| Rising outsourcing in building management | +2.8% | GCC core markets | Medium term (2–4 years) |

| Heightened safety and security needs | +1.9% | High-risk locations | Short term (≤ 2 years) |

| Technological advancements in facility management | +2.1% | UAE, Saudi Arabia, Qatar | Medium term (2–4 years) |

| ESG-driven facility operations demand | +1.7% | UAE, Saudi Arabia | Long term (≥ 4 years) |

| FM demand from giga mixed-use projects | +1.4% | Saudi Arabia, UAE, Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Infrastructure Development

Saudi Arabia alone had awarded significant construction contracts in 2024 under Vision 2030, and NEOM’s USD 500 billion masterplan stimulated significant spike in sector-wide wages, underscoring how large-scale projects fuelled service volumes across the Middle East and Africa facility management market. In Africa, the syndicated facility raised by Africa Finance Corporation in March 2024 signaled renewed capital inflows aimed at closing the funding gap and thereby broadening the asset base requiring lifecycle support. The UAE real estate boom similarly lifted demand for technical asset care in premium office, residential, and retail stock. As a cumulative result, facility executives sought providers able to scale quickly, standardize processes, and manage complex stakeholder groups across multi-phase developments.

Rising Outsourcing in Building Management

Outsourcing gained momentum after landmark deployments such as the King Abdullah Financial District, where an integrated contract underpinned by IBM Maximo boosted customer-satisfaction scores by 95% while lowering corrective maintenance outlays, demonstrating quantifiable value creation for owners.[1]IBM "Delivering great customer service at a mega real estate development," ibm.com Regulatory bodies followed suit; for example, the Middle East Facility Management Association and Rera Ajman signed a June 2024 accord to formalise best practice and training pathways, institutionalising outsourced models in residential towers and mixed-use precincts. Healthcare operators were early adopters, entrusting critical-environment compliance to external teams steeped in infection-control protocols. Outcome-based contracts tied payments to uptime and energy KPIs, aligning incentives and lengthening average contract tenures.

Technological Advancements in Facility Management

IoT, AI and machine-learning deployments reached commercial scale. Dubai Electricity and Water Authority invested in AI and smart-grid solutions that cut portfolio-level energy use by double-digit percentages. Case studies such as a Dubai Grade-A office block where smart-lighting controls reduced annual consumption by 25% and yielded a 2.67-year payback illustrated tangible economic benefits.[2]MileSight Network Technology Co; Ltd. "Smart Lighting Control with IoT." milesight.com Predictive analytics pushed mean-time-between-failure figures higher and trimmed maintenance budgets significantly in HVAC, elevator and chilled-water systems. Providers that paired engineering acumen with data science capability enjoyed a clear competitive edge across the Middle East and Africa facility management market.

ESG-Driven Facility Operations Demand

Investors amplified scrutiny of carbon footprints, prompting asset owners to pursue LEED, BREEAM or national green-building ratings. Facility contracts therefore embedded clauses on renewable-energy integration, waste-diversion targets and indoor-air-quality dashboards. In the UAE, new commercial leases required energy-intensity disclosure, accelerating retrofits of legacy stock with efficient chillers and building-automation upgrades. These sustainability obligations are reshaping procurement criteria across the UAE facility management. Saudi Arabia framed sustainability standards within Vision 2030, making ESG compliance a prerequisite for access to public-sector awards. Service partners capable of delivering quantified reductions in greenhouse-gas emissions captured premium fees and multi-year renewals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled labour shortages | -2.1% | Africa, GCC | Medium term (2–4 years) |

| Regulatory challenges | -1.3% | Fragmented MEA markets | Short term (≤ 2 years) |

| Volatile economic conditions and oil price swings | -1.8% | Hydrocarbon economies | Short term (≤ 2 years) |

| Fragmented FM standards across MEA countries | -0.9% | Region-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled Labour Shortages

Africa faced a significant demand for additional project-management professionals annually through 2030. However, training pipelines struggled to meet this demand, leaving critical supervisory positions unfilled and hindering the growth of the Middle East and Africa facility management market. In the Gulf, mechanical-electrical-plumbing firms reported mid-management knowledge gaps that delayed the implementation of digital systems and reduced productivity. In 2024, there is a significant need for upskilling in the construction sector, leading employers to hesitate in investing in training due to high personnel turnover. The scarcity of green-building specialisms further compounded the challenges faced in smart-asset optimisation projects.

Volatile Economic Conditions and Oil Price Swings

Oil-linked fiscal cycles introduced budget uncertainty into public-sector real-estate programmes. The World Bank expected Middle East and North Africa GDP to grow only 2.6% in 2025, cautioning that shifts in crude output agreements or commodity prices could derail planned capital works.[3]World Bank "Growth in the Middle East and North Africa Forecast to Moderately Accelerate in 2025 Amidst Uncertainty," worldbank.org In Saudi Arabia, construction-material costs escalated sharply, prompting contractors to seek price-variation clauses or delay bid submissions, a pattern that slowed award timelines for ancillary facility contracts. Meanwhile, owners demanded flexible service-fee structures that transferred part of inflation risk to providers, eroding margins and complicating long-term resource planning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Anchor Spend While Soft Services Accelerate

Hard services controlled 56.25% of the Middle East and Africa facility management market in 2025, underpinned by mandatory HVAC, fire-safety and asset-integrity programs designed for harsh climates and high-occupancy assets. Within that basket, MEP services captured most spend, as energy-optimisation retrofits became obligatory for Grade-A stock. Soft services displayed brisk 12.78% CAGR and were increasingly bundled into integrated contracts that elevated occupant-wellbeing metrics and ESG reporting quality.

Soft-service growth reflected expanded scope spanning sustainable cleaning chemicals, wellness certifications and tenant-engagement analytics. Although smaller in absolute value, soft services represented a strategic pathway for providers to embed themselves in client organisations and cross-sell higher-margin advisory work. The dynamic signalled further incremental share gain for soft services within the Middle East and Africa facility management market size during the forecast horizon.

By Offering Type: Outsourcing Builds Scale Across Integrated and Bundled Models

Outsourced agreements captured 63.20% revenue in 2025 and were forecast to log a 13.85% CAGR through 2031, supported by proven TCO reductions and access to digital toolsets not economical for single owners to develop internally. Integrated facility management contracts grew fastest because they streamlined vendor interfaces and handed single-point accountability for multi-discipline outcomes.

Tier-one clients tested outcome-based remuneration that tied fee escalation to quantified energy-savings and uptime thresholds, anchoring fresh revenue pools for data-savvy operators in the Middle East and Africa facility management market. In-house teams survived mainly in high-security government, defence or critical-infrastructure settings but tended to outsource specialist modules such as predictive diagnostics or vertical-transport maintenance.

By End-User Industry: Commercial Assets Lead; Industrial Facilities Scale Up

The commercial segment, including Grade-A offices and data centres, accounted for 38.50% of the Middle East and Africa facility management market size in 2025, owing to the density of premium real-estate stock in Dubai, Riyadh and Johannesburg. Owners demanded continuous service across mixed-use precincts that blend workspace, retail and hospitality elements.

Industrial and process plants registered the strongest 14.55% CAGR outlook as Gulf states localised manufacturing and downstream energy chains. High-spec clean-rooms, logistics hubs and energy parks required technical competence in process safety and continuous-operation standards, allowing providers to deploy predictive analytics and digital twins that heightened barrier-to-entry thresholds.

Geography Analysis

Saudi Arabia’s project pipeline, featuring NEOM, The Red Sea and King Salman Energy Park, underpinned multi-billion-USD FM outsourcing deals and attracted new entrants such as Dussmann Group, which opened a Riyadh hub in late 2024 to capture national volumes. Construction-cost inflation and tight labour markets incentivised owners to contract providers with proven procurement leverage and automated workforce-scheduling systems.

The United Arab Emirates retained its role as a technology testbed where early adoption of AI-based energy-management suites bolstered provider margins. Dubai’s construction costs remained below peer capitals, advancing speculative office and logistics builds that required post-handover FM mobilisation within compressed timeframes. The country also served as a regional headquarters for multinationals orchestrating wider Middle East and Africa facility management market activities.

Across Africa, South Africa’s mature FM supply chains allowed corporates to outsource non-core services en masse, whereas Egypt’s new-capital developments and hospital modernisation programmes widened scope for integrated contracts. Nigeria’s scale and rapid urbanisation placed pressure on power, water and HVAC infrastructure, opening avenues for performance-based maintenance deals. Although public-sector liquidity gaps persisted, multilateral lenders such as AFC continued to unlock project funding, gradually enlarging the continental asset base under management.

Competitive Landscape

The market remained moderately fragmented. Global majors such as Sodexo, ISS and CBRE leveraged scale, standard operating procedures and global supply frameworks to win marquee multi-country mandates. Regional specialists including Emrill, Imdaad and Farnek competed on local-authority relationships, bilingual workforce capability and sector-specific depth. Joint ventures grew more common as players sought to blend international best practice with in-country value requirements.

Technology investment dictated positioning. CBRE’s financial-year 2024 uplift in facilities-management revenue stemmed partly from enterprise analytics suites that delivered portfolio-level insights to Fortune 500 occupiers. Farnek introduced data-linked command centres and, in January 2025, created a dedicated events-sector subsidiary to service an expanding MICE calendar. Healthcare and district-cooling niches granted high barriers to entry; Empower’s Q3 2024 record-breaking plant in Business Bay illustrated the scale advantages accessible to incumbents.

Price competition stayed intense on single-service tenders, but integrated-FM and outcome-based contracts rewarded differentiation, fostering consolidation among mid-sized players. Providers that proved adept at workforce skilling, digital-platform adoption and ESG reporting commanded premium pricing and renewal rates above 90%, indicating evolving buyer preferences throughout the Middle East and Africa facility management market.

Middle East and Africa Facility Management Industry Leaders

-

EFS Facilities Services Group

-

Emrill Services LLC

-

Farnek Services LLC

-

Sodexo, Inc.

-

G4S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hyatt opened more than 11,000 rooms globally in Q1 2025 and plans to triple its Saudi portfolio within five years, elevating hospitality service demand across housekeeping, technical support, and guest-experience functions. This expansion is expected to drive significant growth in the facility management market, particularly in the areas of maintenance, cleaning, and guest service management.

- March 2025: Emrill reported 9% revenue growth for 2024 on the back of increased residential contracts and received the Dubai Chamber of Commerce ESG Label for improvements in resource efficiency and workforce welfare. This growth highlights the rising demand for facility management services in residential sectors, with a focus on sustainability and employee well-being

- January 2025: The Middle East Facility Management Association launched the Mustadam Certified Sustainability Facility Manager credential to standardize competency in sustainable operations across the region. This initiative is expected to enhance the adoption of sustainable practices in the facility management market, aligning with global environmental goals.

- January 2024: DHL Global Forwarding finalized its acquisition of Danzas AEI Emirates, adding 20 logistics facilities and 1,100 staff across the UAE to its regional network, which requires integrated hard and soft services to maintain throughput reliability. This acquisition is likely to increase the need for facility management services to ensure operational efficiency and compliance with logistics standards.

Middle East and Africa Facility Management Market Report Scope

Facility management services involve the building upkeep, utilities, maintenance operations, waste services, and security, among others. Increasing construction activities in the Middle East are significantly driving the market's growth.

The Middle East and Africa facility management market is segmented by type (in-house facility management and outsourced facility management (single, bundled, and integrated)), end user (commercial, institutional, public/infrastructure, industrial, healthcare, and other end users), and Country (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, South Africa, Egypt, Nigeria, and Rest of Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industry |

By Country

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| South Africa |

| Egypt |

| Nigeria |

| Rest of Middle East and Africa |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industry | ||

| By Country | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving the rapid growth of the Middle East and Africa facility management market?

Urbanisation, massive infrastructure pipelines valued at USD 3.7 trillion and stringent sustainability mandates are increasing demand for integrated, technology-centric services that optimise building performance.

Which service category contributes the most revenue today?

Hard services-covering mechanical, electrical, plumbing and HVAC-remain the largest revenue contributor because their reliability is critical to business continuity in harsh regional climates.

Why is integrated facility management gaining popularity?

Clients prefer a single governance framework that consolidates multiple services, reduces duplication and uses data analytics to drive continuous improvement, which explains the 13.45% Saudi CAGR for IFM through 2026.

What challenges most affect service providers?

Skilled-labour shortages in technical roles add wage pressure and increase training costs, while inconsistent regulatory standards across countries complicate cross-border operations.

What technologies will define future competitive advantage?

IoT-driven condition monitoring, digital twins for real-time asset modelling and AI-assisted predictive maintenance will differentiate providers capable of translating data into measurable client outcomes.

Page last updated on: